Fama-French 3-Factor Model: Regression and Stock Style Analysis

VerifiedAdded on 2022/08/14

|3

|1074

|20

Project

AI Summary

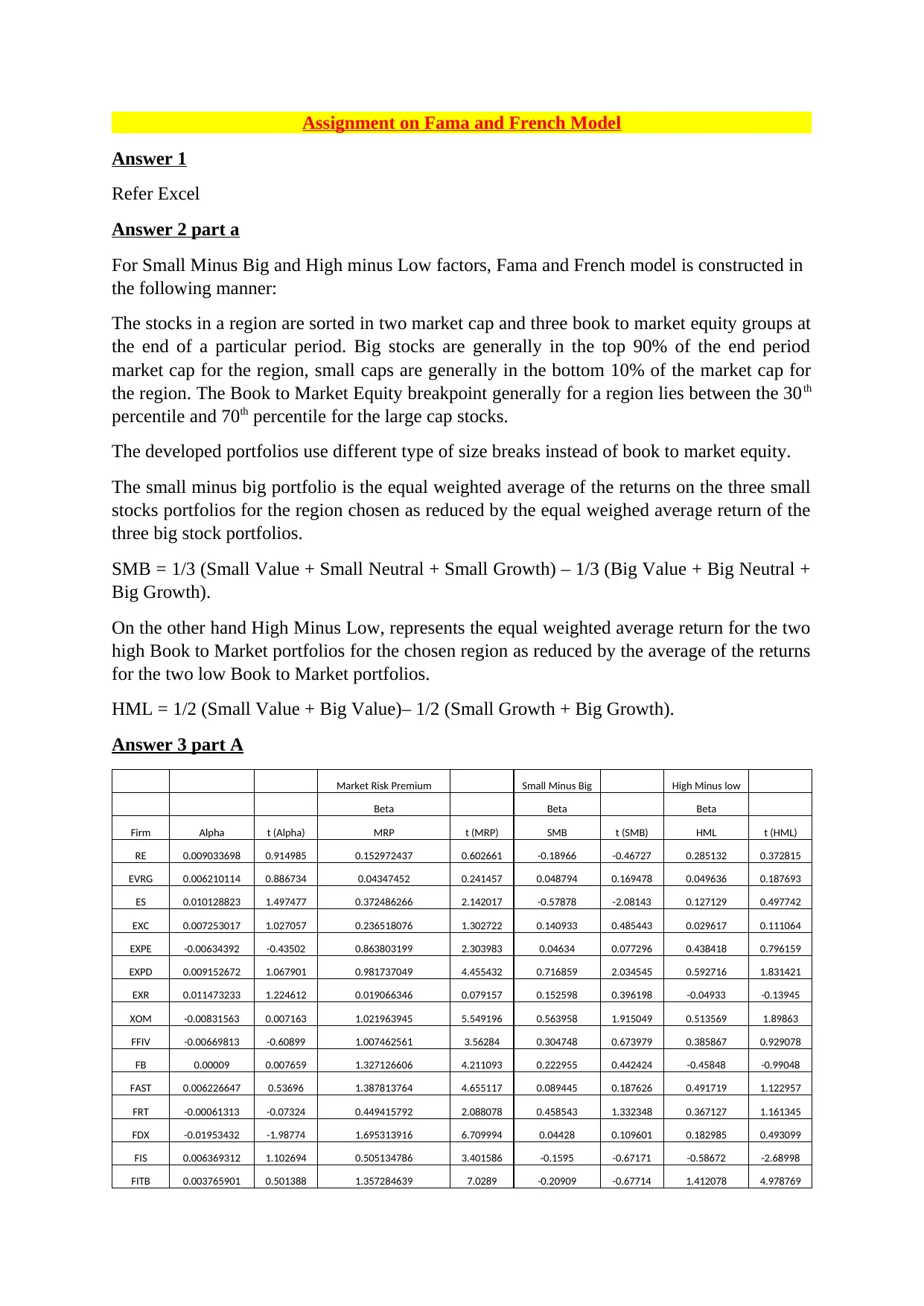

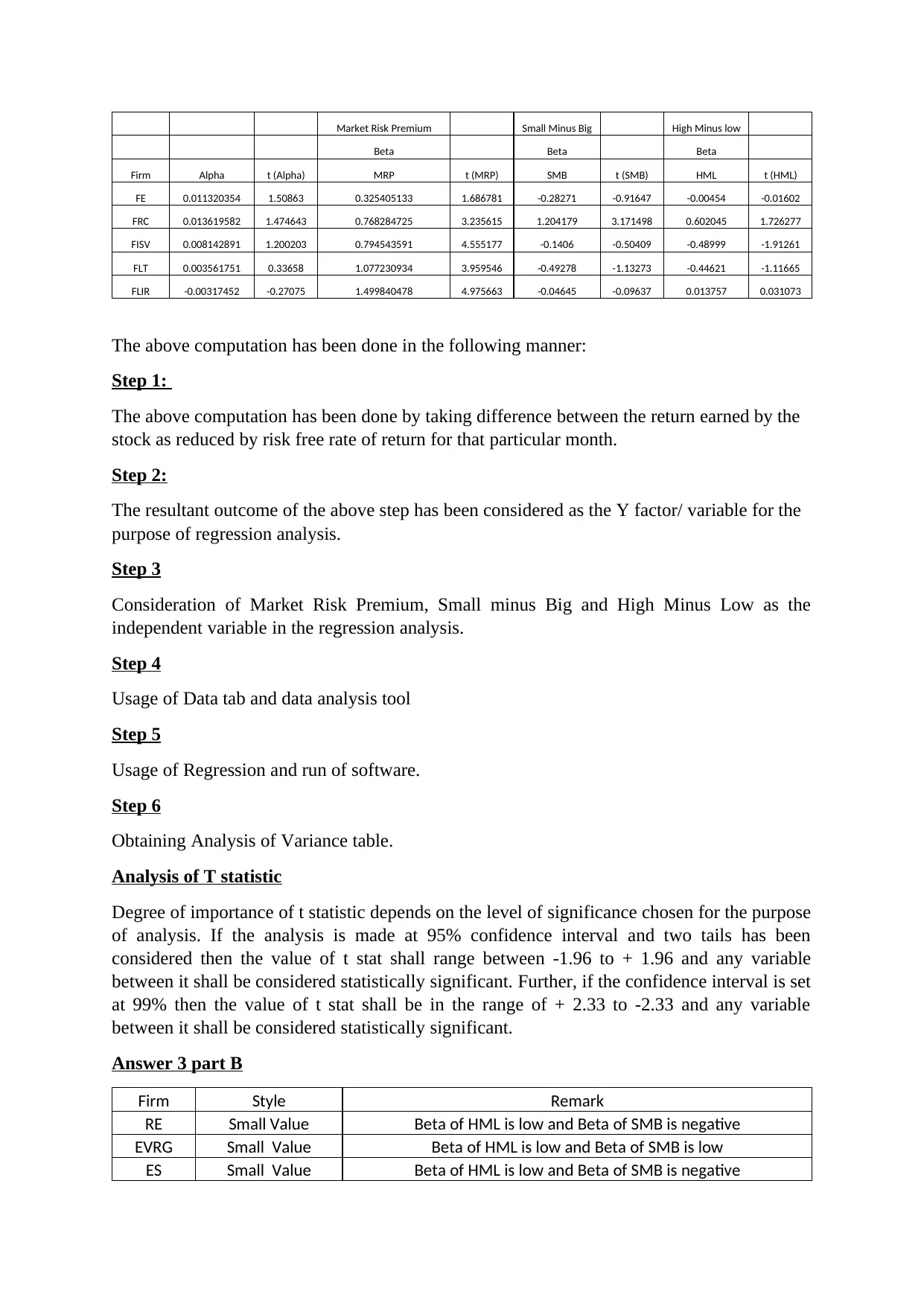

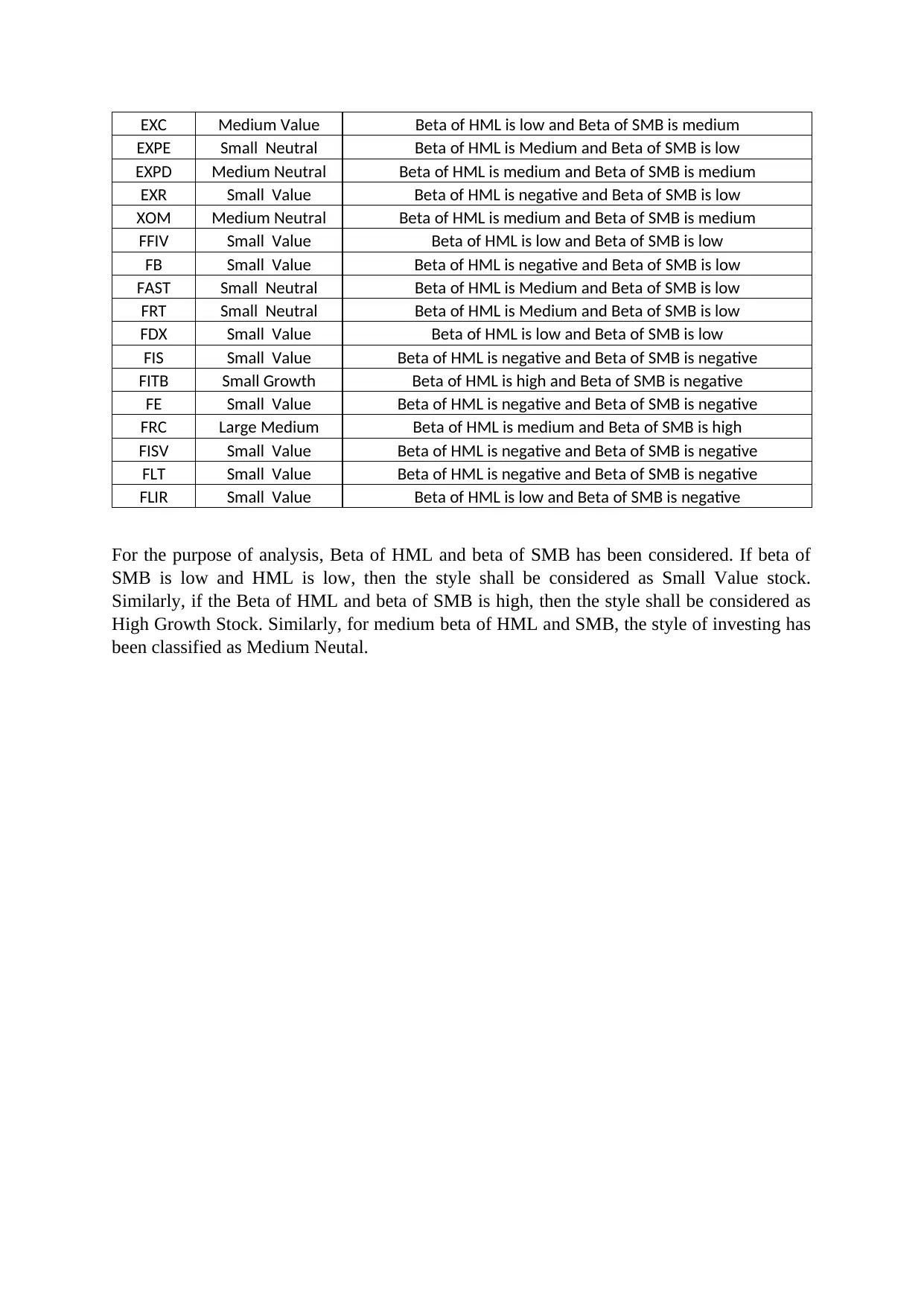

This assignment involves a financial analysis project focused on the Fama-French 3-factor model. The project utilizes real financial data for twenty stocks, employing multiple regression analysis to estimate the model. The solution details the construction of Small Minus Big (SMB) and High Minus Low (HML) factors, and the calculation of market risk premium. The student performs regression analysis to determine the significance of each factor, interpreting t-statistics and analyzing the impact of SMB and HML on individual stock returns. The assignment also classifies stocks based on their style (e.g., Small Value, Medium Neutral) according to the betas of HML and SMB. The process includes data preparation, regression execution, and the interpretation of results to discern whether a stock return significantly loads on one or more of the three factors and to discuss the empirical findings.

1 out of 3

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.