Taxation Law Assignment: Deductions, Credits, and Assessable Income

VerifiedAdded on 2020/02/19

|11

|2906

|83

Homework Assignment

AI Summary

This taxation law assignment solution addresses several key issues in Australian tax law. Answer 1 examines whether various expenses, such as moving machinery costs, asset revaluation expenses, and legal costs related to business wind-up, are deductible under section 8-1 of the ITAA 1997, referencing relevant case law. Answer 2 focuses on whether Big Bank can claim input tax credits for advertising expenses, considering GST implications and relevant legislation. Answer 3 involves the computation of assessable income, including employment, rental, dividend, and interest income from both Australian and international sources, along with the deduction of various expenses. The solution provides detailed analysis and application of relevant tax laws and regulations.

TAXATION LAW

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Taxation law

Answer 1

Issue

Whether the following elements are allowed as deductions under section 8-1 of ITAA 1997?

According to section 8-1 of ITAA 1997, deductible expenses are of two kinds; firstly, the one which is incurred

while earning the measurable income, and secondly, incurred on continuing the business from which the

measurable capital is earned. Expelling of the expenses are only done for the ones which are not private/domestic,

capital in nature also including the ones which are in association to the earning of the not liable income (Pratt &

Kulsrud, 2013).

Application

The cost of moving machinery to a new site

It is to be noted that the expense required to purchase a new machine and to shift it from the purchasing site

to the required destination is capital in nature. This is because the shifting charge is also included in the

buying cost and termed as the capital cost of machinery purchasing. This type of capital coat is never taken

into consideration as per the 8-1 section of ITAA and is not treated as deductible expenses. The expenses

spent on the machinery shall always be summed up with the capital cost on the basis that it is old

machinery or new machinery (Gilders & Walpole, 2016). For instance, if the machinery is new then the

total costs spent on it till date shall be added to the capital cost and termed as the capital of the asset. Other

expenses include transportation expenses and commissioning expenses. But considering the cost of

transportation of the old machinery to a new destination, then the particular expense can be defined as a

deductible expense. It was held in the case of W Neville & Co v FCT (1937) that expenses those connected

with a business purpose must be allowed as deduction.

The cost of revaluing assets to effect insurance cover

The amount spends in the revaluing the property of the company so as to claim release is only

accepted if the received amount is used for regenerating the loss of income which is wholly or

partially related to the assessable income of the company. Insurances can be claimed by the

company only upon the rise of two cases. Firstly, if the insurance has been claimed for some

machinery that has been capital in nature, and now has been destroyed by some risen situations. In

this, the claim has been made to recover the machinery loss (Fullerton et. al, 2017). It shall be

2

Answer 1

Issue

Whether the following elements are allowed as deductions under section 8-1 of ITAA 1997?

According to section 8-1 of ITAA 1997, deductible expenses are of two kinds; firstly, the one which is incurred

while earning the measurable income, and secondly, incurred on continuing the business from which the

measurable capital is earned. Expelling of the expenses are only done for the ones which are not private/domestic,

capital in nature also including the ones which are in association to the earning of the not liable income (Pratt &

Kulsrud, 2013).

Application

The cost of moving machinery to a new site

It is to be noted that the expense required to purchase a new machine and to shift it from the purchasing site

to the required destination is capital in nature. This is because the shifting charge is also included in the

buying cost and termed as the capital cost of machinery purchasing. This type of capital coat is never taken

into consideration as per the 8-1 section of ITAA and is not treated as deductible expenses. The expenses

spent on the machinery shall always be summed up with the capital cost on the basis that it is old

machinery or new machinery (Gilders & Walpole, 2016). For instance, if the machinery is new then the

total costs spent on it till date shall be added to the capital cost and termed as the capital of the asset. Other

expenses include transportation expenses and commissioning expenses. But considering the cost of

transportation of the old machinery to a new destination, then the particular expense can be defined as a

deductible expense. It was held in the case of W Neville & Co v FCT (1937) that expenses those connected

with a business purpose must be allowed as deduction.

The cost of revaluing assets to effect insurance cover

The amount spends in the revaluing the property of the company so as to claim release is only

accepted if the received amount is used for regenerating the loss of income which is wholly or

partially related to the assessable income of the company. Insurances can be claimed by the

company only upon the rise of two cases. Firstly, if the insurance has been claimed for some

machinery that has been capital in nature, and now has been destroyed by some risen situations. In

this, the claim has been made to recover the machinery loss (Fullerton et. al, 2017). It shall be

2

Taxation law

very obvious in this case that the insurance money provided can only be used in the recovery of

the loss and in no case can be shown in the income statements of the company’s business.

According to the second way, if the claims are made for the asset loss which has been shown as

stocks in trade then, these assets are directly taken into account as for the business and related to

the assessable income because they are not capital in nature. All this is obviously done to provide

profits to the business and so are termed as business expenses. But all these expenses should be

recorded in the profit and loss accounts of the company and used for the recovery of the lost assets

(Fullerton et. 2017).

Thus, if the revaluing of the assets is done then the expenses claimed are allowable as per the

section 8-1 of the ITAA 1997. It was held in the case of Charles Moore & Co (WA) P/L v FC of

T (1956) that financial transactions that form a part of the business activities must be deductible.

According to section 8-1 of ITAA 1997, deductible expenses are of two kinds; firstly, the one which is

incurred while earning the measurable income, and secondly, incurred on continuing the business from

which the measurable capital is earned. Expelling of the expenses are only done for the ones which are not

private/domestic, capital in nature also including the ones which are in association to the earning of the not

liable income (Gilders & Walpole, 2016).

So according to the given case, if it is taken into account with the s 8-1 then, the costs claimed by the

company with an unfavorable decision for the winding up is not in association with the s 8-1. This situation

arises because the claims put up are neither for earning assessable income and neither to continue the

business for earning the assessable income. The total cost paid by the company should be checked

regularly so as to not let it turn into big numbers because it will not be treated as the money spent on the

company’s business. It was held by the Federal court in the case of FC of T v Cooper (1991) that the

expenses incurred by the tax payer to carry on the operations and in the normal course of business must be

considered as a deduction.

But the expense shown in the case is a legal cost which has been claimed for the continuance of the

business so as to earn the assessable income and thus this type of cost is perfectly allowed to be claimed as

per the section 25-5.

According to section 8-1 of ITAA 1997, deductible expenses are of two kinds; firstly, the one which is

incurred while earning the measurable income, and secondly, incurred on continuing the business from

which the measurable capital is earned. Expelling of the expenses are only done for the ones which are not

3

very obvious in this case that the insurance money provided can only be used in the recovery of

the loss and in no case can be shown in the income statements of the company’s business.

According to the second way, if the claims are made for the asset loss which has been shown as

stocks in trade then, these assets are directly taken into account as for the business and related to

the assessable income because they are not capital in nature. All this is obviously done to provide

profits to the business and so are termed as business expenses. But all these expenses should be

recorded in the profit and loss accounts of the company and used for the recovery of the lost assets

(Fullerton et. 2017).

Thus, if the revaluing of the assets is done then the expenses claimed are allowable as per the

section 8-1 of the ITAA 1997. It was held in the case of Charles Moore & Co (WA) P/L v FC of

T (1956) that financial transactions that form a part of the business activities must be deductible.

According to section 8-1 of ITAA 1997, deductible expenses are of two kinds; firstly, the one which is

incurred while earning the measurable income, and secondly, incurred on continuing the business from

which the measurable capital is earned. Expelling of the expenses are only done for the ones which are not

private/domestic, capital in nature also including the ones which are in association to the earning of the not

liable income (Gilders & Walpole, 2016).

So according to the given case, if it is taken into account with the s 8-1 then, the costs claimed by the

company with an unfavorable decision for the winding up is not in association with the s 8-1. This situation

arises because the claims put up are neither for earning assessable income and neither to continue the

business for earning the assessable income. The total cost paid by the company should be checked

regularly so as to not let it turn into big numbers because it will not be treated as the money spent on the

company’s business. It was held by the Federal court in the case of FC of T v Cooper (1991) that the

expenses incurred by the tax payer to carry on the operations and in the normal course of business must be

considered as a deduction.

But the expense shown in the case is a legal cost which has been claimed for the continuance of the

business so as to earn the assessable income and thus this type of cost is perfectly allowed to be claimed as

per the section 25-5.

According to section 8-1 of ITAA 1997, deductible expenses are of two kinds; firstly, the one which is

incurred while earning the measurable income, and secondly, incurred on continuing the business from

which the measurable capital is earned. Expelling of the expenses are only done for the ones which are not

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Taxation law

private/domestic, capital in nature also including the ones which are in association to the earning of the

nonliable income (Kobestky, 2005).

In the explained matter it is very clear that all the expenses claimed in the case are not at all subjected to

any category wise division. There is no expense separately tagged as private or revenue or any other. All

the claimed costs are just defined as for business purposes only. Also, the claimed expenses have been

shown as an effort to recover the capital which is a portion of the assessable income. It was held in the case

of W Neville & Co v FCT (1937) that expenses related to business activity would appear in the deductible

expenses. It is also seen that if the expenses are categorized than the legal costs for the mortgaging purpose

would obviously appear to be out of the section 8-1 because of its capital nature and would not be part of

the deductible expenses while the other ones would surely be included.

Conclusion

From the above discussion, it is clear that for expenses to be considered as an allowable expense it must

have a direct bearing on the business activity and must be done in the business course. There are various

expenses that are incurred while conducting the business and the above situation clearly stresses that there

must be an establishment with the business activities. The ones that do not fall under the ambit of the

business activity is altogether ignored.

.

4

private/domestic, capital in nature also including the ones which are in association to the earning of the

nonliable income (Kobestky, 2005).

In the explained matter it is very clear that all the expenses claimed in the case are not at all subjected to

any category wise division. There is no expense separately tagged as private or revenue or any other. All

the claimed costs are just defined as for business purposes only. Also, the claimed expenses have been

shown as an effort to recover the capital which is a portion of the assessable income. It was held in the case

of W Neville & Co v FCT (1937) that expenses related to business activity would appear in the deductible

expenses. It is also seen that if the expenses are categorized than the legal costs for the mortgaging purpose

would obviously appear to be out of the section 8-1 because of its capital nature and would not be part of

the deductible expenses while the other ones would surely be included.

Conclusion

From the above discussion, it is clear that for expenses to be considered as an allowable expense it must

have a direct bearing on the business activity and must be done in the business course. There are various

expenses that are incurred while conducting the business and the above situation clearly stresses that there

must be an establishment with the business activities. The ones that do not fall under the ambit of the

business activity is altogether ignored.

.

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Taxation law

Answer-2

Issue

Will Big Bank be able to claim the input tax credits in tune to the advertisement expenses that are incurred amount

to $1,650,000?

Rule

The Big Bank Ltd is a national level insurance company which is GST registered and has over 50 branches, a 10-

storey office, and various call centers to communicate with its customers. For a long time, the company has been

facilitating its customers with its services in Australia. The launch of the home and contents policies by the

company is a crucial step in expanding its business but the company is willing to install a new accounting system

as the company is now GST registered and from now on the amounts collected by premium policies will be GST

charged (Kenny et. al, 2017). So for undertaking this idea promotion has to be done. A similar instance was

observed in the case of Rio Tinto Services Ltd v Commissioner of Taxation [2015] FCA 94 where the federal court

came to a conclusion that the taxpayer would not be able to input tax credits on acquisitions that are in tune to the

input tax supplies a GST supplies. If a direct link has been established then the acquisition is defined as partly

creditable.

A thorough decision on the part of the company has been taken to expand its business through the medium of

advertising so as to begin its era into the insurance field with a bang. Printing media, television, radio are some of

the base methods adopted by the company to advertise its business (Khadem, 2017).

The Big Bank Ltd was ready and spent a huge amount of $16,50,000 for the advertising purposes only. This

massive amount spent includes $5,50,000 for only promoting the newly launched product of the company. The

remaining amount left was spent in advertising for the facilities that the company already had from before. The

promotional advisor proposed a tax invoice of $16,50,000 to the company. As the company is GST registered so

the Big Bank Ltd is allowed to enjoy the profits earned as per the GST credits provided if it is claimed (Nethercott

et. al, 2013).

Application

The Big Bank Ltd is able to enjoy the GST credits on the advertising tax credit because the amount spent by them

is taken into consideration as business expenses and can be used only for business purposes. This expense made by

the company cannot be treated as capital in nature because it is not long-lasting and has to be proposed time to time

5

Answer-2

Issue

Will Big Bank be able to claim the input tax credits in tune to the advertisement expenses that are incurred amount

to $1,650,000?

Rule

The Big Bank Ltd is a national level insurance company which is GST registered and has over 50 branches, a 10-

storey office, and various call centers to communicate with its customers. For a long time, the company has been

facilitating its customers with its services in Australia. The launch of the home and contents policies by the

company is a crucial step in expanding its business but the company is willing to install a new accounting system

as the company is now GST registered and from now on the amounts collected by premium policies will be GST

charged (Kenny et. al, 2017). So for undertaking this idea promotion has to be done. A similar instance was

observed in the case of Rio Tinto Services Ltd v Commissioner of Taxation [2015] FCA 94 where the federal court

came to a conclusion that the taxpayer would not be able to input tax credits on acquisitions that are in tune to the

input tax supplies a GST supplies. If a direct link has been established then the acquisition is defined as partly

creditable.

A thorough decision on the part of the company has been taken to expand its business through the medium of

advertising so as to begin its era into the insurance field with a bang. Printing media, television, radio are some of

the base methods adopted by the company to advertise its business (Khadem, 2017).

The Big Bank Ltd was ready and spent a huge amount of $16,50,000 for the advertising purposes only. This

massive amount spent includes $5,50,000 for only promoting the newly launched product of the company. The

remaining amount left was spent in advertising for the facilities that the company already had from before. The

promotional advisor proposed a tax invoice of $16,50,000 to the company. As the company is GST registered so

the Big Bank Ltd is allowed to enjoy the profits earned as per the GST credits provided if it is claimed (Nethercott

et. al, 2013).

Application

The Big Bank Ltd is able to enjoy the GST credits on the advertising tax credit because the amount spent by them

is taken into consideration as business expenses and can be used only for business purposes. This expense made by

the company cannot be treated as capital in nature because it is not long-lasting and has to be proposed time to time

5

Taxation law

and so it is wise to summon them up together and depict them as a positive feature of the company. Whenever the

company makes any transaction in association with the expense for the principles of the company, and if this made

transaction includes GST then in such cases the company has the full power to exercise control on the credits of

the GST as the company paid for it (Barcokzy, 2010). This type of credits enjoyed is termed as GST credits or

input tax credits.

As stated by Sadiq et. al (2017) GST can be claimed as per the following conditions:

The expenses incurred for the purchase of goods and supplies are for the purpose of business and not for

personal use.

The price at which the items or supplies are purchased includes GST.

A consideration is to be paid for the purchasing of items or supplies.

The items or supplies provider has proposed a tax invoice for the meticulous possessions or supplies and

that includes GST.

Conclusion

No matter the amount spent is massive but it all finally comes under the portion of advertising for which the

company has paid GST. The tax invoice of $16,50,000 comprised of the television advertisement worth of

$5.50.000 and the left over the amount for other promotional mediums. All this will help in expanding the business

while it is only 2% of the company’s capital and the remaining 98% is fulfilled through the loans given and the

deposits made by the company’s costumes for which commission and interest rates are charged. All this makes the

company fully eligible to claim the GST credits as per the received advertising bill.

6

and so it is wise to summon them up together and depict them as a positive feature of the company. Whenever the

company makes any transaction in association with the expense for the principles of the company, and if this made

transaction includes GST then in such cases the company has the full power to exercise control on the credits of

the GST as the company paid for it (Barcokzy, 2010). This type of credits enjoyed is termed as GST credits or

input tax credits.

As stated by Sadiq et. al (2017) GST can be claimed as per the following conditions:

The expenses incurred for the purchase of goods and supplies are for the purpose of business and not for

personal use.

The price at which the items or supplies are purchased includes GST.

A consideration is to be paid for the purchasing of items or supplies.

The items or supplies provider has proposed a tax invoice for the meticulous possessions or supplies and

that includes GST.

Conclusion

No matter the amount spent is massive but it all finally comes under the portion of advertising for which the

company has paid GST. The tax invoice of $16,50,000 comprised of the television advertisement worth of

$5.50.000 and the left over the amount for other promotional mediums. All this will help in expanding the business

while it is only 2% of the company’s capital and the remaining 98% is fulfilled through the loans given and the

deposits made by the company’s costumes for which commission and interest rates are charged. All this makes the

company fully eligible to claim the GST credits as per the received advertising bill.

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Taxation law

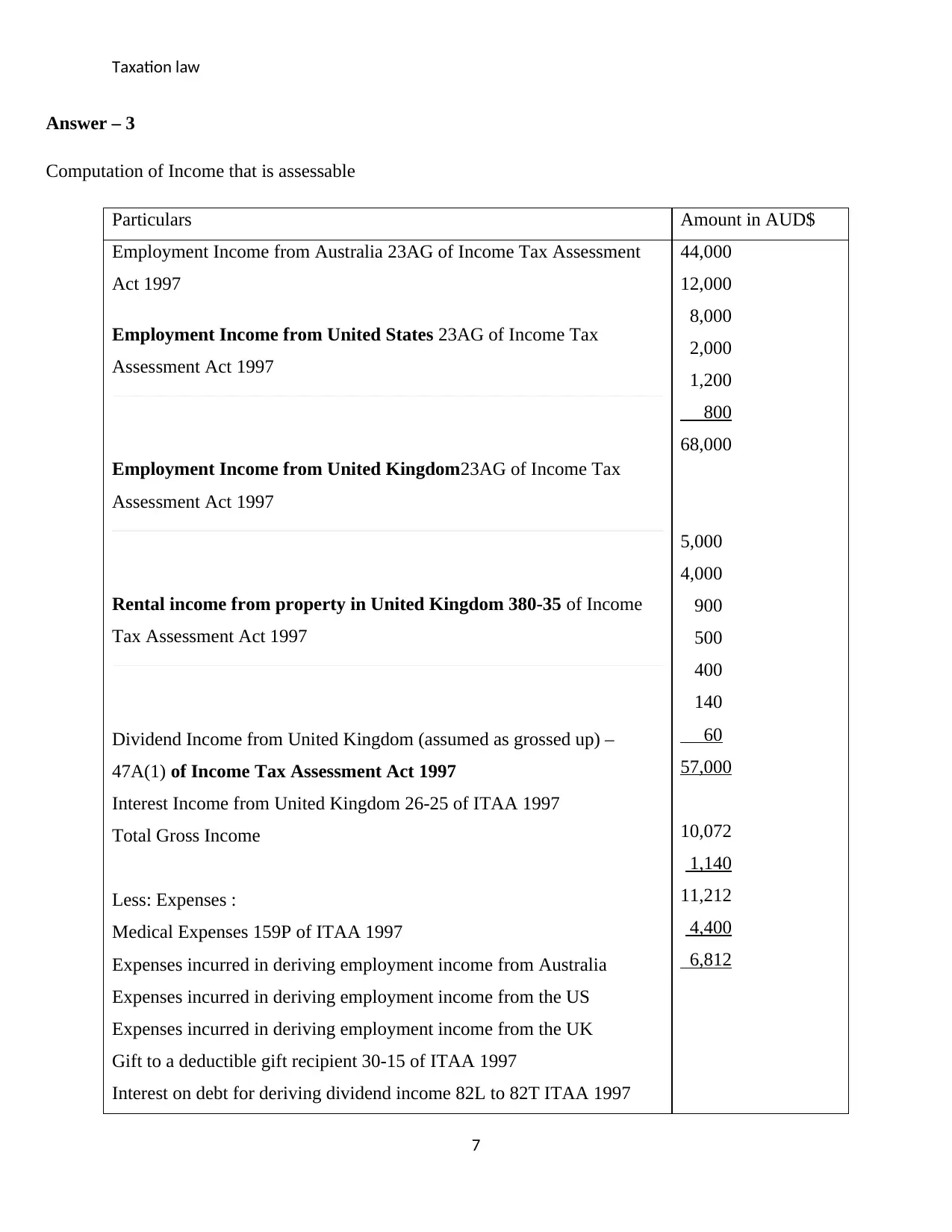

Answer – 3

Computation of Income that is assessable

Particulars Amount in AUD$

Employment Income from Australia 23AG of Income Tax Assessment

Act 1997

Employment Income from United States 23AG of Income Tax

Assessment Act 1997

Employment Income from United Kingdom23AG of Income Tax

Assessment Act 1997

Rental income from property in United Kingdom 380-35 of Income

Tax Assessment Act 1997

Dividend Income from United Kingdom (assumed as grossed up) –

47A(1) of Income Tax Assessment Act 1997

Interest Income from United Kingdom 26-25 of ITAA 1997

Total Gross Income

Less: Expenses :

Medical Expenses 159P of ITAA 1997

Expenses incurred in deriving employment income from Australia

Expenses incurred in deriving employment income from the US

Expenses incurred in deriving employment income from the UK

Gift to a deductible gift recipient 30-15 of ITAA 1997

Interest on debt for deriving dividend income 82L to 82T ITAA 1997

44,000

12,000

8,000

2,000

1,200

800

68,000

5,000

4,000

900

500

400

140

60

57,000

10,072

1,140

11,212

4,400

6,812

7

Answer – 3

Computation of Income that is assessable

Particulars Amount in AUD$

Employment Income from Australia 23AG of Income Tax Assessment

Act 1997

Employment Income from United States 23AG of Income Tax

Assessment Act 1997

Employment Income from United Kingdom23AG of Income Tax

Assessment Act 1997

Rental income from property in United Kingdom 380-35 of Income

Tax Assessment Act 1997

Dividend Income from United Kingdom (assumed as grossed up) –

47A(1) of Income Tax Assessment Act 1997

Interest Income from United Kingdom 26-25 of ITAA 1997

Total Gross Income

Less: Expenses :

Medical Expenses 159P of ITAA 1997

Expenses incurred in deriving employment income from Australia

Expenses incurred in deriving employment income from the US

Expenses incurred in deriving employment income from the UK

Gift to a deductible gift recipient 30-15 of ITAA 1997

Interest on debt for deriving dividend income 82L to 82T ITAA 1997

44,000

12,000

8,000

2,000

1,200

800

68,000

5,000

4,000

900

500

400

140

60

57,000

10,072

1,140

11,212

4,400

6,812

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Taxation law

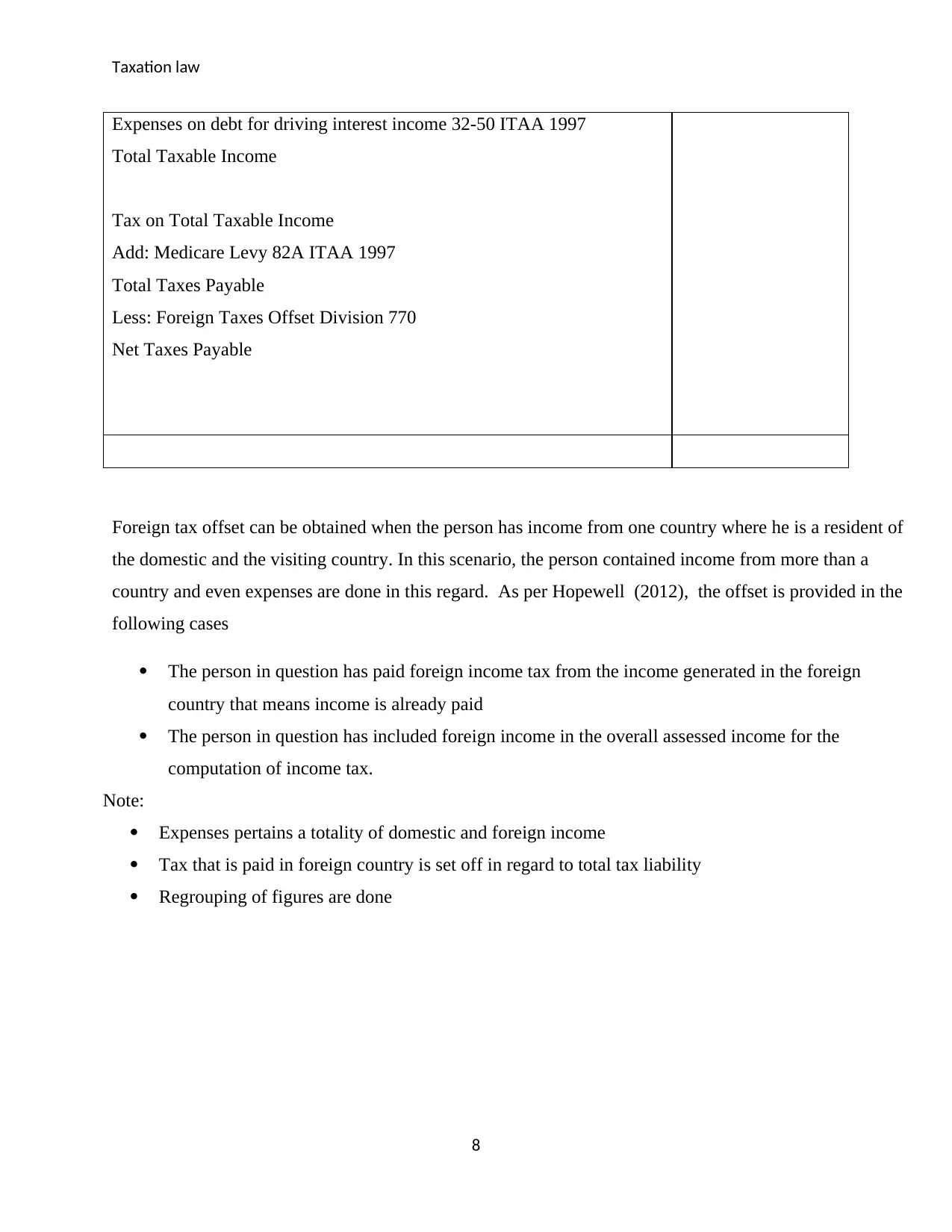

Expenses on debt for driving interest income 32-50 ITAA 1997

Total Taxable Income

Tax on Total Taxable Income

Add: Medicare Levy 82A ITAA 1997

Total Taxes Payable

Less: Foreign Taxes Offset Division 770

Net Taxes Payable

Foreign tax offset can be obtained when the person has income from one country where he is a resident of

the domestic and the visiting country. In this scenario, the person contained income from more than a

country and even expenses are done in this regard. As per Hopewell (2012), the offset is provided in the

following cases

The person in question has paid foreign income tax from the income generated in the foreign

country that means income is already paid

The person in question has included foreign income in the overall assessed income for the

computation of income tax.

Note:

Expenses pertains a totality of domestic and foreign income

Tax that is paid in foreign country is set off in regard to total tax liability

Regrouping of figures are done

8

Expenses on debt for driving interest income 32-50 ITAA 1997

Total Taxable Income

Tax on Total Taxable Income

Add: Medicare Levy 82A ITAA 1997

Total Taxes Payable

Less: Foreign Taxes Offset Division 770

Net Taxes Payable

Foreign tax offset can be obtained when the person has income from one country where he is a resident of

the domestic and the visiting country. In this scenario, the person contained income from more than a

country and even expenses are done in this regard. As per Hopewell (2012), the offset is provided in the

following cases

The person in question has paid foreign income tax from the income generated in the foreign

country that means income is already paid

The person in question has included foreign income in the overall assessed income for the

computation of income tax.

Note:

Expenses pertains a totality of domestic and foreign income

Tax that is paid in foreign country is set off in regard to total tax liability

Regrouping of figures are done

8

Taxation law

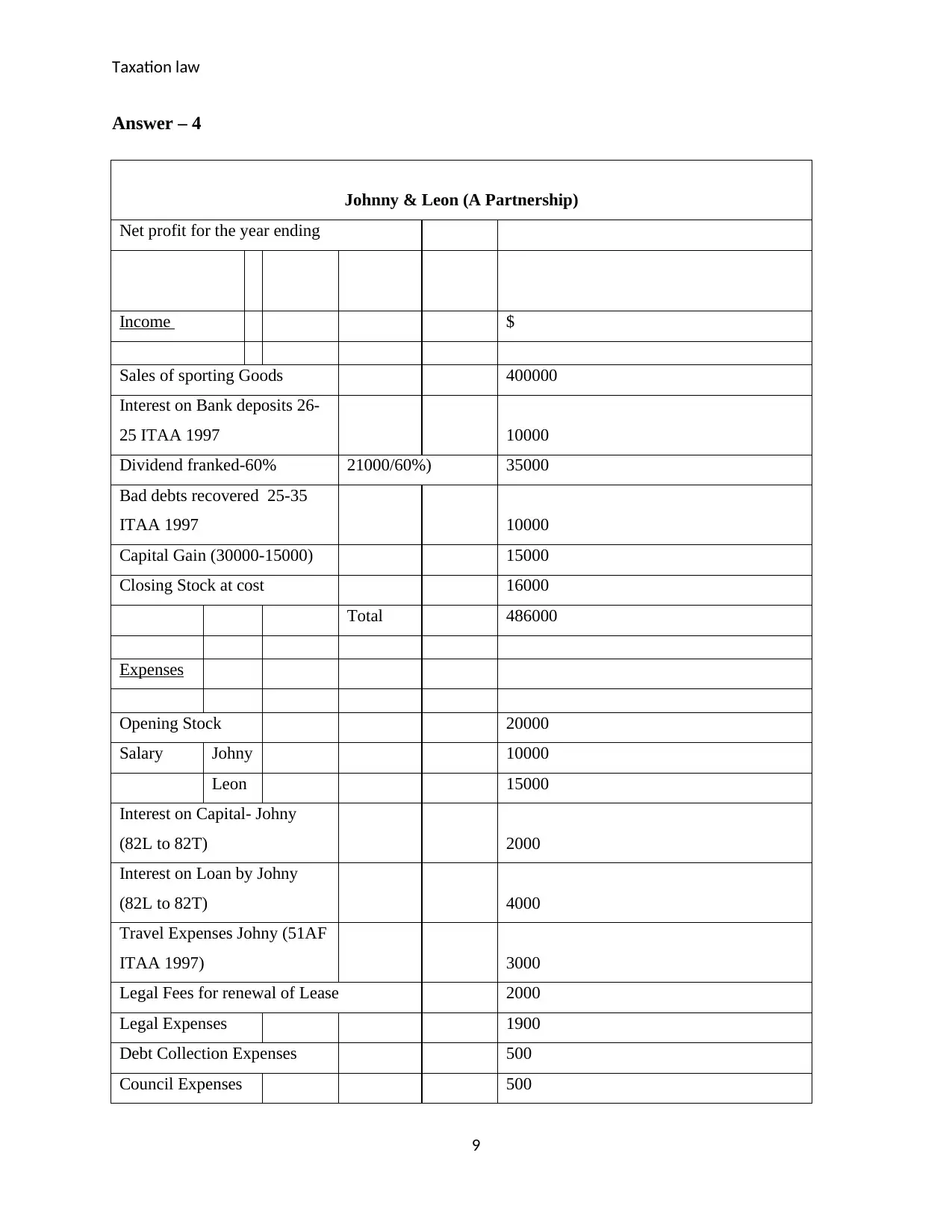

Answer – 4

Johnny & Leon (A Partnership)

Net profit for the year ending

Income $

Sales of sporting Goods 400000

Interest on Bank deposits 26-

25 ITAA 1997 10000

Dividend franked-60% 21000/60%) 35000

Bad debts recovered 25-35

ITAA 1997 10000

Capital Gain (30000-15000) 15000

Closing Stock at cost 16000

Total 486000

Expenses

Opening Stock 20000

Salary Johny 10000

Leon 15000

Interest on Capital- Johny

(82L to 82T) 2000

Interest on Loan by Johny

(82L to 82T) 4000

Travel Expenses Johny (51AF

ITAA 1997) 3000

Legal Fees for renewal of Lease 2000

Legal Expenses 1900

Debt Collection Expenses 500

Council Expenses 500

9

Answer – 4

Johnny & Leon (A Partnership)

Net profit for the year ending

Income $

Sales of sporting Goods 400000

Interest on Bank deposits 26-

25 ITAA 1997 10000

Dividend franked-60% 21000/60%) 35000

Bad debts recovered 25-35

ITAA 1997 10000

Capital Gain (30000-15000) 15000

Closing Stock at cost 16000

Total 486000

Expenses

Opening Stock 20000

Salary Johny 10000

Leon 15000

Interest on Capital- Johny

(82L to 82T) 2000

Interest on Loan by Johny

(82L to 82T) 4000

Travel Expenses Johny (51AF

ITAA 1997) 3000

Legal Fees for renewal of Lease 2000

Legal Expenses 1900

Debt Collection Expenses 500

Council Expenses 500

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Taxation law

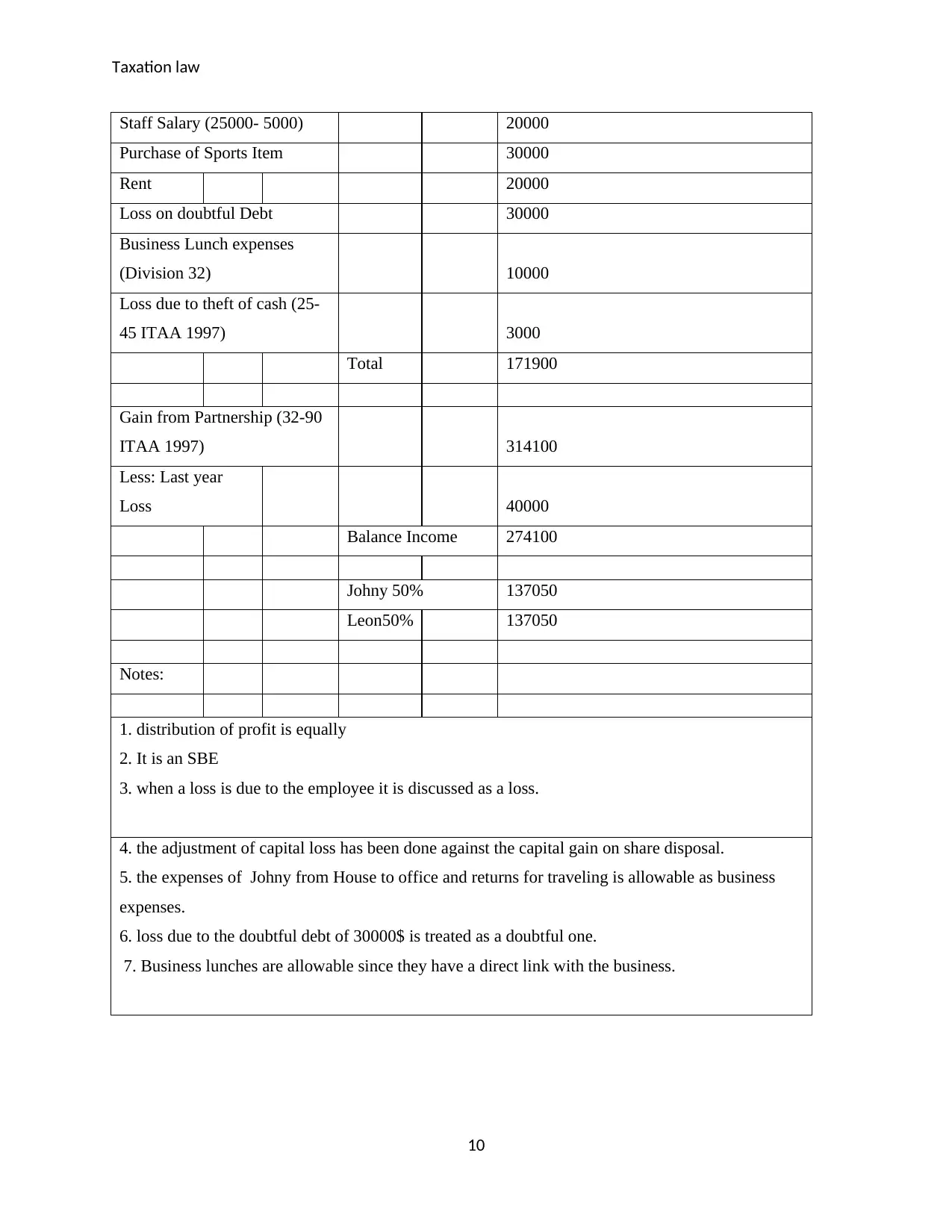

Staff Salary (25000- 5000) 20000

Purchase of Sports Item 30000

Rent 20000

Loss on doubtful Debt 30000

Business Lunch expenses

(Division 32) 10000

Loss due to theft of cash (25-

45 ITAA 1997) 3000

Total 171900

Gain from Partnership (32-90

ITAA 1997) 314100

Less: Last year

Loss 40000

Balance Income 274100

Johny 50% 137050

Leon50% 137050

Notes:

1. distribution of profit is equally

2. It is an SBE

3. when a loss is due to the employee it is discussed as a loss.

4. the adjustment of capital loss has been done against the capital gain on share disposal.

5. the expenses of Johny from House to office and returns for traveling is allowable as business

expenses.

6. loss due to the doubtful debt of 30000$ is treated as a doubtful one.

7. Business lunches are allowable since they have a direct link with the business.

10

Staff Salary (25000- 5000) 20000

Purchase of Sports Item 30000

Rent 20000

Loss on doubtful Debt 30000

Business Lunch expenses

(Division 32) 10000

Loss due to theft of cash (25-

45 ITAA 1997) 3000

Total 171900

Gain from Partnership (32-90

ITAA 1997) 314100

Less: Last year

Loss 40000

Balance Income 274100

Johny 50% 137050

Leon50% 137050

Notes:

1. distribution of profit is equally

2. It is an SBE

3. when a loss is due to the employee it is discussed as a loss.

4. the adjustment of capital loss has been done against the capital gain on share disposal.

5. the expenses of Johny from House to office and returns for traveling is allowable as business

expenses.

6. loss due to the doubtful debt of 30000$ is treated as a doubtful one.

7. Business lunches are allowable since they have a direct link with the business.

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Taxation law

References

Barcokzy, S 2010, Australian Tax Casebook, CCH Australia Ltd

Fullerton,I.G, Deutsch, R, Friezer, M.L, Hanley,P & Snape, T 2017, The Australian Tax

Handbook Tax Return Edition 2017, Thomson Reuters: Australia

Fullerton,I.G, Deutsch, R, Friezer, M.L, Hanley,P & Snape, T 2017, The Australian Tax

Gilders, T & Walpole, B.C 2016, Understanding Taxation Law 2016, LexisNexis

Hopewell, L 2012, Australia tax inquiry opens submissions, viewed 12 September 2017,

www.zdnet.com.au.

Kenny, P, Blissenden, M, & Villios, S 2017, Australian Tax 2017, Thomson Reuters: Australia

Khadem, S 2017, News Australia loses appeal in Federal Court on $15m tax bill, viewed 12

September 2017 http://www.smh.com.au/business/the-economy/news-australia-loses-appeal-in-

federal-court-on-15m-tax-bill-20170609-gwnz0b.html

Kobestky, M 2005, Income Tax: Text, Materials and Essential Cases, Sydney: The Federation

Press

Nethercott, L, Richardson, G & Devos,K. 2013, Australian Taxation Study Manual, Sydney.

Pratt, J. W & Kulsrud, W N 2013, Federal Taxation, Oxford university press.

Sadiq, K, Coleman, C , Hanegbi, R, Jogarajan,S, Krever, R, Obst, R, Teoh, J & Ting, A 2017,

Principles of Taxation Law 2017, Law book Australia

11

References

Barcokzy, S 2010, Australian Tax Casebook, CCH Australia Ltd

Fullerton,I.G, Deutsch, R, Friezer, M.L, Hanley,P & Snape, T 2017, The Australian Tax

Handbook Tax Return Edition 2017, Thomson Reuters: Australia

Fullerton,I.G, Deutsch, R, Friezer, M.L, Hanley,P & Snape, T 2017, The Australian Tax

Gilders, T & Walpole, B.C 2016, Understanding Taxation Law 2016, LexisNexis

Hopewell, L 2012, Australia tax inquiry opens submissions, viewed 12 September 2017,

www.zdnet.com.au.

Kenny, P, Blissenden, M, & Villios, S 2017, Australian Tax 2017, Thomson Reuters: Australia

Khadem, S 2017, News Australia loses appeal in Federal Court on $15m tax bill, viewed 12

September 2017 http://www.smh.com.au/business/the-economy/news-australia-loses-appeal-in-

federal-court-on-15m-tax-bill-20170609-gwnz0b.html

Kobestky, M 2005, Income Tax: Text, Materials and Essential Cases, Sydney: The Federation

Press

Nethercott, L, Richardson, G & Devos,K. 2013, Australian Taxation Study Manual, Sydney.

Pratt, J. W & Kulsrud, W N 2013, Federal Taxation, Oxford university press.

Sadiq, K, Coleman, C , Hanegbi, R, Jogarajan,S, Krever, R, Obst, R, Teoh, J & Ting, A 2017,

Principles of Taxation Law 2017, Law book Australia

11

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.