ABC Costing and Performance Analysis: Management Accounting Homework

VerifiedAdded on 2022/09/02

|15

|2132

|29

Homework Assignment

AI Summary

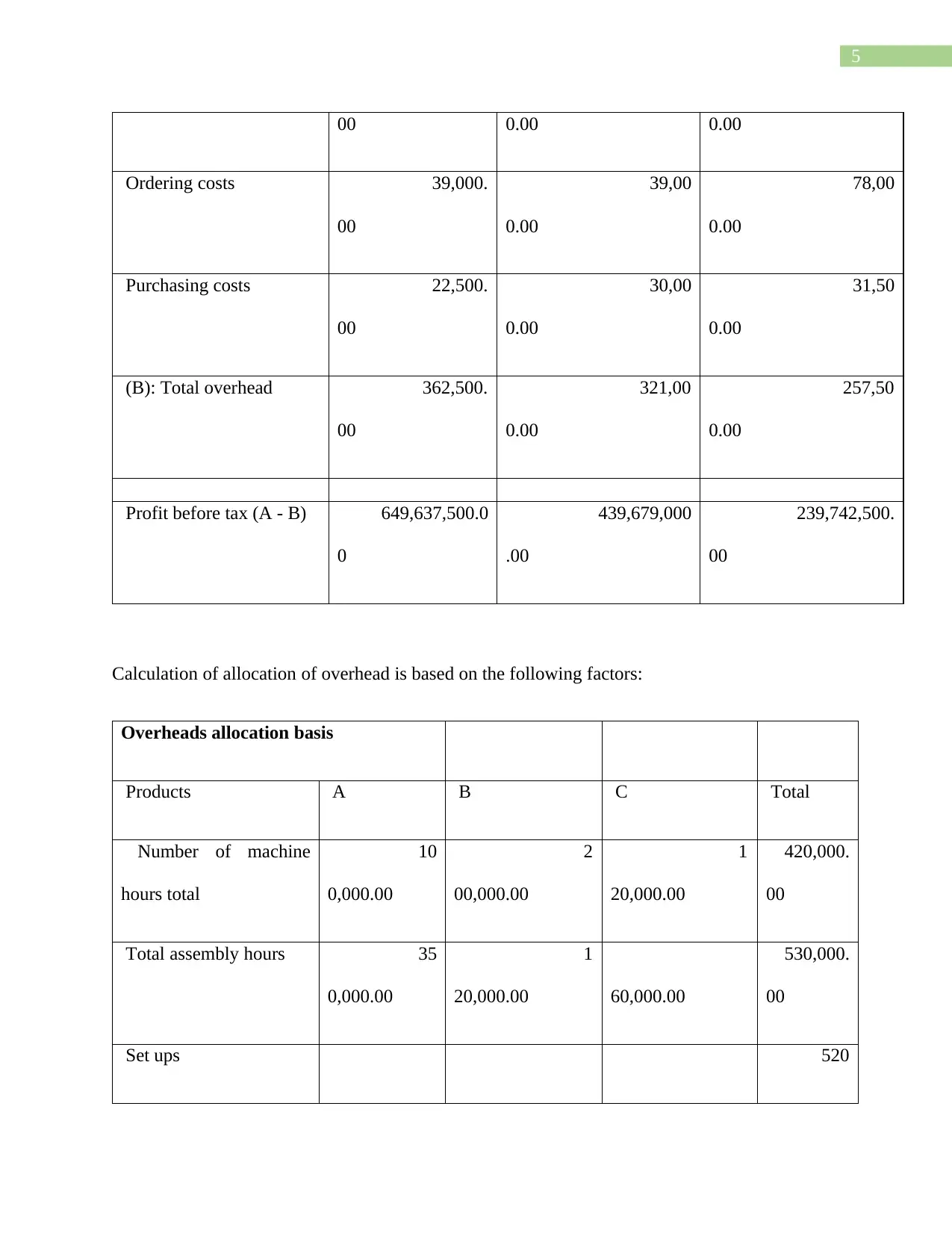

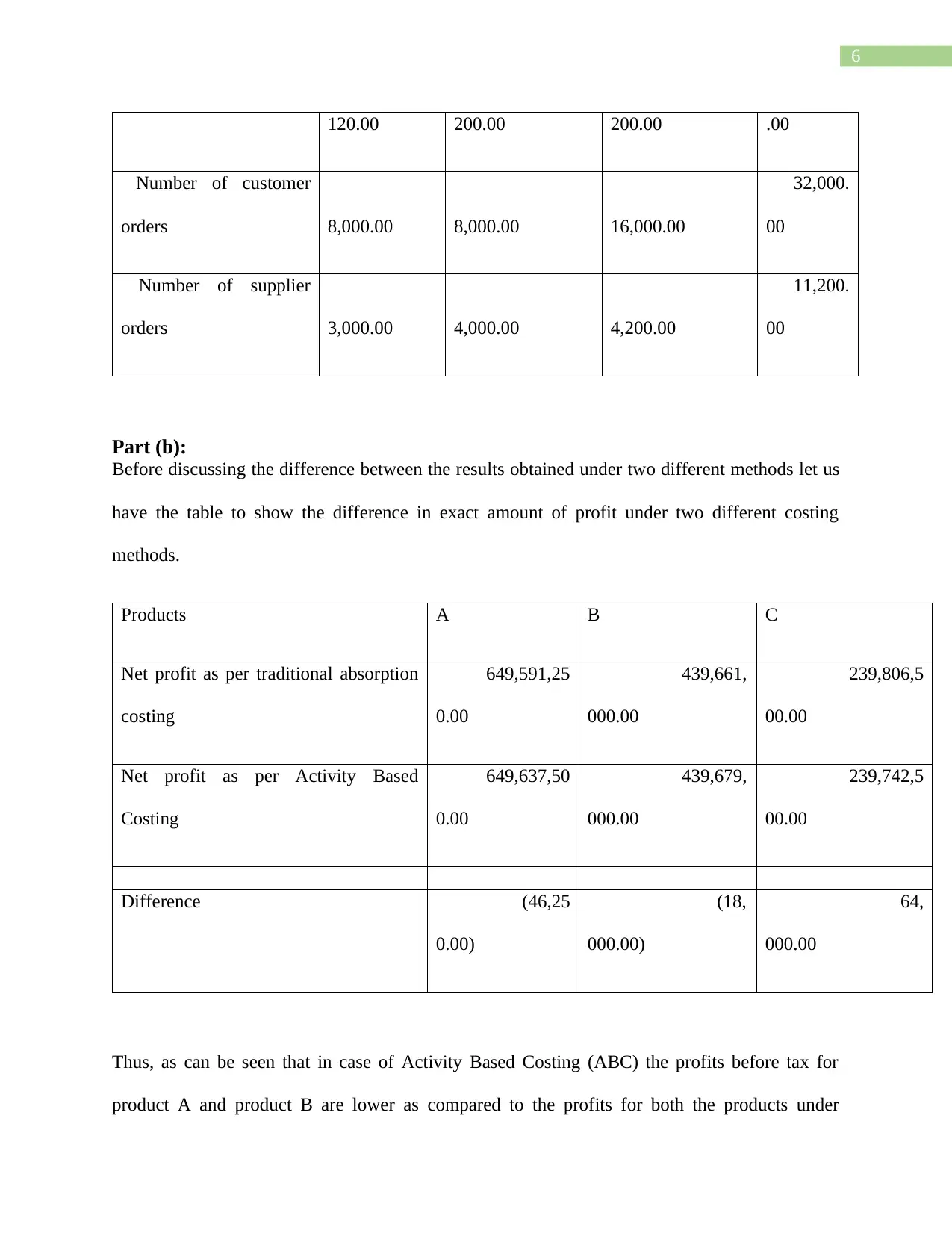

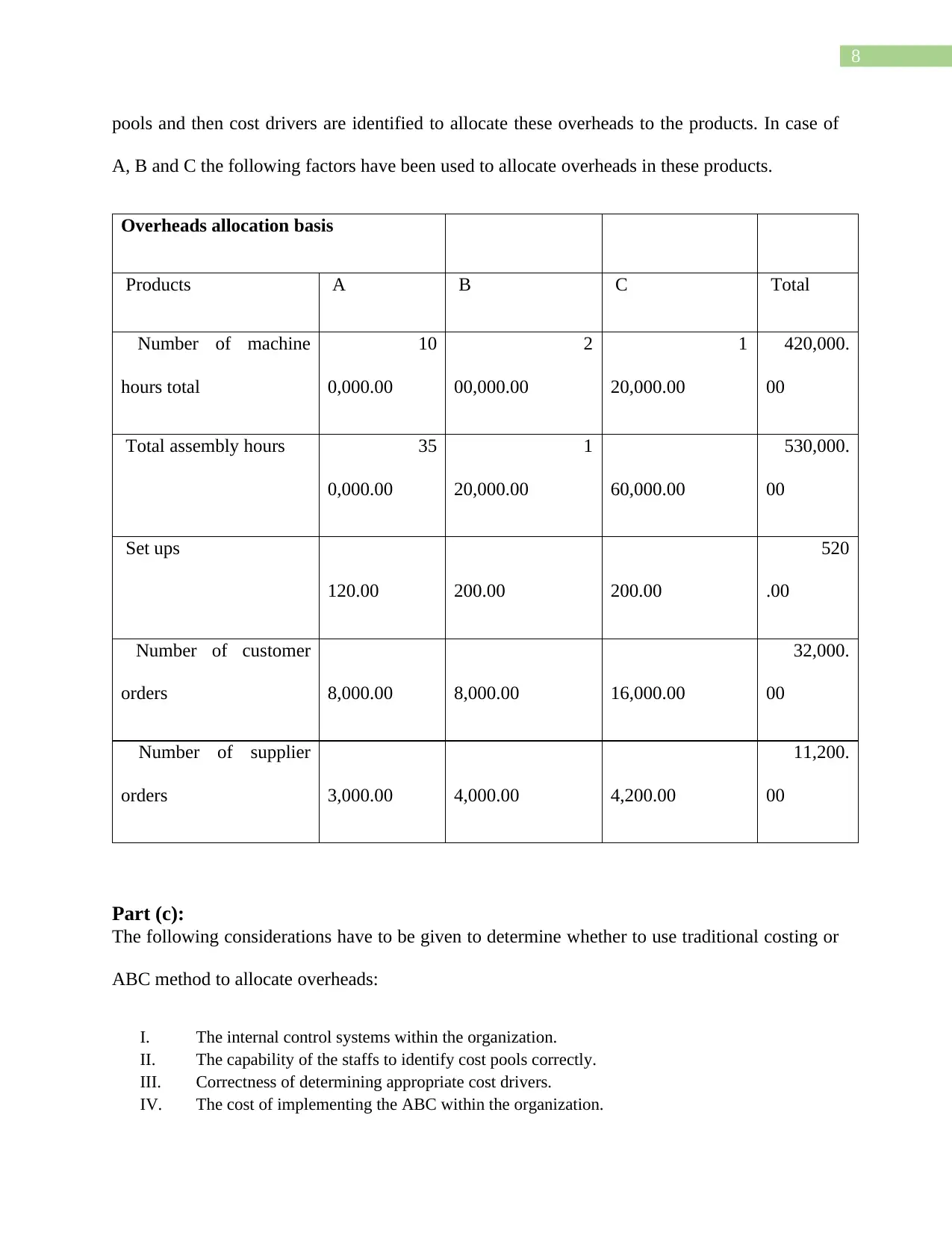

This homework assignment from a Management Control and Finance course at Copenhagen Business School explores Activity Based Costing (ABC) and its application. The student analyzes the profitability of three products using both traditional absorption costing and ABC methods, calculating overhead allocations based on machine hours and assembly hours. The assignment compares the results of the two costing methods, highlighting the differences in profit before tax for each product and explaining the impact of different overhead allocation bases. It also examines budgeting and accounting systems within a Social Assistance department, evaluating budget variances and suggesting improvements, emphasizing the importance of stakeholder coordination and communication. Finally, the assignment assesses the performance of a restaurant using financial data, market share, and a balanced scorecard, while also considering the restaurant's intellectual capital components such as the number of meals served, turnover, and special themes. The assignment aims to provide a comprehensive understanding of cost accounting, budgeting, and performance evaluation techniques.

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.