Finance Assignment: Calculating WACC and Intrinsic Value - FY2013 Data

VerifiedAdded on 2020/04/21

|5

|591

|147

Homework Assignment

AI Summary

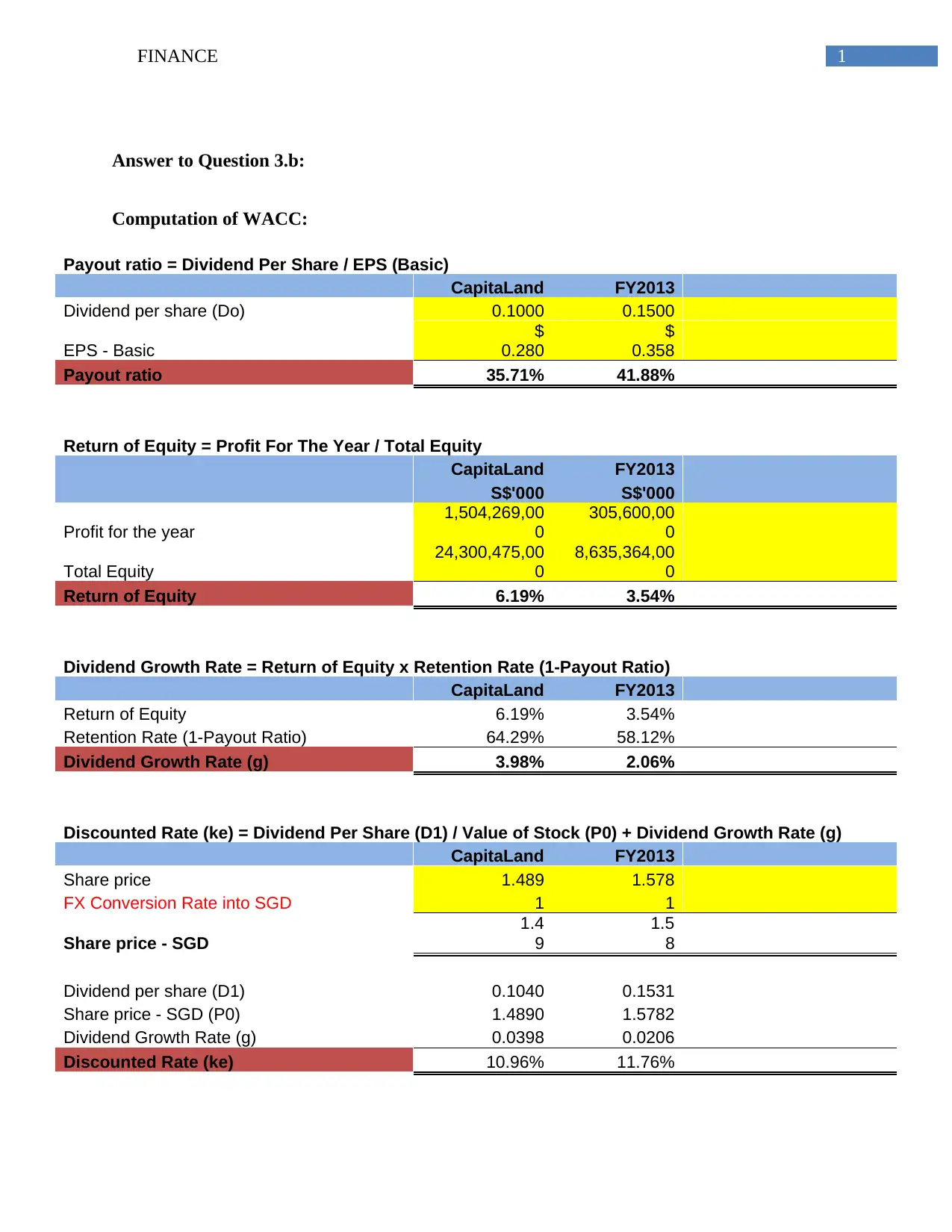

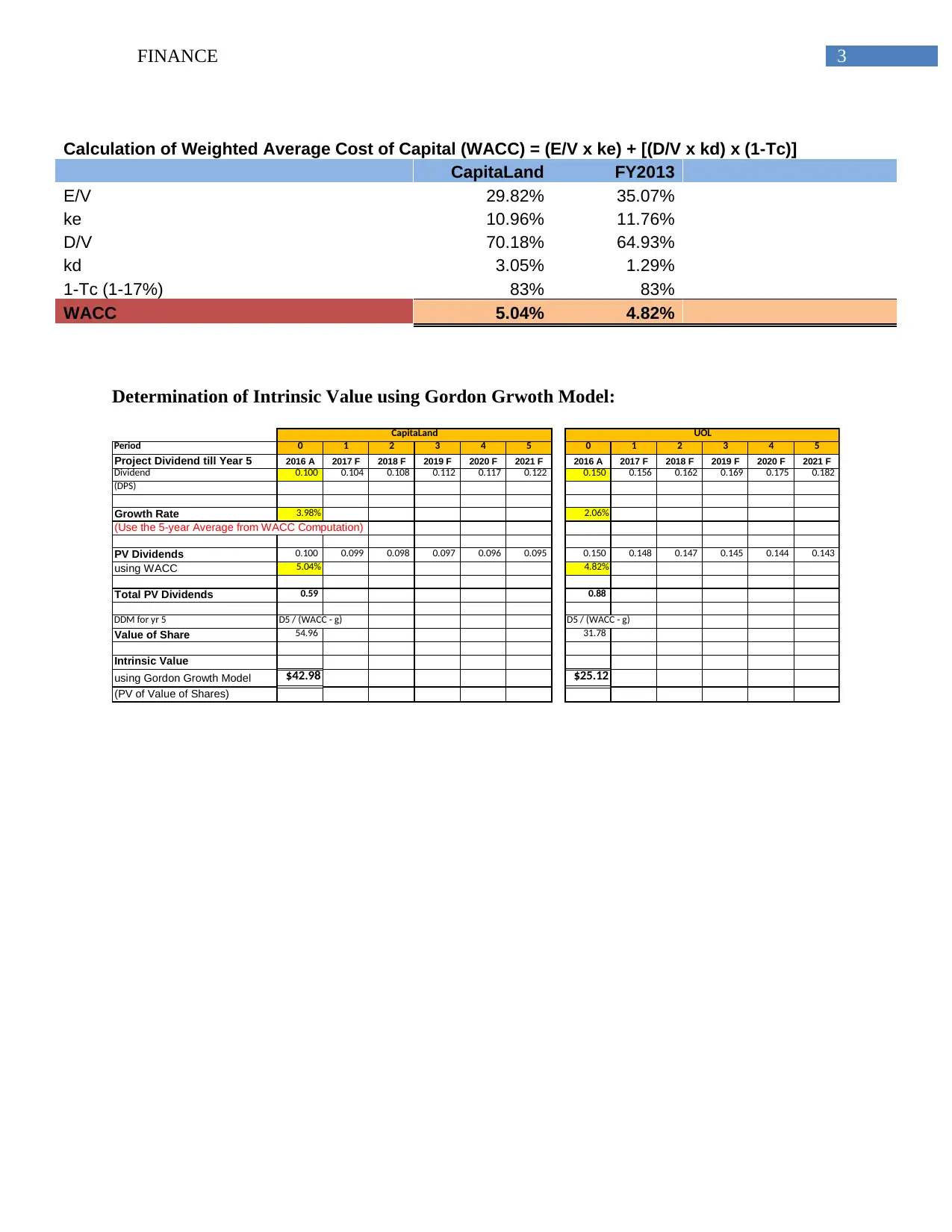

This finance assignment provides a detailed analysis of CapitaLand's financial data for the fiscal year 2013. The solution calculates the Weighted Average Cost of Capital (WACC), including the cost of equity and cost of debt, using financial statements and relevant formulas. It also computes the intrinsic value of the company using the Gordon Growth Model. The assignment demonstrates the steps involved in determining the payout ratio, return on equity, and dividend growth rate. Furthermore, it includes the calculation of the cost of debt based on the company's financial structure. The assignment concludes with a bibliography of sources used for the analysis. This solution is available on Desklib, a platform offering AI-based study tools and academic resources for students.

1 out of 5

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.