Cost and Management Accounting Report: Serta and Tempu Beds Analysis

VerifiedAdded on 2023/01/11

|9

|2627

|76

Report

AI Summary

This report delves into the core concepts of cost and management accounting, presenting a comprehensive analysis of unit manufacturing costs for Serta and Tempu beds. It examines traditional costing methods and contrasts them with activity-based costing (ABC), illustrating how ABC can provide a more accurate allocation of overhead costs. The report includes calculations of unit manufacturing costs, assesses the impact of machine hours on cost distortion, and evaluates the financial implications of a proposed discount strategy. Furthermore, it explores a case study involving Adam Smith's decision-making regarding suppliers and raw materials, emphasizing the importance of product quality and ethical considerations. The report also advises Santana Corporation on implementing ABC, outlining appropriate activities and activity drivers, and discussing the associated benefits and costs. Overall, the report provides a practical application of accounting principles to aid in business decision-making.

Cost and management

accounting

1

accounting

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

Contents...........................................................................................................................................2

INTRODUCTION...........................................................................................................................4

TASK 1............................................................................................................................................4

Calculation of the unit manufacturing cost of the Serta and the Tempu bed..............................4

Calculate the unit manufacturing cost of the Serta and the Tempu using activity-based costing.

.....................................................................................................................................................4

3. Is the cost of the Tempu bed distorted by the use of machine hours to allocate total

manufacturing overhead to production, and, if so by how much per unit...................................4

4. Assume that the current selling price of the Tempu bed is $280 and the marketing director

has proposed to offer a $30 discount to increase sales. Is the discount advisable? Advise

management. Show supporting calculations................................................................................4

Explanation of Conventional costing will always distort product costs costin...........................4

TASK 2............................................................................................................................................5

Decision Adam Smith should take with regards to the supplier and raw material......................5

Advise Santana Corporation on suggested activities and activity drivers, explaining to

management why you consider these appropriate.......................................................................6

Explanation of why management of Santana Corporation on the potential benefits and costs

associated with implementing an Activity Based Costing system.zed business activities in......8

CONCLUSION................................................................................................................................8

REFRENCES...................................................................................................................................8

2

Contents...........................................................................................................................................2

INTRODUCTION...........................................................................................................................4

TASK 1............................................................................................................................................4

Calculation of the unit manufacturing cost of the Serta and the Tempu bed..............................4

Calculate the unit manufacturing cost of the Serta and the Tempu using activity-based costing.

.....................................................................................................................................................4

3. Is the cost of the Tempu bed distorted by the use of machine hours to allocate total

manufacturing overhead to production, and, if so by how much per unit...................................4

4. Assume that the current selling price of the Tempu bed is $280 and the marketing director

has proposed to offer a $30 discount to increase sales. Is the discount advisable? Advise

management. Show supporting calculations................................................................................4

Explanation of Conventional costing will always distort product costs costin...........................4

TASK 2............................................................................................................................................5

Decision Adam Smith should take with regards to the supplier and raw material......................5

Advise Santana Corporation on suggested activities and activity drivers, explaining to

management why you consider these appropriate.......................................................................6

Explanation of why management of Santana Corporation on the potential benefits and costs

associated with implementing an Activity Based Costing system.zed business activities in......8

CONCLUSION................................................................................................................................8

REFRENCES...................................................................................................................................8

2

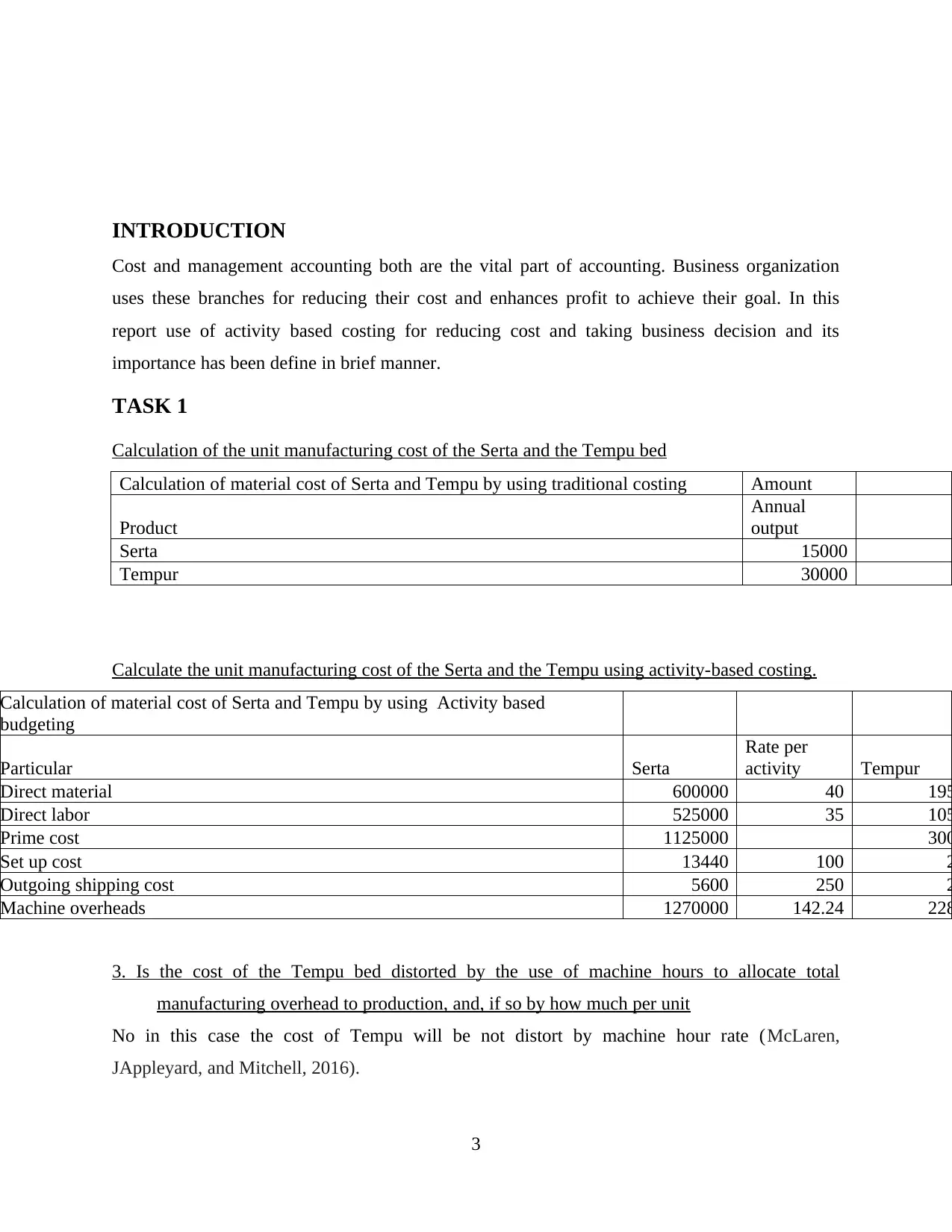

INTRODUCTION

Cost and management accounting both are the vital part of accounting. Business organization

uses these branches for reducing their cost and enhances profit to achieve their goal. In this

report use of activity based costing for reducing cost and taking business decision and its

importance has been define in brief manner.

TASK 1

Calculation of the unit manufacturing cost of the Serta and the Tempu bed

Calculation of material cost of Serta and Tempu by using traditional costing Amount

Product

Annual

output

Serta 15000

Tempur 30000

Calculate the unit manufacturing cost of the Serta and the Tempu using activity-based costing.

Calculation of material cost of Serta and Tempu by using Activity based

budgeting

Particular Serta

Rate per

activity Tempur

Direct material 600000 40 195

Direct labor 525000 35 105

Prime cost 1125000 300

Set up cost 13440 100 2

Outgoing shipping cost 5600 250 2

Machine overheads 1270000 142.24 228

3. Is the cost of the Tempu bed distorted by the use of machine hours to allocate total

manufacturing overhead to production, and, if so by how much per unit

No in this case the cost of Tempu will be not distort by machine hour rate (McLaren,

JAppleyard, and Mitchell, 2016).

3

Cost and management accounting both are the vital part of accounting. Business organization

uses these branches for reducing their cost and enhances profit to achieve their goal. In this

report use of activity based costing for reducing cost and taking business decision and its

importance has been define in brief manner.

TASK 1

Calculation of the unit manufacturing cost of the Serta and the Tempu bed

Calculation of material cost of Serta and Tempu by using traditional costing Amount

Product

Annual

output

Serta 15000

Tempur 30000

Calculate the unit manufacturing cost of the Serta and the Tempu using activity-based costing.

Calculation of material cost of Serta and Tempu by using Activity based

budgeting

Particular Serta

Rate per

activity Tempur

Direct material 600000 40 195

Direct labor 525000 35 105

Prime cost 1125000 300

Set up cost 13440 100 2

Outgoing shipping cost 5600 250 2

Machine overheads 1270000 142.24 228

3. Is the cost of the Tempu bed distorted by the use of machine hours to allocate total

manufacturing overhead to production, and, if so by how much per unit

No in this case the cost of Tempu will be not distort by machine hour rate (McLaren,

JAppleyard, and Mitchell, 2016).

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

4. Assume that the current selling price of the Tempu bed is $280 and the marketing director has

proposed to offer a $30 discount to increase sales. Is the discount advisable? Advise

management. Show supporting calculations.

No in this situation discount is not advisable because it will inure loss as compare to its

manufacturing cost.

Explanation of Conventional costing will always distort product costs costing

Conventional costing is a type of costing in which overheads are allocated to the products

on volume based measures that means labour hours machine hours and unit produced. It also

known as traditional costing. In this method factory overheads are allocated on the basis of

resource consumed in production process. This method of accounting used in predication of

profits. Conventional costing used causes and effect method which takes into account the direct

and indirect costs and overheads within the business. In traditional coating overheads are related

with the cost centres. And then its cost objectives .Traditional cost accosting it is assumed that

cost objective consume resource and it is structure oriented , Traditional costing system reveals

less accurate costs(Basiruddin, Benyasrisawat and Rasid, 2014).

ABC costing technique of accounting has been developed in order to fulfil the limitations of

traditional costing. This costing method has big limitation or weakness is that it only considered

production factor for measuring their cost and allocation of overheads. Even many products of

business organization do not uses the overhands in proportion to the volume of products

produced within the manufacturing process. There will be many types of cost are reason of non

production which is related with the products’ characteristics , size, its compatibility,

complexity, tends of conventional costing distort product of cost . This refers that there would be

too much cost had been charge on allocation of overheads to products. While too little ovehareds

are allocated to other products of manufacturing products. This type of distortion are known as

cross subsidies distortions. ABC analysis solve these problems thus managers of business

organization special manufacturing industries used ABC analysis rather hen prefer the traditional

based costing method.ABC cost method management department divide each product cost in

different categories of cost drivers. Through which they can easily solve the problem f distortion

of product cost. The rules and procedure of working of traditional costing system are made in a

manner that production cost always distort to the product cost.

4

proposed to offer a $30 discount to increase sales. Is the discount advisable? Advise

management. Show supporting calculations.

No in this situation discount is not advisable because it will inure loss as compare to its

manufacturing cost.

Explanation of Conventional costing will always distort product costs costing

Conventional costing is a type of costing in which overheads are allocated to the products

on volume based measures that means labour hours machine hours and unit produced. It also

known as traditional costing. In this method factory overheads are allocated on the basis of

resource consumed in production process. This method of accounting used in predication of

profits. Conventional costing used causes and effect method which takes into account the direct

and indirect costs and overheads within the business. In traditional coating overheads are related

with the cost centres. And then its cost objectives .Traditional cost accosting it is assumed that

cost objective consume resource and it is structure oriented , Traditional costing system reveals

less accurate costs(Basiruddin, Benyasrisawat and Rasid, 2014).

ABC costing technique of accounting has been developed in order to fulfil the limitations of

traditional costing. This costing method has big limitation or weakness is that it only considered

production factor for measuring their cost and allocation of overheads. Even many products of

business organization do not uses the overhands in proportion to the volume of products

produced within the manufacturing process. There will be many types of cost are reason of non

production which is related with the products’ characteristics , size, its compatibility,

complexity, tends of conventional costing distort product of cost . This refers that there would be

too much cost had been charge on allocation of overheads to products. While too little ovehareds

are allocated to other products of manufacturing products. This type of distortion are known as

cross subsidies distortions. ABC analysis solve these problems thus managers of business

organization special manufacturing industries used ABC analysis rather hen prefer the traditional

based costing method.ABC cost method management department divide each product cost in

different categories of cost drivers. Through which they can easily solve the problem f distortion

of product cost. The rules and procedure of working of traditional costing system are made in a

manner that production cost always distort to the product cost.

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TASK 2

Decision Adam Smith should take with regards to the supplier and raw material.

Adam Smith is the owner of Button Pty Limited their cost of manufacturing beds goes high thus

they are unable to generate higher rate of return. A supplier offers them to provide raw material

at lower rate through which they can easily cover up their manufacturing cost and able to earn

higher return of profit. But their raw material has some minor defects which may lead to

provides many sleeping problems for their customers.

As per the Australian law Adam Smith should not accept the proposal of supplier because the

quality of raw materials is not good and they have directs even though Adam Smith ready for

give compensate to their clients but goodwill of the company decreases and their manufacturing

cost may reduce by accepting the offer but due to decrement in the reputation of their firm , the

customer satisfaction rate goes down and their selling rate also decreases this will automatically

reduce the profit earn by Button PTY limited. Thus they did not accept the offer of supplier even

customers also claim for damages and compensation according to the Australian Consumers Act

.Thus Adam Smith must provide high qualities of products and service to their customer even

though they not get higher return of profit at initial rate but their target marked area increase with

increment of customers satisfaction rate (Rieckhof, Bergmann and Guenther,2015).A

manufacturing owner of Australian Mills was sued because of ignorance by a individual who

already wore them and in contract with demerits for an sulphite residual left in manufacturing

process. The plaintiff able proc that the pants of the manufacturing organization was have

defects because of contain extra chemicals but theses chemicals not shown whatever the

chemical outstanding was due for any either meticulous insufficiency procedure of

manufacturing. The court decided the continuation of the extreme chemical was of itself

siuuffiecnt proof of carless and upheld the allege of negligence on the Australian Knitting Mills.

The consumer have right to sue case or file against for retailers they can claim for damages and

if the Damage is high then the retailer may be sued for give panties.

An damage can be caused partially by imperfect commodities and partially by performance on

the component of the person who has been hurt or continuous smash up to their possessions.

Court of Australia may be reduced the value of damages . The compensation rate get high id f

the retailers sell the products to their clients when they have an idean regarding the fault and

they till sell their products to target market. In the case of Adam Smite they have knowledge

5

Decision Adam Smith should take with regards to the supplier and raw material.

Adam Smith is the owner of Button Pty Limited their cost of manufacturing beds goes high thus

they are unable to generate higher rate of return. A supplier offers them to provide raw material

at lower rate through which they can easily cover up their manufacturing cost and able to earn

higher return of profit. But their raw material has some minor defects which may lead to

provides many sleeping problems for their customers.

As per the Australian law Adam Smith should not accept the proposal of supplier because the

quality of raw materials is not good and they have directs even though Adam Smith ready for

give compensate to their clients but goodwill of the company decreases and their manufacturing

cost may reduce by accepting the offer but due to decrement in the reputation of their firm , the

customer satisfaction rate goes down and their selling rate also decreases this will automatically

reduce the profit earn by Button PTY limited. Thus they did not accept the offer of supplier even

customers also claim for damages and compensation according to the Australian Consumers Act

.Thus Adam Smith must provide high qualities of products and service to their customer even

though they not get higher return of profit at initial rate but their target marked area increase with

increment of customers satisfaction rate (Rieckhof, Bergmann and Guenther,2015).A

manufacturing owner of Australian Mills was sued because of ignorance by a individual who

already wore them and in contract with demerits for an sulphite residual left in manufacturing

process. The plaintiff able proc that the pants of the manufacturing organization was have

defects because of contain extra chemicals but theses chemicals not shown whatever the

chemical outstanding was due for any either meticulous insufficiency procedure of

manufacturing. The court decided the continuation of the extreme chemical was of itself

siuuffiecnt proof of carless and upheld the allege of negligence on the Australian Knitting Mills.

The consumer have right to sue case or file against for retailers they can claim for damages and

if the Damage is high then the retailer may be sued for give panties.

An damage can be caused partially by imperfect commodities and partially by performance on

the component of the person who has been hurt or continuous smash up to their possessions.

Court of Australia may be reduced the value of damages . The compensation rate get high id f

the retailers sell the products to their clients when they have an idean regarding the fault and

they till sell their products to target market. In the case of Adam Smite they have knowledge

5

regarding the damages and fault nit the raw materials even it was a miner fault but hay may

because of buffs health issue for their clients they may have duffers’ problems of splaying and

other. Thus if t any of their customers sue case on the organization regarding fault gulpers of

beds then court charge them high rate ode penalties. Thus Adam Smith would not accept the

defaced materials offer of supplier in order to maintain sustanivity of their organization within

the market. Unwarranted

TASK 3

Advise Santana Corporation on suggested activities and activity drivers, explaining to

management why you consider these appropriate.

Santana Corporation is provides grocery product and services as wholesaler supllier target

market area. They provide various types of products and service within the market. They use

conventional costing system. To increase their profitability rate they use customer’s profitability

analysis tool which is the part of cost and management accounting. With the use of this

methodology manger of Santana will be able to identify profitably rate of each clients. With the

use of attributing cost of each client activity. Santana Corporation should be use activity based

costing method which can easily able to distribute cost activities to each group and thy able to

identify cost incurred on each activity (Powers, Higham, Broussard and Phillips, 2016).

Activity based costing is a system that focus on activities as fundamental cost objectives ad

utilizes cost of these activities as building blocks or compiling the cost of other cost object.

Activity based costing facilitates strategic cost management . ABC not only shows how activities

consume resource and how products or customers trigger activities but also assign costs to

product or customers according to the resource consume. ABC describes information for manger

to mange activities to improve competitiveness and achieve strategic goals. ABC is a type of cost

accounting strategy which assigns cost to business activities rather than business products and

services. Thus Santana Corporation used this costing method to apply in their organization and

management strategy. Activity base costing increasing the number of cost pools used to

accumulate overhead cost. The number of pools depends upon the cosy driving activities. Thus

instead of accumulating overheads cost in single company wise pool if department pools the cost

are accumulated by activities. These method charges overheads cost in indecent jobs or products

in propane to the cost driving activities in place of a blanket rate based on direct labour cost or

6

because of buffs health issue for their clients they may have duffers’ problems of splaying and

other. Thus if t any of their customers sue case on the organization regarding fault gulpers of

beds then court charge them high rate ode penalties. Thus Adam Smith would not accept the

defaced materials offer of supplier in order to maintain sustanivity of their organization within

the market. Unwarranted

TASK 3

Advise Santana Corporation on suggested activities and activity drivers, explaining to

management why you consider these appropriate.

Santana Corporation is provides grocery product and services as wholesaler supllier target

market area. They provide various types of products and service within the market. They use

conventional costing system. To increase their profitability rate they use customer’s profitability

analysis tool which is the part of cost and management accounting. With the use of this

methodology manger of Santana will be able to identify profitably rate of each clients. With the

use of attributing cost of each client activity. Santana Corporation should be use activity based

costing method which can easily able to distribute cost activities to each group and thy able to

identify cost incurred on each activity (Powers, Higham, Broussard and Phillips, 2016).

Activity based costing is a system that focus on activities as fundamental cost objectives ad

utilizes cost of these activities as building blocks or compiling the cost of other cost object.

Activity based costing facilitates strategic cost management . ABC not only shows how activities

consume resource and how products or customers trigger activities but also assign costs to

product or customers according to the resource consume. ABC describes information for manger

to mange activities to improve competitiveness and achieve strategic goals. ABC is a type of cost

accounting strategy which assigns cost to business activities rather than business products and

services. Thus Santana Corporation used this costing method to apply in their organization and

management strategy. Activity base costing increasing the number of cost pools used to

accumulate overhead cost. The number of pools depends upon the cosy driving activities. Thus

instead of accumulating overheads cost in single company wise pool if department pools the cost

are accumulated by activities. These method charges overheads cost in indecent jobs or products

in propane to the cost driving activities in place of a blanket rate based on direct labour cost or

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

direct hours or machine hours. It improves the traceability of the overhead costs which results in

more accurate unit cost data for management.

Santana Corporation used this method in their business activities because though most of cost

incurred for individual customers are simply produced cost there is also an overhead component

such as unusually high customer services levels products return handling an cooperative

marketing agreements. An ABC system can sort through these additional overheads cost and

help a person to detriment which customer are actually earning a retainable profit. This analysis

may result in some unprofitable customers being turned away or more emphasis being placed on

those customers who are earning the company to largest profits. ABC costing system is more

better than traditional system of costing (Hoque, 2014).

Management department of Santana Corporation use activity drivers for determining their

customers cost. These are following

Activity drivers are those hat influence the business cost of operations. They are reason of

contributing in incurring expenses. For Grocery Corporation the management department maybe

used number of suppliers invoices proceed.

Check paid

Number of customers invoice issues

Square footage used Time taken in distribution

Number of sells calls

Numbers of retailers

Numbers of working order

Number of warehouse picks

All these activity deriver of Santana Corporation helps in minting a strong relation between cost

pools and activities. They directly influence the other variable.

Explanation of why management of Santana Corporation on the potential benefits and costs

associated with implementing an Activity Based Costing system.zed business activities in

Activity based costing helps in recognize method of costing is help in learning about

products and it will useful for allocation of resource of corporation in effective manner.

According to the research article A state of art on activity based costing. Implementation of this

method and organization helps in consultation of time and easily recognized cost incurred of

7

more accurate unit cost data for management.

Santana Corporation used this method in their business activities because though most of cost

incurred for individual customers are simply produced cost there is also an overhead component

such as unusually high customer services levels products return handling an cooperative

marketing agreements. An ABC system can sort through these additional overheads cost and

help a person to detriment which customer are actually earning a retainable profit. This analysis

may result in some unprofitable customers being turned away or more emphasis being placed on

those customers who are earning the company to largest profits. ABC costing system is more

better than traditional system of costing (Hoque, 2014).

Management department of Santana Corporation use activity drivers for determining their

customers cost. These are following

Activity drivers are those hat influence the business cost of operations. They are reason of

contributing in incurring expenses. For Grocery Corporation the management department maybe

used number of suppliers invoices proceed.

Check paid

Number of customers invoice issues

Square footage used Time taken in distribution

Number of sells calls

Numbers of retailers

Numbers of working order

Number of warehouse picks

All these activity deriver of Santana Corporation helps in minting a strong relation between cost

pools and activities. They directly influence the other variable.

Explanation of why management of Santana Corporation on the potential benefits and costs

associated with implementing an Activity Based Costing system.zed business activities in

Activity based costing helps in recognize method of costing is help in learning about

products and it will useful for allocation of resource of corporation in effective manner.

According to the research article A state of art on activity based costing. Implementation of this

method and organization helps in consultation of time and easily recognized cost incurred of

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

various parts of business organization; activity. As Santana Corporation is work its small

supermarket and its target area includes various small retailers. With the use of ABC technique

they are able to identify how many order they received within the month, their sales forecast.

Able to compare their past and current sales target. Saran organization will be able to understand

the connect of cost in easy way. hey can able to change their procedure an even they have attain

profits y using this method as by adopintin this method the hare be to gernat profit and gain

competitive business advantage. Activity based ting helps them to generate more profit minimize

cost though cutting high incurred activities extra cost.

It helps to understand the behaviour of overhead costs and their relationship to products services

customers and market. Saran Corporation will be able to allocate their resource to those activities

that will increase shareholders value and increase their client (Kober and et.al. 2016).

Activity based costing method use them to incurred profitability analysis to operation decision. It

ensure

CONCLUSION

From the above analyse it has been concluded that cost an management accounting play

essential role in management of business organization by reducing their cost. With the use

of effective activity based costing method manager will be able to earn profit.

8

supermarket and its target area includes various small retailers. With the use of ABC technique

they are able to identify how many order they received within the month, their sales forecast.

Able to compare their past and current sales target. Saran organization will be able to understand

the connect of cost in easy way. hey can able to change their procedure an even they have attain

profits y using this method as by adopintin this method the hare be to gernat profit and gain

competitive business advantage. Activity based ting helps them to generate more profit minimize

cost though cutting high incurred activities extra cost.

It helps to understand the behaviour of overhead costs and their relationship to products services

customers and market. Saran Corporation will be able to allocate their resource to those activities

that will increase shareholders value and increase their client (Kober and et.al. 2016).

Activity based costing method use them to incurred profitability analysis to operation decision. It

ensure

CONCLUSION

From the above analyse it has been concluded that cost an management accounting play

essential role in management of business organization by reducing their cost. With the use

of effective activity based costing method manager will be able to earn profit.

8

REFRENCES

Books and journals

Laitinen, E. K., 2014. Influence of cost accounting change on performance of manufacturing

firms. Advances in accounting, 30(1), pp.230-240.

McLaren, J., Appleyard, T. and Mitchell, F., 2016. The rise and fall of management accounting

systems: A case study investigation of EVA™. The British Accounting Review, 48(3),

pp.341-358.

Basiruddin, R., Benyasrisawat, P. and Rasid, S. Z. A., 2014. Audit quality and cost of equity

capital. Afro-Asian Journal of Finance and Accounting 3, 4(2), pp.95-111.

Rieckhof, R., Bergmann, A. and Guenther, E., 2015. Interrelating material flow cost accounting

with management control systems to introduce resource efficiency into strategy. Journal

of Cleaner Production, 108, pp.1262-1278.

Powers, J .G., Higham, C., Broussard, K. and Phillips, T.J., 2016. Wound healing and treating

wounds: Chronic wound care and management. Journal of the American Academy of

Dermatology, 74(4), pp.607-625.

Hoque, Z., 2014. 20 years of studies on the balanced scorecard: Trends, accomplishments, gaps

and opportunities for future research. The British accounting review, 46(1), pp.33-59.

Kober, H., Lacadie, C. M., Wexler, B.E ., Malison, R. T., Sinha, R. and Potenza, M.N., 2016.

Brain activity during cocaine craving and gambling urges: an fMRI

study. Neuropsychopharmacology, 41(2), pp.628-637.

9

Books and journals

Laitinen, E. K., 2014. Influence of cost accounting change on performance of manufacturing

firms. Advances in accounting, 30(1), pp.230-240.

McLaren, J., Appleyard, T. and Mitchell, F., 2016. The rise and fall of management accounting

systems: A case study investigation of EVA™. The British Accounting Review, 48(3),

pp.341-358.

Basiruddin, R., Benyasrisawat, P. and Rasid, S. Z. A., 2014. Audit quality and cost of equity

capital. Afro-Asian Journal of Finance and Accounting 3, 4(2), pp.95-111.

Rieckhof, R., Bergmann, A. and Guenther, E., 2015. Interrelating material flow cost accounting

with management control systems to introduce resource efficiency into strategy. Journal

of Cleaner Production, 108, pp.1262-1278.

Powers, J .G., Higham, C., Broussard, K. and Phillips, T.J., 2016. Wound healing and treating

wounds: Chronic wound care and management. Journal of the American Academy of

Dermatology, 74(4), pp.607-625.

Hoque, Z., 2014. 20 years of studies on the balanced scorecard: Trends, accomplishments, gaps

and opportunities for future research. The British accounting review, 46(1), pp.33-59.

Kober, H., Lacadie, C. M., Wexler, B.E ., Malison, R. T., Sinha, R. and Potenza, M.N., 2016.

Brain activity during cocaine craving and gambling urges: an fMRI

study. Neuropsychopharmacology, 41(2), pp.628-637.

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 9

Related Documents

![Management Accounting: Costing Analysis of Office Desks - [Company]](/_next/image/?url=https%3A%2F%2Fdesklib.com%2Fmedia%2Fimages%2Fjv%2Fc197923795a34b81bdce50f667d18d4c.jpg&w=256&q=75)

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.