Comprehensive Audit Assurance and Compliance Report for DIPL Company

VerifiedAdded on 2020/02/24

|12

|2407

|40

Report

AI Summary

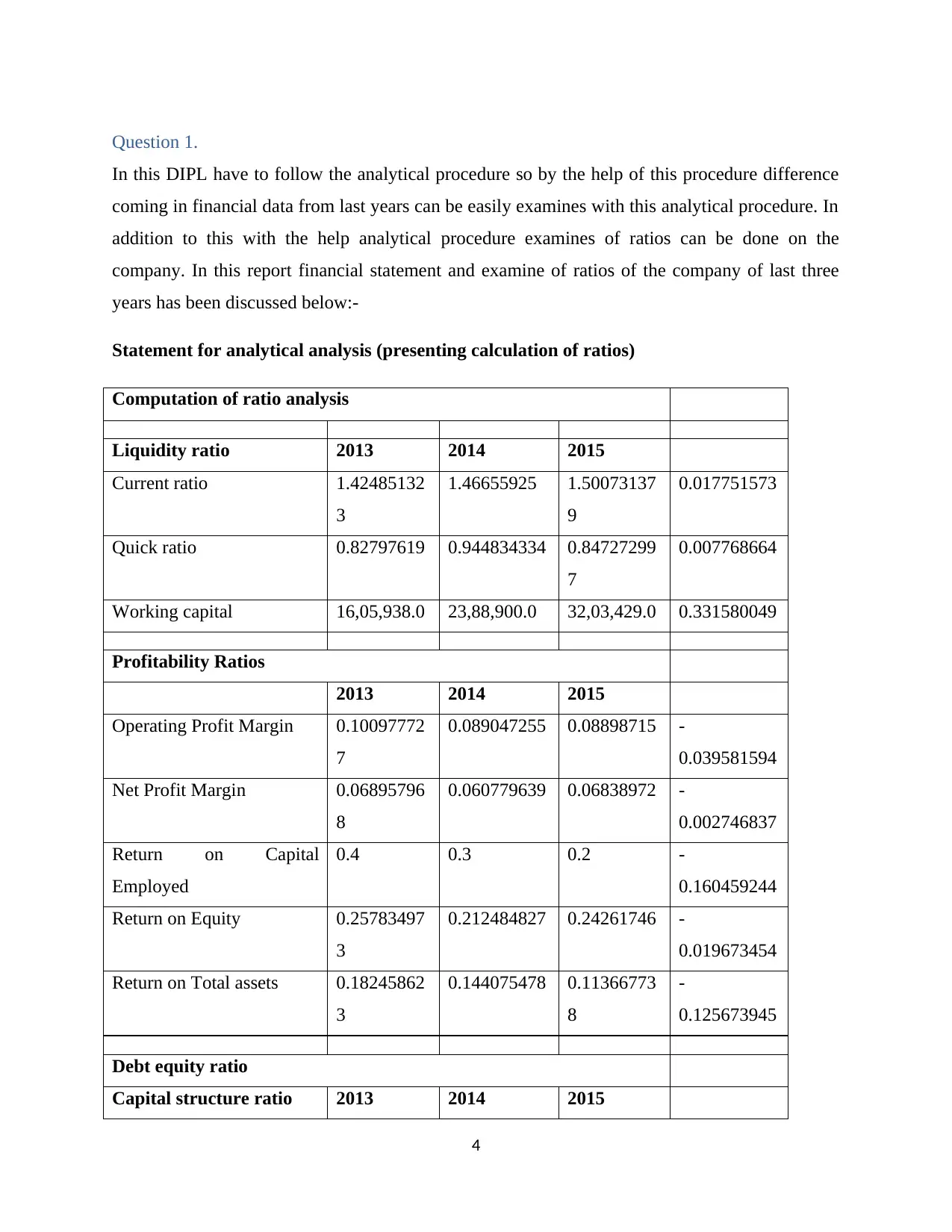

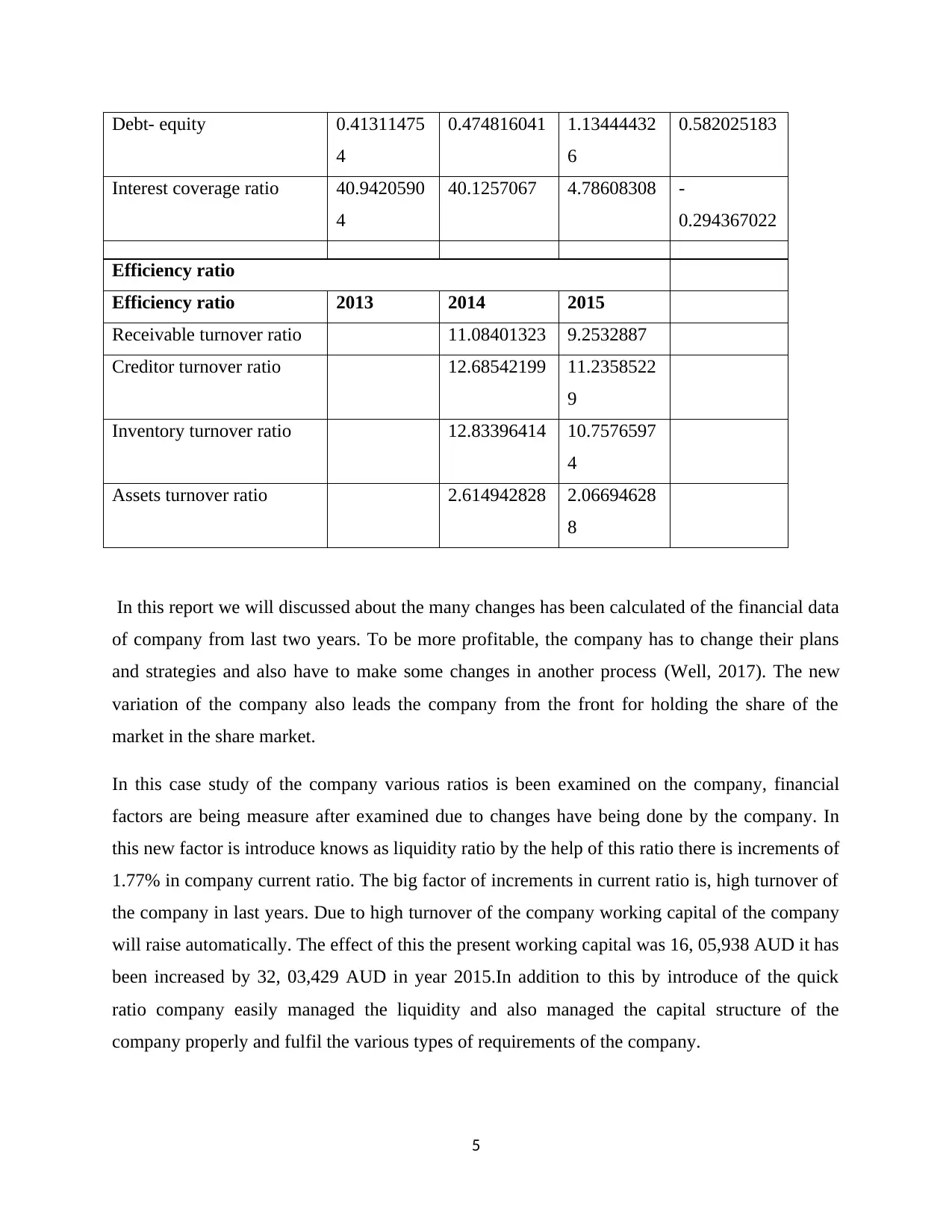

This report provides an in-depth analysis of the audit assurance and compliance for DIPL, an Australian-based printing company. It begins with an introduction to the company and the purpose of examining its financial statements, focusing on ratio analysis and the verification of statement accuracy. The report then delves into analytical procedures, comparing financial data over three years (2013-2015) to assess trends in liquidity, profitability, and capital structure ratios. It highlights significant changes, such as fluctuations in current and quick ratios, operating profit margins, and debt-to-equity ratios, and discusses their implications for the company's performance. The report also examines inherent risk factors, including intentional misstatements, international and domestic reporting standards, and key fraud risk factors like interest amounts and debt-to-equity ratios. It identifies potential fraud activities and the auditor's role in mitigating these risks, emphasizing the need for accurate financial reporting and compliance with accounting standards to avoid non-compliance risks and ensure stakeholders' trust. The analysis includes a discussion of how auditors can identify and address the identified fraud risks and other inconsistencies in the financial statements.

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.