Comprehensive Audit Report: Cloud 9 Inc. Financial Statement Review

VerifiedAdded on 2023/04/25

|12

|2228

|464

Report

AI Summary

This report provides a detailed analysis of the financial statements of Cloud 9 Inc., focusing on key aspects of the auditing process. It begins with the computation of planning materiality, outlining how auditors determine the acceptable level of misstatement in financial statements. The report then delves into analytical procedures, examining financial ratios related to profitability, liquidity, efficiency, and solvency to assess the company's financial performance and identify potential risks. Special areas of consideration, such as revenue from stores and wholesale, inventory, debtors, and debt figures, are highlighted. The report also includes a section on compensation disclosures, comparing the remuneration policies of BHP Billiton Ltd, Boral Ltd, and Ausdrill Ltd, linking executive compensation with company performance and share prices. The report concludes by summarizing the key findings and implications of the audit procedures, offering a comprehensive overview of Cloud 9 Inc.'s financial health and compliance with regulatory requirements. The report utilizes financial data from annual reports to support its analysis, providing a practical application of auditing principles.

Running head: AUDITING

Auditing

Name of the Student:

Name of the University:

Author’s Note

Auditing

Name of the Student:

Name of the University:

Author’s Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

AUDITING

Table of Contents

Part 1................................................................................................................................................2

Computation of Planning Materiality..........................................................................................2

Part 2................................................................................................................................................4

Analytical Procedure...................................................................................................................4

Special Area of Consideration.....................................................................................................7

Compensation Disclosures...............................................................................................................8

Introduction..................................................................................................................................8

Payment Mode of Executives......................................................................................................8

Highest PayScale of Executives................................................................................................10

Linking Remuneration with Profit/Share price of the Business................................................10

Conclusion.................................................................................................................................10

Reference.......................................................................................................................................12

AUDITING

Table of Contents

Part 1................................................................................................................................................2

Computation of Planning Materiality..........................................................................................2

Part 2................................................................................................................................................4

Analytical Procedure...................................................................................................................4

Special Area of Consideration.....................................................................................................7

Compensation Disclosures...............................................................................................................8

Introduction..................................................................................................................................8

Payment Mode of Executives......................................................................................................8

Highest PayScale of Executives................................................................................................10

Linking Remuneration with Profit/Share price of the Business................................................10

Conclusion.................................................................................................................................10

Reference.......................................................................................................................................12

2

AUDITING

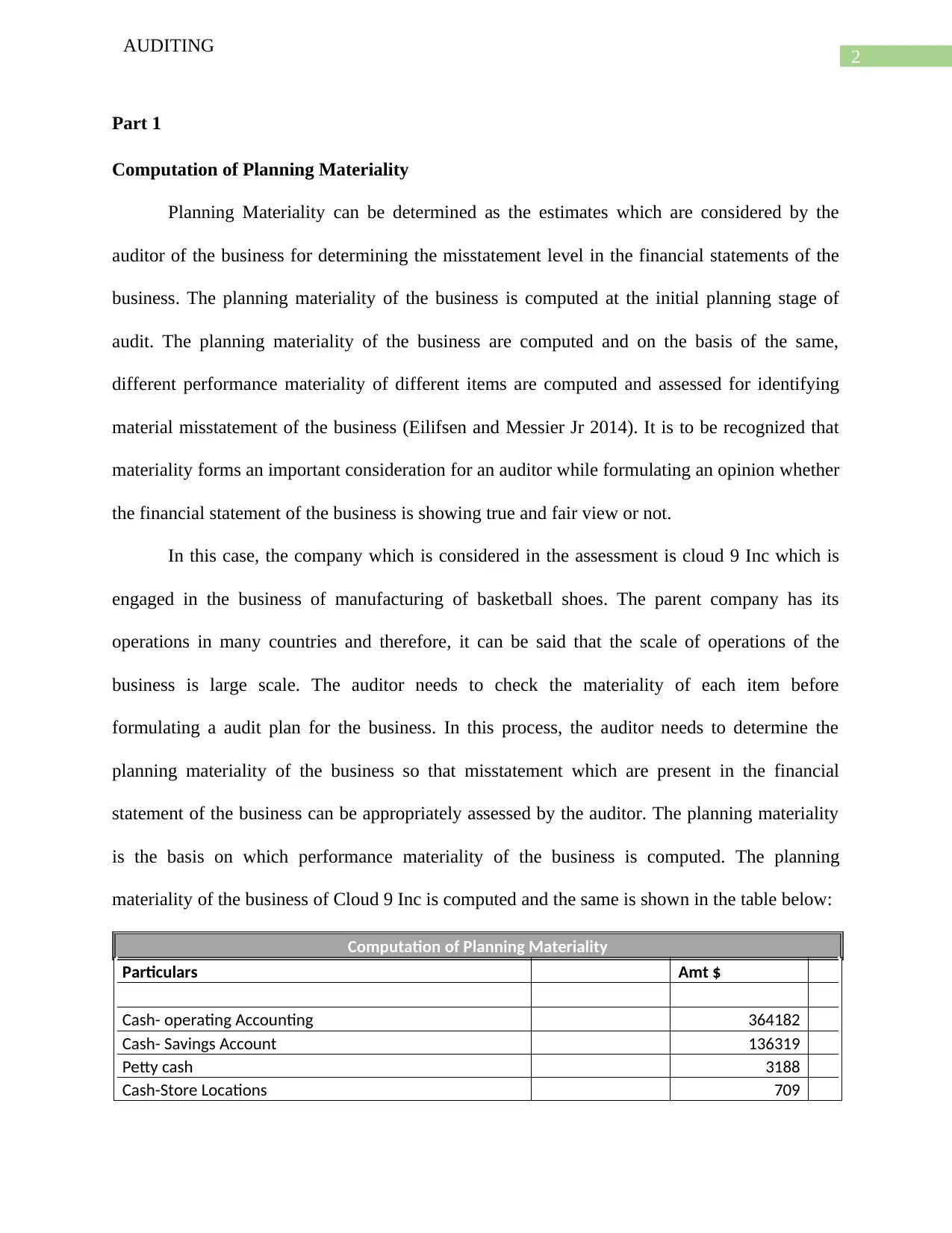

Part 1

Computation of Planning Materiality

Planning Materiality can be determined as the estimates which are considered by the

auditor of the business for determining the misstatement level in the financial statements of the

business. The planning materiality of the business is computed at the initial planning stage of

audit. The planning materiality of the business are computed and on the basis of the same,

different performance materiality of different items are computed and assessed for identifying

material misstatement of the business (Eilifsen and Messier Jr 2014). It is to be recognized that

materiality forms an important consideration for an auditor while formulating an opinion whether

the financial statement of the business is showing true and fair view or not.

In this case, the company which is considered in the assessment is cloud 9 Inc which is

engaged in the business of manufacturing of basketball shoes. The parent company has its

operations in many countries and therefore, it can be said that the scale of operations of the

business is large scale. The auditor needs to check the materiality of each item before

formulating a audit plan for the business. In this process, the auditor needs to determine the

planning materiality of the business so that misstatement which are present in the financial

statement of the business can be appropriately assessed by the auditor. The planning materiality

is the basis on which performance materiality of the business is computed. The planning

materiality of the business of Cloud 9 Inc is computed and the same is shown in the table below:

Computation of Planning Materiality

Particulars Amt $

Cash- operating Accounting 364182

Cash- Savings Account 136319

Petty cash 3188

Cash-Store Locations 709

AUDITING

Part 1

Computation of Planning Materiality

Planning Materiality can be determined as the estimates which are considered by the

auditor of the business for determining the misstatement level in the financial statements of the

business. The planning materiality of the business is computed at the initial planning stage of

audit. The planning materiality of the business are computed and on the basis of the same,

different performance materiality of different items are computed and assessed for identifying

material misstatement of the business (Eilifsen and Messier Jr 2014). It is to be recognized that

materiality forms an important consideration for an auditor while formulating an opinion whether

the financial statement of the business is showing true and fair view or not.

In this case, the company which is considered in the assessment is cloud 9 Inc which is

engaged in the business of manufacturing of basketball shoes. The parent company has its

operations in many countries and therefore, it can be said that the scale of operations of the

business is large scale. The auditor needs to check the materiality of each item before

formulating a audit plan for the business. In this process, the auditor needs to determine the

planning materiality of the business so that misstatement which are present in the financial

statement of the business can be appropriately assessed by the auditor. The planning materiality

is the basis on which performance materiality of the business is computed. The planning

materiality of the business of Cloud 9 Inc is computed and the same is shown in the table below:

Computation of Planning Materiality

Particulars Amt $

Cash- operating Accounting 364182

Cash- Savings Account 136319

Petty cash 3188

Cash-Store Locations 709

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

AUDITING

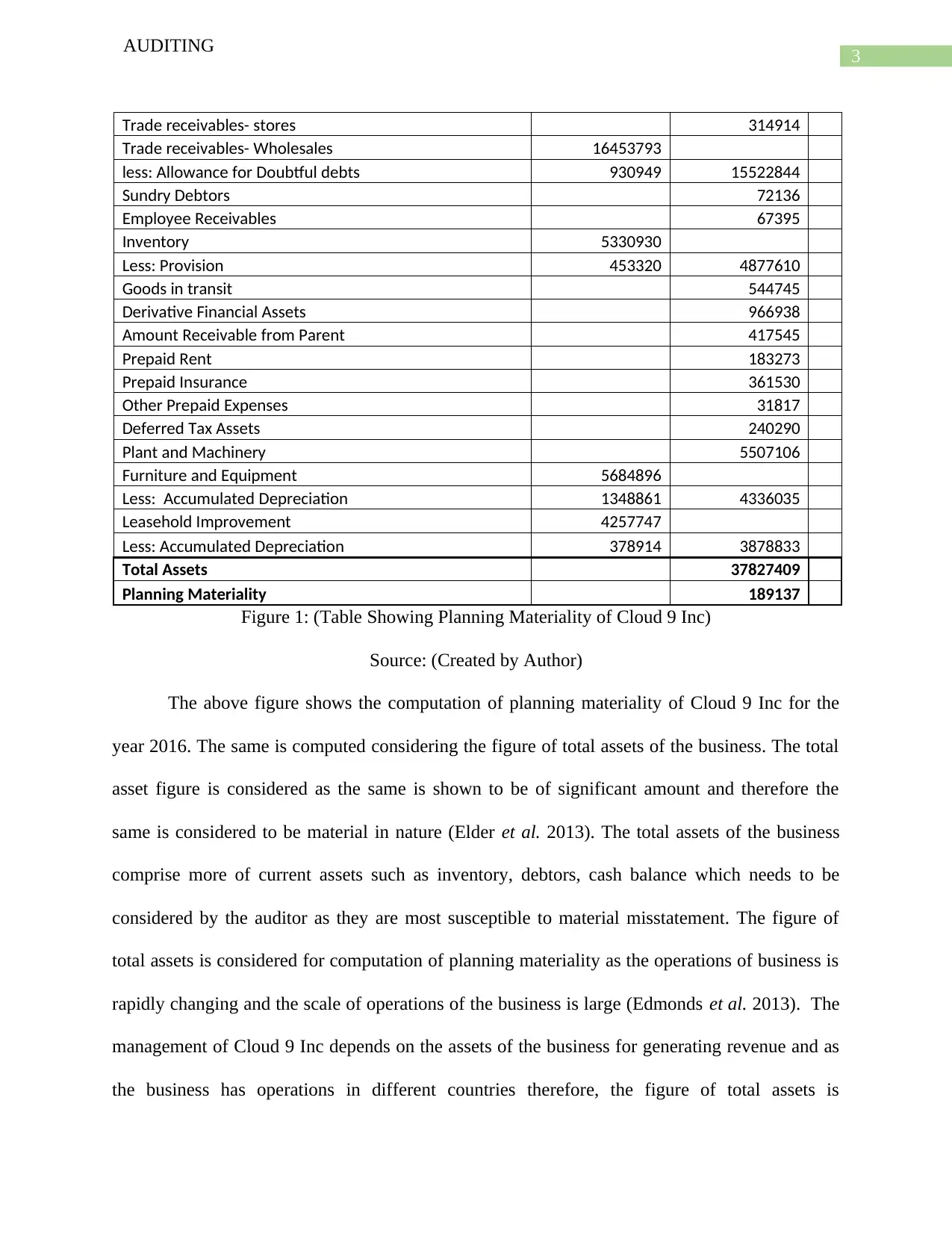

Trade receivables- stores 314914

Trade receivables- Wholesales 16453793

less: Allowance for Doubtful debts 930949 15522844

Sundry Debtors 72136

Employee Receivables 67395

Inventory 5330930

Less: Provision 453320 4877610

Goods in transit 544745

Derivative Financial Assets 966938

Amount Receivable from Parent 417545

Prepaid Rent 183273

Prepaid Insurance 361530

Other Prepaid Expenses 31817

Deferred Tax Assets 240290

Plant and Machinery 5507106

Furniture and Equipment 5684896

Less: Accumulated Depreciation 1348861 4336035

Leasehold Improvement 4257747

Less: Accumulated Depreciation 378914 3878833

Total Assets 37827409

Planning Materiality 189137

Figure 1: (Table Showing Planning Materiality of Cloud 9 Inc)

Source: (Created by Author)

The above figure shows the computation of planning materiality of Cloud 9 Inc for the

year 2016. The same is computed considering the figure of total assets of the business. The total

asset figure is considered as the same is shown to be of significant amount and therefore the

same is considered to be material in nature (Elder et al. 2013). The total assets of the business

comprise more of current assets such as inventory, debtors, cash balance which needs to be

considered by the auditor as they are most susceptible to material misstatement. The figure of

total assets is considered for computation of planning materiality as the operations of business is

rapidly changing and the scale of operations of the business is large (Edmonds et al. 2013). The

management of Cloud 9 Inc depends on the assets of the business for generating revenue and as

the business has operations in different countries therefore, the figure of total assets is

AUDITING

Trade receivables- stores 314914

Trade receivables- Wholesales 16453793

less: Allowance for Doubtful debts 930949 15522844

Sundry Debtors 72136

Employee Receivables 67395

Inventory 5330930

Less: Provision 453320 4877610

Goods in transit 544745

Derivative Financial Assets 966938

Amount Receivable from Parent 417545

Prepaid Rent 183273

Prepaid Insurance 361530

Other Prepaid Expenses 31817

Deferred Tax Assets 240290

Plant and Machinery 5507106

Furniture and Equipment 5684896

Less: Accumulated Depreciation 1348861 4336035

Leasehold Improvement 4257747

Less: Accumulated Depreciation 378914 3878833

Total Assets 37827409

Planning Materiality 189137

Figure 1: (Table Showing Planning Materiality of Cloud 9 Inc)

Source: (Created by Author)

The above figure shows the computation of planning materiality of Cloud 9 Inc for the

year 2016. The same is computed considering the figure of total assets of the business. The total

asset figure is considered as the same is shown to be of significant amount and therefore the

same is considered to be material in nature (Elder et al. 2013). The total assets of the business

comprise more of current assets such as inventory, debtors, cash balance which needs to be

considered by the auditor as they are most susceptible to material misstatement. The figure of

total assets is considered for computation of planning materiality as the operations of business is

rapidly changing and the scale of operations of the business is large (Edmonds et al. 2013). The

management of Cloud 9 Inc depends on the assets of the business for generating revenue and as

the business has operations in different countries therefore, the figure of total assets is

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

AUDITING

appropriate for computing the planning materiality for the purpose of audit (Glover, Prawitt and

Drake 2014). In addition to this, the auditor needs to consider the figure which is important and

the total assets is a very significant figure shown in the financial statements.

Part 2

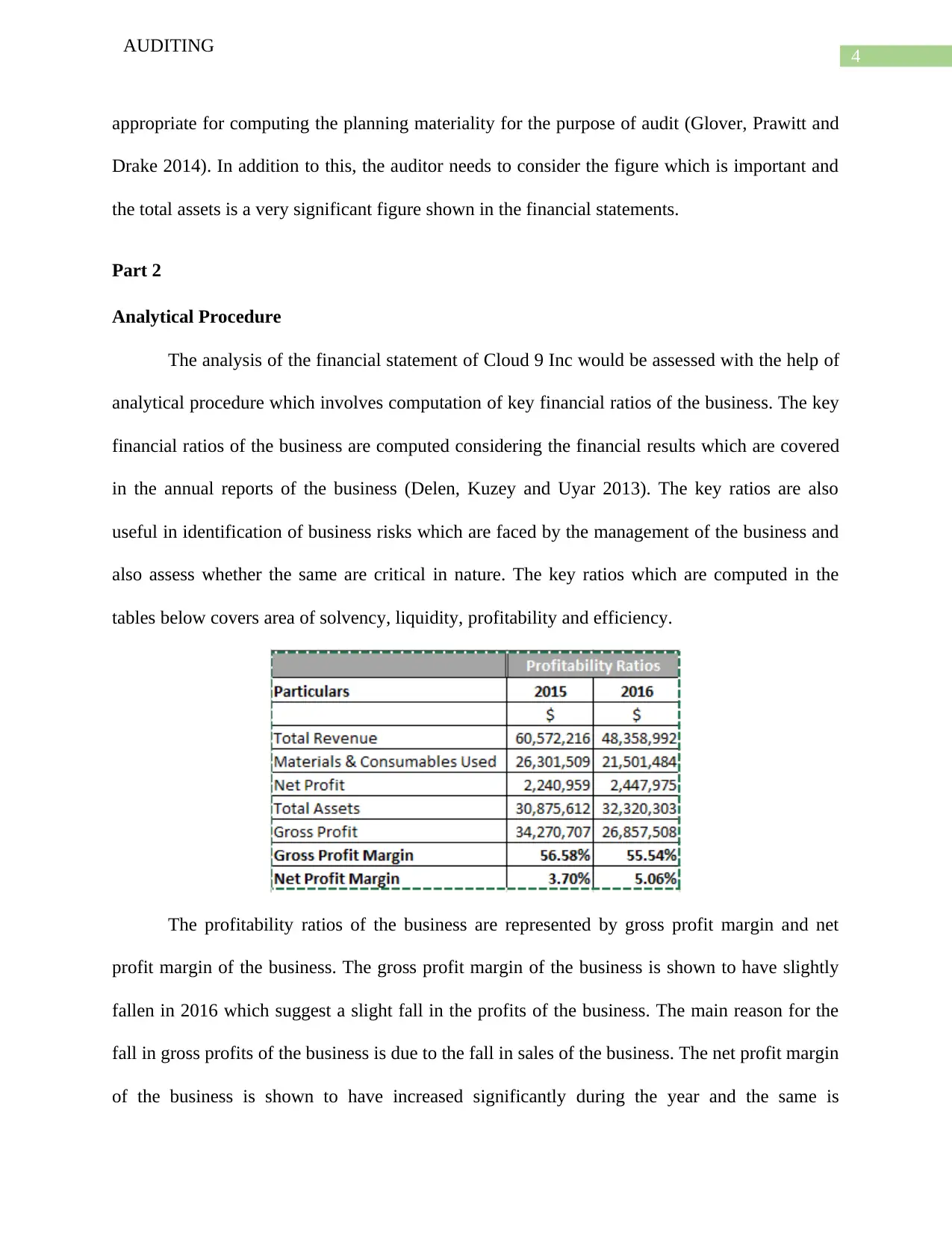

Analytical Procedure

The analysis of the financial statement of Cloud 9 Inc would be assessed with the help of

analytical procedure which involves computation of key financial ratios of the business. The key

financial ratios of the business are computed considering the financial results which are covered

in the annual reports of the business (Delen, Kuzey and Uyar 2013). The key ratios are also

useful in identification of business risks which are faced by the management of the business and

also assess whether the same are critical in nature. The key ratios which are computed in the

tables below covers area of solvency, liquidity, profitability and efficiency.

The profitability ratios of the business are represented by gross profit margin and net

profit margin of the business. The gross profit margin of the business is shown to have slightly

fallen in 2016 which suggest a slight fall in the profits of the business. The main reason for the

fall in gross profits of the business is due to the fall in sales of the business. The net profit margin

of the business is shown to have increased significantly during the year and the same is

AUDITING

appropriate for computing the planning materiality for the purpose of audit (Glover, Prawitt and

Drake 2014). In addition to this, the auditor needs to consider the figure which is important and

the total assets is a very significant figure shown in the financial statements.

Part 2

Analytical Procedure

The analysis of the financial statement of Cloud 9 Inc would be assessed with the help of

analytical procedure which involves computation of key financial ratios of the business. The key

financial ratios of the business are computed considering the financial results which are covered

in the annual reports of the business (Delen, Kuzey and Uyar 2013). The key ratios are also

useful in identification of business risks which are faced by the management of the business and

also assess whether the same are critical in nature. The key ratios which are computed in the

tables below covers area of solvency, liquidity, profitability and efficiency.

The profitability ratios of the business are represented by gross profit margin and net

profit margin of the business. The gross profit margin of the business is shown to have slightly

fallen in 2016 which suggest a slight fall in the profits of the business. The main reason for the

fall in gross profits of the business is due to the fall in sales of the business. The net profit margin

of the business is shown to have increased significantly during the year and the same is

5

AUDITING

computed to be 5.06%. This is mainly due to the reduction in costs of the business (Xu et al.

2014). The auditor needs to ensure that the costs of the business are appropriately presented in

the annual reports as they can directly affect the revenues of the business.

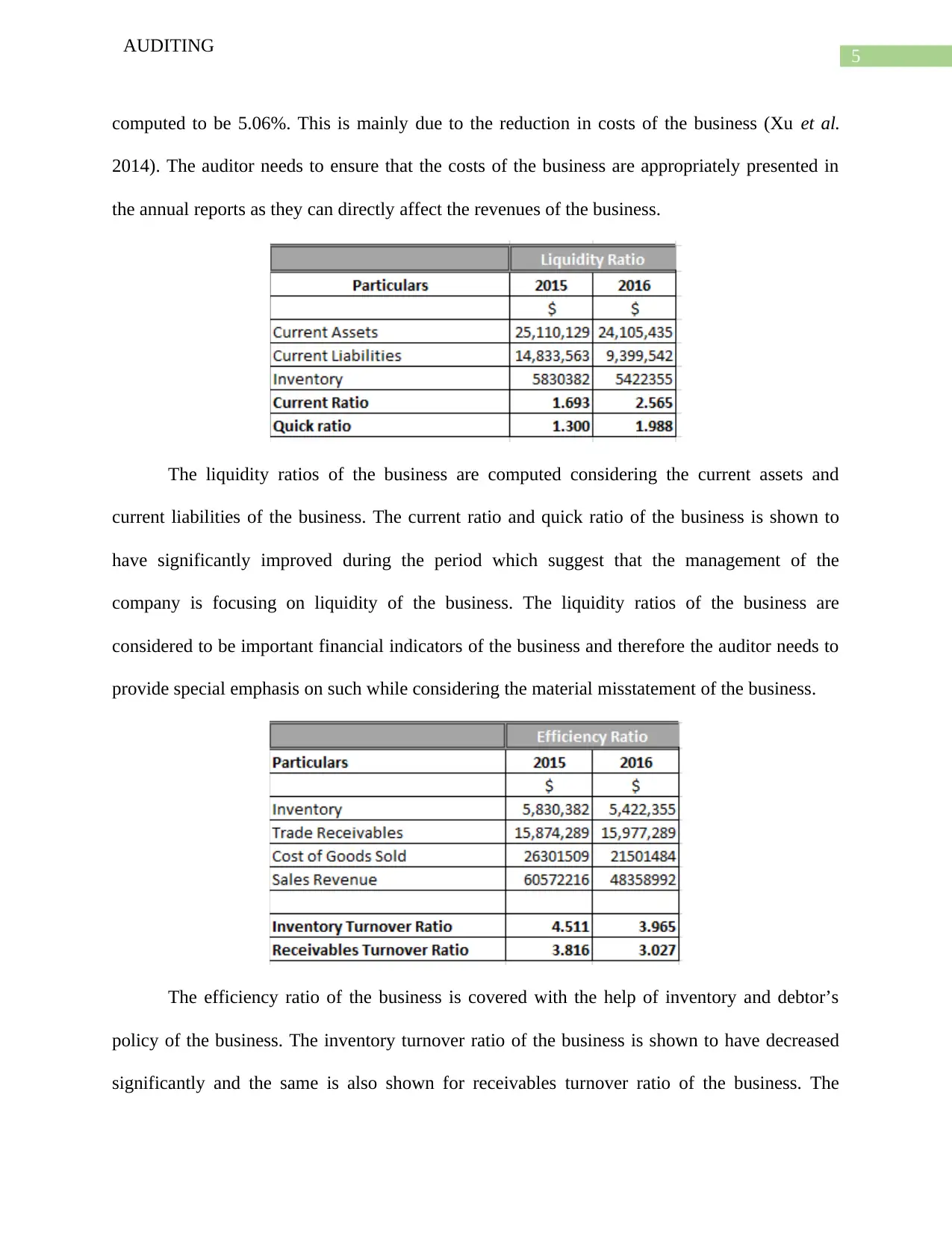

The liquidity ratios of the business are computed considering the current assets and

current liabilities of the business. The current ratio and quick ratio of the business is shown to

have significantly improved during the period which suggest that the management of the

company is focusing on liquidity of the business. The liquidity ratios of the business are

considered to be important financial indicators of the business and therefore the auditor needs to

provide special emphasis on such while considering the material misstatement of the business.

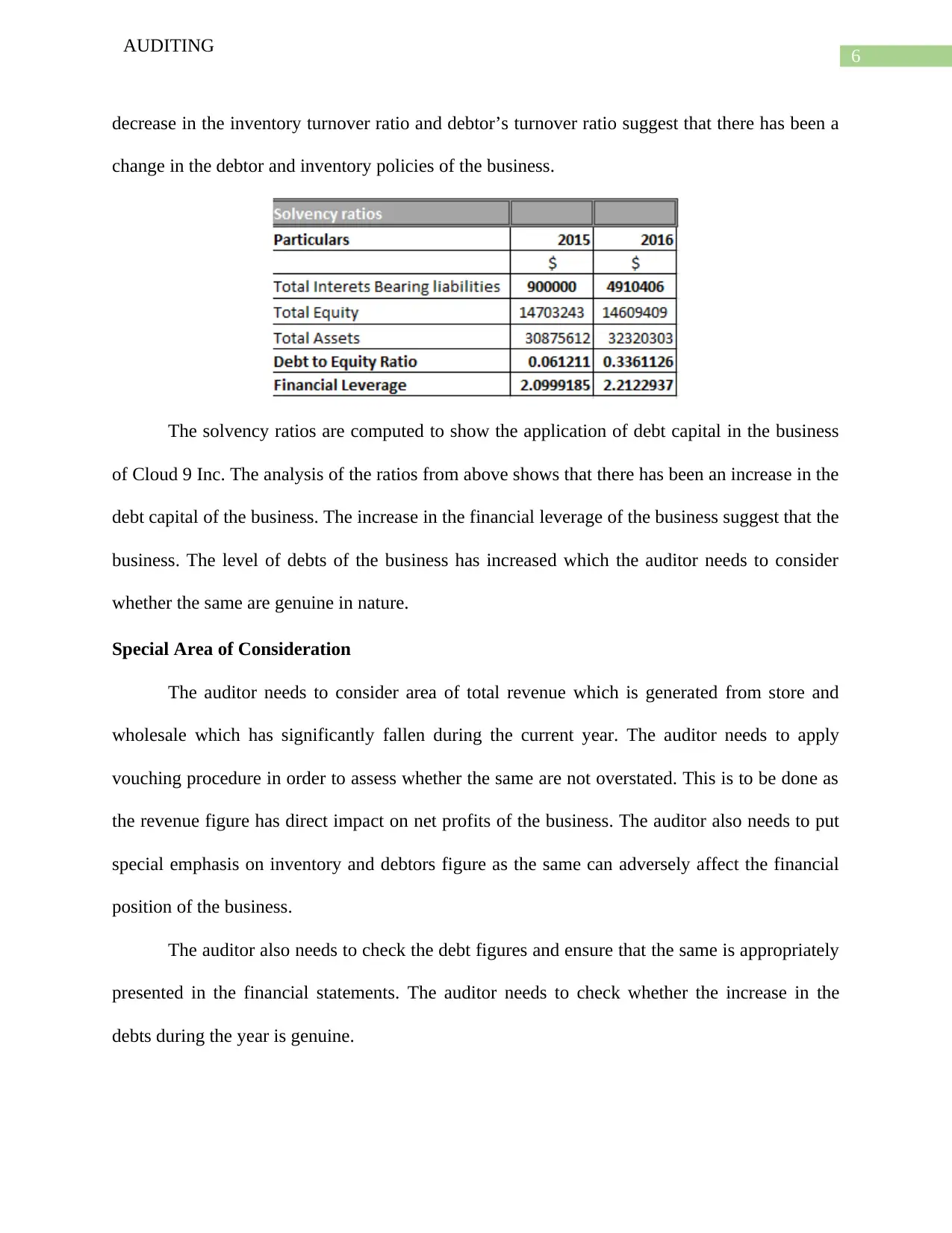

The efficiency ratio of the business is covered with the help of inventory and debtor’s

policy of the business. The inventory turnover ratio of the business is shown to have decreased

significantly and the same is also shown for receivables turnover ratio of the business. The

AUDITING

computed to be 5.06%. This is mainly due to the reduction in costs of the business (Xu et al.

2014). The auditor needs to ensure that the costs of the business are appropriately presented in

the annual reports as they can directly affect the revenues of the business.

The liquidity ratios of the business are computed considering the current assets and

current liabilities of the business. The current ratio and quick ratio of the business is shown to

have significantly improved during the period which suggest that the management of the

company is focusing on liquidity of the business. The liquidity ratios of the business are

considered to be important financial indicators of the business and therefore the auditor needs to

provide special emphasis on such while considering the material misstatement of the business.

The efficiency ratio of the business is covered with the help of inventory and debtor’s

policy of the business. The inventory turnover ratio of the business is shown to have decreased

significantly and the same is also shown for receivables turnover ratio of the business. The

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

AUDITING

decrease in the inventory turnover ratio and debtor’s turnover ratio suggest that there has been a

change in the debtor and inventory policies of the business.

The solvency ratios are computed to show the application of debt capital in the business

of Cloud 9 Inc. The analysis of the ratios from above shows that there has been an increase in the

debt capital of the business. The increase in the financial leverage of the business suggest that the

business. The level of debts of the business has increased which the auditor needs to consider

whether the same are genuine in nature.

Special Area of Consideration

The auditor needs to consider area of total revenue which is generated from store and

wholesale which has significantly fallen during the current year. The auditor needs to apply

vouching procedure in order to assess whether the same are not overstated. This is to be done as

the revenue figure has direct impact on net profits of the business. The auditor also needs to put

special emphasis on inventory and debtors figure as the same can adversely affect the financial

position of the business.

The auditor also needs to check the debt figures and ensure that the same is appropriately

presented in the financial statements. The auditor needs to check whether the increase in the

debts during the year is genuine.

AUDITING

decrease in the inventory turnover ratio and debtor’s turnover ratio suggest that there has been a

change in the debtor and inventory policies of the business.

The solvency ratios are computed to show the application of debt capital in the business

of Cloud 9 Inc. The analysis of the ratios from above shows that there has been an increase in the

debt capital of the business. The increase in the financial leverage of the business suggest that the

business. The level of debts of the business has increased which the auditor needs to consider

whether the same are genuine in nature.

Special Area of Consideration

The auditor needs to consider area of total revenue which is generated from store and

wholesale which has significantly fallen during the current year. The auditor needs to apply

vouching procedure in order to assess whether the same are not overstated. This is to be done as

the revenue figure has direct impact on net profits of the business. The auditor also needs to put

special emphasis on inventory and debtors figure as the same can adversely affect the financial

position of the business.

The auditor also needs to check the debt figures and ensure that the same is appropriately

presented in the financial statements. The auditor needs to check whether the increase in the

debts during the year is genuine.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

AUDITING

Compensation Disclosures

Introduction

The companies which are considered for this part are BHP Billiton Ltd, Boral Ltd and

Ausdrill Ltd which all belongs to mining industry. The annual reports of the business are

considered for identifying the remuneration policies of the companies and also the remunerations

report which is formulated by the business.

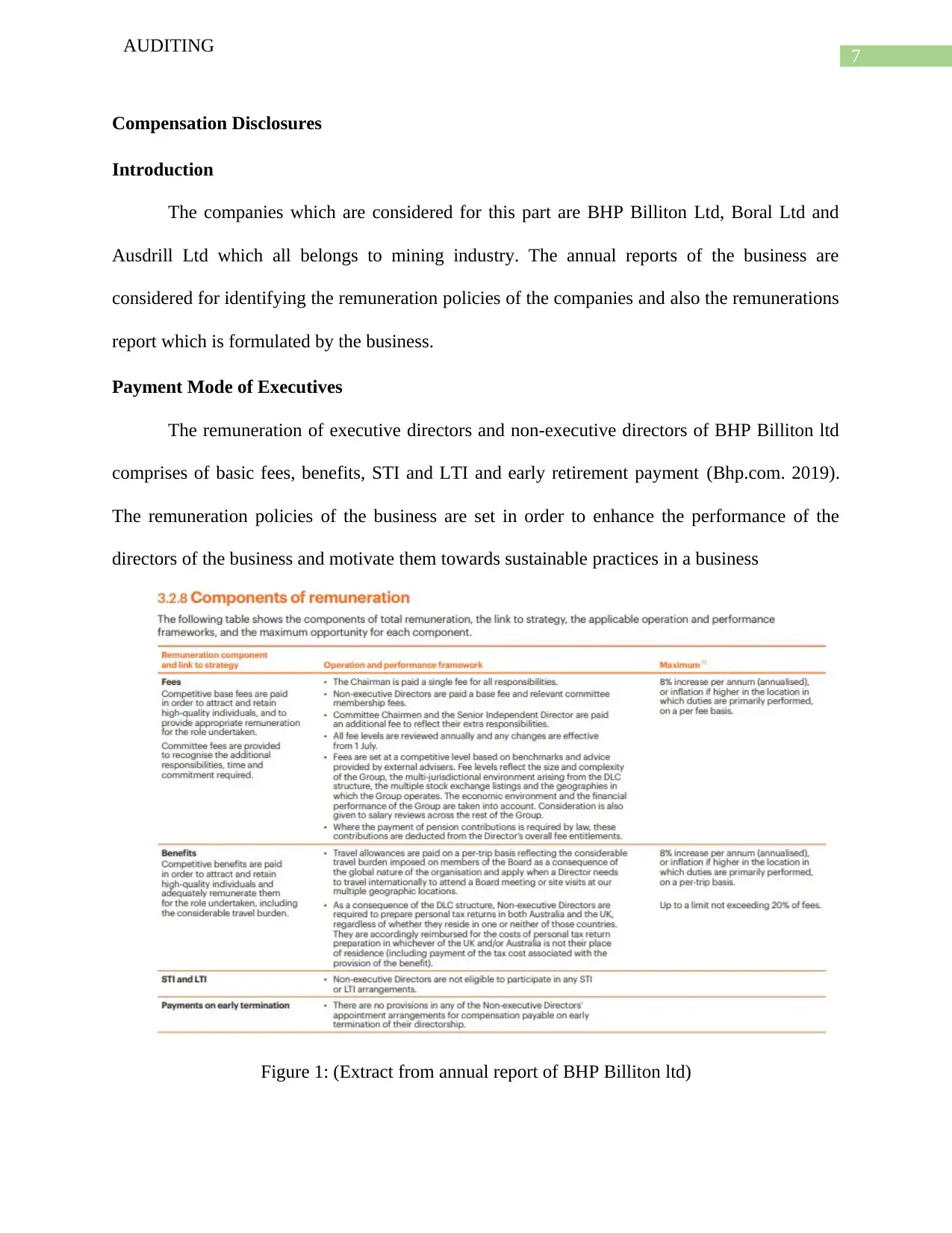

Payment Mode of Executives

The remuneration of executive directors and non-executive directors of BHP Billiton ltd

comprises of basic fees, benefits, STI and LTI and early retirement payment (Bhp.com. 2019).

The remuneration policies of the business are set in order to enhance the performance of the

directors of the business and motivate them towards sustainable practices in a business

Figure 1: (Extract from annual report of BHP Billiton ltd)

AUDITING

Compensation Disclosures

Introduction

The companies which are considered for this part are BHP Billiton Ltd, Boral Ltd and

Ausdrill Ltd which all belongs to mining industry. The annual reports of the business are

considered for identifying the remuneration policies of the companies and also the remunerations

report which is formulated by the business.

Payment Mode of Executives

The remuneration of executive directors and non-executive directors of BHP Billiton ltd

comprises of basic fees, benefits, STI and LTI and early retirement payment (Bhp.com. 2019).

The remuneration policies of the business are set in order to enhance the performance of the

directors of the business and motivate them towards sustainable practices in a business

Figure 1: (Extract from annual report of BHP Billiton ltd)

8

AUDITING

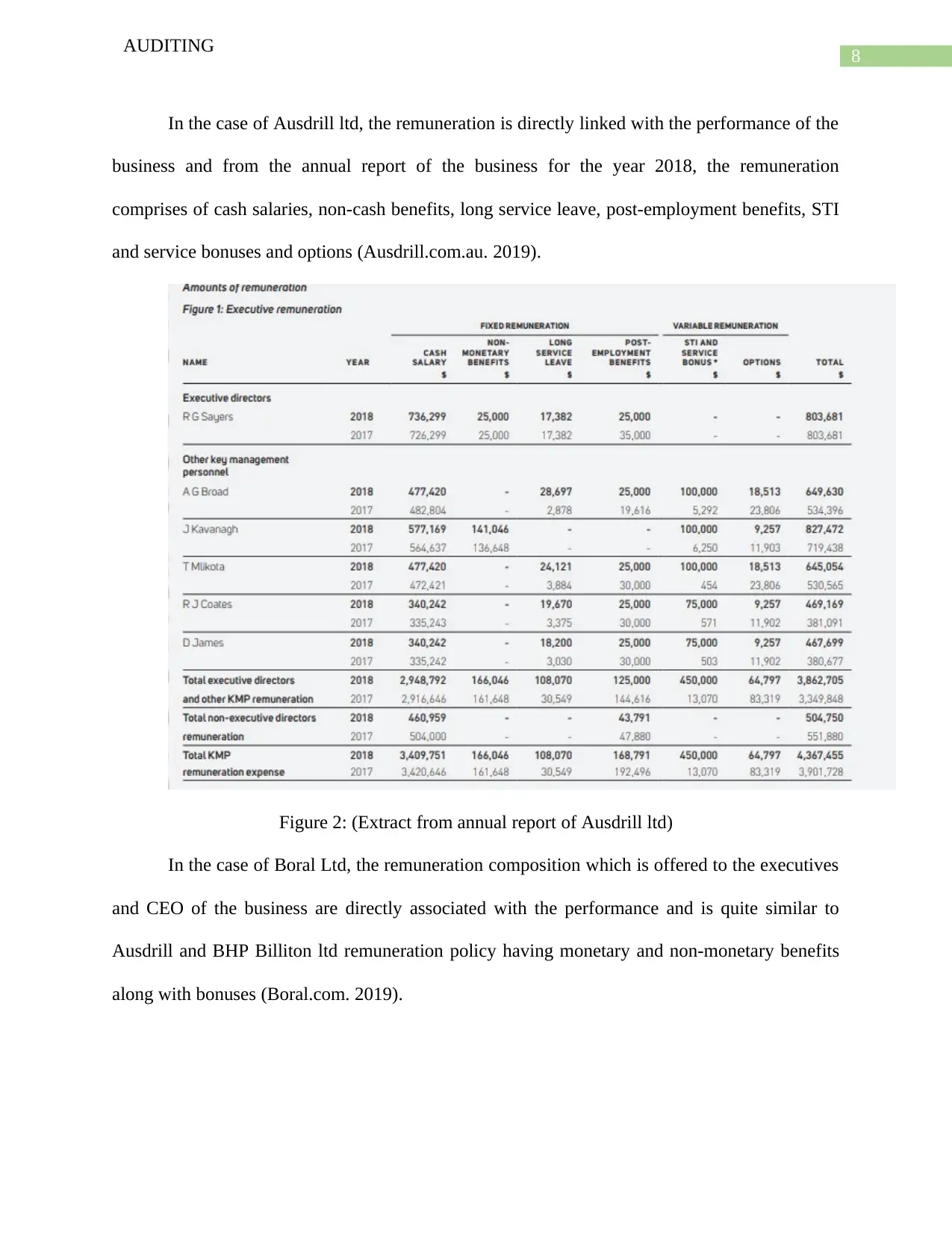

In the case of Ausdrill ltd, the remuneration is directly linked with the performance of the

business and from the annual report of the business for the year 2018, the remuneration

comprises of cash salaries, non-cash benefits, long service leave, post-employment benefits, STI

and service bonuses and options (Ausdrill.com.au. 2019).

Figure 2: (Extract from annual report of Ausdrill ltd)

In the case of Boral Ltd, the remuneration composition which is offered to the executives

and CEO of the business are directly associated with the performance and is quite similar to

Ausdrill and BHP Billiton ltd remuneration policy having monetary and non-monetary benefits

along with bonuses (Boral.com. 2019).

AUDITING

In the case of Ausdrill ltd, the remuneration is directly linked with the performance of the

business and from the annual report of the business for the year 2018, the remuneration

comprises of cash salaries, non-cash benefits, long service leave, post-employment benefits, STI

and service bonuses and options (Ausdrill.com.au. 2019).

Figure 2: (Extract from annual report of Ausdrill ltd)

In the case of Boral Ltd, the remuneration composition which is offered to the executives

and CEO of the business are directly associated with the performance and is quite similar to

Ausdrill and BHP Billiton ltd remuneration policy having monetary and non-monetary benefits

along with bonuses (Boral.com. 2019).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

AUDITING

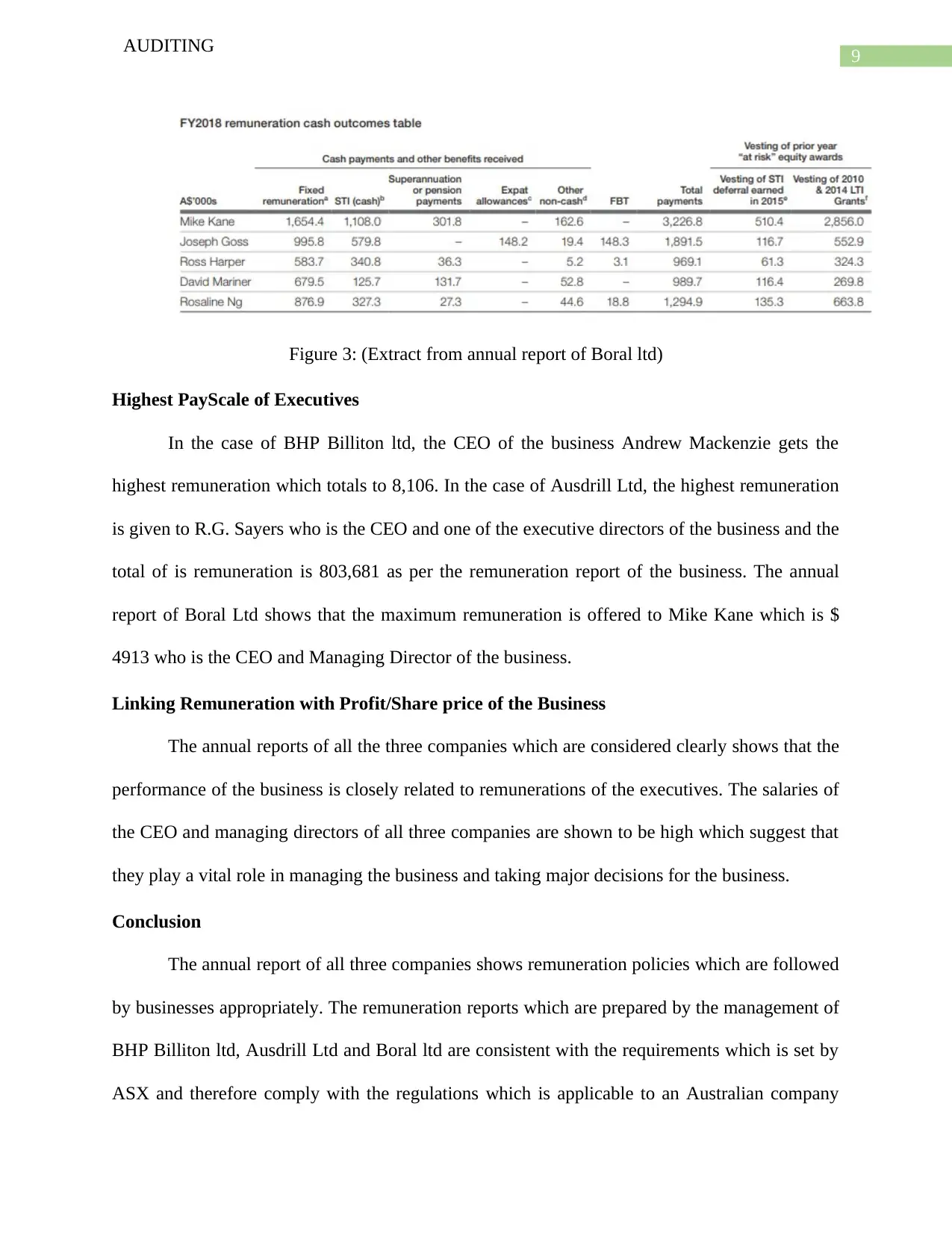

Figure 3: (Extract from annual report of Boral ltd)

Highest PayScale of Executives

In the case of BHP Billiton ltd, the CEO of the business Andrew Mackenzie gets the

highest remuneration which totals to 8,106. In the case of Ausdrill Ltd, the highest remuneration

is given to R.G. Sayers who is the CEO and one of the executive directors of the business and the

total of is remuneration is 803,681 as per the remuneration report of the business. The annual

report of Boral Ltd shows that the maximum remuneration is offered to Mike Kane which is $

4913 who is the CEO and Managing Director of the business.

Linking Remuneration with Profit/Share price of the Business

The annual reports of all the three companies which are considered clearly shows that the

performance of the business is closely related to remunerations of the executives. The salaries of

the CEO and managing directors of all three companies are shown to be high which suggest that

they play a vital role in managing the business and taking major decisions for the business.

Conclusion

The annual report of all three companies shows remuneration policies which are followed

by businesses appropriately. The remuneration reports which are prepared by the management of

BHP Billiton ltd, Ausdrill Ltd and Boral ltd are consistent with the requirements which is set by

ASX and therefore comply with the regulations which is applicable to an Australian company

AUDITING

Figure 3: (Extract from annual report of Boral ltd)

Highest PayScale of Executives

In the case of BHP Billiton ltd, the CEO of the business Andrew Mackenzie gets the

highest remuneration which totals to 8,106. In the case of Ausdrill Ltd, the highest remuneration

is given to R.G. Sayers who is the CEO and one of the executive directors of the business and the

total of is remuneration is 803,681 as per the remuneration report of the business. The annual

report of Boral Ltd shows that the maximum remuneration is offered to Mike Kane which is $

4913 who is the CEO and Managing Director of the business.

Linking Remuneration with Profit/Share price of the Business

The annual reports of all the three companies which are considered clearly shows that the

performance of the business is closely related to remunerations of the executives. The salaries of

the CEO and managing directors of all three companies are shown to be high which suggest that

they play a vital role in managing the business and taking major decisions for the business.

Conclusion

The annual report of all three companies shows remuneration policies which are followed

by businesses appropriately. The remuneration reports which are prepared by the management of

BHP Billiton ltd, Ausdrill Ltd and Boral ltd are consistent with the requirements which is set by

ASX and therefore comply with the regulations which is applicable to an Australian company

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

AUDITING

which is listed. The remuneration of the executive directors and non-executive directors are

appropriately presented in the financial statements of the business.

AUDITING

which is listed. The remuneration of the executive directors and non-executive directors are

appropriately presented in the financial statements of the business.

11

AUDITING

Reference

Ausdrill.com.au. (2019). [online] Available at:

http://www.ausdrill.com.au/files/2018_Ausdrill_Annual_Report.pdf [Accessed 28 Jan. 2019].

Bhp.com. (2019). [online] Available at:

https://www.bhp.com/-/media/documents/investors/annual-reports/2018/

bhpannualreport2018.pdf [Accessed 28 Jan. 2019].

Boral.com. (2019). [online] Available at:

https://www.boral.com/sites/corporate/files/media/field_document/Boral-Annual-Report-

2018.pdf [Accessed 28 Jan. 2019].

Delen, D., Kuzey, C. and Uyar, A., 2013. Measuring firm performance using financial ratios: A

decision tree approach. Expert Systems with Applications, 40(10), pp.3970-3983.

Edmonds, T.P., McNair, F.M., Olds, P.R. and Milam, E.E., 2013. Fundamental financial

accounting concepts. New York, NY: McGraw-Hill Irwin.

Eilifsen, A. and Messier Jr, W.F., 2014. Materiality guidance of the major public accounting

firms. Auditing: A Journal of Practice & Theory, 34(2), pp.3-26.

Elder, R.J., Akresh, A.D., Glover, S.M., Higgs, J.L. and Liljegren, J., 2013. Audit sampling

research: A synthesis and implications for future research. Auditing: A Journal of Practice &

Theory, 32(sp1), pp.99-129.

Glover, S.M., Prawitt, D.F. and Drake, M.S., 2014. Between a rock and a hard place: A path

forward for using substantive analytical procedures in auditing large P&L accounts:

Commentary and analysis. Auditing: A Journal of Practice & Theory, 34(3), pp.161-179.

Xu, W., Xiao, Z., Dang, X., Yang, D. and Yang, X., 2014. Financial ratio selection for business

failure prediction using soft set theory. Knowledge-Based Systems, 63, pp.59-67.

AUDITING

Reference

Ausdrill.com.au. (2019). [online] Available at:

http://www.ausdrill.com.au/files/2018_Ausdrill_Annual_Report.pdf [Accessed 28 Jan. 2019].

Bhp.com. (2019). [online] Available at:

https://www.bhp.com/-/media/documents/investors/annual-reports/2018/

bhpannualreport2018.pdf [Accessed 28 Jan. 2019].

Boral.com. (2019). [online] Available at:

https://www.boral.com/sites/corporate/files/media/field_document/Boral-Annual-Report-

2018.pdf [Accessed 28 Jan. 2019].

Delen, D., Kuzey, C. and Uyar, A., 2013. Measuring firm performance using financial ratios: A

decision tree approach. Expert Systems with Applications, 40(10), pp.3970-3983.

Edmonds, T.P., McNair, F.M., Olds, P.R. and Milam, E.E., 2013. Fundamental financial

accounting concepts. New York, NY: McGraw-Hill Irwin.

Eilifsen, A. and Messier Jr, W.F., 2014. Materiality guidance of the major public accounting

firms. Auditing: A Journal of Practice & Theory, 34(2), pp.3-26.

Elder, R.J., Akresh, A.D., Glover, S.M., Higgs, J.L. and Liljegren, J., 2013. Audit sampling

research: A synthesis and implications for future research. Auditing: A Journal of Practice &

Theory, 32(sp1), pp.99-129.

Glover, S.M., Prawitt, D.F. and Drake, M.S., 2014. Between a rock and a hard place: A path

forward for using substantive analytical procedures in auditing large P&L accounts:

Commentary and analysis. Auditing: A Journal of Practice & Theory, 34(3), pp.161-179.

Xu, W., Xiao, Z., Dang, X., Yang, D. and Yang, X., 2014. Financial ratio selection for business

failure prediction using soft set theory. Knowledge-Based Systems, 63, pp.59-67.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.