Corporate Accounting Report: Acquisition Analysis and Journal Entries

VerifiedAdded on 2023/04/24

|7

|763

|290

Report

AI Summary

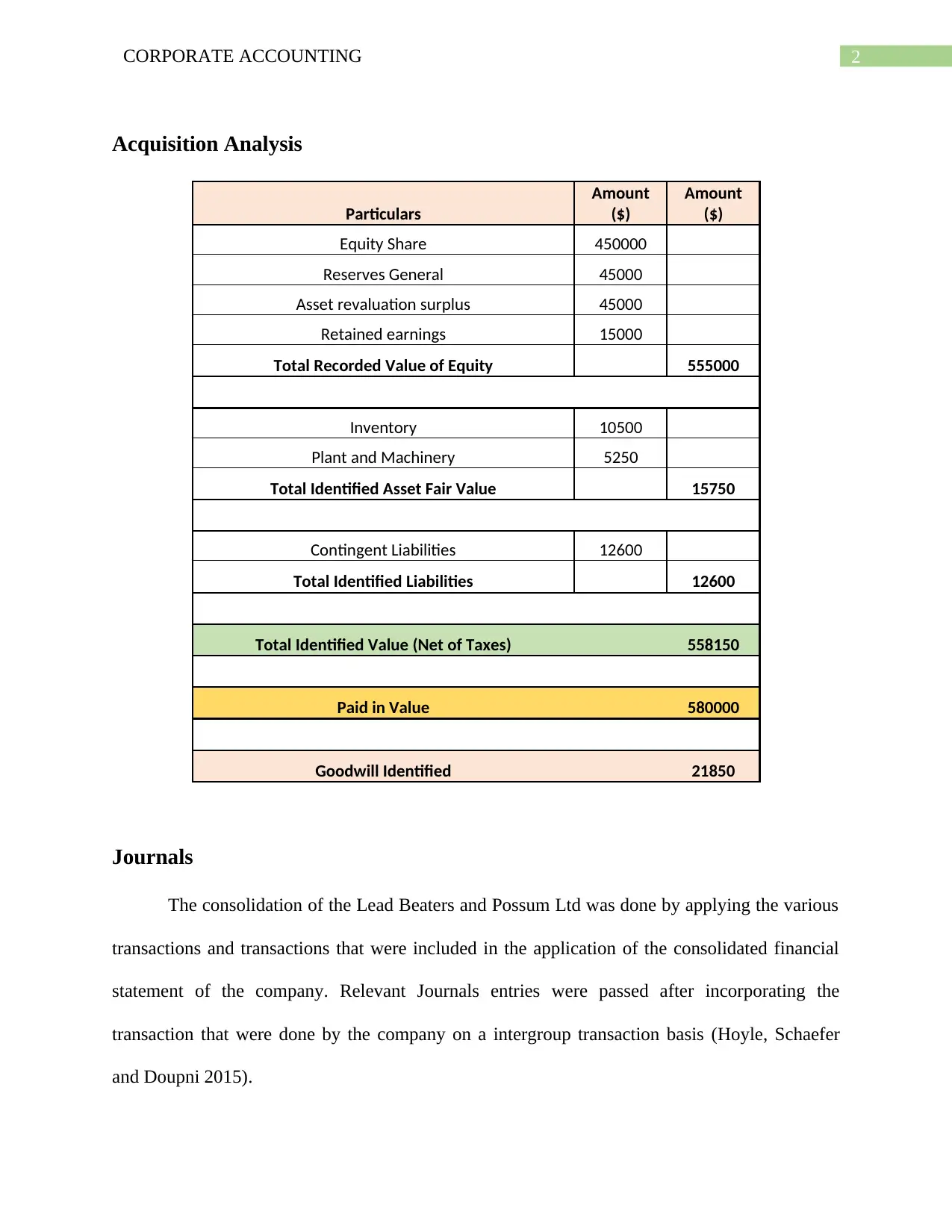

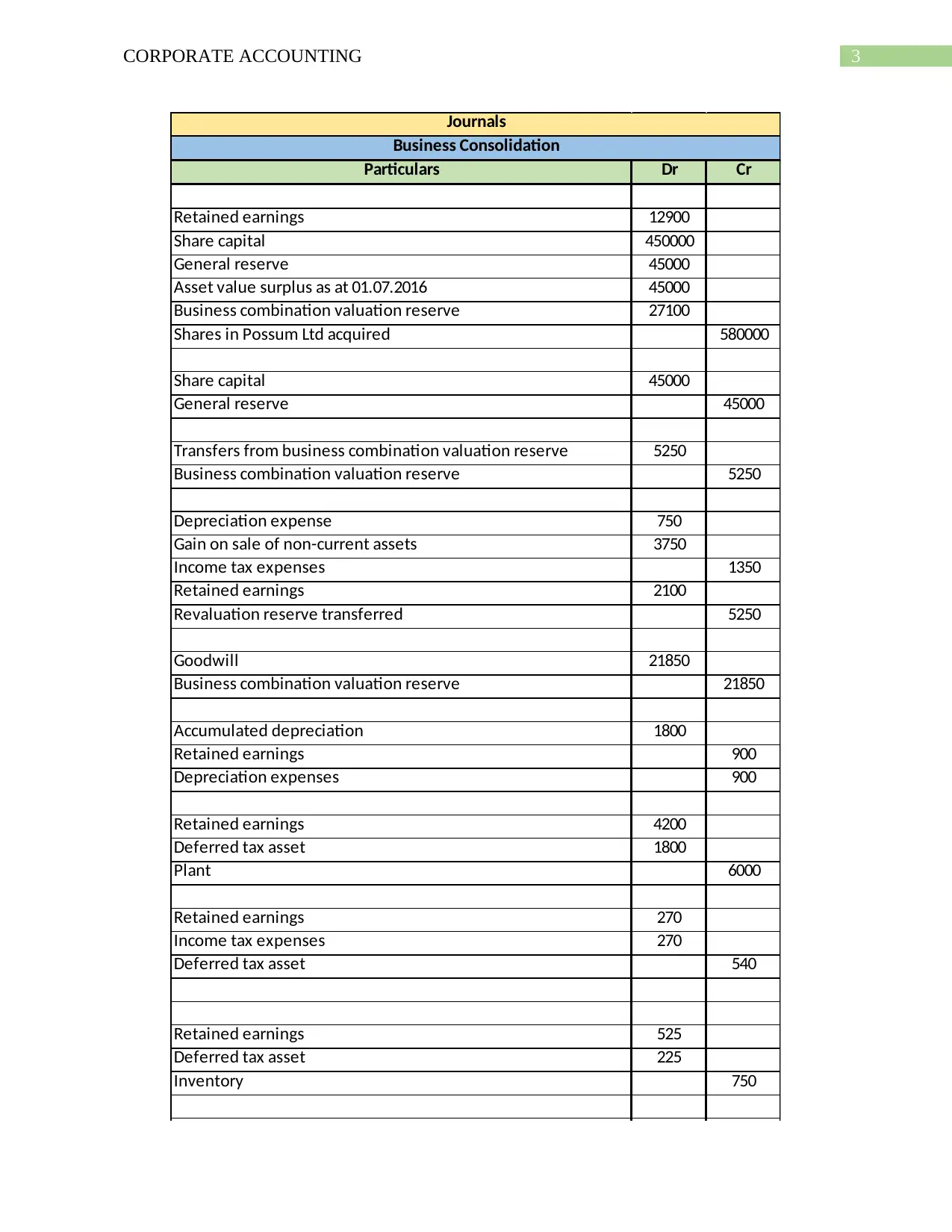

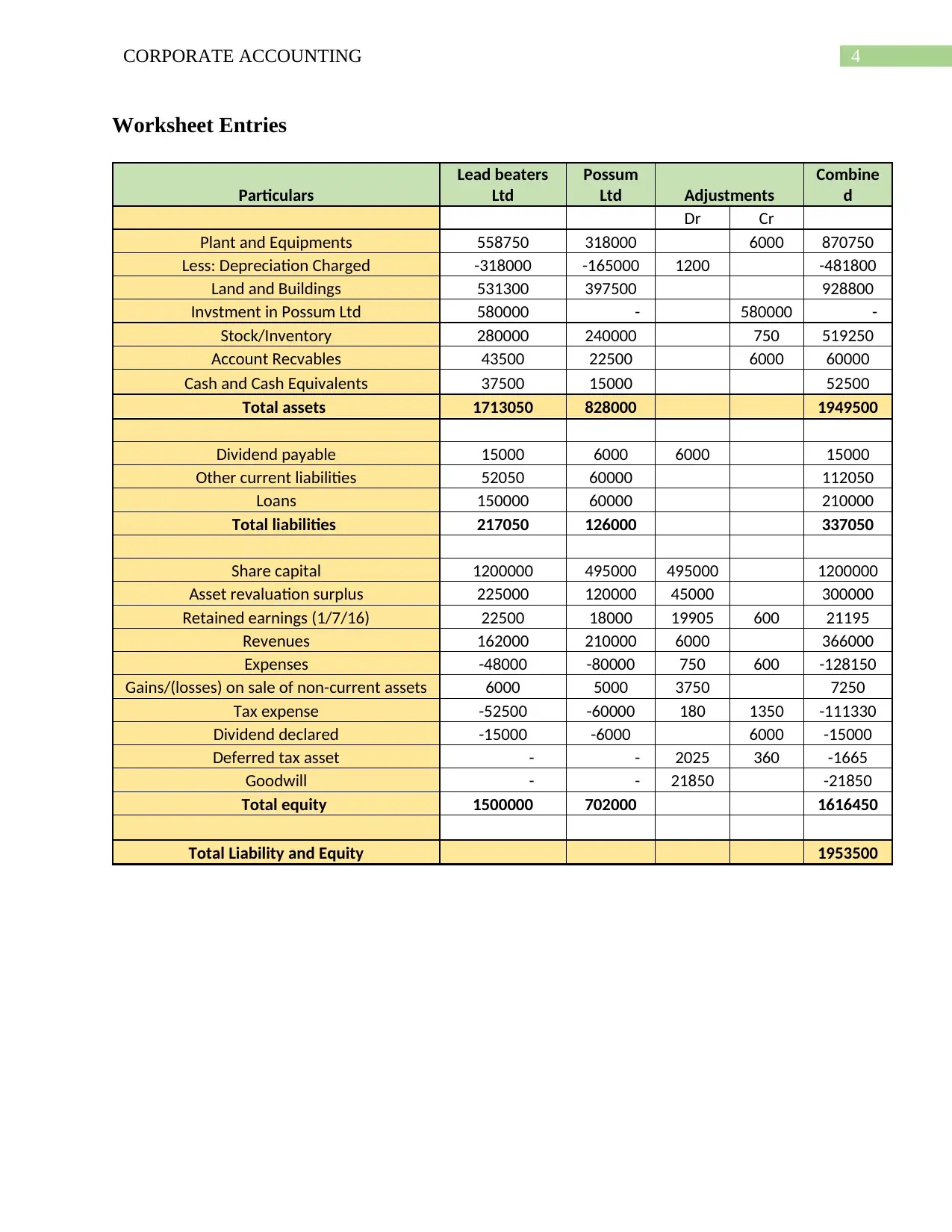

This report provides a comprehensive analysis of corporate accounting principles, focusing on the acquisition of Possum Ltd by Lead Beaters. It includes detailed journal entries for the consolidation process, incorporating adjustments for inventory, plant and machinery, and contingent liabilities, with a tax rate of 30% considered. The calculation of goodwill is explained, based on the difference between the actual amount paid and the net identified fair value of the acquired company. Furthermore, the report presents worksheet entries, illustrating the consolidated financial position, and offers a rationale behind each transaction, referencing relevant accounting standards and practices. This document is intended to provide a clear understanding of the complexities involved in corporate acquisitions and consolidated financial statement preparation.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.