MGT723 Research Project: Carbon Disclosure and Industry Performance

VerifiedAdded on 2021/05/31

|11

|1870

|33

Report

AI Summary

This research project, identified as MGT723, investigates the impact of voluntary carbon disclosure and carbon emissions on organizational performance. The study utilizes data from the Carbon Disclosure Project (CDP) survey, encompassing 306 organizations. The project formulates hypotheses, detailing the data collection process, which includes disclosure scores, carbon emission scopes, and organizational initiatives. The analysis employs descriptive statistics, correlation analysis, and the Mann-Whitney U Test, with results presented through tables and figures. The findings reveal a weak negative correlation between carbon emissions and disclosure scores, alongside an insignificant relationship. The report concludes with references to relevant literature.

Running Head: MGT723 RESEARCH PROJECT

MGT723 Research Project

Legitimacy Theory and Carbon Disclosure

Name of the Student

Name of the University

Author Note

MGT723 Research Project

Legitimacy Theory and Carbon Disclosure

Name of the Student

Name of the University

Author Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1MGT723 RESEARCH PROJECT

Table of Contents

Introduction................................................................................................................................2

Conceptual Framework..............................................................................................................2

Hypothesis..................................................................................................................................2

Data Collection...........................................................................................................................3

Data Analysis – Descriptive.......................................................................................................4

Descriptive Statistics..............................................................................................................5

Inferential Statistics....................................................................................................................8

References................................................................................................................................10

Table of Contents

Introduction................................................................................................................................2

Conceptual Framework..............................................................................................................2

Hypothesis..................................................................................................................................2

Data Collection...........................................................................................................................3

Data Analysis – Descriptive.......................................................................................................4

Descriptive Statistics..............................................................................................................5

Inferential Statistics....................................................................................................................8

References................................................................................................................................10

2MGT723 RESEARCH PROJECT

Introduction

This is a research project where the main interest of the study is assessing the impact

of voluntary disclosure and carbon emission on the performance of the organization

(Albertini 2013). This is a new concept and assessment of the actions to be taken in the future

in order to manage the risks and the opportunities to the organization is done with the help of

quantitative analysis (Saka & Oshika 2014). The data collection and the analysis and

interpretation of the data is presented in this report. Analysis will be conducted with the help

of SPSS. Analysis will be conducted based on the information collected from 306

organizations on 2015.

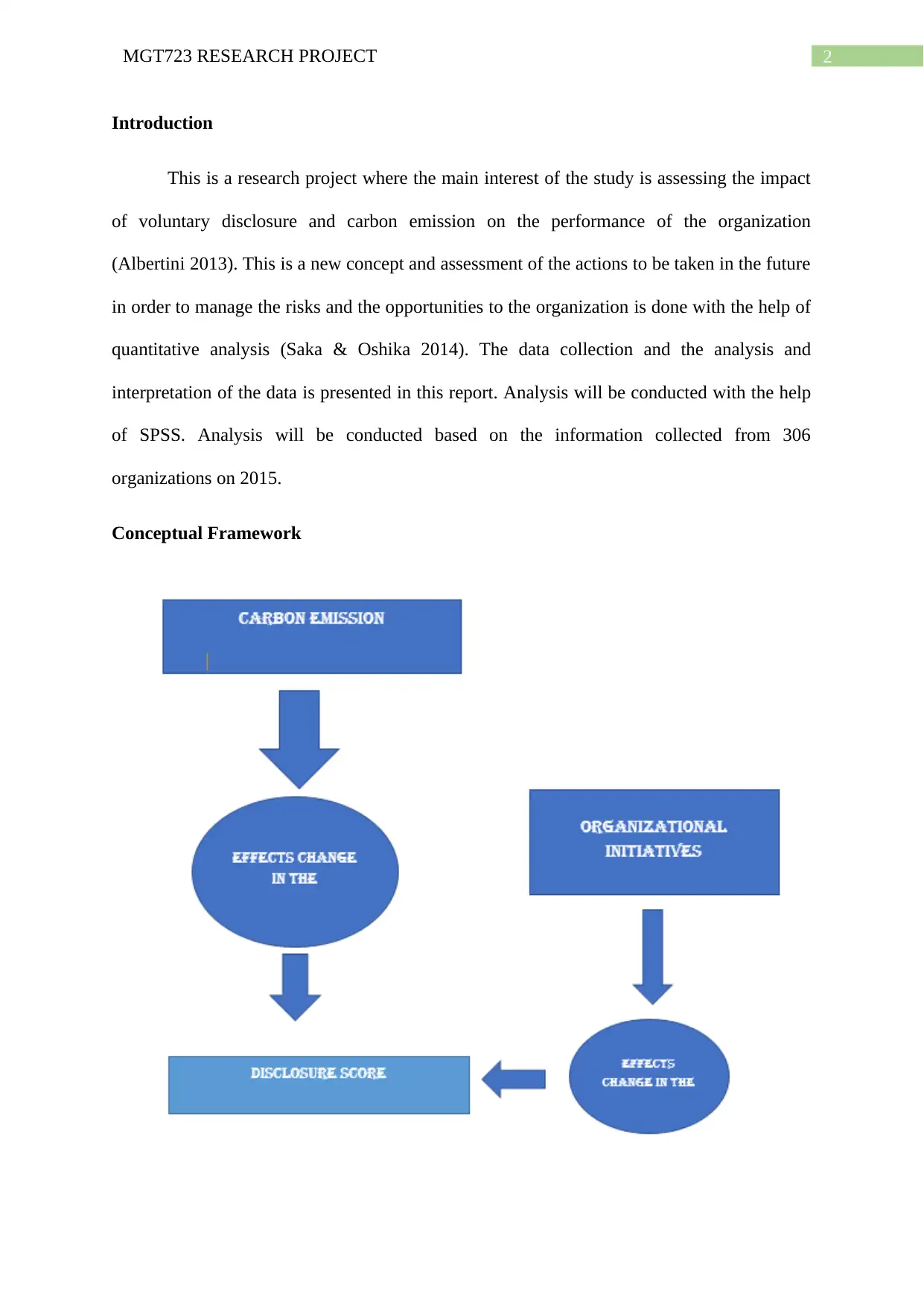

Conceptual Framework

Introduction

This is a research project where the main interest of the study is assessing the impact

of voluntary disclosure and carbon emission on the performance of the organization

(Albertini 2013). This is a new concept and assessment of the actions to be taken in the future

in order to manage the risks and the opportunities to the organization is done with the help of

quantitative analysis (Saka & Oshika 2014). The data collection and the analysis and

interpretation of the data is presented in this report. Analysis will be conducted with the help

of SPSS. Analysis will be conducted based on the information collected from 306

organizations on 2015.

Conceptual Framework

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3MGT723 RESEARCH PROJECT

Hypothesis

The null and the alternate hypothesis on the basis of this research study can be stated

as follows:

Null Hypothesis (H0): No significant relationship exists between the industry performance

based on voluntary disclosure and carbon emission

Alternate Hypothesis (HA): Significant relationship exists between the industry performance

based on voluntary disclosure and carbon emission

Data Collection

The dataset contains information about 306 selected organizations that have

participated in the Carbon Disclosure Project survey. These information was collected as a

result of the CDP (Carbon Disclosure project) survey. The respective data have been

collected from the companies in terms of disclosure scores, scopes of carbon emissions and

initiatives taken by the organization. The results of the analysis have to be generalized as the

collected information id for 2015 while the recorded disclosure scores are from 2012 – 2015

(Luo, Lan & Tang 2012).

The whole dataset is available from the CDP survey and has been shortened to the

required variables. There are three variables which are distinguished as the independent

variable, the dependent variable and the control variable. Rest of the variables that were

present in the dataset and not considered have been removed (Karanja, Zaveri & Ahmed

2013).

Sample Description

The summary of the disclosure scores are shown with the help of the mean and the

median. A median value of all the disclosure scored over the years have been allocated to the

Hypothesis

The null and the alternate hypothesis on the basis of this research study can be stated

as follows:

Null Hypothesis (H0): No significant relationship exists between the industry performance

based on voluntary disclosure and carbon emission

Alternate Hypothesis (HA): Significant relationship exists between the industry performance

based on voluntary disclosure and carbon emission

Data Collection

The dataset contains information about 306 selected organizations that have

participated in the Carbon Disclosure Project survey. These information was collected as a

result of the CDP (Carbon Disclosure project) survey. The respective data have been

collected from the companies in terms of disclosure scores, scopes of carbon emissions and

initiatives taken by the organization. The results of the analysis have to be generalized as the

collected information id for 2015 while the recorded disclosure scores are from 2012 – 2015

(Luo, Lan & Tang 2012).

The whole dataset is available from the CDP survey and has been shortened to the

required variables. There are three variables which are distinguished as the independent

variable, the dependent variable and the control variable. Rest of the variables that were

present in the dataset and not considered have been removed (Karanja, Zaveri & Ahmed

2013).

Sample Description

The summary of the disclosure scores are shown with the help of the mean and the

median. A median value of all the disclosure scored over the years have been allocated to the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4MGT723 RESEARCH PROJECT

disclosure scores variable considered for the study. For the second variable carbon emissions,

the figures on gross global emissions have been clubbed in to this variable (Pallant 2013).

The organizational objective has been recoded as 1 which indicates “yes” and 0, which

indicates “No”. Appropriate statistical analysis have been performed on these variables

(Delvore 2011).

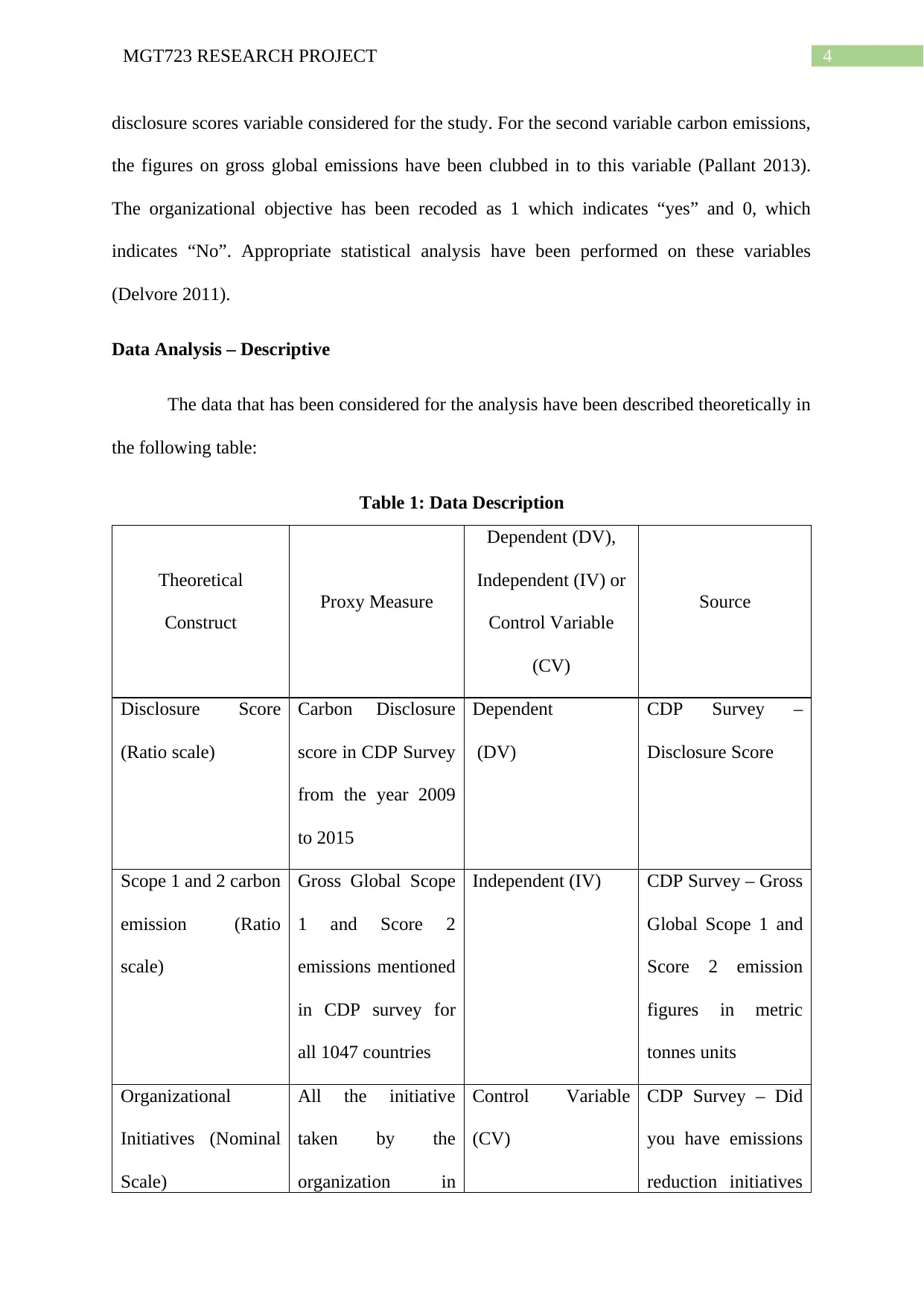

Data Analysis – Descriptive

The data that has been considered for the analysis have been described theoretically in

the following table:

Table 1: Data Description

Theoretical

Construct

Proxy Measure

Dependent (DV),

Independent (IV) or

Control Variable

(CV)

Source

Disclosure Score

(Ratio scale)

Carbon Disclosure

score in CDP Survey

from the year 2009

to 2015

Dependent

(DV)

CDP Survey –

Disclosure Score

Scope 1 and 2 carbon

emission (Ratio

scale)

Gross Global Scope

1 and Score 2

emissions mentioned

in CDP survey for

all 1047 countries

Independent (IV) CDP Survey – Gross

Global Scope 1 and

Score 2 emission

figures in metric

tonnes units

Organizational

Initiatives (Nominal

Scale)

All the initiative

taken by the

organization in

Control Variable

(CV)

CDP Survey – Did

you have emissions

reduction initiatives

disclosure scores variable considered for the study. For the second variable carbon emissions,

the figures on gross global emissions have been clubbed in to this variable (Pallant 2013).

The organizational objective has been recoded as 1 which indicates “yes” and 0, which

indicates “No”. Appropriate statistical analysis have been performed on these variables

(Delvore 2011).

Data Analysis – Descriptive

The data that has been considered for the analysis have been described theoretically in

the following table:

Table 1: Data Description

Theoretical

Construct

Proxy Measure

Dependent (DV),

Independent (IV) or

Control Variable

(CV)

Source

Disclosure Score

(Ratio scale)

Carbon Disclosure

score in CDP Survey

from the year 2009

to 2015

Dependent

(DV)

CDP Survey –

Disclosure Score

Scope 1 and 2 carbon

emission (Ratio

scale)

Gross Global Scope

1 and Score 2

emissions mentioned

in CDP survey for

all 1047 countries

Independent (IV) CDP Survey – Gross

Global Scope 1 and

Score 2 emission

figures in metric

tonnes units

Organizational

Initiatives (Nominal

Scale)

All the initiative

taken by the

organization in

Control Variable

(CV)

CDP Survey – Did

you have emissions

reduction initiatives

5MGT723 RESEARCH PROJECT

categorical values

(Yes = 2 and No =

1)

that were active?

The descriptive statistics for the data has been calculated according to the nature of

the data that has been described in the above given table.

Descriptive Statistics

It can be seen clearly from table 1 that the variable “organizational initiatives” has

been considered as a nominal variable and hence only the frequency distribution table has

been produced based on the responses recorded for the variable.

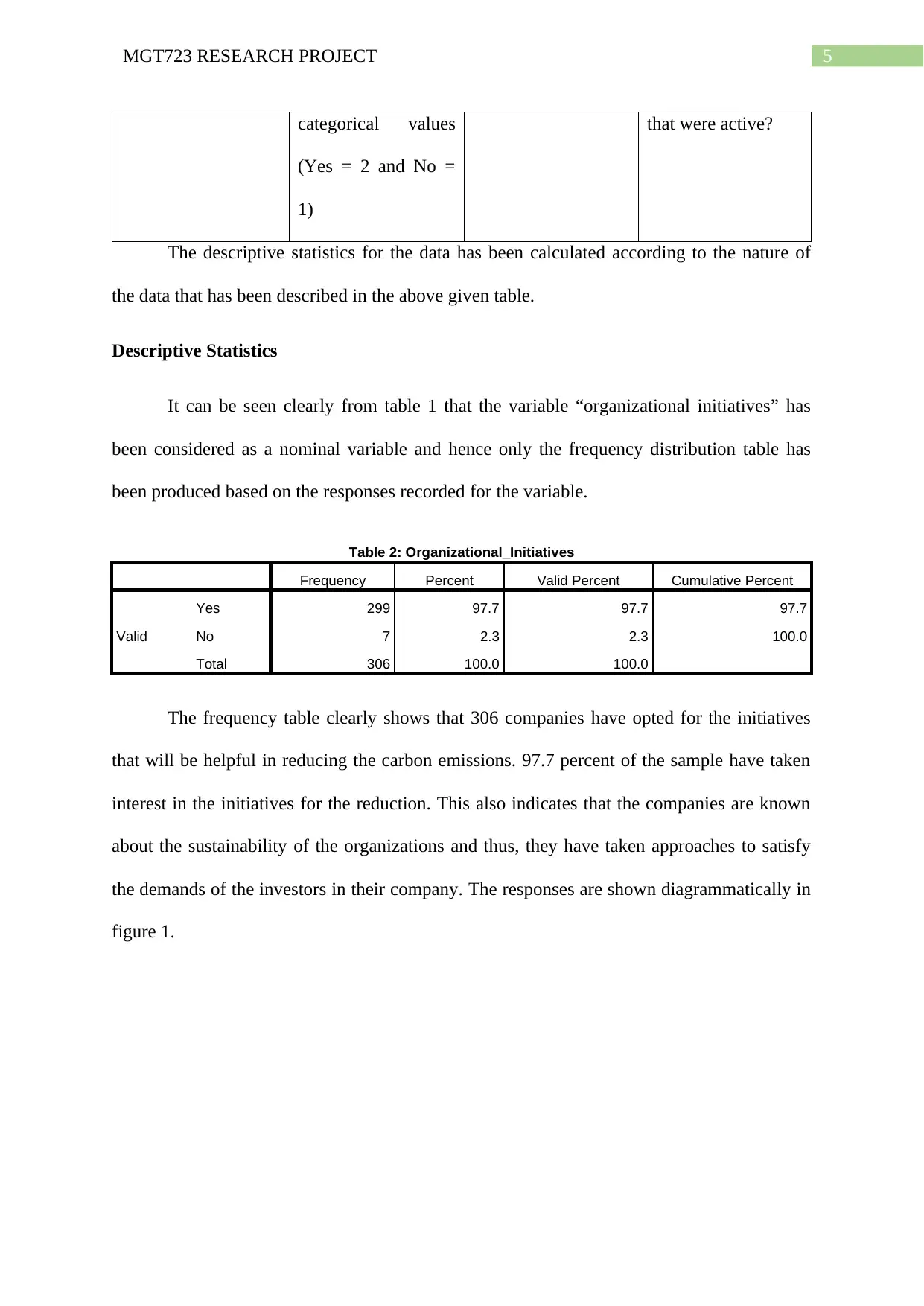

Table 2: Organizational_Initiatives

Frequency Percent Valid Percent Cumulative Percent

Valid

Yes 299 97.7 97.7 97.7

No 7 2.3 2.3 100.0

Total 306 100.0 100.0

The frequency table clearly shows that 306 companies have opted for the initiatives

that will be helpful in reducing the carbon emissions. 97.7 percent of the sample have taken

interest in the initiatives for the reduction. This also indicates that the companies are known

about the sustainability of the organizations and thus, they have taken approaches to satisfy

the demands of the investors in their company. The responses are shown diagrammatically in

figure 1.

categorical values

(Yes = 2 and No =

1)

that were active?

The descriptive statistics for the data has been calculated according to the nature of

the data that has been described in the above given table.

Descriptive Statistics

It can be seen clearly from table 1 that the variable “organizational initiatives” has

been considered as a nominal variable and hence only the frequency distribution table has

been produced based on the responses recorded for the variable.

Table 2: Organizational_Initiatives

Frequency Percent Valid Percent Cumulative Percent

Valid

Yes 299 97.7 97.7 97.7

No 7 2.3 2.3 100.0

Total 306 100.0 100.0

The frequency table clearly shows that 306 companies have opted for the initiatives

that will be helpful in reducing the carbon emissions. 97.7 percent of the sample have taken

interest in the initiatives for the reduction. This also indicates that the companies are known

about the sustainability of the organizations and thus, they have taken approaches to satisfy

the demands of the investors in their company. The responses are shown diagrammatically in

figure 1.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6MGT723 RESEARCH PROJECT

Figure 1: Organizational Initiatives to reduce Carbon Emission

The disclosure score and the scopes of carbon emissions are given in ratio scale and

hence descriptive statistics can be evaluated from them. The descriptive statistics are given in

the following table:

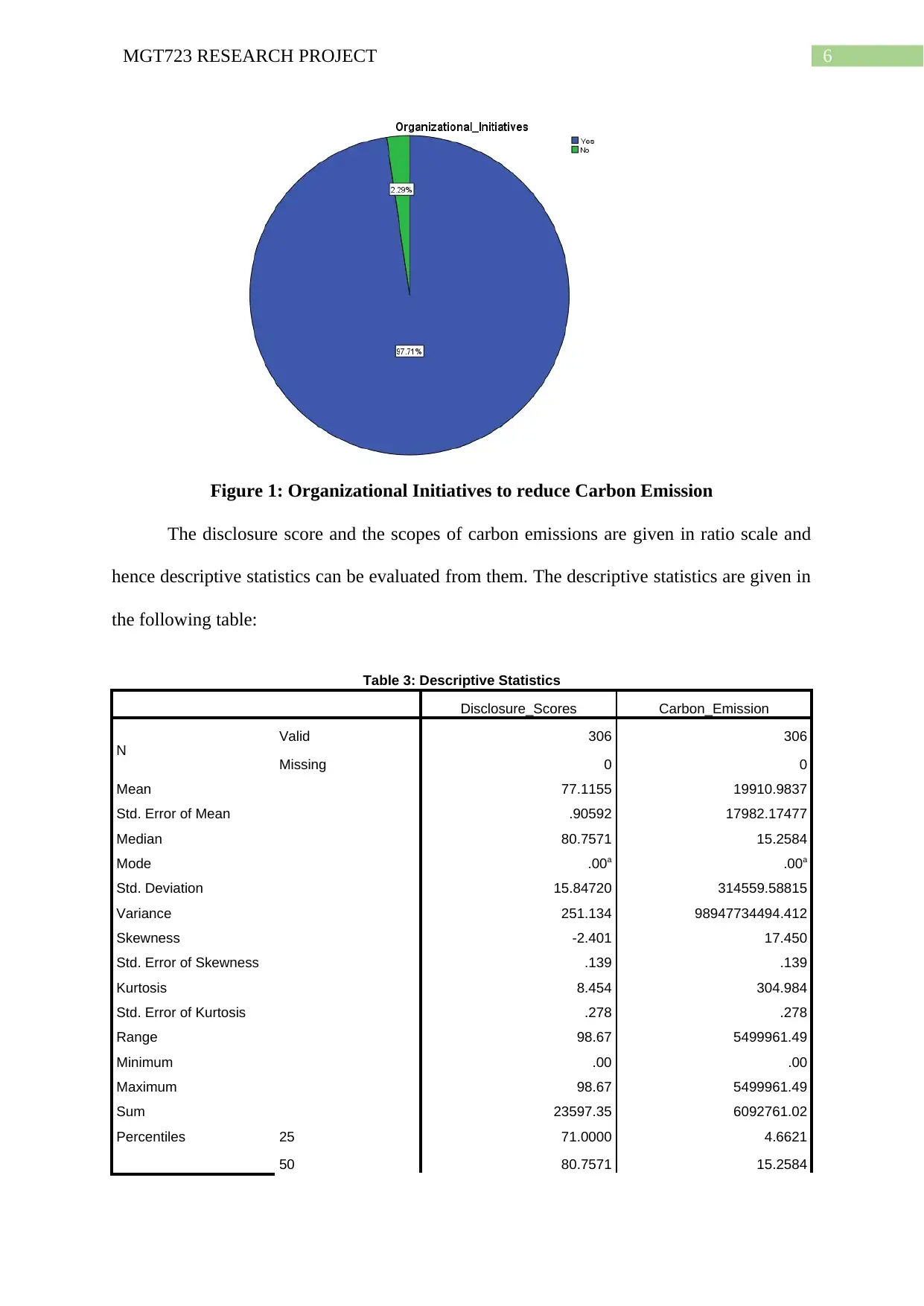

Table 3: Descriptive Statistics

Disclosure_Scores Carbon_Emission

N Valid 306 306

Missing 0 0

Mean 77.1155 19910.9837

Std. Error of Mean .90592 17982.17477

Median 80.7571 15.2584

Mode .00a .00a

Std. Deviation 15.84720 314559.58815

Variance 251.134 98947734494.412

Skewness -2.401 17.450

Std. Error of Skewness .139 .139

Kurtosis 8.454 304.984

Std. Error of Kurtosis .278 .278

Range 98.67 5499961.49

Minimum .00 .00

Maximum 98.67 5499961.49

Sum 23597.35 6092761.02

Percentiles 25 71.0000 4.6621

50 80.7571 15.2584

Figure 1: Organizational Initiatives to reduce Carbon Emission

The disclosure score and the scopes of carbon emissions are given in ratio scale and

hence descriptive statistics can be evaluated from them. The descriptive statistics are given in

the following table:

Table 3: Descriptive Statistics

Disclosure_Scores Carbon_Emission

N Valid 306 306

Missing 0 0

Mean 77.1155 19910.9837

Std. Error of Mean .90592 17982.17477

Median 80.7571 15.2584

Mode .00a .00a

Std. Deviation 15.84720 314559.58815

Variance 251.134 98947734494.412

Skewness -2.401 17.450

Std. Error of Skewness .139 .139

Kurtosis 8.454 304.984

Std. Error of Kurtosis .278 .278

Range 98.67 5499961.49

Minimum .00 .00

Maximum 98.67 5499961.49

Sum 23597.35 6092761.02

Percentiles 25 71.0000 4.6621

50 80.7571 15.2584

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7MGT723 RESEARCH PROJECT

75 86.5714 86.3346

a. Multiple modes exist. The smallest value is shown

The variable disclosure score is given out of 100 which indicates the position of the

firm in the financial reports. It can be seen from the mean value that 77.12 percent of the

companies have provided the disclosure scores. The median value of 80.76 shows that 50

percent of the companies have a voluntary disclosure score of above 80.76. The mode of the

data has not been obtained. This indicates inequality in the mean, the median and the mode

and thus violates normality (Blanca et al. 2013). Thus, the data is not distributed normally. A

high standard deviation of 15.85 indicated variability in the scores. The negative value of

skewness (-2.401) indicates that the data is negatively skewed (Park 2015). The histogram

given below shows the shape of the data for the disclosure scores.

Figure 2: Distribution of Carbon Disclosure Scores

The carbon emissions of the company are given in metric tonnes and it can be seen

from the analysis that the average emission is 19910.98 metric tonnes. The median emission

is found to be 15.26 metric tonnes and there is no mode to the data. This indicates inequality

in the mean, the median and the mode and thus violates normality. Thus, the data is not

distributed normally. A high standard deviation of 314559.59 indicated variability in the

75 86.5714 86.3346

a. Multiple modes exist. The smallest value is shown

The variable disclosure score is given out of 100 which indicates the position of the

firm in the financial reports. It can be seen from the mean value that 77.12 percent of the

companies have provided the disclosure scores. The median value of 80.76 shows that 50

percent of the companies have a voluntary disclosure score of above 80.76. The mode of the

data has not been obtained. This indicates inequality in the mean, the median and the mode

and thus violates normality (Blanca et al. 2013). Thus, the data is not distributed normally. A

high standard deviation of 15.85 indicated variability in the scores. The negative value of

skewness (-2.401) indicates that the data is negatively skewed (Park 2015). The histogram

given below shows the shape of the data for the disclosure scores.

Figure 2: Distribution of Carbon Disclosure Scores

The carbon emissions of the company are given in metric tonnes and it can be seen

from the analysis that the average emission is 19910.98 metric tonnes. The median emission

is found to be 15.26 metric tonnes and there is no mode to the data. This indicates inequality

in the mean, the median and the mode and thus violates normality. Thus, the data is not

distributed normally. A high standard deviation of 314559.59 indicated variability in the

8MGT723 RESEARCH PROJECT

scores. The positive value of skewness (17.450) indicates that the data is positively skewed

(De Vaus 2013). The histogram given below shows the shape of the data for the carbon

emission.

Figure 3: Distribution of Carbon Emission

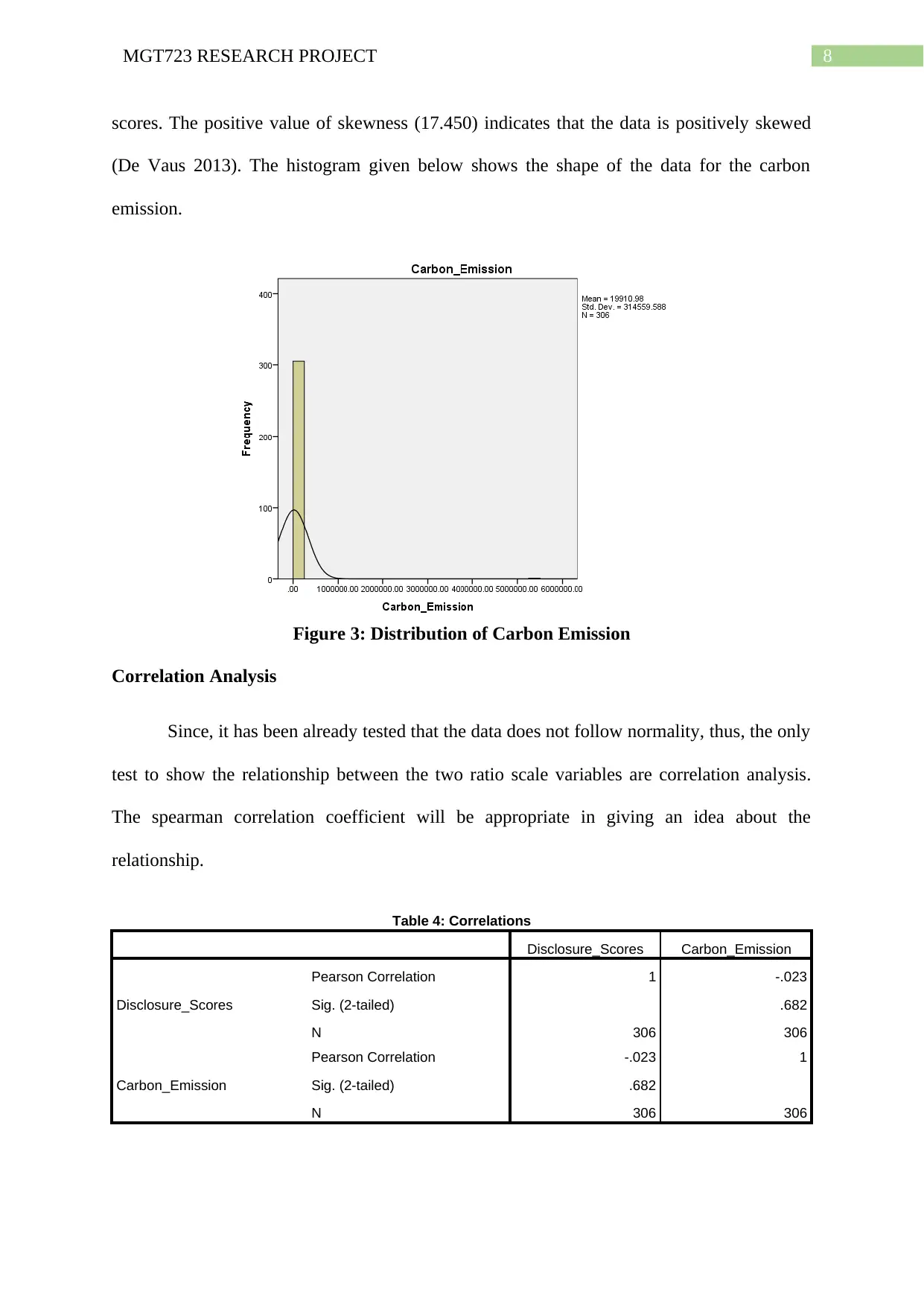

Correlation Analysis

Since, it has been already tested that the data does not follow normality, thus, the only

test to show the relationship between the two ratio scale variables are correlation analysis.

The spearman correlation coefficient will be appropriate in giving an idea about the

relationship.

Table 4: Correlations

Disclosure_Scores Carbon_Emission

Disclosure_Scores

Pearson Correlation 1 -.023

Sig. (2-tailed) .682

N 306 306

Carbon_Emission

Pearson Correlation -.023 1

Sig. (2-tailed) .682

N 306 306

scores. The positive value of skewness (17.450) indicates that the data is positively skewed

(De Vaus 2013). The histogram given below shows the shape of the data for the carbon

emission.

Figure 3: Distribution of Carbon Emission

Correlation Analysis

Since, it has been already tested that the data does not follow normality, thus, the only

test to show the relationship between the two ratio scale variables are correlation analysis.

The spearman correlation coefficient will be appropriate in giving an idea about the

relationship.

Table 4: Correlations

Disclosure_Scores Carbon_Emission

Disclosure_Scores

Pearson Correlation 1 -.023

Sig. (2-tailed) .682

N 306 306

Carbon_Emission

Pearson Correlation -.023 1

Sig. (2-tailed) .682

N 306 306

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9MGT723 RESEARCH PROJECT

It can be seen from the correlation table that there is a weak negative relationship

between the independent and the dependent variable. The correlation coefficient is not

significant at α=0.01 as the p value is higher than α. Thus, there exists an insignificant

relationship between Carbon emission and carbon disclosure scores.

Inferential Statistics

Mann-Whitney U Test

To test the differences in the average values of a variable with respect to two different

categories, an independent sample t-test is conducted. In case if an independent sample t-test,

there is an assumption that the data is normally distributed. In this case, as already seen from

the descriptive statistics that the data is not normally distributed. Thus, the non-parametric

test which is used to test the difference in the average values of two groups is used. Thus is

the Mann-Whitney U Test. The dependent variable considered here is in ratio scale whereas

the control variable is categorical. Thus, Mann-Whitney test would be the most appropriate

test in this case as the data also violates normality. However, when compared as the case of

control variable then Mann Whitney Test is considered to be apt as it has two categories as

Yes or No.

The test statistics is based on two – tailed which has asymptotic significance. This

data can be concluded that disclosure scores of the organization over the years is statistically

significant in taking organization initiative to reduce carbon emission if the p-value obtained

from conducting the test results to be more than 0.05.

It can be seen from the correlation table that there is a weak negative relationship

between the independent and the dependent variable. The correlation coefficient is not

significant at α=0.01 as the p value is higher than α. Thus, there exists an insignificant

relationship between Carbon emission and carbon disclosure scores.

Inferential Statistics

Mann-Whitney U Test

To test the differences in the average values of a variable with respect to two different

categories, an independent sample t-test is conducted. In case if an independent sample t-test,

there is an assumption that the data is normally distributed. In this case, as already seen from

the descriptive statistics that the data is not normally distributed. Thus, the non-parametric

test which is used to test the difference in the average values of two groups is used. Thus is

the Mann-Whitney U Test. The dependent variable considered here is in ratio scale whereas

the control variable is categorical. Thus, Mann-Whitney test would be the most appropriate

test in this case as the data also violates normality. However, when compared as the case of

control variable then Mann Whitney Test is considered to be apt as it has two categories as

Yes or No.

The test statistics is based on two – tailed which has asymptotic significance. This

data can be concluded that disclosure scores of the organization over the years is statistically

significant in taking organization initiative to reduce carbon emission if the p-value obtained

from conducting the test results to be more than 0.05.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10MGT723 RESEARCH PROJECT

References

Albertini, E., 2013. Does environmental management improve financial performance? A

meta-analytical review. Organization & Environment, 26(4), pp.431-457.

Blanca, M.J., Arnau, J., López-Montiel, D., Bono, R. and Bendayan, R., 2013. Skewness and

kurtosis in real data samples. Methodology.

De Vaus, D., 2013. Surveys in social research. Routledge.

Devore, J.L., 2011. Probability and Statistics for Engineering and the Sciences. Cengage

learning.

Karanja, E., Zaveri, J. and Ahmed, A., 2013. How do MIS researchers handle missing data in

survey-based research: A content analysis approach. International Journal of Information

Management, 33(5), pp.734-751.

Luo, L., Lan, Y.C. and Tang, Q., 2012. Corporate incentives to disclose carbon information:

Evidence from the CDP Global 500 report. Journal of International Financial Management

& Accounting, 23(2), pp.93-120.

Pallant, J., 2013. SPSS survival manual. McGraw-Hill Education (UK).

Park, H.M., 2015. Univariate analysis and normality test using SAS, Stata, and SPSS.

Saka, C. and Oshika, T., 2014. Disclosure effects, carbon emissions and corporate

value. Sustainability Accounting, Management and Policy Journal, 5(1), pp.22-45.

References

Albertini, E., 2013. Does environmental management improve financial performance? A

meta-analytical review. Organization & Environment, 26(4), pp.431-457.

Blanca, M.J., Arnau, J., López-Montiel, D., Bono, R. and Bendayan, R., 2013. Skewness and

kurtosis in real data samples. Methodology.

De Vaus, D., 2013. Surveys in social research. Routledge.

Devore, J.L., 2011. Probability and Statistics for Engineering and the Sciences. Cengage

learning.

Karanja, E., Zaveri, J. and Ahmed, A., 2013. How do MIS researchers handle missing data in

survey-based research: A content analysis approach. International Journal of Information

Management, 33(5), pp.734-751.

Luo, L., Lan, Y.C. and Tang, Q., 2012. Corporate incentives to disclose carbon information:

Evidence from the CDP Global 500 report. Journal of International Financial Management

& Accounting, 23(2), pp.93-120.

Pallant, J., 2013. SPSS survival manual. McGraw-Hill Education (UK).

Park, H.M., 2015. Univariate analysis and normality test using SAS, Stata, and SPSS.

Saka, C. and Oshika, T., 2014. Disclosure effects, carbon emissions and corporate

value. Sustainability Accounting, Management and Policy Journal, 5(1), pp.22-45.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.