Comprehensive Report: Managing Business Performance, Margrin Company

VerifiedAdded on 2023/01/06

|11

|3249

|54

Report

AI Summary

This report provides a comprehensive analysis of managing business performance, focusing on key concepts and their application within a business context. The report begins by explaining the principle of lifecycle costing and evaluating its relevance for Margrin Company, including a discussion on how it differs from traditional cost accounting and its benefits such as effective decision-making and long-term incentives. It then presents a budgeted result for Margrin, analyzing the company's performance over three years and identifying areas for improvement, such as boosting sales to maximize profit margins. The report also examines incremental budgeting, explaining its common usage and identifying its drawbacks, such as the potential for excessive spending and hindering creative ideas. Furthermore, the report delves into environmental management accounting (EMA), detailing its role in the modern business environment and its benefits, such as improving revenue, reducing costs, and enhancing the company's reputation. Finally, the report explores Total Quality Management (TQM), outlining its features and emphasizing its customer-focused approach. Overall, the report offers valuable insights into various aspects of business performance management, providing practical recommendations for Margrin Company and other businesses to enhance their efficiency and profitability.

Managing Business Performance

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

INTRODUCTION...........................................................................................................................2

MAIN BODY..................................................................................................................................2

Question 1........................................................................................................................................2

1. Explain the principle behind lifecycle costing and evaluate that why Margrin in particular

should consider this lifecycle principle.......................................................................................2

2. Produce the budgeted result.....................................................................................................3

3. Explain that why incremental budgeting is common method of budgeting and identify the

problems in this approach............................................................................................................4

Question 2........................................................................................................................................5

1. Environmental management accounting..................................................................................5

2. Explain the concepts of Total Quality Management and identify its features.........................6

3. Calculate the target cost of the Sims........................................................................................8

CONCLUSION................................................................................................................................8

REFERENCES..............................................................................................................................10

1

MAIN BODY..................................................................................................................................2

Question 1........................................................................................................................................2

1. Explain the principle behind lifecycle costing and evaluate that why Margrin in particular

should consider this lifecycle principle.......................................................................................2

2. Produce the budgeted result.....................................................................................................3

3. Explain that why incremental budgeting is common method of budgeting and identify the

problems in this approach............................................................................................................4

Question 2........................................................................................................................................5

1. Environmental management accounting..................................................................................5

2. Explain the concepts of Total Quality Management and identify its features.........................6

3. Calculate the target cost of the Sims........................................................................................8

CONCLUSION................................................................................................................................8

REFERENCES..............................................................................................................................10

1

INTRODUCTION

Managing business performance is the act of establishing organisational targets, evaluating

the strategies used to accomplish those goals, and then finding opportunities for members to

manage those objectives more efficiently (Alexandridis and et.al., 2018). Through gathering and

analysing data, an organisation may recognise the impact of management changes on results, and

then adjust those solutions to improve, create a more efficient process. The key thing that

required noting about company performance management is that, it is used to optimize the

utilization of employees and management. The use of indicators is only a means of control, with

an increased profitability for that reason. This assessment based on two different questions where

first one is about principle behind the lifecycle costing and why incremental budgeting is one of

the common approaches. In addition, second question is about role of environmental

management accounting in the modern business environment.

MAIN BODY

Question 1

1. Explain the principle behind lifecycle costing and evaluate that why Margrin in particular

should consider this lifecycle principle

Life-cycle cost analysis (LCCA) is a tool for determining the overall maintenance costs of

the plant. It considered all the costs which obtained from business, maintaining and disposing of

a design or engineering method (Chin and Gallagher, 2019). LCCA is particularly useful when

plan options that meet similar performance requirements but vary with regard to original costs

and operating costs need to be evaluated in order to choose the one that maximises net savings.

For example, LCCA can help decide if the installation of a high-performance HVAC or glazing

device, which can raise initial costs but resulting in significantly reduced operational and

maintenance costs, is cost-effective or not. LCCA is not useful for distribution of the budget.

Margrin consider this lifecycle principle because it is varies from the traditional cost

accounting technique, which records cost object efficiency on a periodic basis such as weekly,

quarterly and annually. Whereas life cycle costing includes measuring cost and cost object sales

like commodity, project etc. over many calendar cycles i.e. estimated cost object life.

2

Managing business performance is the act of establishing organisational targets, evaluating

the strategies used to accomplish those goals, and then finding opportunities for members to

manage those objectives more efficiently (Alexandridis and et.al., 2018). Through gathering and

analysing data, an organisation may recognise the impact of management changes on results, and

then adjust those solutions to improve, create a more efficient process. The key thing that

required noting about company performance management is that, it is used to optimize the

utilization of employees and management. The use of indicators is only a means of control, with

an increased profitability for that reason. This assessment based on two different questions where

first one is about principle behind the lifecycle costing and why incremental budgeting is one of

the common approaches. In addition, second question is about role of environmental

management accounting in the modern business environment.

MAIN BODY

Question 1

1. Explain the principle behind lifecycle costing and evaluate that why Margrin in particular

should consider this lifecycle principle

Life-cycle cost analysis (LCCA) is a tool for determining the overall maintenance costs of

the plant. It considered all the costs which obtained from business, maintaining and disposing of

a design or engineering method (Chin and Gallagher, 2019). LCCA is particularly useful when

plan options that meet similar performance requirements but vary with regard to original costs

and operating costs need to be evaluated in order to choose the one that maximises net savings.

For example, LCCA can help decide if the installation of a high-performance HVAC or glazing

device, which can raise initial costs but resulting in significantly reduced operational and

maintenance costs, is cost-effective or not. LCCA is not useful for distribution of the budget.

Margrin consider this lifecycle principle because it is varies from the traditional cost

accounting technique, which records cost object efficiency on a periodic basis such as weekly,

quarterly and annually. Whereas life cycle costing includes measuring cost and cost object sales

like commodity, project etc. over many calendar cycles i.e. estimated cost object life.

2

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Product life-cycle analysis is also a method used to provide such a long-term image of the

feasibility of the product range, feedback mostly on efficacy of life-cycle management and

executing data to explain the impact on the economy of the option chosen in the development,

design phase, etc. It is often seen as a way to boost the management of production costs. It is

necessary to track and calculate costs at-point of the product life cycle. Principle of lifecycle cost

includes the several features or characteristics which attract Margrin Company to consider these

principles and these are as follow:

Product life-cycle costing includes measuring the costs and sales of a product over many

calendar cycles during its life-cycle. It helps the Margrin Company to evaluate cost and

total sales of their brand new game GFX.

Product life cycle cost tracks the expense of research & design and production and the

overall extent of these costs for each particular product relative to the profit of the item

(Fodor, 2020). Margrin identify the exact amount of spending on research & development

regarding new game.

Each step of the product life-cycle introduces various risks and opportunities that may

consider various effective strategies. With the help of principle, Margrin able to build

effective strategy which helps in minimising risk or maximising opportunity.

The life-cycle of the product can be extended by seeking new uses or users or by the

consumption of current users. Basically, it helps in attracting more users which maximise

the overall sales.

Use of Life cycle principle in Margrin Company provide several benefits such as, it results in

quicker revenue-generating behaviour or lower costs than might otherwise be regarded. It

ensures effective decision-making by a more reliable and practical measurement of sales and

costs, at least at the basic stage of the life cycle. It encourages long-term incentives. It offers an

aggregate structure for the consideration of cumulative incremental costs over the lifetime of the

product.

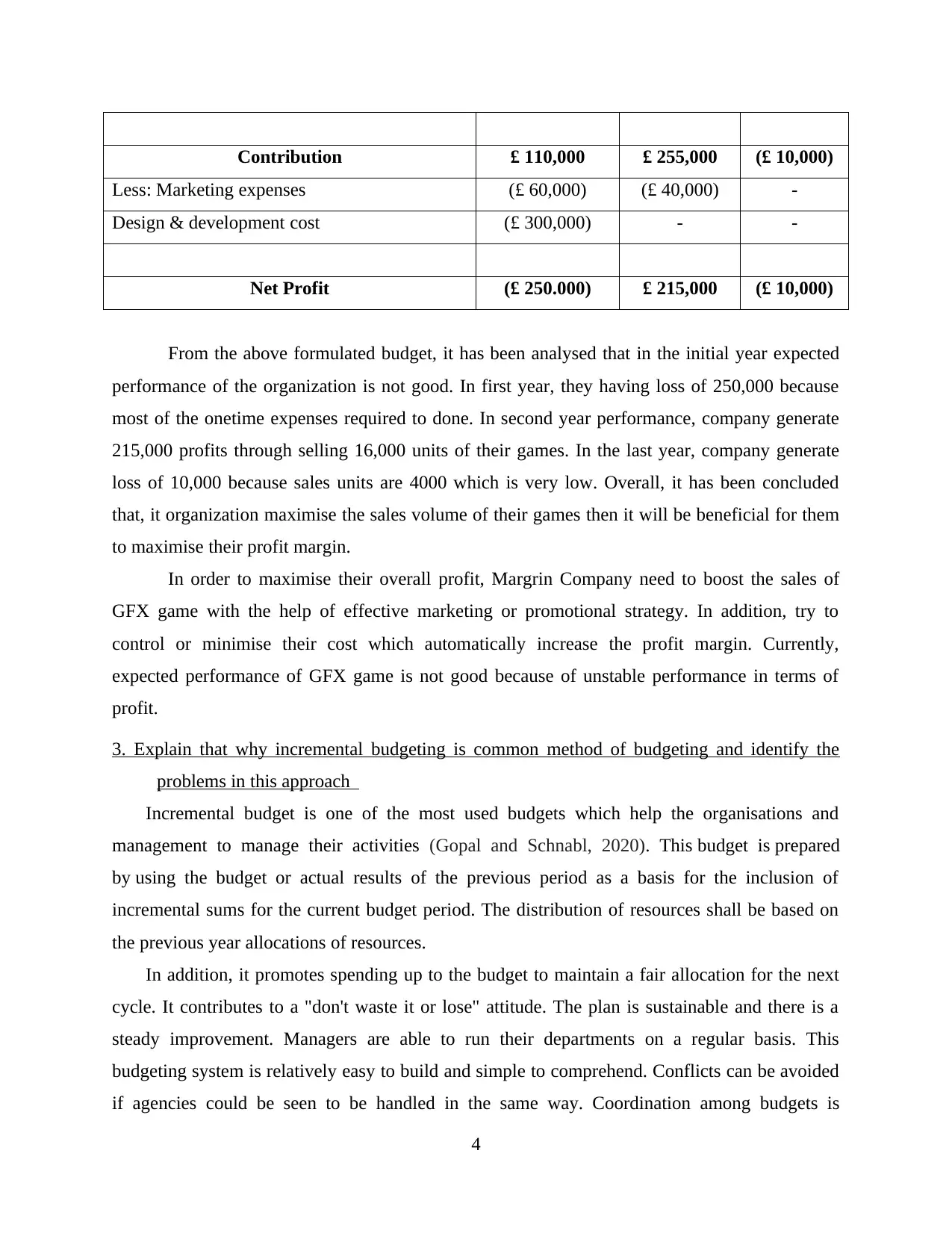

2. Produce the budgeted result

Particulars Year 1 Year 2 Year 3

Sales Unit £ 8000 £ 16000 £ 4000

Sales value (Unit * Selling Price) £ 240,000 £ 480,000 £ 120,000

Less: Cost (£ 130,000) (£ 225,000) (£ 130,000)

3

feasibility of the product range, feedback mostly on efficacy of life-cycle management and

executing data to explain the impact on the economy of the option chosen in the development,

design phase, etc. It is often seen as a way to boost the management of production costs. It is

necessary to track and calculate costs at-point of the product life cycle. Principle of lifecycle cost

includes the several features or characteristics which attract Margrin Company to consider these

principles and these are as follow:

Product life-cycle costing includes measuring the costs and sales of a product over many

calendar cycles during its life-cycle. It helps the Margrin Company to evaluate cost and

total sales of their brand new game GFX.

Product life cycle cost tracks the expense of research & design and production and the

overall extent of these costs for each particular product relative to the profit of the item

(Fodor, 2020). Margrin identify the exact amount of spending on research & development

regarding new game.

Each step of the product life-cycle introduces various risks and opportunities that may

consider various effective strategies. With the help of principle, Margrin able to build

effective strategy which helps in minimising risk or maximising opportunity.

The life-cycle of the product can be extended by seeking new uses or users or by the

consumption of current users. Basically, it helps in attracting more users which maximise

the overall sales.

Use of Life cycle principle in Margrin Company provide several benefits such as, it results in

quicker revenue-generating behaviour or lower costs than might otherwise be regarded. It

ensures effective decision-making by a more reliable and practical measurement of sales and

costs, at least at the basic stage of the life cycle. It encourages long-term incentives. It offers an

aggregate structure for the consideration of cumulative incremental costs over the lifetime of the

product.

2. Produce the budgeted result

Particulars Year 1 Year 2 Year 3

Sales Unit £ 8000 £ 16000 £ 4000

Sales value (Unit * Selling Price) £ 240,000 £ 480,000 £ 120,000

Less: Cost (£ 130,000) (£ 225,000) (£ 130,000)

3

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contribution £ 110,000 £ 255,000 (£ 10,000)

Less: Marketing expenses (£ 60,000) (£ 40,000) -

Design & development cost (£ 300,000) - -

Net Profit (£ 250.000) £ 215,000 (£ 10,000)

From the above formulated budget, it has been analysed that in the initial year expected

performance of the organization is not good. In first year, they having loss of 250,000 because

most of the onetime expenses required to done. In second year performance, company generate

215,000 profits through selling 16,000 units of their games. In the last year, company generate

loss of 10,000 because sales units are 4000 which is very low. Overall, it has been concluded

that, it organization maximise the sales volume of their games then it will be beneficial for them

to maximise their profit margin.

In order to maximise their overall profit, Margrin Company need to boost the sales of

GFX game with the help of effective marketing or promotional strategy. In addition, try to

control or minimise their cost which automatically increase the profit margin. Currently,

expected performance of GFX game is not good because of unstable performance in terms of

profit.

3. Explain that why incremental budgeting is common method of budgeting and identify the

problems in this approach

Incremental budget is one of the most used budgets which help the organisations and

management to manage their activities (Gopal and Schnabl, 2020). This budget is prepared

by using the budget or actual results of the previous period as a basis for the inclusion of

incremental sums for the current budget period. The distribution of resources shall be based on

the previous year allocations of resources.

In addition, it promotes spending up to the budget to maintain a fair allocation for the next

cycle. It contributes to a "don't waste it or lose" attitude. The plan is sustainable and there is a

steady improvement. Managers are able to run their departments on a regular basis. This

budgeting system is relatively easy to build and simple to comprehend. Conflicts can be avoided

if agencies could be seen to be handled in the same way. Coordination among budgets is

4

Less: Marketing expenses (£ 60,000) (£ 40,000) -

Design & development cost (£ 300,000) - -

Net Profit (£ 250.000) £ 215,000 (£ 10,000)

From the above formulated budget, it has been analysed that in the initial year expected

performance of the organization is not good. In first year, they having loss of 250,000 because

most of the onetime expenses required to done. In second year performance, company generate

215,000 profits through selling 16,000 units of their games. In the last year, company generate

loss of 10,000 because sales units are 4000 which is very low. Overall, it has been concluded

that, it organization maximise the sales volume of their games then it will be beneficial for them

to maximise their profit margin.

In order to maximise their overall profit, Margrin Company need to boost the sales of

GFX game with the help of effective marketing or promotional strategy. In addition, try to

control or minimise their cost which automatically increase the profit margin. Currently,

expected performance of GFX game is not good because of unstable performance in terms of

profit.

3. Explain that why incremental budgeting is common method of budgeting and identify the

problems in this approach

Incremental budget is one of the most used budgets which help the organisations and

management to manage their activities (Gopal and Schnabl, 2020). This budget is prepared

by using the budget or actual results of the previous period as a basis for the inclusion of

incremental sums for the current budget period. The distribution of resources shall be based on

the previous year allocations of resources.

In addition, it promotes spending up to the budget to maintain a fair allocation for the next

cycle. It contributes to a "don't waste it or lose" attitude. The plan is sustainable and there is a

steady improvement. Managers are able to run their departments on a regular basis. This

budgeting system is relatively easy to build and simple to comprehend. Conflicts can be avoided

if agencies could be seen to be handled in the same way. Coordination among budgets is

4

sufficient to accomplish. The effect of changes can be easily seen or identified in this budgeting

method.

Due to above discussed reasons, incremental budgeting is common method but it also has

several problems which discussed below:

This strategy is not suggested as it does not take into consideration changing

circumstances which can further affect the final outcomes.

Incremental budgeting can lead to excessive expenditure for a business (Hertati and et.al.,

2020). The explanation for this is that, the departments within the same organisation

prefer to invest all the resources they have been allotted in the budget for one year in

order to acquire a higher sum of money during the next budgeting cycle.

This kind of budgeting may hinder the development of creative ideas and growth. As

current budgets are based on projections from previous budget.

The main principle within incremental budgets is continuous stability of business

performance. As a result, budgets are usually not reactive to future adjustments that may

result from unexpected events or other unforeseen factors.

The flexibility of incremental budgets will not provide any motivation to the management

of organisation to examine its budgets with a determination to having savings in

spending. The absence of a review process leaves budgets exposed to waste, inaccurate

assumptions and errors.

Question 2

1. Environmental management accounting

Role of environmental management accounting within modern business environment:

EMA is the production and review of monetary and non - monetary evidence to improve

internal environmental performance management. It complements the traditional framework for

financial management accounting with the goal of implementing effective processes to better

define and distribute environmental costs (Lee and Shin, 2018). The key fields of application for

EMA are commodity pricing, budgeting, expenditure estimation, cost measurement and savings

for environmental projects or the establishment of quantitative performance goals.

They interpreted EMA as just an extension of traditional accounting, which concerns

environmental effects of businesses assessed in monetary units and the organizational related

5

method.

Due to above discussed reasons, incremental budgeting is common method but it also has

several problems which discussed below:

This strategy is not suggested as it does not take into consideration changing

circumstances which can further affect the final outcomes.

Incremental budgeting can lead to excessive expenditure for a business (Hertati and et.al.,

2020). The explanation for this is that, the departments within the same organisation

prefer to invest all the resources they have been allotted in the budget for one year in

order to acquire a higher sum of money during the next budgeting cycle.

This kind of budgeting may hinder the development of creative ideas and growth. As

current budgets are based on projections from previous budget.

The main principle within incremental budgets is continuous stability of business

performance. As a result, budgets are usually not reactive to future adjustments that may

result from unexpected events or other unforeseen factors.

The flexibility of incremental budgets will not provide any motivation to the management

of organisation to examine its budgets with a determination to having savings in

spending. The absence of a review process leaves budgets exposed to waste, inaccurate

assumptions and errors.

Question 2

1. Environmental management accounting

Role of environmental management accounting within modern business environment:

EMA is the production and review of monetary and non - monetary evidence to improve

internal environmental performance management. It complements the traditional framework for

financial management accounting with the goal of implementing effective processes to better

define and distribute environmental costs (Lee and Shin, 2018). The key fields of application for

EMA are commodity pricing, budgeting, expenditure estimation, cost measurement and savings

for environmental projects or the establishment of quantitative performance goals.

They interpreted EMA as just an extension of traditional accounting, which concerns

environmental effects of businesses assessed in monetary units and the organizational related

5

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

influences on environmental structures expressed in metric quantities. EMA could be seen as

essential part of the environmental accounting system and described as 'use of financial and

material information for internal staff. Inside this framework, the various EMA strategies such as

ecological life cycle costing or environmental cost accounting can be defined and applied. The

administration of the Margrin Company may choose proper tools on the bases of their data

requirements. There are several roles plays by the EMA inside the modern business environment

and these are as follow:

Improving revenue or minimizing sales destruction: Customer perception of the

environmental effect of goods and services is gradually impacting their attitudes and

purchasing behaviour.

Cost reduction: Reducing the excessive use of production services has a positive direct

effect on cost reduction. Advancements to systems can also minimise costs.

Reducing failure costs: Engaging in systems that minimize the risk and cost effect of

failure, as well as the need to handle waste or start cleaning up environmental

consequences.

Improving the reputation of the organisation: This will make it easier to recruit good

skills, minimise talent turnover and charge a premium.

By using this environmental management accounting (EMA), Margrin Company can boost

their overall performance as well as minimise the cost through minimising wastage or advancing

technology. In addition, with the help of it organization is able to attract skilled people or it

improves business reputation (Pierce and Snyder, 2018). With the help of it, managers of

Margrin are able to identify environmental impacts, prospects for change and associated

financial impacts. Assign control of changes to people and agree on steps and goals. Develop

systems and processes for monitoring, evaluating and reporting on environmental results.

2. Explain the concepts of Total Quality Management and identify its features

Total Quality Management (TQM) is characterised as a model for management that

focuses on consumers and the production of products and services which meet requirements and

exceeding customer expectations. Total Quality Management (TQM) is a management

methodology that emerged in the 1950s which has become increasingly popular since before the

early 1980s. Total quality is a summary of the philosophy, attitude and organisation of a business

that aims to provide consumers with goods and services according to the needs. Culture means

6

essential part of the environmental accounting system and described as 'use of financial and

material information for internal staff. Inside this framework, the various EMA strategies such as

ecological life cycle costing or environmental cost accounting can be defined and applied. The

administration of the Margrin Company may choose proper tools on the bases of their data

requirements. There are several roles plays by the EMA inside the modern business environment

and these are as follow:

Improving revenue or minimizing sales destruction: Customer perception of the

environmental effect of goods and services is gradually impacting their attitudes and

purchasing behaviour.

Cost reduction: Reducing the excessive use of production services has a positive direct

effect on cost reduction. Advancements to systems can also minimise costs.

Reducing failure costs: Engaging in systems that minimize the risk and cost effect of

failure, as well as the need to handle waste or start cleaning up environmental

consequences.

Improving the reputation of the organisation: This will make it easier to recruit good

skills, minimise talent turnover and charge a premium.

By using this environmental management accounting (EMA), Margrin Company can boost

their overall performance as well as minimise the cost through minimising wastage or advancing

technology. In addition, with the help of it organization is able to attract skilled people or it

improves business reputation (Pierce and Snyder, 2018). With the help of it, managers of

Margrin are able to identify environmental impacts, prospects for change and associated

financial impacts. Assign control of changes to people and agree on steps and goals. Develop

systems and processes for monitoring, evaluating and reporting on environmental results.

2. Explain the concepts of Total Quality Management and identify its features

Total Quality Management (TQM) is characterised as a model for management that

focuses on consumers and the production of products and services which meet requirements and

exceeding customer expectations. Total Quality Management (TQM) is a management

methodology that emerged in the 1950s which has become increasingly popular since before the

early 1980s. Total quality is a summary of the philosophy, attitude and organisation of a business

that aims to provide consumers with goods and services according to the needs. Culture means

6

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

maintaining in all areas of the company's activities, with procedures being carried for the first

time and errors and waste being eliminated from activities. Constructing a customer-focused

environment and gathering and studying evidence which supports the consumer's efforts are key

components of the framework (Shaxson, 2018). This is achieved by a data-based, fact-based part

of the continuous improvement and an effective communication paradigm for the whole

organisation. by using this approach, managers of Margrin Company can improve quality of their

management which helps in maximising production as well as profitability.

There are several features which make total quality management approach most desirable

and some of it is as follow:

Customer focused: It is one of the major feature of TQM is to customer focused where

they take feedback from customers and further improve their performance or process to

improve their products & services quality.

Employee’s involvement: In order to resolve the problems, TQM understand that

employee’s involvement is essential to get better solution because they are directly

related with the process of producing products & services.

Process orientation: In an organization, everything has a process. If it is the process of

recruiting workers or the process of ordering raw material or designing something. There

are phases that take the lead. TQM organisations are reviewing steps in the process, fine-

tuning certain steps, and trying to remove unnecessary activities that could save money

and time.

Mutually dependent system: Many organisations have a variety of divisions or areas of

specialisation, but all have processes that facilitate the final distribution of goods.

Organizations that run TQM incorporate these internal processes to create a streamlined

method. For example, build training for all workers that demonstrates quality principles

and explains why they're doing it and explain the vision and purpose of the company.

Strategic approach: Businesses operating under the TQM model using several strategies

which helps to accomplish mission and vision (Taskforce, 2018). They create a strategic

strategy and using that as a foundation of their quality efforts and of all decision-making.

Take time to build a mission and vision statement and then use it to direct the

implementation of a growth strategy.

7

time and errors and waste being eliminated from activities. Constructing a customer-focused

environment and gathering and studying evidence which supports the consumer's efforts are key

components of the framework (Shaxson, 2018). This is achieved by a data-based, fact-based part

of the continuous improvement and an effective communication paradigm for the whole

organisation. by using this approach, managers of Margrin Company can improve quality of their

management which helps in maximising production as well as profitability.

There are several features which make total quality management approach most desirable

and some of it is as follow:

Customer focused: It is one of the major feature of TQM is to customer focused where

they take feedback from customers and further improve their performance or process to

improve their products & services quality.

Employee’s involvement: In order to resolve the problems, TQM understand that

employee’s involvement is essential to get better solution because they are directly

related with the process of producing products & services.

Process orientation: In an organization, everything has a process. If it is the process of

recruiting workers or the process of ordering raw material or designing something. There

are phases that take the lead. TQM organisations are reviewing steps in the process, fine-

tuning certain steps, and trying to remove unnecessary activities that could save money

and time.

Mutually dependent system: Many organisations have a variety of divisions or areas of

specialisation, but all have processes that facilitate the final distribution of goods.

Organizations that run TQM incorporate these internal processes to create a streamlined

method. For example, build training for all workers that demonstrates quality principles

and explains why they're doing it and explain the vision and purpose of the company.

Strategic approach: Businesses operating under the TQM model using several strategies

which helps to accomplish mission and vision (Taskforce, 2018). They create a strategic

strategy and using that as a foundation of their quality efforts and of all decision-making.

Take time to build a mission and vision statement and then use it to direct the

implementation of a growth strategy.

7

Above discussed features of TQM helps the Margrin Company to improve their quality

through focusing on customers and eliminate the non-valuable activities from the business

process.

3. Calculate the target cost of the Sims

Target costing: It is an accounting method in which businesses set cost goals compared to

market price and profit margin they expect to gain. Holding costs just below relevant goals helps

businesses produce income.

Given Information:

Selling price = £ 55

Profit margin = 30% of selling price

Formula:

Target Cost = Selling price – Profit margin (30% of selling price)

= £ 55 - £ 16.5

= £ 38.5

Target cost of the Sims is 38.5 per unit and 30% profit margin is enough for the

organization. Target costing can also be compared with cost-plus pricing, wherein firms set rates

by applying a profit margin to whichever costs they receive. Target costing is a much more

competitive strategy since it stresses performance in order to keep the business down. Target

costing is especially important for any organisation with low profit margins and strong

competition.

Target cost of “The Sims” video game is £ 38.5 which includes all the direct and indirect

expenses such as material cost, labour cost, machining cost, design and quality assurance cost

(Ye, Bian and Xu, 2018). In addition, for the marketing and distribution they have to spend

which is also included in the cost of making video game which deducted from the overall sakes

to identify target cost. Along with it, company also include the warranty cost which minimise

their profit but provide assurance to the customers regarding video game and they attract more.

CONCLUSION

From the above discussion it has been concluded that managing business performance is

very essential to done. It helps the organization to manager their business operational activities

by using principle of life cycle costing. In this principle, company able to evaluate their total cost

8

through focusing on customers and eliminate the non-valuable activities from the business

process.

3. Calculate the target cost of the Sims

Target costing: It is an accounting method in which businesses set cost goals compared to

market price and profit margin they expect to gain. Holding costs just below relevant goals helps

businesses produce income.

Given Information:

Selling price = £ 55

Profit margin = 30% of selling price

Formula:

Target Cost = Selling price – Profit margin (30% of selling price)

= £ 55 - £ 16.5

= £ 38.5

Target cost of the Sims is 38.5 per unit and 30% profit margin is enough for the

organization. Target costing can also be compared with cost-plus pricing, wherein firms set rates

by applying a profit margin to whichever costs they receive. Target costing is a much more

competitive strategy since it stresses performance in order to keep the business down. Target

costing is especially important for any organisation with low profit margins and strong

competition.

Target cost of “The Sims” video game is £ 38.5 which includes all the direct and indirect

expenses such as material cost, labour cost, machining cost, design and quality assurance cost

(Ye, Bian and Xu, 2018). In addition, for the marketing and distribution they have to spend

which is also included in the cost of making video game which deducted from the overall sakes

to identify target cost. Along with it, company also include the warranty cost which minimise

their profit but provide assurance to the customers regarding video game and they attract more.

CONCLUSION

From the above discussion it has been concluded that managing business performance is

very essential to done. It helps the organization to manager their business operational activities

by using principle of life cycle costing. In this principle, company able to evaluate their total cost

8

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

as well as sales which further help in building strategic strategies or managers also to made

effective decisions which helps in encouraging performance. Along with it, incremental

budgeting is one of the most common budgeting methods which are used by the organization due

to some specific features. But, this budgeting method also has several issues which cause the

final outcomes. Incremental budgeting is not flexible because it is unable to accept the changes

throughout the period which cause the results.

9

effective decisions which helps in encouraging performance. Along with it, incremental

budgeting is one of the most common budgeting methods which are used by the organization due

to some specific features. But, this budgeting method also has several issues which cause the

final outcomes. Incremental budgeting is not flexible because it is unable to accept the changes

throughout the period which cause the results.

9

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books & Journals

Alexandridis, G. and et.al., 2018. A survey of shipping finance research: Setting the future

research agenda. Transportation Research Part E: Logistics and Transportation

Review. 115. pp.164-212.

Chin, G. T. and Gallagher, K. P., 2019. Coordinated credit spaces: The globalization of Chinese

development finance. Development and change. 50(1). pp.245-274.

Fodor, P., 2020. The Business of State: Ottoman Finance Administration and Ruling Elites in

Transition (1580s-1615) (Vol. 28). de Gruyter.

Gopal, M. and Schnabl, P., 2020. The Rise of Finance Companies and FinTech Lenders in Small

Business Lending. Available at SSRN.

Hertati, L. and et.al., 2020. The Effects of Economic Crisis on Business Finance. International

Journal of Economics and Financial Issues. 10(3). pp.236-244.

Lee, I. and Shin, Y. J., 2018. Fintech: Ecosystem, business models, investment decisions, and

challenges. Business Horizons. 61(1). pp.35-46.

Pierce, L. and Snyder, J. A., 2018. The historical slave trade and firm access to finance in

Africa. The Review of Financial Studies. 31(1). pp.142-174.

Shaxson, N., 2018. The finance curse: How global finance is making us all poorer. Random

House.

Taskforce, B. F., 2018. Better finance, better world. Consultation Paper.

Ye, X., Bian, X. and Xu, Q., 2018, July. Empirical analysis and optimization for supply chain

finance business process based on Petri nets. In 2018 15th International Conference on

Service Systems and Service Management (ICSSSM) (pp. 1-6). IEEE.

10

Books & Journals

Alexandridis, G. and et.al., 2018. A survey of shipping finance research: Setting the future

research agenda. Transportation Research Part E: Logistics and Transportation

Review. 115. pp.164-212.

Chin, G. T. and Gallagher, K. P., 2019. Coordinated credit spaces: The globalization of Chinese

development finance. Development and change. 50(1). pp.245-274.

Fodor, P., 2020. The Business of State: Ottoman Finance Administration and Ruling Elites in

Transition (1580s-1615) (Vol. 28). de Gruyter.

Gopal, M. and Schnabl, P., 2020. The Rise of Finance Companies and FinTech Lenders in Small

Business Lending. Available at SSRN.

Hertati, L. and et.al., 2020. The Effects of Economic Crisis on Business Finance. International

Journal of Economics and Financial Issues. 10(3). pp.236-244.

Lee, I. and Shin, Y. J., 2018. Fintech: Ecosystem, business models, investment decisions, and

challenges. Business Horizons. 61(1). pp.35-46.

Pierce, L. and Snyder, J. A., 2018. The historical slave trade and firm access to finance in

Africa. The Review of Financial Studies. 31(1). pp.142-174.

Shaxson, N., 2018. The finance curse: How global finance is making us all poorer. Random

House.

Taskforce, B. F., 2018. Better finance, better world. Consultation Paper.

Ye, X., Bian, X. and Xu, Q., 2018, July. Empirical analysis and optimization for supply chain

finance business process based on Petri nets. In 2018 15th International Conference on

Service Systems and Service Management (ICSSSM) (pp. 1-6). IEEE.

10

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.