Taxation Law Assignment: Deductions, GST, and Income

VerifiedAdded on 2019/10/31

|11

|2459

|165

Homework Assignment

AI Summary

This assignment addresses several key issues in taxation law. The first section examines the deductibility of expenses, including the cost of moving machinery, asset revaluation for insurance, and legal expenses in various scenarios. The second part analyzes the ability of a company to claim input tax credits for advertising expenditure, considering the relevant GST rules. The third section focuses on calculating assessable incomes, deductions, and foreign tax offsets for an individual. The final section assesses the net income of a partnership, identifying assessable income, deductions, and the treatment of various expenses, including partner salaries, interest, and bad debts. The assignment provides detailed analysis and application of relevant sections of the ITAA 1997 to determine the tax implications in each case.

TAXATION LAW

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Taxation law

Answer-1

1)

Issue- Whether or not the Cost of moving machinery to a new site allowable as a deduction

under s 8-1 while computing the assessable income.

Rule- According to the s 8-1 of the ITAA 1997, those expenses which are incurred directly or

indirectly in running the business are treated as allowable expenses. Further, those expenses

which are of capital nature or are incurred in relation to purchasing, transportation, and

installation of a capital asset purchased or are for domestic or private use are not allowed as a

deduction under s 8-1 (Barcokzy, 2010).

Application- It was held in the case of W Neville & Co v FCT (1937) that the expenses done for

the purpose of the business must be provided as a deduction (Barcokzy, 2010). In the given

question, it is not clear that whether the machinery being moved to the new site is a brand new

machine which is being transported from the seller place to buyer’s site the or it is an old

machine which is being transported from one site to another. In the former case that is where the

new machinery purchased is being transported to the buyer’s site then the expenses that will be

incurred in such transportation shall be treated as included in the cost of machinery purchased

and shall not be allowed as a deduction from the assessable income. In the latter case, if the old

machinery is being transported from one site to another, for example in case of road construction

the road rollers are shifted from one site to another once the work gets completed at the first site.

In such case, the transportation cost shall be treated as a business expenditure and shall be

allowed as a deduction under s 8-1of ITAA 1997 (Sadiq et. al, 2017).

Conclusion- If the machinery is old and is being transported from one site to another for

completion of business purpose, and then the cost shall be considered as transportation cost and

shall be allowable as a deduction under s 8-1 (Kobestky, 2005).

2

Answer-1

1)

Issue- Whether or not the Cost of moving machinery to a new site allowable as a deduction

under s 8-1 while computing the assessable income.

Rule- According to the s 8-1 of the ITAA 1997, those expenses which are incurred directly or

indirectly in running the business are treated as allowable expenses. Further, those expenses

which are of capital nature or are incurred in relation to purchasing, transportation, and

installation of a capital asset purchased or are for domestic or private use are not allowed as a

deduction under s 8-1 (Barcokzy, 2010).

Application- It was held in the case of W Neville & Co v FCT (1937) that the expenses done for

the purpose of the business must be provided as a deduction (Barcokzy, 2010). In the given

question, it is not clear that whether the machinery being moved to the new site is a brand new

machine which is being transported from the seller place to buyer’s site the or it is an old

machine which is being transported from one site to another. In the former case that is where the

new machinery purchased is being transported to the buyer’s site then the expenses that will be

incurred in such transportation shall be treated as included in the cost of machinery purchased

and shall not be allowed as a deduction from the assessable income. In the latter case, if the old

machinery is being transported from one site to another, for example in case of road construction

the road rollers are shifted from one site to another once the work gets completed at the first site.

In such case, the transportation cost shall be treated as a business expenditure and shall be

allowed as a deduction under s 8-1of ITAA 1997 (Sadiq et. al, 2017).

Conclusion- If the machinery is old and is being transported from one site to another for

completion of business purpose, and then the cost shall be considered as transportation cost and

shall be allowable as a deduction under s 8-1 (Kobestky, 2005).

2

Taxation law

2)

Issue- Whether or not the cost of revaluing assets to effect insurance cover allowable as a

deduction under s 8-1 while computing the assessable income.

Rule- According to the s 8-1 of the ITAA 1997, those expenses which are incurred directly or

indirectly in running the regular business activity and earning of assessable income are treated as

allowable expenses. If the expenses of revaluation of assets are related to the fixed assets, then

such expenses shall not be treated as allowable expenses under s 8-1. If the expenses are related

to assets such as stock which directly affect the calculation of assessable income, then such

expenses shall be treated as allowable expenses under s 8-1.

Application and Conclusion- in the given question, it is not clear that whether the evaluation is

being done for fixed assets or inventories. For determining the allowable expenses, it is

important to know whether such expenses being incurred are affecting the income making

capacity or are affecting the fixed assets. In case the expense is recurring in nature and are being

incurred for evaluation of inventories for the insurance cover for recovery of loss from

destruction of inventories, then the same shall be allowable expenses for deduction under s 8-1 as

the inventories are directly related to the calculation of assessable income.

3)

Issue – whether the legal expenses incurred by a company opposing a petition for winding up

allowable as a deduction under section 8-1 of ITAA 1997 or not.

Rule- the expenses that are deductible under s 8-1 of ITAA 1997 are those which are either

incurred in earning the taxable income or are incurred while carrying on the regular business

activities through which the said assessable income shall be earned. Deduction of those expenses

is not allowed which are either capital in nature or expenses which are private or domestic in

nature or the expenses which are in relation to earning of exempt income. The expenses which

are incurred for keeping the company in running position shall be allowed as business expenses.

Application and Conclusion- there may be two outcomes of the given situation. One is that the

company may lose the petition case and the company gets winded up and the second case that

the company shall win the case and company shall continue with its operations normally. But in

3

2)

Issue- Whether or not the cost of revaluing assets to effect insurance cover allowable as a

deduction under s 8-1 while computing the assessable income.

Rule- According to the s 8-1 of the ITAA 1997, those expenses which are incurred directly or

indirectly in running the regular business activity and earning of assessable income are treated as

allowable expenses. If the expenses of revaluation of assets are related to the fixed assets, then

such expenses shall not be treated as allowable expenses under s 8-1. If the expenses are related

to assets such as stock which directly affect the calculation of assessable income, then such

expenses shall be treated as allowable expenses under s 8-1.

Application and Conclusion- in the given question, it is not clear that whether the evaluation is

being done for fixed assets or inventories. For determining the allowable expenses, it is

important to know whether such expenses being incurred are affecting the income making

capacity or are affecting the fixed assets. In case the expense is recurring in nature and are being

incurred for evaluation of inventories for the insurance cover for recovery of loss from

destruction of inventories, then the same shall be allowable expenses for deduction under s 8-1 as

the inventories are directly related to the calculation of assessable income.

3)

Issue – whether the legal expenses incurred by a company opposing a petition for winding up

allowable as a deduction under section 8-1 of ITAA 1997 or not.

Rule- the expenses that are deductible under s 8-1 of ITAA 1997 are those which are either

incurred in earning the taxable income or are incurred while carrying on the regular business

activities through which the said assessable income shall be earned. Deduction of those expenses

is not allowed which are either capital in nature or expenses which are private or domestic in

nature or the expenses which are in relation to earning of exempt income. The expenses which

are incurred for keeping the company in running position shall be allowed as business expenses.

Application and Conclusion- there may be two outcomes of the given situation. One is that the

company may lose the petition case and the company gets winded up and the second case that

the company shall win the case and company shall continue with its operations normally. But in

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Taxation law

both the cases the expenses incurred will not result in earning of the assessable income directly

(Pratt & Kulsrud, 2013). The said expense is just necessary to save the business from winding

up. Hence the same shall not be treated as business expenses under s 8-1.

4)

Issue – whether the Legal Expenses incurred for services of a solicitor in respect of a number of

matters, including conveyance, discharge of a mortgage, and general legal advice relating to a

client’s business operations. (The Solicitor account does not separate the costs for various

matters.)

Rule- the expenses that are deductible under s 8-1 of ITAA 1997 are those which are either

incurred in earning the taxable income or are incurred while carrying on the regular business

activities through which the said assessable income shall be earned. Deduction of those expenses

is not allowed which are either capital in nature or expenses which are private or domestic in

nature or the expenses which are in relation to earning of exempt income (Nethercott et. al,

2013). The expenses which are incurred for keeping the company in running position shall be

allowed as business expenses.

Application and Conclusion- in the given case the solicitor has given varied services which

include general business expenses and other charges which may be categorized into capital

nature expense such as the discharge of a mortgage. The solicitor does not separate the costs for

different matters. Hence it shall be assumed in the given case that all the costs have been directly

and indirectly incurred for the discharge of mortgage (Cartwright, 2013). In such assumption, the

costs shall not be allowed as a deduction under s 8-1, but shall be deductible under another

section of ITAA 1997.

4

both the cases the expenses incurred will not result in earning of the assessable income directly

(Pratt & Kulsrud, 2013). The said expense is just necessary to save the business from winding

up. Hence the same shall not be treated as business expenses under s 8-1.

4)

Issue – whether the Legal Expenses incurred for services of a solicitor in respect of a number of

matters, including conveyance, discharge of a mortgage, and general legal advice relating to a

client’s business operations. (The Solicitor account does not separate the costs for various

matters.)

Rule- the expenses that are deductible under s 8-1 of ITAA 1997 are those which are either

incurred in earning the taxable income or are incurred while carrying on the regular business

activities through which the said assessable income shall be earned. Deduction of those expenses

is not allowed which are either capital in nature or expenses which are private or domestic in

nature or the expenses which are in relation to earning of exempt income (Nethercott et. al,

2013). The expenses which are incurred for keeping the company in running position shall be

allowed as business expenses.

Application and Conclusion- in the given case the solicitor has given varied services which

include general business expenses and other charges which may be categorized into capital

nature expense such as the discharge of a mortgage. The solicitor does not separate the costs for

different matters. Hence it shall be assumed in the given case that all the costs have been directly

and indirectly incurred for the discharge of mortgage (Cartwright, 2013). In such assumption, the

costs shall not be allowed as a deduction under s 8-1, but shall be deductible under another

section of ITAA 1997.

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Taxation law

Answer-2

Issue

Will Big Bank Limited will be able to claim input tax credits with respect to its advertising

expenditure or not?

Rule

The GST paid on a particular expense is allowed to be taken as input tax credit by the business

entities when a few conditions are fulfilled. Firstly, the entity that is claiming the input tax credit

needs to be GST registered. Hence, the registration is important when it comes to claiming of

GST. The expense on which GST is being claimed is a recurring business expense in nature. This

means it should happen on a continuous basis and not a one-time act. Moreover, the proper

invoice has been issued and GST has been separately mentioned in the invoice. The segregation

must be clearly indicated that enables to have a better grasp of the matter (Goldberg, 2017).

Application

Big Bank Limited is a massive bank with more than 50 branches, 10 storied office, and various

call centers. Now with a view of expansion Big Bank has started Home and Content Insurance

Services. It has to change its accounting system as well as advertises for the new business. Big

Bank has budgeted $ 16,50,000 for the advertisement campaign including television media and

another mode of televisions like radio and print. The advertising company has issued a bill of $

16,50,000 for advertisement campaign including GST. Now the Bank is required to claim the

GST charged on the advertisement bill as input claimed. Our view in this regard is that input

credit on advertising bill shall be allowed to Big Bank Ltd. because expenditure is in the nature

of revenue expenses and also has been incurred as business expenses other than capital expense

(Kenny, 2016). In case the expense was of capital nature, GST would have been added to the

cost of the asset. The input available shall be allowed as a set off against Bank’s GST liability.

The reasons for allowance of GST as input credit is that the Bank is registered under GST

provisions, and the GST has been mentioned in the Tax Invoice and also that the expense on

5

Answer-2

Issue

Will Big Bank Limited will be able to claim input tax credits with respect to its advertising

expenditure or not?

Rule

The GST paid on a particular expense is allowed to be taken as input tax credit by the business

entities when a few conditions are fulfilled. Firstly, the entity that is claiming the input tax credit

needs to be GST registered. Hence, the registration is important when it comes to claiming of

GST. The expense on which GST is being claimed is a recurring business expense in nature. This

means it should happen on a continuous basis and not a one-time act. Moreover, the proper

invoice has been issued and GST has been separately mentioned in the invoice. The segregation

must be clearly indicated that enables to have a better grasp of the matter (Goldberg, 2017).

Application

Big Bank Limited is a massive bank with more than 50 branches, 10 storied office, and various

call centers. Now with a view of expansion Big Bank has started Home and Content Insurance

Services. It has to change its accounting system as well as advertises for the new business. Big

Bank has budgeted $ 16,50,000 for the advertisement campaign including television media and

another mode of televisions like radio and print. The advertising company has issued a bill of $

16,50,000 for advertisement campaign including GST. Now the Bank is required to claim the

GST charged on the advertisement bill as input claimed. Our view in this regard is that input

credit on advertising bill shall be allowed to Big Bank Ltd. because expenditure is in the nature

of revenue expenses and also has been incurred as business expenses other than capital expense

(Kenny, 2016). In case the expense was of capital nature, GST would have been added to the

cost of the asset. The input available shall be allowed as a set off against Bank’s GST liability.

The reasons for allowance of GST as input credit is that the Bank is registered under GST

provisions, and the GST has been mentioned in the Tax Invoice and also that the expense on

5

Taxation law

which GST has been claimed is a business expense. Moreover, it is a recurring expenditure as

business promotion is an important part of the growth of a business (Adams, 2011).

Conclusion

The Big Bank Limited shall claim the input tax credit of GST as all the requisite conditions are

fulfilled. It is irrelevant regarding the sum involved in advertising and in which the GST has

been paid (Cane & Conaghan, 2009). The tax invoice amounting to $16,50000 includes the

television advertisement comprising of $5,50000 and the amount left aside is for the promotions.

This will enable the business to expand. This consists of 2% of the capital of the company and

the remaining 98% is catered with the help of loans and the deposits by the customers over

which commission and interest rates are applicable. Hence, the company is totally eligible for

GST

6

which GST has been claimed is a business expense. Moreover, it is a recurring expenditure as

business promotion is an important part of the growth of a business (Adams, 2011).

Conclusion

The Big Bank Limited shall claim the input tax credit of GST as all the requisite conditions are

fulfilled. It is irrelevant regarding the sum involved in advertising and in which the GST has

been paid (Cane & Conaghan, 2009). The tax invoice amounting to $16,50000 includes the

television advertisement comprising of $5,50000 and the amount left aside is for the promotions.

This will enable the business to expand. This consists of 2% of the capital of the company and

the remaining 98% is catered with the help of loans and the deposits by the customers over

which commission and interest rates are applicable. Hence, the company is totally eligible for

GST

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Taxation law

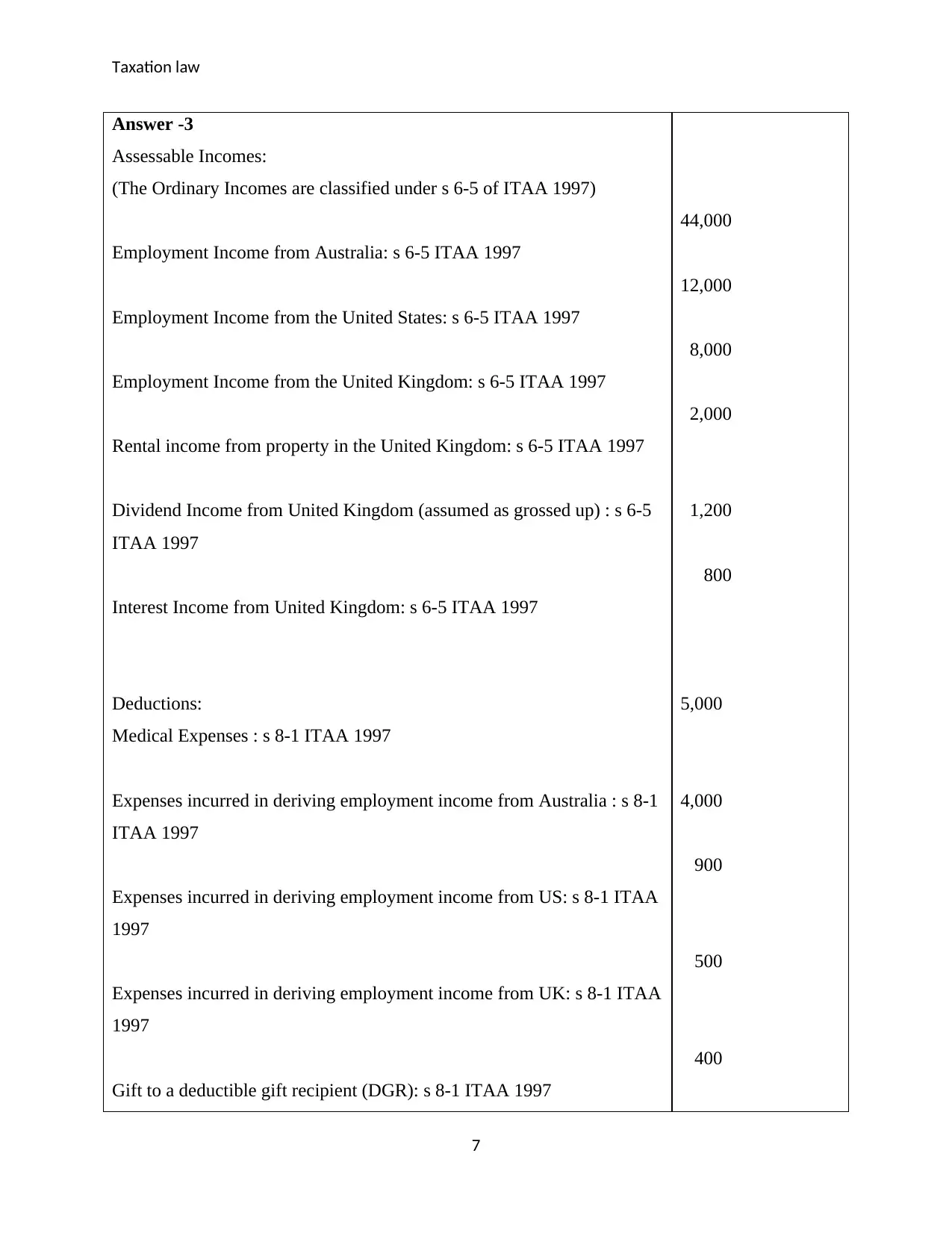

Answer -3

Assessable Incomes:

(The Ordinary Incomes are classified under s 6-5 of ITAA 1997)

Employment Income from Australia: s 6-5 ITAA 1997

Employment Income from the United States: s 6-5 ITAA 1997

Employment Income from the United Kingdom: s 6-5 ITAA 1997

Rental income from property in the United Kingdom: s 6-5 ITAA 1997

Dividend Income from United Kingdom (assumed as grossed up) : s 6-5

ITAA 1997

Interest Income from United Kingdom: s 6-5 ITAA 1997

Deductions:

Medical Expenses : s 8-1 ITAA 1997

Expenses incurred in deriving employment income from Australia : s 8-1

ITAA 1997

Expenses incurred in deriving employment income from US: s 8-1 ITAA

1997

Expenses incurred in deriving employment income from UK: s 8-1 ITAA

1997

Gift to a deductible gift recipient (DGR): s 8-1 ITAA 1997

44,000

12,000

8,000

2,000

1,200

800

5,000

4,000

900

500

400

7

Answer -3

Assessable Incomes:

(The Ordinary Incomes are classified under s 6-5 of ITAA 1997)

Employment Income from Australia: s 6-5 ITAA 1997

Employment Income from the United States: s 6-5 ITAA 1997

Employment Income from the United Kingdom: s 6-5 ITAA 1997

Rental income from property in the United Kingdom: s 6-5 ITAA 1997

Dividend Income from United Kingdom (assumed as grossed up) : s 6-5

ITAA 1997

Interest Income from United Kingdom: s 6-5 ITAA 1997

Deductions:

Medical Expenses : s 8-1 ITAA 1997

Expenses incurred in deriving employment income from Australia : s 8-1

ITAA 1997

Expenses incurred in deriving employment income from US: s 8-1 ITAA

1997

Expenses incurred in deriving employment income from UK: s 8-1 ITAA

1997

Gift to a deductible gift recipient (DGR): s 8-1 ITAA 1997

44,000

12,000

8,000

2,000

1,200

800

5,000

4,000

900

500

400

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Taxation law

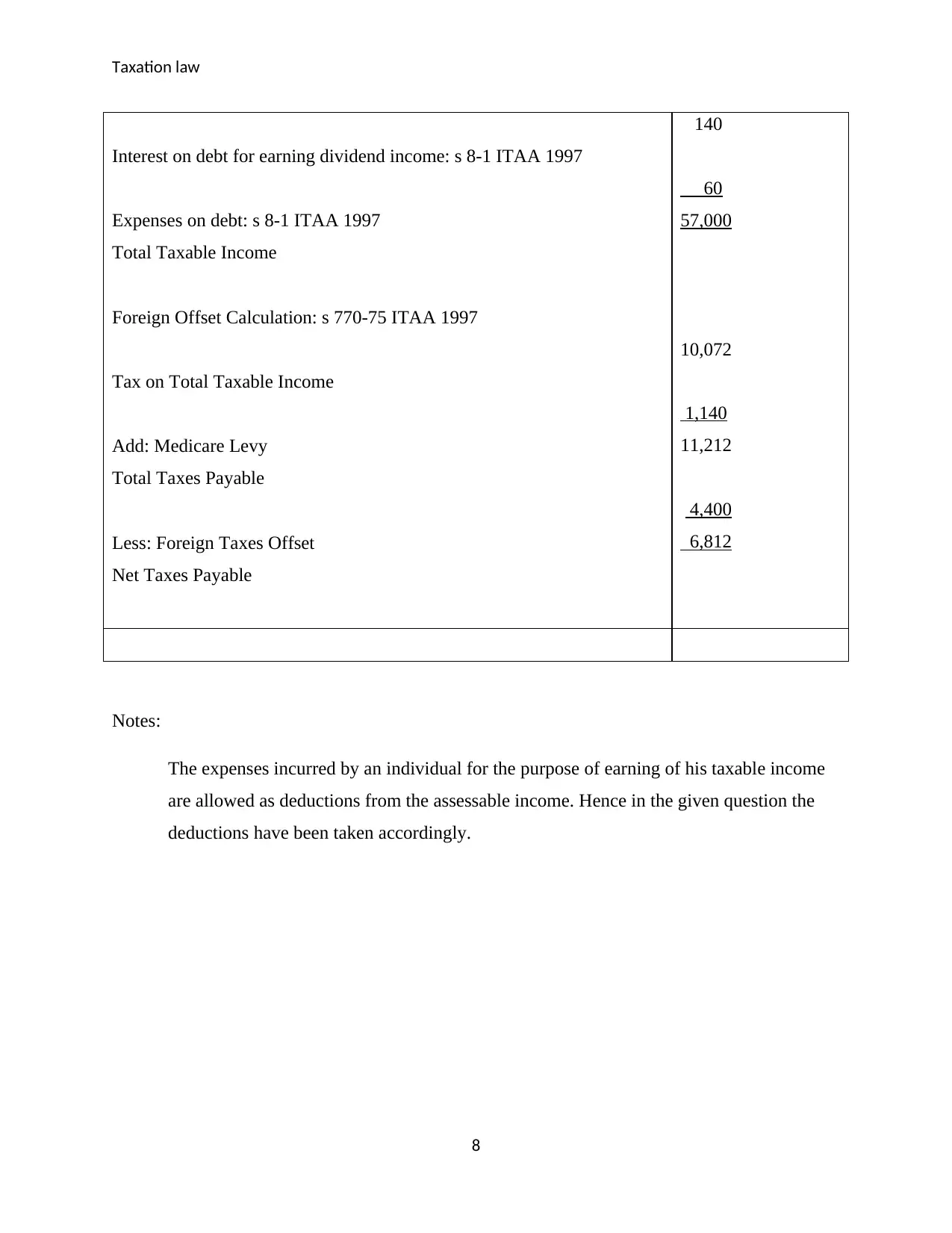

Interest on debt for earning dividend income: s 8-1 ITAA 1997

Expenses on debt: s 8-1 ITAA 1997

Total Taxable Income

Foreign Offset Calculation: s 770-75 ITAA 1997

Tax on Total Taxable Income

Add: Medicare Levy

Total Taxes Payable

Less: Foreign Taxes Offset

Net Taxes Payable

140

60

57,000

10,072

1,140

11,212

4,400

6,812

Notes:

The expenses incurred by an individual for the purpose of earning of his taxable income

are allowed as deductions from the assessable income. Hence in the given question the

deductions have been taken accordingly.

8

Interest on debt for earning dividend income: s 8-1 ITAA 1997

Expenses on debt: s 8-1 ITAA 1997

Total Taxable Income

Foreign Offset Calculation: s 770-75 ITAA 1997

Tax on Total Taxable Income

Add: Medicare Levy

Total Taxes Payable

Less: Foreign Taxes Offset

Net Taxes Payable

140

60

57,000

10,072

1,140

11,212

4,400

6,812

Notes:

The expenses incurred by an individual for the purpose of earning of his taxable income

are allowed as deductions from the assessable income. Hence in the given question the

deductions have been taken accordingly.

8

Taxation law

Answer-4

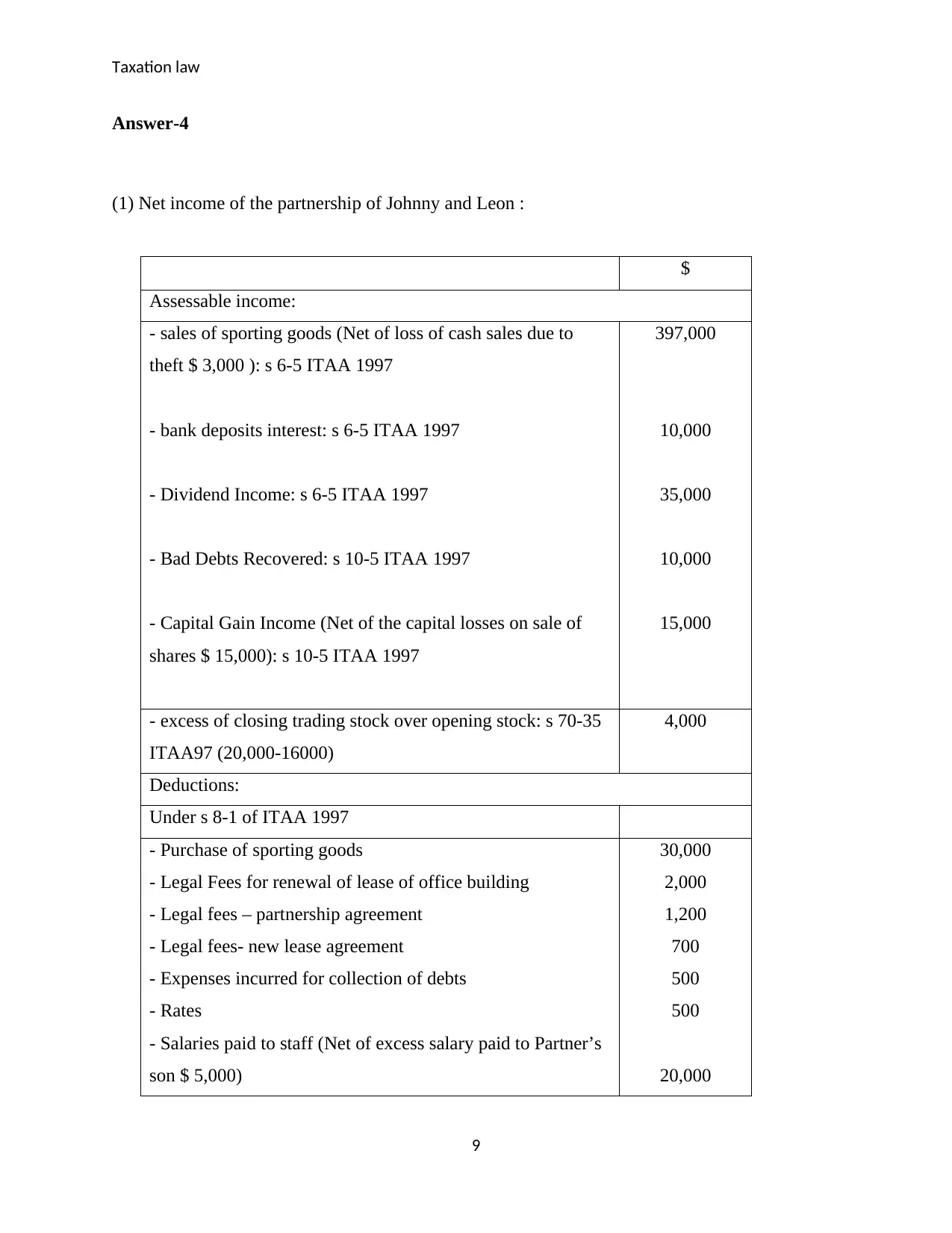

(1) Net income of the partnership of Johnny and Leon :

$

Assessable income:

- sales of sporting goods (Net of loss of cash sales due to

theft $ 3,000 ): s 6-5 ITAA 1997

- bank deposits interest: s 6-5 ITAA 1997

- Dividend Income: s 6-5 ITAA 1997

- Bad Debts Recovered: s 10-5 ITAA 1997

- Capital Gain Income (Net of the capital losses on sale of

shares $ 15,000): s 10-5 ITAA 1997

397,000

10,000

35,000

10,000

15,000

- excess of closing trading stock over opening stock: s 70-35

ITAA97 (20,000-16000)

4,000

Deductions:

Under s 8-1 of ITAA 1997

- Purchase of sporting goods

- Legal Fees for renewal of lease of office building

- Legal fees – partnership agreement

- Legal fees- new lease agreement

- Expenses incurred for collection of debts

- Rates

- Salaries paid to staff (Net of excess salary paid to Partner’s

son $ 5,000)

30,000

2,000

1,200

700

500

500

20,000

9

Answer-4

(1) Net income of the partnership of Johnny and Leon :

$

Assessable income:

- sales of sporting goods (Net of loss of cash sales due to

theft $ 3,000 ): s 6-5 ITAA 1997

- bank deposits interest: s 6-5 ITAA 1997

- Dividend Income: s 6-5 ITAA 1997

- Bad Debts Recovered: s 10-5 ITAA 1997

- Capital Gain Income (Net of the capital losses on sale of

shares $ 15,000): s 10-5 ITAA 1997

397,000

10,000

35,000

10,000

15,000

- excess of closing trading stock over opening stock: s 70-35

ITAA97 (20,000-16000)

4,000

Deductions:

Under s 8-1 of ITAA 1997

- Purchase of sporting goods

- Legal Fees for renewal of lease of office building

- Legal fees – partnership agreement

- Legal fees- new lease agreement

- Expenses incurred for collection of debts

- Rates

- Salaries paid to staff (Net of excess salary paid to Partner’s

son $ 5,000)

30,000

2,000

1,200

700

500

500

20,000

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Taxation law

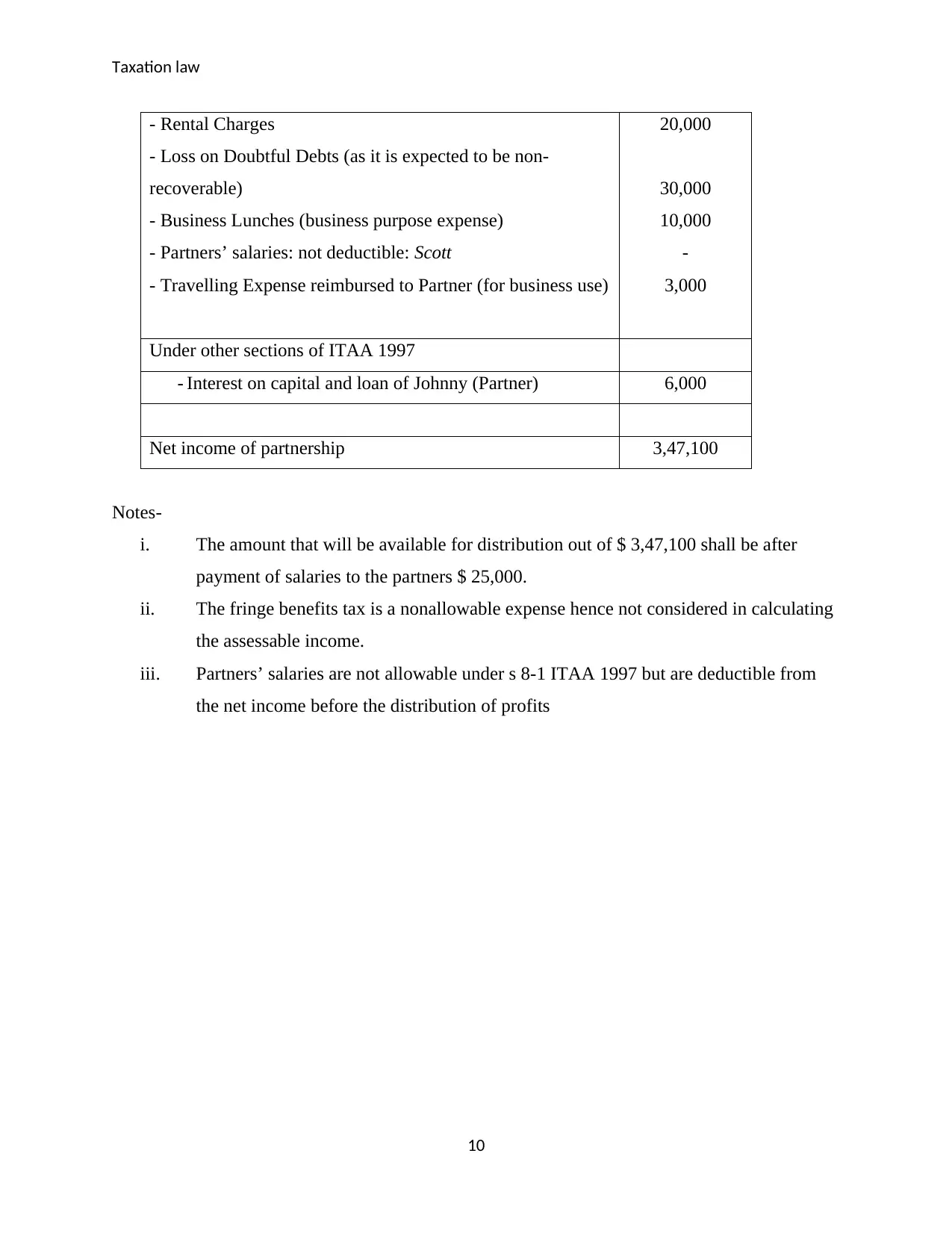

- Rental Charges

- Loss on Doubtful Debts (as it is expected to be non-

recoverable)

- Business Lunches (business purpose expense)

- Partners’ salaries: not deductible: Scott

- Travelling Expense reimbursed to Partner (for business use)

20,000

30,000

10,000

-

3,000

Under other sections of ITAA 1997

- Interest on capital and loan of Johnny (Partner) 6,000

Net income of partnership 3,47,100

Notes-

i. The amount that will be available for distribution out of $ 3,47,100 shall be after

payment of salaries to the partners $ 25,000.

ii. The fringe benefits tax is a nonallowable expense hence not considered in calculating

the assessable income.

iii. Partners’ salaries are not allowable under s 8-1 ITAA 1997 but are deductible from

the net income before the distribution of profits

10

- Rental Charges

- Loss on Doubtful Debts (as it is expected to be non-

recoverable)

- Business Lunches (business purpose expense)

- Partners’ salaries: not deductible: Scott

- Travelling Expense reimbursed to Partner (for business use)

20,000

30,000

10,000

-

3,000

Under other sections of ITAA 1997

- Interest on capital and loan of Johnny (Partner) 6,000

Net income of partnership 3,47,100

Notes-

i. The amount that will be available for distribution out of $ 3,47,100 shall be after

payment of salaries to the partners $ 25,000.

ii. The fringe benefits tax is a nonallowable expense hence not considered in calculating

the assessable income.

iii. Partners’ salaries are not allowable under s 8-1 ITAA 1997 but are deductible from

the net income before the distribution of profits

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Taxation law

References

Adams, J 2011, What is The Difference Between Tax Avoidance and Tax Evasion?, viewed 19

September 2017 https://www.taxinsider.co.uk/680-

What_is_The_Difference_Between_Tax_Avoidance_and_Tax_Evasion.html

Barcokzy, S 2010, Australian Tax Casebook, CCH Australia Ltd

Cane, P & Conaghan, J 2009, The new oxford companion to law, Oxford university Press.

Cartwright, M 2013, Death to the Australia Tax?, viewed 18 September 2017,

https://www.ato.gov.au/Individuals/Deceased-estates/Being-an-executor/Tax-responsibilities

Goldberg, S.G 2017, The Death of the Income Tax: A Progressive Consumption Tax and the

Path to Fiscal Reform, Oxford Press.

Kenny, B. V 2016, Australian Tax 2016, Thomson Reuters (Professional) Australia Limited

Kobestky, M 2005, Income Tax: Text, Materials and Essential Cases, Sydney: The Federation

Press

Nethercott, L, Richardson, G & Devos,K. 2013, Australian Taxation Study Manual, Sydney.

Pratt, J. W & Kulsrud, W N 2013, Federal Taxation, Oxford university press.

Sadiq, K, Coleman, C , Hanegbi, R, Jogarajan,S, Krever, R, Obst, R, Teoh, J & Ting, A 2017,

Principles of Taxation Law 2017, Law book Australia

11

References

Adams, J 2011, What is The Difference Between Tax Avoidance and Tax Evasion?, viewed 19

September 2017 https://www.taxinsider.co.uk/680-

What_is_The_Difference_Between_Tax_Avoidance_and_Tax_Evasion.html

Barcokzy, S 2010, Australian Tax Casebook, CCH Australia Ltd

Cane, P & Conaghan, J 2009, The new oxford companion to law, Oxford university Press.

Cartwright, M 2013, Death to the Australia Tax?, viewed 18 September 2017,

https://www.ato.gov.au/Individuals/Deceased-estates/Being-an-executor/Tax-responsibilities

Goldberg, S.G 2017, The Death of the Income Tax: A Progressive Consumption Tax and the

Path to Fiscal Reform, Oxford Press.

Kenny, B. V 2016, Australian Tax 2016, Thomson Reuters (Professional) Australia Limited

Kobestky, M 2005, Income Tax: Text, Materials and Essential Cases, Sydney: The Federation

Press

Nethercott, L, Richardson, G & Devos,K. 2013, Australian Taxation Study Manual, Sydney.

Pratt, J. W & Kulsrud, W N 2013, Federal Taxation, Oxford university press.

Sadiq, K, Coleman, C , Hanegbi, R, Jogarajan,S, Krever, R, Obst, R, Teoh, J & Ting, A 2017,

Principles of Taxation Law 2017, Law book Australia

11

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.