Auditing Assignment: Financial Statement Analysis and Ratios

VerifiedAdded on 2019/11/08

|7

|1601

|165

Homework Assignment

AI Summary

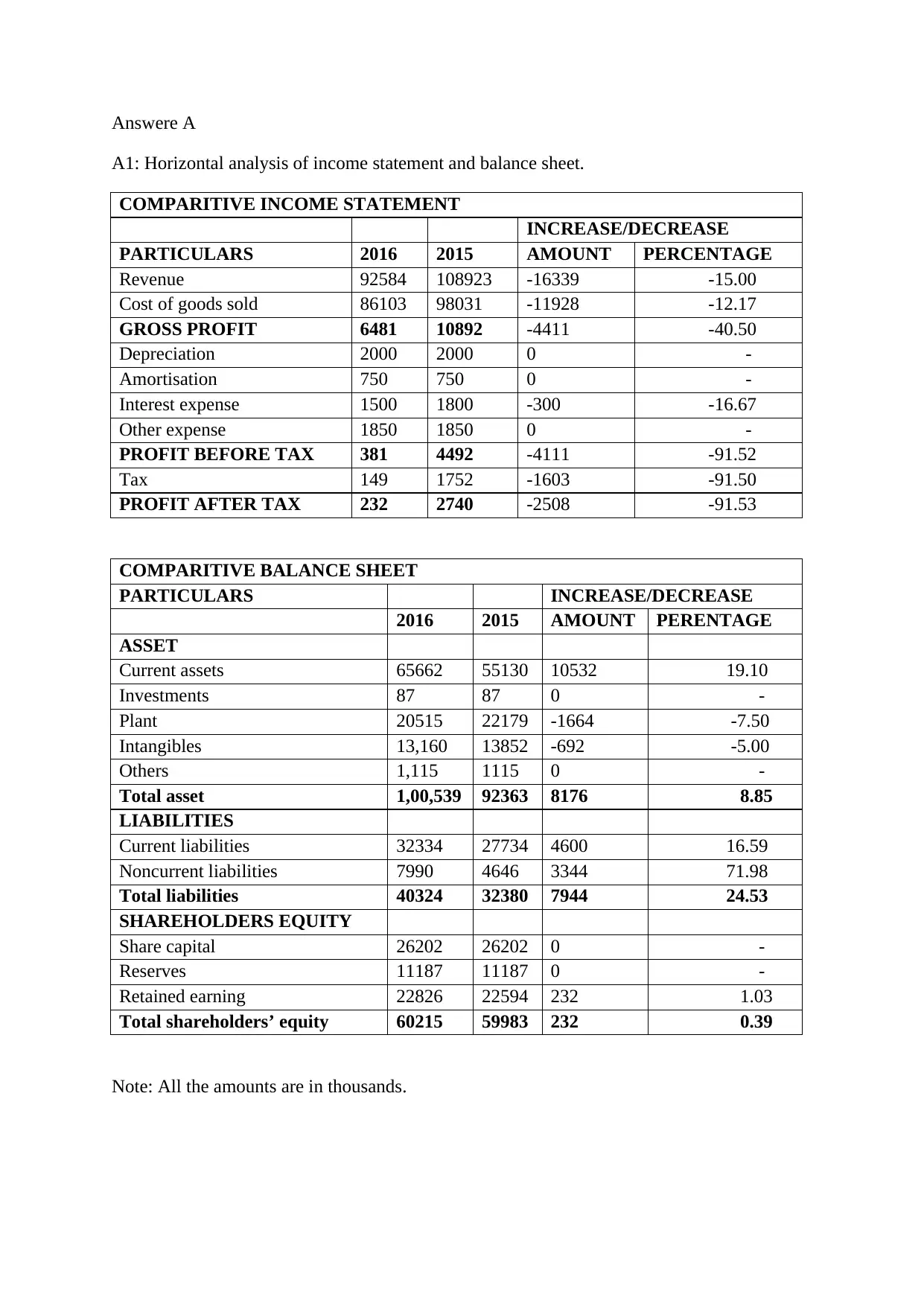

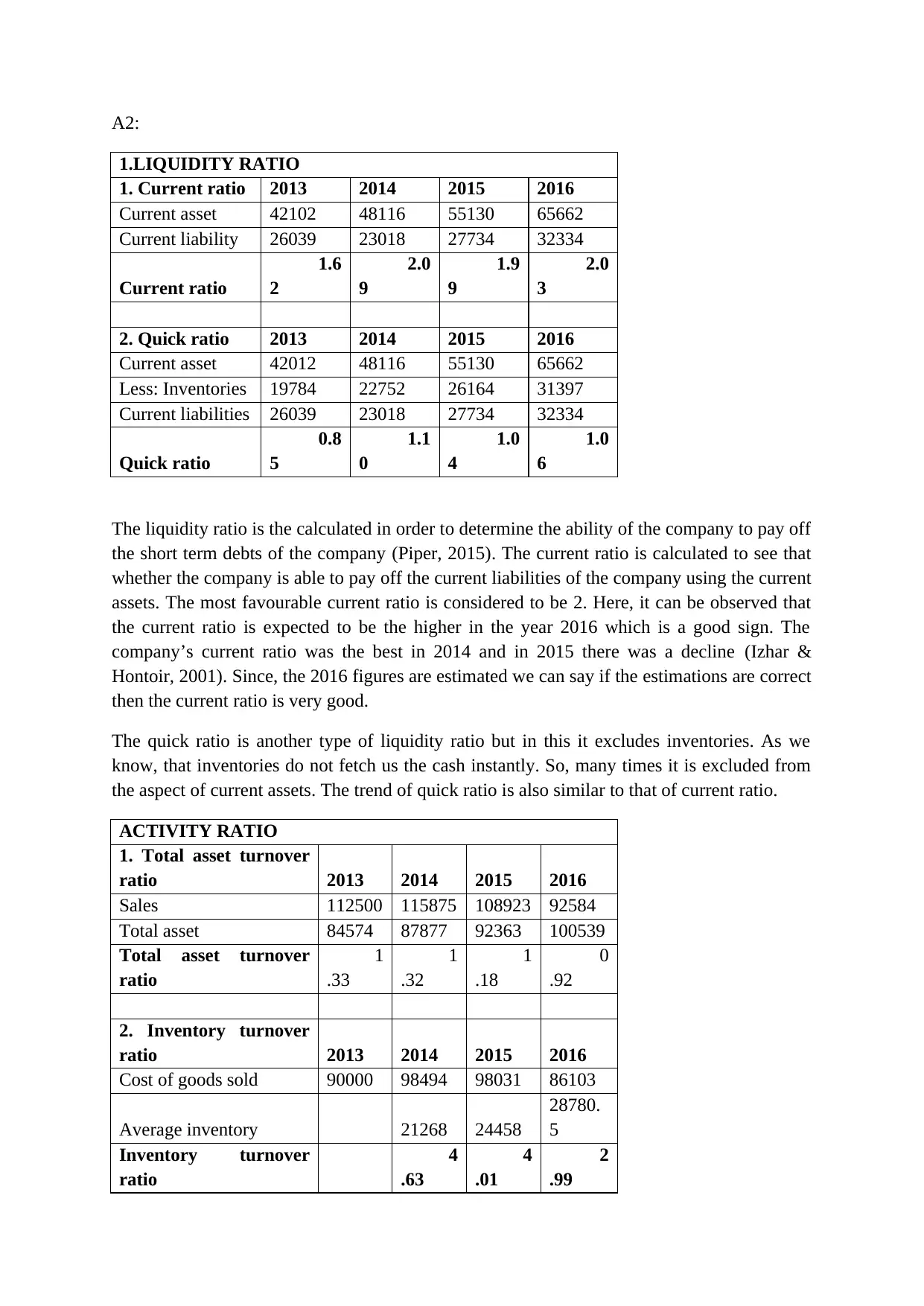

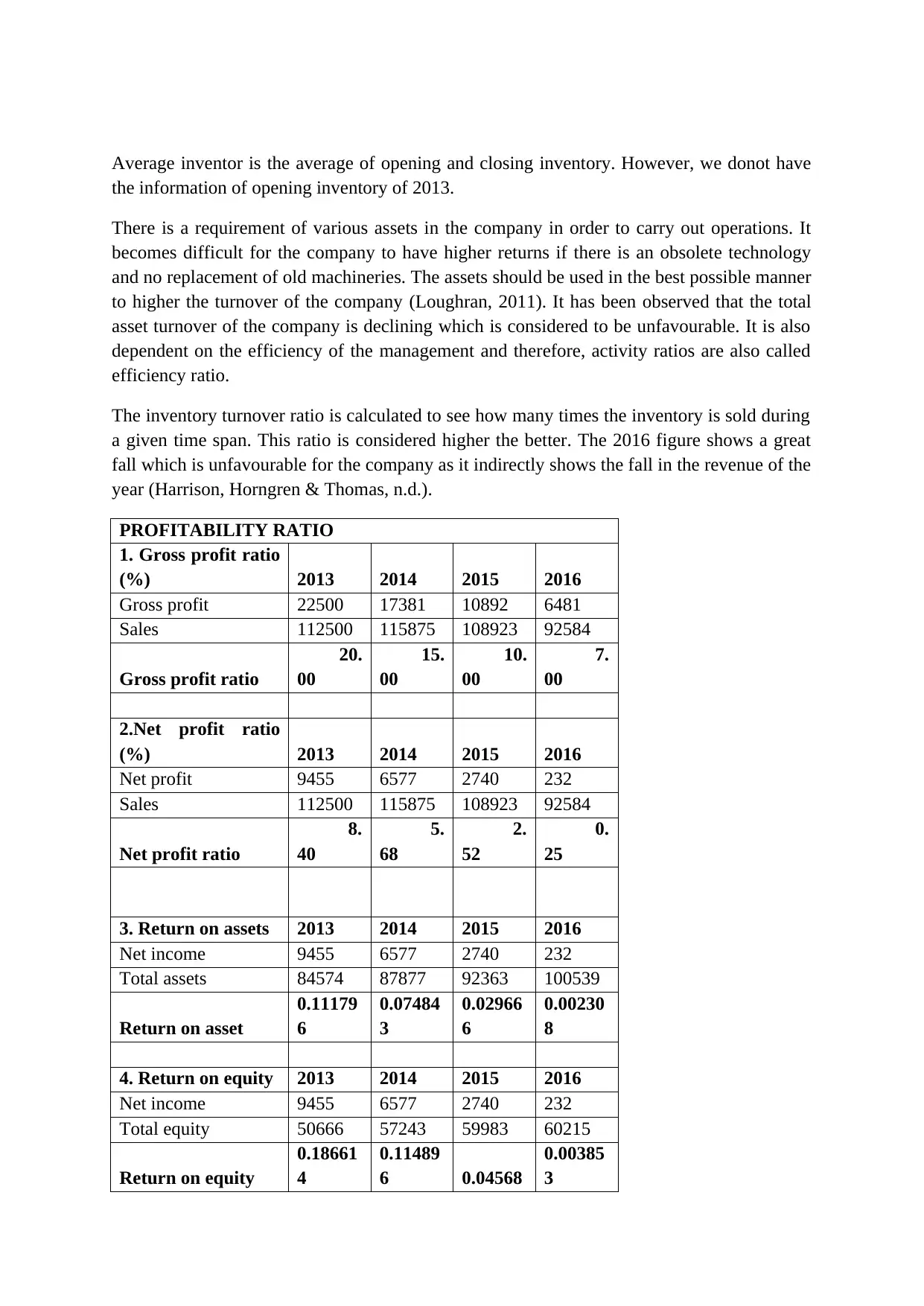

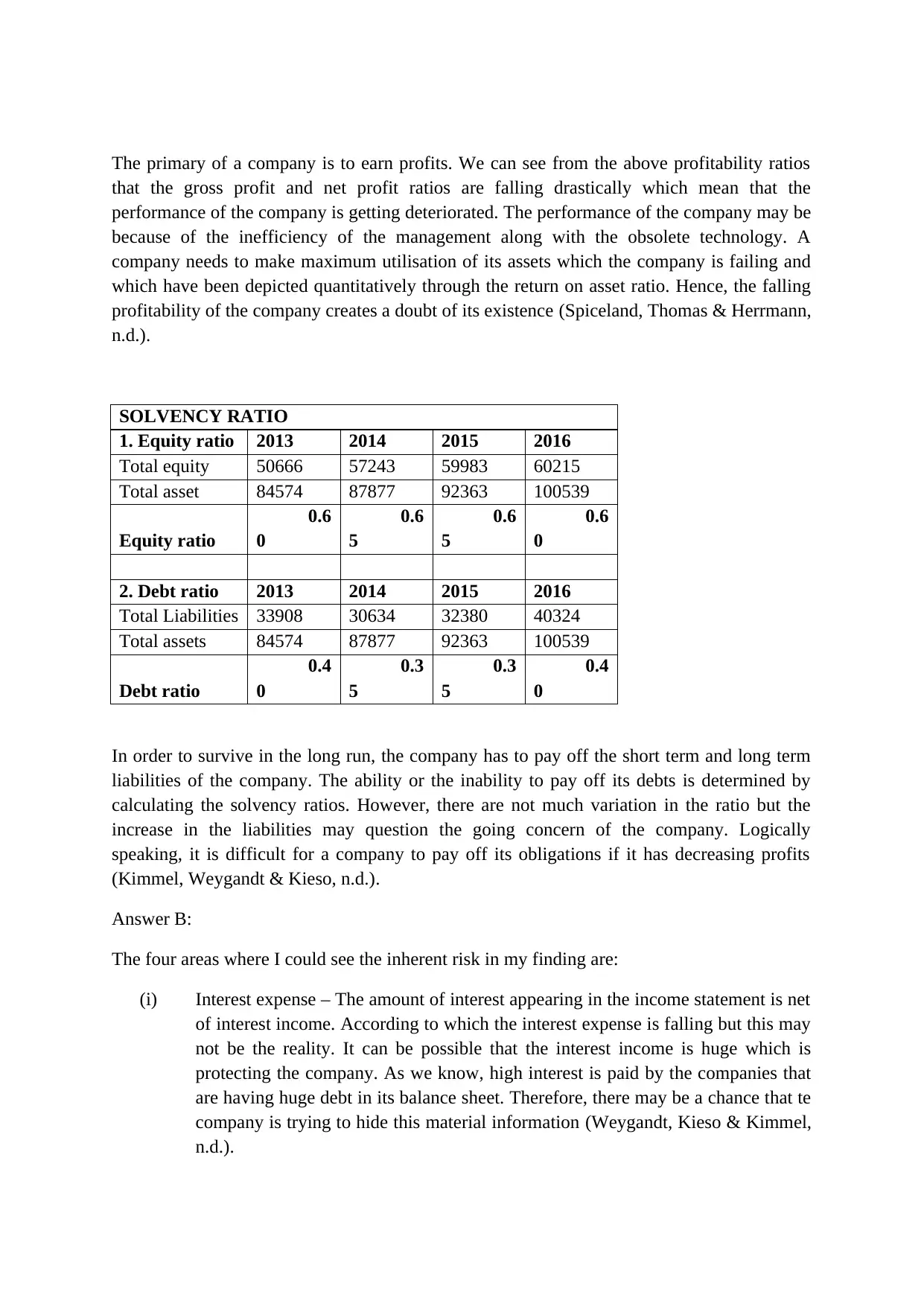

This auditing assignment provides a comparative financial analysis of income statements and balance sheets, including horizontal analysis to identify trends. It calculates and interprets various financial ratios, such as current, quick, total asset turnover, inventory turnover, gross profit, net profit, return on assets, return on equity, equity, and debt ratios over a period of time. The assignment assesses liquidity, activity, profitability, and solvency. The analysis identifies potential risks within the financial data, focusing on interest expense, intangibles, revenue and gross profit discrepancies, and the reliance on estimated figures. The document references key financial accounting principles and includes a list of cited sources for further study. This assignment is a valuable resource for students on Desklib, offering a comprehensive understanding of financial statement analysis and auditing principles.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.