A Study on the Regulation of Australian Banks: Past, Present, Future

VerifiedAdded on 2020/02/23

|10

|3105

|35

Report

AI Summary

This report provides a comprehensive overview of the regulation of Australian banks. It begins with a historical perspective, tracing the evolution of banking regulations in Australia from the early days to the present. The report then details the current structure of bank regulations, highlighting the roles of key regulatory bodies such as the Australian Prudential Regulation Authority (APRA), the Australian Securities and Investments Commission (ASIC), and the Reserve Bank of Australia (RBA). It examines the impact of regulations, including those related to capital adequacy and compliance. Furthermore, the report explores the future of banking regulations in Australia, considering factors like technological advancements, customer behavior, and global economic trends. It also discusses recommendations for future regulation, including the need for ongoing supervision, adaptation to financial innovation, and maintaining a strong corporate governance framework to ensure the stability and integrity of the Australian banking sector. The report concludes by emphasizing the importance of proactive regulation and the need for banks to view compliance not merely as a management of external risk but as a critical asset.

RUNNING HEAD: REGULATION OF AUSTRALIAN BANKS

PAST, PRESENT AND FUTURE OF

AUSTRALIAN BANK’S REGULATIONS

PAST, PRESENT AND FUTURE OF

AUSTRALIAN BANK’S REGULATIONS

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REGULATION OF AUSTRALIAN BANKS 1

Table of Contents

Introduction...........................................................................................................................................1

History of Australian Banks’ Regulations...............................................................................................1

Present Structure of Bank’s Regulations................................................................................................2

Future of Banking Regulations in Australia............................................................................................4

Recommendations for future regulation in Australian Banks................................................................6

Supervision over regulations.............................................................................................................6

Regulations and financial innovation.................................................................................................6

Conclusions............................................................................................................................................6

References.............................................................................................................................................8

Table of Contents

Introduction...........................................................................................................................................1

History of Australian Banks’ Regulations...............................................................................................1

Present Structure of Bank’s Regulations................................................................................................2

Future of Banking Regulations in Australia............................................................................................4

Recommendations for future regulation in Australian Banks................................................................6

Supervision over regulations.............................................................................................................6

Regulations and financial innovation.................................................................................................6

Conclusions............................................................................................................................................6

References.............................................................................................................................................8

REGULATION OF AUSTRALIAN BANKS 2

Introduction

Banking is a major sector in the economy of Australia and it contributes significant portion in

the country’s economic condition. The financial sector of Australia is extremely liquid strong

and sophisticated and therefore it is ranked at the fourth position in the entire world for the

size of its pool of assets i.e. the investments funds. The banking sector of Australia

constitutes mainly four prime banks which are as follows:

Commonwealth Bank of Australia

Westpac Banking Corporation

National Australia Bank

Australia and New Zealand Banking Group

Due to the financial stability maintained by the banking companies in Australia and the

activities of finance such as lending and borrowing functions, the financial sector of Australia

has been rated as the best financial centres in the world. Apart from the activities of financial

intermediation, the banks in Australia are also involve in other functions such as stock

broking activities, financial market trading, insurance activities etc. The banking regulation

includes different areas such as the legislative framework under which the Banks and other

financial institutions are working, the regulatory bodies that are controlling the banking

sector, the supervisory bodies of financial sector, licensing policies of banking industries etc.

History of Australian Banks’ Regulations

The first bank that was started in Australia in 1817 was the bank of New South Wales. The

increase in the values of the properties in Australia caused the crisis in Australian bank. In the

past, the regulation in the banking sector was not much stringent and there was no tight

control of government over the banks of Australia due to which many commercial banks

were failed to operate. The country had to face huge depression in 1930 due which there a

series of bank failures. But after the depression’s end, the banking regulation in Australia was

made strict which made it nearly impossible to set up any branch in Australia for the foreign

owned banks. Resultantly, the banks in Australia were quite less in comparison to the other

countries. With the tight regulation, the Australian banks were bifurcated in two main

categories i.e. the Savings Banks and the Trading Bank (Joshi, Cahill & Sidhu, 2010). Since the

regulatory framework for the banking industry was getting extremely strict, another type of

non-banking finance organisations in financial system were started getting developed like the

Introduction

Banking is a major sector in the economy of Australia and it contributes significant portion in

the country’s economic condition. The financial sector of Australia is extremely liquid strong

and sophisticated and therefore it is ranked at the fourth position in the entire world for the

size of its pool of assets i.e. the investments funds. The banking sector of Australia

constitutes mainly four prime banks which are as follows:

Commonwealth Bank of Australia

Westpac Banking Corporation

National Australia Bank

Australia and New Zealand Banking Group

Due to the financial stability maintained by the banking companies in Australia and the

activities of finance such as lending and borrowing functions, the financial sector of Australia

has been rated as the best financial centres in the world. Apart from the activities of financial

intermediation, the banks in Australia are also involve in other functions such as stock

broking activities, financial market trading, insurance activities etc. The banking regulation

includes different areas such as the legislative framework under which the Banks and other

financial institutions are working, the regulatory bodies that are controlling the banking

sector, the supervisory bodies of financial sector, licensing policies of banking industries etc.

History of Australian Banks’ Regulations

The first bank that was started in Australia in 1817 was the bank of New South Wales. The

increase in the values of the properties in Australia caused the crisis in Australian bank. In the

past, the regulation in the banking sector was not much stringent and there was no tight

control of government over the banks of Australia due to which many commercial banks

were failed to operate. The country had to face huge depression in 1930 due which there a

series of bank failures. But after the depression’s end, the banking regulation in Australia was

made strict which made it nearly impossible to set up any branch in Australia for the foreign

owned banks. Resultantly, the banks in Australia were quite less in comparison to the other

countries. With the tight regulation, the Australian banks were bifurcated in two main

categories i.e. the Savings Banks and the Trading Bank (Joshi, Cahill & Sidhu, 2010). Since the

regulatory framework for the banking industry was getting extremely strict, another type of

non-banking finance organisations in financial system were started getting developed like the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

REGULATION OF AUSTRALIAN BANKS 3

credit union and the building societies. As these institutions were not recognised as banks

they were free from the strict regulatory policies of banking system it privileged them give

and take loans at higher rates of interest but at the same time they were allowed to provide

only the limited services. However, the regulatory policies of banking sector in Australia

were being removed at a slow pace in 1960 and as a result of which the classification of

banks as trading and savings banks was nullified and every Australian bank was given the

liberty to work as merchant banks to perform their functioning in the money market (Griffith-

Jones & Rodriguez, 2016). Moreover, the banks were given the independence to set the rates of

interests on their own. As deregulation of banking industry was being carried out, the controls

in the foreign exchange areas well also completely abandoned leading to the easy float of

Australian currency i.e. the Australian dollar in 1983 (Singleton & Verhoef, 2010). The changes

in the regulatory policies allowed those non- banking finance institutions to turn into banks

without any requirement of demutualisation. After this, in 1990 the Australian government

started with a policy known as four pillars policy in context with the Australian Banking

System, through which it restricted the mergers of the four major banks. This act of

government was well established policy and not merely a formal regulation.

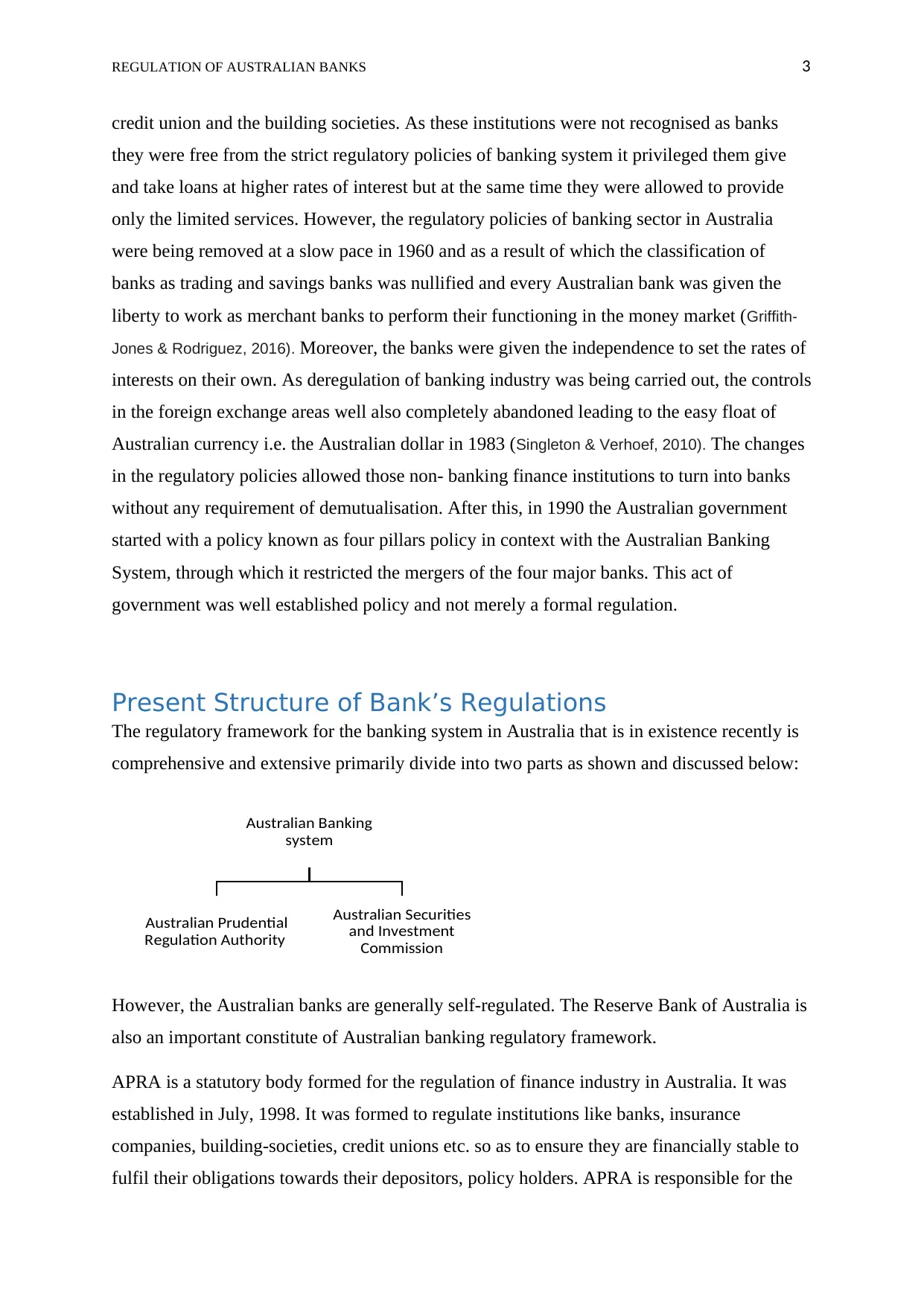

Present Structure of Bank’s Regulations

The regulatory framework for the banking system in Australia that is in existence recently is

comprehensive and extensive primarily divide into two parts as shown and discussed below:

However, the Australian banks are generally self-regulated. The Reserve Bank of Australia is

also an important constitute of Australian banking regulatory framework.

APRA is a statutory body formed for the regulation of finance industry in Australia. It was

established in July, 1998. It was formed to regulate institutions like banks, insurance

companies, building-societies, credit unions etc. so as to ensure they are financially stable to

fulfil their obligations towards their depositors, policy holders. APRA is responsible for the

Australian Banking

system

Australian Prudential

Regulation Authority

Australian Securities

and Investment

Commission

credit union and the building societies. As these institutions were not recognised as banks

they were free from the strict regulatory policies of banking system it privileged them give

and take loans at higher rates of interest but at the same time they were allowed to provide

only the limited services. However, the regulatory policies of banking sector in Australia

were being removed at a slow pace in 1960 and as a result of which the classification of

banks as trading and savings banks was nullified and every Australian bank was given the

liberty to work as merchant banks to perform their functioning in the money market (Griffith-

Jones & Rodriguez, 2016). Moreover, the banks were given the independence to set the rates of

interests on their own. As deregulation of banking industry was being carried out, the controls

in the foreign exchange areas well also completely abandoned leading to the easy float of

Australian currency i.e. the Australian dollar in 1983 (Singleton & Verhoef, 2010). The changes

in the regulatory policies allowed those non- banking finance institutions to turn into banks

without any requirement of demutualisation. After this, in 1990 the Australian government

started with a policy known as four pillars policy in context with the Australian Banking

System, through which it restricted the mergers of the four major banks. This act of

government was well established policy and not merely a formal regulation.

Present Structure of Bank’s Regulations

The regulatory framework for the banking system in Australia that is in existence recently is

comprehensive and extensive primarily divide into two parts as shown and discussed below:

However, the Australian banks are generally self-regulated. The Reserve Bank of Australia is

also an important constitute of Australian banking regulatory framework.

APRA is a statutory body formed for the regulation of finance industry in Australia. It was

established in July, 1998. It was formed to regulate institutions like banks, insurance

companies, building-societies, credit unions etc. so as to ensure they are financially stable to

fulfil their obligations towards their depositors, policy holders. APRA is responsible for the

Australian Banking

system

Australian Prudential

Regulation Authority

Australian Securities

and Investment

Commission

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REGULATION OF AUSTRALIAN BANKS 4

supervision and providing the licenses to operate to various superannuation funds and the

insurance companies (Dollery, Kortt & Grant , 2013). The institutions of finance to whom APRA

is regulating, are required to provide the report of their operations to APRA on a regular

basis. APRA has announced certain guidelines on capital adequacy ratio to be maintained by

banks, which are in line with the BASEL II guidelines.

ASIC is an independent body with the key responsibility of regulation of certain financial

companies and banks. Along with that it also has the responsibility of ensuring the protection

of the consumer’s right, imparting financial literacy, overseeing the corporate governance

practices, managing the financial services etc. As the regulators of Australian banks ASIC

assesses the efficiency with which the banks are complying the regulatory requirements

applicable on the Australian banks.

Reserve Bank of Australia: The reserve bank is given the responsibility to formulate the

banking policies and to issue of norms of operations of Australian banks. It is the central

bank of Australia and the powers are assigned to it through the Reserve Bank Act. RBA also

provides various services relating to banking to the government of Australia and to the other

financial institutions and banks operating in Australia. The RBA seeks to encourage the

maintenance of stability in the financial system of banking institutions and it also ensures the

safety in the system of payments deployed by the banks. The currency notes of Australian

country are also issue by the Reserve Bank of Australia.

There is a drastic increase in the number of inquiries and investigations of the Australian

banking institutions over last few years as the regulations towards the banking sector is

getting stringent gradually. The bank regulators of the banks are requiring the banking

institutions to be more compliant towards the rules framed therein. The violations of which

includes heavy fines and penalty provisions. The regulations are quite tight in certain areas

such as the money laundering activities, breach of bank’s code of conduct, activities of

insider trading and other crimes in the financial areas are involving heavy litigations to

prevent such an unethical conduct in banking sectors as public invests their huge funds in

these financial institutions therefore a greater level of transparency is required to be

maintained by the banks.

Moreover, the current reforms that have introduced in the banking sector all over the globe

have the objectives of enhancing the quality and quantity of capitals of banks and to instigate

its consistency in the liquidity position of banks. These reforms are also targeted to achieve

supervision and providing the licenses to operate to various superannuation funds and the

insurance companies (Dollery, Kortt & Grant , 2013). The institutions of finance to whom APRA

is regulating, are required to provide the report of their operations to APRA on a regular

basis. APRA has announced certain guidelines on capital adequacy ratio to be maintained by

banks, which are in line with the BASEL II guidelines.

ASIC is an independent body with the key responsibility of regulation of certain financial

companies and banks. Along with that it also has the responsibility of ensuring the protection

of the consumer’s right, imparting financial literacy, overseeing the corporate governance

practices, managing the financial services etc. As the regulators of Australian banks ASIC

assesses the efficiency with which the banks are complying the regulatory requirements

applicable on the Australian banks.

Reserve Bank of Australia: The reserve bank is given the responsibility to formulate the

banking policies and to issue of norms of operations of Australian banks. It is the central

bank of Australia and the powers are assigned to it through the Reserve Bank Act. RBA also

provides various services relating to banking to the government of Australia and to the other

financial institutions and banks operating in Australia. The RBA seeks to encourage the

maintenance of stability in the financial system of banking institutions and it also ensures the

safety in the system of payments deployed by the banks. The currency notes of Australian

country are also issue by the Reserve Bank of Australia.

There is a drastic increase in the number of inquiries and investigations of the Australian

banking institutions over last few years as the regulations towards the banking sector is

getting stringent gradually. The bank regulators of the banks are requiring the banking

institutions to be more compliant towards the rules framed therein. The violations of which

includes heavy fines and penalty provisions. The regulations are quite tight in certain areas

such as the money laundering activities, breach of bank’s code of conduct, activities of

insider trading and other crimes in the financial areas are involving heavy litigations to

prevent such an unethical conduct in banking sectors as public invests their huge funds in

these financial institutions therefore a greater level of transparency is required to be

maintained by the banks.

Moreover, the current reforms that have introduced in the banking sector all over the globe

have the objectives of enhancing the quality and quantity of capitals of banks and to instigate

its consistency in the liquidity position of banks. These reforms are also targeted to achieve

REGULATION OF AUSTRALIAN BANKS 5

the greater level of transparency in banking sectors through the proper and necessary

disclosures thereby strengthening the banks’ performance (Uddin & Suzuki, 2011).

In the past the original Basel Original accord 1988 was implemented and then in 2008 the

new Basel Capital Framework was introduced. As with the new reform as Basel III, the

compliance requirements have also increased (Eubanks, 2010). The committee which is

handed over the function of implementation of Basel III is required to ensure the consistent

delivery of outcomes in the banking sector. The proposal of APRA for the implementation of

the Capital Reform Basel III was passed in the month of September 2011. And the banking

institutions in Australia have to comply with the reform requirements at the soonest. At the

same time APRA has refused to accept any alternative accounting treatment for particular

items in the calculation of regulatory capital (Angelini, et al., 2015). The requirements of Basel

III were applicable globally on the financial institutions, as a whole. However there is an

element which is exclusively applicable to certain countries since Australia is one among

those countries as it has very intense system of banking. The name of that element is D-SIB

which the framework for dealing Domestic Systematically Important Banks.

Future of Banking Regulations in Australia

The banking in future will not be the same banking in current period as there are extensive

forces which are influencing the Australian banking sector behaviour of customers, changes

in democracy, technological advancements, governmental regulations and the depression in

the global economy. To create the financial gains for the shareholders, the Australian banks

needs to be remove the complexities of banking sectors and to be more compliant towards the

regulations made by the government for the financial industries. According to Bill Clinton,

the time of moderate or negligible regulations is now passed and the regulators of Australian

banks have restarted to impose stringent regulatory requirements to the banking sectors.

To improve the operations and the financial performance the banks in Australia will have to

be re-focussed on their approach towards the compliances of regulatory requirements made

by the Australian regulators of banking industry (Bologna, 2010). Not only the maintenance of

transparency in banking functions is required out for better compliance of regulations but also

the serious commitment of firm towards the goodwill maintenance in the market through

excellent credit ratings. The eminent credit rating of a bank itself is the valuable asset for the

banks as it will have positive influence on the regulators thereby helping the banks to avoid

the greater level of transparency in banking sectors through the proper and necessary

disclosures thereby strengthening the banks’ performance (Uddin & Suzuki, 2011).

In the past the original Basel Original accord 1988 was implemented and then in 2008 the

new Basel Capital Framework was introduced. As with the new reform as Basel III, the

compliance requirements have also increased (Eubanks, 2010). The committee which is

handed over the function of implementation of Basel III is required to ensure the consistent

delivery of outcomes in the banking sector. The proposal of APRA for the implementation of

the Capital Reform Basel III was passed in the month of September 2011. And the banking

institutions in Australia have to comply with the reform requirements at the soonest. At the

same time APRA has refused to accept any alternative accounting treatment for particular

items in the calculation of regulatory capital (Angelini, et al., 2015). The requirements of Basel

III were applicable globally on the financial institutions, as a whole. However there is an

element which is exclusively applicable to certain countries since Australia is one among

those countries as it has very intense system of banking. The name of that element is D-SIB

which the framework for dealing Domestic Systematically Important Banks.

Future of Banking Regulations in Australia

The banking in future will not be the same banking in current period as there are extensive

forces which are influencing the Australian banking sector behaviour of customers, changes

in democracy, technological advancements, governmental regulations and the depression in

the global economy. To create the financial gains for the shareholders, the Australian banks

needs to be remove the complexities of banking sectors and to be more compliant towards the

regulations made by the government for the financial industries. According to Bill Clinton,

the time of moderate or negligible regulations is now passed and the regulators of Australian

banks have restarted to impose stringent regulatory requirements to the banking sectors.

To improve the operations and the financial performance the banks in Australia will have to

be re-focussed on their approach towards the compliances of regulatory requirements made

by the Australian regulators of banking industry (Bologna, 2010). Not only the maintenance of

transparency in banking functions is required out for better compliance of regulations but also

the serious commitment of firm towards the goodwill maintenance in the market through

excellent credit ratings. The eminent credit rating of a bank itself is the valuable asset for the

banks as it will have positive influence on the regulators thereby helping the banks to avoid

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

REGULATION OF AUSTRALIAN BANKS 6

the unpleasant interventions of the regulators. Since the quality of any banks compliance

practices towards the regulations is shared publically through the annual reports and the

governmental mediums therefore the banks must not consider these regulations as the

management of external risk on business rather these requirements should be assumed as the

management of a most vital asset of the banks which is needed to be fostered. The privileges

of having good or excellent credit ratings are enormous for any financial institution. The

banks must accept that the major regulatory bodies such as APRA, ASIC and RBA are in the

exclusive position to deal with the antitrust concerns that may prevent the banking company

to incorporate the changes which are in public interest.

The Australian regulations will still continue to remain focused on the corporate governance

requirements for the banking and the other financial sectors. But the introduction of new

capital requirements through the implementation of Basel III capital reforms will strengthen

the banking industry and at the same time will provide the industry with the key challenges.

In spite of the numerous global uncertainties such as delayed implementation of new capital

reforms, APRA and ASIC are closely checking and monitoring the developments that are

going on in the banking industry in today’s era. The Australian regulators have to cope with

the international standards otherwise it would lead to inefficiencies in the banking sector with

increased level of risks. Even after the stricter regulations the banking sectors are

encountering the issues of failures in the compliance requirements, violations of code of

conduct with in the regulatory framework are being reported which requires holistic attention

of the regulatory bodies for Australian Banks (Jeucken, 2010). The bank’s top level

management such as the Board of Directors etc. are required to define the corporate culture

within their banking organisations so as to have a strong compliance framework. Therefore

the Australian regulations needs to be more attentive towards these corporate values and must

make the required rules in such areas. The regulations must also be extended towards the

business strategies formulated and implemented by the Australian banks and the financial

institutions and they should also provide for the interest of banks interests i.e. the banks must

be regulated to not perform anything prejudicial in the public or the customers’ interests.

The new standard on financial institutions are soon to be introduced in near future i.e. 2018

and they will put higher regulatory requirements to be complied with in accordance with the

IFRS 9. Moreover, the new payment platform is also developed collectively by many

financial institutions so that it will lead to detection of fraud done by the banking institutions,

money laundering practices and will manage the liquidity and credit limits of the banks. From

the unpleasant interventions of the regulators. Since the quality of any banks compliance

practices towards the regulations is shared publically through the annual reports and the

governmental mediums therefore the banks must not consider these regulations as the

management of external risk on business rather these requirements should be assumed as the

management of a most vital asset of the banks which is needed to be fostered. The privileges

of having good or excellent credit ratings are enormous for any financial institution. The

banks must accept that the major regulatory bodies such as APRA, ASIC and RBA are in the

exclusive position to deal with the antitrust concerns that may prevent the banking company

to incorporate the changes which are in public interest.

The Australian regulations will still continue to remain focused on the corporate governance

requirements for the banking and the other financial sectors. But the introduction of new

capital requirements through the implementation of Basel III capital reforms will strengthen

the banking industry and at the same time will provide the industry with the key challenges.

In spite of the numerous global uncertainties such as delayed implementation of new capital

reforms, APRA and ASIC are closely checking and monitoring the developments that are

going on in the banking industry in today’s era. The Australian regulators have to cope with

the international standards otherwise it would lead to inefficiencies in the banking sector with

increased level of risks. Even after the stricter regulations the banking sectors are

encountering the issues of failures in the compliance requirements, violations of code of

conduct with in the regulatory framework are being reported which requires holistic attention

of the regulatory bodies for Australian Banks (Jeucken, 2010). The bank’s top level

management such as the Board of Directors etc. are required to define the corporate culture

within their banking organisations so as to have a strong compliance framework. Therefore

the Australian regulations needs to be more attentive towards these corporate values and must

make the required rules in such areas. The regulations must also be extended towards the

business strategies formulated and implemented by the Australian banks and the financial

institutions and they should also provide for the interest of banks interests i.e. the banks must

be regulated to not perform anything prejudicial in the public or the customers’ interests.

The new standard on financial institutions are soon to be introduced in near future i.e. 2018

and they will put higher regulatory requirements to be complied with in accordance with the

IFRS 9. Moreover, the new payment platform is also developed collectively by many

financial institutions so that it will lead to detection of fraud done by the banking institutions,

money laundering practices and will manage the liquidity and credit limits of the banks. From

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REGULATION OF AUSTRALIAN BANKS 7

2017 the Australian regulators together with the other international regulatory bodies will

necessitate the collaboration with new participants to deal with requirements of daily margin

maintenance.

Recommendations for future regulation in Australian

Banks

Supervision over regulations

The financial stability cannot be attained only through tight regulations as it also requires

good amount of supervision at a higher level for the same. Regulations cannot be assumed as

the alternative solution of supervision. As supervision has its own importance it must be

considered and the drawback of extremely tight regulations on the banking industry must be

analysed by the regulators. As APRA’s has already been serving the Australian banking

industry with the focus on supervision approach it must be retained further by the regulators

with the implementation of new rules that are agreed upon (Brämer & Gischer, 2012).

Regulations and financial innovation

The innovation that is being carried out in the banking or the financial system over several

years has made it easy for the public to raise funds from banks at flexible loan terms and at

lower interest rates. Innovation has helped the financial systems to maintain the risk involved

in their banking business more efficiently and effectively. However, with such practices of

innovation in their functions and services, it is difficult to frame the regulations for the new

services as it is not very clear in the initial stage as to what the bank products actually are. So

the Australian regulators must consider as to how to deal with the financial innovations

coming up in the banking sector of Australia. However, the supervisor of banking industry

must track the areas of financial innovations to supervise the banking companies to manage

the risks in new areas of service.

Conclusions

It is well demonstrated from the above research that the Australian banks have performed

much better than the banks in the other countries over a period of time. The main reason for

2017 the Australian regulators together with the other international regulatory bodies will

necessitate the collaboration with new participants to deal with requirements of daily margin

maintenance.

Recommendations for future regulation in Australian

Banks

Supervision over regulations

The financial stability cannot be attained only through tight regulations as it also requires

good amount of supervision at a higher level for the same. Regulations cannot be assumed as

the alternative solution of supervision. As supervision has its own importance it must be

considered and the drawback of extremely tight regulations on the banking industry must be

analysed by the regulators. As APRA’s has already been serving the Australian banking

industry with the focus on supervision approach it must be retained further by the regulators

with the implementation of new rules that are agreed upon (Brämer & Gischer, 2012).

Regulations and financial innovation

The innovation that is being carried out in the banking or the financial system over several

years has made it easy for the public to raise funds from banks at flexible loan terms and at

lower interest rates. Innovation has helped the financial systems to maintain the risk involved

in their banking business more efficiently and effectively. However, with such practices of

innovation in their functions and services, it is difficult to frame the regulations for the new

services as it is not very clear in the initial stage as to what the bank products actually are. So

the Australian regulators must consider as to how to deal with the financial innovations

coming up in the banking sector of Australia. However, the supervisor of banking industry

must track the areas of financial innovations to supervise the banking companies to manage

the risks in new areas of service.

Conclusions

It is well demonstrated from the above research that the Australian banks have performed

much better than the banks in the other countries over a period of time. The main reason for

REGULATION OF AUSTRALIAN BANKS 8

the same is the APRA’s strict regulations and supervision for the banking sector in Australia

and also because of the sound economic position of Australian markets. The performance

also indicates Australian bank’s higher standards of operations than that of other countries.

International regulatory bodies along with the major regulators of Australian financial

markets viz. APRA, ASIC and RBA have provided consistent and comprehensive regulatory

frameworks to the financial institutions to adhere on and the Australian banks have responded

to the regulatory requirements in an adequate manner. The regulations imposed by the

governmental authorities have both positive as well as the negative impacts as these are good

enough for the safety and transparency point of view, at the same time the banks tends to lose

their key focus on the operations when they are much concerned about the compliance

requirements.

the same is the APRA’s strict regulations and supervision for the banking sector in Australia

and also because of the sound economic position of Australian markets. The performance

also indicates Australian bank’s higher standards of operations than that of other countries.

International regulatory bodies along with the major regulators of Australian financial

markets viz. APRA, ASIC and RBA have provided consistent and comprehensive regulatory

frameworks to the financial institutions to adhere on and the Australian banks have responded

to the regulatory requirements in an adequate manner. The regulations imposed by the

governmental authorities have both positive as well as the negative impacts as these are good

enough for the safety and transparency point of view, at the same time the banks tends to lose

their key focus on the operations when they are much concerned about the compliance

requirements.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

REGULATION OF AUSTRALIAN BANKS 9

References:

Angelini, P., Clerc, L., Cúrdia, V., Gambacorta, L., Gerali, A., Locarno, A., Motto, R.,

Roeger, W., Van den Heuvel, S. and Vlček, J., 2015. Basel III: Long‐term Impact on

Economic Performance and Fluctuations. The Manchester School, 83(2), pp.217-251.

Bologna, P., 2010. Australian banking system resilience: What should be expected looking

forward? An international perspective.

Brämer, P. and Gischer, H., 2012. Domestic systemically important banks: An indicator-

based measurement approach for the australian banking system. Univ., Faculty of

Economics and Management.

Dollery, B.E., Kortt, M.A. and Grant, B.J., 2013. Funding the future: Financial sustainability

and infrastructure finance in Australian local government.

Eubanks, W.W., 2010. Status of the Basel III Capital Adequacy Accord. DIANE Publishing.

Griffith-Jones, S. and Rodriguez, E. eds., 2016. Cross-conditionality banking regulation and

Third-World debt. Springer.

Jeucken, M., 2010. Sustainable finance and banking: the financial sector and the future of

the planet. Routledge.

Joshi, M., Cahill, D. and Sidhu, J., 2010. Intellectual capital performance in the banking

sector: An assessment of Australian owned banks. Journal of Human Resource Costing &

Accounting, 14(2), pp.151-170.

Singleton, J. and Verhoef, G., 2010. Regulation, deregulation, and internationalisation in

South African and New Zealand banking. Business history, 52(4), pp.536-563.

Uddin, S.S. and Suzuki, Y., 2011. Financial reform, ownership and performance in banking

industry: The case of Bangladesh. International Journal of Business and Management, 6(7),

p.28.

References:

Angelini, P., Clerc, L., Cúrdia, V., Gambacorta, L., Gerali, A., Locarno, A., Motto, R.,

Roeger, W., Van den Heuvel, S. and Vlček, J., 2015. Basel III: Long‐term Impact on

Economic Performance and Fluctuations. The Manchester School, 83(2), pp.217-251.

Bologna, P., 2010. Australian banking system resilience: What should be expected looking

forward? An international perspective.

Brämer, P. and Gischer, H., 2012. Domestic systemically important banks: An indicator-

based measurement approach for the australian banking system. Univ., Faculty of

Economics and Management.

Dollery, B.E., Kortt, M.A. and Grant, B.J., 2013. Funding the future: Financial sustainability

and infrastructure finance in Australian local government.

Eubanks, W.W., 2010. Status of the Basel III Capital Adequacy Accord. DIANE Publishing.

Griffith-Jones, S. and Rodriguez, E. eds., 2016. Cross-conditionality banking regulation and

Third-World debt. Springer.

Jeucken, M., 2010. Sustainable finance and banking: the financial sector and the future of

the planet. Routledge.

Joshi, M., Cahill, D. and Sidhu, J., 2010. Intellectual capital performance in the banking

sector: An assessment of Australian owned banks. Journal of Human Resource Costing &

Accounting, 14(2), pp.151-170.

Singleton, J. and Verhoef, G., 2010. Regulation, deregulation, and internationalisation in

South African and New Zealand banking. Business history, 52(4), pp.536-563.

Uddin, S.S. and Suzuki, Y., 2011. Financial reform, ownership and performance in banking

industry: The case of Bangladesh. International Journal of Business and Management, 6(7),

p.28.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.