ACCT20073 Company Accounting: Financial Statement Consolidation

VerifiedAdded on 2023/06/07

|7

|996

|82

Homework Assignment

AI Summary

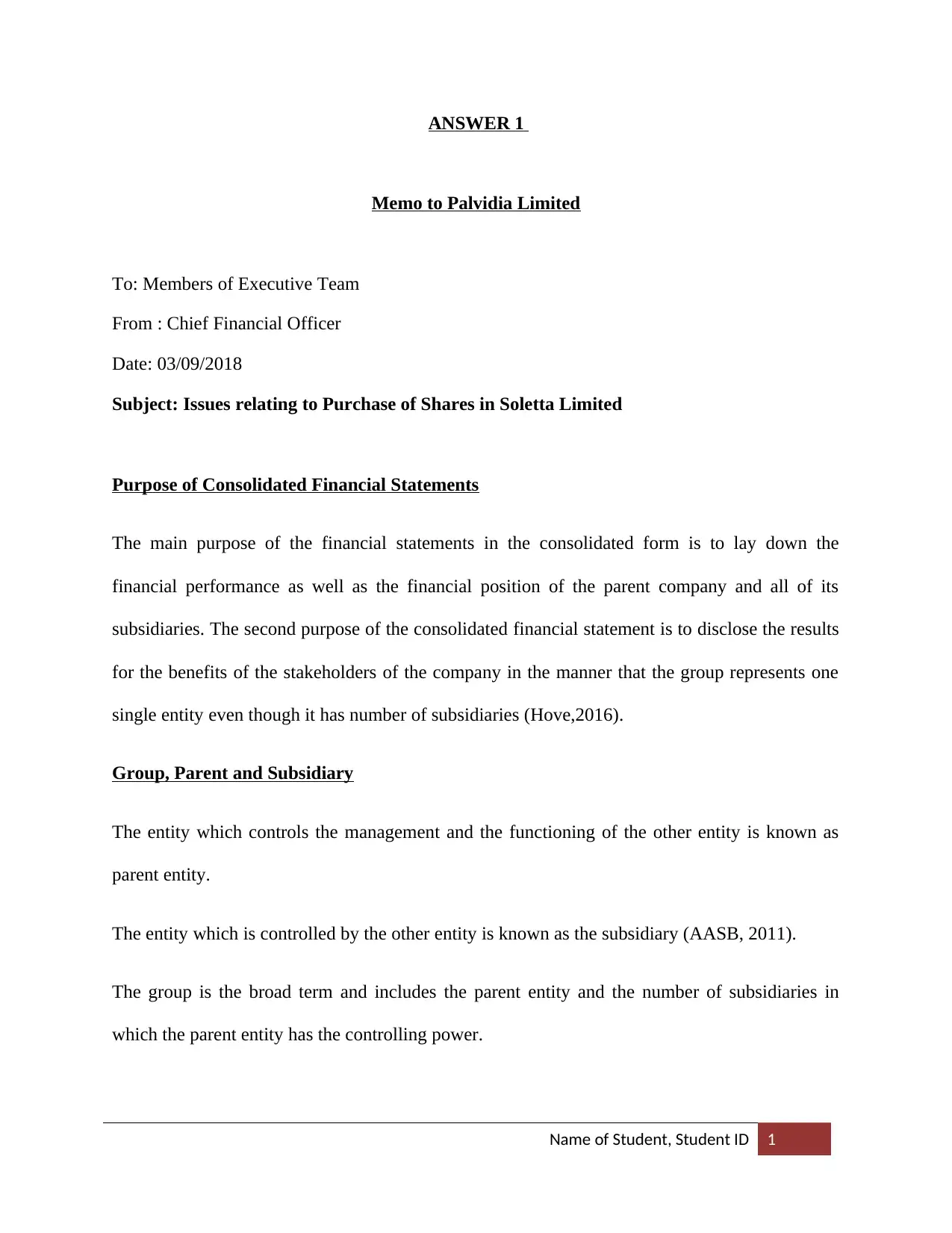

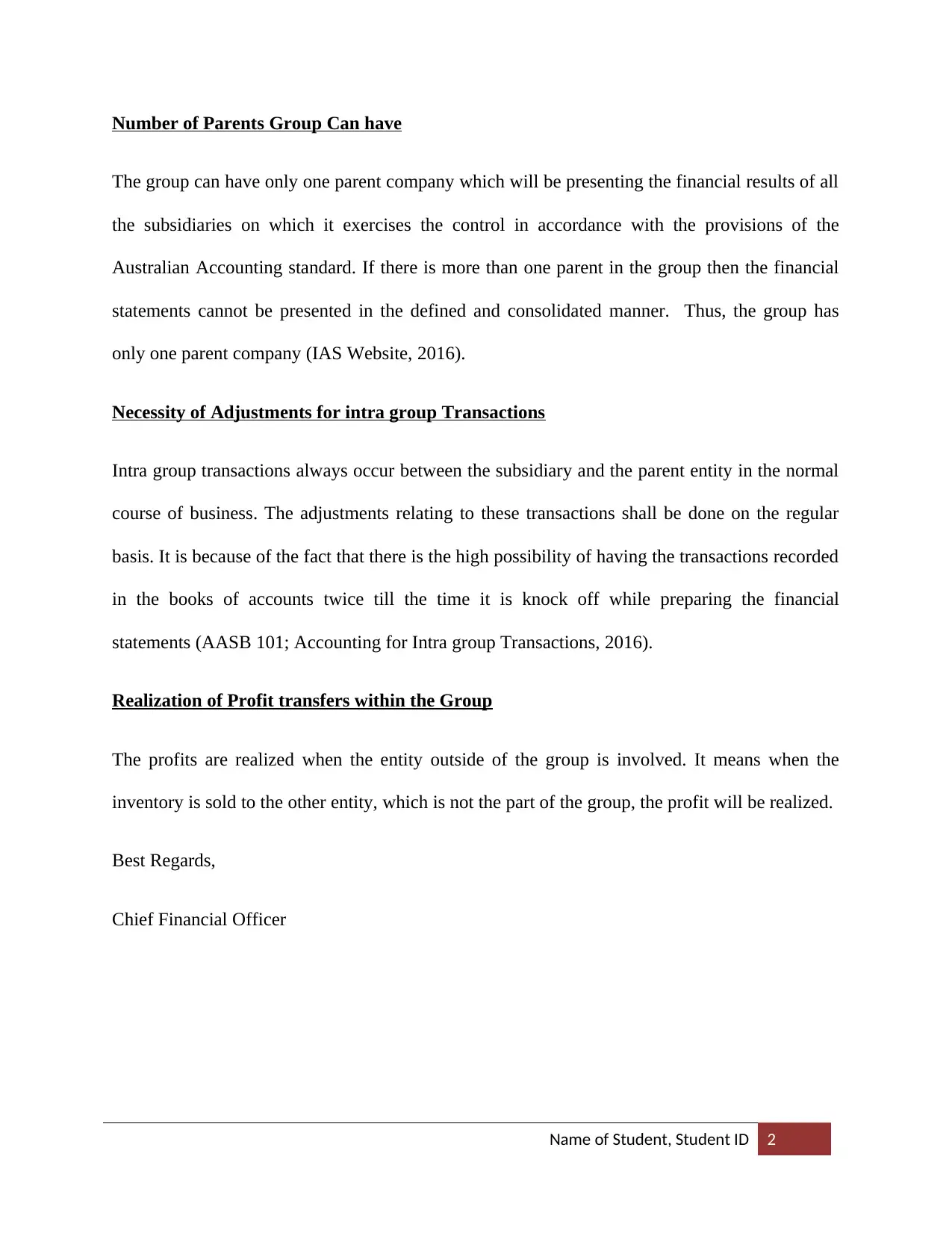

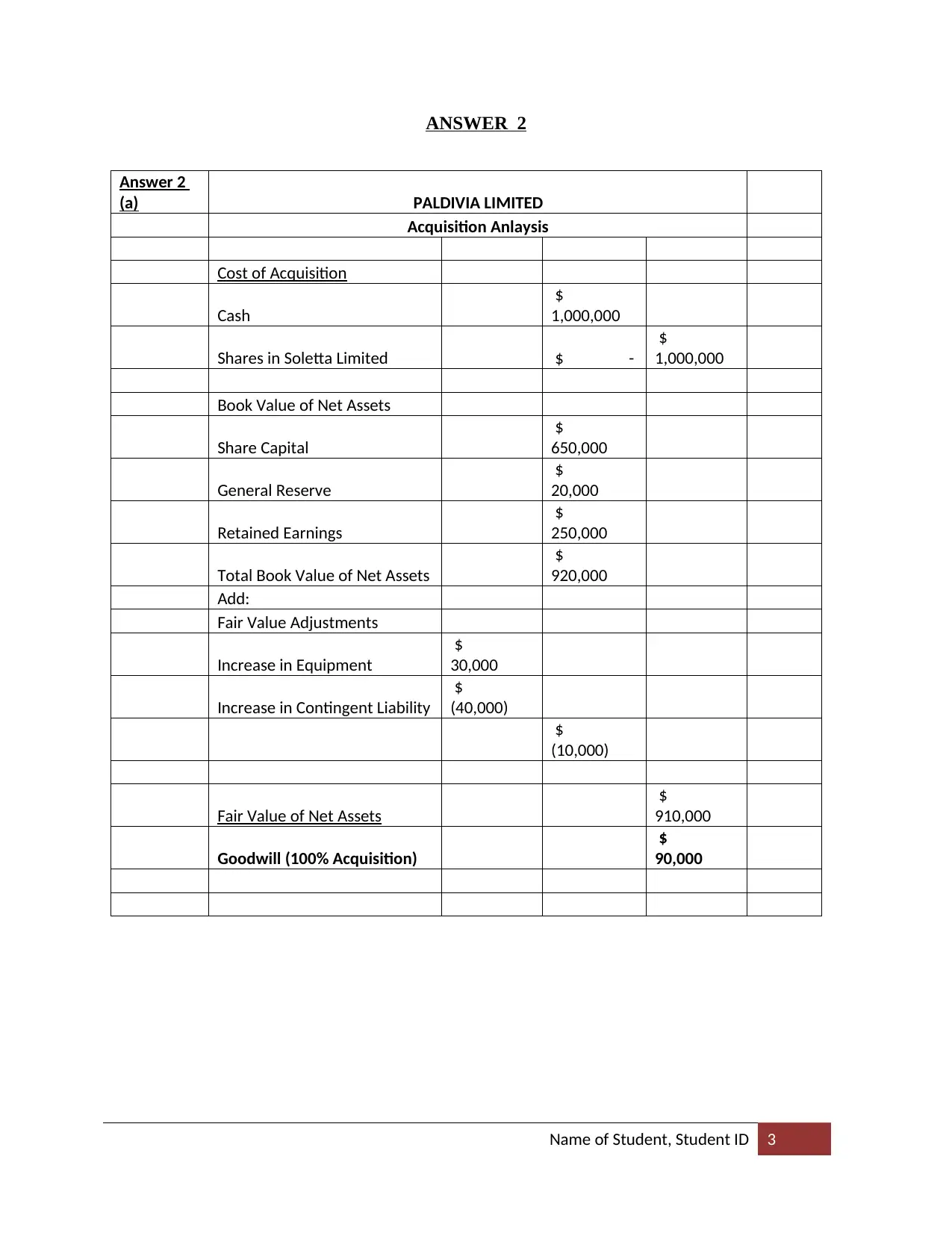

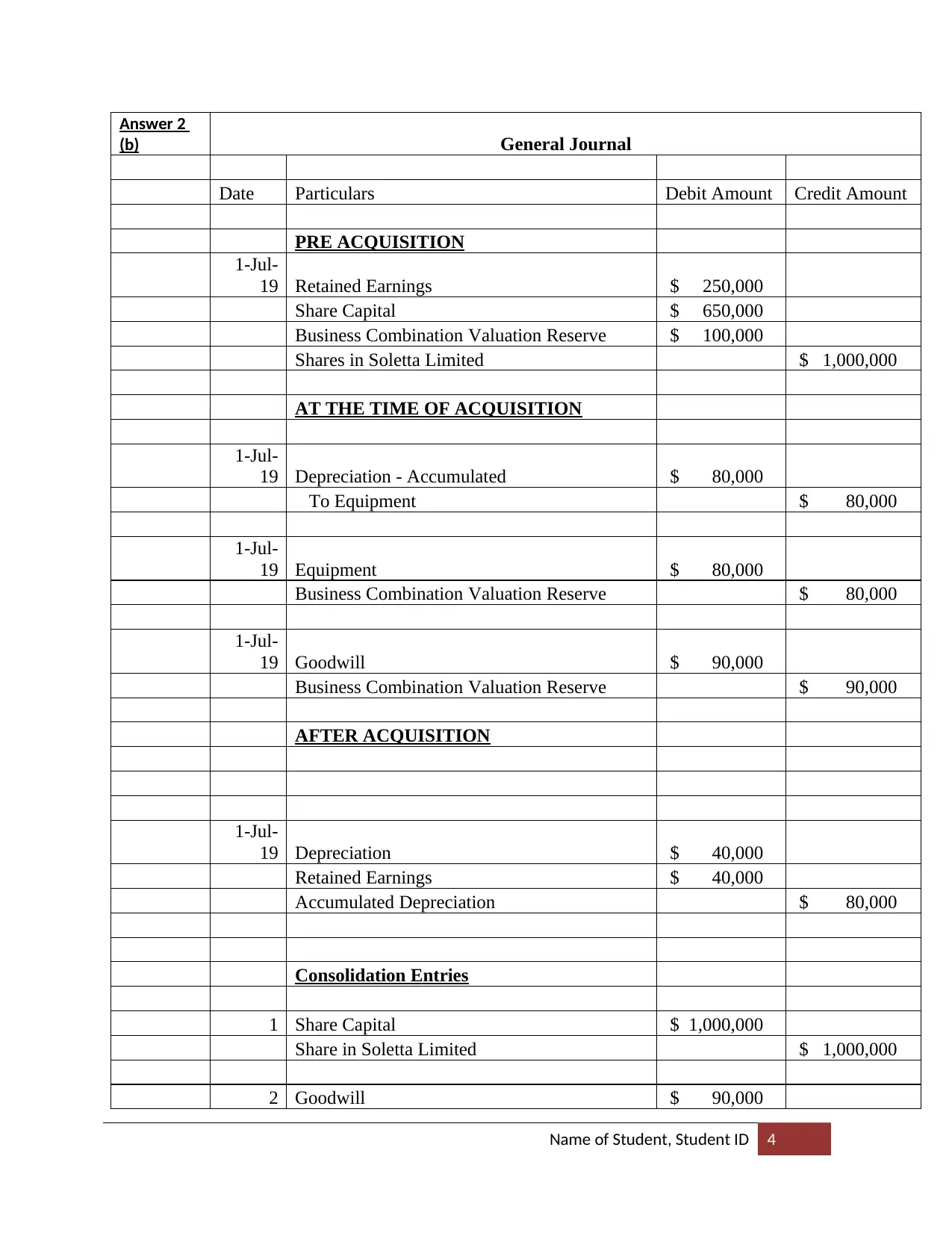

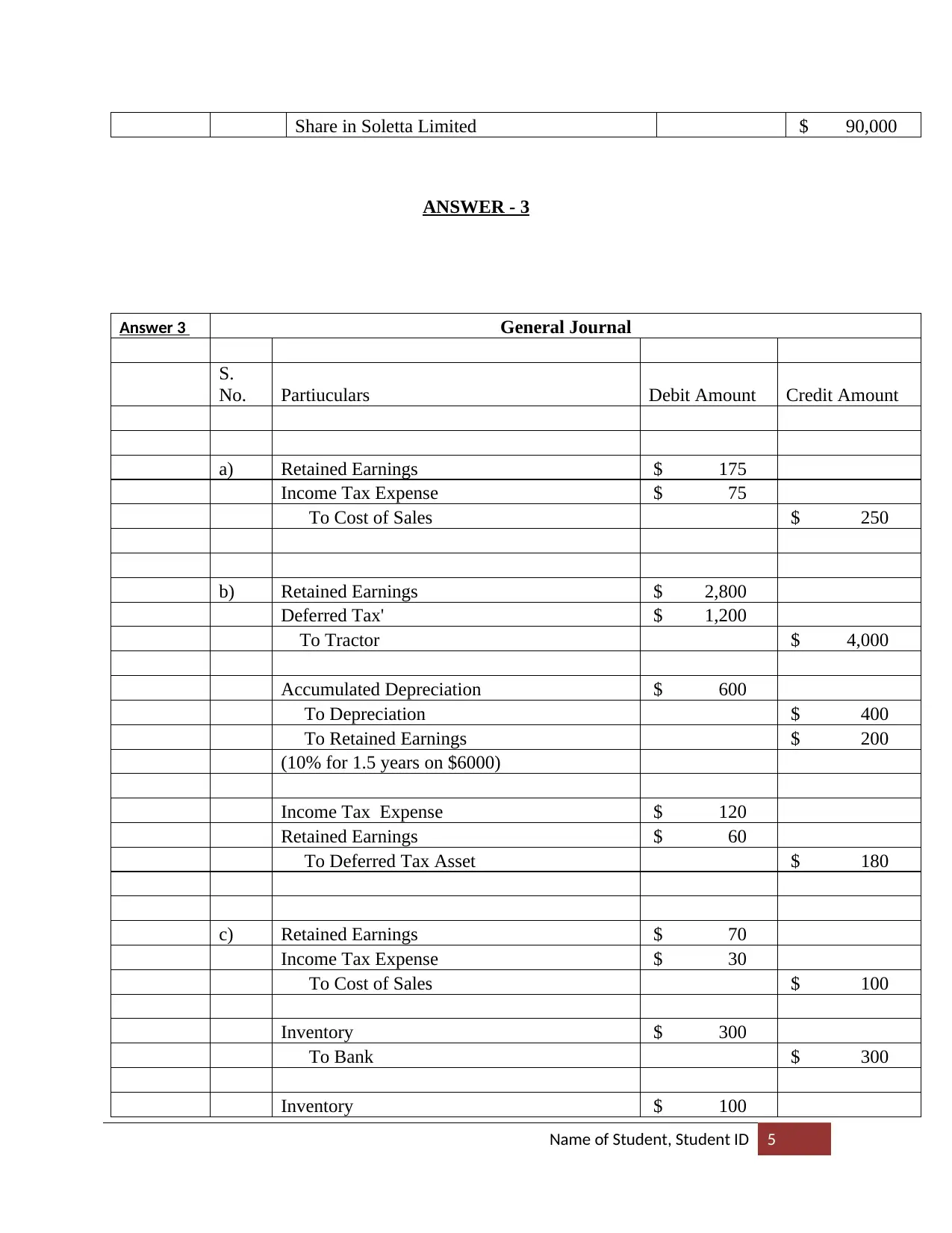

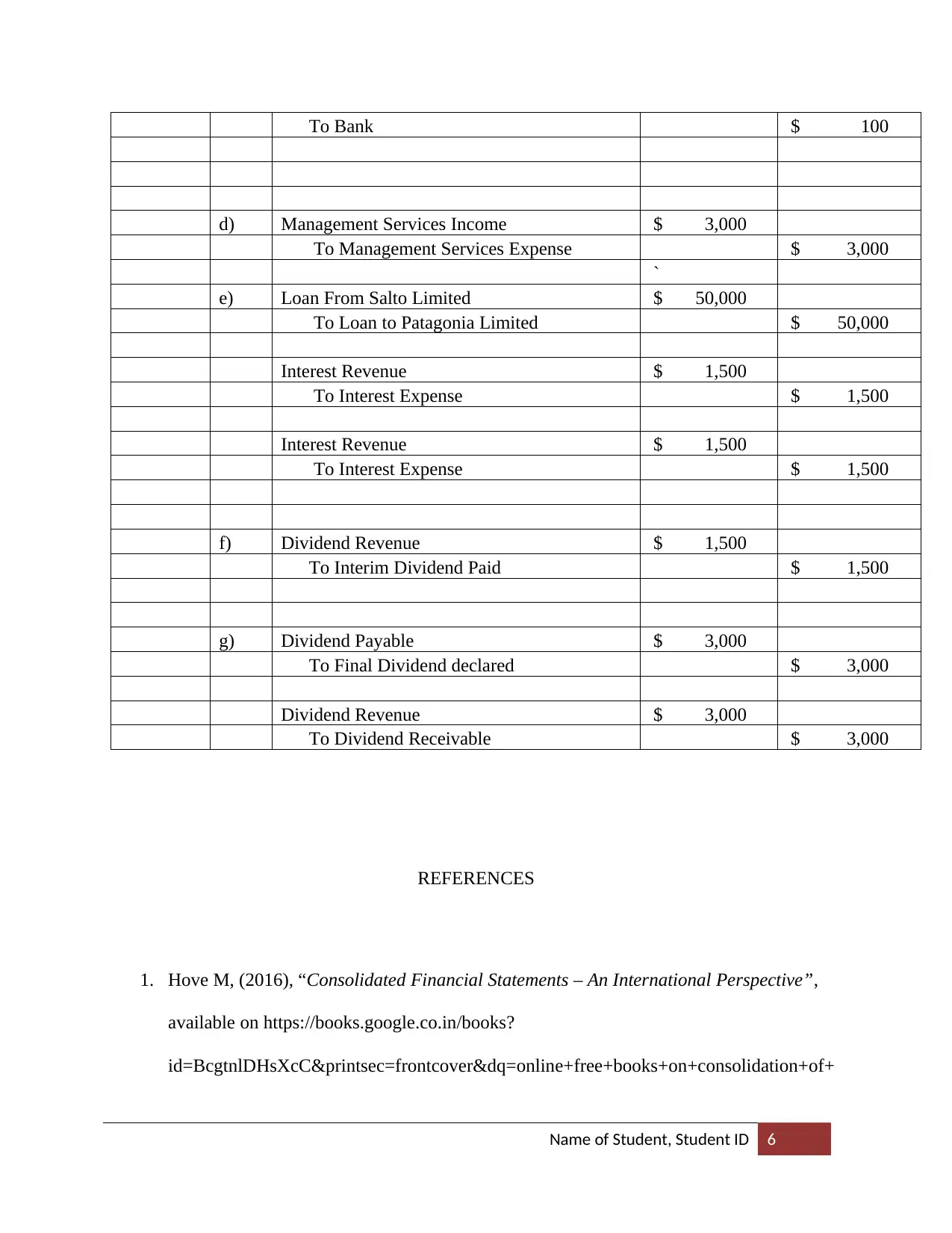

This assignment solution addresses various aspects of consolidated financial statements, including the purpose of consolidation, definitions of group, parent, and subsidiary, and the necessity of adjustments for intra-group transactions. It includes a memo discussing issues related to the purchase of shares in Soletta Limited, an acquisition analysis calculating goodwill, and general journal entries for pre-acquisition, at the time of acquisition, and post-acquisition adjustments. Furthermore, it covers consolidation entries and adjustments related to retained earnings, income tax, depreciation, management services, loans, interest revenue, and dividends. The solution provides detailed calculations and journal entries to illustrate the consolidation process and the accounting treatment of intra-group transactions.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.