Critical Use Accounting Information: Financial Analysis Report

VerifiedAdded on 2021/05/31

|11

|2406

|16

Report

AI Summary

This report provides a detailed analysis of the critical use of accounting information, focusing on the generation of shareholder wealth through the comparison of Bisalloy Steel Group Limited and Aurelia Metals Ltd. It examines key financial ratios such as asset turnover ratio, net profit margin ratio, and return on assets (ROA) to assess company performance. The report delves into the measurement of resources and wealth, differentiating between monetary and non-monetary wealth, and discusses the limitations of ROA, including the impact of intangible assets and borrowed capital. Real-world examples, such as the case of Motorola, are used to illustrate the practical implications of these financial metrics. The report concludes by suggesting improvements to ROA calculations to provide a more accurate picture of a company's financial health by incorporating liabilities.

Running head: CRITICAL USE ACCOUNTING INFORMATION

Critical use accounting information

Name of the student

Name of the university

Student ID

Author note

Critical use accounting information

Name of the student

Name of the university

Student ID

Author note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1CRITICAL USE ACCOUNTING INFORMATION

Table of Contents

Answer (a)..................................................................................................................................2

Answer (b)..................................................................................................................................2

Answer (c)..................................................................................................................................4

Answer (d)..................................................................................................................................8

Reference....................................................................................................................................9

Table of Contents

Answer (a)..................................................................................................................................2

Answer (b)..................................................................................................................................2

Answer (c)..................................................................................................................................4

Answer (d)..................................................................................................................................8

Reference....................................................................................................................................9

2CRITICAL USE ACCOUNTING INFORMATION

Answer (a)

Comparing and contrasting the generation of shareholder’s wealth

Bisalloy steel group Limited Aurelia metals Ltd

Ratio 2015 2016 2017 2015 2016 2017

Return on assets 0.06 0.07 0.06 -1.13 0.10 0.15

Asset turnover ratio 1.29 1.56 2.37 0.09 1.75 0.92

Net profit margin ratio 4.62 3.16 2.74 -893.77 11.90 17.81

Asset turnover ratio – the asset turnover ratio of the company measures the efficiency of the

company with regard to producing of the revenue. Therefore, the ratio can determine the

performance of the company. It is identified that the asset turnover ratio of Bisalloy group for

the years 2015, 2016 and 2017 are in increasing trend and it reached to 2.37 from 1.29. on the

other hand, the asset turnover ratio of Aurelia metals was fluctuating and it just reached to

0.92 from 0.09 (Alghifari, Triharjono & Juhaeni, 2013).

Net profit margin ratio –it measures the efficiency of the company to earn profit from the

sales after paying off the expenses. It can be identified that the net profit of Bisalloy is in

decreasing trend whereas the net profit for Aurelia for 2015 is in negative. However, for other

2 years that is 2016 and 2017 the net profit of Aurelia is comparatively better as compared to

Bisalloy steel group (Niresh & Thirunavukkarasu, 2014).

Therefore, if above mentioned both the ratios are taken into consideration it can be

stated that the Bisalloy group is more efficient in generating shareholder’s wealth as

compared to Aurelia Steel.

Answer (b)

Return on assets – the return on asset ratio or the return on the total assets is the profitability

ratio that is used to measure net income of the company generated by the total assets of the

company during specific period of time through comparing it with the net income of the

company. It measures the efficiency of the company regarding managing of its asset for

generating the profits during the particular period (Li, 2015). ROA is calculated through

dividing the net income by the average assets of the company. It can be identified that the

return on assets of Bisalloy Steel group ltd for the year 2015, 2016 and 2017 is 0.06, 0.07 and

Answer (a)

Comparing and contrasting the generation of shareholder’s wealth

Bisalloy steel group Limited Aurelia metals Ltd

Ratio 2015 2016 2017 2015 2016 2017

Return on assets 0.06 0.07 0.06 -1.13 0.10 0.15

Asset turnover ratio 1.29 1.56 2.37 0.09 1.75 0.92

Net profit margin ratio 4.62 3.16 2.74 -893.77 11.90 17.81

Asset turnover ratio – the asset turnover ratio of the company measures the efficiency of the

company with regard to producing of the revenue. Therefore, the ratio can determine the

performance of the company. It is identified that the asset turnover ratio of Bisalloy group for

the years 2015, 2016 and 2017 are in increasing trend and it reached to 2.37 from 1.29. on the

other hand, the asset turnover ratio of Aurelia metals was fluctuating and it just reached to

0.92 from 0.09 (Alghifari, Triharjono & Juhaeni, 2013).

Net profit margin ratio –it measures the efficiency of the company to earn profit from the

sales after paying off the expenses. It can be identified that the net profit of Bisalloy is in

decreasing trend whereas the net profit for Aurelia for 2015 is in negative. However, for other

2 years that is 2016 and 2017 the net profit of Aurelia is comparatively better as compared to

Bisalloy steel group (Niresh & Thirunavukkarasu, 2014).

Therefore, if above mentioned both the ratios are taken into consideration it can be

stated that the Bisalloy group is more efficient in generating shareholder’s wealth as

compared to Aurelia Steel.

Answer (b)

Return on assets – the return on asset ratio or the return on the total assets is the profitability

ratio that is used to measure net income of the company generated by the total assets of the

company during specific period of time through comparing it with the net income of the

company. It measures the efficiency of the company regarding managing of its asset for

generating the profits during the particular period (Li, 2015). ROA is calculated through

dividing the net income by the average assets of the company. It can be identified that the

return on assets of Bisalloy Steel group ltd for the year 2015, 2016 and 2017 is 0.06, 0.07 and

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3CRITICAL USE ACCOUNTING INFORMATION

0.06 respectively. On the other hand the RA of Aurelia metals for the year 2015, 2016 and

2017 were -1.13, 0.10 and 0.15 respectively. Therefore, except for 2015 the return on assets

of Aurelia metals ltd is comparatively better for the year 2016 as well as 2017.

ROA on the assets signifies that the amount of the money earned against each dollar

of the assets. Hence, the higher return on the assets value signifies that the business is more

efficient and profitable. Further, it is noteworthy that the ROA shall not be compared across

the industries; rather it shall be compared among the companies with regard to analysing their

efficiency in utilizing the assets. Further, ROA is also used for measuring how the company

is asset intensive (Grant, 2016). If the ROA of the company is lower, the company will be

considered as more asset-intensive. On the contrary, if the ROA of the asset is higher, then

the company will be regarded as less asset-intensive. ROA is generally used by the analysts

who perform the financial analysis of the company’s performance. ROA is crucial as it helps

in comparing the companies to compare their profitability positions (Graves & Shan, 2014).

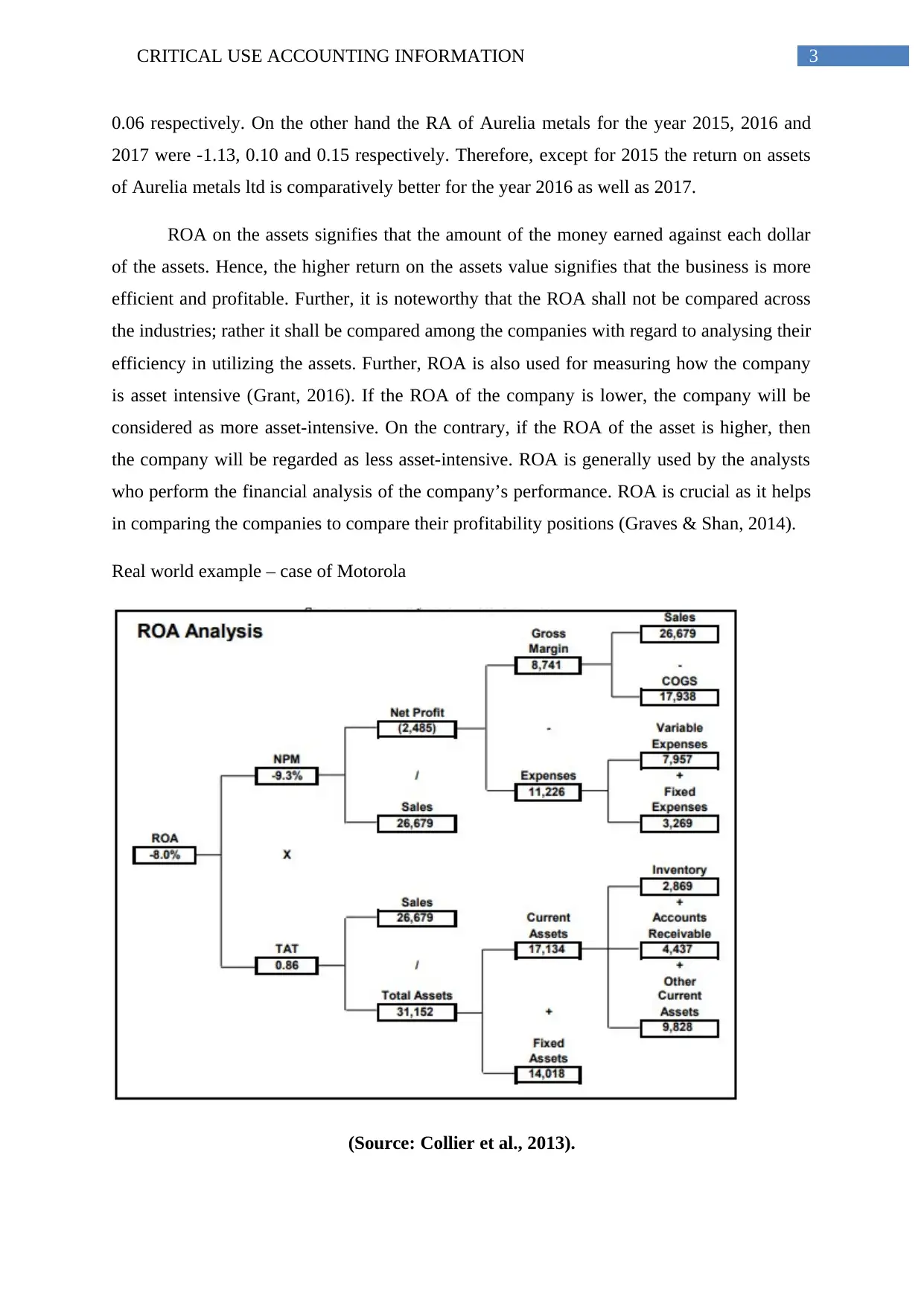

Real world example – case of Motorola

(Source: Collier et al., 2013).

0.06 respectively. On the other hand the RA of Aurelia metals for the year 2015, 2016 and

2017 were -1.13, 0.10 and 0.15 respectively. Therefore, except for 2015 the return on assets

of Aurelia metals ltd is comparatively better for the year 2016 as well as 2017.

ROA on the assets signifies that the amount of the money earned against each dollar

of the assets. Hence, the higher return on the assets value signifies that the business is more

efficient and profitable. Further, it is noteworthy that the ROA shall not be compared across

the industries; rather it shall be compared among the companies with regard to analysing their

efficiency in utilizing the assets. Further, ROA is also used for measuring how the company

is asset intensive (Grant, 2016). If the ROA of the company is lower, the company will be

considered as more asset-intensive. On the contrary, if the ROA of the asset is higher, then

the company will be regarded as less asset-intensive. ROA is generally used by the analysts

who perform the financial analysis of the company’s performance. ROA is crucial as it helps

in comparing the companies to compare their profitability positions (Graves & Shan, 2014).

Real world example – case of Motorola

(Source: Collier et al., 2013).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4CRITICAL USE ACCOUNTING INFORMATION

It can be identified from the above image that the large amounts of fixed and variable

expenses are adversely impacting the ROA. As per the management’s view, these expenses

particularly the variable expenses that include the general, administrative and selling

expenses are required to be evaluated closely as they are considered as easily controllable.

Further, the increase in the revenue may also help to increase the ROA status. Although

overall poor market condition is also responsible for the low sales figure of Motorola, the

management also critically evaluated the reason why it lost market share in some of its key

business segment over the last few years that led to poor operating results. The management

therefore took the decision to develop the business and business strategy for increasing the

sales and controlling the fixed and variable expenses at the same time (Collier et al., 2013).

It can be seen that the ROA of Aurelia Metals Ltd is -1.13 for the year 2015, it

signifies that the negative net income of the company led to negative return on assets.

Therefore, the company should have been try to control its fixed as well as variable expenses

that will increase its net income (Muhammad & Scrimgeour, 2014). Further, it shall carry on

some market research regarding the customer demand, preference so that it can increase its

sales which in turn will help to increase the net income as well as the ROA. On the other

hand the ROA of Bisalloy Steel Group for all the 3 years are 0.06, 0.07 and 0.06 respectively

for the year 2015, 2016 and 2017. Therefore, to increase the ROA the company must try to

increase its net income through controlling its fixed as well as variable expenses. Further, it

can also try to increase its revenue through market research (Xiang, Worthington & Higgs,

2015).

Answer (c)

Measurement of resources and wealth with company asset and profits

The surplus that remains after payment of total cost from the revenue and from which

the tax is computed and the dividend is paid is known as the profit. Profit is represented to

reduce the liabilities, increasing the assets and increasing the wealth of the company. Further,

it furnishes the resources of the company available for investing in the future operations and

the absence of which may lead to extinction of the company. As indicator of the comparative

performances, it is less valuable as compared to return on investment that is also known as

gain, earnings or income. On the other hand the net assets represents the cash, tangible assets

like land, building, property and other intangible assets reduced by the liabilities of the

It can be identified from the above image that the large amounts of fixed and variable

expenses are adversely impacting the ROA. As per the management’s view, these expenses

particularly the variable expenses that include the general, administrative and selling

expenses are required to be evaluated closely as they are considered as easily controllable.

Further, the increase in the revenue may also help to increase the ROA status. Although

overall poor market condition is also responsible for the low sales figure of Motorola, the

management also critically evaluated the reason why it lost market share in some of its key

business segment over the last few years that led to poor operating results. The management

therefore took the decision to develop the business and business strategy for increasing the

sales and controlling the fixed and variable expenses at the same time (Collier et al., 2013).

It can be seen that the ROA of Aurelia Metals Ltd is -1.13 for the year 2015, it

signifies that the negative net income of the company led to negative return on assets.

Therefore, the company should have been try to control its fixed as well as variable expenses

that will increase its net income (Muhammad & Scrimgeour, 2014). Further, it shall carry on

some market research regarding the customer demand, preference so that it can increase its

sales which in turn will help to increase the net income as well as the ROA. On the other

hand the ROA of Bisalloy Steel Group for all the 3 years are 0.06, 0.07 and 0.06 respectively

for the year 2015, 2016 and 2017. Therefore, to increase the ROA the company must try to

increase its net income through controlling its fixed as well as variable expenses. Further, it

can also try to increase its revenue through market research (Xiang, Worthington & Higgs,

2015).

Answer (c)

Measurement of resources and wealth with company asset and profits

The surplus that remains after payment of total cost from the revenue and from which

the tax is computed and the dividend is paid is known as the profit. Profit is represented to

reduce the liabilities, increasing the assets and increasing the wealth of the company. Further,

it furnishes the resources of the company available for investing in the future operations and

the absence of which may lead to extinction of the company. As indicator of the comparative

performances, it is less valuable as compared to return on investment that is also known as

gain, earnings or income. On the other hand the net assets represents the cash, tangible assets

like land, building, property and other intangible assets reduced by the liabilities of the

5CRITICAL USE ACCOUNTING INFORMATION

company. Total of all the assets of any economic unit that is used to generate the current

income or that has the potential to create the future income includes the human capital and

natural resources. However, it excludes the securities and money as it represents claims to the

wealth only. 2 common economic wealth types are –

Monetary wealth – it represents that anything can be sold or bought and for which a

market exists there and therefore the price. However, the market price represents the

commodity price only and not the value necessarily. For instance, the product that is

sold or services provided by the company (Heikal, Khaddafi & Ummah, 2014).

Non-monetary wealth – these things are depended on scarce resources and there is a

demand for threes things but are not sold or bought in the regular market and

therefore, price is not fixed. For instance, goodwill and patents.

Limitations of ROA

ROA is the valuation multiples that are commonly used by the investors for

evaluating the potential investments. Main objective of this ratio is determining the efficiency

of the company to work on its assets available with it. Though this ratio is beneficial, some

limitations are also there those are associated with the company. They are as follows –

Intangible assets – the biggest limitations associated with ROA is that it does not

consider the intangible assets. Most of the companies in present scenario heavily rely

on the the intangible assets for providing great deal of the value to the entity (Graves

& Shan, 2014).

Borrowed capital – another limitation associated with using the ROA is that it does

not consider borrowed capital. Large company’s success is generally depends on the

combination of equity and debt financing. If this metric is used for making

investment decisions the investor will ignore the borrowed capital part of the

company that plays important in making investment decisions (Cook & Glass, 2014).

Incorporating above limitations in comparability of the companies

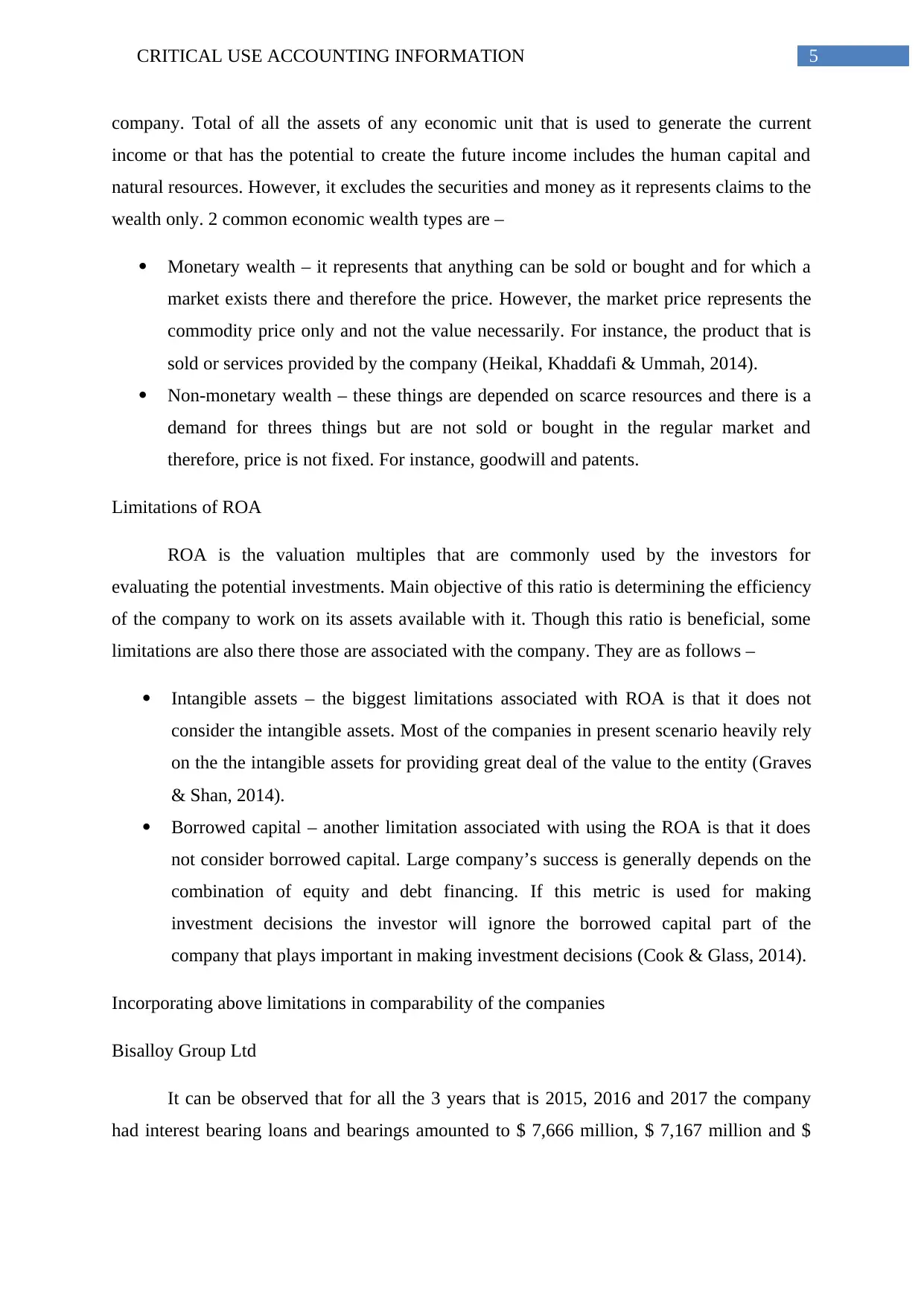

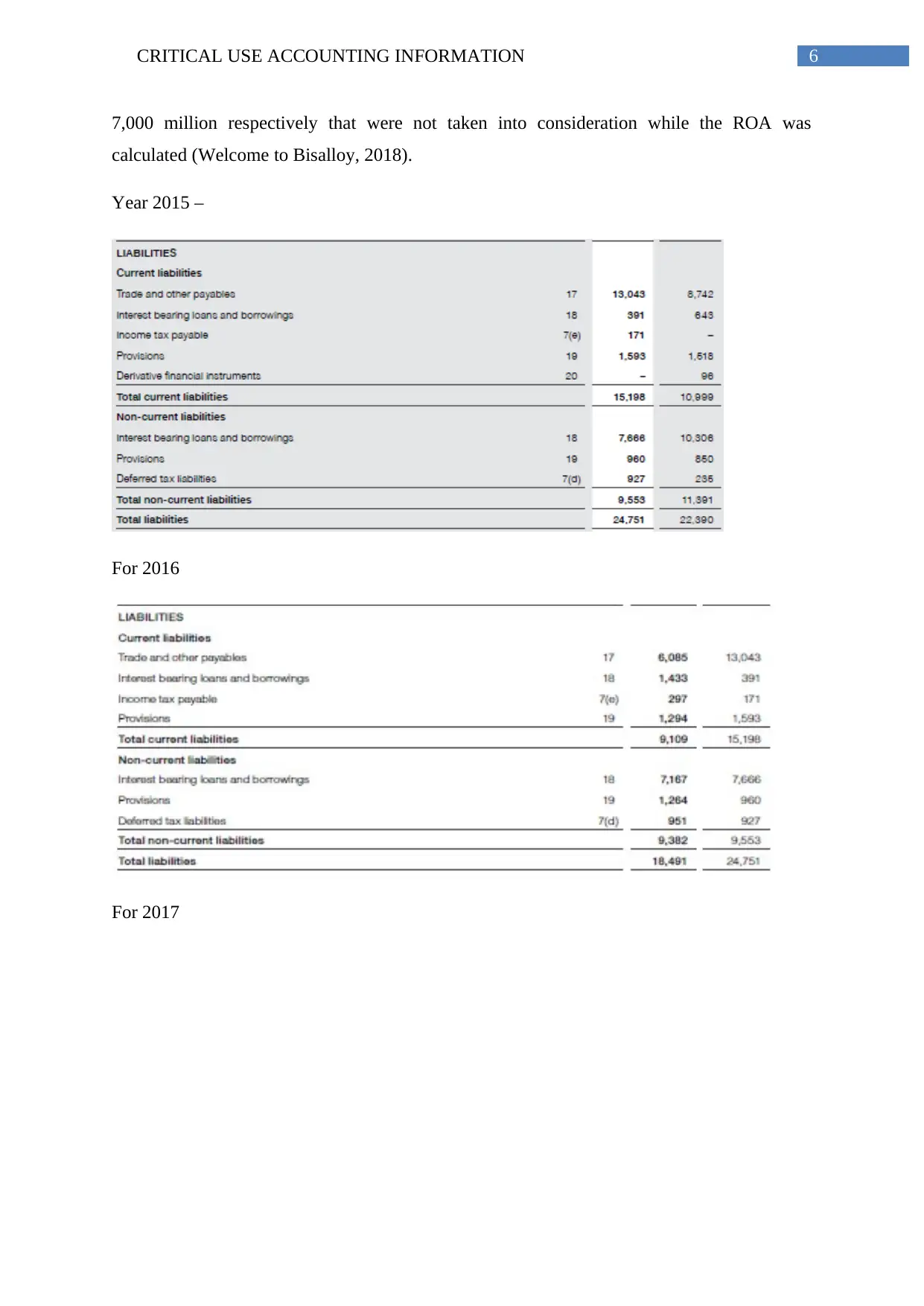

Bisalloy Group Ltd

It can be observed that for all the 3 years that is 2015, 2016 and 2017 the company

had interest bearing loans and bearings amounted to $ 7,666 million, $ 7,167 million and $

company. Total of all the assets of any economic unit that is used to generate the current

income or that has the potential to create the future income includes the human capital and

natural resources. However, it excludes the securities and money as it represents claims to the

wealth only. 2 common economic wealth types are –

Monetary wealth – it represents that anything can be sold or bought and for which a

market exists there and therefore the price. However, the market price represents the

commodity price only and not the value necessarily. For instance, the product that is

sold or services provided by the company (Heikal, Khaddafi & Ummah, 2014).

Non-monetary wealth – these things are depended on scarce resources and there is a

demand for threes things but are not sold or bought in the regular market and

therefore, price is not fixed. For instance, goodwill and patents.

Limitations of ROA

ROA is the valuation multiples that are commonly used by the investors for

evaluating the potential investments. Main objective of this ratio is determining the efficiency

of the company to work on its assets available with it. Though this ratio is beneficial, some

limitations are also there those are associated with the company. They are as follows –

Intangible assets – the biggest limitations associated with ROA is that it does not

consider the intangible assets. Most of the companies in present scenario heavily rely

on the the intangible assets for providing great deal of the value to the entity (Graves

& Shan, 2014).

Borrowed capital – another limitation associated with using the ROA is that it does

not consider borrowed capital. Large company’s success is generally depends on the

combination of equity and debt financing. If this metric is used for making

investment decisions the investor will ignore the borrowed capital part of the

company that plays important in making investment decisions (Cook & Glass, 2014).

Incorporating above limitations in comparability of the companies

Bisalloy Group Ltd

It can be observed that for all the 3 years that is 2015, 2016 and 2017 the company

had interest bearing loans and bearings amounted to $ 7,666 million, $ 7,167 million and $

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6CRITICAL USE ACCOUNTING INFORMATION

7,000 million respectively that were not taken into consideration while the ROA was

calculated (Welcome to Bisalloy, 2018).

Year 2015 –

For 2016

For 2017

7,000 million respectively that were not taken into consideration while the ROA was

calculated (Welcome to Bisalloy, 2018).

Year 2015 –

For 2016

For 2017

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7CRITICAL USE ACCOUNTING INFORMATION

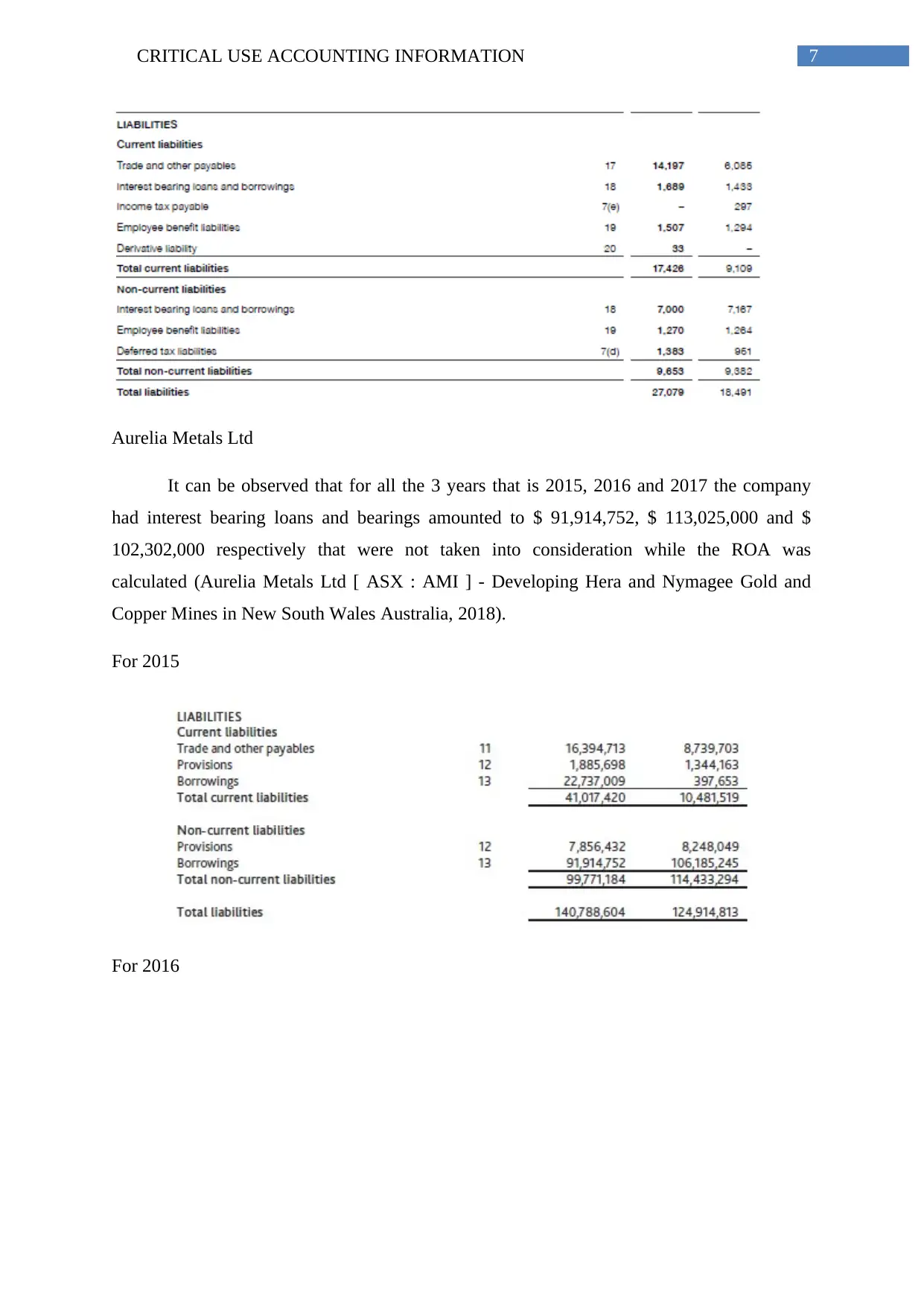

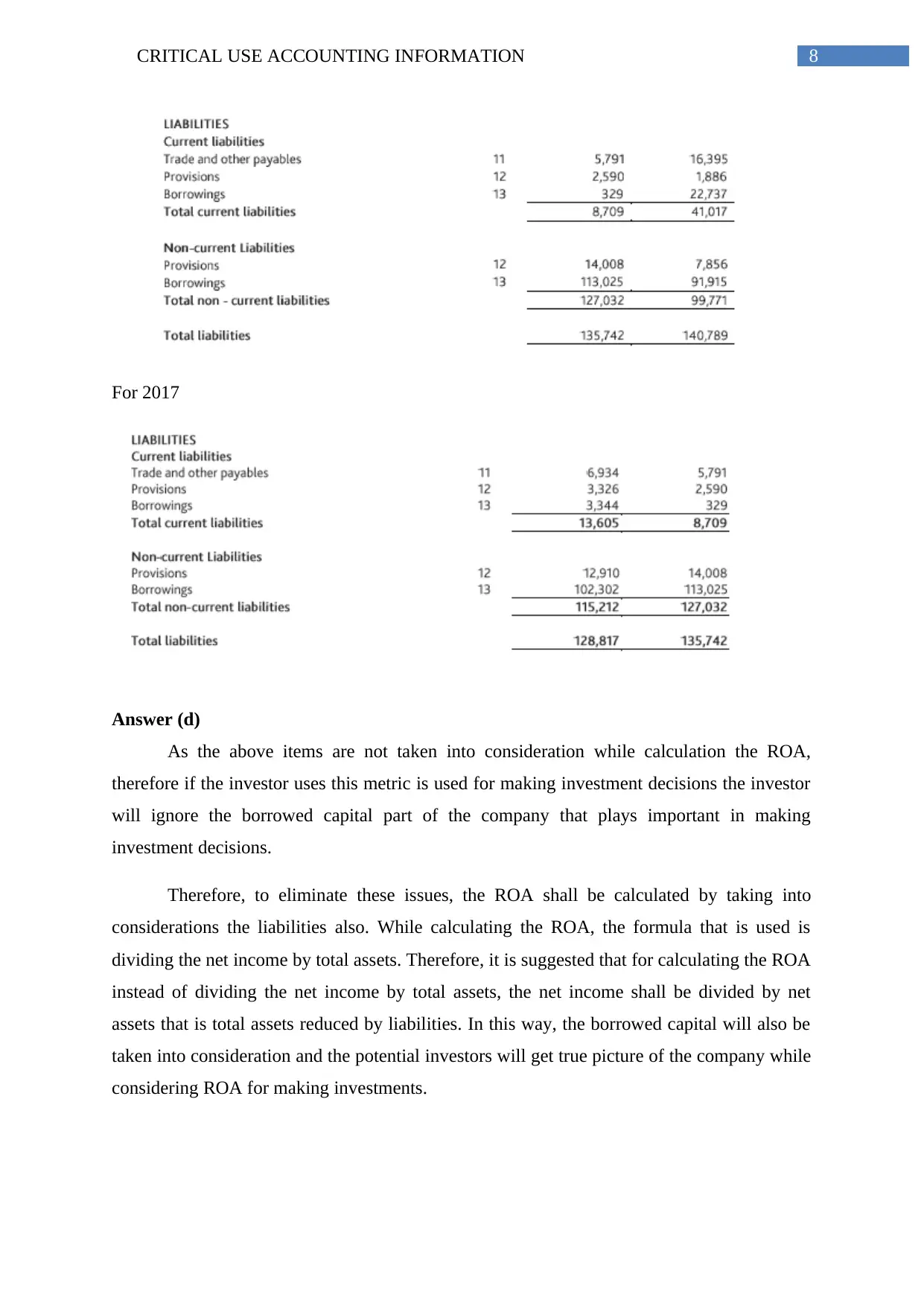

Aurelia Metals Ltd

It can be observed that for all the 3 years that is 2015, 2016 and 2017 the company

had interest bearing loans and bearings amounted to $ 91,914,752, $ 113,025,000 and $

102,302,000 respectively that were not taken into consideration while the ROA was

calculated (Aurelia Metals Ltd [ ASX : AMI ] - Developing Hera and Nymagee Gold and

Copper Mines in New South Wales Australia, 2018).

For 2015

For 2016

Aurelia Metals Ltd

It can be observed that for all the 3 years that is 2015, 2016 and 2017 the company

had interest bearing loans and bearings amounted to $ 91,914,752, $ 113,025,000 and $

102,302,000 respectively that were not taken into consideration while the ROA was

calculated (Aurelia Metals Ltd [ ASX : AMI ] - Developing Hera and Nymagee Gold and

Copper Mines in New South Wales Australia, 2018).

For 2015

For 2016

8CRITICAL USE ACCOUNTING INFORMATION

For 2017

Answer (d)

As the above items are not taken into consideration while calculation the ROA,

therefore if the investor uses this metric is used for making investment decisions the investor

will ignore the borrowed capital part of the company that plays important in making

investment decisions.

Therefore, to eliminate these issues, the ROA shall be calculated by taking into

considerations the liabilities also. While calculating the ROA, the formula that is used is

dividing the net income by total assets. Therefore, it is suggested that for calculating the ROA

instead of dividing the net income by total assets, the net income shall be divided by net

assets that is total assets reduced by liabilities. In this way, the borrowed capital will also be

taken into consideration and the potential investors will get true picture of the company while

considering ROA for making investments.

For 2017

Answer (d)

As the above items are not taken into consideration while calculation the ROA,

therefore if the investor uses this metric is used for making investment decisions the investor

will ignore the borrowed capital part of the company that plays important in making

investment decisions.

Therefore, to eliminate these issues, the ROA shall be calculated by taking into

considerations the liabilities also. While calculating the ROA, the formula that is used is

dividing the net income by total assets. Therefore, it is suggested that for calculating the ROA

instead of dividing the net income by total assets, the net income shall be divided by net

assets that is total assets reduced by liabilities. In this way, the borrowed capital will also be

taken into consideration and the potential investors will get true picture of the company while

considering ROA for making investments.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9CRITICAL USE ACCOUNTING INFORMATION

Reference

Alghifari, S., Triharjono, S., & Juhaeni, Y. (2013). Effect of return on assets (ROA) against

Tobin's Q: Studies in food and beverage company in Indonesia stock exchange years

2007-2011. International Journal Of Science and Research (IJSR), 2, 108-116.

Aurelia Metals Ltd [ ASX : AMI ] - Developing Hera and Nymagee Gold and Copper Mines

in New South Wales Australia. (2018). Aureliametals.com. Retrieved 5 May 2018,

from http://www.aureliametals.com/public/default.aspx?id=1&Lvl=1

Collier, H., Grai, T., Haslitt, S., & McGowan, C. (2013). Using Actual Financial Accounting

Information To Conduct Financial Ratio Analysis: The Case Of Motorola [Ebook]

(pp. 27-28). University of Wollongong. Retrieved from

http://file:///C:/Users/user00/Downloads/887-Article%20Text-3499-1-10-

20110106.pdf

Cook, A., & Glass, C. (2014). Women and top leadership positions: Towards an institutional

analysis. Gender, Work & Organization, 21(1), 91-103.

Grant, R. M. (2016). Contemporary strategy analysis: Text and cases edition. John Wiley &

Sons.

Graves, C., & Shan, Y. G. (2014). An empirical analysis of the effect of internationalization

on the performance of unlisted family and nonfamily firms in Australia. Family

Business Review, 27(2), 142-160.

Graves, C., & Shan, Y. G. (2014). An empirical analysis of the effect of internationalization

on the performance of unlisted family and nonfamily firms in Australia. Family

Business Review, 27(2), 142-160.

Heikal, M., Khaddafi, M., & Ummah, A. (2014). Influence analysis of return on assets

(ROA), return on equity (ROE), net profit margin (NPM), debt to equity ratio (DER),

and current ratio (CR), against corporate profit growth in automotive in Indonesia

Stock Exchange. International Journal of Academic Research in Business and Social

Sciences, 4(12), 101.

Li, X. (2015). Accounting conservatism and the cost of capital: An international

analysis. Journal of Business Finance & Accounting, 42(5-6), 555-582.

Reference

Alghifari, S., Triharjono, S., & Juhaeni, Y. (2013). Effect of return on assets (ROA) against

Tobin's Q: Studies in food and beverage company in Indonesia stock exchange years

2007-2011. International Journal Of Science and Research (IJSR), 2, 108-116.

Aurelia Metals Ltd [ ASX : AMI ] - Developing Hera and Nymagee Gold and Copper Mines

in New South Wales Australia. (2018). Aureliametals.com. Retrieved 5 May 2018,

from http://www.aureliametals.com/public/default.aspx?id=1&Lvl=1

Collier, H., Grai, T., Haslitt, S., & McGowan, C. (2013). Using Actual Financial Accounting

Information To Conduct Financial Ratio Analysis: The Case Of Motorola [Ebook]

(pp. 27-28). University of Wollongong. Retrieved from

http://file:///C:/Users/user00/Downloads/887-Article%20Text-3499-1-10-

20110106.pdf

Cook, A., & Glass, C. (2014). Women and top leadership positions: Towards an institutional

analysis. Gender, Work & Organization, 21(1), 91-103.

Grant, R. M. (2016). Contemporary strategy analysis: Text and cases edition. John Wiley &

Sons.

Graves, C., & Shan, Y. G. (2014). An empirical analysis of the effect of internationalization

on the performance of unlisted family and nonfamily firms in Australia. Family

Business Review, 27(2), 142-160.

Graves, C., & Shan, Y. G. (2014). An empirical analysis of the effect of internationalization

on the performance of unlisted family and nonfamily firms in Australia. Family

Business Review, 27(2), 142-160.

Heikal, M., Khaddafi, M., & Ummah, A. (2014). Influence analysis of return on assets

(ROA), return on equity (ROE), net profit margin (NPM), debt to equity ratio (DER),

and current ratio (CR), against corporate profit growth in automotive in Indonesia

Stock Exchange. International Journal of Academic Research in Business and Social

Sciences, 4(12), 101.

Li, X. (2015). Accounting conservatism and the cost of capital: An international

analysis. Journal of Business Finance & Accounting, 42(5-6), 555-582.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10CRITICAL USE ACCOUNTING INFORMATION

Muhammad, N., & Scrimgeour, F. (2014). Stock returns and fundamentals in the Australian

market. Asian Journal of Finance & Accounting, 6(1), 271-290.

Niresh, A., & Thirunavukkarasu, V. (2014). Firm size and profitability: A study of listed

manufacturing firms in Sri Lanka.

Welcome to Bisalloy . (2018). Bisalloy.com.au. Retrieved 5 May 2018, from

https://www.bisalloy.com.au/

Xiang, D., Worthington, A. C., & Higgs, H. (2015). Discouraged finance seekers: An

analysis of Australian small and medium-sized enterprises. International Small

Business Journal, 33(7), 689-707.

Muhammad, N., & Scrimgeour, F. (2014). Stock returns and fundamentals in the Australian

market. Asian Journal of Finance & Accounting, 6(1), 271-290.

Niresh, A., & Thirunavukkarasu, V. (2014). Firm size and profitability: A study of listed

manufacturing firms in Sri Lanka.

Welcome to Bisalloy . (2018). Bisalloy.com.au. Retrieved 5 May 2018, from

https://www.bisalloy.com.au/

Xiang, D., Worthington, A. C., & Higgs, H. (2015). Discouraged finance seekers: An

analysis of Australian small and medium-sized enterprises. International Small

Business Journal, 33(7), 689-707.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.