Finance for Managers: Break-Even Analysis and Decision Making

VerifiedAdded on 2022/12/27

|12

|1125

|31

Presentation

AI Summary

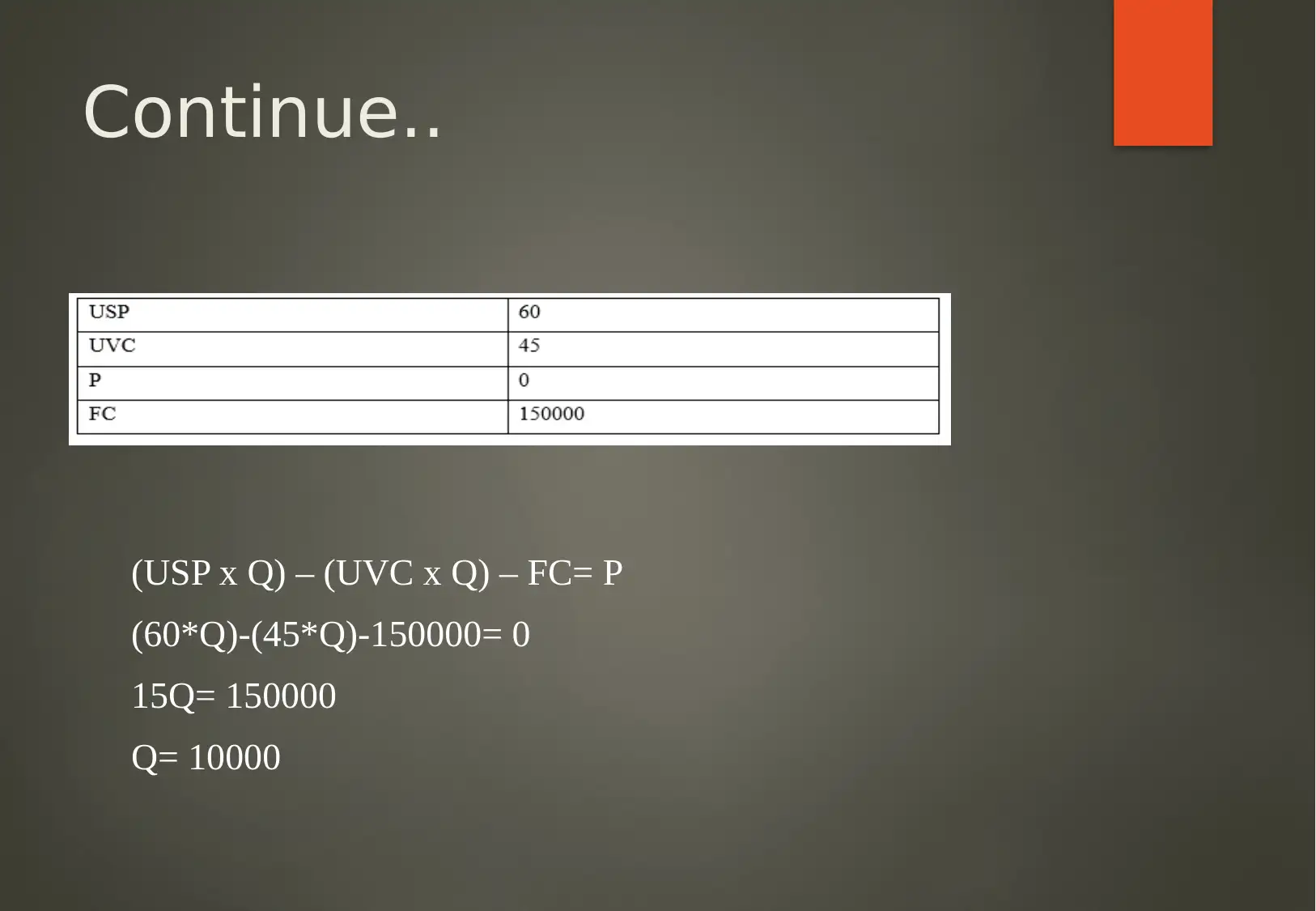

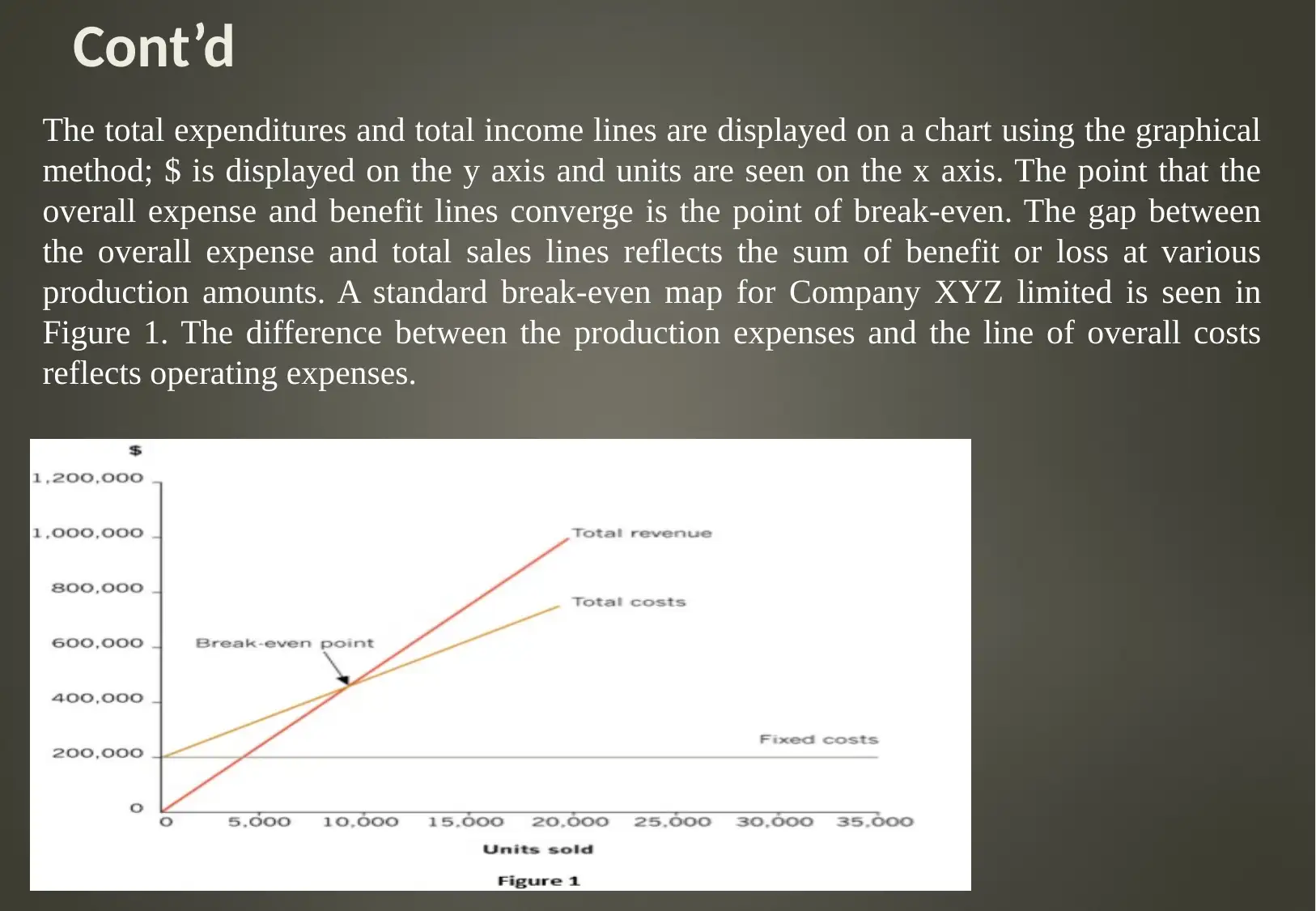

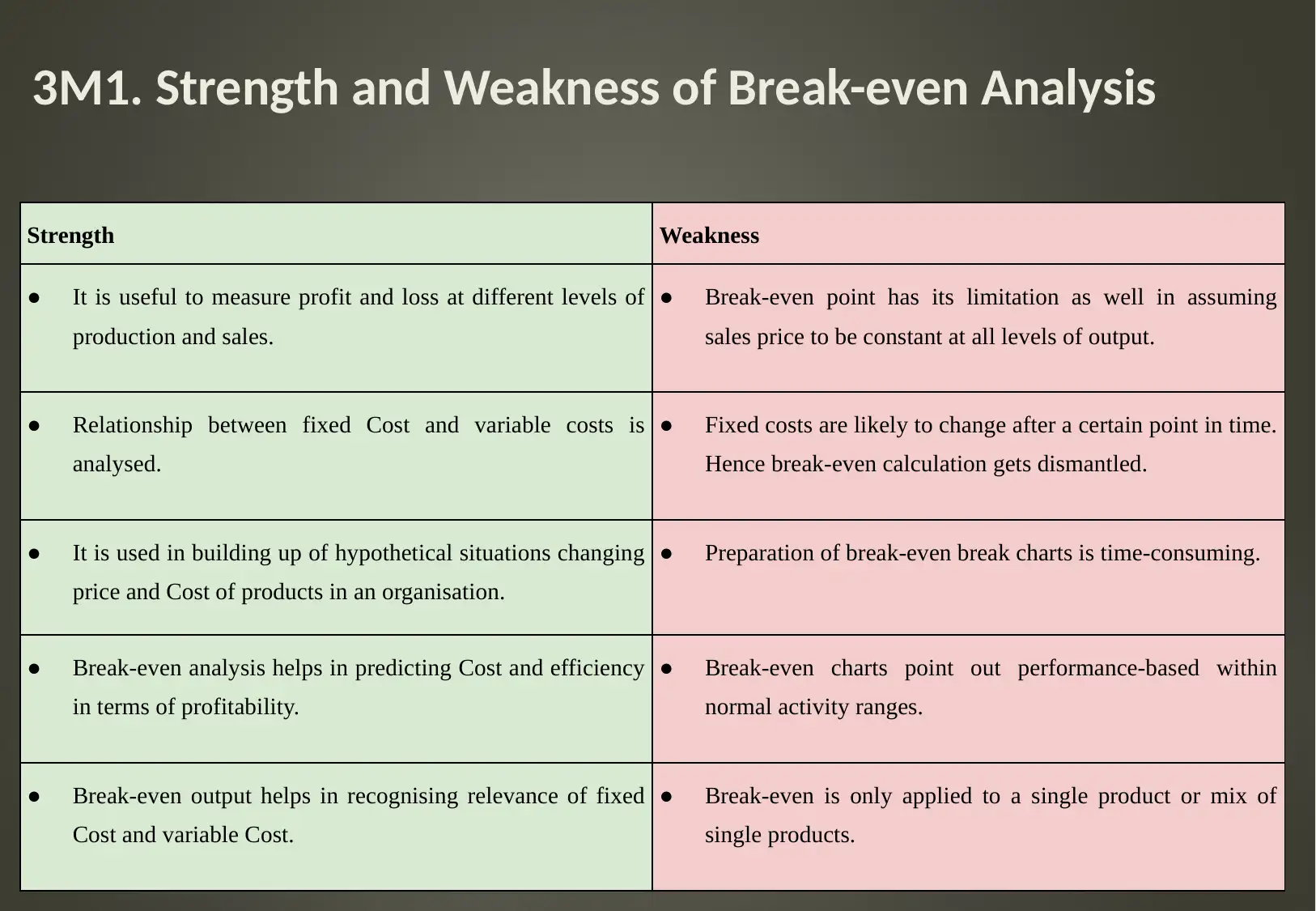

This presentation provides a comprehensive overview of break-even analysis, a crucial concept in finance for managers. It begins with an introduction to the break-even concept, its calculation, and a discussion of its strengths and weaknesses. The presentation delves into organizational cost analysis, differentiating between fixed and variable costs, direct and indirect costs, and other relevant cost categories. It explores marginal and absorption costing methods and their impact on business decisions. A case study of XYZ Limited is used to demonstrate the application of break-even calculations, including the graphical method for determining the break-even point. The presentation also analyzes the impact of changes in costs and revenue on the break-even output, emphasizing the importance of these factors in financial planning and decision-making. References are included for further study.

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.