DIPL Audit Assurance: Financial Statement Analysis & Compliance

VerifiedAdded on 2020/02/24

|10

|1718

|44

Report

AI Summary

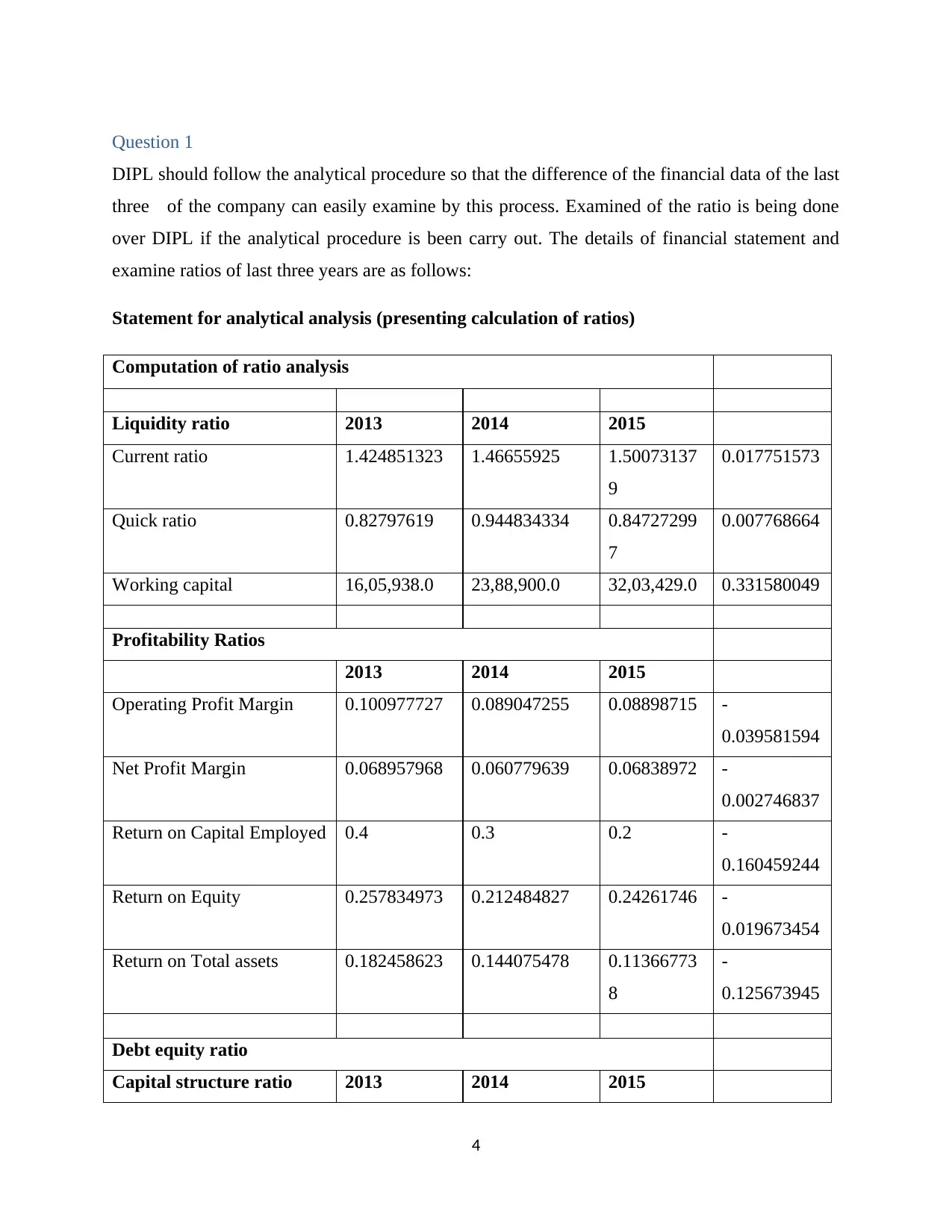

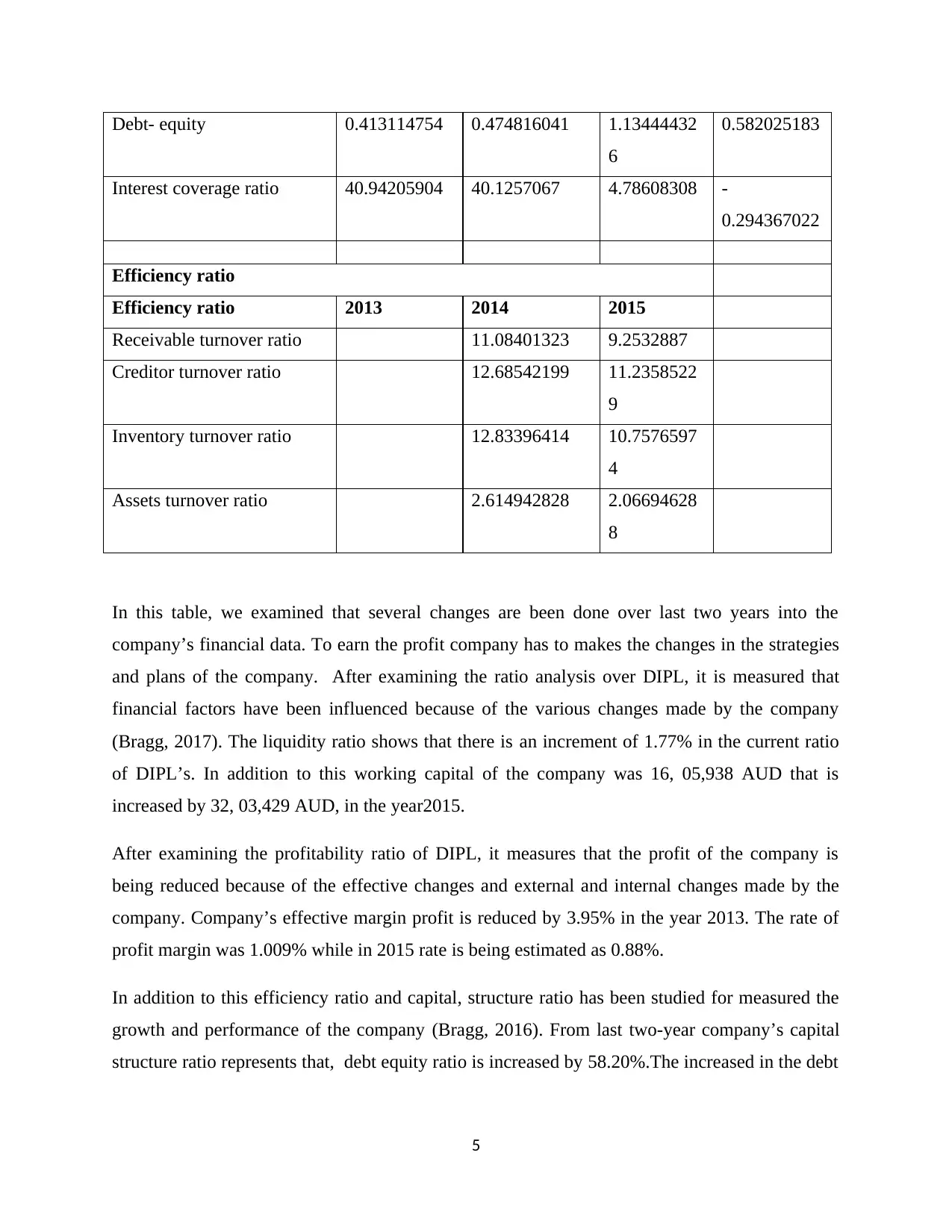

This report provides an audit assurance and compliance analysis of Double Ink Printers Limited (DIPL), an Australian printing company. It examines the company's financial statements, performs ratio analysis for the years 2013-2015, and identifies potential inherent risk factors. The analysis covers liquidity, profitability, capital structure, and efficiency ratios, revealing changes in the company's financial data and strategies. The report also discusses intentional misstatements and compliance with international and domestic reporting standards. Key fraud risk factors, such as changes in interest amounts and debt-to-equity ratios, are identified, emphasizing the auditors' responsibility to evaluate inaccuracies and potential fraud. The conclusion suggests that DIPL may have engaged in unethical activities and accounting irregularities to minimize tax liabilities and impress investors, leading to inherent risks.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.