Audit, Assurance and Compliance Report

VerifiedAdded on 2020/02/24

|10

|1414

|52

Report

AI Summary

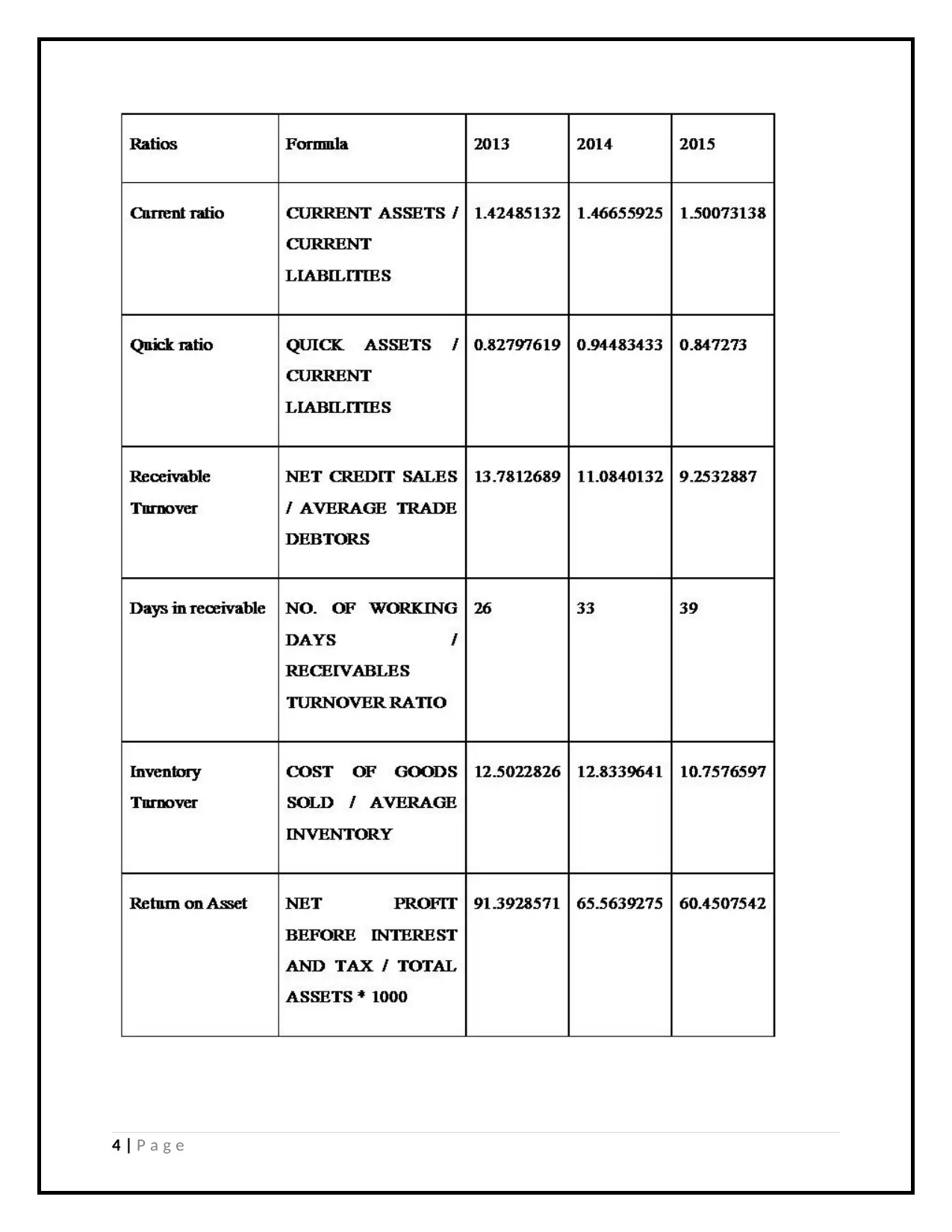

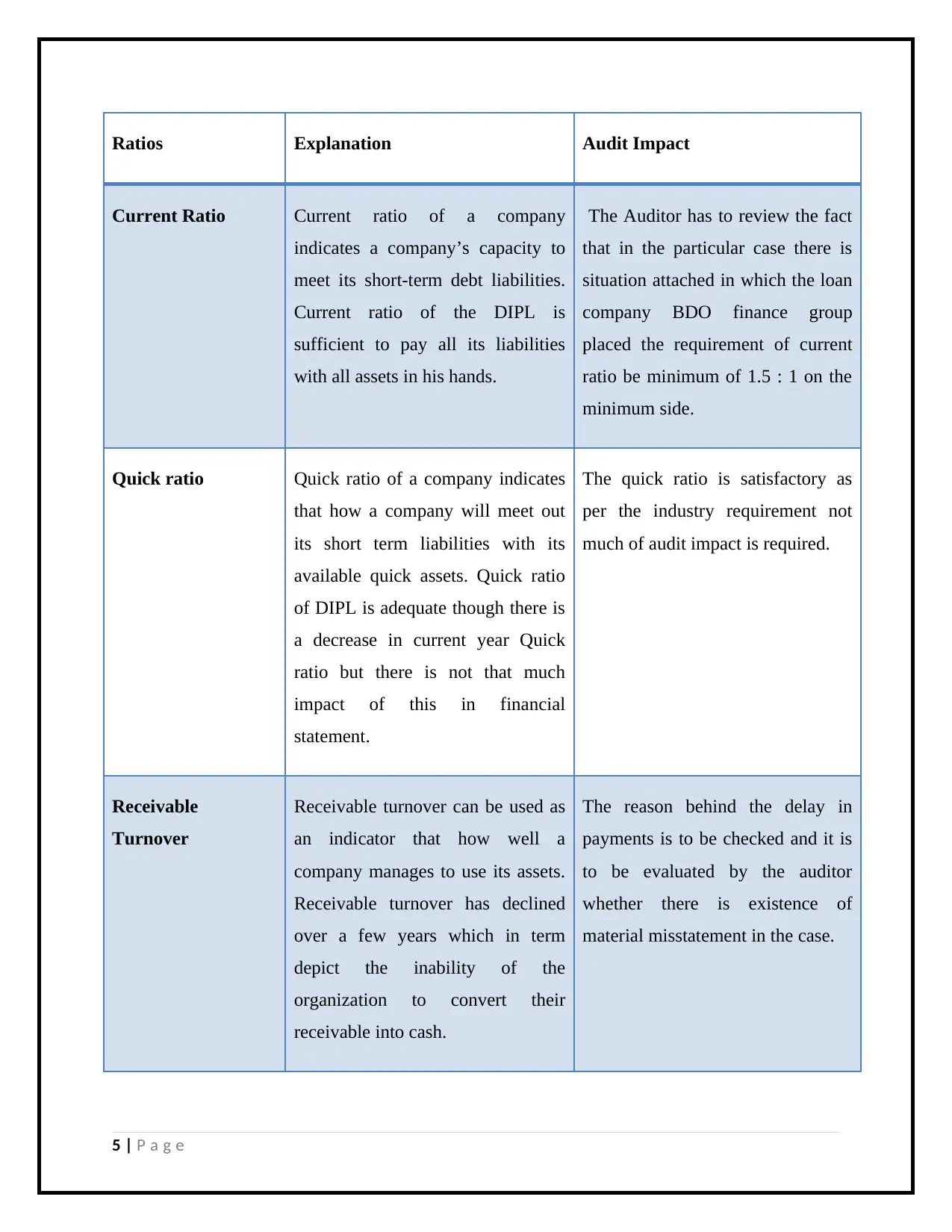

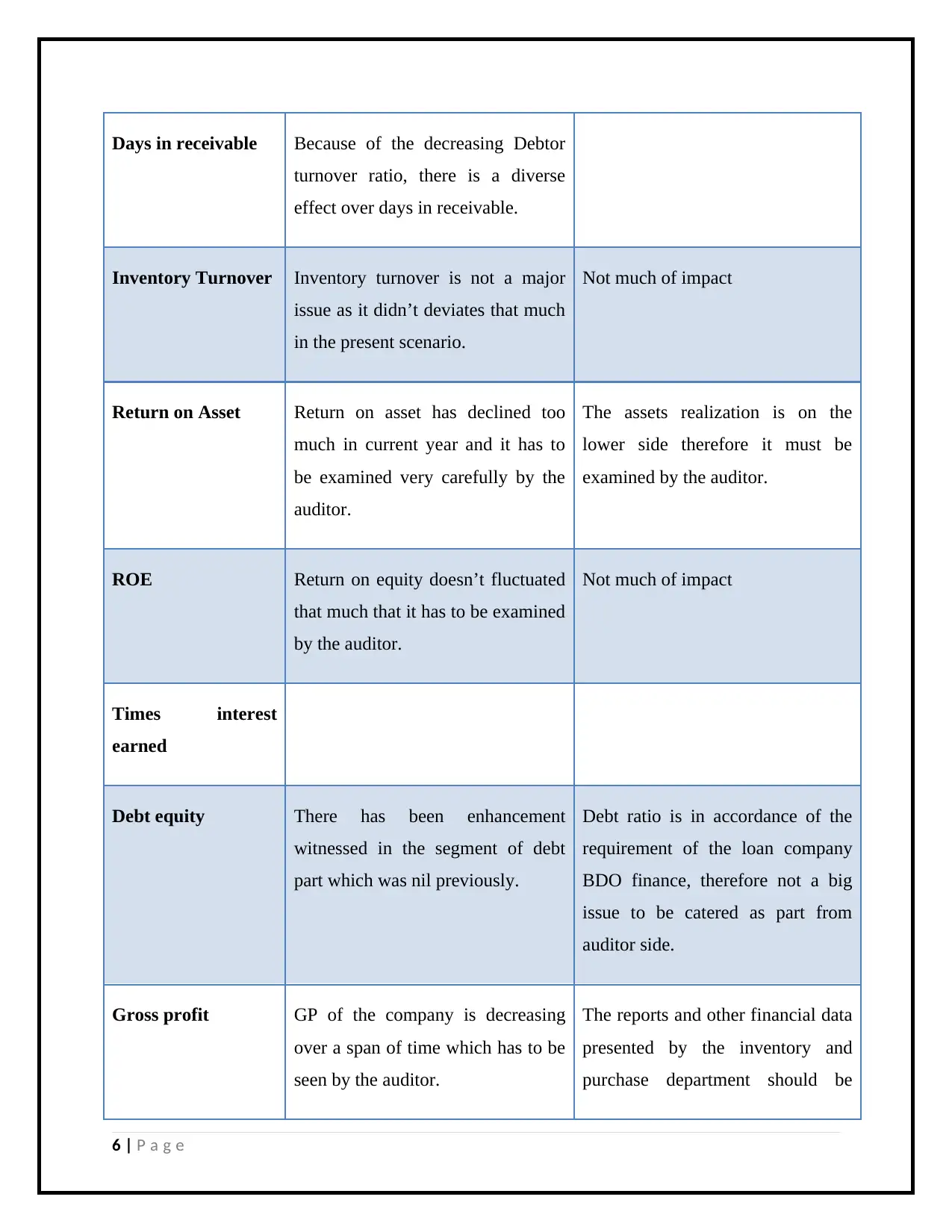

This report covers various aspects of audit, assurance, and compliance, including analytical procedures, inherent risks, and fraud detection. It discusses the financial ratios of Double Ink Printers Ltd., evaluates the impact of these ratios on audit processes, and highlights key areas for auditors to focus on to minimize risks. The report also references relevant literature to support the analysis.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.