Auditing and Compliance Report: Financial Analysis of DIPL Ltd

VerifiedAdded on 2020/03/07

|11

|2816

|20

Report

AI Summary

This report provides an in-depth analysis of auditing procedures, financial ratios, and risk assessment for DIPL Ltd. It examines substantive procedures, trend and ratio analysis to evaluate the company's financial performance over a three-year period, highlighting liquidity, profitability, and asset turnover. The report identifies inherent risks related to cash receipts, bad debts, inventory, and accounts receivables, emphasizing the impact of ineffective internal controls and a new IT system. Furthermore, it explores fraud risks stemming from accounting system flaws and improper internal mechanisms, discussing the auditor's role in mitigating these risks. The report emphasizes the importance of effective bank reconciliation, management scrutiny, and the auditor's understanding of the IT system to ensure accurate financial reporting and informed decision-making. The report also stresses the impact of management's involvement in fraudulent activities and its effect on the auditor's decision.

AUDIT & COMPLIANCE

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Auditing

Answer to 1

Substantive procedures are those activities that are performed by an auditor during the

substantive stage of an audit wherein evidence is collected in order to fulfill the completeness

and efficacy of account balances and other transactions (Ghandar & Tsahuridu, 2016). In simple

words, with the assistance of such procedure, organizations gain an ability to analyze and

anticipate the future strategies. Furthermore, organizations can easily utilize such collected

evidence in order to terminate material misstatements from their financial statements.

Nevertheless, it is very significant for an auditor to make use of such processes in order to bring

effectiveness upon the organization. In relation to this, the auditor must utilize his

professionalism and experience to anticipate future course of action (Elder et. al, 2010). All these

concerns make the relevance of substantive procedures more effective to the auditor.

In the case of DIPL ltd, the following analytical process can be taken into account. In the first

stage, trend analysis can be implemented to observe variations in the figures of corresponding

items incorporated in the financial statements over a period. However, in order to conduct trend

analysis in order to anticipate future aspects, experience, and enhanced judgement is very

necessary. Such analytical process can be easily implemented in a company and the identified

trends can be utilized in order to obtain assistance in the decision-making process (Gilbert et. al,

2005). The next analytical process relates to ratio analysis wherein the financial performance of a

company can be highlighted and a comparison can be made between the ratios of different

companies or years. Nevertheless, effective testing, control measures, and analysis can also serve

as a significant analytical process in the decision-making process.

The best way to comment on the financial performance is to perform ratio analysis that will shed

light on the performance as per various parameters. It enables to compare the performance of

various years.

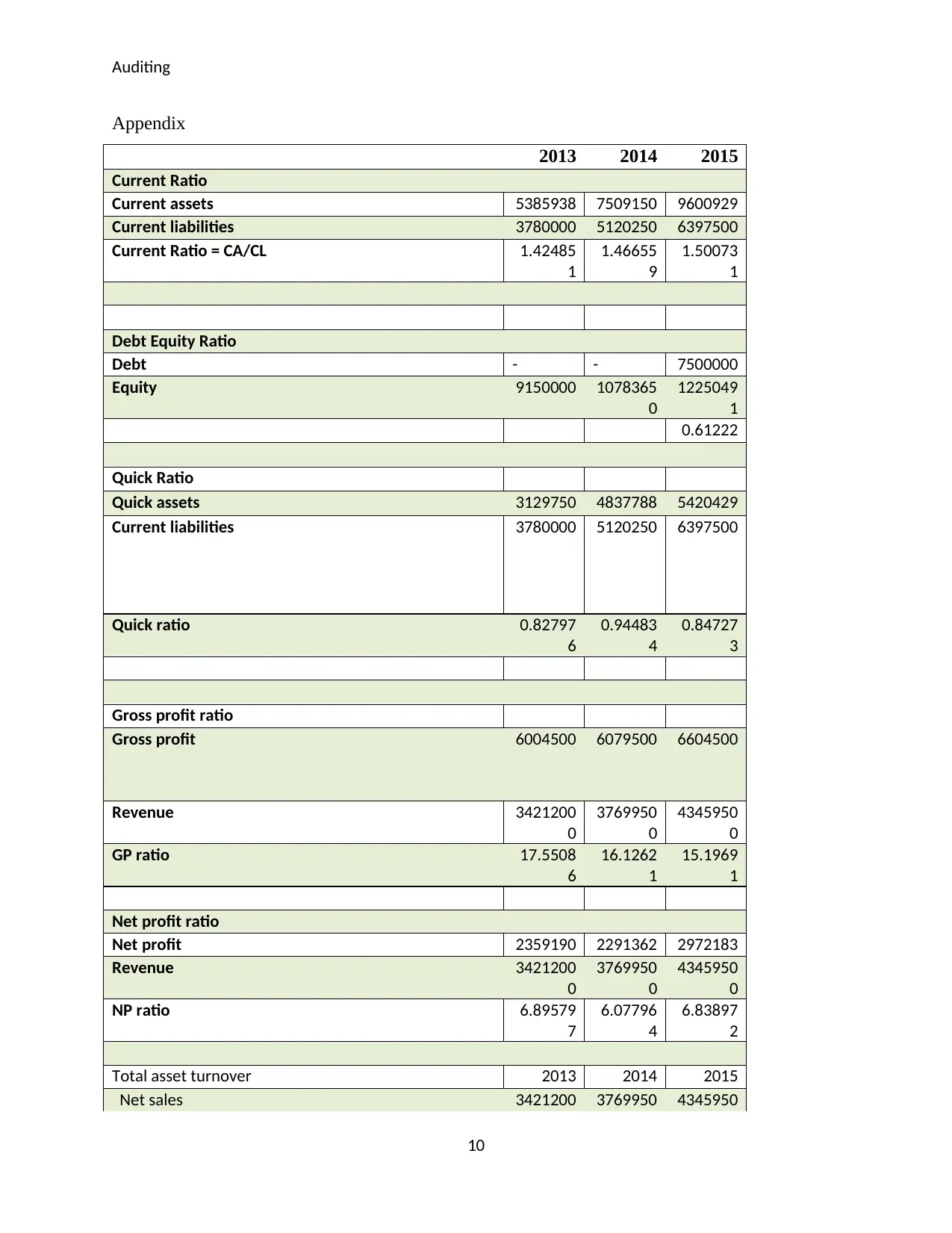

Ratio 2013 2014 2015

Current Ratio 1.424 1.466 1.500

Net Profit Ratio 6.895 6.077 6.838

Debt-Equity Ratio Nil Nil 0.612

Gross Profit Ratio 17.550 16.126 15.196

2

Answer to 1

Substantive procedures are those activities that are performed by an auditor during the

substantive stage of an audit wherein evidence is collected in order to fulfill the completeness

and efficacy of account balances and other transactions (Ghandar & Tsahuridu, 2016). In simple

words, with the assistance of such procedure, organizations gain an ability to analyze and

anticipate the future strategies. Furthermore, organizations can easily utilize such collected

evidence in order to terminate material misstatements from their financial statements.

Nevertheless, it is very significant for an auditor to make use of such processes in order to bring

effectiveness upon the organization. In relation to this, the auditor must utilize his

professionalism and experience to anticipate future course of action (Elder et. al, 2010). All these

concerns make the relevance of substantive procedures more effective to the auditor.

In the case of DIPL ltd, the following analytical process can be taken into account. In the first

stage, trend analysis can be implemented to observe variations in the figures of corresponding

items incorporated in the financial statements over a period. However, in order to conduct trend

analysis in order to anticipate future aspects, experience, and enhanced judgement is very

necessary. Such analytical process can be easily implemented in a company and the identified

trends can be utilized in order to obtain assistance in the decision-making process (Gilbert et. al,

2005). The next analytical process relates to ratio analysis wherein the financial performance of a

company can be highlighted and a comparison can be made between the ratios of different

companies or years. Nevertheless, effective testing, control measures, and analysis can also serve

as a significant analytical process in the decision-making process.

The best way to comment on the financial performance is to perform ratio analysis that will shed

light on the performance as per various parameters. It enables to compare the performance of

various years.

Ratio 2013 2014 2015

Current Ratio 1.424 1.466 1.500

Net Profit Ratio 6.895 6.077 6.838

Debt-Equity Ratio Nil Nil 0.612

Gross Profit Ratio 17.550 16.126 15.196

2

Auditing

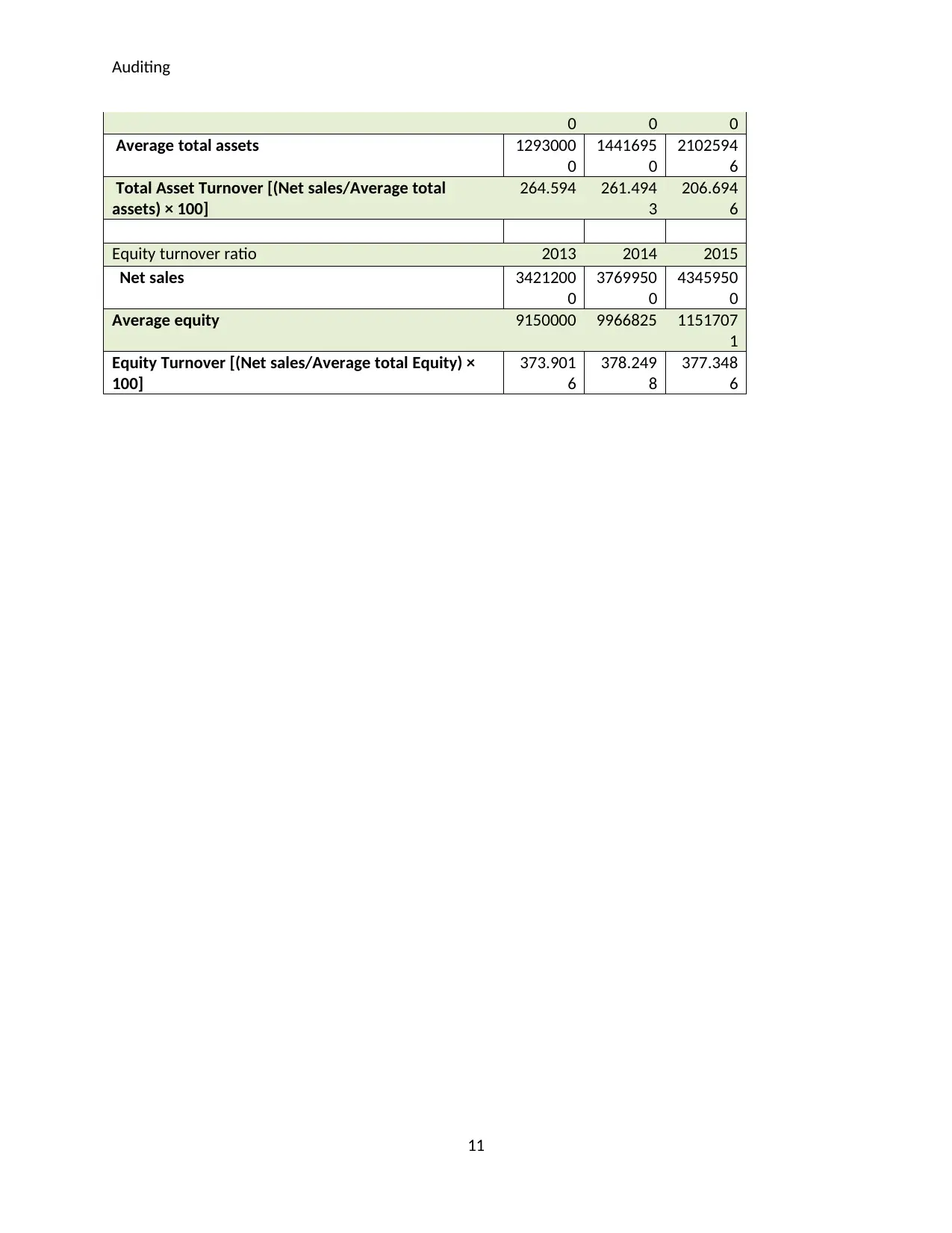

Total Asset Turnover 264.594 261.4943 206.6946

The aforesaid ratio analysis depicts that DIPL has been effective in its operations. This can be

proved by the fact that the current ratio of DIPL is consistently below two that shows nil

problems in relation to liquidity. In simple words, this means that the company can easily pay off

its debt obligations within a specified time (Brealey et. al, 2014). Further, the net profit ratio

shows a consistent track record in each of the three years, which means that the company is

capable in transforming its revenue into gains. Similarly, the debt-equity ratio of 0.612 in the

year 2015 can be attributed to the fact that the company had borrowed interest-bearing liabilities

in that year. However, for the debt-equity ratio to be effective, it must be an admixture of both

debt and equity, but in this case, only debt forms part of the ratio. In contrast to this, the gross

profit ratio of the company has witnessed a decline over the three-year period. This decline

depicts that the company is facing issues associated with its profitability and therefore, it must

carve out ways to get rid of such issues (Brigs, 2013). Further, the total asset turnover indicates

that the company has utilized the assets in an effective manner and that is evident from a strong

asset turnover ratio.

In association with the above-mentioned evaluation of the ratios of DIPL Ltd, there are few

significant concerns that must be highlighted. First, the decline in cash balances of the company

over the years clearly gives rise to the fact that the company is not in a very good position in

terms of liquidity. Second is the enhancement of bad debts over the three-year period that is a

very bad indicator in terms of both profitability and liquidity. Further, the figures of stock in the

financials of the company depict a dubious situation because it can be seen that the inventories

have significantly increased over the years (Brigs, 2013). In addition, it can be observed from the

accounts receivables of the company that it has also enhanced significantly, which portrays that

huge resources are being blocked in the same. In relation to this, it must be taken into account

that blockage of funds within a company is a very negative aspect for future aspects because it

cannot only hamper the working capital requirements but also affect the entire business as a

3

Total Asset Turnover 264.594 261.4943 206.6946

The aforesaid ratio analysis depicts that DIPL has been effective in its operations. This can be

proved by the fact that the current ratio of DIPL is consistently below two that shows nil

problems in relation to liquidity. In simple words, this means that the company can easily pay off

its debt obligations within a specified time (Brealey et. al, 2014). Further, the net profit ratio

shows a consistent track record in each of the three years, which means that the company is

capable in transforming its revenue into gains. Similarly, the debt-equity ratio of 0.612 in the

year 2015 can be attributed to the fact that the company had borrowed interest-bearing liabilities

in that year. However, for the debt-equity ratio to be effective, it must be an admixture of both

debt and equity, but in this case, only debt forms part of the ratio. In contrast to this, the gross

profit ratio of the company has witnessed a decline over the three-year period. This decline

depicts that the company is facing issues associated with its profitability and therefore, it must

carve out ways to get rid of such issues (Brigs, 2013). Further, the total asset turnover indicates

that the company has utilized the assets in an effective manner and that is evident from a strong

asset turnover ratio.

In association with the above-mentioned evaluation of the ratios of DIPL Ltd, there are few

significant concerns that must be highlighted. First, the decline in cash balances of the company

over the years clearly gives rise to the fact that the company is not in a very good position in

terms of liquidity. Second is the enhancement of bad debts over the three-year period that is a

very bad indicator in terms of both profitability and liquidity. Further, the figures of stock in the

financials of the company depict a dubious situation because it can be seen that the inventories

have significantly increased over the years (Brigs, 2013). In addition, it can be observed from the

accounts receivables of the company that it has also enhanced significantly, which portrays that

huge resources are being blocked in the same. In relation to this, it must be taken into account

that blockage of funds within a company is a very negative aspect for future aspects because it

cannot only hamper the working capital requirements but also affect the entire business as a

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Auditing

whole. On a whole, all these scenarios must be taken into consideration as soon as possible so

that future complexities can be mitigated.

Answer to 2

There are few inherent risks accommodated in the financials of DIPL Ltd that can pose a big

threat to its performance in the long-term. Such inherent risks occur due to omission or errors

forming part of the financials of the company. Moreover, owing to ineffective internal control

measures, such risks hamper the company’s affairs in a very negative way, thereby putting its

goodwill at stake. The inherent risks forming part of the financials of DIPL are as follows:

The cashier records every receipt obtained from the debtors on a regular basis but the

problem in this scenario is the recognition of such receipts that is done through mailing

facilities. In other words, the cashier records the receipt from the mail obtained from

debtors wherein the cheques are encompassed. Besides, the policy of recording receipts is

conducted in such a way that it has no interconnection with adjustment of accounts

receivables and encashment of cheque (Messier, 2013). On a whole, this strategy will

play a significant role in establishing big differences. Further, another accountant

undertakes the job of reconciling the bank statement at the end of every month that shows

ineffectiveness on the company’s part in the adoption of a systematic method. Therefore,

if the company conducts such strategy, it will result in major complications because of

the emergence of inaccuracies in the financial statements. Moreover, the auditors will

also be diverted due to such ineffectiveness as they rely on the company’s financials to

conduct the audit process and if such financials contain any grave mistakes (unintentional

or intentional), then such errors if not discovered by the auditor will be depicted in the

auditor’s report too (Geoffrey et. al, 2016).

DIPL Ltd has undertaken a task of installing a new information technology system in its

system so that every transaction can be easily recorded with ease. However, the company

has not taken into consideration prior analysis and staff control before the installation of

such new system. In simple words, lack of ample staff and qualities among them to

become accustomed to the new system is vital for effective functioning. Moreover, it can

also be viewed that the installation was not investigated properly, thereby resulting into

immense complexities for the company (Goodstein, 2011). This can be proved by the fact

4

whole. On a whole, all these scenarios must be taken into consideration as soon as possible so

that future complexities can be mitigated.

Answer to 2

There are few inherent risks accommodated in the financials of DIPL Ltd that can pose a big

threat to its performance in the long-term. Such inherent risks occur due to omission or errors

forming part of the financials of the company. Moreover, owing to ineffective internal control

measures, such risks hamper the company’s affairs in a very negative way, thereby putting its

goodwill at stake. The inherent risks forming part of the financials of DIPL are as follows:

The cashier records every receipt obtained from the debtors on a regular basis but the

problem in this scenario is the recognition of such receipts that is done through mailing

facilities. In other words, the cashier records the receipt from the mail obtained from

debtors wherein the cheques are encompassed. Besides, the policy of recording receipts is

conducted in such a way that it has no interconnection with adjustment of accounts

receivables and encashment of cheque (Messier, 2013). On a whole, this strategy will

play a significant role in establishing big differences. Further, another accountant

undertakes the job of reconciling the bank statement at the end of every month that shows

ineffectiveness on the company’s part in the adoption of a systematic method. Therefore,

if the company conducts such strategy, it will result in major complications because of

the emergence of inaccuracies in the financial statements. Moreover, the auditors will

also be diverted due to such ineffectiveness as they rely on the company’s financials to

conduct the audit process and if such financials contain any grave mistakes (unintentional

or intentional), then such errors if not discovered by the auditor will be depicted in the

auditor’s report too (Geoffrey et. al, 2016).

DIPL Ltd has undertaken a task of installing a new information technology system in its

system so that every transaction can be easily recorded with ease. However, the company

has not taken into consideration prior analysis and staff control before the installation of

such new system. In simple words, lack of ample staff and qualities among them to

become accustomed to the new system is vital for effective functioning. Moreover, it can

also be viewed that the installation was not investigated properly, thereby resulting into

immense complexities for the company (Goodstein, 2011). This can be proved by the fact

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Auditing

that initial examinations were conducted during the installation period but the

transactions were not properly apportioned to their actual period. As a result, the income

figures of the company depicted lesser amount (Zhang et. al, 2007). On a whole, due to a

misstatement in the company’s financials and flaws in the accounting system, the

accountants gained an undue advantage to manipulate the figures for their personal

causes. This can be proved by the fact that the officials and other staff of the company

were already aware of such a situation and this clearly could have granted them an

opportunity to take advantage of the same (Wright et. al, 2012). On a whole, the

implementation of the new accounting software plays a key role in generating inherent

risks for the company, thereby resulting into immoral measures and vast variations in the

entire business.

From the above-mentioned risks, it can be concluded that material misstatements can easily incur

in the company’s financials because such risks can persuade the decision-making ability. Thus,

proper internal control measures and effective IT system is the need of the hour in such a

scenario.

5

that initial examinations were conducted during the installation period but the

transactions were not properly apportioned to their actual period. As a result, the income

figures of the company depicted lesser amount (Zhang et. al, 2007). On a whole, due to a

misstatement in the company’s financials and flaws in the accounting system, the

accountants gained an undue advantage to manipulate the figures for their personal

causes. This can be proved by the fact that the officials and other staff of the company

were already aware of such a situation and this clearly could have granted them an

opportunity to take advantage of the same (Wright et. al, 2012). On a whole, the

implementation of the new accounting software plays a key role in generating inherent

risks for the company, thereby resulting into immoral measures and vast variations in the

entire business.

From the above-mentioned risks, it can be concluded that material misstatements can easily incur

in the company’s financials because such risks can persuade the decision-making ability. Thus,

proper internal control measures and effective IT system is the need of the hour in such a

scenario.

5

Auditing

Answer to 3(a)

There are two types of fraud risks owing to the business nature of DIPL Ltd:

Due to an improper examination of the new IT system, inaccurate details were

incorporated into the system, thereby resulting in inappropriate accounting figures in the

financial statements. Therefore, the biggest fraud risk in such a case is that of hampering

the account balances. Moreover, because of such improper measures, accountants can

easily gain an advantage to influence the account balances in a way that they never are

caught (Douglas et. al, 2015). For example, it may happen that the accountants write off

some outstanding amounts and settle them outside for self-interest benefits. On a whole,

the new IT system can result in a grave scenario because of inefficacies in recording the

data.

Since the company records its receipts through mailing facilities, it can encounter severe

complications because bank certification is missing in such scenario, thereby resulting in

fraudulent practices on the part of accountants. In relation to such a situation, it is very

significant that prior and effective verification is done with the bank with the help of a

bank statement so that the accountants can easily refer any amount that necessitates

authentication (Jubb, 2012). Further, it can also be observed that the company has been

conducting immoral internal control mechanisms within its affairs. As a result, it may

happen that such accountants transfer the resources of the company to a wrong person

and take advantage of the same funds for personal causes (Douglas et. al, 2015). Hence,

this cannot only affect the financial position of DIPL but also its resources as a whole. On

a whole, an effective bank reconciliation system has become the need of the hour in such

scenario. In addition, it is the responsibility of the management to carefully scrutinize

every detail forming part of the financial statements of the company on a regular basis so

that a stronger connection can be established, thereby ultimately resulting into enhanced

transparency.

Answer to 3(b)

The decision of auditor may fail to prove effective if the management is also indulged in

conducting such fraudulent steps. The key reason behind such ideology can be attributed to the

6

Answer to 3(a)

There are two types of fraud risks owing to the business nature of DIPL Ltd:

Due to an improper examination of the new IT system, inaccurate details were

incorporated into the system, thereby resulting in inappropriate accounting figures in the

financial statements. Therefore, the biggest fraud risk in such a case is that of hampering

the account balances. Moreover, because of such improper measures, accountants can

easily gain an advantage to influence the account balances in a way that they never are

caught (Douglas et. al, 2015). For example, it may happen that the accountants write off

some outstanding amounts and settle them outside for self-interest benefits. On a whole,

the new IT system can result in a grave scenario because of inefficacies in recording the

data.

Since the company records its receipts through mailing facilities, it can encounter severe

complications because bank certification is missing in such scenario, thereby resulting in

fraudulent practices on the part of accountants. In relation to such a situation, it is very

significant that prior and effective verification is done with the bank with the help of a

bank statement so that the accountants can easily refer any amount that necessitates

authentication (Jubb, 2012). Further, it can also be observed that the company has been

conducting immoral internal control mechanisms within its affairs. As a result, it may

happen that such accountants transfer the resources of the company to a wrong person

and take advantage of the same funds for personal causes (Douglas et. al, 2015). Hence,

this cannot only affect the financial position of DIPL but also its resources as a whole. On

a whole, an effective bank reconciliation system has become the need of the hour in such

scenario. In addition, it is the responsibility of the management to carefully scrutinize

every detail forming part of the financial statements of the company on a regular basis so

that a stronger connection can be established, thereby ultimately resulting into enhanced

transparency.

Answer to 3(b)

The decision of auditor may fail to prove effective if the management is also indulged in

conducting such fraudulent steps. The key reason behind such ideology can be attributed to the

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Auditing

fact that the management has full responsibility and control over its financial statements, and

manipulating it is very easier for them. Besides, the manipulation done by the management is

very problematic to be identified by the auditor in the financial statements (Tepalagul, 2015).

Therefore, the auditor must plan his strategies in a way that it can mitigate all inefficacies in the

financial statements. For such purpose, authenticated documents like tax challans, ledgers, etc

must be taken note of. Further, the company’s cash position may also depict a distinct scenario if

all resources are not timely deposited with the bank, thereby resulting in affecting the auditor’s

role in a negative way (Cappelleto, 2010). On a whole, this can degrade the audit quality because

the irrelevant decision will be made owing to inappropriate financials made by the management.

In addition, the auditor must also be accustomed to the new IT system installed in the company

and since inappropriate recording was implemented in the initial stages, the audit quality can be

degraded. In simple words, the inefficacies in the testing segment can play a key role in

establishing hurdles for the auditor and the company as a whole (Jubb, 2012). Moreover, it might

also happen that because of ineffective testing of the new system, issues like piracy, data breach,

etc can occur. On a whole, because of the wrong implementation of the new system, the decision

of auditor may be influenced and result into the wrong judgement (Hoffelder, 2012). Therefore,

it is very vital for the auditor to know proper and accurate details about the new IT system

because being accustomed to a new system will consume an immense amount of time and since

the management feeds it, the decision offered by the auditor based on such information will

altogether result in an ineffective decision.

7

fact that the management has full responsibility and control over its financial statements, and

manipulating it is very easier for them. Besides, the manipulation done by the management is

very problematic to be identified by the auditor in the financial statements (Tepalagul, 2015).

Therefore, the auditor must plan his strategies in a way that it can mitigate all inefficacies in the

financial statements. For such purpose, authenticated documents like tax challans, ledgers, etc

must be taken note of. Further, the company’s cash position may also depict a distinct scenario if

all resources are not timely deposited with the bank, thereby resulting in affecting the auditor’s

role in a negative way (Cappelleto, 2010). On a whole, this can degrade the audit quality because

the irrelevant decision will be made owing to inappropriate financials made by the management.

In addition, the auditor must also be accustomed to the new IT system installed in the company

and since inappropriate recording was implemented in the initial stages, the audit quality can be

degraded. In simple words, the inefficacies in the testing segment can play a key role in

establishing hurdles for the auditor and the company as a whole (Jubb, 2012). Moreover, it might

also happen that because of ineffective testing of the new system, issues like piracy, data breach,

etc can occur. On a whole, because of the wrong implementation of the new system, the decision

of auditor may be influenced and result into the wrong judgement (Hoffelder, 2012). Therefore,

it is very vital for the auditor to know proper and accurate details about the new IT system

because being accustomed to a new system will consume an immense amount of time and since

the management feeds it, the decision offered by the auditor based on such information will

altogether result in an ineffective decision.

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Auditing

References

Brealey, R, Myers, S. & Allen, F 2014, Principles of corporate finance, New York: McGraw-

Hill/Irwin.

Brigs, A 2013, Financial reporting & analysis, Mason, Ohio: South-Western.

Cappelleto, G. 2010, Challenges Facing Accounting Education in Australia, AFAANZ,

Douglas M.B, Todd, D.F & Hermanson, D.R 2015, ‘The Effects of Internal Audit Report Type

and Reporting Relationship on Internal Auditors' Risk’, Judgments.Accounting Horizons, vol.

29, no. 3, pp. 695-718.

Elder, J. R, Beasley S. M.& Arens A. A 2010, Auditing and Assurance Services, Person

Education, New Jersey: USA

Geoffrey D. B, Joleen K, K. Kelli S & David A. W 2016, ‘Attracting Applicants for In-House

and Outsourced Internal Audit Positions: Views from External Auditors’, Accounting Horizons,

vol. 30, no. 1, pp. 143-156.

Ghandar, A & Tsahuridu, E 2013, The Auditing Handbook 2013, Australia: Pearson.

Gilbert, W. Joseph J & Terry J. E 2005, The Use of Control Self-Assessment by Independent

Auditors, The CPA Journal, vol.3, pp. 66-92

Goodstein, E 2011, Ethics and Economics, Economics and the Environment, Wiley

Hoffelder, K 2012, New Audit Standard Encourages More Talking, Harvard Press.

Jubb, C 2012, Auditing: A Business Risk Approach, Australia: Cengage

Messier, F. W 2013, Auditing and Assurance Services - A systematic approach, 9th ed. Australia:

McGraw Hill.

Tepalagul, N. & Lin, L 2015 ‘Auditor Independence and Audit Quality A Literature Review’,

Journal of Accounting, Auditing & Finance vol. 30, no. 1, pp. 101-121.

Wright, M.K. & Charles, J 2012, ‘Auditor independence and internal information systems audit

quality’, Business Studies Journal vol. 4, no. 2, pp. 63-84

8

References

Brealey, R, Myers, S. & Allen, F 2014, Principles of corporate finance, New York: McGraw-

Hill/Irwin.

Brigs, A 2013, Financial reporting & analysis, Mason, Ohio: South-Western.

Cappelleto, G. 2010, Challenges Facing Accounting Education in Australia, AFAANZ,

Douglas M.B, Todd, D.F & Hermanson, D.R 2015, ‘The Effects of Internal Audit Report Type

and Reporting Relationship on Internal Auditors' Risk’, Judgments.Accounting Horizons, vol.

29, no. 3, pp. 695-718.

Elder, J. R, Beasley S. M.& Arens A. A 2010, Auditing and Assurance Services, Person

Education, New Jersey: USA

Geoffrey D. B, Joleen K, K. Kelli S & David A. W 2016, ‘Attracting Applicants for In-House

and Outsourced Internal Audit Positions: Views from External Auditors’, Accounting Horizons,

vol. 30, no. 1, pp. 143-156.

Ghandar, A & Tsahuridu, E 2013, The Auditing Handbook 2013, Australia: Pearson.

Gilbert, W. Joseph J & Terry J. E 2005, The Use of Control Self-Assessment by Independent

Auditors, The CPA Journal, vol.3, pp. 66-92

Goodstein, E 2011, Ethics and Economics, Economics and the Environment, Wiley

Hoffelder, K 2012, New Audit Standard Encourages More Talking, Harvard Press.

Jubb, C 2012, Auditing: A Business Risk Approach, Australia: Cengage

Messier, F. W 2013, Auditing and Assurance Services - A systematic approach, 9th ed. Australia:

McGraw Hill.

Tepalagul, N. & Lin, L 2015 ‘Auditor Independence and Audit Quality A Literature Review’,

Journal of Accounting, Auditing & Finance vol. 30, no. 1, pp. 101-121.

Wright, M.K. & Charles, J 2012, ‘Auditor independence and internal information systems audit

quality’, Business Studies Journal vol. 4, no. 2, pp. 63-84

8

Auditing

Zhang, Y, Zhou,J & Zhou, N 2007, ‘Audit committee quality, auditor independence, and

internal control weakness’, Journal of Accounting and Public Policy vol. 26, pp. 300-327.

9

Zhang, Y, Zhou,J & Zhou, N 2007, ‘Audit committee quality, auditor independence, and

internal control weakness’, Journal of Accounting and Public Policy vol. 26, pp. 300-327.

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Auditing

Appendix

2013 2014 2015

Current Ratio

Current assets 5385938 7509150 9600929

Current liabilities 3780000 5120250 6397500

Current Ratio = CA/CL 1.42485

1

1.46655

9

1.50073

1

Debt Equity Ratio

Debt - - 7500000

Equity 9150000 1078365

0

1225049

1

0.61222

Quick Ratio

Quick assets 3129750 4837788 5420429

Current liabilities 3780000 5120250 6397500

Quick ratio 0.82797

6

0.94483

4

0.84727

3

Gross profit ratio

Gross profit 6004500 6079500 6604500

Revenue 3421200

0

3769950

0

4345950

0

GP ratio 17.5508

6

16.1262

1

15.1969

1

Net profit ratio

Net profit 2359190 2291362 2972183

Revenue 3421200

0

3769950

0

4345950

0

NP ratio 6.89579

7

6.07796

4

6.83897

2

Total asset turnover 2013 2014 2015

Net sales 3421200 3769950 4345950

10

Appendix

2013 2014 2015

Current Ratio

Current assets 5385938 7509150 9600929

Current liabilities 3780000 5120250 6397500

Current Ratio = CA/CL 1.42485

1

1.46655

9

1.50073

1

Debt Equity Ratio

Debt - - 7500000

Equity 9150000 1078365

0

1225049

1

0.61222

Quick Ratio

Quick assets 3129750 4837788 5420429

Current liabilities 3780000 5120250 6397500

Quick ratio 0.82797

6

0.94483

4

0.84727

3

Gross profit ratio

Gross profit 6004500 6079500 6604500

Revenue 3421200

0

3769950

0

4345950

0

GP ratio 17.5508

6

16.1262

1

15.1969

1

Net profit ratio

Net profit 2359190 2291362 2972183

Revenue 3421200

0

3769950

0

4345950

0

NP ratio 6.89579

7

6.07796

4

6.83897

2

Total asset turnover 2013 2014 2015

Net sales 3421200 3769950 4345950

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Auditing

0 0 0

Average total assets 1293000

0

1441695

0

2102594

6

Total Asset Turnover [(Net sales/Average total

assets) × 100]

264.594 261.494

3

206.694

6

Equity turnover ratio 2013 2014 2015

Net sales 3421200

0

3769950

0

4345950

0

Average equity 9150000 9966825 1151707

1

Equity Turnover [(Net sales/Average total Equity) ×

100]

373.901

6

378.249

8

377.348

6

11

0 0 0

Average total assets 1293000

0

1441695

0

2102594

6

Total Asset Turnover [(Net sales/Average total

assets) × 100]

264.594 261.494

3

206.694

6

Equity turnover ratio 2013 2014 2015

Net sales 3421200

0

3769950

0

4345950

0

Average equity 9150000 9966825 1151707

1

Equity Turnover [(Net sales/Average total Equity) ×

100]

373.901

6

378.249

8

377.348

6

11

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.