Management Accounting: Costing Analysis of Office Desks - [Company]

VerifiedAdded on 2020/03/23

|4

|720

|47

Homework Assignment

AI Summary

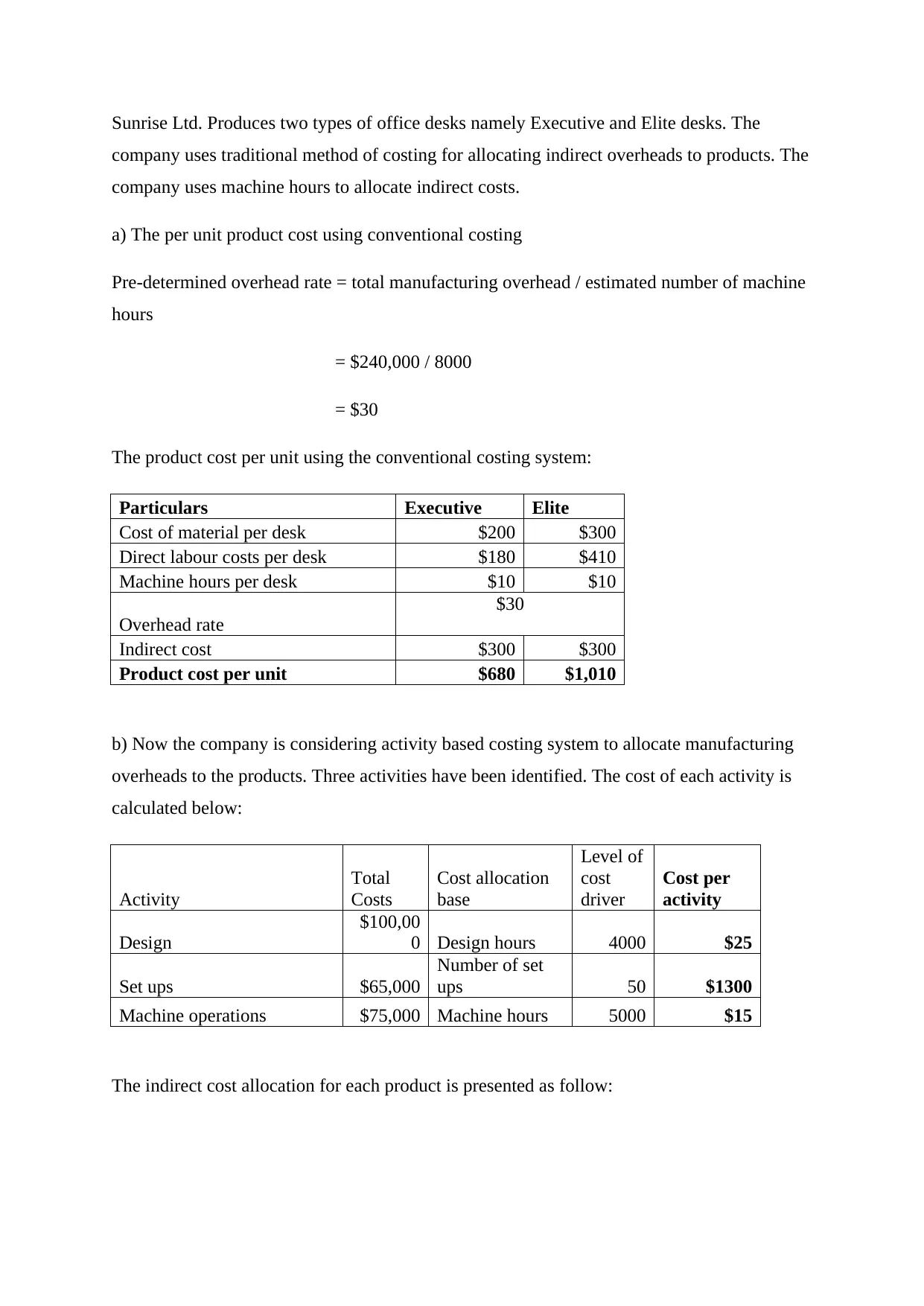

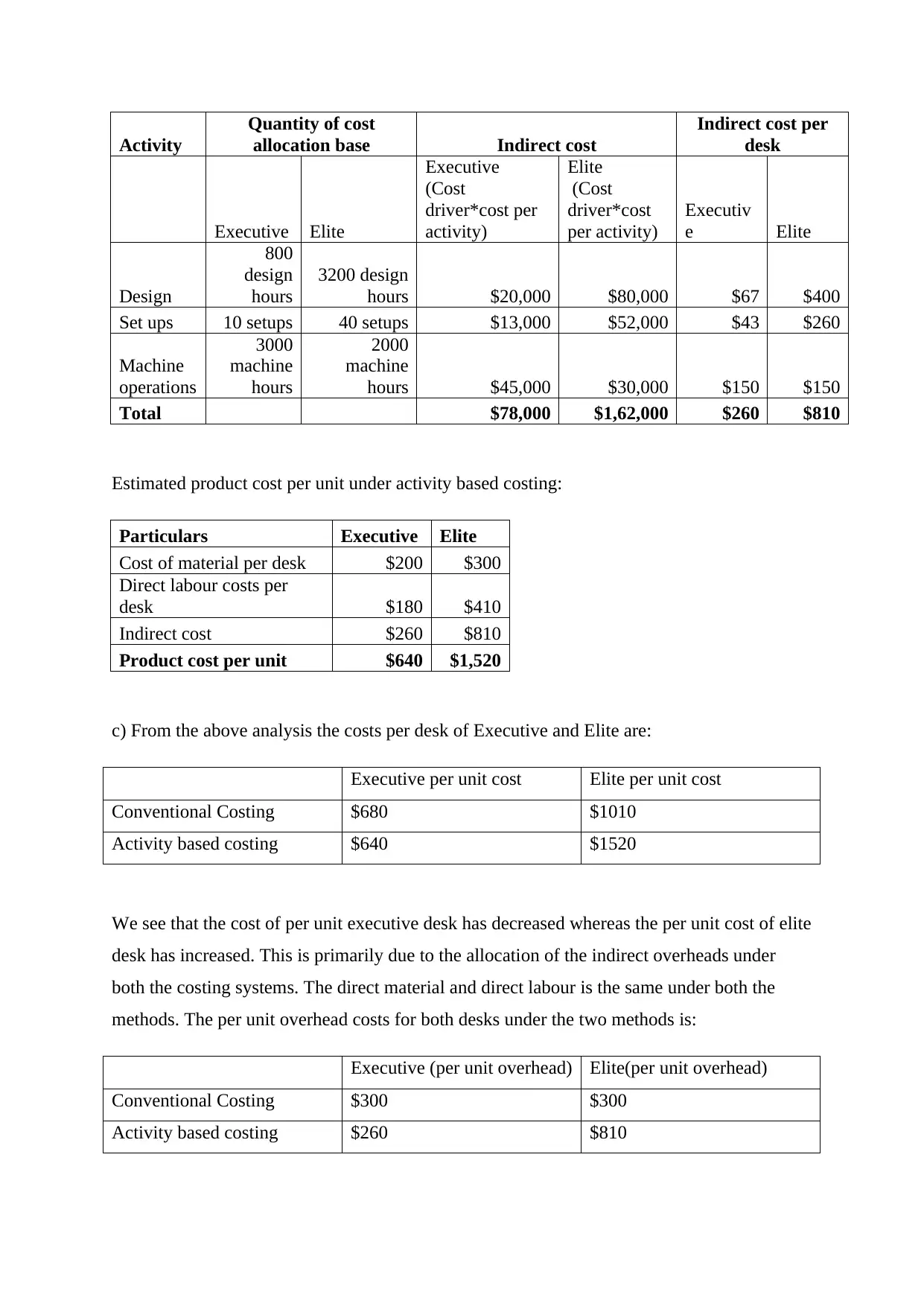

This assignment analyzes the management accounting practices of Sunrise Ltd., a company producing Executive and Elite office desks. The core focus is a comparative analysis of two costing methods: traditional costing and activity-based costing (ABC). The solution details the calculation of per-unit product costs under both systems, using machine hours for overhead allocation in the traditional method and identifying design hours, setups, and machine operations as cost drivers for ABC. The analysis reveals how different overhead allocation methods impact the cost of each desk type, demonstrating a shift in cost allocation from traditional to ABC. The assignment also explores the implications of the costing methods, including how the cost per unit changes for both desk types. The solution includes a detailed breakdown of costs, allocation bases, and the impact on product pricing, offering a practical application of management accounting principles, and concludes with a bibliography of resources used.

1 out of 4

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.