MGT723 Research Project Semester 2 2017: Carbon Emission Disclosure

VerifiedAdded on 2020/04/07

|8

|1755

|90

Project

AI Summary

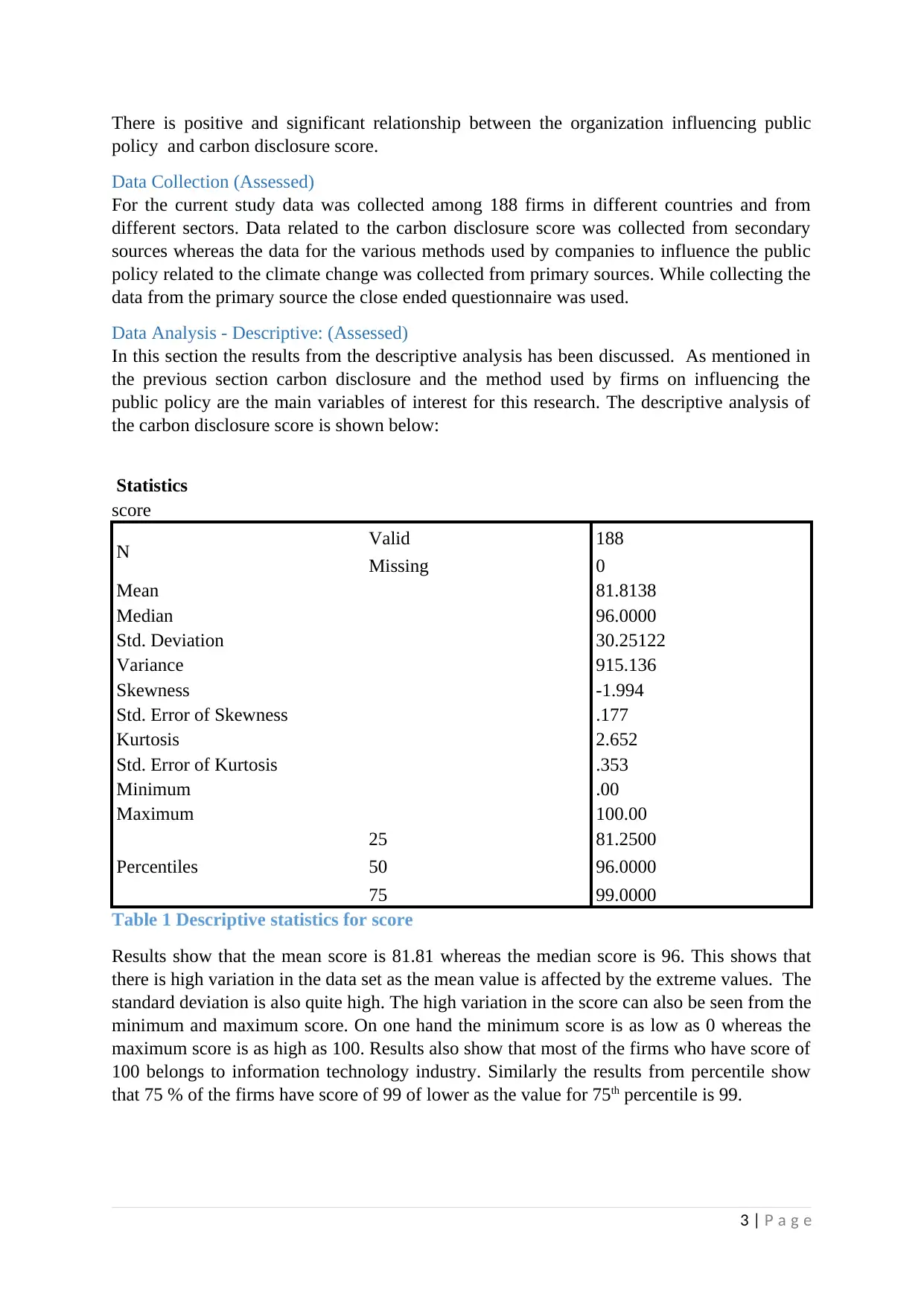

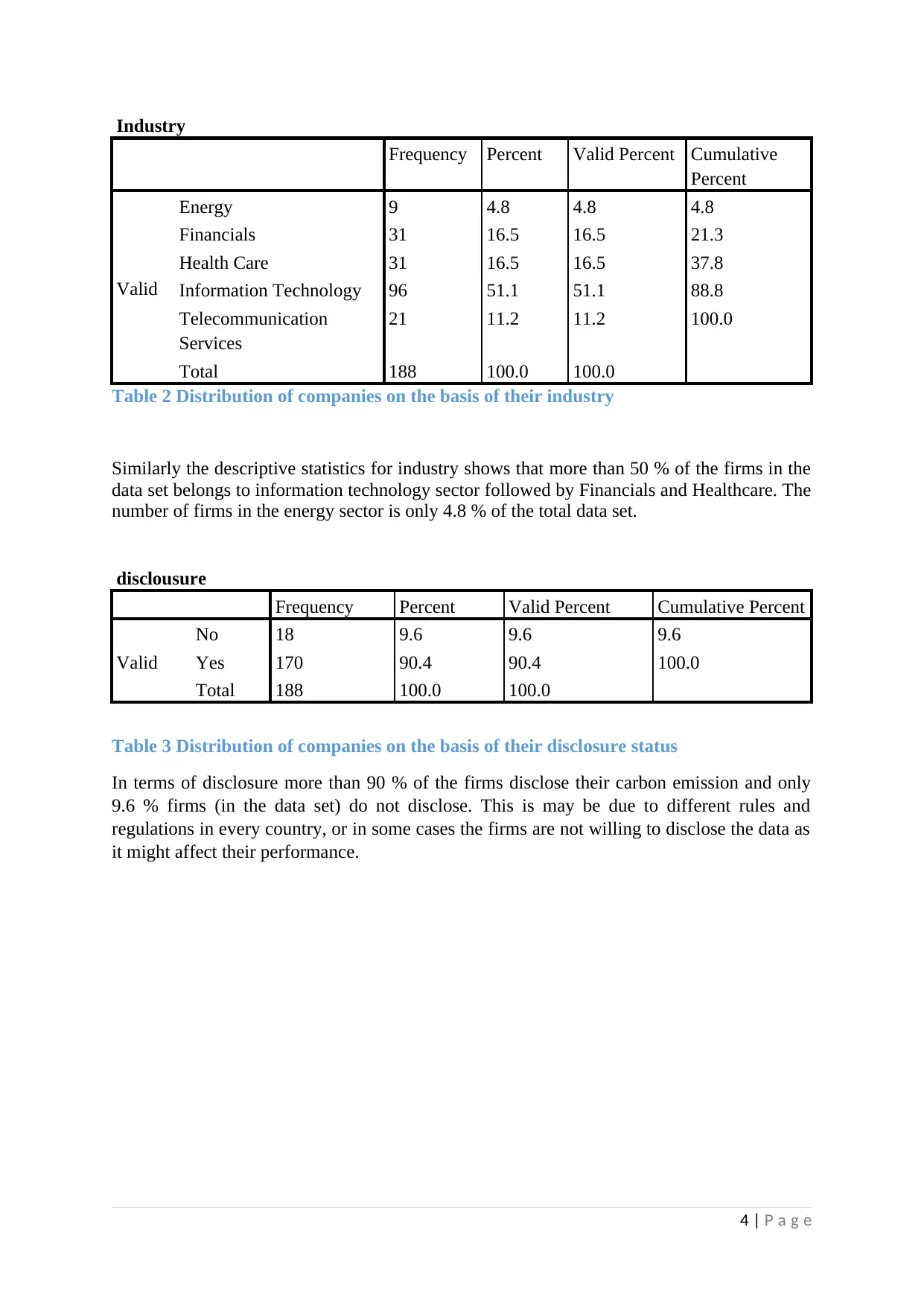

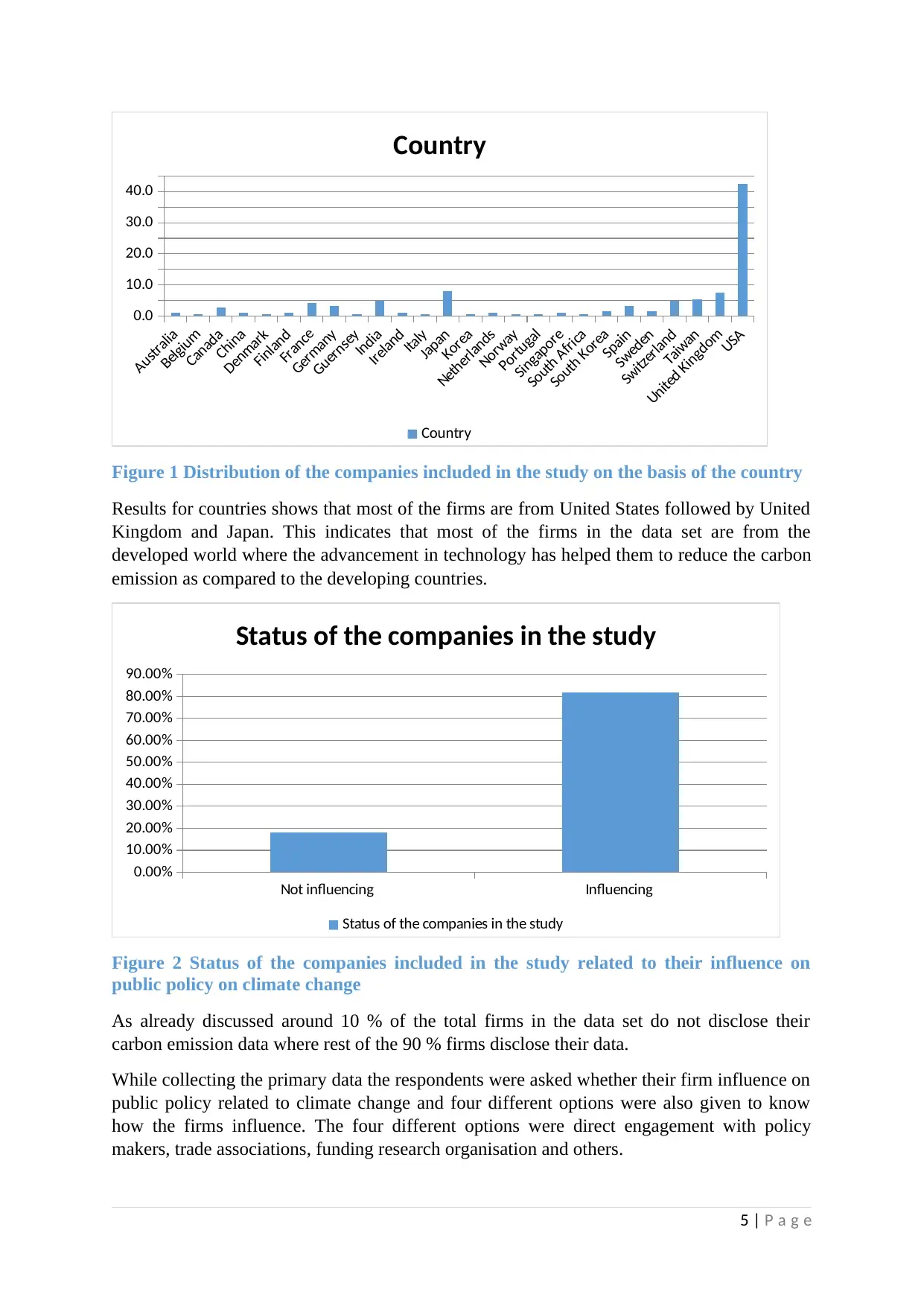

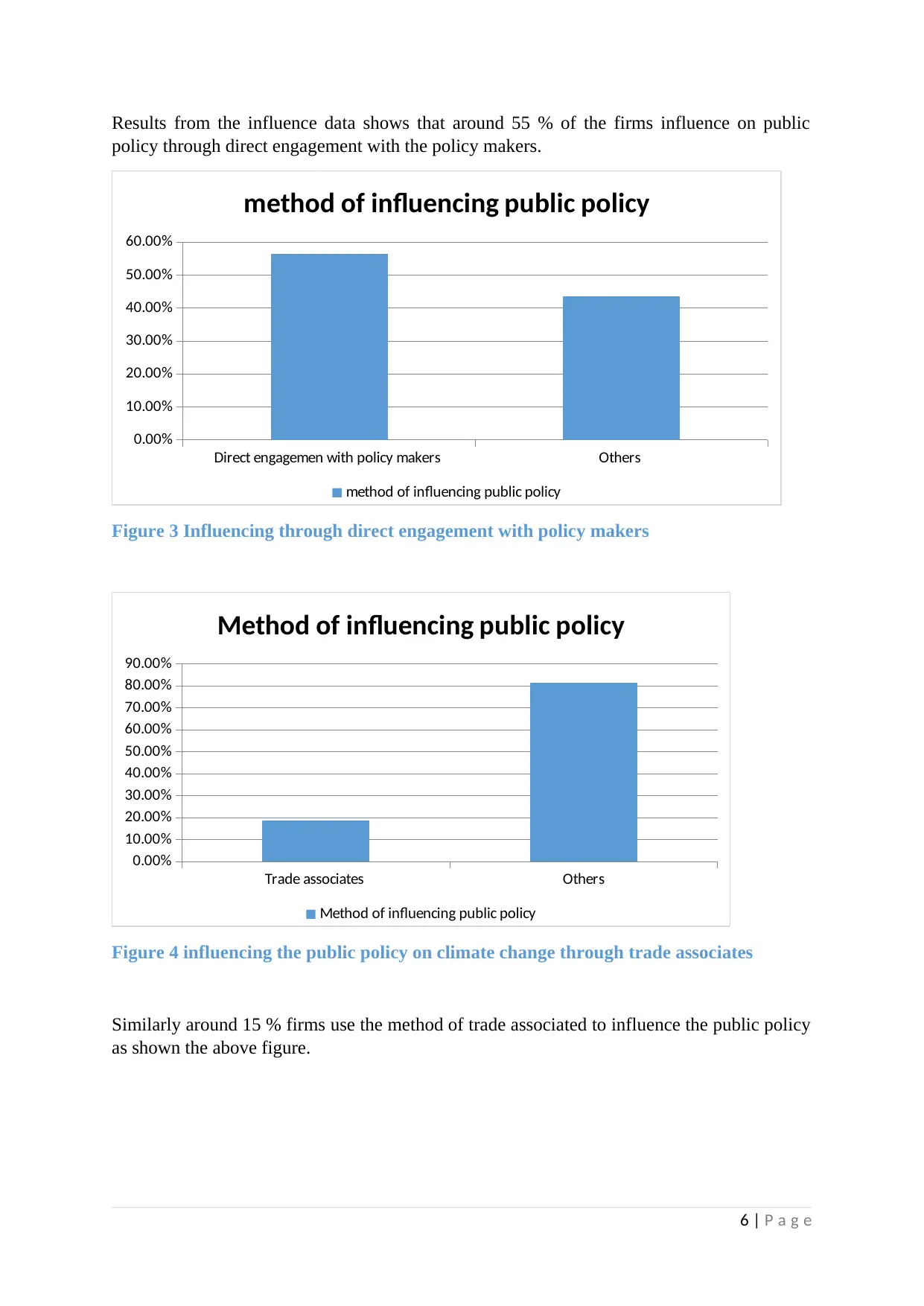

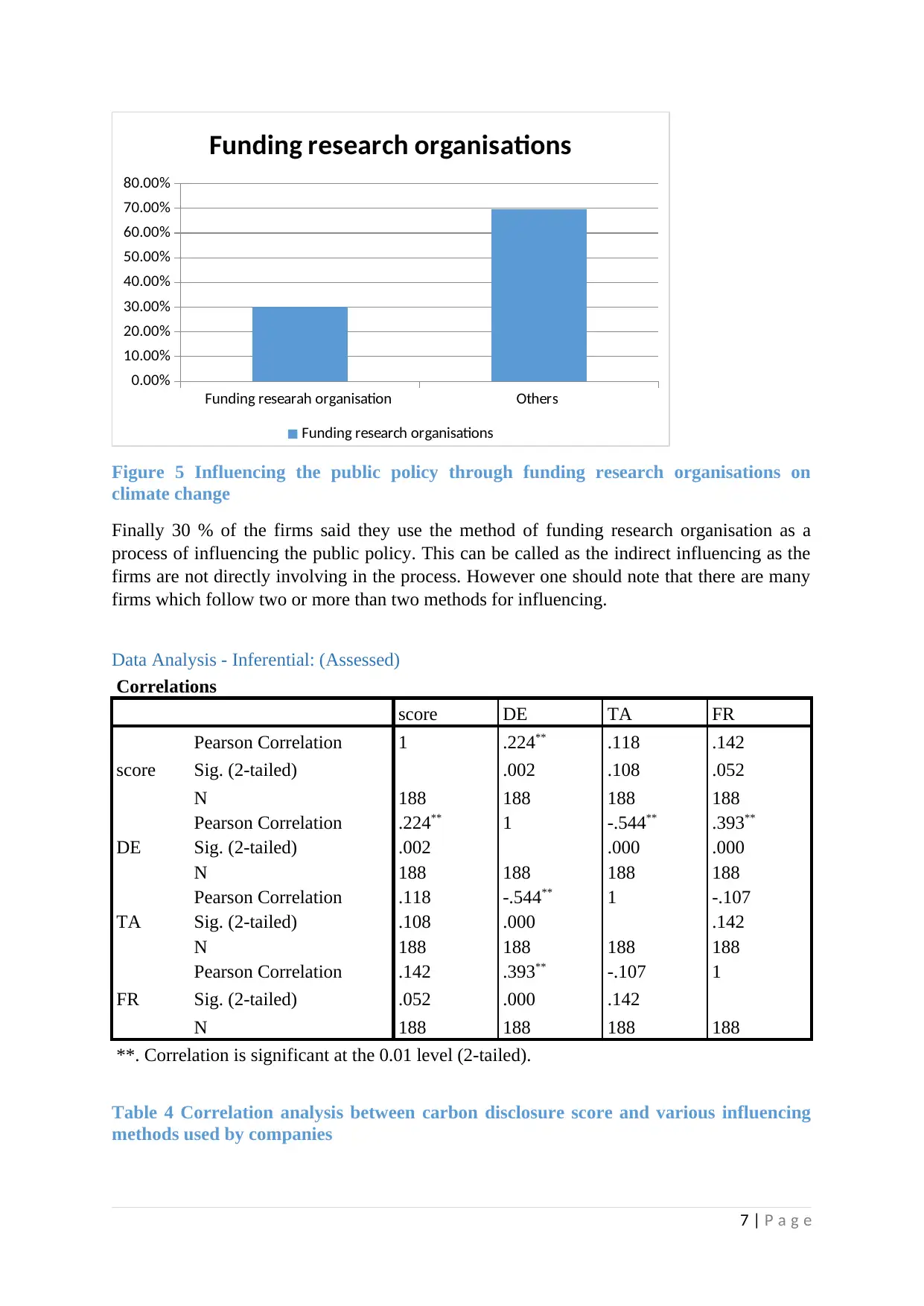

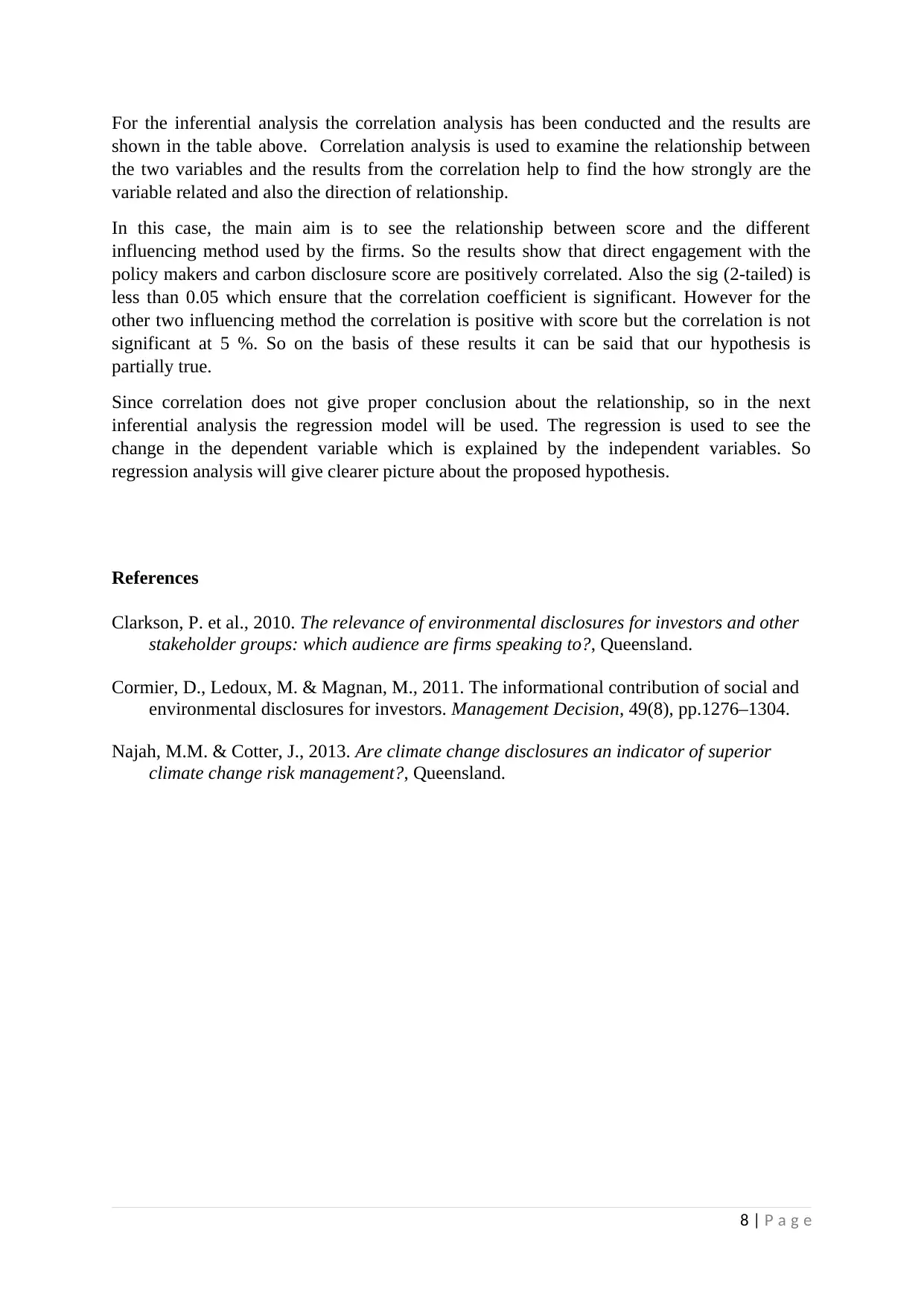

This research project, for MGT723, investigates the relationship between carbon disclosure scores and how organizations influence public policy related to climate change. The study analyzes data from 188 firms across different countries and sectors, collected through secondary sources for carbon disclosure scores and primary sources via questionnaires for influencing methods. The research employs descriptive statistics to analyze the carbon disclosure score, revealing a high variation in the data, and examines the distribution of companies across industries and their disclosure status. Inferential analysis, using correlation analysis, explores the relationships between carbon disclosure and various influencing methods, such as direct engagement with policy makers, trade associations, and funding research organizations. The findings indicate a positive correlation between direct engagement and carbon disclosure scores, providing insights into the complex dynamics between environmental performance and public policy influence.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.