Detailed Report: Australian Banking Sector, Challenges, and Solutions

VerifiedAdded on 2020/05/16

|14

|2847

|69

Report

AI Summary

This report provides a comprehensive overview of the Australian banking system. It begins with a historical perspective, tracing the evolution of banking in Australia from its inception in 1817. The report then delves into the significant role the banking sector plays in the Australian economy, highlighting its contributions to employment, small business lending, and government revenue. It examines the regulatory framework, including key legislation like the Banking Act 1959 and the Reserve Bank Act 1959, which govern and oversee the banking sector. The report discusses the various services offered by Australian banks, such as financing, transactional services, risk management, and advisory services. Furthermore, it addresses the challenges faced by the sector, including lower interest rates, regulatory pressures, technological advancements, and the rise of Fin-tech companies. The report concludes by suggesting actions and roles to solve these problems, emphasizing the need for enhanced competition, regulatory adjustments, and adapting to digital banking trends. The role of the banking sector in maintaining inflation is also discussed.

Running Head: Banking Sector of Australia

Australian Banking System

Australian Banking System

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Banking Sector of Australia 1

Executive Summary:

In this report, the system of banking in Australian is being discussed. The banking system in

Australia is in existence since long back. Various banks were established since the year 1817

when the first Australian bank was incorporated. Banking is considered as the integral part of

Australian economy due to its soundness and efficiency. It not only provides finance to the

Australian communities but also contributes to the revenue generation for the country through

its operations. There are various laws that regulate the banking system in Australia. Those

laws are being discussed below. But even after having a successful system of banking, the

banking sector has to face various challenges in the Australian economy and this report

discusses such problems and the actions that must be taken to overcome such problems.

Executive Summary:

In this report, the system of banking in Australian is being discussed. The banking system in

Australia is in existence since long back. Various banks were established since the year 1817

when the first Australian bank was incorporated. Banking is considered as the integral part of

Australian economy due to its soundness and efficiency. It not only provides finance to the

Australian communities but also contributes to the revenue generation for the country through

its operations. There are various laws that regulate the banking system in Australia. Those

laws are being discussed below. But even after having a successful system of banking, the

banking sector has to face various challenges in the Australian economy and this report

discusses such problems and the actions that must be taken to overcome such problems.

Banking Sector of Australia 2

Table of Contents

Executive Summary:...........................................................................................................................1

Introduction..........................................................................................................................................3

History of banking sector......................................................................................................................4

Support of banking system in economy...............................................................................................4

Problems faced by banking sector........................................................................................................5

Action and role to solve problem faced by banking system................................................................6

Australian laws that regulate banking sector.......................................................................................6

Services provided by Australian banking.............................................................................................7

Role of banking sector to maintain inflation........................................................................................8

Conclusion.............................................................................................................................................9

References..........................................................................................................................................10

Table of Contents

Executive Summary:...........................................................................................................................1

Introduction..........................................................................................................................................3

History of banking sector......................................................................................................................4

Support of banking system in economy...............................................................................................4

Problems faced by banking sector........................................................................................................5

Action and role to solve problem faced by banking system................................................................6

Australian laws that regulate banking sector.......................................................................................6

Services provided by Australian banking.............................................................................................7

Role of banking sector to maintain inflation........................................................................................8

Conclusion.............................................................................................................................................9

References..........................................................................................................................................10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Banking Sector of Australia 3

Introduction

Banking is a system which is mainly concerned about the deposit taking and lending of such

deposited funds to the required parties. But the scope of banking function has a wide scope

and it covers several activities. A banking system is one of most significant part of any

economy as it promotes the effective flow of funds for the development of country’s

economy. The financial system i.e. the banking sector of Australia has a record of successful

existence due to the robustness of its functions. It is considered the central part of Australian

economy due to the soundness, safety and efficiency maintained by it in performing its

overall functions. The concept of banking in Australia was recognised long years back after

which the Australian economy has faced various ups and downs in the areas of its financial

system but it has always managed to come up such fluctuations successfully.

Introduction

Banking is a system which is mainly concerned about the deposit taking and lending of such

deposited funds to the required parties. But the scope of banking function has a wide scope

and it covers several activities. A banking system is one of most significant part of any

economy as it promotes the effective flow of funds for the development of country’s

economy. The financial system i.e. the banking sector of Australia has a record of successful

existence due to the robustness of its functions. It is considered the central part of Australian

economy due to the soundness, safety and efficiency maintained by it in performing its

overall functions. The concept of banking in Australia was recognised long years back after

which the Australian economy has faced various ups and downs in the areas of its financial

system but it has always managed to come up such fluctuations successfully.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Banking Sector of Australia 4

History of banking sector:

In year 1817, the first Australian bank was established in Sydney with the name of Bank of

South Wales. The Australian banking sector had to face a financial crisis in 1893 due to the

speculative boom in the property market of Australia in 1880s. The crisis occurred in the time

when there was very less governmental or regulatory control on the banks of Australia and

hence it caused failures of various commercial banks (Hickson & Turner, 2002). Until 1910,

private bank notes and the treasury notes were circulated in Australian economy. However, in

1910 Australian pound was issued as the Australian’s legal tender. Then in year 1911, the

commonwealth bank was established by the federal government of Australia. Along with the

other countries, Australia was also the victim of great depression that occurred in 1930 and

caused a series of bank failures in the country. In response to the 1930’s depression, the

Australian banking was made tightly regulated. It was almost impossible for the banks from

foreign countries to set up their branches in Australia and due to this Australian economy has

lesser banks in comparison to other countries like Hong Kong and US (Merrett, 2002). The

Australian banks were bifurcated between savings and trading banks. Majority of savings

banks were state government owned and their activities were confined to provision of

mortgage loans. Trading banks were typically merchant banks that did not offer services to

general public.

Support of banking system in economy

The efficient and effective system of banking is an integral part of economy of the country.

The banks in Australia have supported the nation in all the good and bad times by positively

contributing to the economic growth and national prosperity. Australian banks have served

the employment to the Australian citizens to a great extent. It has provided around 150000

History of banking sector:

In year 1817, the first Australian bank was established in Sydney with the name of Bank of

South Wales. The Australian banking sector had to face a financial crisis in 1893 due to the

speculative boom in the property market of Australia in 1880s. The crisis occurred in the time

when there was very less governmental or regulatory control on the banks of Australia and

hence it caused failures of various commercial banks (Hickson & Turner, 2002). Until 1910,

private bank notes and the treasury notes were circulated in Australian economy. However, in

1910 Australian pound was issued as the Australian’s legal tender. Then in year 1911, the

commonwealth bank was established by the federal government of Australia. Along with the

other countries, Australia was also the victim of great depression that occurred in 1930 and

caused a series of bank failures in the country. In response to the 1930’s depression, the

Australian banking was made tightly regulated. It was almost impossible for the banks from

foreign countries to set up their branches in Australia and due to this Australian economy has

lesser banks in comparison to other countries like Hong Kong and US (Merrett, 2002). The

Australian banks were bifurcated between savings and trading banks. Majority of savings

banks were state government owned and their activities were confined to provision of

mortgage loans. Trading banks were typically merchant banks that did not offer services to

general public.

Support of banking system in economy

The efficient and effective system of banking is an integral part of economy of the country.

The banks in Australia have supported the nation in all the good and bad times by positively

contributing to the economic growth and national prosperity. Australian banks have served

the employment to the Australian citizens to a great extent. It has provided around 150000

Banking Sector of Australia 5

jobs in the Australian nation

(ABA’s Economic report, 2015). The country’s banks provide loans of around 1 million to

the small businesses for their growth and development. As the Australian banks have sound

capital blocking and also sophisticated safeguards against frauds and other crimes, they

support the household savings of countries citizens. These banks contribute significantly to

the revenue of the government which in turn helps in the overall development of the

country’s economy. In year 2014 banking sector had made the tax payment of around $13.7

billion to the government. Banking industry is the largest service industry in respect of

economic contribution and is contributing almost equal to 9.3% to the GDP of country as the

finance industry has contributed $138.6 billion in 2015 to the economy of Australia

(Kirkwood & Nahm, 2006). The overall banking system of banking offers a wide gamut of

financial services and products to all customer segments such as personal lending, general

insurance, financial advice and credit card facilities etc. so that the customers can arrange

deploy their the funds in the best possible manner.

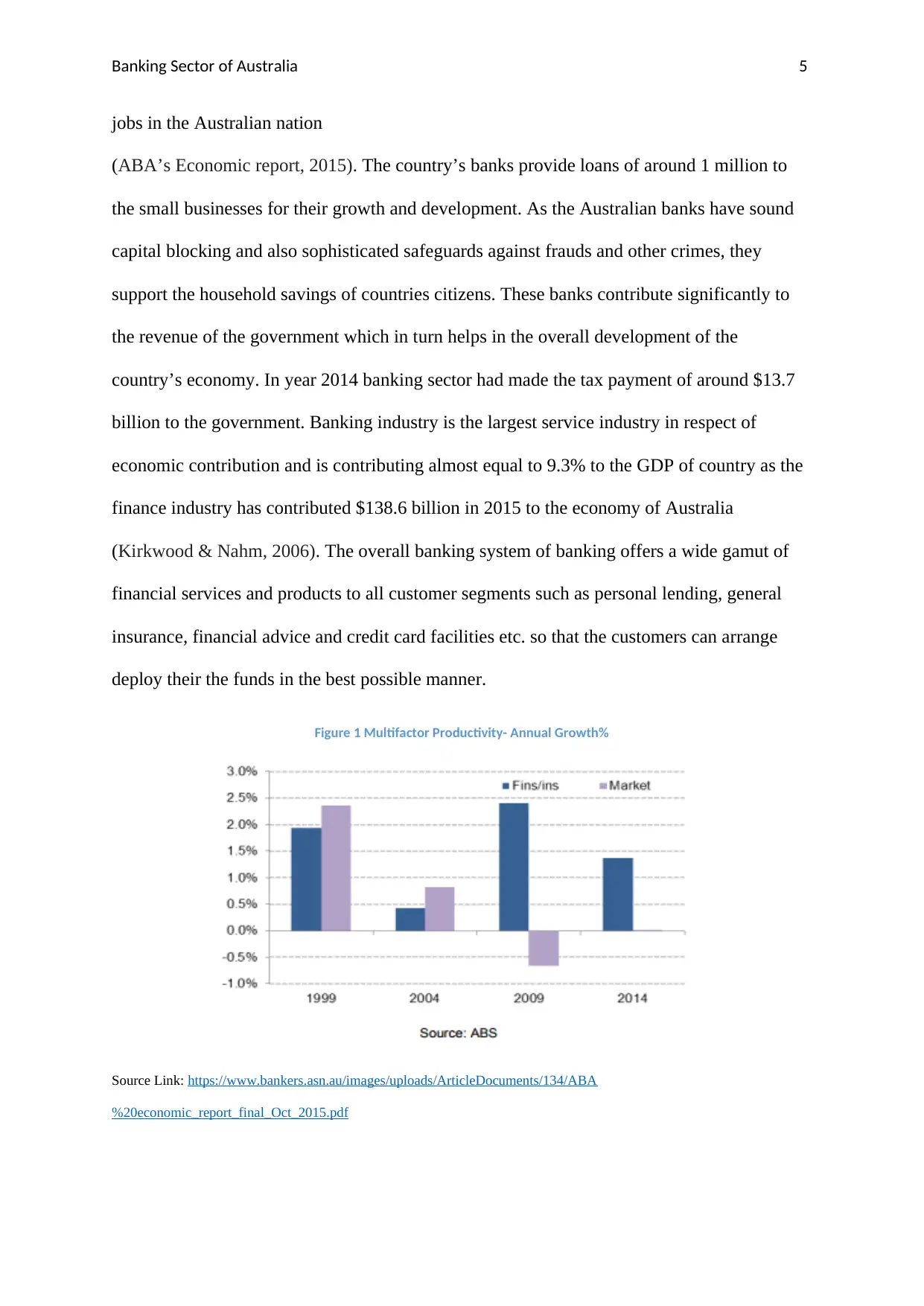

Figure 1 Multifactor Productivity- Annual Growth%

Source Link: https://www.bankers.asn.au/images/uploads/ArticleDocuments/134/ABA

%20economic_report_final_Oct_2015.pdf

jobs in the Australian nation

(ABA’s Economic report, 2015). The country’s banks provide loans of around 1 million to

the small businesses for their growth and development. As the Australian banks have sound

capital blocking and also sophisticated safeguards against frauds and other crimes, they

support the household savings of countries citizens. These banks contribute significantly to

the revenue of the government which in turn helps in the overall development of the

country’s economy. In year 2014 banking sector had made the tax payment of around $13.7

billion to the government. Banking industry is the largest service industry in respect of

economic contribution and is contributing almost equal to 9.3% to the GDP of country as the

finance industry has contributed $138.6 billion in 2015 to the economy of Australia

(Kirkwood & Nahm, 2006). The overall banking system of banking offers a wide gamut of

financial services and products to all customer segments such as personal lending, general

insurance, financial advice and credit card facilities etc. so that the customers can arrange

deploy their the funds in the best possible manner.

Figure 1 Multifactor Productivity- Annual Growth%

Source Link: https://www.bankers.asn.au/images/uploads/ArticleDocuments/134/ABA

%20economic_report_final_Oct_2015.pdf

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Banking Sector of Australia 6

This shows the improvement in the bank’s productivity in areas of labour and capital

utilisation and hence it can be said that banks are contributing positively to the growth of

economy since last many years.

Figure 2: Banks’ interest paid ($bn)

Source Link: https://www.bankers.asn.au/images/uploads/ArticleDocuments/134/ABA

%20economic_report_final_Oct_2015.pdf

The above figure shows that the retails banks are paying considerable interest to the account

holders on term and savings deposits etc. which becomes the part of their income from other

sources.

Problems faced by banking sector:

Though the banking system of Australia is quite strong and safe, it has to face some

challenges in the post period of global financial crisis (Sathye, 2001). The banks have to face

longer periods of lower rates of interests. The profitability of the banks is deeply pressurised

due to the lower interest rates and weakens the operating environment. These lower interest

rates also exert pressure on rise in housing prices (Australian Government, 2015). The

sensitivity of bank towards housing market shocks has been increased since 2008 as longer

This shows the improvement in the bank’s productivity in areas of labour and capital

utilisation and hence it can be said that banks are contributing positively to the growth of

economy since last many years.

Figure 2: Banks’ interest paid ($bn)

Source Link: https://www.bankers.asn.au/images/uploads/ArticleDocuments/134/ABA

%20economic_report_final_Oct_2015.pdf

The above figure shows that the retails banks are paying considerable interest to the account

holders on term and savings deposits etc. which becomes the part of their income from other

sources.

Problems faced by banking sector:

Though the banking system of Australia is quite strong and safe, it has to face some

challenges in the post period of global financial crisis (Sathye, 2001). The banks have to face

longer periods of lower rates of interests. The profitability of the banks is deeply pressurised

due to the lower interest rates and weakens the operating environment. These lower interest

rates also exert pressure on rise in housing prices (Australian Government, 2015). The

sensitivity of bank towards housing market shocks has been increased since 2008 as longer

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Banking Sector of Australia 7

period of lower interest rates can cause more credit flow to housing market. After the global

financial crisis, there have been imposed heavy regulatory reforms on the banking sector

which creates pressure on the banks and thereby causes them to underperform. Due to the

technological advancements, the customers of the banks are abandoning the use of traditional

banking services and relying on the online services and banks fails to offer them the desired

services (Joseph, McClure & Joseph, 1999). Also increasing introduction of Fin-tech

companies which are providing financial services with the use of software is causing heavy

competitive pressure on the banking sector. Therefore, the banks are pressurised to adopt the

environment of digital banking (Lichtenstein & Williamson, 2006). Moreover, for every

banking institution operating in the market, data held by it is of significant importance

whereas in the case of digital banking, the financial data maintained by them is prone to

various risk exposures such as data loss, data manipulation etc.

Action and role to solve problem faced by

banking system

The competitive pressures must be enhanced in the banking industry to increase the

efficiency in the market. But such competition must be kept balanced with maintaining

stability. The pressure from the Governmental bodies in the form of various reforms must be

released. To enhance the accountability and increasing the independence of banking sectors

some areas are to be improved. The regulatory perimeters need to be changed in Australia to

cope up with the changes in the economic environment of economic system. The

superannuation assets have been expanded rapidly

period of lower interest rates can cause more credit flow to housing market. After the global

financial crisis, there have been imposed heavy regulatory reforms on the banking sector

which creates pressure on the banks and thereby causes them to underperform. Due to the

technological advancements, the customers of the banks are abandoning the use of traditional

banking services and relying on the online services and banks fails to offer them the desired

services (Joseph, McClure & Joseph, 1999). Also increasing introduction of Fin-tech

companies which are providing financial services with the use of software is causing heavy

competitive pressure on the banking sector. Therefore, the banks are pressurised to adopt the

environment of digital banking (Lichtenstein & Williamson, 2006). Moreover, for every

banking institution operating in the market, data held by it is of significant importance

whereas in the case of digital banking, the financial data maintained by them is prone to

various risk exposures such as data loss, data manipulation etc.

Action and role to solve problem faced by

banking system

The competitive pressures must be enhanced in the banking industry to increase the

efficiency in the market. But such competition must be kept balanced with maintaining

stability. The pressure from the Governmental bodies in the form of various reforms must be

released. To enhance the accountability and increasing the independence of banking sectors

some areas are to be improved. The regulatory perimeters need to be changed in Australia to

cope up with the changes in the economic environment of economic system. The

superannuation assets have been expanded rapidly

Banking Sector of Australia 8

Australian laws that regulate banking sector

The prime acts that regulates the banking institutions such as banks incorporated in Australia,

representative offices set up in Australia and branches of various foreign banks, specialised

credit institutions or unions and the building societies of Australia are regulated by following

laws:

Banking Act 1959: All the banking companies incorporated in Australia, are controlled and

regulated by the banking act.

Reserve bank act, 1959: The reserve bank of Australia is regulated by the reserve bank act.

The said act gives specific powers and obligations to the reserve bank (Bade & Parkin, 1988).

Corporations act, 2001: This act is a principle legislation that sets out regulations and laws

that applies on Australian business entities at both federal as well as interstate level. It mainly

emphasises on the corporate bodies but also entails some laws applicable on partnership

firms.

Financial Sector Act, 2001 (Collection of data act): This act was commenced in 2001 and it

vested the responsibility of registration of Australian financial corporations to the Australian

Prudential Regulatory body. However, it does not give powers to APRA to oversee the

activities of registered financial incorporations. The act is meant to primarily facilitate the

statistical data collection.

Financial Sector act, 2001 (Shareholdings): This act is applicable on the financial sector

companies which are subject to the limit of 15% shareholding. It majorly deals with the

acquisition of shares by persons in the company.

Services provided by Australian banking:

Australian laws that regulate banking sector

The prime acts that regulates the banking institutions such as banks incorporated in Australia,

representative offices set up in Australia and branches of various foreign banks, specialised

credit institutions or unions and the building societies of Australia are regulated by following

laws:

Banking Act 1959: All the banking companies incorporated in Australia, are controlled and

regulated by the banking act.

Reserve bank act, 1959: The reserve bank of Australia is regulated by the reserve bank act.

The said act gives specific powers and obligations to the reserve bank (Bade & Parkin, 1988).

Corporations act, 2001: This act is a principle legislation that sets out regulations and laws

that applies on Australian business entities at both federal as well as interstate level. It mainly

emphasises on the corporate bodies but also entails some laws applicable on partnership

firms.

Financial Sector Act, 2001 (Collection of data act): This act was commenced in 2001 and it

vested the responsibility of registration of Australian financial corporations to the Australian

Prudential Regulatory body. However, it does not give powers to APRA to oversee the

activities of registered financial incorporations. The act is meant to primarily facilitate the

statistical data collection.

Financial Sector act, 2001 (Shareholdings): This act is applicable on the financial sector

companies which are subject to the limit of 15% shareholding. It majorly deals with the

acquisition of shares by persons in the company.

Services provided by Australian banking:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Banking Sector of Australia 9

The banking sector of Australia provides a wide range of services:

Financing and investing activities: The banks in Australia provide finances to the business

entities to expand and develop their businesses. These banks also facilitate deposits of the

surplus funds or savings of the business entities or individuals so that returns can be

generated on such deposits (Reserve Bank of Australia, 2018).

Transactional services: Banks also performs various collection services for their clients under

which the banking organisations collects payments from the debtors of their clients directly to

their banks accounts and intimates them on time to time basis about the collection process.

They also manages the payment mechanism of their clients through the modes of cheques,

direct transfers or through electronic fund transfer schemes.

Risk management services: Australian banks provides solutions to safeguard the Australian

business entities against the currency fluctuation and also the movements in interest and

commodity rates.

Superannuation and insurance: The Australian banking sector provides superannuation

services and it also provides insurance services to the clients.

Advisory services: The banks provide advices on financial investments and protection from

various financial risks and they also provide advices to corporate on potential mergers and

acquisitions and capital markets etc. (Australia and New Zealand Banking Group Limited

2015).

The banks also issue credit or debit cards to their customers and then performs processing of

electronic debit and credit card transaction their behalf.

These banks also facilitate the maintenance of foreign exchange reserves so that the

customers can buy the foreign exchange to enter into foreign transactions.

The banking sector of Australia provides a wide range of services:

Financing and investing activities: The banks in Australia provide finances to the business

entities to expand and develop their businesses. These banks also facilitate deposits of the

surplus funds or savings of the business entities or individuals so that returns can be

generated on such deposits (Reserve Bank of Australia, 2018).

Transactional services: Banks also performs various collection services for their clients under

which the banking organisations collects payments from the debtors of their clients directly to

their banks accounts and intimates them on time to time basis about the collection process.

They also manages the payment mechanism of their clients through the modes of cheques,

direct transfers or through electronic fund transfer schemes.

Risk management services: Australian banks provides solutions to safeguard the Australian

business entities against the currency fluctuation and also the movements in interest and

commodity rates.

Superannuation and insurance: The Australian banking sector provides superannuation

services and it also provides insurance services to the clients.

Advisory services: The banks provide advices on financial investments and protection from

various financial risks and they also provide advices to corporate on potential mergers and

acquisitions and capital markets etc. (Australia and New Zealand Banking Group Limited

2015).

The banks also issue credit or debit cards to their customers and then performs processing of

electronic debit and credit card transaction their behalf.

These banks also facilitate the maintenance of foreign exchange reserves so that the

customers can buy the foreign exchange to enter into foreign transactions.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Banking Sector of Australia

10

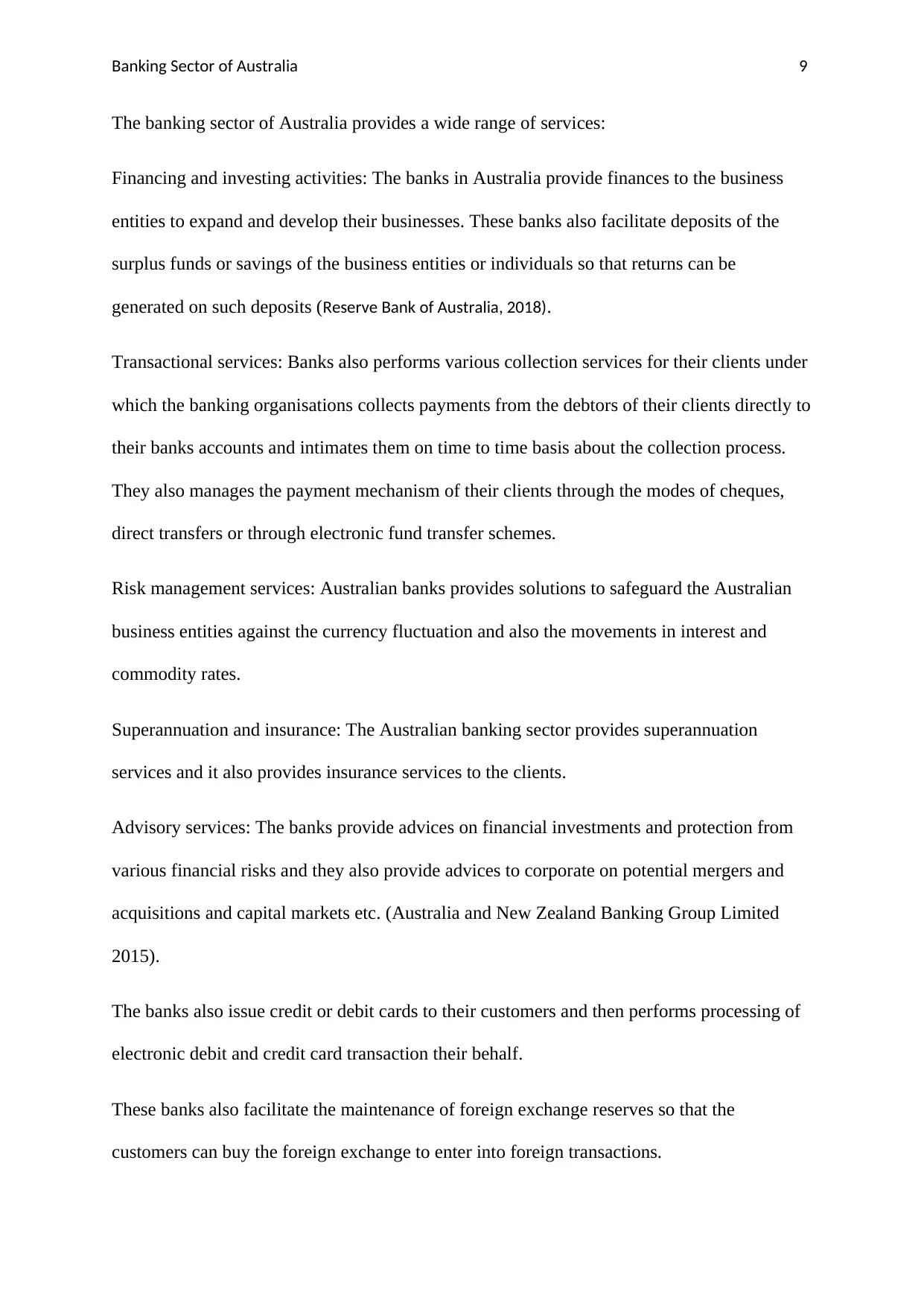

Figure 3: Products on market

Source Link: https://www.bankers.asn.au/images/uploads/ArticleDocuments/134/ABA

%20economic_report_final_Oct_2015.pdf

The above figure shows that banks are providing maximum proportion of financial services

to the customers than other bodies such as unions and building societies (CUBS) or non-

authorised deposit-taking institutions (non-ADIs)

Role of banking sector to maintain inflation:

Inflation is the economic situation in which the prices of goods and services increase over a

period of time. The price instability can lead to severe instability in the overall financial

system of the country. The financial shocks due to inflation can adversely affect the economy

of the country. A weak financial system can make it difficult for the economy to achieve

growth and pursue its objective of price stability. The financial system especially the banking

sector has undergone significant changes to influence the system’s efficiency and stability

(Debelle, 1996). The financial system’s stability is well- established responsibility of Reserve

Bank. In fulfilling the overall responsibility, Reserve bank has a vital role to play in reducing

the risk of financial disruptions and in responding to the situations of financial disturbance

due to the extreme inflationary forces. The reserve banks of Australia continuously formulate

and monitor various monetary policies to maintain the inflation in the country. The RBA

communicates its views with the relevant agencies. A forum called Council of Financial

10

Figure 3: Products on market

Source Link: https://www.bankers.asn.au/images/uploads/ArticleDocuments/134/ABA

%20economic_report_final_Oct_2015.pdf

The above figure shows that banks are providing maximum proportion of financial services

to the customers than other bodies such as unions and building societies (CUBS) or non-

authorised deposit-taking institutions (non-ADIs)

Role of banking sector to maintain inflation:

Inflation is the economic situation in which the prices of goods and services increase over a

period of time. The price instability can lead to severe instability in the overall financial

system of the country. The financial shocks due to inflation can adversely affect the economy

of the country. A weak financial system can make it difficult for the economy to achieve

growth and pursue its objective of price stability. The financial system especially the banking

sector has undergone significant changes to influence the system’s efficiency and stability

(Debelle, 1996). The financial system’s stability is well- established responsibility of Reserve

Bank. In fulfilling the overall responsibility, Reserve bank has a vital role to play in reducing

the risk of financial disruptions and in responding to the situations of financial disturbance

due to the extreme inflationary forces. The reserve banks of Australia continuously formulate

and monitor various monetary policies to maintain the inflation in the country. The RBA

communicates its views with the relevant agencies. A forum called Council of Financial

Banking Sector of Australia

11

Regulators has been formed to maintain financial stability in the system. The CFR takes

together the reserve bank, APRA and ASIC to contribute to the effectiveness of stability of

financial system by stabilising the inflation in the country (Reserve Bank of Australia, 2018).

Conclusion

Therefore, it can be concluded that banking sector plays significant role in the economic

development of the Australia. The financial system is also found to be quite stable and sound

to nurture the growth of the economy. Its role in the economic development of the country is

significant. However, even after the efficient functioning and performance, the banking

sector of the country has to face various challenges due to the digitisation and modernisation

in the economy. These challenges need to be overcome to strengthen the economy of

Australia. The Australian must make efforts to reduce the challenges faced by the finance

sector by lessening the overall burden of fiscal reforms on the banking sector. It must make

the banking system more independent and transparent to generate the trust of Australian

community in the banking sector.

11

Regulators has been formed to maintain financial stability in the system. The CFR takes

together the reserve bank, APRA and ASIC to contribute to the effectiveness of stability of

financial system by stabilising the inflation in the country (Reserve Bank of Australia, 2018).

Conclusion

Therefore, it can be concluded that banking sector plays significant role in the economic

development of the Australia. The financial system is also found to be quite stable and sound

to nurture the growth of the economy. Its role in the economic development of the country is

significant. However, even after the efficient functioning and performance, the banking

sector of the country has to face various challenges due to the digitisation and modernisation

in the economy. These challenges need to be overcome to strengthen the economy of

Australia. The Australian must make efforts to reduce the challenges faced by the finance

sector by lessening the overall burden of fiscal reforms on the banking sector. It must make

the banking system more independent and transparent to generate the trust of Australian

community in the banking sector.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.