Semester 3, 2019: BAO3306 Auditing Report on Reece Group Limited

VerifiedAdded on 2022/08/28

|12

|4211

|12

Report

AI Summary

This auditing report, prepared for the BAO3306 course, examines the audit of Reece Group Limited. The report begins with an executive summary outlining the auditor's responsibilities, including understanding the client's business, identifying high-risk accounts, determining planning materiality, and assessing audit risks. The report then provides a detailed understanding of Reece Group Limited, focusing on its control environment, risk assessment process, information system, control activities, and monitoring of controls. The report identifies and assesses five significant accounts: revenue and other income, cash and cash equivalents, receivables, inventory, and long-term borrowing, detailing the associated risks of material misstatements for each. The report discusses planning materiality, emphasizing its role in evaluating misstatements. Finally, it assesses potential risks associated with the identified accounts. The report concludes with a summary of findings, providing a comprehensive overview of the audit process and key considerations.

ASSIGNMENT

BAO3306 AUDITING

REPORT

Penalty

- Exceeding the 3000 words limit: TWO (2) marks deduction.

- Exceeding the 30% similarity index limit: FOUR (4) marks deduction.

- Late submission: TWO (2) marks deduction per day including weekends.

Plagiarism

Plagiarism is defined as presenting someone else’s work, including the

work of other students, as one’s own. Any ideas or materials taken from

another source for either written or oral use must be fully acknowledged, unless

the information is common knowledge. All students are strongly advised to do

the following:

BAO3306 AUDITING

REPORT

Penalty

- Exceeding the 3000 words limit: TWO (2) marks deduction.

- Exceeding the 30% similarity index limit: FOUR (4) marks deduction.

- Late submission: TWO (2) marks deduction per day including weekends.

Plagiarism

Plagiarism is defined as presenting someone else’s work, including the

work of other students, as one’s own. Any ideas or materials taken from

another source for either written or oral use must be fully acknowledged, unless

the information is common knowledge. All students are strongly advised to do

the following:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

- goto http://wcf.vu.edu.au/GovernancePolicy/PDF/POA040915000.PDF

- enter School of Accounting and Finance

- enter Student Resources

- read the PLAGIARISM POLICY.

Semester TRI_3 , 2019

Executive summary

The auditors have the responsibility to develop the audit plan by considering all related

aspects like understanding the client, identification of accounts with high risk of material

misstatements, setting planning materiality level and assessment of the audit risks. First part

of this report obtains understanding on the business of the client that is Reece Group Limited.

The second part identifies the five accounts which are prone to high material misstatements.

The third part of the report discuses about different aspects that need to be taken into

consideration for the determination of planning materiality level. The last part of the report

assesses what can go wrong with the identified accounts in relation to the assessment of audit

risks.

- enter School of Accounting and Finance

- enter Student Resources

- read the PLAGIARISM POLICY.

Semester TRI_3 , 2019

Executive summary

The auditors have the responsibility to develop the audit plan by considering all related

aspects like understanding the client, identification of accounts with high risk of material

misstatements, setting planning materiality level and assessment of the audit risks. First part

of this report obtains understanding on the business of the client that is Reece Group Limited.

The second part identifies the five accounts which are prone to high material misstatements.

The third part of the report discuses about different aspects that need to be taken into

consideration for the determination of planning materiality level. The last part of the report

assesses what can go wrong with the identified accounts in relation to the assessment of audit

risks.

Table of Contents

Introduction................................................................................................................................3

Key information.........................................................................................................................4

Our understanding of the client..............................................................................................4

Our assessment of significant accounts..................................................................................5

Our planning materiality........................................................................................................6

Our assessment of what can go wrong...................................................................................6

Conclusion..................................................................................................................................8

Appendix....................................................................................................................................9

References................................................................................................................................11

Introduction................................................................................................................................3

Key information.........................................................................................................................4

Our understanding of the client..............................................................................................4

Our assessment of significant accounts..................................................................................5

Our planning materiality........................................................................................................6

Our assessment of what can go wrong...................................................................................6

Conclusion..................................................................................................................................8

Appendix....................................................................................................................................9

References................................................................................................................................11

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Introduction

Audit and assurance is a major aspect for the investors and other stakeholders in order

to enhance the credibility of the disclosed financial information of the firms. In an assurance

engagement, the main aim of an auditor is to gain adequate evidence for expressing a

conclusion in order to improve the intended users’ level of confidence on the disclosed

financial information on different financial reports. ASA 200 indicates that the main

objective of the auditors in the audit of financial reports is expressing an opinion on whether

the client has prepared the financial statements in accordance with the required financial

reporting framework and whether there is any material misstatement in the financial

statements (auasb.gov.au 2020). It requires to be mentioned that the responsibility of the

auditors is to take into account all the required aspects while planning and carrying out the

audit of any client. In order to proceed with the audit of a client, an auditor must gain

adequate understating of the client as this is required for the determination of inherent risk of

audit. After that, the auditor needs to identify the key accounts that can be at the risk of

material misstatements. The next step is to determine the level of planning materiality in

order to ascertain whether there is material misstatement or not. Lastly, it is required for the

auditor to undertake risk assessment for assessing what can go wrong with the selected

accounts. The main aim of this report is to undertake all the above-mentioned steps for

undertaking the audit of Reece Group Limited.

Key information

Our understanding of the client

According to ASA 315 Identifying and Assessing the Risks of Material Misstatement

through Understanding the Entity and Its Environment, Para 3, an auditor’s objective is the

recognition of material misstatements risks by understanding the audit client and its

environment that consists of internal control (Fontaine, Letaifa & Herda 2013). This

particular standard is also applicable for the audit of Reece Group Limited where the external

auditor is required to gain understanding of different aspects of Reece Group Limited.

According to ASA 315, there are five specific components of the internal control of Reece

Group Limited that the external auditor needs to assess; they are control environment, risk

assessment process of the entity, information system, control activities and monitoring the

controls (auasb.gov.au 2020). The external auditor of Reece Group Limited is required to

assess these five components for gaining understating on the company.

Control Environment – Control environment consists of the culture, structure and discipline

of a company. Reece Group Limited has a clearly defined organizational structure where the

responsibilities of the management are clearly defined. The company has effectively

segregated the duties while delegating the limits of the authority. As mentioned in the

Corporate Governance statement of Reece Group Limited, the board of the company has put

key emphasis on the ethical aspects like honesty and integrity in all the business dealings.

The company has its own Code of Conduct and Code of Business Ethics for over viewing the

business activities (reecegroup.com.au 2020).

Risk Assessment Process –Reece Group Limited has an effective risk management

mechanism where the company does not only aim to eliminate the risks, but identify, monitor

and manage the material risk of business (reecegroup.com.au 2020). The Board of Directors

of the firm has developed a Risk and Compliance Committee in order to determine and

implement the risk management controls in the daily business conducts. This risk

Audit and assurance is a major aspect for the investors and other stakeholders in order

to enhance the credibility of the disclosed financial information of the firms. In an assurance

engagement, the main aim of an auditor is to gain adequate evidence for expressing a

conclusion in order to improve the intended users’ level of confidence on the disclosed

financial information on different financial reports. ASA 200 indicates that the main

objective of the auditors in the audit of financial reports is expressing an opinion on whether

the client has prepared the financial statements in accordance with the required financial

reporting framework and whether there is any material misstatement in the financial

statements (auasb.gov.au 2020). It requires to be mentioned that the responsibility of the

auditors is to take into account all the required aspects while planning and carrying out the

audit of any client. In order to proceed with the audit of a client, an auditor must gain

adequate understating of the client as this is required for the determination of inherent risk of

audit. After that, the auditor needs to identify the key accounts that can be at the risk of

material misstatements. The next step is to determine the level of planning materiality in

order to ascertain whether there is material misstatement or not. Lastly, it is required for the

auditor to undertake risk assessment for assessing what can go wrong with the selected

accounts. The main aim of this report is to undertake all the above-mentioned steps for

undertaking the audit of Reece Group Limited.

Key information

Our understanding of the client

According to ASA 315 Identifying and Assessing the Risks of Material Misstatement

through Understanding the Entity and Its Environment, Para 3, an auditor’s objective is the

recognition of material misstatements risks by understanding the audit client and its

environment that consists of internal control (Fontaine, Letaifa & Herda 2013). This

particular standard is also applicable for the audit of Reece Group Limited where the external

auditor is required to gain understanding of different aspects of Reece Group Limited.

According to ASA 315, there are five specific components of the internal control of Reece

Group Limited that the external auditor needs to assess; they are control environment, risk

assessment process of the entity, information system, control activities and monitoring the

controls (auasb.gov.au 2020). The external auditor of Reece Group Limited is required to

assess these five components for gaining understating on the company.

Control Environment – Control environment consists of the culture, structure and discipline

of a company. Reece Group Limited has a clearly defined organizational structure where the

responsibilities of the management are clearly defined. The company has effectively

segregated the duties while delegating the limits of the authority. As mentioned in the

Corporate Governance statement of Reece Group Limited, the board of the company has put

key emphasis on the ethical aspects like honesty and integrity in all the business dealings.

The company has its own Code of Conduct and Code of Business Ethics for over viewing the

business activities (reecegroup.com.au 2020).

Risk Assessment Process –Reece Group Limited has an effective risk management

mechanism where the company does not only aim to eliminate the risks, but identify, monitor

and manage the material risk of business (reecegroup.com.au 2020). The Board of Directors

of the firm has developed a Risk and Compliance Committee in order to determine and

implement the risk management controls in the daily business conducts. This risk

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

management process assesses, evaluates and mitigates risks such as strategic risk, reputation

risk, product and service quality risk, ethical conduct in business risks, financial risks and

others (Tepalagul and Lin 2015).

Information System – It is mentioned in the Corporate Governance Statement of Reece

Group Limited that one of the major responsibilities of the Board of Directors of the firms is

to provide the approval of the annual reports and disclosure in the market while overseeing

the processes of the company to make disclosure in timely and balanced manner of all the

material information on financial and non-financial aspects (reecegroup.com.au 2020). The

Board is also responsible to appoint, undertaken and properly check the material information

in the annual general meeting.

Control Activities –Reece Group Limited has its Audit Committee whose one crucial

responsibility is reviewing the risk management framework of Reece Group Limited along

with its internal control (reecegroup.com.au 2020). In addition, Reece Group Limited has

employed stable and reliable management reporting system along with appropriate

accounting control. In addition, the Board of Directors of Reece Group Limited is responsible

to set and monitor strategic plans as well as objectives that include measuring and monitoring

the performance of senior executives. Incompatible duties have been segregated properly

with the aim to eliminate the scope of frauds (Dao and Pham 2014).

Monitoring of Controls – The key responsibilities of the Board of Directors of Reece Group

Limited include monitoring the strategic plans as well as corporate objectives, monitoring the

functional and operational activities of the company, monitoring the business’s capital

expenditures, monitoring the compliance of the company with the regulatory and legal

necessities along with overall governance’s efficiency, monitoring compliance of Reece

Group Limited with its own business and ethical standards that includes codes of conduct and

values of the company and monitoring the senior executives’ performance. The Audit

Committee is responsible to monitor the development of accounting and financial reporting,

monitoring the external audit’s progress and monitoring the matters associated with Code of

Conducts and Whistleblower Policy (reecegroup.com.au 2020).

Our assessment of significant accounts

According to ASA 200 Overall Objectives of the Independent Auditor and the

Conduct of an Audit in Accordance with Australian Auditing Standards, audit risk can be

considered as a risk of expressing an unsuitable audit opinion in the presence of materially

misstated financial statements (auasb.gov.au 2020). It is needed for the auditor of Reece

Group Limited to undertake the risk assessment procedure for the identification of the areas

of risk of material misstatements. Appropriate analytical procedures need to be applied by the

auditors in this stage and simple comparison will be used for assessing the risks of Reece

Group Limited (Jans, Alles and Vasarhelyi 2014). Five accounts with the risk of material

misstatements of Reece Group Limited are discussed below:

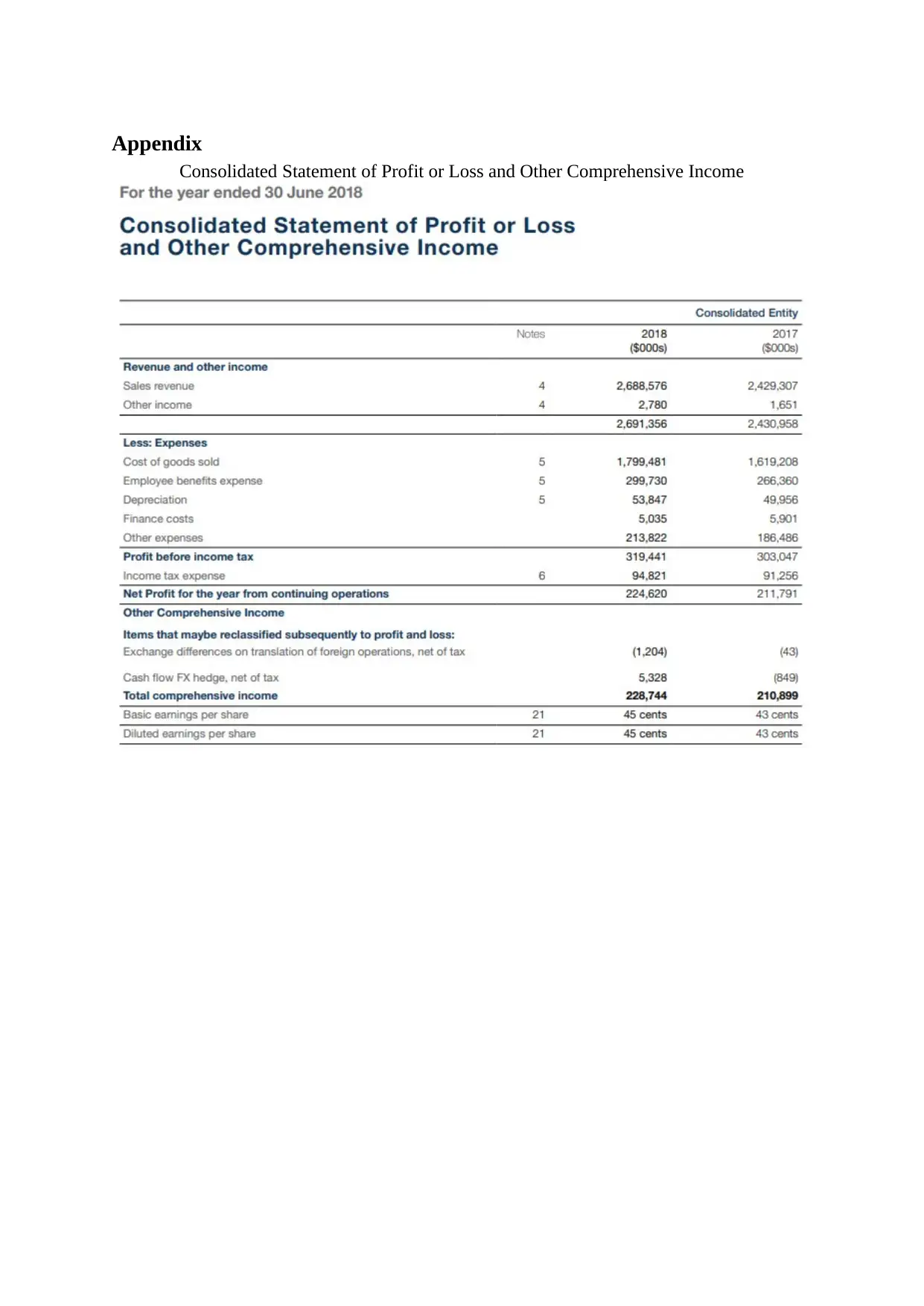

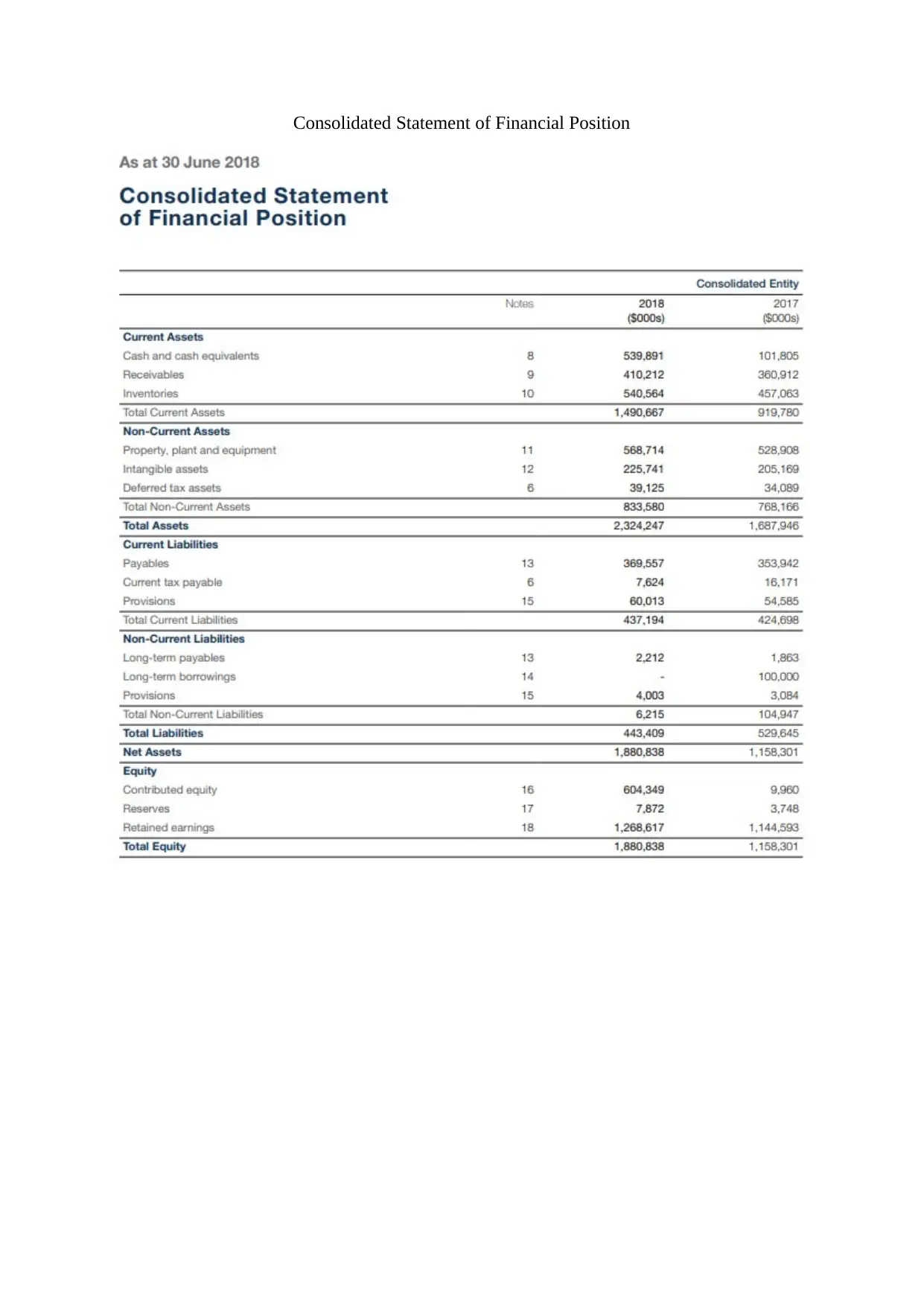

Revenue and Other Income – It can be seen from the 2018 Annual Report of Reece Group

Limited that there is significant rise in the revenue and other income of the company in 2018

from 2017 that is from $2430958000 to $2691356000 (reecegroup.com.au 2020). Sales

revenue is considered as significant account and this large increase in this account casts

significant doubt on the fact that that can be material misstatement in this account. The

important assertions associated with this account are occurrence, accuracy, cut-off and

completeness. Therefore, this account is at the risks of material misstatement (Lobo and Zhao

2013).

risk, product and service quality risk, ethical conduct in business risks, financial risks and

others (Tepalagul and Lin 2015).

Information System – It is mentioned in the Corporate Governance Statement of Reece

Group Limited that one of the major responsibilities of the Board of Directors of the firms is

to provide the approval of the annual reports and disclosure in the market while overseeing

the processes of the company to make disclosure in timely and balanced manner of all the

material information on financial and non-financial aspects (reecegroup.com.au 2020). The

Board is also responsible to appoint, undertaken and properly check the material information

in the annual general meeting.

Control Activities –Reece Group Limited has its Audit Committee whose one crucial

responsibility is reviewing the risk management framework of Reece Group Limited along

with its internal control (reecegroup.com.au 2020). In addition, Reece Group Limited has

employed stable and reliable management reporting system along with appropriate

accounting control. In addition, the Board of Directors of Reece Group Limited is responsible

to set and monitor strategic plans as well as objectives that include measuring and monitoring

the performance of senior executives. Incompatible duties have been segregated properly

with the aim to eliminate the scope of frauds (Dao and Pham 2014).

Monitoring of Controls – The key responsibilities of the Board of Directors of Reece Group

Limited include monitoring the strategic plans as well as corporate objectives, monitoring the

functional and operational activities of the company, monitoring the business’s capital

expenditures, monitoring the compliance of the company with the regulatory and legal

necessities along with overall governance’s efficiency, monitoring compliance of Reece

Group Limited with its own business and ethical standards that includes codes of conduct and

values of the company and monitoring the senior executives’ performance. The Audit

Committee is responsible to monitor the development of accounting and financial reporting,

monitoring the external audit’s progress and monitoring the matters associated with Code of

Conducts and Whistleblower Policy (reecegroup.com.au 2020).

Our assessment of significant accounts

According to ASA 200 Overall Objectives of the Independent Auditor and the

Conduct of an Audit in Accordance with Australian Auditing Standards, audit risk can be

considered as a risk of expressing an unsuitable audit opinion in the presence of materially

misstated financial statements (auasb.gov.au 2020). It is needed for the auditor of Reece

Group Limited to undertake the risk assessment procedure for the identification of the areas

of risk of material misstatements. Appropriate analytical procedures need to be applied by the

auditors in this stage and simple comparison will be used for assessing the risks of Reece

Group Limited (Jans, Alles and Vasarhelyi 2014). Five accounts with the risk of material

misstatements of Reece Group Limited are discussed below:

Revenue and Other Income – It can be seen from the 2018 Annual Report of Reece Group

Limited that there is significant rise in the revenue and other income of the company in 2018

from 2017 that is from $2430958000 to $2691356000 (reecegroup.com.au 2020). Sales

revenue is considered as significant account and this large increase in this account casts

significant doubt on the fact that that can be material misstatement in this account. The

important assertions associated with this account are occurrence, accuracy, cut-off and

completeness. Therefore, this account is at the risks of material misstatement (Lobo and Zhao

2013).

Cash and Cash Equivalents – As per the 2018 Annual Report of Reece Group Limited,

there has been a major increase in the cash and cash equivalent that is from $101,805,000 in

2018 to $539,891,000 in 2018 (reecegroup.com.au 2020). Increase in cash and cash

equivalent improve the short-term liquidity position of the companies and this can be a major

aim of the management of Reece Group Limited to overstate cash and cash equivalent for

improving the liquidity position. Therefore, this particular account is largely at the risks of

material misstatements because of overstatement (Kochetova-Kozloski, Kozloski and

Messier Jr 2013).

Receivables – 2018 Annual Report of Reece Group Limited shows that there is a major

increase in the debtors of Reece Group Limited from 2017 to 2018 that is from $360,912,000

in 2017 to $410,212,000 in 2018 (reecegroup.com.au 2020). There are three important

transactions that create major impact on the receivable balances; they are sales, cash receipts

and sales return and allowance. Since sales and cash and cash equivalents are of significant

risk of material misstatements, their effects can be on the balance of receivable. For this

reason, the account of receivable is required to be considered at the high risk of material

misstatements (Czerney, Schmidt and Thompson 2014).

Inventory – It can be seen from the 2018 Annual Report of Reece Group Limited that

inventories of the company has largely increased from $457,063,000 in 2017 to $540,564,000

in 2018 (reecegroup.com.au 2020). Increase in inventory improved the short-term liquidity

position of the companies and the same is also applicable for Reece Group Limited which

provides the management of the company the reason to overstate this account. Moreover,

there are three crucial transactions that affect the balance of inventory which are purchase,

cash payments and inventory possess. For these reasons, the account of inventory is also at

the high risk of material misstatements (Bhattacharjee, Maletta and Moreno 2015).

Long-term Borrowing – It can be seen from the 2018 Annual Report of Reece Group

Limited that the long-term borrowing of the company worth $100,000,000 in 2017 has been

fully repaid by the company in 2018 (reecegroup.com.au 2020). Since the main risk

associated with this account is understatement, this account is at the most risk of material

misstatements. On the other hand, two significant types of processes create impact on the

balance of this account that are cash payments and purchase. In the presence of these reason,

this accounts needs to be considered at the risk of material misstatement (Czerney, Schmidt

and Thompson 2014).

Our planning materiality

Materiality is considered as a crucial concept in auditing that includes the

misstatements creating major influence on the decision making process of the users of the

financial reports of the clients. As a foundation of the opinions of the auditors, it is required

by the auditors to acquire rational guarantee on there is material misstatement in the financial

reports of the clients or not. This makes increases the significance of the concept of

materiality in auditing. Auditors apply this as audit planning stage along with performing

audit and evaluating the impacts of material misstatements on the overall audit.

The use of materiality in auditing can be seen in order to test and asses the legitimacy

of information in the financial statements and associated notes. The presence of all

materiality related rules and regulations can be seen under ASA 320 Materiality in Planning

and Performing an Audit (auasb.gov.au 2020). It is needed for the auditor of Reece Group

Limited to utilize his/her professional judgment and understanding of the client at the time to

set panning materiality level and the auditor also needs to be alert of the primary users of the

financial statements. The auditor of Reece Group Limited has the option to select the

there has been a major increase in the cash and cash equivalent that is from $101,805,000 in

2018 to $539,891,000 in 2018 (reecegroup.com.au 2020). Increase in cash and cash

equivalent improve the short-term liquidity position of the companies and this can be a major

aim of the management of Reece Group Limited to overstate cash and cash equivalent for

improving the liquidity position. Therefore, this particular account is largely at the risks of

material misstatements because of overstatement (Kochetova-Kozloski, Kozloski and

Messier Jr 2013).

Receivables – 2018 Annual Report of Reece Group Limited shows that there is a major

increase in the debtors of Reece Group Limited from 2017 to 2018 that is from $360,912,000

in 2017 to $410,212,000 in 2018 (reecegroup.com.au 2020). There are three important

transactions that create major impact on the receivable balances; they are sales, cash receipts

and sales return and allowance. Since sales and cash and cash equivalents are of significant

risk of material misstatements, their effects can be on the balance of receivable. For this

reason, the account of receivable is required to be considered at the high risk of material

misstatements (Czerney, Schmidt and Thompson 2014).

Inventory – It can be seen from the 2018 Annual Report of Reece Group Limited that

inventories of the company has largely increased from $457,063,000 in 2017 to $540,564,000

in 2018 (reecegroup.com.au 2020). Increase in inventory improved the short-term liquidity

position of the companies and the same is also applicable for Reece Group Limited which

provides the management of the company the reason to overstate this account. Moreover,

there are three crucial transactions that affect the balance of inventory which are purchase,

cash payments and inventory possess. For these reasons, the account of inventory is also at

the high risk of material misstatements (Bhattacharjee, Maletta and Moreno 2015).

Long-term Borrowing – It can be seen from the 2018 Annual Report of Reece Group

Limited that the long-term borrowing of the company worth $100,000,000 in 2017 has been

fully repaid by the company in 2018 (reecegroup.com.au 2020). Since the main risk

associated with this account is understatement, this account is at the most risk of material

misstatements. On the other hand, two significant types of processes create impact on the

balance of this account that are cash payments and purchase. In the presence of these reason,

this accounts needs to be considered at the risk of material misstatement (Czerney, Schmidt

and Thompson 2014).

Our planning materiality

Materiality is considered as a crucial concept in auditing that includes the

misstatements creating major influence on the decision making process of the users of the

financial reports of the clients. As a foundation of the opinions of the auditors, it is required

by the auditors to acquire rational guarantee on there is material misstatement in the financial

reports of the clients or not. This makes increases the significance of the concept of

materiality in auditing. Auditors apply this as audit planning stage along with performing

audit and evaluating the impacts of material misstatements on the overall audit.

The use of materiality in auditing can be seen in order to test and asses the legitimacy

of information in the financial statements and associated notes. The presence of all

materiality related rules and regulations can be seen under ASA 320 Materiality in Planning

and Performing an Audit (auasb.gov.au 2020). It is needed for the auditor of Reece Group

Limited to utilize his/her professional judgment and understanding of the client at the time to

set panning materiality level and the auditor also needs to be alert of the primary users of the

financial statements. The auditor of Reece Group Limited has the option to select the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

appropriate base of materiality either from income statement items or from balance sheet

item. The main items of income statement are revenue, gross profit or profit before tax; and

the key items of balance sheet are total equity or total assets. Professional judgment of the

auditor needs to be used while selecting the appropriate base (Eilifsen and Messier Jr 2014).

It can be seen from the annual report of Reece Group Limited that the company has been bale

in registering large amount of revenues over the years; and therefore, revenue is the

appropriate base for the planning materiality level of Reece Group Limited. According to

ASA 320 Materiality in Planning and Performing an Audit, Para A8, professional

judgements need to be applied by the auditor to determine the percentage; and it needs to be

taken into consideration that there is a relationship between the chosen benchmark and

percentage. Therefore, in case of Reece Group Limited, 0.025% is considered as the

appropriate percentage that is to be charged on total revenue. The level of materiality of

Reece Group Limited is calculated below:

Planning Materiality Level = Revenue × 0.025%

= $ 2,691,356,000 × 0.00025

= $672839

Our assessment of what can go wrong

After obtaining the required understanding on the client and identifying the significant

accounts, it is needed for the auditors to assess what can go wrong in these accounts or the

presence of material misstatements in these accounts. This helps in providing the basis to

design and perform additional audit procedures. One crucial part of this is the prioritisation of

the identified risks as this helps in determining what audit procedures need to be undertaken.

The following discussion shows discusses about what can go wrong with these five selected

accounts:

Revenue and Other Income – It is discussed in the above that the sales revenue of Reece

Group Limited has majorly increased in 2018 and this indicates towards the presence of fraud

risk. It is mentioned in the annual report of Reece Group Limited that the company faces

major competition and interruption from unlikely sources. It means Reece Group Limited

operates in a highly competitive industry where the pressure is on its management to achieve

high sales targets. This particular aspect creates the risk of overstating the sales figure in

manipulative and fraudulent manner. This risk cannot be reduced with the company’s internal

control which implies that the inherent risk in this aspect is high for Reece Group Limited

(McKee 2014).

Cash and Cash Equivalents – Earlier discussion indicates that there is significant increase

in the cash and cash equivalent of Reece Group Limited in 2018 and this is also an indicator

that there may be overstatement of cash and cash equivalent by the management to enhance

its short-term liquidity position. It can be the outcome of the competitive pressure on the

company. In addition, Reece Group Limited might have running low of cash which can raise

significant doubt on its ability to continue as a going concern since the core operation of it

were not able to fetch adequate cash. It implies that Reece Group Limited has a high inherent

risk (Boritz, Kochetova-Kozloski and Robinson 2014).

Receivables – It can also be seen that receivables of Reece Group Limited have also

increased in 2018 and two fraudulent activities can be involved in this. First, the management

of Reece Group Limited may have realized the dues from the debtors but did not report it in

the period when it was collected and this will show increased receivables amount. Second,

the management may have used incorrect provision associated with the collection of

receivables. However, the intention behind both of these actions is to enhance the short-term

item. The main items of income statement are revenue, gross profit or profit before tax; and

the key items of balance sheet are total equity or total assets. Professional judgment of the

auditor needs to be used while selecting the appropriate base (Eilifsen and Messier Jr 2014).

It can be seen from the annual report of Reece Group Limited that the company has been bale

in registering large amount of revenues over the years; and therefore, revenue is the

appropriate base for the planning materiality level of Reece Group Limited. According to

ASA 320 Materiality in Planning and Performing an Audit, Para A8, professional

judgements need to be applied by the auditor to determine the percentage; and it needs to be

taken into consideration that there is a relationship between the chosen benchmark and

percentage. Therefore, in case of Reece Group Limited, 0.025% is considered as the

appropriate percentage that is to be charged on total revenue. The level of materiality of

Reece Group Limited is calculated below:

Planning Materiality Level = Revenue × 0.025%

= $ 2,691,356,000 × 0.00025

= $672839

Our assessment of what can go wrong

After obtaining the required understanding on the client and identifying the significant

accounts, it is needed for the auditors to assess what can go wrong in these accounts or the

presence of material misstatements in these accounts. This helps in providing the basis to

design and perform additional audit procedures. One crucial part of this is the prioritisation of

the identified risks as this helps in determining what audit procedures need to be undertaken.

The following discussion shows discusses about what can go wrong with these five selected

accounts:

Revenue and Other Income – It is discussed in the above that the sales revenue of Reece

Group Limited has majorly increased in 2018 and this indicates towards the presence of fraud

risk. It is mentioned in the annual report of Reece Group Limited that the company faces

major competition and interruption from unlikely sources. It means Reece Group Limited

operates in a highly competitive industry where the pressure is on its management to achieve

high sales targets. This particular aspect creates the risk of overstating the sales figure in

manipulative and fraudulent manner. This risk cannot be reduced with the company’s internal

control which implies that the inherent risk in this aspect is high for Reece Group Limited

(McKee 2014).

Cash and Cash Equivalents – Earlier discussion indicates that there is significant increase

in the cash and cash equivalent of Reece Group Limited in 2018 and this is also an indicator

that there may be overstatement of cash and cash equivalent by the management to enhance

its short-term liquidity position. It can be the outcome of the competitive pressure on the

company. In addition, Reece Group Limited might have running low of cash which can raise

significant doubt on its ability to continue as a going concern since the core operation of it

were not able to fetch adequate cash. It implies that Reece Group Limited has a high inherent

risk (Boritz, Kochetova-Kozloski and Robinson 2014).

Receivables – It can also be seen that receivables of Reece Group Limited have also

increased in 2018 and two fraudulent activities can be involved in this. First, the management

of Reece Group Limited may have realized the dues from the debtors but did not report it in

the period when it was collected and this will show increased receivables amount. Second,

the management may have used incorrect provision associated with the collection of

receivables. However, the intention behind both of these actions is to enhance the short-term

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

liquidity position of the company. This risk could be mitigated through internal control and

therefore, the control risk is risk in this case (Fortvingler 2016).

Inventory – Inventories of Reece Group Limited has significantly increased in the year of

2018 which indicates towards the overstatement of inventory by the management for

enhancing the short-term liquidity position. It needs to be mentioned that cash received

majorly connected with inventories where cash is generated from the sale of inventories.

However, increase in cash as well as inventories in Reece Group Limited indicate towards the

presence of fraud around inventories. This risk could be mitigated with effective internal

control and therefore, control risk is high in this case (Fukukawa, Mock and Srivastava

2014).

Long-term Borrowing – It can be seen from the above that the long-term borrowings of

Reece Group Limited has been fully repaid in 2018 and it indicates towards the presence of

understatement of long-term borrowings in 2018 by its management. The main intention of

the management of the company behind this understatement may be the plan to raise further

debt or renegotiate a loan. Presence of huge debt would affect the company’s long-term

liquidity and solvency position to take more loans. Therefore, the management of Reece

Group Limited may have understated the long-term debts or may have classified the long-

term debts incorrectly. In this context, it needs to be mentioned that this increases the

inherent risks of audit of Reece Group Limited associated with long-term debts (Favere-

Marchesi 2013).

Conclusion

The above analysis undertakes the analysis of different steps in the audit planning of

Reece Group Limited. It can be seen from the above that Reece Group Limited operates in a

highly competitive industry where in likely forces disrupt its business operations. The

company has become able in establishing an effective internal control by taking into

consideration all the necessary aspects such as the implementation of an effective risk

management framework, effective distribution and segregation of the duties of senior

executives, control on financial reporting and others. The report also shows that there are five

accounts that are at the high risk of material misstatements; they are sales revenue account,

cash and cash equivalent account, receivables account, inventories account and long-term

borrowings account. The balances of these accounts have fluctuated in 2018 unexpectedly

which raises the doubt of the presence of material misstatements in them. This report

discusses about the necessary aspects associated with the determination of planning

materiality of the audit of Reece Group Limited by discussing the consideration of necessary

aspects in materiality determination such as appropriate base and selection of percentage. The

planning materiality level of Reece Group Limited is obtained by charging 2.5% on total

sales. The last parts show that presence of frauds in the mentioned five accounts with the aim

to achieve certain objectives of the management of Reece Group Limited. The increase in

sales revenue can be the outcome of competitive pressure on the management to post higher

amount of sales. The increase in cash and cash equivalent, receivables and inventories can be

the reason to enhance short-term liquidity position and to mitigate the going concern risk.

The decrease in long-term borrowings can be the reason to improve long-term liquidity

position for raising more loans.

therefore, the control risk is risk in this case (Fortvingler 2016).

Inventory – Inventories of Reece Group Limited has significantly increased in the year of

2018 which indicates towards the overstatement of inventory by the management for

enhancing the short-term liquidity position. It needs to be mentioned that cash received

majorly connected with inventories where cash is generated from the sale of inventories.

However, increase in cash as well as inventories in Reece Group Limited indicate towards the

presence of fraud around inventories. This risk could be mitigated with effective internal

control and therefore, control risk is high in this case (Fukukawa, Mock and Srivastava

2014).

Long-term Borrowing – It can be seen from the above that the long-term borrowings of

Reece Group Limited has been fully repaid in 2018 and it indicates towards the presence of

understatement of long-term borrowings in 2018 by its management. The main intention of

the management of the company behind this understatement may be the plan to raise further

debt or renegotiate a loan. Presence of huge debt would affect the company’s long-term

liquidity and solvency position to take more loans. Therefore, the management of Reece

Group Limited may have understated the long-term debts or may have classified the long-

term debts incorrectly. In this context, it needs to be mentioned that this increases the

inherent risks of audit of Reece Group Limited associated with long-term debts (Favere-

Marchesi 2013).

Conclusion

The above analysis undertakes the analysis of different steps in the audit planning of

Reece Group Limited. It can be seen from the above that Reece Group Limited operates in a

highly competitive industry where in likely forces disrupt its business operations. The

company has become able in establishing an effective internal control by taking into

consideration all the necessary aspects such as the implementation of an effective risk

management framework, effective distribution and segregation of the duties of senior

executives, control on financial reporting and others. The report also shows that there are five

accounts that are at the high risk of material misstatements; they are sales revenue account,

cash and cash equivalent account, receivables account, inventories account and long-term

borrowings account. The balances of these accounts have fluctuated in 2018 unexpectedly

which raises the doubt of the presence of material misstatements in them. This report

discusses about the necessary aspects associated with the determination of planning

materiality of the audit of Reece Group Limited by discussing the consideration of necessary

aspects in materiality determination such as appropriate base and selection of percentage. The

planning materiality level of Reece Group Limited is obtained by charging 2.5% on total

sales. The last parts show that presence of frauds in the mentioned five accounts with the aim

to achieve certain objectives of the management of Reece Group Limited. The increase in

sales revenue can be the outcome of competitive pressure on the management to post higher

amount of sales. The increase in cash and cash equivalent, receivables and inventories can be

the reason to enhance short-term liquidity position and to mitigate the going concern risk.

The decrease in long-term borrowings can be the reason to improve long-term liquidity

position for raising more loans.

Appendix

Consolidated Statement of Profit or Loss and Other Comprehensive Income

Consolidated Statement of Profit or Loss and Other Comprehensive Income

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Consolidated Statement of Financial Position

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

References

Aasb.gov.au. 2020. Materiality. [online] Available at:

https://www.aasb.gov.au/admin/file/content105/c9/AASB1031_12-13.pdf [Accessed 12 Jan.

2020].

Auasb.gov.au. 2020. Auditing Standard ASA 200 Overall Objectives of the Independent

Auditor and the Conduct of an Audit in Accordance with Australian Auditing Standards.

[online] Available at:

https://www.auasb.gov.au/admin/file/content102/c3/ASA_200_Compiled_2019-FRL.pdf

[Accessed 12 Jan. 2020].

Auasb.gov.au. 2020. Auditing Standard ASA 315 Identifying and Assessing the Risks of

Material Misstatement through Understanding the Entity and Its Environment. [online]

Available at:

https://www.auasb.gov.au/admin/file/content102/c3/ASA_315_Compiled_2015.pdf

[Accessed 12 Jan. 2020].

Auasb.gov.au. 2020. Auditing Standard ASA 320 Materiality in Planning and Performing an

Audit. [online] Available at:

https://www.auasb.gov.au/admin/file/content102/c3/ASA_320_Compiled_2015.pdf

[Accessed 12 Jan. 2020].

Bhattacharjee, S., Maletta, M.J. and Moreno, K.K., 2015. The role of account subjectivity and

risk of material misstatement on auditors' internal audit reliance judgments. Accounting

Horizons, 30(2), pp.225-238.

Boritz, J.E., Kochetova-Kozloski, N. and Robinson, L., 2014. Are fraud specialists relatively

more effective than auditors at modifying audit programs in the presence of fraud risk?. The

Accounting Review, 90(3), pp.881-915.

Czerney, K., Schmidt, J.J. and Thompson, A.M., 2014. Does auditor explanatory language in

unqualified audit reports indicate increased financial misstatement risk?. The Accounting

Review, 89(6), pp.2115-2149.

Dao, M. and Pham, T., 2014. Audit tenure, auditor specialization and audit report

lag. Managerial Auditing Journal, 29(6), pp.490-512.

Eilifsen, A. and Messier Jr, W.F., 2014. Materiality guidance of the major public accounting

firms. Auditing: A Journal of Practice & Theory, 34(2), pp.3-26.

Favere-Marchesi, M., 2013. Effects of decomposition and categorization on fraud-risk

assessments. Auditing: A Journal of Practice & Theory, 32(4), pp.201-219.

Fontaine, R., Letaifa, S. B., & Herda, D. (2013). An interview study to understand the

reasons clients change audit firms and the client's perceived value of the audit

service. Current Issues in Auditing, 7(1), A1-A14.

Fortvingler, J., 2016. Different approaches to fraud risk assessment and their implications on

audit planning. Periodica Polytechnica Social and Management Sciences, 24(2), pp.102-112.

Fukukawa, H., Mock, T.J. and Srivastava, R.P., 2014. Assessing the risk of fraud at Olympus

and identifying an effective audit plan. The Japanese Accounting Review, 4(2014), pp.1-25.

Jans, M., Alles, M.G. and Vasarhelyi, M.A., 2014. A field study on the use of process mining

of event logs as an analytical procedure in auditing. The Accounting Review, 89(5), pp.1751-

1773.

Kochetova-Kozloski, N., Kozloski, T.M. and Messier Jr, W.F., 2013. Auditor business

process analysis and linkages among auditor risk judgments. Auditing: A Journal of Practice

& Theory, 32(3), pp.123-139.

Aasb.gov.au. 2020. Materiality. [online] Available at:

https://www.aasb.gov.au/admin/file/content105/c9/AASB1031_12-13.pdf [Accessed 12 Jan.

2020].

Auasb.gov.au. 2020. Auditing Standard ASA 200 Overall Objectives of the Independent

Auditor and the Conduct of an Audit in Accordance with Australian Auditing Standards.

[online] Available at:

https://www.auasb.gov.au/admin/file/content102/c3/ASA_200_Compiled_2019-FRL.pdf

[Accessed 12 Jan. 2020].

Auasb.gov.au. 2020. Auditing Standard ASA 315 Identifying and Assessing the Risks of

Material Misstatement through Understanding the Entity and Its Environment. [online]

Available at:

https://www.auasb.gov.au/admin/file/content102/c3/ASA_315_Compiled_2015.pdf

[Accessed 12 Jan. 2020].

Auasb.gov.au. 2020. Auditing Standard ASA 320 Materiality in Planning and Performing an

Audit. [online] Available at:

https://www.auasb.gov.au/admin/file/content102/c3/ASA_320_Compiled_2015.pdf

[Accessed 12 Jan. 2020].

Bhattacharjee, S., Maletta, M.J. and Moreno, K.K., 2015. The role of account subjectivity and

risk of material misstatement on auditors' internal audit reliance judgments. Accounting

Horizons, 30(2), pp.225-238.

Boritz, J.E., Kochetova-Kozloski, N. and Robinson, L., 2014. Are fraud specialists relatively

more effective than auditors at modifying audit programs in the presence of fraud risk?. The

Accounting Review, 90(3), pp.881-915.

Czerney, K., Schmidt, J.J. and Thompson, A.M., 2014. Does auditor explanatory language in

unqualified audit reports indicate increased financial misstatement risk?. The Accounting

Review, 89(6), pp.2115-2149.

Dao, M. and Pham, T., 2014. Audit tenure, auditor specialization and audit report

lag. Managerial Auditing Journal, 29(6), pp.490-512.

Eilifsen, A. and Messier Jr, W.F., 2014. Materiality guidance of the major public accounting

firms. Auditing: A Journal of Practice & Theory, 34(2), pp.3-26.

Favere-Marchesi, M., 2013. Effects of decomposition and categorization on fraud-risk

assessments. Auditing: A Journal of Practice & Theory, 32(4), pp.201-219.

Fontaine, R., Letaifa, S. B., & Herda, D. (2013). An interview study to understand the

reasons clients change audit firms and the client's perceived value of the audit

service. Current Issues in Auditing, 7(1), A1-A14.

Fortvingler, J., 2016. Different approaches to fraud risk assessment and their implications on

audit planning. Periodica Polytechnica Social and Management Sciences, 24(2), pp.102-112.

Fukukawa, H., Mock, T.J. and Srivastava, R.P., 2014. Assessing the risk of fraud at Olympus

and identifying an effective audit plan. The Japanese Accounting Review, 4(2014), pp.1-25.

Jans, M., Alles, M.G. and Vasarhelyi, M.A., 2014. A field study on the use of process mining

of event logs as an analytical procedure in auditing. The Accounting Review, 89(5), pp.1751-

1773.

Kochetova-Kozloski, N., Kozloski, T.M. and Messier Jr, W.F., 2013. Auditor business

process analysis and linkages among auditor risk judgments. Auditing: A Journal of Practice

& Theory, 32(3), pp.123-139.

Lobo, G.J. and Zhao, Y., 2013. Relation between audit effort and financial report

misstatements: Evidence from quarterly and annual restatements. The Accounting

Review, 88(4), pp.1385-1412.

McKee, T.E., 2014. Evaluating financial fraud risk during audit planning. The CPA

Journal, 84(10), p.28.

Reecegroup.com.au. 2020. Annual Report – 2018. [online] Available at:

https://www.reecegroup.com.au/site-assets/Downloads/180830-Reece-Group-2018-Annual-

Report-FINAL.pdf [Accessed 12 Jan. 2020].

Tepalagul, N. and Lin, L., 2015. Auditor independence and audit quality: A literature

review. Journal of Accounting, Auditing & Finance, 30(1), pp.101-121.

misstatements: Evidence from quarterly and annual restatements. The Accounting

Review, 88(4), pp.1385-1412.

McKee, T.E., 2014. Evaluating financial fraud risk during audit planning. The CPA

Journal, 84(10), p.28.

Reecegroup.com.au. 2020. Annual Report – 2018. [online] Available at:

https://www.reecegroup.com.au/site-assets/Downloads/180830-Reece-Group-2018-Annual-

Report-FINAL.pdf [Accessed 12 Jan. 2020].

Tepalagul, N. and Lin, L., 2015. Auditor independence and audit quality: A literature

review. Journal of Accounting, Auditing & Finance, 30(1), pp.101-121.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.