Cost Accounting: Calculations, CVP Analysis, and Profit Statements

VerifiedAdded on 2021/11/16

|7

|1970

|353

Homework Assignment

AI Summary

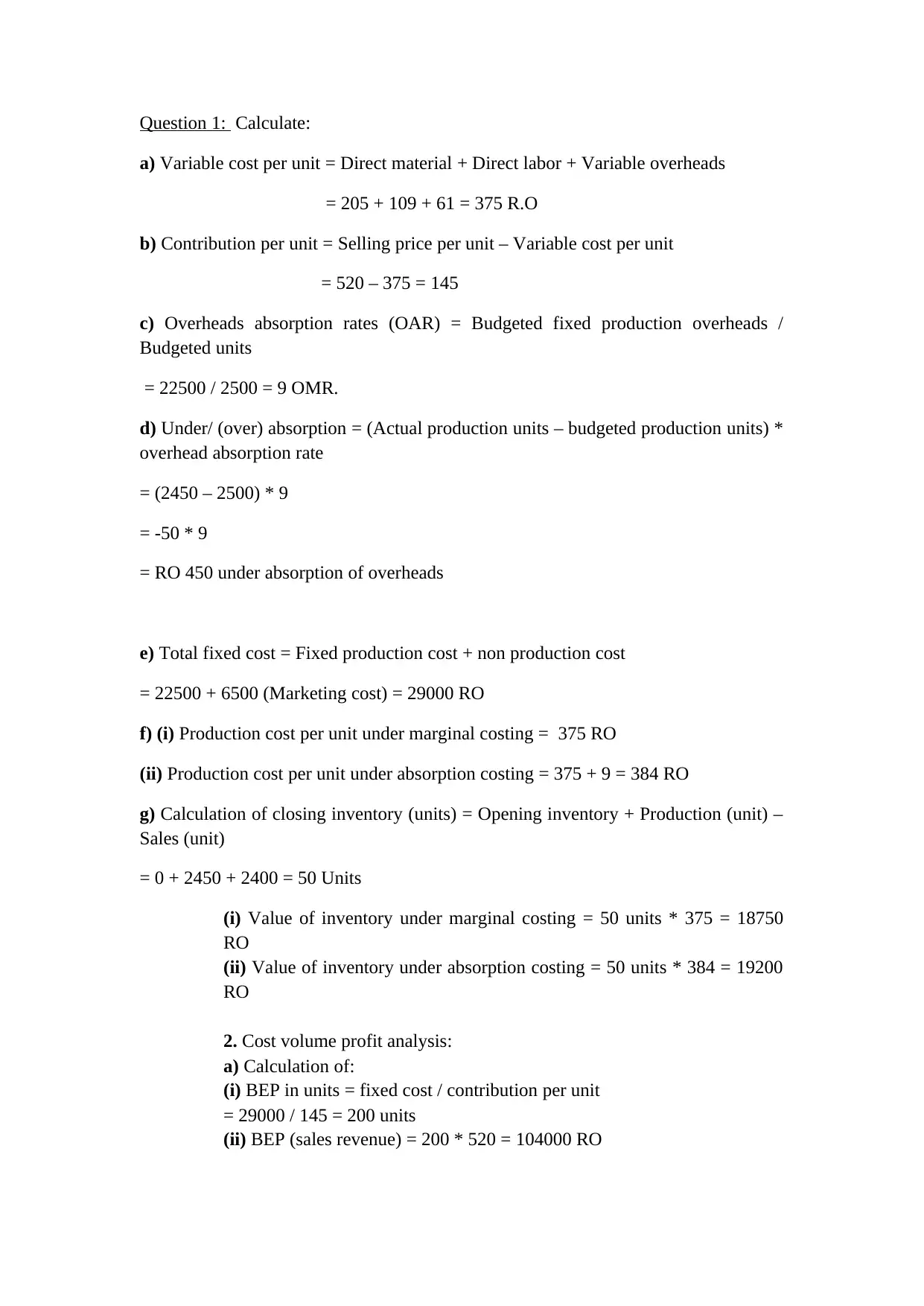

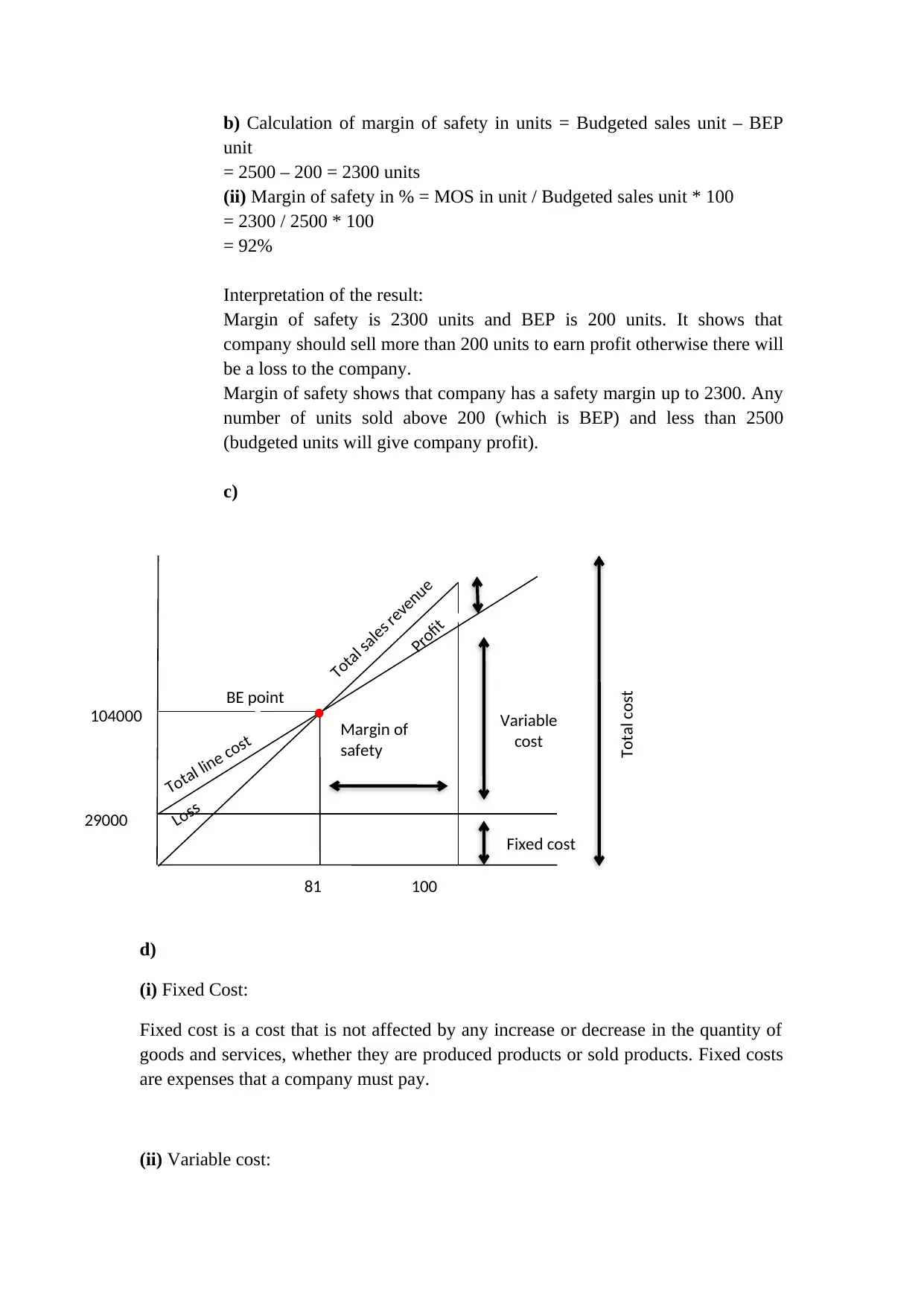

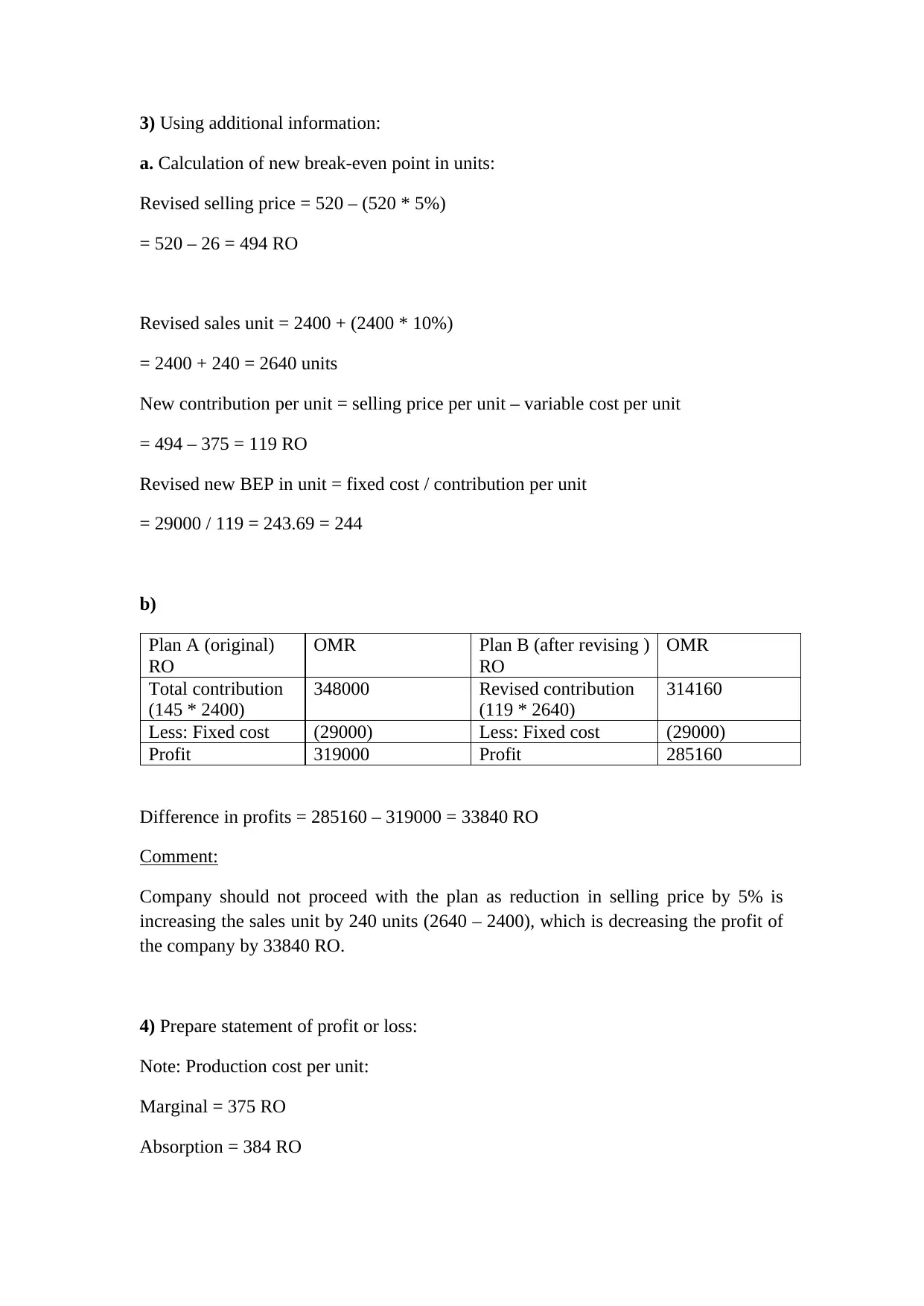

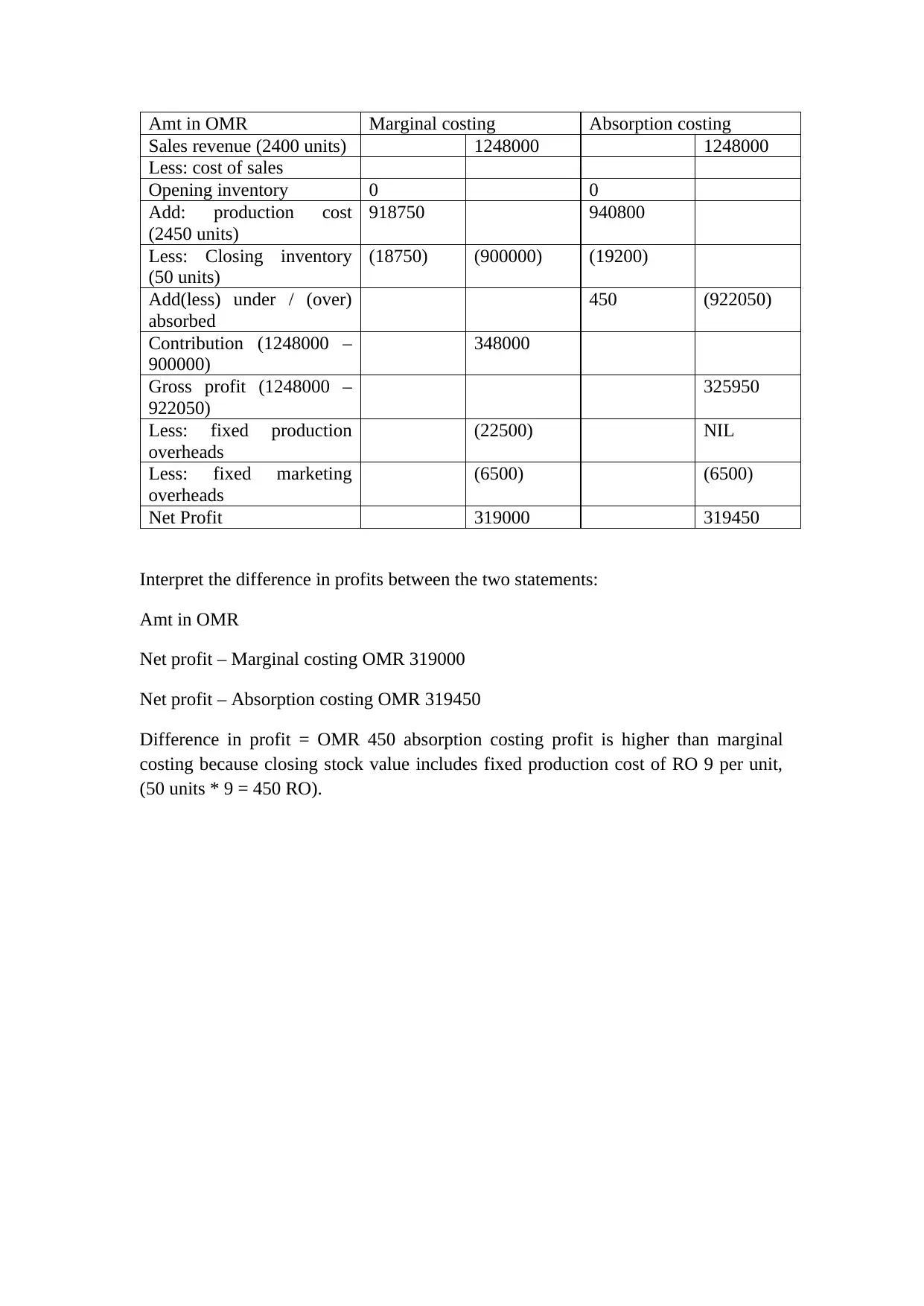

This document presents a comprehensive solution to a cost accounting assignment. It begins with detailed calculations of variable costs, contribution per unit, overhead absorption rates, and under/over absorption. The solution then delves into Cost-Volume-Profit (CVP) analysis, including break-even points, margin of safety calculations, and interpretations. It defines and differentiates between fixed, variable, and semi-variable costs, providing real-world examples. The assignment further explores the impact of changes in selling prices and sales units on profitability, comparing the original plan with a revised plan. Finally, the solution includes the preparation of profit and loss statements using both absorption and marginal costing methods, comparing the resulting net profits and explaining the differences. The document incorporates several sources to support the analysis and conclusions.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.