Comparing FIFO and Weighted Average in Process Costing - Auto Ltd

VerifiedAdded on 2023/06/10

|13

|984

|248

Presentation

AI Summary

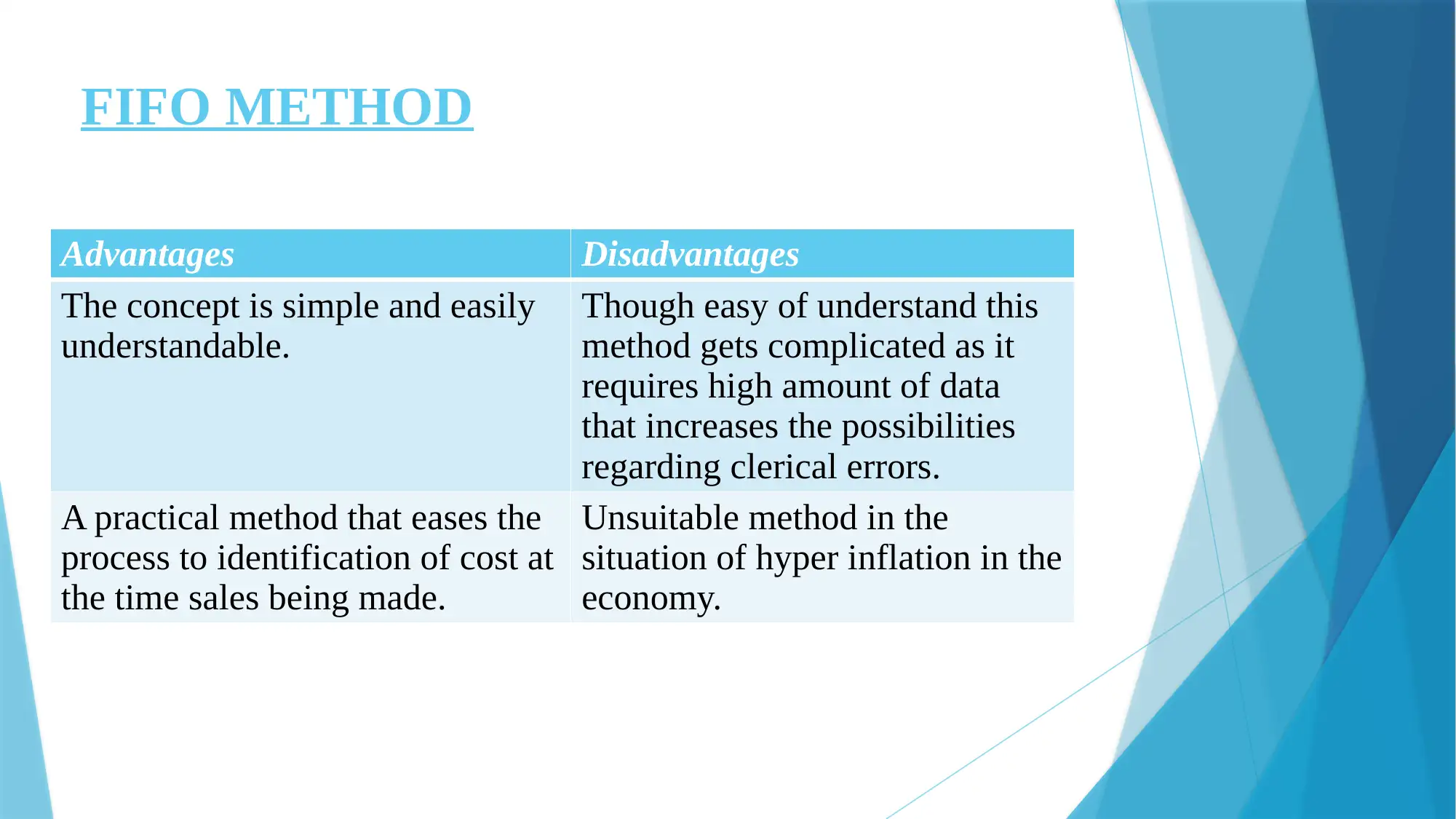

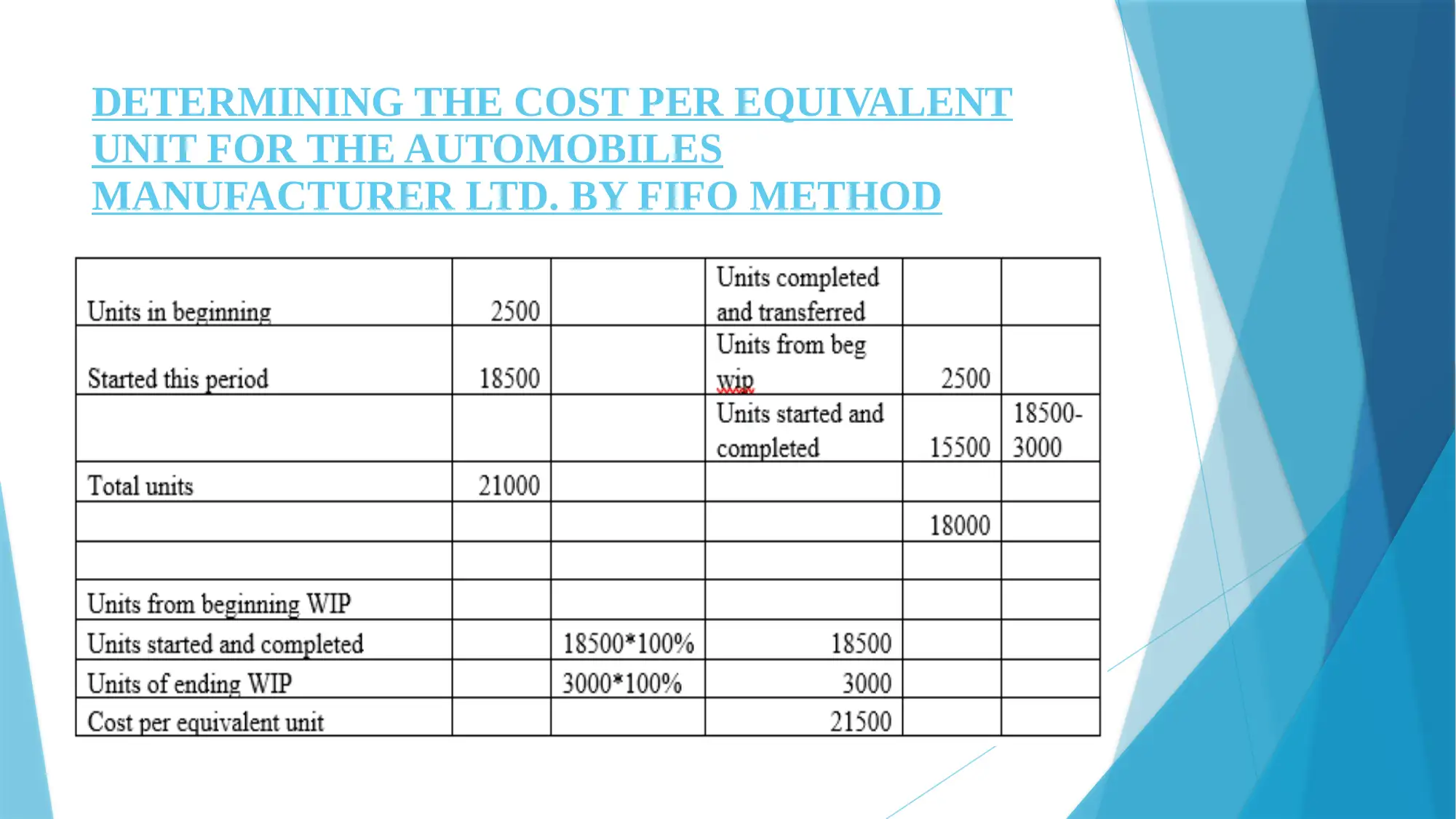

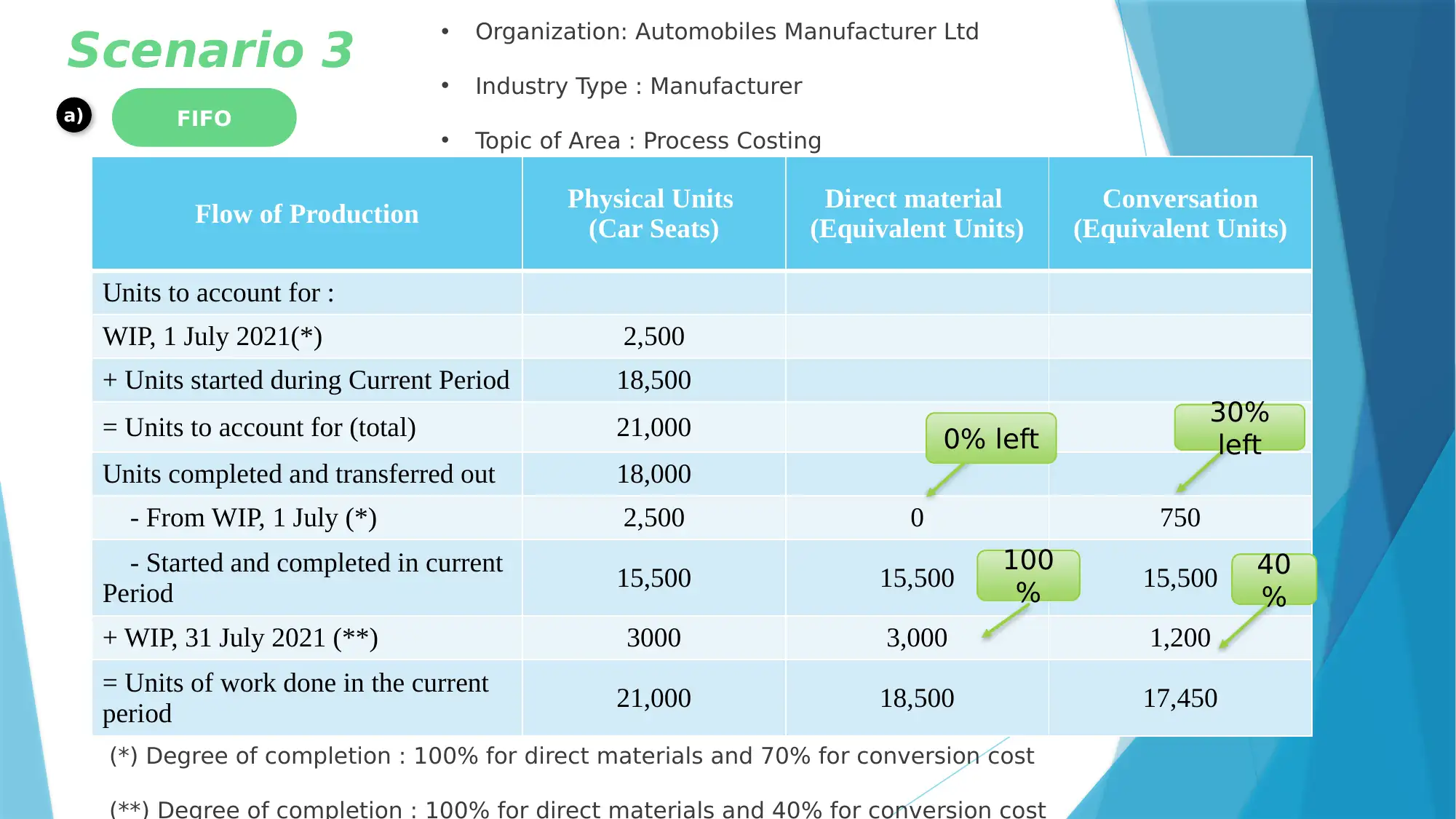

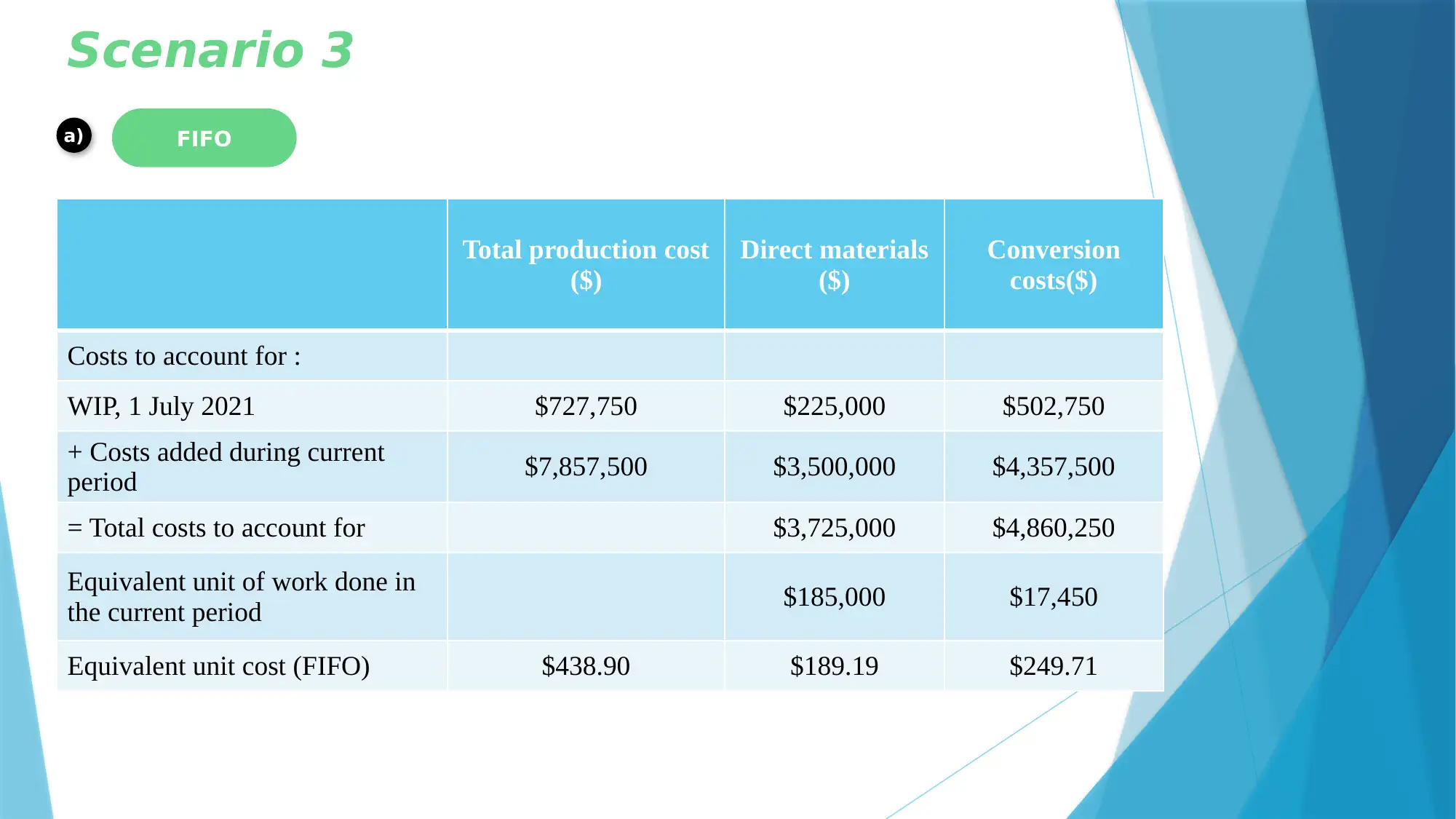

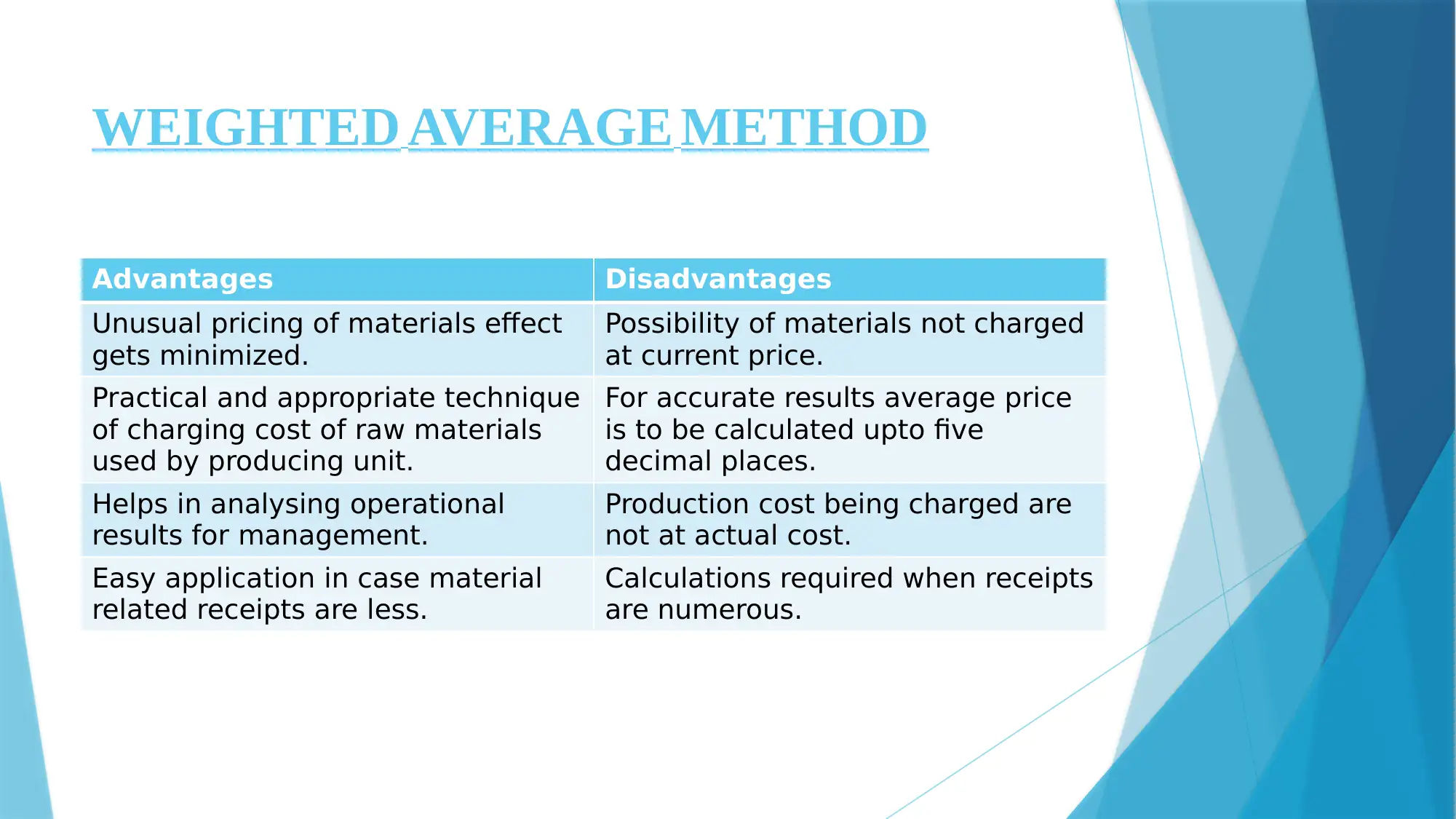

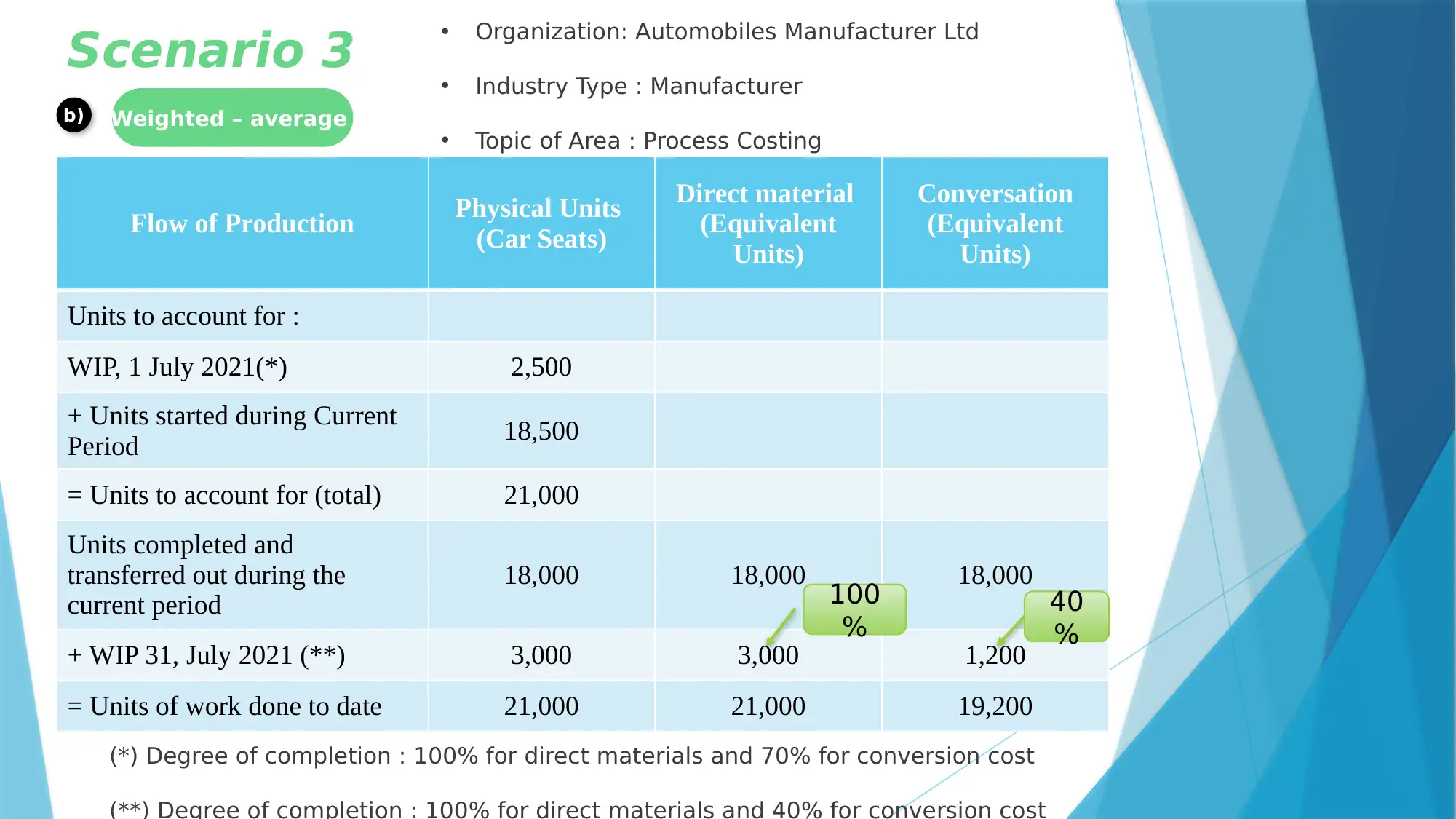

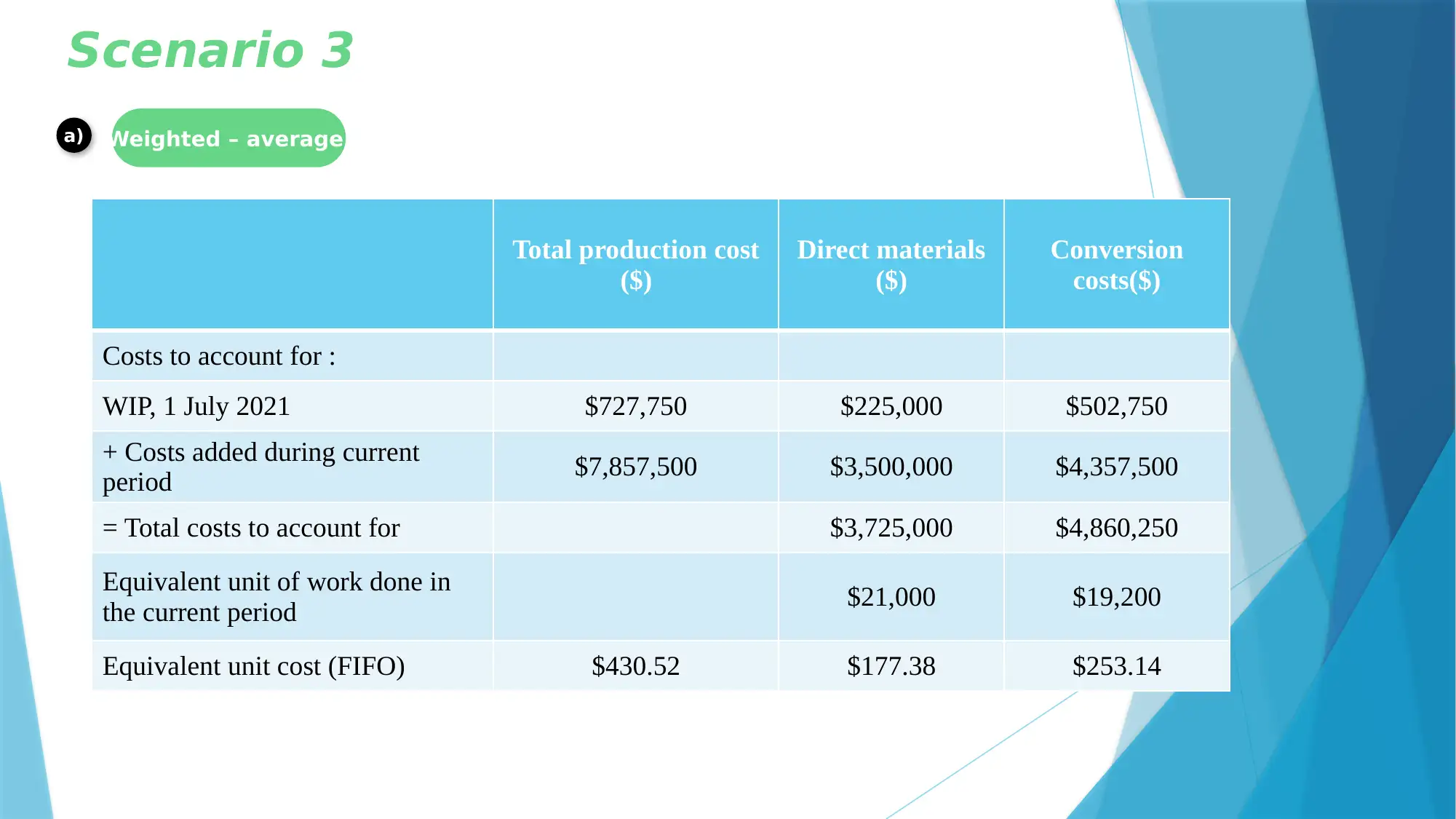

This presentation delves into financial management, focusing on process costing and comparing the FIFO (First-In, First-Out) and weighted average methods. It begins by defining financial management and process costing, then outlines the advantages and disadvantages of each costing method. A detailed scenario involving Automobiles Manufacturer Ltd is used to calculate the cost per equivalent unit using both FIFO and weighted average methods, demonstrating the practical application of each. The presentation concludes by summarizing the key aspects of financial management and process costing, highlighting the usefulness of these methods in enterprise financial analysis. References to relevant books and journals are also included to support the analysis and provide further reading.

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.