LSME505 Business Finance: Costing, Budgeting, and Variance Analysis

VerifiedAdded on 2022/12/14

|17

|2668

|203

Report

AI Summary

This business finance assignment explores cost management, budgeting, and variance analysis. Part A focuses on cost classification (fixed, variable, semi-variable), break-even analysis, and the importance of cost classification in pricing decisions. The report includes calculations for contribution per unit, break-even points, and margin of safety. It also presents marginal and absorption costing statements and discusses their differences. Part B delves into budgeting, its role in controlling business operations, and various budgetary techniques like variance analysis, responsibility accounting, fund adjustment, and zero-based budgeting. The assignment provides calculations for material price and usage variance, labor rate and efficiency variances, and fixed overhead expenditure variance. Finally, it includes a budget for controlling operations, including direct material, direct labor, and overhead budgets.

BUSINESS FINANCE

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................3

Part A...............................................................................................................................................3

Part B...............................................................................................................................................6

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

INTRODUCTION...........................................................................................................................3

Part A...............................................................................................................................................3

Part B...............................................................................................................................................6

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

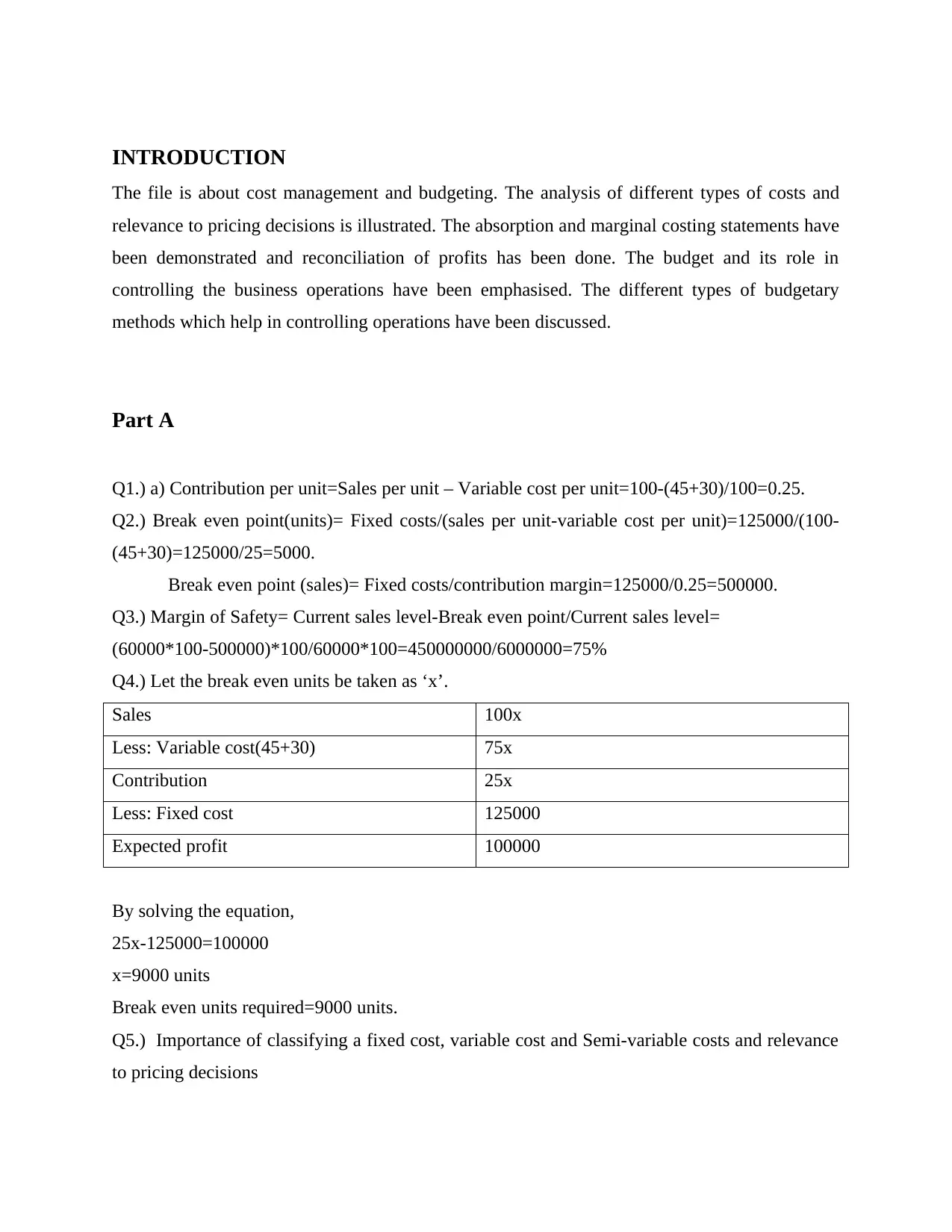

INTRODUCTION

The file is about cost management and budgeting. The analysis of different types of costs and

relevance to pricing decisions is illustrated. The absorption and marginal costing statements have

been demonstrated and reconciliation of profits has been done. The budget and its role in

controlling the business operations have been emphasised. The different types of budgetary

methods which help in controlling operations have been discussed.

Part A

Q1.) a) Contribution per unit=Sales per unit – Variable cost per unit=100-(45+30)/100=0.25.

Q2.) Break even point(units)= Fixed costs/(sales per unit-variable cost per unit)=125000/(100-

(45+30)=125000/25=5000.

Break even point (sales)= Fixed costs/contribution margin=125000/0.25=500000.

Q3.) Margin of Safety= Current sales level-Break even point/Current sales level=

(60000*100-500000)*100/60000*100=450000000/6000000=75%

Q4.) Let the break even units be taken as ‘x’.

Sales 100x

Less: Variable cost(45+30) 75x

Contribution 25x

Less: Fixed cost 125000

Expected profit 100000

By solving the equation,

25x-125000=100000

x=9000 units

Break even units required=9000 units.

Q5.) Importance of classifying a fixed cost, variable cost and Semi-variable costs and relevance

to pricing decisions

The file is about cost management and budgeting. The analysis of different types of costs and

relevance to pricing decisions is illustrated. The absorption and marginal costing statements have

been demonstrated and reconciliation of profits has been done. The budget and its role in

controlling the business operations have been emphasised. The different types of budgetary

methods which help in controlling operations have been discussed.

Part A

Q1.) a) Contribution per unit=Sales per unit – Variable cost per unit=100-(45+30)/100=0.25.

Q2.) Break even point(units)= Fixed costs/(sales per unit-variable cost per unit)=125000/(100-

(45+30)=125000/25=5000.

Break even point (sales)= Fixed costs/contribution margin=125000/0.25=500000.

Q3.) Margin of Safety= Current sales level-Break even point/Current sales level=

(60000*100-500000)*100/60000*100=450000000/6000000=75%

Q4.) Let the break even units be taken as ‘x’.

Sales 100x

Less: Variable cost(45+30) 75x

Contribution 25x

Less: Fixed cost 125000

Expected profit 100000

By solving the equation,

25x-125000=100000

x=9000 units

Break even units required=9000 units.

Q5.) Importance of classifying a fixed cost, variable cost and Semi-variable costs and relevance

to pricing decisions

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

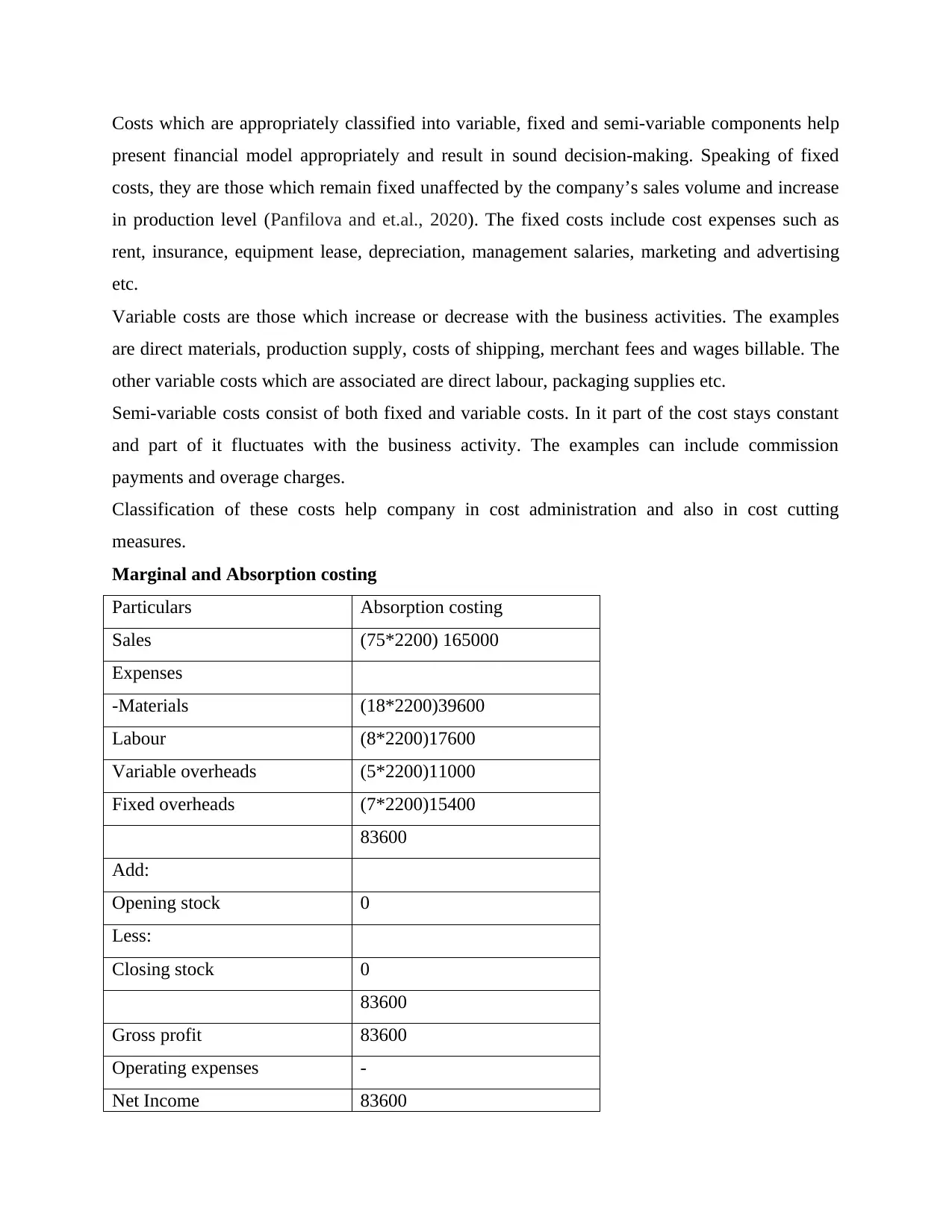

Costs which are appropriately classified into variable, fixed and semi-variable components help

present financial model appropriately and result in sound decision-making. Speaking of fixed

costs, they are those which remain fixed unaffected by the company’s sales volume and increase

in production level (Panfilova and et.al., 2020). The fixed costs include cost expenses such as

rent, insurance, equipment lease, depreciation, management salaries, marketing and advertising

etc.

Variable costs are those which increase or decrease with the business activities. The examples

are direct materials, production supply, costs of shipping, merchant fees and wages billable. The

other variable costs which are associated are direct labour, packaging supplies etc.

Semi-variable costs consist of both fixed and variable costs. In it part of the cost stays constant

and part of it fluctuates with the business activity. The examples can include commission

payments and overage charges.

Classification of these costs help company in cost administration and also in cost cutting

measures.

Marginal and Absorption costing

Particulars Absorption costing

Sales (75*2200) 165000

Expenses

-Materials (18*2200)39600

Labour (8*2200)17600

Variable overheads (5*2200)11000

Fixed overheads (7*2200)15400

83600

Add:

Opening stock 0

Less:

Closing stock 0

83600

Gross profit 83600

Operating expenses -

Net Income 83600

present financial model appropriately and result in sound decision-making. Speaking of fixed

costs, they are those which remain fixed unaffected by the company’s sales volume and increase

in production level (Panfilova and et.al., 2020). The fixed costs include cost expenses such as

rent, insurance, equipment lease, depreciation, management salaries, marketing and advertising

etc.

Variable costs are those which increase or decrease with the business activities. The examples

are direct materials, production supply, costs of shipping, merchant fees and wages billable. The

other variable costs which are associated are direct labour, packaging supplies etc.

Semi-variable costs consist of both fixed and variable costs. In it part of the cost stays constant

and part of it fluctuates with the business activity. The examples can include commission

payments and overage charges.

Classification of these costs help company in cost administration and also in cost cutting

measures.

Marginal and Absorption costing

Particulars Absorption costing

Sales (75*2200) 165000

Expenses

-Materials (18*2200)39600

Labour (8*2200)17600

Variable overheads (5*2200)11000

Fixed overheads (7*2200)15400

83600

Add:

Opening stock 0

Less:

Closing stock 0

83600

Gross profit 83600

Operating expenses -

Net Income 83600

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

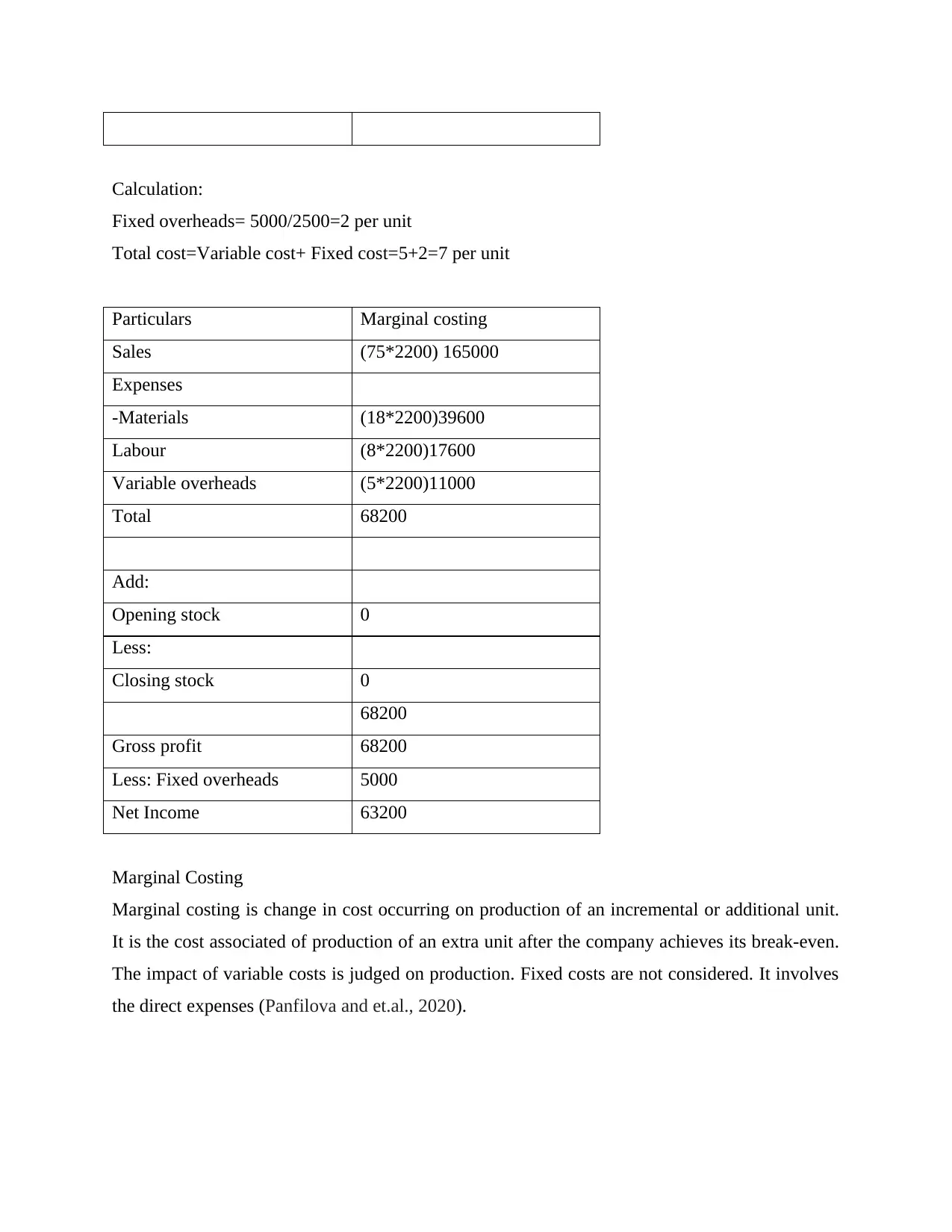

Calculation:

Fixed overheads= 5000/2500=2 per unit

Total cost=Variable cost+ Fixed cost=5+2=7 per unit

Particulars Marginal costing

Sales (75*2200) 165000

Expenses

-Materials (18*2200)39600

Labour (8*2200)17600

Variable overheads (5*2200)11000

Total 68200

Add:

Opening stock 0

Less:

Closing stock 0

68200

Gross profit 68200

Less: Fixed overheads 5000

Net Income 63200

Marginal Costing

Marginal costing is change in cost occurring on production of an incremental or additional unit.

It is the cost associated of production of an extra unit after the company achieves its break-even.

The impact of variable costs is judged on production. Fixed costs are not considered. It involves

the direct expenses (Panfilova and et.al., 2020).

Fixed overheads= 5000/2500=2 per unit

Total cost=Variable cost+ Fixed cost=5+2=7 per unit

Particulars Marginal costing

Sales (75*2200) 165000

Expenses

-Materials (18*2200)39600

Labour (8*2200)17600

Variable overheads (5*2200)11000

Total 68200

Add:

Opening stock 0

Less:

Closing stock 0

68200

Gross profit 68200

Less: Fixed overheads 5000

Net Income 63200

Marginal Costing

Marginal costing is change in cost occurring on production of an incremental or additional unit.

It is the cost associated of production of an extra unit after the company achieves its break-even.

The impact of variable costs is judged on production. Fixed costs are not considered. It involves

the direct expenses (Panfilova and et.al., 2020).

Absorption Costing

Total absorption cost accounting is a methodology of accounting price that entails the total price

of producing or providing a service. TAC includes not simply the prices of materials and labour,

however conjointly of all producing overheads. The price value of every cost center may be

direct or indirect.

It can be seen that marginal costing does not focus on fixed overhead costing on per unit basis

while absorption costing does. The key variations between marginal and absorption cost

accounting are: marginal cost accounting allows short term making of decisions and absorption

cost accounting calculates the value of output in addition as providing the closing inventory

valuation for inclusion within the monetary statements.

Part B

Q1.) Use of Budgets in controlling the operations of business

Planning: Budget helps management to forecast the future. It requires managers to signify

different departmental, operational and managerial objectives where the available resources are

allocated efficiently to achieve the objectives (Talmon and Faliszewski, 2019).

Communication: The budget is one means where all departments agree to the goals of the

organisation. It is a means to coordinate different operational functions of departments.

Responsibility: Budget assigns responsibility for utilising allocated financial resources to

achieve the operational objectives. The budget is a monetary tool by which managers compare

different costs and benefits of various activities and this helps them in allocation of various

resources appropriately.

Appraisal: The actual organizational results against the budget are compared through which

performance of manager can be evaluated. The departments which could achieve the targets

within budgetary constraints are analysed and determined and the source of variances are also

analysed for the departments which could not do so.

Total absorption cost accounting is a methodology of accounting price that entails the total price

of producing or providing a service. TAC includes not simply the prices of materials and labour,

however conjointly of all producing overheads. The price value of every cost center may be

direct or indirect.

It can be seen that marginal costing does not focus on fixed overhead costing on per unit basis

while absorption costing does. The key variations between marginal and absorption cost

accounting are: marginal cost accounting allows short term making of decisions and absorption

cost accounting calculates the value of output in addition as providing the closing inventory

valuation for inclusion within the monetary statements.

Part B

Q1.) Use of Budgets in controlling the operations of business

Planning: Budget helps management to forecast the future. It requires managers to signify

different departmental, operational and managerial objectives where the available resources are

allocated efficiently to achieve the objectives (Talmon and Faliszewski, 2019).

Communication: The budget is one means where all departments agree to the goals of the

organisation. It is a means to coordinate different operational functions of departments.

Responsibility: Budget assigns responsibility for utilising allocated financial resources to

achieve the operational objectives. The budget is a monetary tool by which managers compare

different costs and benefits of various activities and this helps them in allocation of various

resources appropriately.

Appraisal: The actual organizational results against the budget are compared through which

performance of manager can be evaluated. The departments which could achieve the targets

within budgetary constraints are analysed and determined and the source of variances are also

analysed for the departments which could not do so.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Monitoring: The budget supports the efforts of manager to monitor operations with

identification of variances and take corrective action where necessary. It allows evaluation of

activities which contribute towards organisational objectives.

Resource Allocation: The budget supports efficient allocation in a way that controls the volume

of goods and services that can be produced. The budget is used to plan the cost of output which

is produced (Talmon and Faliszewski, 2019).

Budgeting is a very important part within the planning and management method. Planning

provides a framework that helps management to develop a thought of action, to estimate future

revenues and prices, to anticipate future events, to scale back uncertainty concerning the longer

term and to extend the possibilities of achieving the goals and objectives of the organisation

through coordination of plans. Control is the method of utilising feedback on actual

performances and results, comparison of the actual results with the plans, taking measurement of

its deviations from set ups and policies and at last taking corrective actions to bring all future

activities in line with the plan.

Budgetary control is basically a method wherever the particular results i.e. actual revenues and

expenses square measure compared with the budget planned before the beginning of the fiscal

year. It highlights the requirement for adjustment of the performance, if needed. It conjointly

shows however well the managers have controlled prices in operations in an accounting period.

BUDGETARY TECHNIQUES

For the aim of fund management, varied techniques are used that are explained as follows

1. Variance Analysis: In the following analysis, Budget is prepared for every and each

department. Further, a comparison is created between the actual and estimated accounting

figures. With the assistance of this system, variances can be found. The variances square

measure any divided into Favorable and Unfavorable Variances. For instance, the distinction

between actual cost and calculable cost are going to be denoted by production variance. This

technique helps in reducing price and is usually used for fund management.

Advantages:

identification of variances and take corrective action where necessary. It allows evaluation of

activities which contribute towards organisational objectives.

Resource Allocation: The budget supports efficient allocation in a way that controls the volume

of goods and services that can be produced. The budget is used to plan the cost of output which

is produced (Talmon and Faliszewski, 2019).

Budgeting is a very important part within the planning and management method. Planning

provides a framework that helps management to develop a thought of action, to estimate future

revenues and prices, to anticipate future events, to scale back uncertainty concerning the longer

term and to extend the possibilities of achieving the goals and objectives of the organisation

through coordination of plans. Control is the method of utilising feedback on actual

performances and results, comparison of the actual results with the plans, taking measurement of

its deviations from set ups and policies and at last taking corrective actions to bring all future

activities in line with the plan.

Budgetary control is basically a method wherever the particular results i.e. actual revenues and

expenses square measure compared with the budget planned before the beginning of the fiscal

year. It highlights the requirement for adjustment of the performance, if needed. It conjointly

shows however well the managers have controlled prices in operations in an accounting period.

BUDGETARY TECHNIQUES

For the aim of fund management, varied techniques are used that are explained as follows

1. Variance Analysis: In the following analysis, Budget is prepared for every and each

department. Further, a comparison is created between the actual and estimated accounting

figures. With the assistance of this system, variances can be found. The variances square

measure any divided into Favorable and Unfavorable Variances. For instance, the distinction

between actual cost and calculable cost are going to be denoted by production variance. This

technique helps in reducing price and is usually used for fund management.

Advantages:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

a) It helps in measure of performances of assorted departments and ascertain the

explanations if they have not performed up to the mark.

b) Material variances are identified wherever prices differ from actual costs.

Disadvantages:

a) Departments might not be guilty for deviation as generally the cause could also be rise in

market costs that it doesn't soak up thought.

b) It can happen that wrong costs are set as normal costs by errors in calculation.

2. Responsibility Accounting: It is thought of to be an honest technique for fund management. In

this, three centres specifically price Centre, Profit Centre and Investment Centre is made. All

these centres are just like the department of the organization and workers are classified on the

idea of those centres. The performance of the staff is manually recorded and their responsibility

is fastened concerning sure goals that may be quantitative or qualitative. This system helps to

require call concerning promotion or change based on employee’s performance.

Advantages:

a) Provides the way to take care of a wide-ranging organisation because it is split in centres.

b)Provides incentives to managers furthermore as staff as per their performance and motivates

for future.

Disadvantages:

a) A sound organisational structure is obligatory for it to be enforced.

b) It needs analysis of the classical technique which might be tedious and time intense.

3. Adjustment of funds: Under this system, top management takes selections concerning

adjustment of funds from one project to a different project. For instance, if a brand new project

started by organisation wants cash and there's surplus cash allotted to an already existing project,

then the excess funds is adjusted against new project for its initial setup. This system facilitates

correct allocation and adjustment of funds and prevents misuse (Miller, Hildreth and Rabin,

2018).

Advantages:

a) It helps in right usage of funds wherever there's a surplus.

explanations if they have not performed up to the mark.

b) Material variances are identified wherever prices differ from actual costs.

Disadvantages:

a) Departments might not be guilty for deviation as generally the cause could also be rise in

market costs that it doesn't soak up thought.

b) It can happen that wrong costs are set as normal costs by errors in calculation.

2. Responsibility Accounting: It is thought of to be an honest technique for fund management. In

this, three centres specifically price Centre, Profit Centre and Investment Centre is made. All

these centres are just like the department of the organization and workers are classified on the

idea of those centres. The performance of the staff is manually recorded and their responsibility

is fastened concerning sure goals that may be quantitative or qualitative. This system helps to

require call concerning promotion or change based on employee’s performance.

Advantages:

a) Provides the way to take care of a wide-ranging organisation because it is split in centres.

b)Provides incentives to managers furthermore as staff as per their performance and motivates

for future.

Disadvantages:

a) A sound organisational structure is obligatory for it to be enforced.

b) It needs analysis of the classical technique which might be tedious and time intense.

3. Adjustment of funds: Under this system, top management takes selections concerning

adjustment of funds from one project to a different project. For instance, if a brand new project

started by organisation wants cash and there's surplus cash allotted to an already existing project,

then the excess funds is adjusted against new project for its initial setup. This system facilitates

correct allocation and adjustment of funds and prevents misuse (Miller, Hildreth and Rabin,

2018).

Advantages:

a) It helps in right usage of funds wherever there's a surplus.

b) It helps in saving the capital for more wants by doing changes of surplus money as

adjustments.

Disadvantages:

a) The adjustment of funds might prove wrong if the project from which funds are adjusted

needs funds in long run.

b) The accounting entries need to be done rigorously of adjustment of funds as discrepancies can

occur afterward.

4. Zero based Budgeting: Another technique that is vastly followed and is standard lately is zero

based budgeting. Beneath this system, budget of next year is taken into account as nil which

might be solely attainable if calculable revenue is adequate to calculable expenses. At that point,

distinction between calculable revenue and calculable expenses are going to be zero. Any excess

quantity of cash is going to be adjusted. This system helps in managing over every and each

quantity of cash spent throughout the year (Nikulina, 2019).

Advantages: a) Accuracy: the tactic is correct in shrewd prices and forming budget because it

focuses on things line by line and uses the present wants of budget allocation for every product.

b)Efficiency: It's economical in allocation of finance because it doesn't concentrate on historical

knowledge and focuses on actual knowledge.

Disadvantages: a) It's time taking process because it takes in account all line expense of

commodities.

b) There's a demand of high manpower to form the budget from scratch therefore seizing time

and value for creating the budget.

Q2.) Material Price Variance=Actual Quantity*(Standard price-Actual price)

=12000*(39-35) =48000. This is favourable as the actual price is less than standard price.

adjustments.

Disadvantages:

a) The adjustment of funds might prove wrong if the project from which funds are adjusted

needs funds in long run.

b) The accounting entries need to be done rigorously of adjustment of funds as discrepancies can

occur afterward.

4. Zero based Budgeting: Another technique that is vastly followed and is standard lately is zero

based budgeting. Beneath this system, budget of next year is taken into account as nil which

might be solely attainable if calculable revenue is adequate to calculable expenses. At that point,

distinction between calculable revenue and calculable expenses are going to be zero. Any excess

quantity of cash is going to be adjusted. This system helps in managing over every and each

quantity of cash spent throughout the year (Nikulina, 2019).

Advantages: a) Accuracy: the tactic is correct in shrewd prices and forming budget because it

focuses on things line by line and uses the present wants of budget allocation for every product.

b)Efficiency: It's economical in allocation of finance because it doesn't concentrate on historical

knowledge and focuses on actual knowledge.

Disadvantages: a) It's time taking process because it takes in account all line expense of

commodities.

b) There's a demand of high manpower to form the budget from scratch therefore seizing time

and value for creating the budget.

Q2.) Material Price Variance=Actual Quantity*(Standard price-Actual price)

=12000*(39-35) =48000. This is favourable as the actual price is less than standard price.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Material Usage Variance= (standard quantity of material used for production – actual quantity

used) × standard price per unit of material) = (6-5)*3=3.

The standard quantity of material is more than the actual thus making the variance favourable.

Labour Rate Variance=Actual hours*actual rate-actual hours*standard rate=2*3-2*5=-4

The labour rate variance is not favourable as the variance is negative.

Labour efficiency variance= (standard hours-actual hours)*standard rate per direct labour

hours=(3-2)*5=5

Fixed overhead expenditure variance=Actual fixed overhead cost-Budgeted fixed overhead

cost=13000-15000=2000.

The variance is favourable as the actual cost is less than budgeted cost.

Q3.) Budget for controlling operations

Particulars Per unit Total

Direct material 18 18*12000=216000

Direct Labour 15 15*12000=180000

Price cost 33 396000

Add: Factory Overheads 15000

Total cost 411000

Direct Materials Budget

Particulars Amount

Production Target 12000 units

Required direct material per unit 6 kg

Desired closing inventory -

Opening Inventory 18

Cost per unit 18

Total Raw materials budget 216000

used) × standard price per unit of material) = (6-5)*3=3.

The standard quantity of material is more than the actual thus making the variance favourable.

Labour Rate Variance=Actual hours*actual rate-actual hours*standard rate=2*3-2*5=-4

The labour rate variance is not favourable as the variance is negative.

Labour efficiency variance= (standard hours-actual hours)*standard rate per direct labour

hours=(3-2)*5=5

Fixed overhead expenditure variance=Actual fixed overhead cost-Budgeted fixed overhead

cost=13000-15000=2000.

The variance is favourable as the actual cost is less than budgeted cost.

Q3.) Budget for controlling operations

Particulars Per unit Total

Direct material 18 18*12000=216000

Direct Labour 15 15*12000=180000

Price cost 33 396000

Add: Factory Overheads 15000

Total cost 411000

Direct Materials Budget

Particulars Amount

Production Target 12000 units

Required direct material per unit 6 kg

Desired closing inventory -

Opening Inventory 18

Cost per unit 18

Total Raw materials budget 216000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Direct Labour Budget

Particulars Amount

Units to be produced 12000

Direct labour hours per unit 2

Total direct labour hours required 3

Labour cost per hour 5

Total Direct Labour cost 15

Variable overhead unit

Particulars Amount

Budgeted production units 12000

Variable factory overhead rate 6

Budgeted variable overhead 48000

Total variable overhead 48000

Fixed overhead expenditure budget

Particulars Amount

Budgeted production units 12000

Fixed factory overhead rate 13000

Budgeted fixed overhead 15000

CONCLUSION

It can be concluded that an organisation has to determine various costs and analyse whether it

has been favourable for them or not. A company which can effectively control operating costs

can only register profits after the departments being able to perform as per budgetary constraints.

A company which can achieve the budgetary guidelines can effectively plan for the future with

the capital generated. The role of budgeting has evolved in many new methods been highlighted

Particulars Amount

Units to be produced 12000

Direct labour hours per unit 2

Total direct labour hours required 3

Labour cost per hour 5

Total Direct Labour cost 15

Variable overhead unit

Particulars Amount

Budgeted production units 12000

Variable factory overhead rate 6

Budgeted variable overhead 48000

Total variable overhead 48000

Fixed overhead expenditure budget

Particulars Amount

Budgeted production units 12000

Fixed factory overhead rate 13000

Budgeted fixed overhead 15000

CONCLUSION

It can be concluded that an organisation has to determine various costs and analyse whether it

has been favourable for them or not. A company which can effectively control operating costs

can only register profits after the departments being able to perform as per budgetary constraints.

A company which can achieve the budgetary guidelines can effectively plan for the future with

the capital generated. The role of budgeting has evolved in many new methods been highlighted

and it shows the efficiency of various budgetary tools that can guide to make a perfect budget for

the company. The different formats of budget have been highlighted.

the company. The different formats of budget have been highlighted.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.