Detailed Report: Managing Business Performance with Costing Principles

VerifiedAdded on 2022/12/23

|12

|3162

|93

Report

AI Summary

This report delves into the application of costing principles within a business context, examining how these principles affect decision-making. It begins by exploring life cycle cost principles, detailing their phases and implications for a company launching new products. The report then analyzes budgeting, including calculations and the project life cycle phases, followed by an examination of incremental budgeting, its advantages, and disadvantages. Furthermore, it addresses the role of environmental management accounting (EMA) in modern businesses, emphasizing its importance in reducing environmental costs and utilizing by-products. The concept of Total Quality Management (TQM) is also discussed, outlining its features and strategic approach. Finally, the report touches upon target costing, providing a holistic view of how costing principles influence business performance and strategic decisions.

MANAGING BUSINESS

PERFORMANCE

PERFORMANCE

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................3

Life cycle cost principles............................................................................................................3

Budget.........................................................................................................................................4

Incremental budgeting.................................................................................................................5

Role of environmental management accounting within modern business environment.............6

Concept of Total Quality Management and its features..............................................................7

Target Cost..................................................................................................................................8

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................11

INTRODUCTION...........................................................................................................................3

Life cycle cost principles............................................................................................................3

Budget.........................................................................................................................................4

Incremental budgeting.................................................................................................................5

Role of environmental management accounting within modern business environment.............6

Concept of Total Quality Management and its features..............................................................7

Target Cost..................................................................................................................................8

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................11

INTRODUCTION

The study is on an organisation using costing principles and how they affect decision-making...

The study emphasises on the life cycle cost principles and its use for the organisation. It gives an

insight into budgeting being used by the company. It addresses questions on incremental budget

and drawbacks of it, environmental costing and quality management concept in organisation. It

emphasises on the implications of target costing for the organisation.

Life cycle cost principles

This is a method for assessment of total cost of facility ownership. It takes in account of

acquisition, owning and disposing of the assets. The principles of life cycle costing are:

a) This approach is basically a structured one which addresses all elements of cost.

b) The 4 phases of life cycle costing include:

i) Introduction: The product is launched in the market with product being released.

With the new product release, it is a high stake time in product’s life cycle which

make or breaks the product’s success in the market. The product promotion costs

are thus distributed here.

ii) Growth: This is the stage where customers buy the product and buy the products

on a momentum. The company’s costs can go on a low in marketing means

company reducing its costs in advertising and promotion to beat the competitors.

The costs are used then to increase the spread of logistics for product distribution

(Santos and et.al.,2020).

iii) Maturity: This is the stage where product reaches a maturity stage and this is a

sign of market saturation. This is the time when sales begin to drop. The pricing

tends to be competitive here at this stage.

iv) Decline: This stage sees the decline in the product sales and consumer behaviour

changes for the product. The company has to now face loss in market share of the

product and the demand fades away.

The study is on an organisation using costing principles and how they affect decision-making...

The study emphasises on the life cycle cost principles and its use for the organisation. It gives an

insight into budgeting being used by the company. It addresses questions on incremental budget

and drawbacks of it, environmental costing and quality management concept in organisation. It

emphasises on the implications of target costing for the organisation.

Life cycle cost principles

This is a method for assessment of total cost of facility ownership. It takes in account of

acquisition, owning and disposing of the assets. The principles of life cycle costing are:

a) This approach is basically a structured one which addresses all elements of cost.

b) The 4 phases of life cycle costing include:

i) Introduction: The product is launched in the market with product being released.

With the new product release, it is a high stake time in product’s life cycle which

make or breaks the product’s success in the market. The product promotion costs

are thus distributed here.

ii) Growth: This is the stage where customers buy the product and buy the products

on a momentum. The company’s costs can go on a low in marketing means

company reducing its costs in advertising and promotion to beat the competitors.

The costs are used then to increase the spread of logistics for product distribution

(Santos and et.al.,2020).

iii) Maturity: This is the stage where product reaches a maturity stage and this is a

sign of market saturation. This is the time when sales begin to drop. The pricing

tends to be competitive here at this stage.

iv) Decline: This stage sees the decline in the product sales and consumer behaviour

changes for the product. The company has to now face loss in market share of the

product and the demand fades away.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Coldarin has to follow these phases of life cycle as it will go under the same phase when

launching of new products.

The principles of cost break down structure in which the structure depends according to

purchasing decisions. The objective is related with identification of all cost elements which are

relevant. The structure of cost break down has to be capable of analysing costs specifically.

The cost estimation principle is necessary for computing the costs as per category. The company

Coldarin deals in developing and selling of games. The production costs and the quantity along

with procurement costs have to be computed (Santos and et.al.,2020).

Discounting principle is used to compare costs and benefits occurring in different intervals of

time where people would usually prefer to get goods and services rather than in future. Coldarin

also has to give such benefits to generate sales. The discounts and benefits depending on the

phase of the product life-cycle has to be judged and accordingly the discounts have to be given.

If the product is in maturity stage, company can try to give maximum discounts. The second

factor is of competitor’s strategy which has to be adhered in mind how they are providing offers

and when they are providing them (Gbededo, Liyanage and Garza-Reyes, 2018).

Budget

Volume of 10000 units=130000(cost)

Cost of 1 unit=130000/10000=13

Volume of 14000 units=150000(cost)

Cost of 1 unit=150000/14000=10.71

Fixed Cost Increase=50%

Let us suppose fixed cost to be half of 10.71 i.e. around 5.35.

Fixed cost increase=50% of 5.35i.e. 5.35+2.17=7.52.

Therefore, unit cost will be 13.23.

Design costs have already been written off earlier in income statement so the would not be

included in the budget.

launching of new products.

The principles of cost break down structure in which the structure depends according to

purchasing decisions. The objective is related with identification of all cost elements which are

relevant. The structure of cost break down has to be capable of analysing costs specifically.

The cost estimation principle is necessary for computing the costs as per category. The company

Coldarin deals in developing and selling of games. The production costs and the quantity along

with procurement costs have to be computed (Santos and et.al.,2020).

Discounting principle is used to compare costs and benefits occurring in different intervals of

time where people would usually prefer to get goods and services rather than in future. Coldarin

also has to give such benefits to generate sales. The discounts and benefits depending on the

phase of the product life-cycle has to be judged and accordingly the discounts have to be given.

If the product is in maturity stage, company can try to give maximum discounts. The second

factor is of competitor’s strategy which has to be adhered in mind how they are providing offers

and when they are providing them (Gbededo, Liyanage and Garza-Reyes, 2018).

Budget

Volume of 10000 units=130000(cost)

Cost of 1 unit=130000/10000=13

Volume of 14000 units=150000(cost)

Cost of 1 unit=150000/14000=10.71

Fixed Cost Increase=50%

Let us suppose fixed cost to be half of 10.71 i.e. around 5.35.

Fixed cost increase=50% of 5.35i.e. 5.35+2.17=7.52.

Therefore, unit cost will be 13.23.

Design costs have already been written off earlier in income statement so the would not be

included in the budget.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

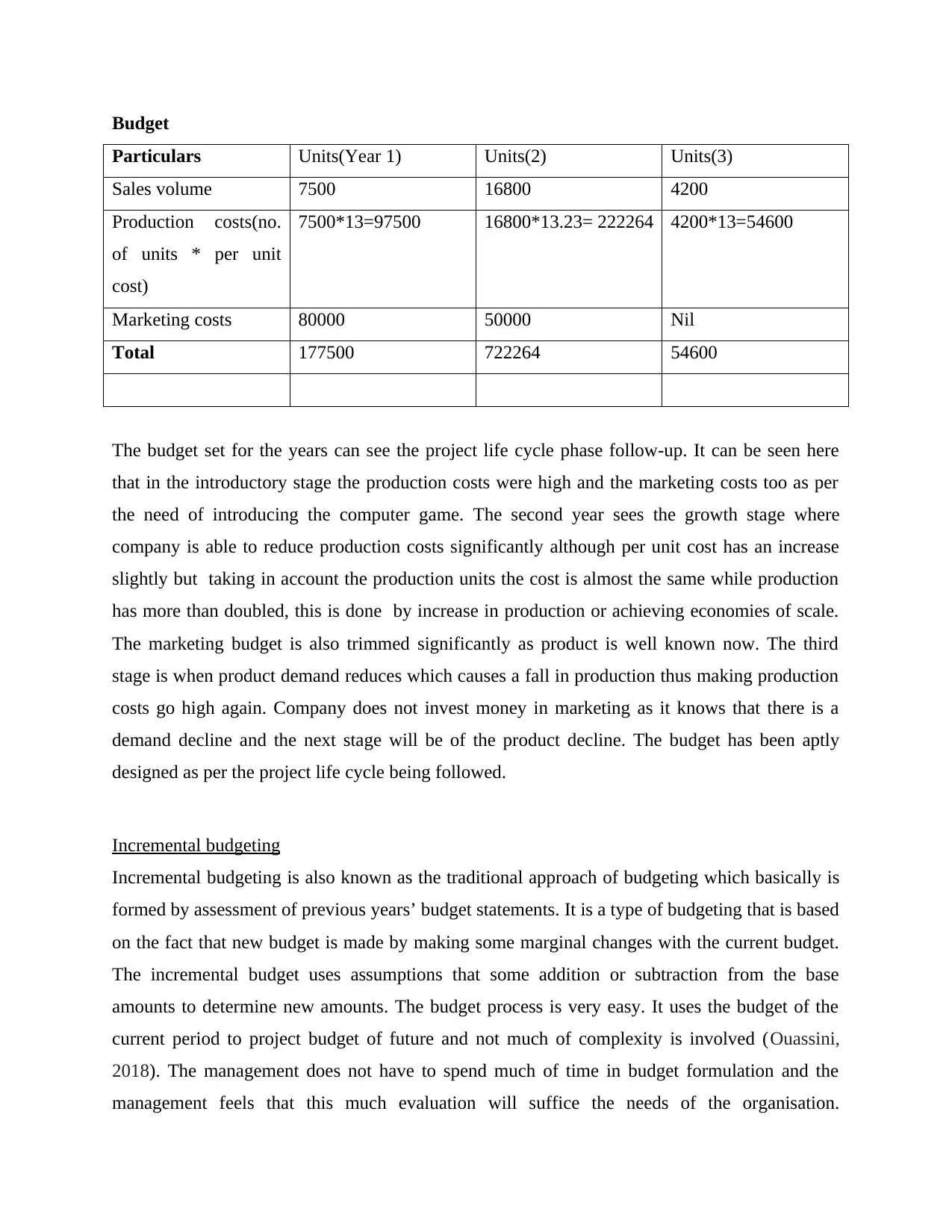

Budget

Particulars Units(Year 1) Units(2) Units(3)

Sales volume 7500 16800 4200

Production costs(no.

of units * per unit

cost)

7500*13=97500 16800*13.23= 222264 4200*13=54600

Marketing costs 80000 50000 Nil

Total 177500 722264 54600

The budget set for the years can see the project life cycle phase follow-up. It can be seen here

that in the introductory stage the production costs were high and the marketing costs too as per

the need of introducing the computer game. The second year sees the growth stage where

company is able to reduce production costs significantly although per unit cost has an increase

slightly but taking in account the production units the cost is almost the same while production

has more than doubled, this is done by increase in production or achieving economies of scale.

The marketing budget is also trimmed significantly as product is well known now. The third

stage is when product demand reduces which causes a fall in production thus making production

costs go high again. Company does not invest money in marketing as it knows that there is a

demand decline and the next stage will be of the product decline. The budget has been aptly

designed as per the project life cycle being followed.

Incremental budgeting

Incremental budgeting is also known as the traditional approach of budgeting which basically is

formed by assessment of previous years’ budget statements. It is a type of budgeting that is based

on the fact that new budget is made by making some marginal changes with the current budget.

The incremental budget uses assumptions that some addition or subtraction from the base

amounts to determine new amounts. The budget process is very easy. It uses the budget of the

current period to project budget of future and not much of complexity is involved (Ouassini,

2018). The management does not have to spend much of time in budget formulation and the

management feels that this much evaluation will suffice the needs of the organisation.

Particulars Units(Year 1) Units(2) Units(3)

Sales volume 7500 16800 4200

Production costs(no.

of units * per unit

cost)

7500*13=97500 16800*13.23= 222264 4200*13=54600

Marketing costs 80000 50000 Nil

Total 177500 722264 54600

The budget set for the years can see the project life cycle phase follow-up. It can be seen here

that in the introductory stage the production costs were high and the marketing costs too as per

the need of introducing the computer game. The second year sees the growth stage where

company is able to reduce production costs significantly although per unit cost has an increase

slightly but taking in account the production units the cost is almost the same while production

has more than doubled, this is done by increase in production or achieving economies of scale.

The marketing budget is also trimmed significantly as product is well known now. The third

stage is when product demand reduces which causes a fall in production thus making production

costs go high again. Company does not invest money in marketing as it knows that there is a

demand decline and the next stage will be of the product decline. The budget has been aptly

designed as per the project life cycle being followed.

Incremental budgeting

Incremental budgeting is also known as the traditional approach of budgeting which basically is

formed by assessment of previous years’ budget statements. It is a type of budgeting that is based

on the fact that new budget is made by making some marginal changes with the current budget.

The incremental budget uses assumptions that some addition or subtraction from the base

amounts to determine new amounts. The budget process is very easy. It uses the budget of the

current period to project budget of future and not much of complexity is involved (Ouassini,

2018). The management does not have to spend much of time in budget formulation and the

management feels that this much evaluation will suffice the needs of the organisation.

Incremental budgeting is based on assumptions that the conditions which had remained stable in

the previous years will continue for the next year also. The department wise budgeting can be

added according to some bit of inflation and the increasing need to move up production.

It is a common form of budgeting because the budget is simple, does not include much

research and calculations. The change in budget are gradual, managers can operate departments

consistently with making only a few changes. The budget is easy to understood by all sections

and coordination is easier to achieve. The funding stability is there in which the departments are

assured that they will be getting a budget increment every next year.

The disadvantages of incremental budgeting are:

a) It promotes unnecessary spending as departments spend all the money they have been

allocated. They do not save for next year as they know they will get money next year

again. It makes the budget less efficient optimally.

b) The budget discourages innovation as it does not go much into calculations and does not

assess the demand which has grown in market. It may happen that competitors are

coming with new products and it is time for company to invest in research and

development. But this budget overlooks the fact and does not give much space for

innovation (Ouassini, 2018).

c) The budget does not account for external factors that there may occur some unanticipated

changes in market which may lead to changes in tax structure, government policies etc.

d) They do not have comprehensive review regarding the budget and does not give any

incentives to company’s management and this is also not effective thus in saving

expenditures.

Role of environmental management accounting within modern business environment

Environmental management accounting (EMA) is being defined as the process of

identification and collection and analysis of two types of information for internal decision

making. This information involves the first physical information and the second monetary

information. The physical information relates with the use and flow of the energy, water and

other resources within the company (Environmental management accounting (EMA), 2021). On

the other side, monetary information relates to environment related cost and earning and savings.

the previous years will continue for the next year also. The department wise budgeting can be

added according to some bit of inflation and the increasing need to move up production.

It is a common form of budgeting because the budget is simple, does not include much

research and calculations. The change in budget are gradual, managers can operate departments

consistently with making only a few changes. The budget is easy to understood by all sections

and coordination is easier to achieve. The funding stability is there in which the departments are

assured that they will be getting a budget increment every next year.

The disadvantages of incremental budgeting are:

a) It promotes unnecessary spending as departments spend all the money they have been

allocated. They do not save for next year as they know they will get money next year

again. It makes the budget less efficient optimally.

b) The budget discourages innovation as it does not go much into calculations and does not

assess the demand which has grown in market. It may happen that competitors are

coming with new products and it is time for company to invest in research and

development. But this budget overlooks the fact and does not give much space for

innovation (Ouassini, 2018).

c) The budget does not account for external factors that there may occur some unanticipated

changes in market which may lead to changes in tax structure, government policies etc.

d) They do not have comprehensive review regarding the budget and does not give any

incentives to company’s management and this is also not effective thus in saving

expenditures.

Role of environmental management accounting within modern business environment

Environmental management accounting (EMA) is being defined as the process of

identification and collection and analysis of two types of information for internal decision

making. This information involves the first physical information and the second monetary

information. The physical information relates with the use and flow of the energy, water and

other resources within the company (Environmental management accounting (EMA), 2021). On

the other side, monetary information relates to environment related cost and earning and savings.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

EMA is a concept which addresses the management information needs required by a manager for

undertaking corporate activities which affect the environment and environment related aspects.

Hence, in this modern business where the consumer and the business pays a lot more

emphasis over the protection of the environment so it is the duty of the companies that they

undertake EMA. This is particularly because of the reason that when the company will undertake

the principles of EMA then it means that company will include the cost relating to environment

and its activities. The major role that EMA plays in the modern business organizations is that all

the major environmental costs can be reduced or eliminated by the company. This is particularly

because of the reason that when the company undertakes the use of the EMA then they minimize

the cost relating to the environment and this reduces this cost.

In addition to this, another major role of the EMA in companies is that with help of this

accounting many of the by- products of the company can be utilised and this can assist company

in earning more profit. Earlier these products were not used but after the implementation of the

EMA the importance of these by- products have been highlighted and these are also used in some

or the productive manner (Latan and et.al., 2018). Moreover, another major role which EMA

plays within the proper functioning of the company is that this assist companies in understanding

the different types of environmental cost and its impact over production of companies. This is

helpful to the company as when the company will know the fact that how the environmental cost

assist in proper management of the business then it is not risky for the company to invest in those

cost and this will improve the production and management system of the company only.

Concept of Total Quality Management and its features

TQM that is total quality management is being defined as the model which assists the

company in focusing on the consumer need and development of the product and service in

accordance with the requirement of consumers. This is being done by creating an integrated

system which is process centred and involve employee involvement and is completely customer

centred. Here the major focus is being laid over the quality of the product and service so that it is

liked by the consumer to a great extent (Pambreni and et.al., 2019). The major features of this

system are as follows-

Customer focused- this is the top most features which involves a major focus over

fulfilling the need and requirement of the consumers.

undertaking corporate activities which affect the environment and environment related aspects.

Hence, in this modern business where the consumer and the business pays a lot more

emphasis over the protection of the environment so it is the duty of the companies that they

undertake EMA. This is particularly because of the reason that when the company will undertake

the principles of EMA then it means that company will include the cost relating to environment

and its activities. The major role that EMA plays in the modern business organizations is that all

the major environmental costs can be reduced or eliminated by the company. This is particularly

because of the reason that when the company undertakes the use of the EMA then they minimize

the cost relating to the environment and this reduces this cost.

In addition to this, another major role of the EMA in companies is that with help of this

accounting many of the by- products of the company can be utilised and this can assist company

in earning more profit. Earlier these products were not used but after the implementation of the

EMA the importance of these by- products have been highlighted and these are also used in some

or the productive manner (Latan and et.al., 2018). Moreover, another major role which EMA

plays within the proper functioning of the company is that this assist companies in understanding

the different types of environmental cost and its impact over production of companies. This is

helpful to the company as when the company will know the fact that how the environmental cost

assist in proper management of the business then it is not risky for the company to invest in those

cost and this will improve the production and management system of the company only.

Concept of Total Quality Management and its features

TQM that is total quality management is being defined as the model which assists the

company in focusing on the consumer need and development of the product and service in

accordance with the requirement of consumers. This is being done by creating an integrated

system which is process centred and involve employee involvement and is completely customer

centred. Here the major focus is being laid over the quality of the product and service so that it is

liked by the consumer to a great extent (Pambreni and et.al., 2019). The major features of this

system are as follows-

Customer focused- this is the top most features which involves a major focus over

fulfilling the need and requirement of the consumers.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Involves employees- this is another feature of TQM which states that for providing top

quality services to the consumer total involvement of the employees is very essential.

This is particularly because of the reason that if employees will not be focused towards

work then this will affect the quality of the product and service.

Process oriented- this is another feature which states that if the process of the company is

not followed then this will definitely affect the working and quality of the product and

service. Hence, the process needs to be simple and easy so that quality is provided to

consumers.

Mutually dependent system- this is also an important feature of the TQM as when the

system is mutually dependent over one another than this will result in better output for

the consumers.

Continuous improvement- this feature of TQM states that when the company will have a

major focus over the quality then this will definitely result in continuous improvement of

the product and services of company. Hence, this continuous improvement will result in

attracting majority of the consumers (What is Total Quality Management (TQM)? 2021).

Strategic approach- for focusing on TQM it is essential for the business to have a major

focus on the strategic approach. In simple words it means that it is essential for the

company to provide for proper mission and vision so that TQM can be managed in

effective and efficient manner.

Target Cost

As, Profit margin= 20% of 60=12

Target cost=Selling price-Profit Margin

=60-12=48

Implications of Target costing

a) It helps in determining the price of the product by market conditions.

b) Profit margin is included in target selling price.

c) It will help management to focus on reduction of costs and effective management of

costs.

quality services to the consumer total involvement of the employees is very essential.

This is particularly because of the reason that if employees will not be focused towards

work then this will affect the quality of the product and service.

Process oriented- this is another feature which states that if the process of the company is

not followed then this will definitely affect the working and quality of the product and

service. Hence, the process needs to be simple and easy so that quality is provided to

consumers.

Mutually dependent system- this is also an important feature of the TQM as when the

system is mutually dependent over one another than this will result in better output for

the consumers.

Continuous improvement- this feature of TQM states that when the company will have a

major focus over the quality then this will definitely result in continuous improvement of

the product and services of company. Hence, this continuous improvement will result in

attracting majority of the consumers (What is Total Quality Management (TQM)? 2021).

Strategic approach- for focusing on TQM it is essential for the business to have a major

focus on the strategic approach. In simple words it means that it is essential for the

company to provide for proper mission and vision so that TQM can be managed in

effective and efficient manner.

Target Cost

As, Profit margin= 20% of 60=12

Target cost=Selling price-Profit Margin

=60-12=48

Implications of Target costing

a) It helps in determining the price of the product by market conditions.

b) Profit margin is included in target selling price.

c) It will help management to focus on reduction of costs and effective management of

costs.

d) Difference between the current and target costs is the cost reduction which is the aim of

management.

e) The team formed integrates activities like designing, manufacturing, marketing etc.

which helps in achieving target cost.

There are advantages of target costing which include:

a) The commitment for improving processes and innovation in products is shown in this

process by management.

b) The cost has to be brought to the expectations of customers and management aim is

achieved if customer feels the value is delivered.

c) The company’s operations also improve drastically with company achieving

economies of scale.

d) The approach to designing and manufacturing products becomes as per target cost

and market driven.

e) The market opportunities can be converted in savings to achieve value for money and

saving costs.

f) Target costing thus helps in product development and improving sales prospects. It

will help Coldarin achieve sales with reduced costs and better sales. The cost and

efforts of managing the product life cycle will get reduced and ultimately benefit the

company (Dăneci-Pătrău and Coca, 2017).

g) It will also assure for the company that profitability targets for product portfolio are

achieved.

h) Coldarin will be able to gain a competitive advantage with continual improvement in

process of cost reduction.

i) Coldarin will also be able to offer value to the stakeholders of the company as the

internal stakeholders will get value for their money.

However, the system can have some drawbacks too as follows:

a) The process of development can be lengthy as the product will have to go through

alterations which will be able to meet the target cost.

management.

e) The team formed integrates activities like designing, manufacturing, marketing etc.

which helps in achieving target cost.

There are advantages of target costing which include:

a) The commitment for improving processes and innovation in products is shown in this

process by management.

b) The cost has to be brought to the expectations of customers and management aim is

achieved if customer feels the value is delivered.

c) The company’s operations also improve drastically with company achieving

economies of scale.

d) The approach to designing and manufacturing products becomes as per target cost

and market driven.

e) The market opportunities can be converted in savings to achieve value for money and

saving costs.

f) Target costing thus helps in product development and improving sales prospects. It

will help Coldarin achieve sales with reduced costs and better sales. The cost and

efforts of managing the product life cycle will get reduced and ultimately benefit the

company (Dăneci-Pătrău and Coca, 2017).

g) It will also assure for the company that profitability targets for product portfolio are

achieved.

h) Coldarin will be able to gain a competitive advantage with continual improvement in

process of cost reduction.

i) Coldarin will also be able to offer value to the stakeholders of the company as the

internal stakeholders will get value for their money.

However, the system can have some drawbacks too as follows:

a) The process of development can be lengthy as the product will have to go through

alterations which will be able to meet the target cost.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

b) The approach requires agreement of several people of various departments as this

strategy will be affecting the company as a whole, thus everybody has to agree to the

strategy.

c) This requires hard work for the project team to reach the target cost (Dăneci-Pătrău,

and Coca, 2017).

d) There can be issues of inferiority in the product quality to meet the target costing set.

Quality has to be maintained as it can demotivate the internal stakeholders and the

customers.

CONCLUSION

The study concludes that costing principles can have merits but drawbacks as well which the

organisation has to deal with. Nevertheless, an organisation using a sum total approach will

always find it to take the right business decisions. The company will benefit by using these

principles in cost reduction as well as cost optimisation. These decisions will affect the investors

positively too leading to its growth.

strategy will be affecting the company as a whole, thus everybody has to agree to the

strategy.

c) This requires hard work for the project team to reach the target cost (Dăneci-Pătrău,

and Coca, 2017).

d) There can be issues of inferiority in the product quality to meet the target costing set.

Quality has to be maintained as it can demotivate the internal stakeholders and the

customers.

CONCLUSION

The study concludes that costing principles can have merits but drawbacks as well which the

organisation has to deal with. Nevertheless, an organisation using a sum total approach will

always find it to take the right business decisions. The company will benefit by using these

principles in cost reduction as well as cost optimisation. These decisions will affect the investors

positively too leading to its growth.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and Journals

Abbas, J., 2020. Impact of total quality management on corporate green performance through the

mediating role of corporate social responsibility. Journal of Cleaner Production, 242,

p.118458.

Dăneci-Pătrău, D. and Coca, C.E., 2017. METHODOLOGICAL CONSIDERATIONS ON THE

PROCESS OF DETERMINING THE TARGET COST. Economics, Management &

Financial Markets, 12(2).

Gbededo, M.A., Liyanage, K. and Garza-Reyes, J.A., 2018. Towards a Life Cycle Sustainability

Analysis: A systematic review of approaches to sustainable manufacturing. Journal of

Cleaner Production, 184, pp.1002-1015.

Gibassier, D. and Alcouffe, S., 2018. Environmental management accounting: the missing link to

sustainability?.

Hamdan, M., Chen, C.K. and Anshari, M., 2020, November. Decision Aid in Budgeting Systems

for Small & Medium Enterprises. In 2020 International Conference on Decision Aid

Sciences and Application (DASA) (pp. 253-257). IEEE.

Latan, H. and et.al., 2018. Effects of environmental strategy, environmental uncertainty and top

management's commitment on corporate environmental performance: The role of

environmental management accounting. Journal of Cleaner Production, 180, pp.297-306.

Latan, H., and et.al., 2018. Effects of environmental strategy, environmental uncertainty and top

management's commitment on corporate environmental performance: The role of

environmental management accounting. Journal of Cleaner Production, 180, pp.297-

306.

Ouassini, I., 2018. An introduction to the concept of Incremental Budgeting and Beyond

Budgeting. Available at SSRN 3140059.

Pambreni, Y. and et.al., 2019. The influence of total quality management toward organization

performance. Management Science Letters, 9(9), pp.1397-1406.

Pambreni, Y., and et.al., 2019. The influence of total quality management toward organization

performance. Management Science Letters, 9(9), pp.1397-1406.

Santos, R. and et.al.,2020. BIM-based life cycle assessment and life cycle costing of an office

building in Western Europe. Building and Environment, 169, p.106568.

Online

Environmental management accounting (EMA). 2021. [Online]. Available through: <

https://www.cgma.org/resources/tools/cost-transformation-model/environmental-

management-accounting.html >

What is Total Quality Management (TQM)? 2021. [Online]. Available through: <

https://thethrivingsmallbusiness.com/benefits-of-total-quality-management-tqm/ >

Books and Journals

Abbas, J., 2020. Impact of total quality management on corporate green performance through the

mediating role of corporate social responsibility. Journal of Cleaner Production, 242,

p.118458.

Dăneci-Pătrău, D. and Coca, C.E., 2017. METHODOLOGICAL CONSIDERATIONS ON THE

PROCESS OF DETERMINING THE TARGET COST. Economics, Management &

Financial Markets, 12(2).

Gbededo, M.A., Liyanage, K. and Garza-Reyes, J.A., 2018. Towards a Life Cycle Sustainability

Analysis: A systematic review of approaches to sustainable manufacturing. Journal of

Cleaner Production, 184, pp.1002-1015.

Gibassier, D. and Alcouffe, S., 2018. Environmental management accounting: the missing link to

sustainability?.

Hamdan, M., Chen, C.K. and Anshari, M., 2020, November. Decision Aid in Budgeting Systems

for Small & Medium Enterprises. In 2020 International Conference on Decision Aid

Sciences and Application (DASA) (pp. 253-257). IEEE.

Latan, H. and et.al., 2018. Effects of environmental strategy, environmental uncertainty and top

management's commitment on corporate environmental performance: The role of

environmental management accounting. Journal of Cleaner Production, 180, pp.297-306.

Latan, H., and et.al., 2018. Effects of environmental strategy, environmental uncertainty and top

management's commitment on corporate environmental performance: The role of

environmental management accounting. Journal of Cleaner Production, 180, pp.297-

306.

Ouassini, I., 2018. An introduction to the concept of Incremental Budgeting and Beyond

Budgeting. Available at SSRN 3140059.

Pambreni, Y. and et.al., 2019. The influence of total quality management toward organization

performance. Management Science Letters, 9(9), pp.1397-1406.

Pambreni, Y., and et.al., 2019. The influence of total quality management toward organization

performance. Management Science Letters, 9(9), pp.1397-1406.

Santos, R. and et.al.,2020. BIM-based life cycle assessment and life cycle costing of an office

building in Western Europe. Building and Environment, 169, p.106568.

Online

Environmental management accounting (EMA). 2021. [Online]. Available through: <

https://www.cgma.org/resources/tools/cost-transformation-model/environmental-

management-accounting.html >

What is Total Quality Management (TQM)? 2021. [Online]. Available through: <

https://thethrivingsmallbusiness.com/benefits-of-total-quality-management-tqm/ >

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.