Cost Accounting Assignment: Comparing Costing Methods and Analysis

VerifiedAdded on 2019/11/25

|4

|1222

|301

Homework Assignment

AI Summary

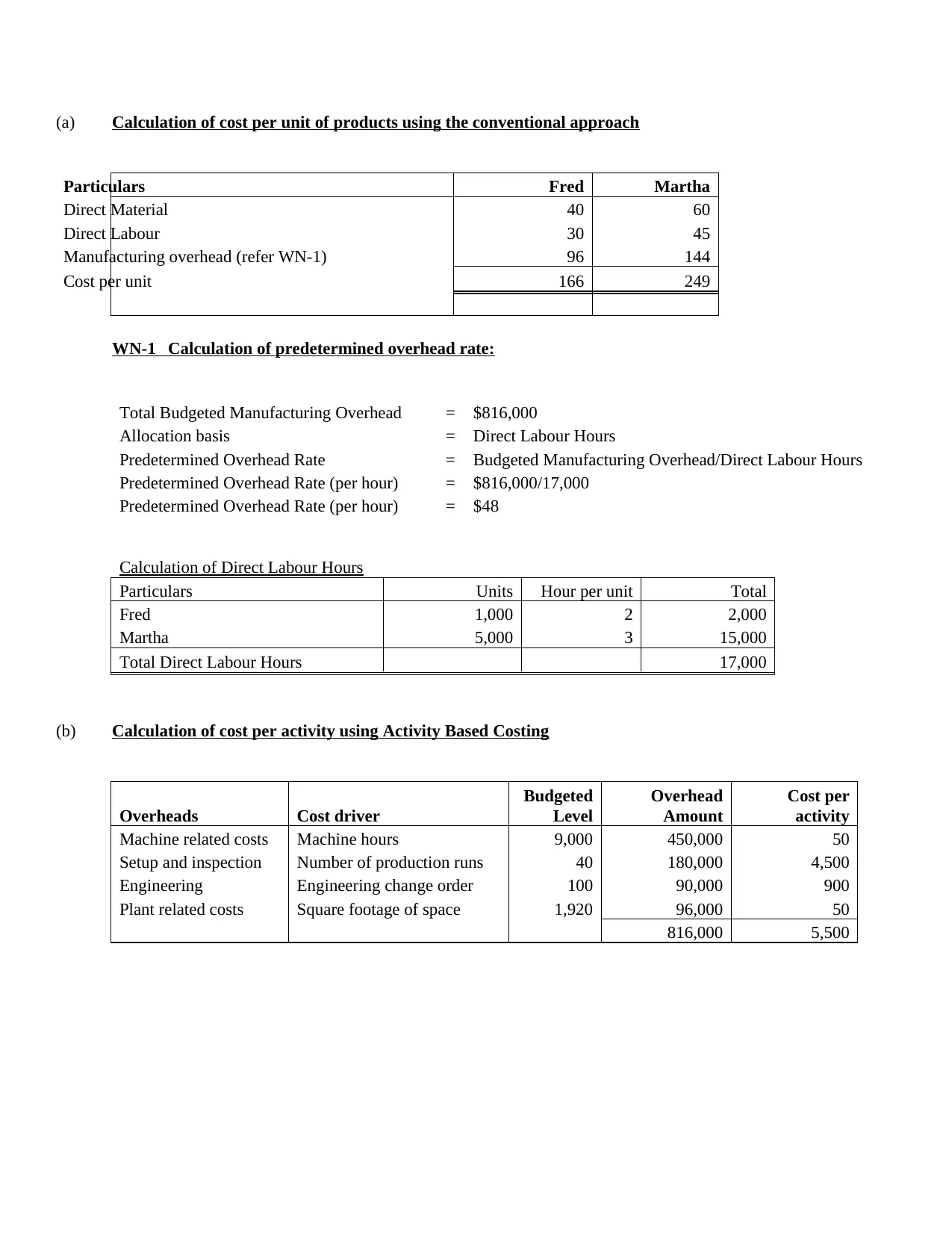

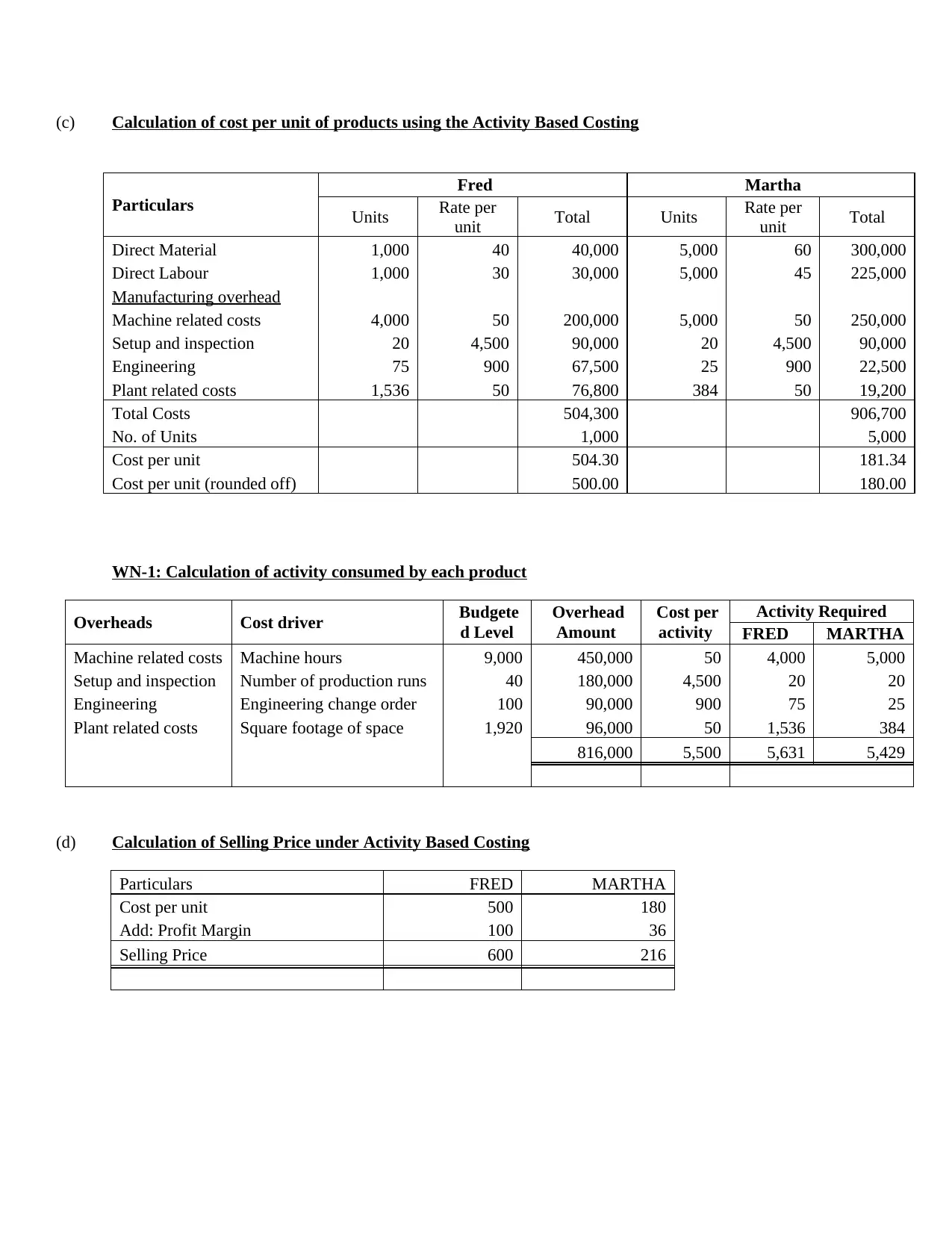

This assignment solution demonstrates the calculation of cost per unit for two products, Fred and Martha, using both conventional and activity-based costing (ABC) methods. The conventional approach utilizes a predetermined overhead rate based on direct labor hours, while ABC allocates overhead based on specific activities and cost drivers, such as machine hours and the number of production runs. The solution includes detailed calculations of overhead rates, cost per unit under both methods, and a comparison highlighting the differences in cost allocation. The analysis reveals that the conventional method can lead to under- or over-costing due to its reliance on a single allocation base, whereas ABC provides a more accurate representation of costs by considering the actual resources consumed by each product. Furthermore, the assignment discusses the advantages of ABC, such as process improvement, scientific cost allocation, and competitive pricing, while also acknowledging its disadvantages, including high implementation costs, data accuracy concerns, and the lengthy implementation process. The solution concludes by comparing the selling prices of the products under ABC and emphasizes the importance of accurate cost allocation for effective management decision-making.

1 out of 4

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.