Assessment 4: Research Proposal on Auditors and Corporate Governance

VerifiedAdded on 2022/11/17

|7

|440

|36

Project

AI Summary

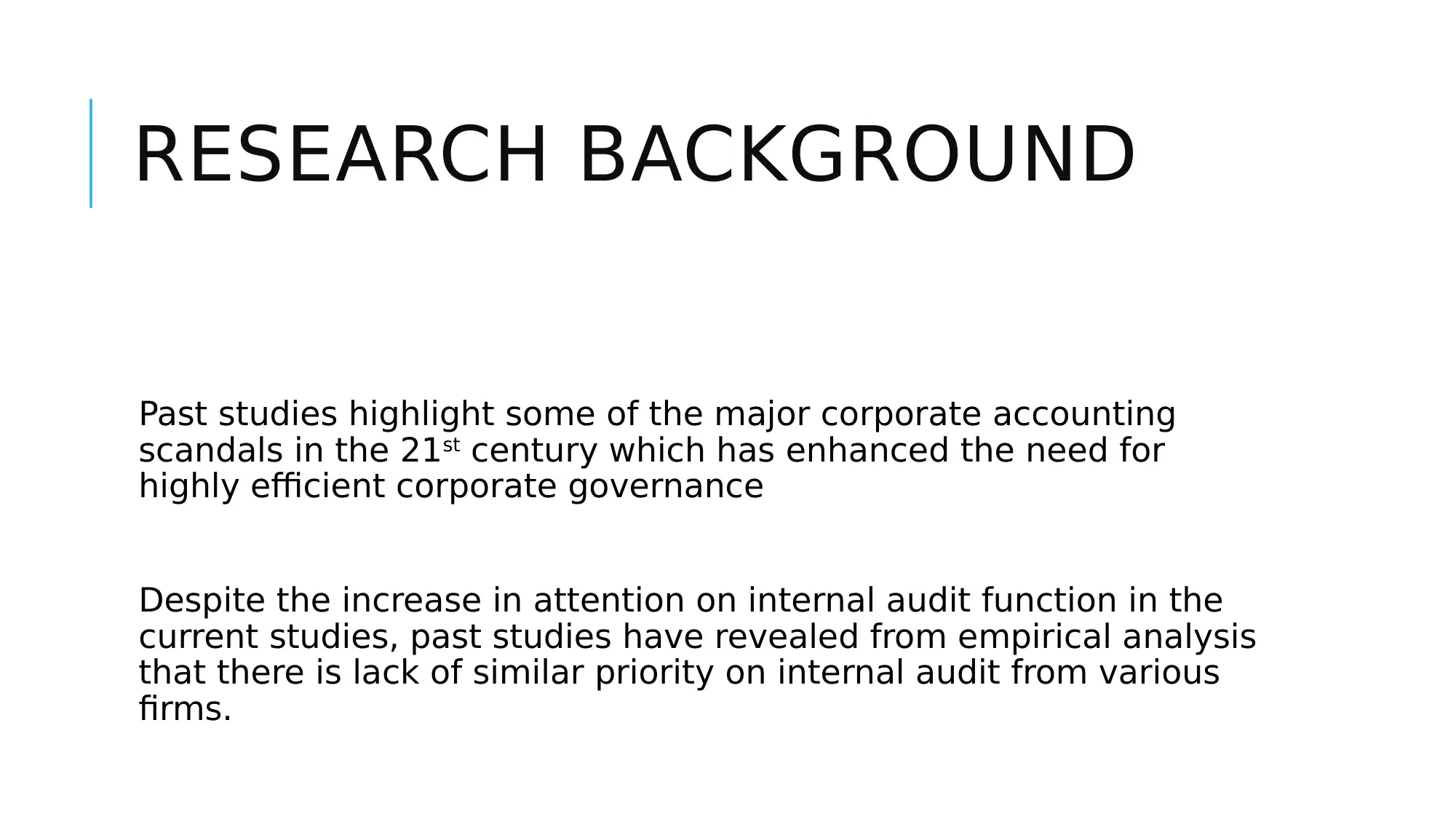

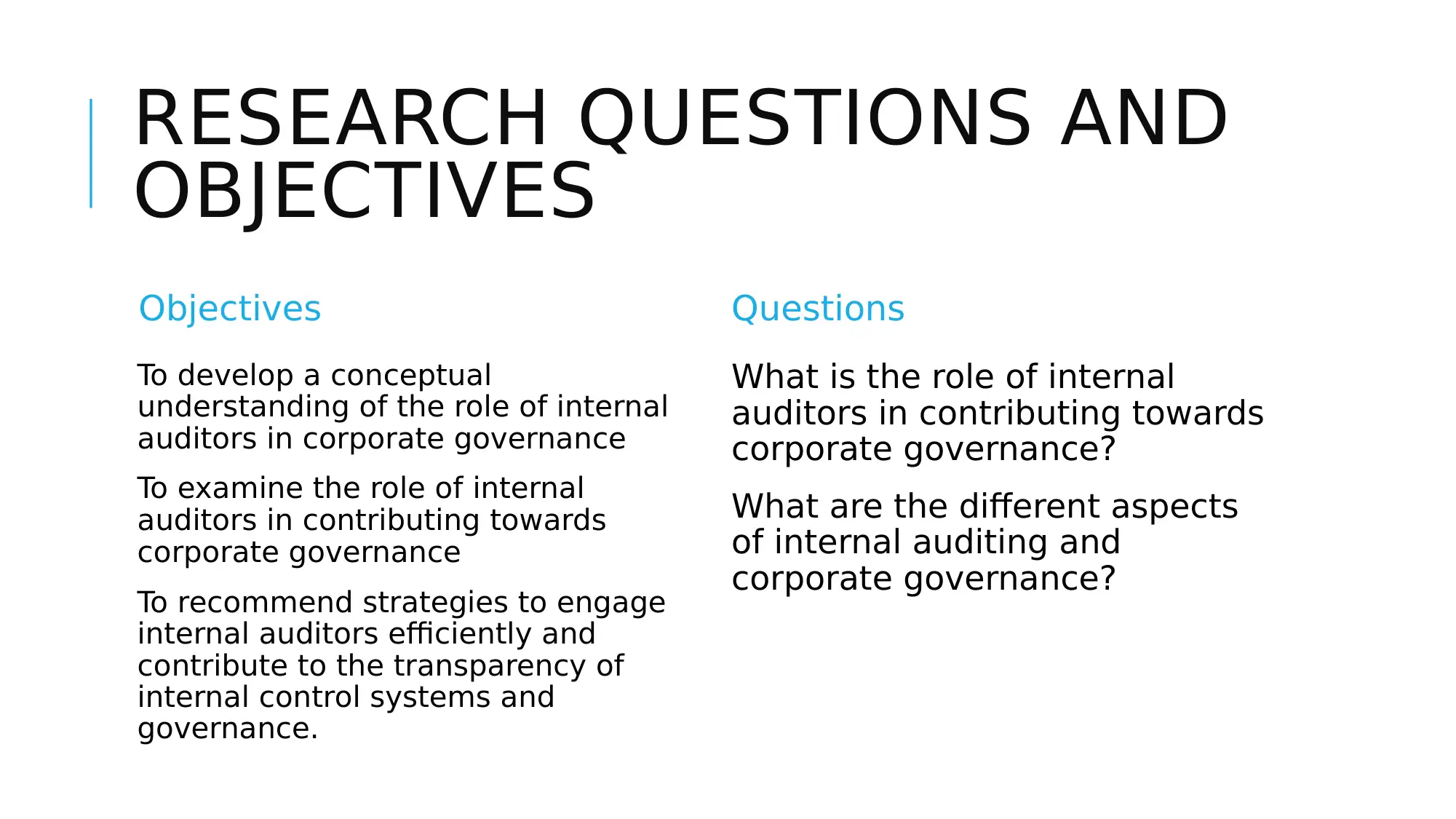

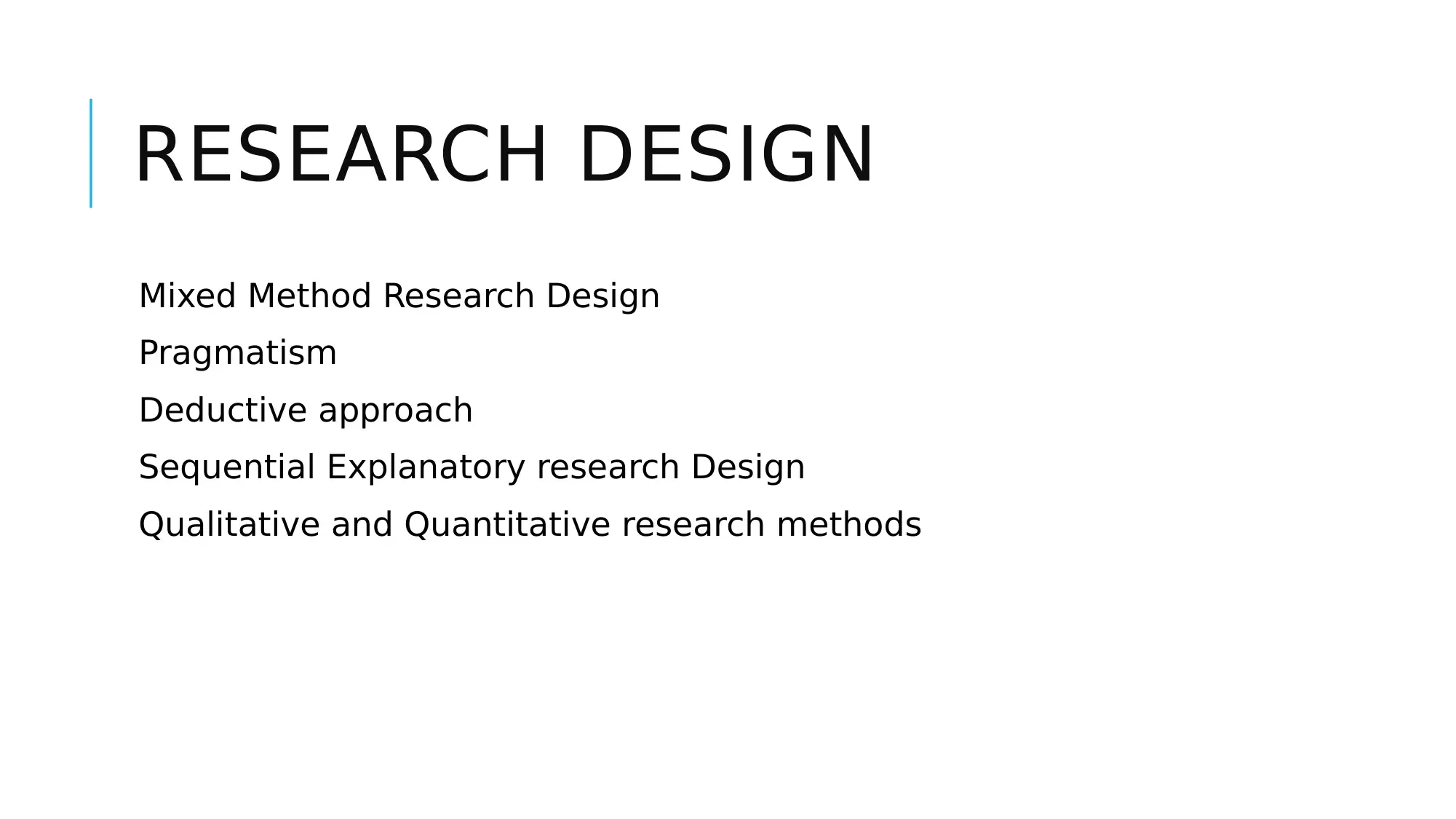

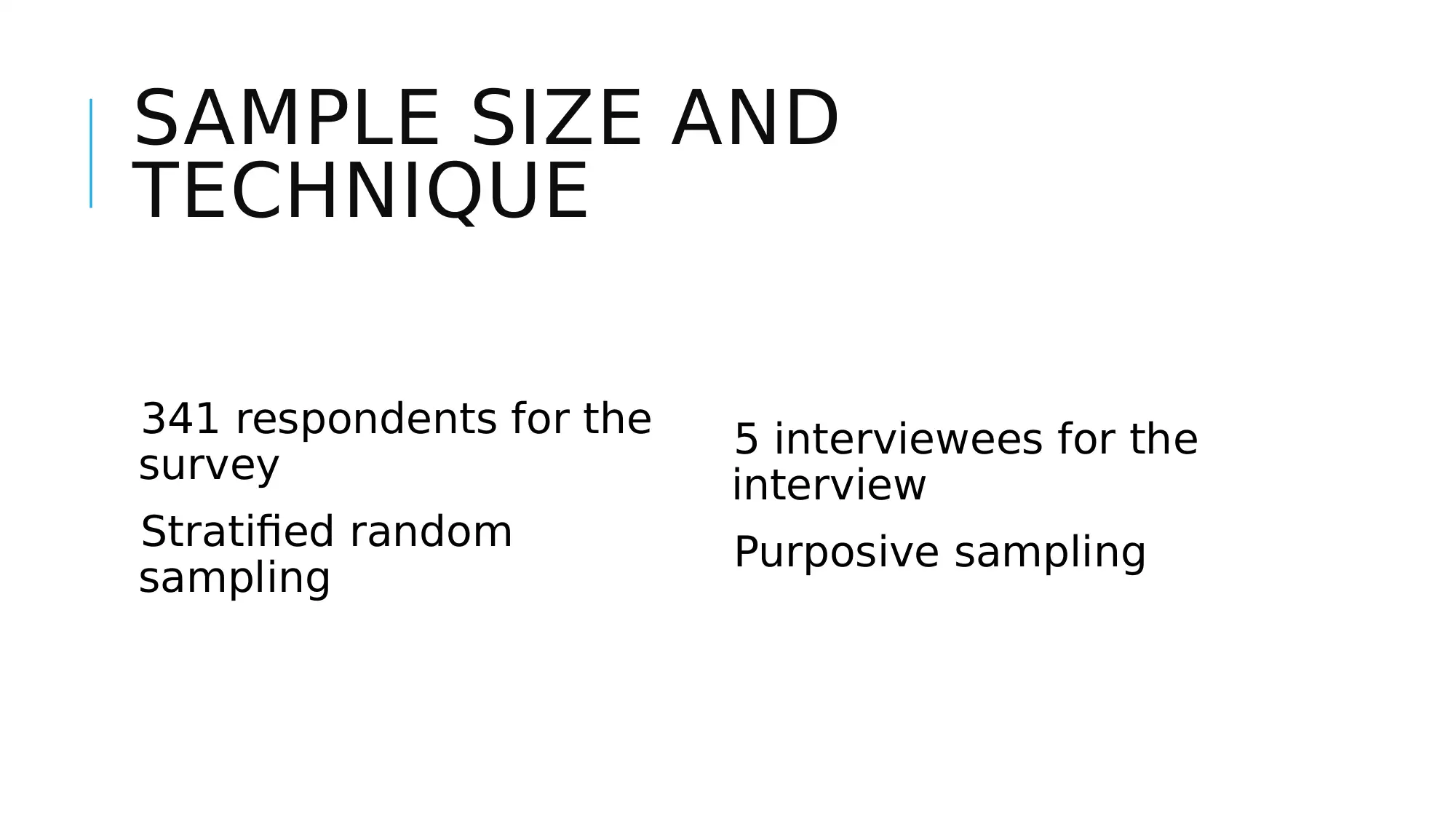

This research proposal examines the crucial role of internal auditors in corporate governance. It begins by highlighting the significance of corporate governance in light of accounting scandals and emphasizes the need for efficient internal audit functions. The research aims to develop a conceptual understanding of the internal auditor's role, examine their contribution to corporate governance, and recommend strategies to enhance their engagement and transparency. The study employs a mixed-methods research design, combining qualitative and quantitative methods, including a survey with 341 respondents and interviews with 5 individuals, to gather comprehensive data. The proposal outlines the research questions, objectives, and the chosen pragmatic, deductive, and sequential explanatory research design, along with the sampling techniques and relevant references. The proposal aims to provide insights into how internal auditors contribute to the transparency of internal control systems and governance.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.