Analysis of Capital Structure and Cost: Debenhams and Marks & Spencer

VerifiedAdded on 2020/10/22

|14

|3385

|177

Report

AI Summary

This report conducts a comparative financial analysis of Debenhams PLC and Marks & Spencer Group PLC, focusing on key aspects of corporate financial management. It examines the capital structure of both companies, analyzing their debt and equity components over a period of time, and calculates the weighted average cost of capital (WACC) to assess the companies' financing costs. The report also delves into the cost of capital using the discounted cash flow (DCF) model to evaluate investment attractiveness. Furthermore, it applies ratio analysis, including current and quick ratios, to assess the financial performance and liquidity of both companies. The analysis provides insights into the financial health and strategic decisions of these two prominent retailers, highlighting their similarities and differences in financial management practices.

CORPORATE

FINANCIAL

MANAGEMENT

FINANCIAL

MANAGEMENT

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION ..........................................................................................................................3

1. Capital structure of companies...........................................................................................3

2. Cost of capital.....................................................................................................................6

3. Ratio Analysis....................................................................................................................8

CONCLUSION .............................................................................................................................10

REFERENCES..............................................................................................................................11

INTRODUCTION ..........................................................................................................................3

1. Capital structure of companies...........................................................................................3

2. Cost of capital.....................................................................................................................6

3. Ratio Analysis....................................................................................................................8

CONCLUSION .............................................................................................................................10

REFERENCES..............................................................................................................................11

INTRODUCTION

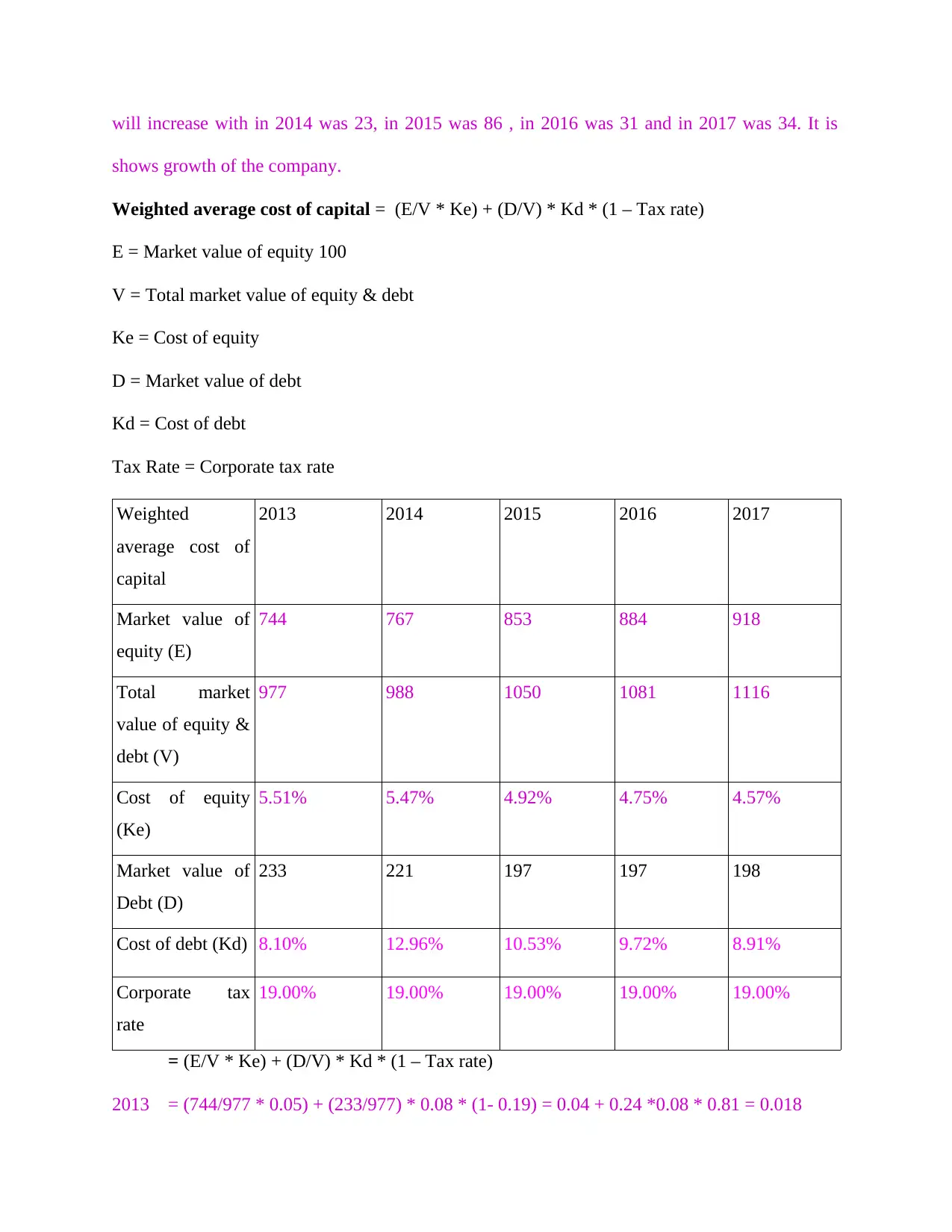

Corporate finance providing help in financial dealing with the capital structure and

source of funding (Chenhall and Moers, 2015). This reports selecting two companies are

Debenhams PLC and Marks and Spencer group PLC. Debenhams plc is a major world-wide,

multi channel trade name with a proud British attribute which trading from over 241 stores

across 22 countries. Marks and Spencer Group plc is a retailer of clothing, food and home

products in the united kingdom. This report covered these topics of selecting companies like as

capital structure, cost of capital and ratio analysis.

MAIN BODY

1. Capital structure of companies

Capital structure mention to the price of debt and equity employed by a firm to finance its

assets and fund its operations (Bertomeu, Beyer and Dye, 2011.).

CAPITAL STRUCTURE OF DEBENHAMS PLC

Capital

structure (in

million)

2013 2014 2015 2016 2017

Total Debt 394 420 350 331 313

Total Equity 744 767 853 884 918

As per the financial statement company have total debt in 2013 was 394 that are

increasing in 2014 with 26 after that in 2015 it was decreasing with 70 and in 2016 it is

continually decreasing with 19 and in 2017 was 18 due to purchase and sale out of long term and

short term debt. Total equity of the company continuous increasing in 2013 was 744 after that it

Corporate finance providing help in financial dealing with the capital structure and

source of funding (Chenhall and Moers, 2015). This reports selecting two companies are

Debenhams PLC and Marks and Spencer group PLC. Debenhams plc is a major world-wide,

multi channel trade name with a proud British attribute which trading from over 241 stores

across 22 countries. Marks and Spencer Group plc is a retailer of clothing, food and home

products in the united kingdom. This report covered these topics of selecting companies like as

capital structure, cost of capital and ratio analysis.

MAIN BODY

1. Capital structure of companies

Capital structure mention to the price of debt and equity employed by a firm to finance its

assets and fund its operations (Bertomeu, Beyer and Dye, 2011.).

CAPITAL STRUCTURE OF DEBENHAMS PLC

Capital

structure (in

million)

2013 2014 2015 2016 2017

Total Debt 394 420 350 331 313

Total Equity 744 767 853 884 918

As per the financial statement company have total debt in 2013 was 394 that are

increasing in 2014 with 26 after that in 2015 it was decreasing with 70 and in 2016 it is

continually decreasing with 19 and in 2017 was 18 due to purchase and sale out of long term and

short term debt. Total equity of the company continuous increasing in 2013 was 744 after that it

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

will increase with in 2014 was 23, in 2015 was 86 , in 2016 was 31 and in 2017 was 34. It is

shows growth of the company.

Weighted average cost of capital = (E/V * Ke) + (D/V) * Kd * (1 – Tax rate)

E = Market value of equity 100

V = Total market value of equity & debt

Ke = Cost of equity

D = Market value of debt

Kd = Cost of debt

Tax Rate = Corporate tax rate

Weighted

average cost of

capital

2013 2014 2015 2016 2017

Market value of

equity (E)

744 767 853 884 918

Total market

value of equity &

debt (V)

977 988 1050 1081 1116

Cost of equity

(Ke)

5.51% 5.47% 4.92% 4.75% 4.57%

Market value of

Debt (D)

233 221 197 197 198

Cost of debt (Kd) 8.10% 12.96% 10.53% 9.72% 8.91%

Corporate tax

rate

19.00% 19.00% 19.00% 19.00% 19.00%

= (E/V * Ke) + (D/V) * Kd * (1 – Tax rate)

2013 = (744/977 * 0.05) + (233/977) * 0.08 * (1- 0.19) = 0.04 + 0.24 *0.08 * 0.81 = 0.018

shows growth of the company.

Weighted average cost of capital = (E/V * Ke) + (D/V) * Kd * (1 – Tax rate)

E = Market value of equity 100

V = Total market value of equity & debt

Ke = Cost of equity

D = Market value of debt

Kd = Cost of debt

Tax Rate = Corporate tax rate

Weighted

average cost of

capital

2013 2014 2015 2016 2017

Market value of

equity (E)

744 767 853 884 918

Total market

value of equity &

debt (V)

977 988 1050 1081 1116

Cost of equity

(Ke)

5.51% 5.47% 4.92% 4.75% 4.57%

Market value of

Debt (D)

233 221 197 197 198

Cost of debt (Kd) 8.10% 12.96% 10.53% 9.72% 8.91%

Corporate tax

rate

19.00% 19.00% 19.00% 19.00% 19.00%

= (E/V * Ke) + (D/V) * Kd * (1 – Tax rate)

2013 = (744/977 * 0.05) + (233/977) * 0.08 * (1- 0.19) = 0.04 + 0.24 *0.08 * 0.81 = 0.018

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

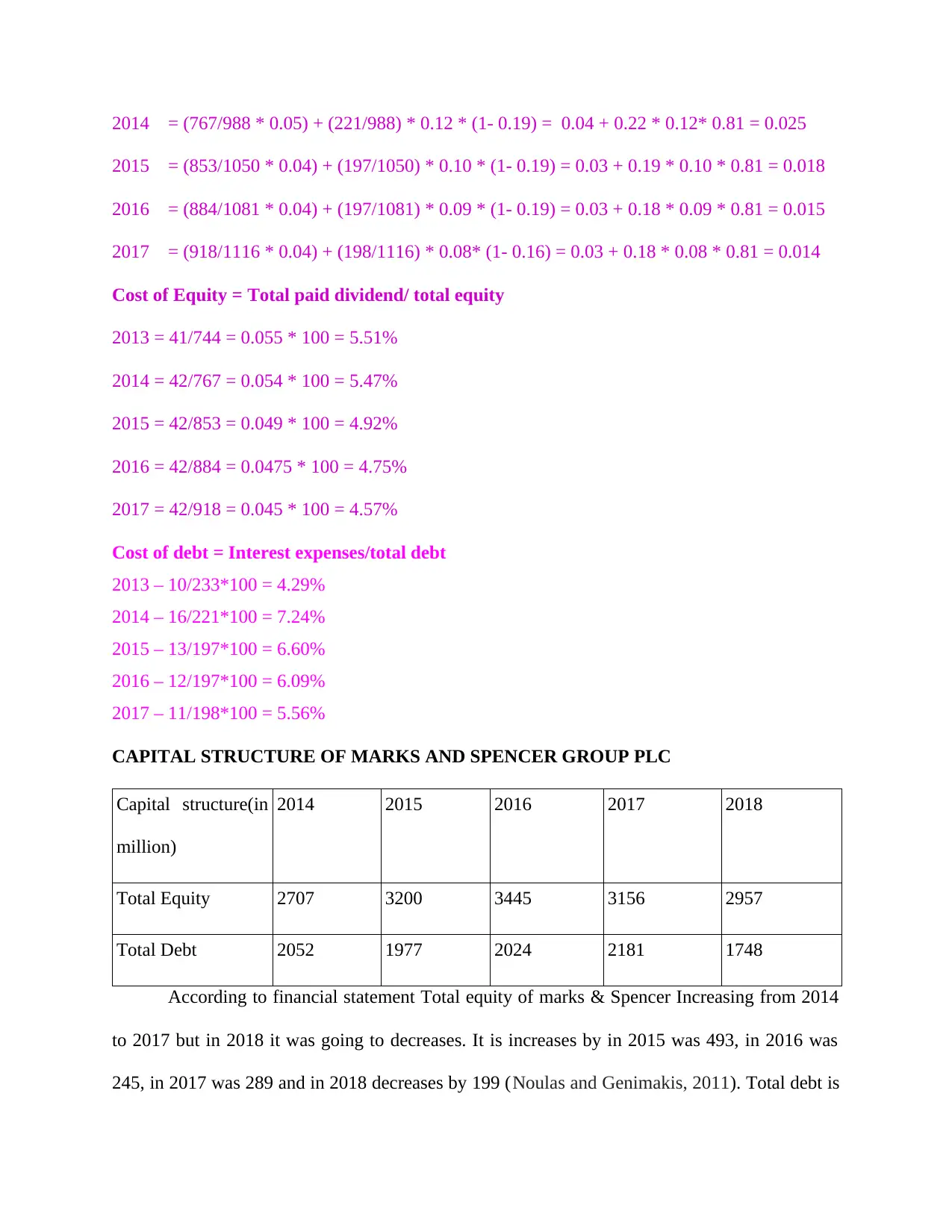

2014 = (767/988 * 0.05) + (221/988) * 0.12 * (1- 0.19) = 0.04 + 0.22 * 0.12* 0.81 = 0.025

2015 = (853/1050 * 0.04) + (197/1050) * 0.10 * (1- 0.19) = 0.03 + 0.19 * 0.10 * 0.81 = 0.018

2016 = (884/1081 * 0.04) + (197/1081) * 0.09 * (1- 0.19) = 0.03 + 0.18 * 0.09 * 0.81 = 0.015

2017 = (918/1116 * 0.04) + (198/1116) * 0.08* (1- 0.16) = 0.03 + 0.18 * 0.08 * 0.81 = 0.014

Cost of Equity = Total paid dividend/ total equity

2013 = 41/744 = 0.055 * 100 = 5.51%

2014 = 42/767 = 0.054 * 100 = 5.47%

2015 = 42/853 = 0.049 * 100 = 4.92%

2016 = 42/884 = 0.0475 * 100 = 4.75%

2017 = 42/918 = 0.045 * 100 = 4.57%

Cost of debt = Interest expenses/total debt

2013 – 10/233*100 = 4.29%

2014 – 16/221*100 = 7.24%

2015 – 13/197*100 = 6.60%

2016 – 12/197*100 = 6.09%

2017 – 11/198*100 = 5.56%

CAPITAL STRUCTURE OF MARKS AND SPENCER GROUP PLC

Capital structure(in

million)

2014 2015 2016 2017 2018

Total Equity 2707 3200 3445 3156 2957

Total Debt 2052 1977 2024 2181 1748

According to financial statement Total equity of marks & Spencer Increasing from 2014

to 2017 but in 2018 it was going to decreases. It is increases by in 2015 was 493, in 2016 was

245, in 2017 was 289 and in 2018 decreases by 199 (Noulas and Genimakis, 2011). Total debt is

2015 = (853/1050 * 0.04) + (197/1050) * 0.10 * (1- 0.19) = 0.03 + 0.19 * 0.10 * 0.81 = 0.018

2016 = (884/1081 * 0.04) + (197/1081) * 0.09 * (1- 0.19) = 0.03 + 0.18 * 0.09 * 0.81 = 0.015

2017 = (918/1116 * 0.04) + (198/1116) * 0.08* (1- 0.16) = 0.03 + 0.18 * 0.08 * 0.81 = 0.014

Cost of Equity = Total paid dividend/ total equity

2013 = 41/744 = 0.055 * 100 = 5.51%

2014 = 42/767 = 0.054 * 100 = 5.47%

2015 = 42/853 = 0.049 * 100 = 4.92%

2016 = 42/884 = 0.0475 * 100 = 4.75%

2017 = 42/918 = 0.045 * 100 = 4.57%

Cost of debt = Interest expenses/total debt

2013 – 10/233*100 = 4.29%

2014 – 16/221*100 = 7.24%

2015 – 13/197*100 = 6.60%

2016 – 12/197*100 = 6.09%

2017 – 11/198*100 = 5.56%

CAPITAL STRUCTURE OF MARKS AND SPENCER GROUP PLC

Capital structure(in

million)

2014 2015 2016 2017 2018

Total Equity 2707 3200 3445 3156 2957

Total Debt 2052 1977 2024 2181 1748

According to financial statement Total equity of marks & Spencer Increasing from 2014

to 2017 but in 2018 it was going to decreases. It is increases by in 2015 was 493, in 2016 was

245, in 2017 was 289 and in 2018 decreases by 199 (Noulas and Genimakis, 2011). Total debt is

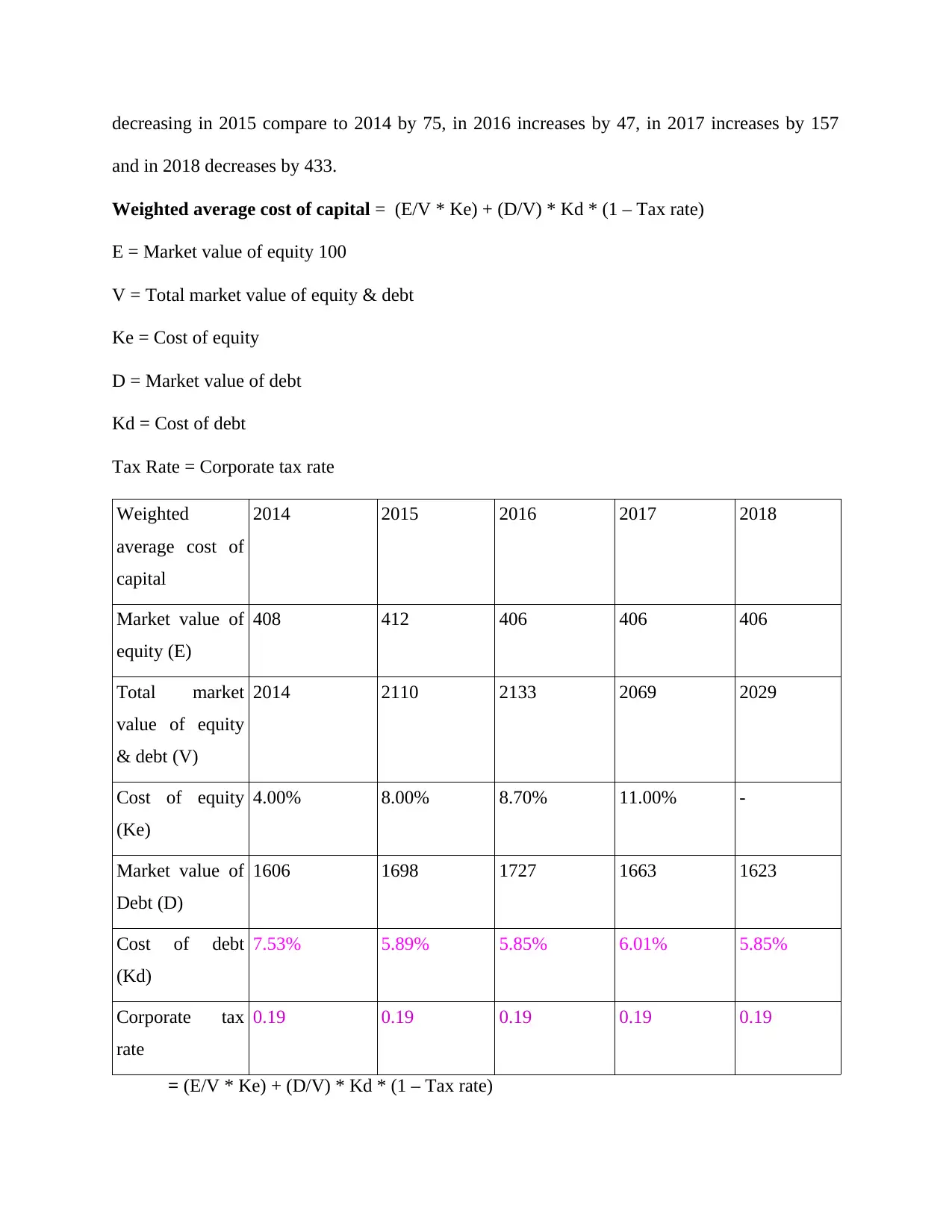

decreasing in 2015 compare to 2014 by 75, in 2016 increases by 47, in 2017 increases by 157

and in 2018 decreases by 433.

Weighted average cost of capital = (E/V * Ke) + (D/V) * Kd * (1 – Tax rate)

E = Market value of equity 100

V = Total market value of equity & debt

Ke = Cost of equity

D = Market value of debt

Kd = Cost of debt

Tax Rate = Corporate tax rate

Weighted

average cost of

capital

2014 2015 2016 2017 2018

Market value of

equity (E)

408 412 406 406 406

Total market

value of equity

& debt (V)

2014 2110 2133 2069 2029

Cost of equity

(Ke)

4.00% 8.00% 8.70% 11.00% -

Market value of

Debt (D)

1606 1698 1727 1663 1623

Cost of debt

(Kd)

7.53% 5.89% 5.85% 6.01% 5.85%

Corporate tax

rate

0.19 0.19 0.19 0.19 0.19

= (E/V * Ke) + (D/V) * Kd * (1 – Tax rate)

and in 2018 decreases by 433.

Weighted average cost of capital = (E/V * Ke) + (D/V) * Kd * (1 – Tax rate)

E = Market value of equity 100

V = Total market value of equity & debt

Ke = Cost of equity

D = Market value of debt

Kd = Cost of debt

Tax Rate = Corporate tax rate

Weighted

average cost of

capital

2014 2015 2016 2017 2018

Market value of

equity (E)

408 412 406 406 406

Total market

value of equity

& debt (V)

2014 2110 2133 2069 2029

Cost of equity

(Ke)

4.00% 8.00% 8.70% 11.00% -

Market value of

Debt (D)

1606 1698 1727 1663 1623

Cost of debt

(Kd)

7.53% 5.89% 5.85% 6.01% 5.85%

Corporate tax

rate

0.19 0.19 0.19 0.19 0.19

= (E/V * Ke) + (D/V) * Kd * (1 – Tax rate)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

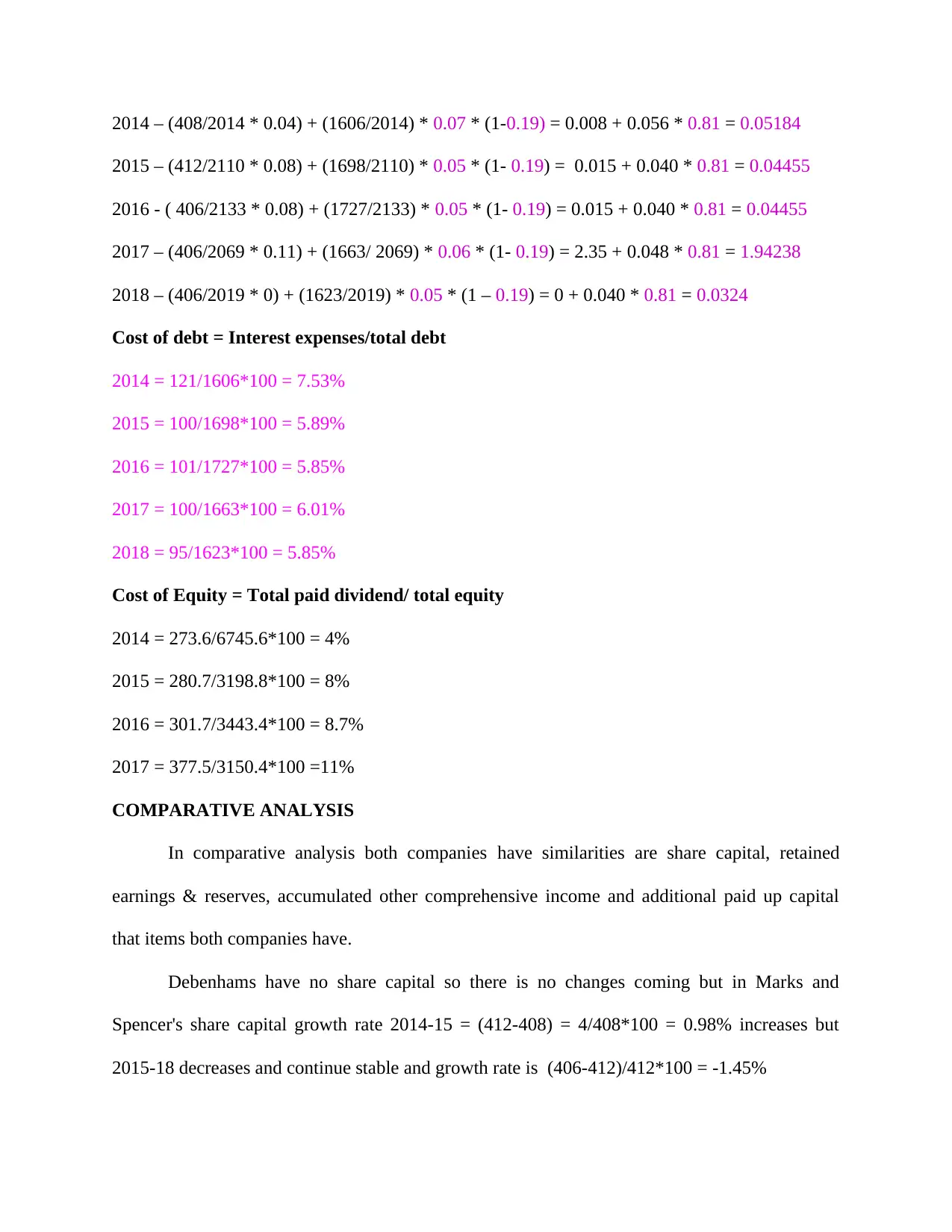

2014 – (408/2014 * 0.04) + (1606/2014) * 0.07 * (1-0.19) = 0.008 + 0.056 * 0.81 = 0.05184

2015 – (412/2110 * 0.08) + (1698/2110) * 0.05 * (1- 0.19) = 0.015 + 0.040 * 0.81 = 0.04455

2016 - ( 406/2133 * 0.08) + (1727/2133) * 0.05 * (1- 0.19) = 0.015 + 0.040 * 0.81 = 0.04455

2017 – (406/2069 * 0.11) + (1663/ 2069) * 0.06 * (1- 0.19) = 2.35 + 0.048 * 0.81 = 1.94238

2018 – (406/2019 * 0) + (1623/2019) * 0.05 * (1 – 0.19) = 0 + 0.040 * 0.81 = 0.0324

Cost of debt = Interest expenses/total debt

2014 = 121/1606*100 = 7.53%

2015 = 100/1698*100 = 5.89%

2016 = 101/1727*100 = 5.85%

2017 = 100/1663*100 = 6.01%

2018 = 95/1623*100 = 5.85%

Cost of Equity = Total paid dividend/ total equity

2014 = 273.6/6745.6*100 = 4%

2015 = 280.7/3198.8*100 = 8%

2016 = 301.7/3443.4*100 = 8.7%

2017 = 377.5/3150.4*100 =11%

COMPARATIVE ANALYSIS

In comparative analysis both companies have similarities are share capital, retained

earnings & reserves, accumulated other comprehensive income and additional paid up capital

that items both companies have.

Debenhams have no share capital so there is no changes coming but in Marks and

Spencer's share capital growth rate 2014-15 = (412-408) = 4/408*100 = 0.98% increases but

2015-18 decreases and continue stable and growth rate is (406-412)/412*100 = -1.45%

2015 – (412/2110 * 0.08) + (1698/2110) * 0.05 * (1- 0.19) = 0.015 + 0.040 * 0.81 = 0.04455

2016 - ( 406/2133 * 0.08) + (1727/2133) * 0.05 * (1- 0.19) = 0.015 + 0.040 * 0.81 = 0.04455

2017 – (406/2069 * 0.11) + (1663/ 2069) * 0.06 * (1- 0.19) = 2.35 + 0.048 * 0.81 = 1.94238

2018 – (406/2019 * 0) + (1623/2019) * 0.05 * (1 – 0.19) = 0 + 0.040 * 0.81 = 0.0324

Cost of debt = Interest expenses/total debt

2014 = 121/1606*100 = 7.53%

2015 = 100/1698*100 = 5.89%

2016 = 101/1727*100 = 5.85%

2017 = 100/1663*100 = 6.01%

2018 = 95/1623*100 = 5.85%

Cost of Equity = Total paid dividend/ total equity

2014 = 273.6/6745.6*100 = 4%

2015 = 280.7/3198.8*100 = 8%

2016 = 301.7/3443.4*100 = 8.7%

2017 = 377.5/3150.4*100 =11%

COMPARATIVE ANALYSIS

In comparative analysis both companies have similarities are share capital, retained

earnings & reserves, accumulated other comprehensive income and additional paid up capital

that items both companies have.

Debenhams have no share capital so there is no changes coming but in Marks and

Spencer's share capital growth rate 2014-15 = (412-408) = 4/408*100 = 0.98% increases but

2015-18 decreases and continue stable and growth rate is (406-412)/412*100 = -1.45%

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

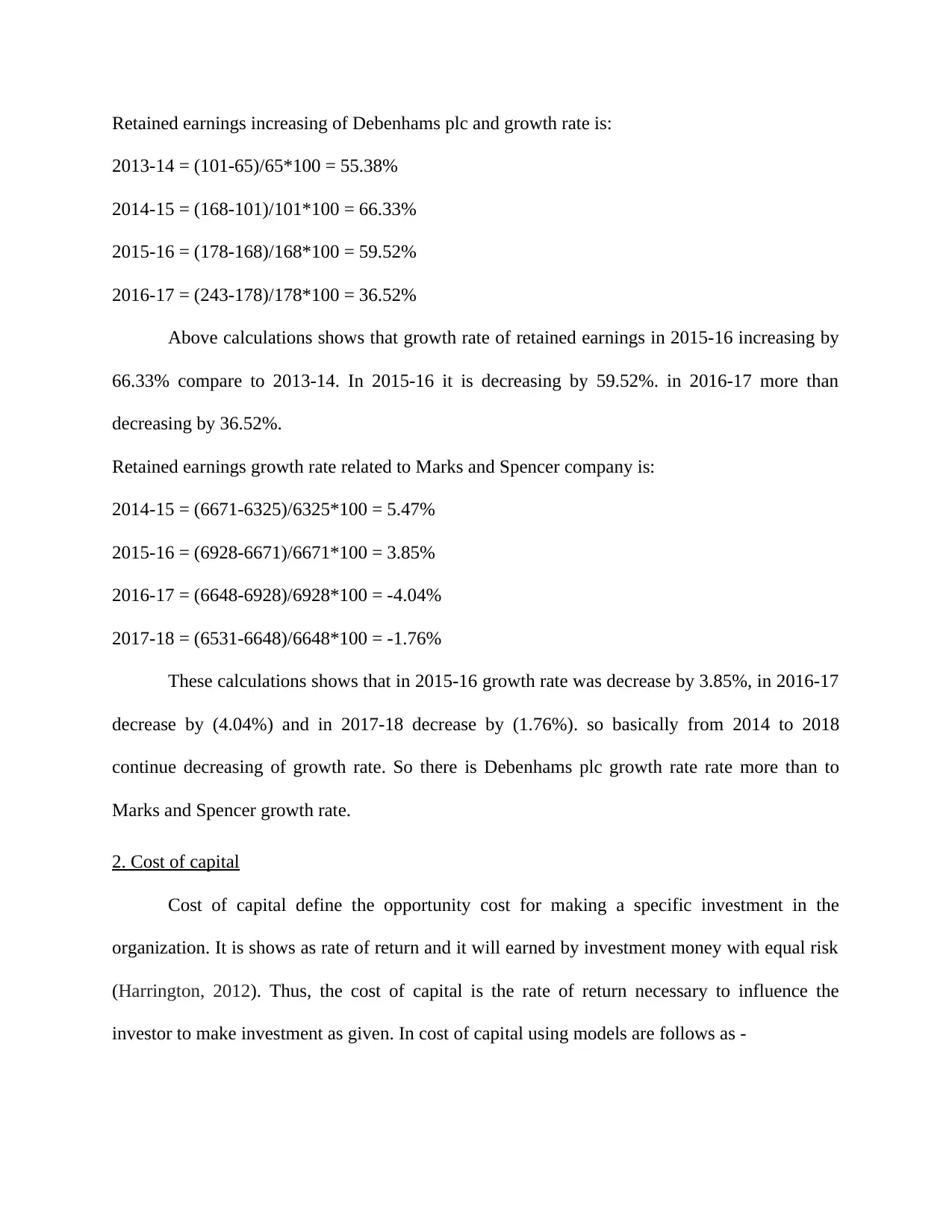

Retained earnings increasing of Debenhams plc and growth rate is:

2013-14 = (101-65)/65*100 = 55.38%

2014-15 = (168-101)/101*100 = 66.33%

2015-16 = (178-168)/168*100 = 59.52%

2016-17 = (243-178)/178*100 = 36.52%

Above calculations shows that growth rate of retained earnings in 2015-16 increasing by

66.33% compare to 2013-14. In 2015-16 it is decreasing by 59.52%. in 2016-17 more than

decreasing by 36.52%.

Retained earnings growth rate related to Marks and Spencer company is:

2014-15 = (6671-6325)/6325*100 = 5.47%

2015-16 = (6928-6671)/6671*100 = 3.85%

2016-17 = (6648-6928)/6928*100 = -4.04%

2017-18 = (6531-6648)/6648*100 = -1.76%

These calculations shows that in 2015-16 growth rate was decrease by 3.85%, in 2016-17

decrease by (4.04%) and in 2017-18 decrease by (1.76%). so basically from 2014 to 2018

continue decreasing of growth rate. So there is Debenhams plc growth rate rate more than to

Marks and Spencer growth rate.

2. Cost of capital

Cost of capital define the opportunity cost for making a specific investment in the

organization. It is shows as rate of return and it will earned by investment money with equal risk

(Harrington, 2012). Thus, the cost of capital is the rate of return necessary to influence the

investor to make investment as given. In cost of capital using models are follows as -

2013-14 = (101-65)/65*100 = 55.38%

2014-15 = (168-101)/101*100 = 66.33%

2015-16 = (178-168)/168*100 = 59.52%

2016-17 = (243-178)/178*100 = 36.52%

Above calculations shows that growth rate of retained earnings in 2015-16 increasing by

66.33% compare to 2013-14. In 2015-16 it is decreasing by 59.52%. in 2016-17 more than

decreasing by 36.52%.

Retained earnings growth rate related to Marks and Spencer company is:

2014-15 = (6671-6325)/6325*100 = 5.47%

2015-16 = (6928-6671)/6671*100 = 3.85%

2016-17 = (6648-6928)/6928*100 = -4.04%

2017-18 = (6531-6648)/6648*100 = -1.76%

These calculations shows that in 2015-16 growth rate was decrease by 3.85%, in 2016-17

decrease by (4.04%) and in 2017-18 decrease by (1.76%). so basically from 2014 to 2018

continue decreasing of growth rate. So there is Debenhams plc growth rate rate more than to

Marks and Spencer growth rate.

2. Cost of capital

Cost of capital define the opportunity cost for making a specific investment in the

organization. It is shows as rate of return and it will earned by investment money with equal risk

(Harrington, 2012). Thus, the cost of capital is the rate of return necessary to influence the

investor to make investment as given. In cost of capital using models are follows as -

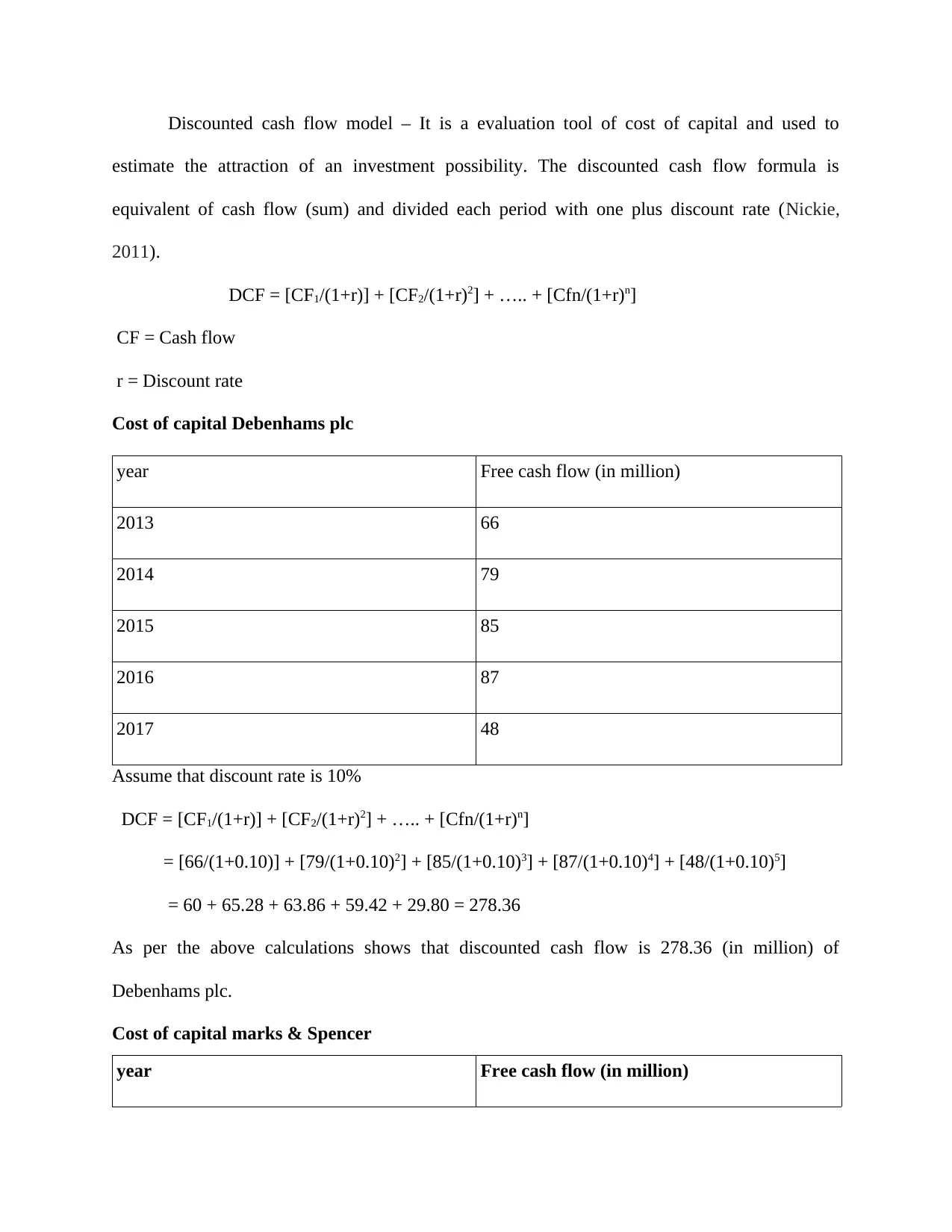

Discounted cash flow model – It is a evaluation tool of cost of capital and used to

estimate the attraction of an investment possibility. The discounted cash flow formula is

equivalent of cash flow (sum) and divided each period with one plus discount rate (Nickie,

2011).

DCF = [CF1/(1+r)] + [CF2/(1+r)2] + ….. + [Cfn/(1+r)n]

CF = Cash flow

r = Discount rate

Cost of capital Debenhams plc

year Free cash flow (in million)

2013 66

2014 79

2015 85

2016 87

2017 48

Assume that discount rate is 10%

DCF = [CF1/(1+r)] + [CF2/(1+r)2] + ….. + [Cfn/(1+r)n]

= [66/(1+0.10)] + [79/(1+0.10)2] + [85/(1+0.10)3] + [87/(1+0.10)4] + [48/(1+0.10)5]

= 60 + 65.28 + 63.86 + 59.42 + 29.80 = 278.36

As per the above calculations shows that discounted cash flow is 278.36 (in million) of

Debenhams plc.

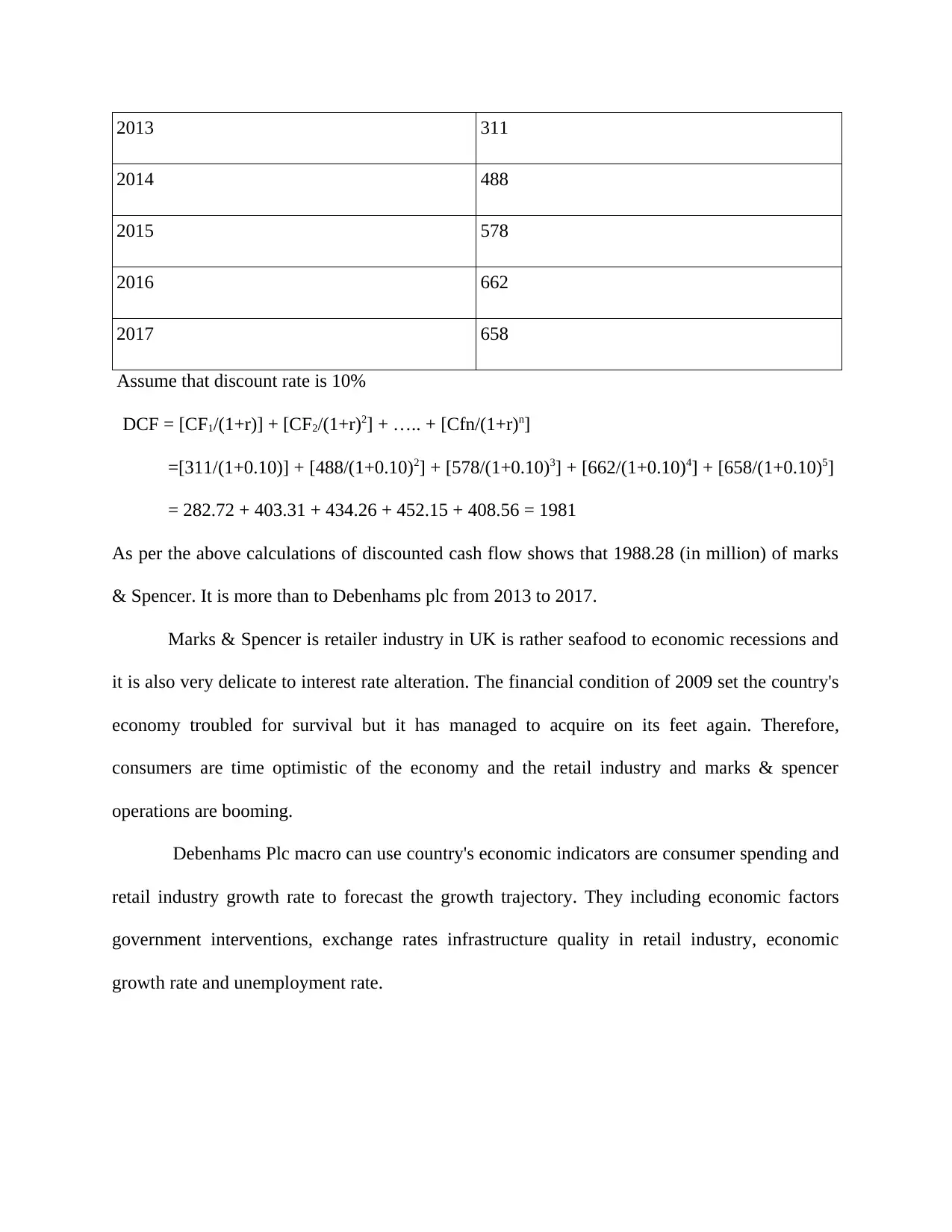

Cost of capital marks & Spencer

year Free cash flow (in million)

estimate the attraction of an investment possibility. The discounted cash flow formula is

equivalent of cash flow (sum) and divided each period with one plus discount rate (Nickie,

2011).

DCF = [CF1/(1+r)] + [CF2/(1+r)2] + ….. + [Cfn/(1+r)n]

CF = Cash flow

r = Discount rate

Cost of capital Debenhams plc

year Free cash flow (in million)

2013 66

2014 79

2015 85

2016 87

2017 48

Assume that discount rate is 10%

DCF = [CF1/(1+r)] + [CF2/(1+r)2] + ….. + [Cfn/(1+r)n]

= [66/(1+0.10)] + [79/(1+0.10)2] + [85/(1+0.10)3] + [87/(1+0.10)4] + [48/(1+0.10)5]

= 60 + 65.28 + 63.86 + 59.42 + 29.80 = 278.36

As per the above calculations shows that discounted cash flow is 278.36 (in million) of

Debenhams plc.

Cost of capital marks & Spencer

year Free cash flow (in million)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

2013 311

2014 488

2015 578

2016 662

2017 658

Assume that discount rate is 10%

DCF = [CF1/(1+r)] + [CF2/(1+r)2] + ….. + [Cfn/(1+r)n]

=[311/(1+0.10)] + [488/(1+0.10)2] + [578/(1+0.10)3] + [662/(1+0.10)4] + [658/(1+0.10)5]

= 282.72 + 403.31 + 434.26 + 452.15 + 408.56 = 1981

As per the above calculations of discounted cash flow shows that 1988.28 (in million) of marks

& Spencer. It is more than to Debenhams plc from 2013 to 2017.

Marks & Spencer is retailer industry in UK is rather seafood to economic recessions and

it is also very delicate to interest rate alteration. The financial condition of 2009 set the country's

economy troubled for survival but it has managed to acquire on its feet again. Therefore,

consumers are time optimistic of the economy and the retail industry and marks & spencer

operations are booming.

Debenhams Plc macro can use country's economic indicators are consumer spending and

retail industry growth rate to forecast the growth trajectory. They including economic factors

government interventions, exchange rates infrastructure quality in retail industry, economic

growth rate and unemployment rate.

2014 488

2015 578

2016 662

2017 658

Assume that discount rate is 10%

DCF = [CF1/(1+r)] + [CF2/(1+r)2] + ….. + [Cfn/(1+r)n]

=[311/(1+0.10)] + [488/(1+0.10)2] + [578/(1+0.10)3] + [662/(1+0.10)4] + [658/(1+0.10)5]

= 282.72 + 403.31 + 434.26 + 452.15 + 408.56 = 1981

As per the above calculations of discounted cash flow shows that 1988.28 (in million) of marks

& Spencer. It is more than to Debenhams plc from 2013 to 2017.

Marks & Spencer is retailer industry in UK is rather seafood to economic recessions and

it is also very delicate to interest rate alteration. The financial condition of 2009 set the country's

economy troubled for survival but it has managed to acquire on its feet again. Therefore,

consumers are time optimistic of the economy and the retail industry and marks & spencer

operations are booming.

Debenhams Plc macro can use country's economic indicators are consumer spending and

retail industry growth rate to forecast the growth trajectory. They including economic factors

government interventions, exchange rates infrastructure quality in retail industry, economic

growth rate and unemployment rate.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

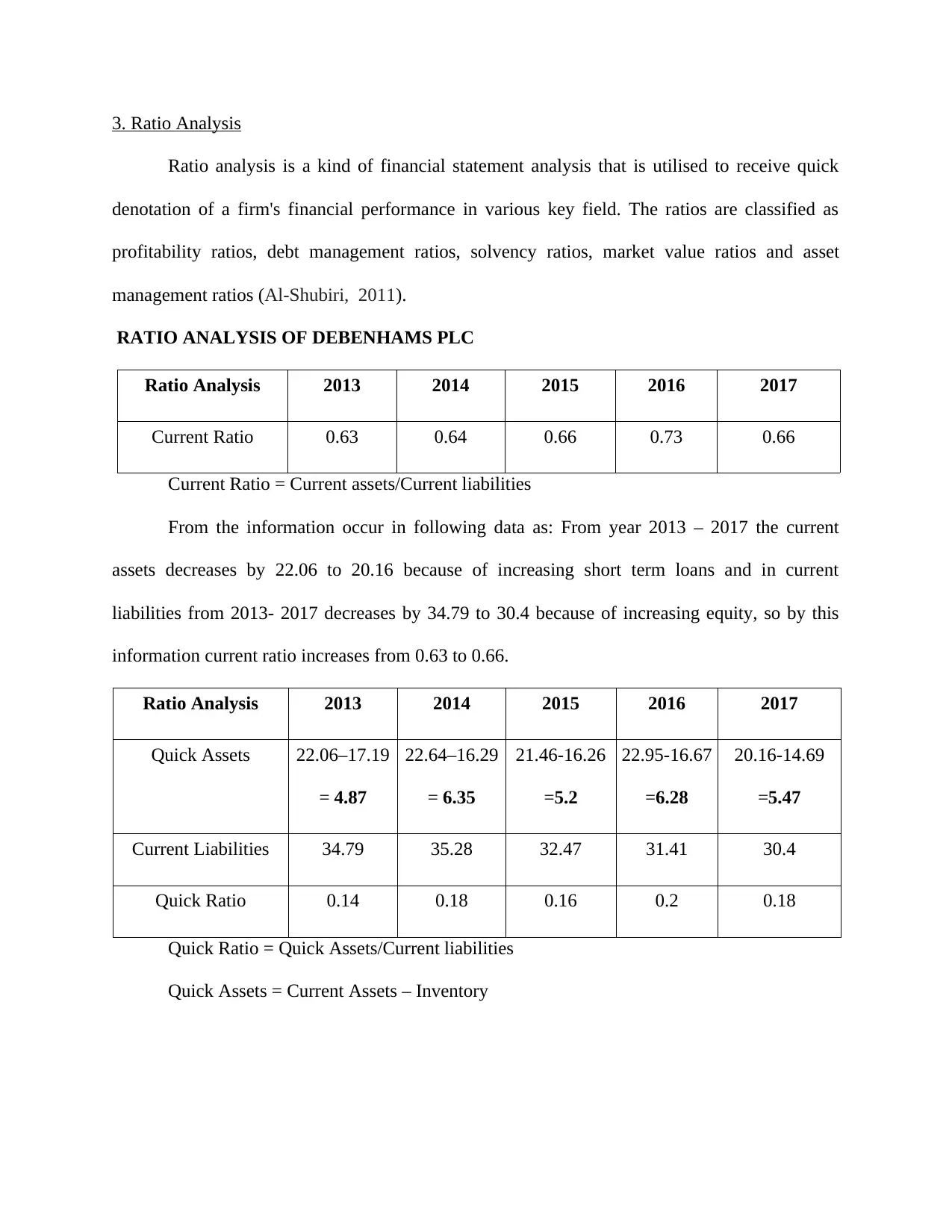

3. Ratio Analysis

Ratio analysis is a kind of financial statement analysis that is utilised to receive quick

denotation of a firm's financial performance in various key field. The ratios are classified as

profitability ratios, debt management ratios, solvency ratios, market value ratios and asset

management ratios (Al-Shubiri, 2011).

RATIO ANALYSIS OF DEBENHAMS PLC

Ratio Analysis 2013 2014 2015 2016 2017

Current Ratio 0.63 0.64 0.66 0.73 0.66

Current Ratio = Current assets/Current liabilities

From the information occur in following data as: From year 2013 – 2017 the current

assets decreases by 22.06 to 20.16 because of increasing short term loans and in current

liabilities from 2013- 2017 decreases by 34.79 to 30.4 because of increasing equity, so by this

information current ratio increases from 0.63 to 0.66.

Ratio Analysis 2013 2014 2015 2016 2017

Quick Assets 22.06–17.19

= 4.87

22.64–16.29

= 6.35

21.46-16.26

=5.2

22.95-16.67

=6.28

20.16-14.69

=5.47

Current Liabilities 34.79 35.28 32.47 31.41 30.4

Quick Ratio 0.14 0.18 0.16 0.2 0.18

Quick Ratio = Quick Assets/Current liabilities

Quick Assets = Current Assets – Inventory

Ratio analysis is a kind of financial statement analysis that is utilised to receive quick

denotation of a firm's financial performance in various key field. The ratios are classified as

profitability ratios, debt management ratios, solvency ratios, market value ratios and asset

management ratios (Al-Shubiri, 2011).

RATIO ANALYSIS OF DEBENHAMS PLC

Ratio Analysis 2013 2014 2015 2016 2017

Current Ratio 0.63 0.64 0.66 0.73 0.66

Current Ratio = Current assets/Current liabilities

From the information occur in following data as: From year 2013 – 2017 the current

assets decreases by 22.06 to 20.16 because of increasing short term loans and in current

liabilities from 2013- 2017 decreases by 34.79 to 30.4 because of increasing equity, so by this

information current ratio increases from 0.63 to 0.66.

Ratio Analysis 2013 2014 2015 2016 2017

Quick Assets 22.06–17.19

= 4.87

22.64–16.29

= 6.35

21.46-16.26

=5.2

22.95-16.67

=6.28

20.16-14.69

=5.47

Current Liabilities 34.79 35.28 32.47 31.41 30.4

Quick Ratio 0.14 0.18 0.16 0.2 0.18

Quick Ratio = Quick Assets/Current liabilities

Quick Assets = Current Assets – Inventory

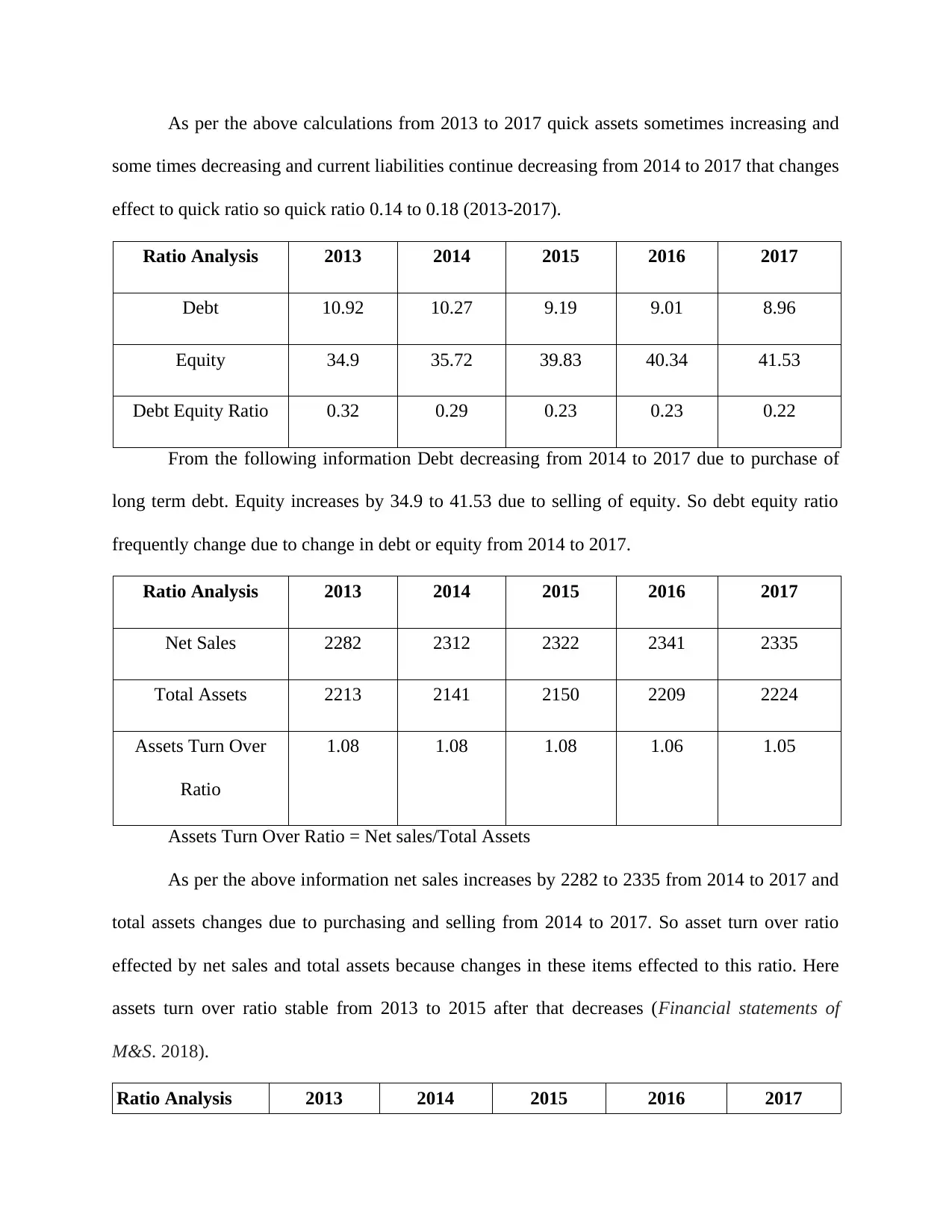

As per the above calculations from 2013 to 2017 quick assets sometimes increasing and

some times decreasing and current liabilities continue decreasing from 2014 to 2017 that changes

effect to quick ratio so quick ratio 0.14 to 0.18 (2013-2017).

Ratio Analysis 2013 2014 2015 2016 2017

Debt 10.92 10.27 9.19 9.01 8.96

Equity 34.9 35.72 39.83 40.34 41.53

Debt Equity Ratio 0.32 0.29 0.23 0.23 0.22

From the following information Debt decreasing from 2014 to 2017 due to purchase of

long term debt. Equity increases by 34.9 to 41.53 due to selling of equity. So debt equity ratio

frequently change due to change in debt or equity from 2014 to 2017.

Ratio Analysis 2013 2014 2015 2016 2017

Net Sales 2282 2312 2322 2341 2335

Total Assets 2213 2141 2150 2209 2224

Assets Turn Over

Ratio

1.08 1.08 1.08 1.06 1.05

Assets Turn Over Ratio = Net sales/Total Assets

As per the above information net sales increases by 2282 to 2335 from 2014 to 2017 and

total assets changes due to purchasing and selling from 2014 to 2017. So asset turn over ratio

effected by net sales and total assets because changes in these items effected to this ratio. Here

assets turn over ratio stable from 2013 to 2015 after that decreases (Financial statements of

M&S. 2018).

Ratio Analysis 2013 2014 2015 2016 2017

some times decreasing and current liabilities continue decreasing from 2014 to 2017 that changes

effect to quick ratio so quick ratio 0.14 to 0.18 (2013-2017).

Ratio Analysis 2013 2014 2015 2016 2017

Debt 10.92 10.27 9.19 9.01 8.96

Equity 34.9 35.72 39.83 40.34 41.53

Debt Equity Ratio 0.32 0.29 0.23 0.23 0.22

From the following information Debt decreasing from 2014 to 2017 due to purchase of

long term debt. Equity increases by 34.9 to 41.53 due to selling of equity. So debt equity ratio

frequently change due to change in debt or equity from 2014 to 2017.

Ratio Analysis 2013 2014 2015 2016 2017

Net Sales 2282 2312 2322 2341 2335

Total Assets 2213 2141 2150 2209 2224

Assets Turn Over

Ratio

1.08 1.08 1.08 1.06 1.05

Assets Turn Over Ratio = Net sales/Total Assets

As per the above information net sales increases by 2282 to 2335 from 2014 to 2017 and

total assets changes due to purchasing and selling from 2014 to 2017. So asset turn over ratio

effected by net sales and total assets because changes in these items effected to this ratio. Here

assets turn over ratio stable from 2013 to 2015 after that decreases (Financial statements of

M&S. 2018).

Ratio Analysis 2013 2014 2015 2016 2017

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.