Corporate Accounting and Reporting: Acquisition Analysis and Journals

VerifiedAdded on 2023/04/22

|9

|466

|404

Report

AI Summary

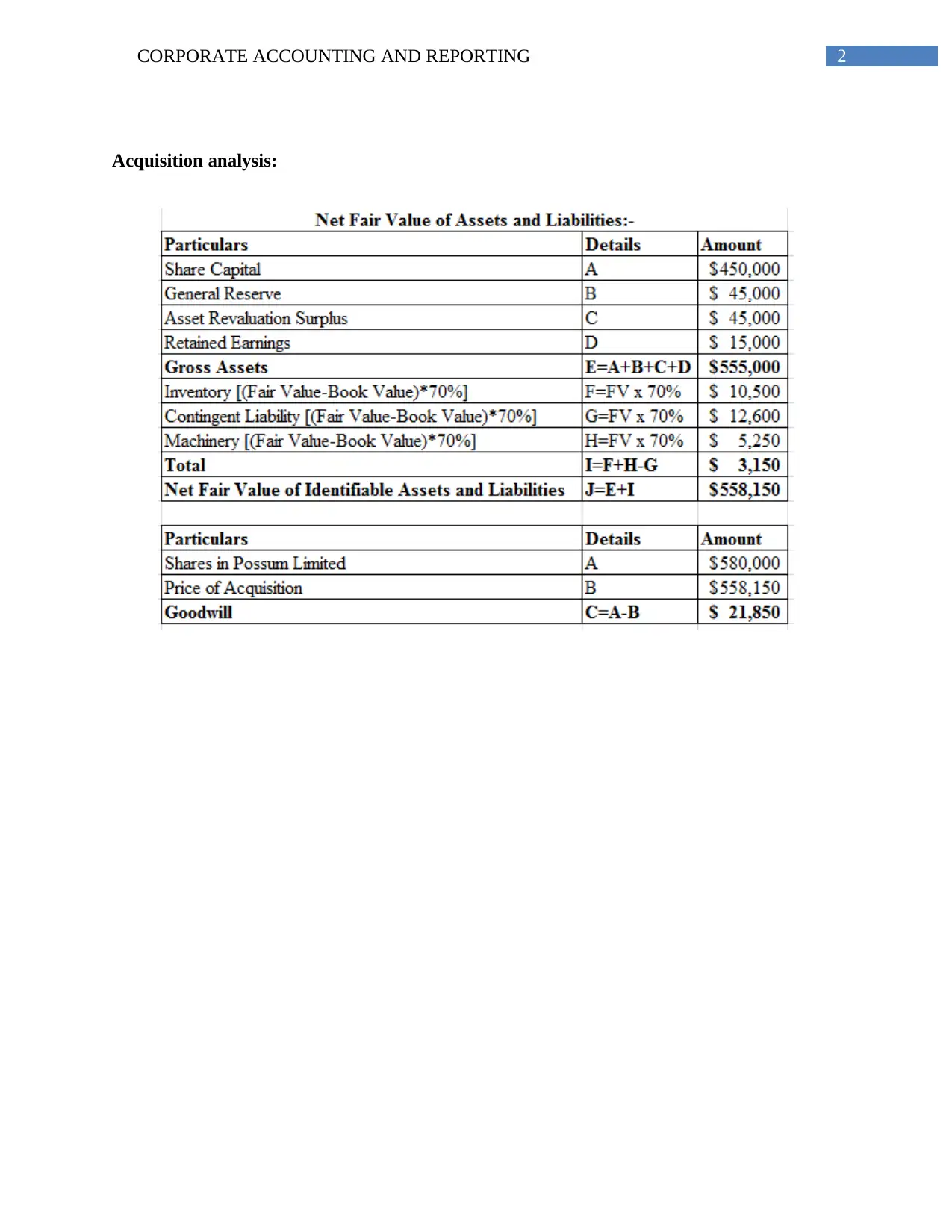

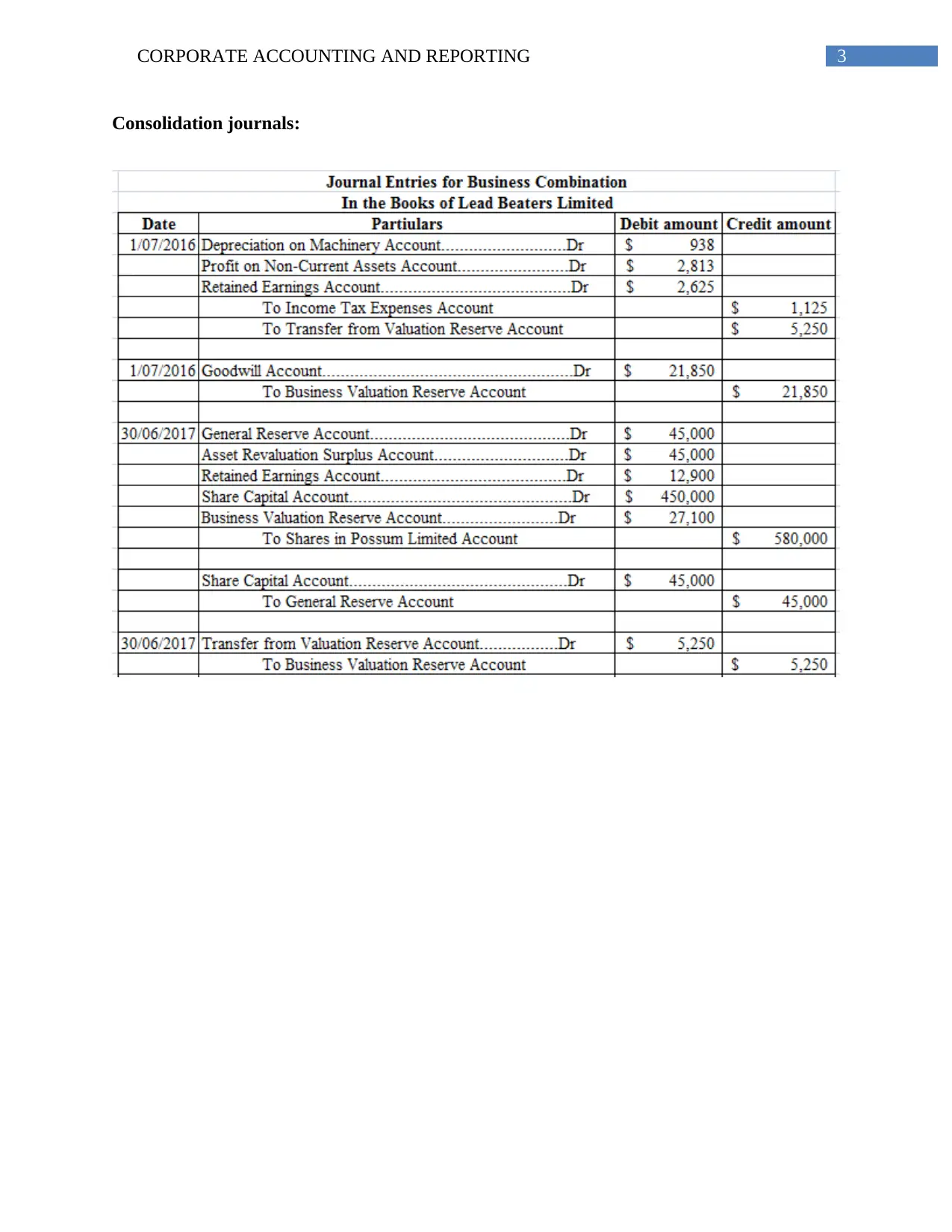

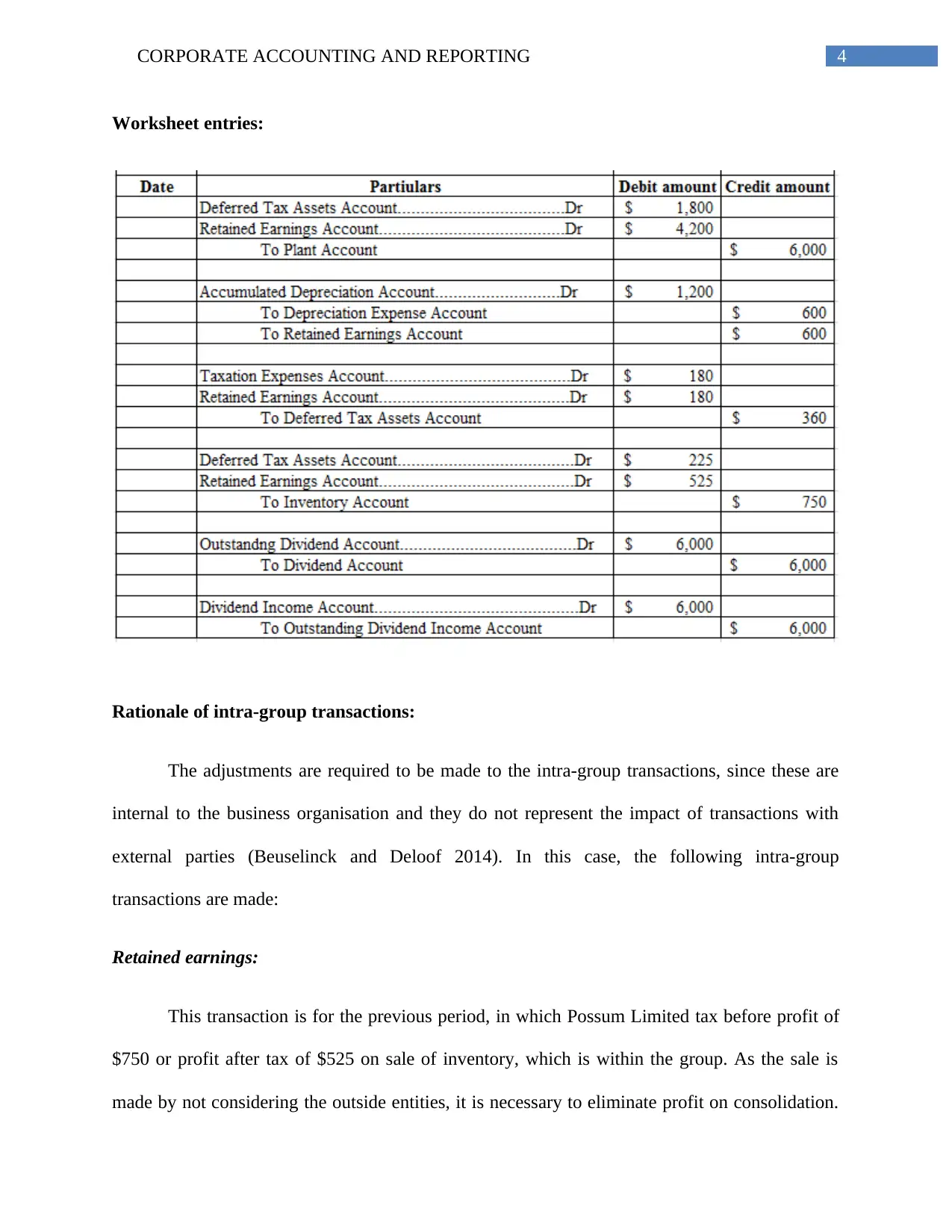

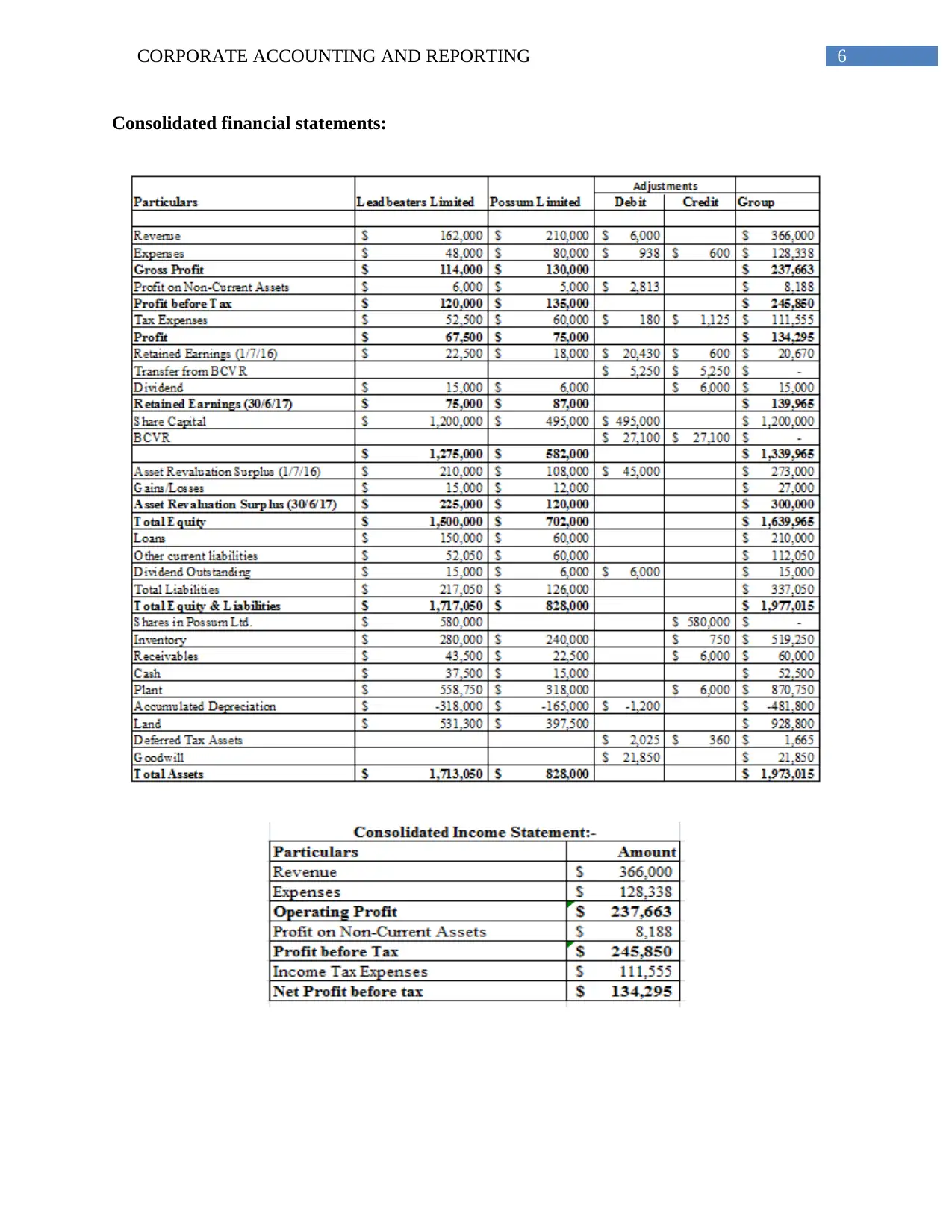

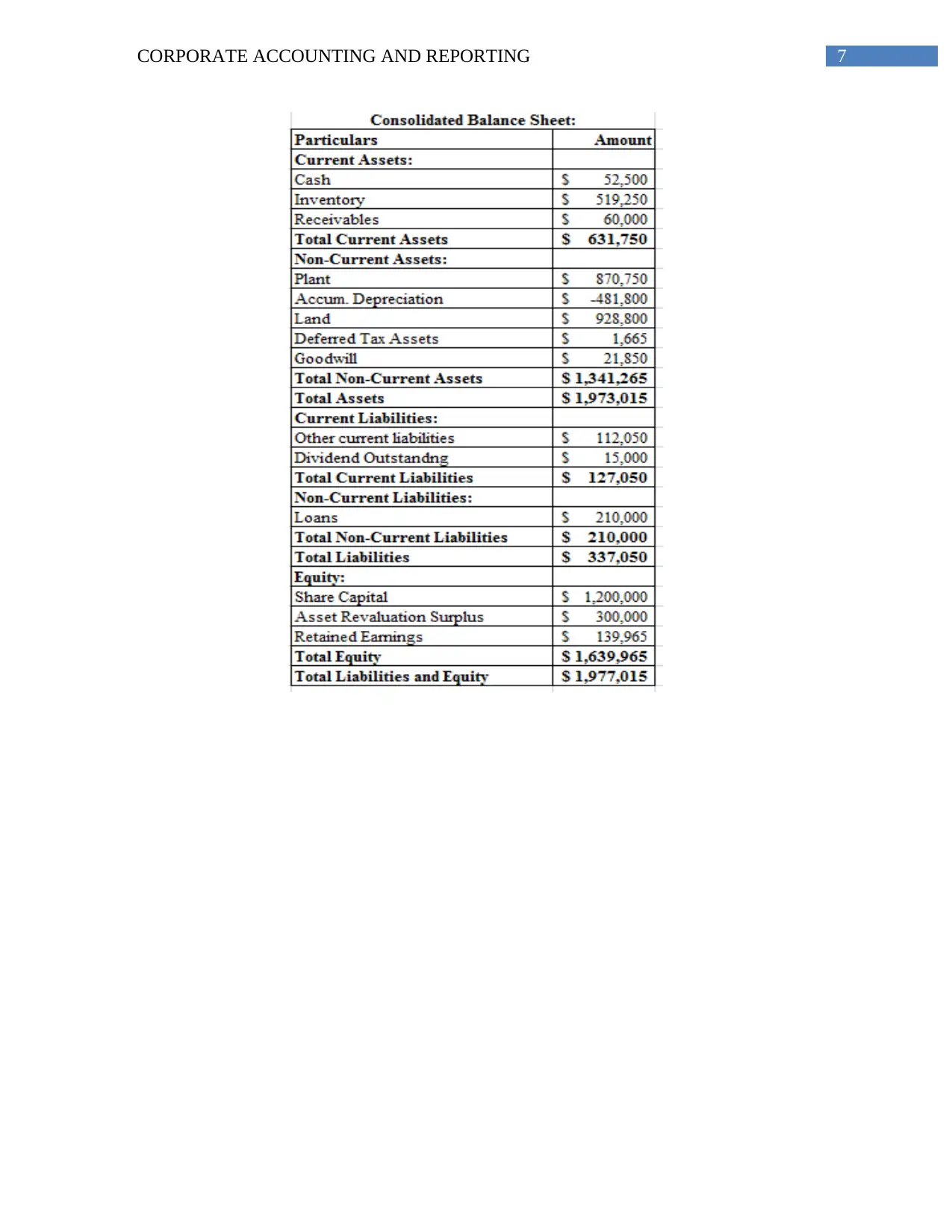

This report provides a detailed analysis of corporate accounting principles, specifically focusing on the consolidation of financial statements. It begins with an acquisition analysis, examining the acquisition of Possum Ltd by Leadbeaters Ltd. The report then delves into consolidation journals, detailing the necessary adjustments for intra-group transactions, such as retained earnings, inventory, and deferred tax assets. The rationale behind these adjustments is explained, emphasizing the elimination of internal profits and the accurate representation of transactions with external parties. The report includes worksheet entries and concludes with consolidated financial statements, demonstrating the combined financial position of the two companies. References to relevant accounting literature are also provided to support the analysis. The assignment covers key aspects of corporate accounting, including acquisition analysis, consolidation journals, intra-group transactions, and the preparation of consolidated financial statements. This report is contributed by a student and available on Desklib, a platform for students to access AI-based study tools.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.