Financial Analysis and Investment Appraisal Report - University

VerifiedAdded on 2021/04/24

|23

|2433

|21

Report

AI Summary

This report provides a comprehensive analysis of financial decision-making for a business, evaluating various investment appraisal methods and their implications. It begins with a decision analysis for Dream Catcher, comparing international and domestic expansion with a no-change scenario, and recommends international expansion based on profit projections. The report then assesses mortgage alternatives for Kyle Dier, comparing lenders like HSBC-UK, Virgin Money, and Chesler Building Society, ultimately recommending HSBC for its lower monthly payments. Next, it reviews profitable models for a table product line, using linear regression across three scenarios to maximize profit. Finally, the report demonstrates investment appraisal methods such as net present value, internal rate of return, accounting rate of return, and payback period, analyzing investment projects for Pierce Plc, and recommending investment in product Y based on payback period and IRR criteria. The report also includes an analysis of expected and actual exam scores, covering topics in Quantitative Methods and Accounting.

Running head: BUSINESS

Business

Name of the Student

Name of the University

Author Note

Business

Name of the Student

Name of the University

Author Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

BUSINESS

Table of Contents

Question 1:.................................................................................................................................3

Introduction:...........................................................................................................................3

Requirement a).......................................................................................................................3

Requirement b).......................................................................................................................4

Conclusion:............................................................................................................................4

Question 2:.................................................................................................................................5

Introduction:...........................................................................................................................5

Requirement a).......................................................................................................................5

Requirement b).......................................................................................................................5

Requirement c).......................................................................................................................9

Requirement d).....................................................................................................................12

Conclusion:..........................................................................................................................13

Question 3:...............................................................................................................................13

Introduction:.........................................................................................................................13

Discussion:...........................................................................................................................13

Conclusion:..........................................................................................................................17

Question 4:...............................................................................................................................18

Introduction:.........................................................................................................................18

Requirement a).....................................................................................................................18

BUSINESS

Table of Contents

Question 1:.................................................................................................................................3

Introduction:...........................................................................................................................3

Requirement a).......................................................................................................................3

Requirement b).......................................................................................................................4

Conclusion:............................................................................................................................4

Question 2:.................................................................................................................................5

Introduction:...........................................................................................................................5

Requirement a).......................................................................................................................5

Requirement b).......................................................................................................................5

Requirement c).......................................................................................................................9

Requirement d).....................................................................................................................12

Conclusion:..........................................................................................................................13

Question 3:...............................................................................................................................13

Introduction:.........................................................................................................................13

Discussion:...........................................................................................................................13

Conclusion:..........................................................................................................................17

Question 4:...............................................................................................................................18

Introduction:.........................................................................................................................18

Requirement a).....................................................................................................................18

2

BUSINESS

Requirement b).....................................................................................................................20

Requirement c).....................................................................................................................21

Conclusion:..........................................................................................................................21

Question 5:...............................................................................................................................22

Requirement a).....................................................................................................................22

Requirement b).....................................................................................................................23

Requirement c).....................................................................................................................24

References list:.........................................................................................................................26

BUSINESS

Requirement b).....................................................................................................................20

Requirement c).....................................................................................................................21

Conclusion:..........................................................................................................................21

Question 5:...............................................................................................................................22

Requirement a).....................................................................................................................22

Requirement b).....................................................................................................................23

Requirement c).....................................................................................................................24

References list:.........................................................................................................................26

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

BUSINESS

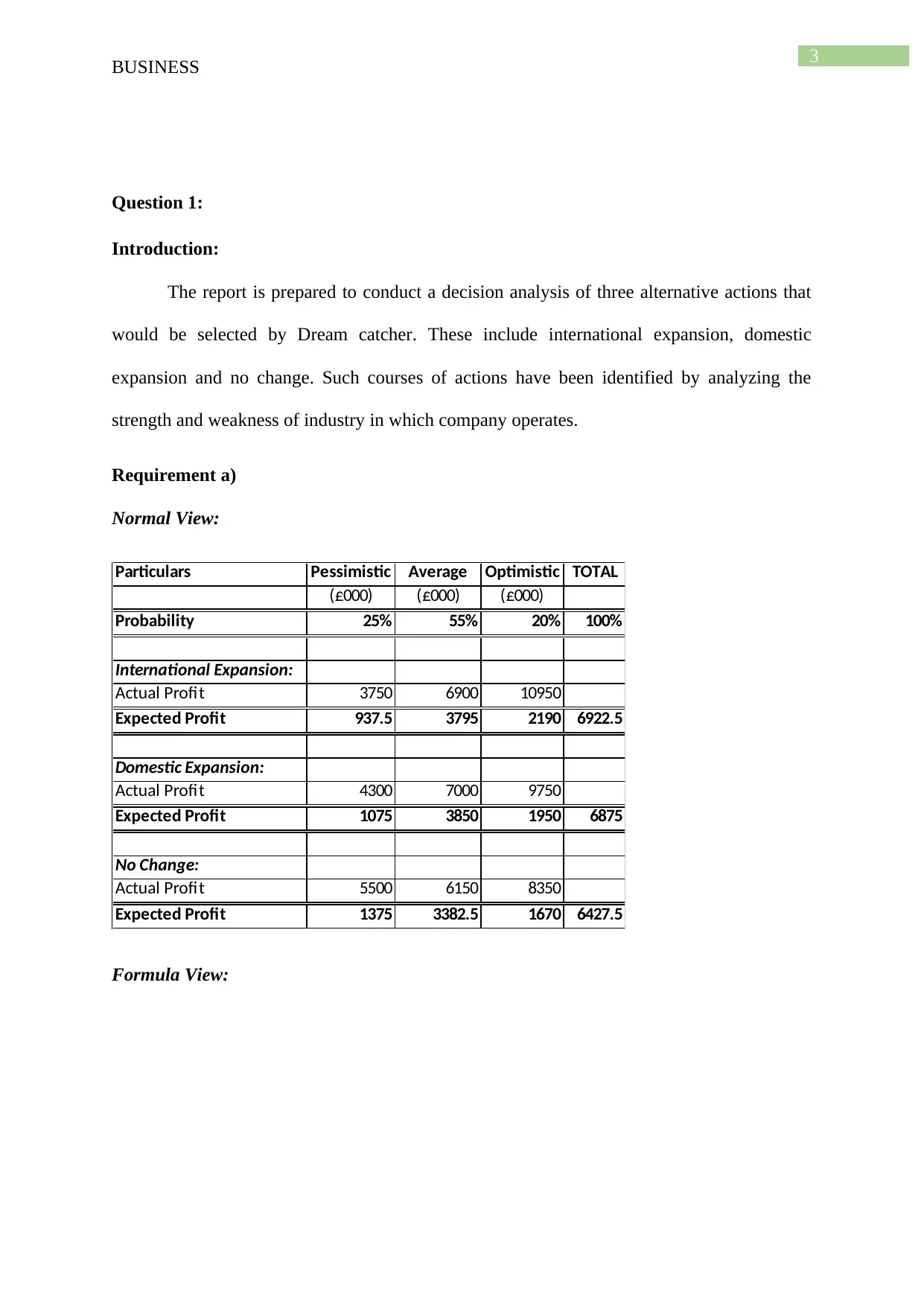

Question 1:

Introduction:

The report is prepared to conduct a decision analysis of three alternative actions that

would be selected by Dream catcher. These include international expansion, domestic

expansion and no change. Such courses of actions have been identified by analyzing the

strength and weakness of industry in which company operates.

Requirement a)

Normal View:

Particulars Pessimistic Average Optimistic TOTAL

(£000) (£000) (£000)

Probability 25% 55% 20% 100%

International Expansion:

Actual Profit 3750 6900 10950

Expected Profit 937.5 3795 2190 6922.5

Domestic Expansion:

Actual Profit 4300 7000 9750

Expected Profit 1075 3850 1950 6875

No Change:

Actual Profit 5500 6150 8350

Expected Profit 1375 3382.5 1670 6427.5

Formula View:

BUSINESS

Question 1:

Introduction:

The report is prepared to conduct a decision analysis of three alternative actions that

would be selected by Dream catcher. These include international expansion, domestic

expansion and no change. Such courses of actions have been identified by analyzing the

strength and weakness of industry in which company operates.

Requirement a)

Normal View:

Particulars Pessimistic Average Optimistic TOTAL

(£000) (£000) (£000)

Probability 25% 55% 20% 100%

International Expansion:

Actual Profit 3750 6900 10950

Expected Profit 937.5 3795 2190 6922.5

Domestic Expansion:

Actual Profit 4300 7000 9750

Expected Profit 1075 3850 1950 6875

No Change:

Actual Profit 5500 6150 8350

Expected Profit 1375 3382.5 1670 6427.5

Formula View:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

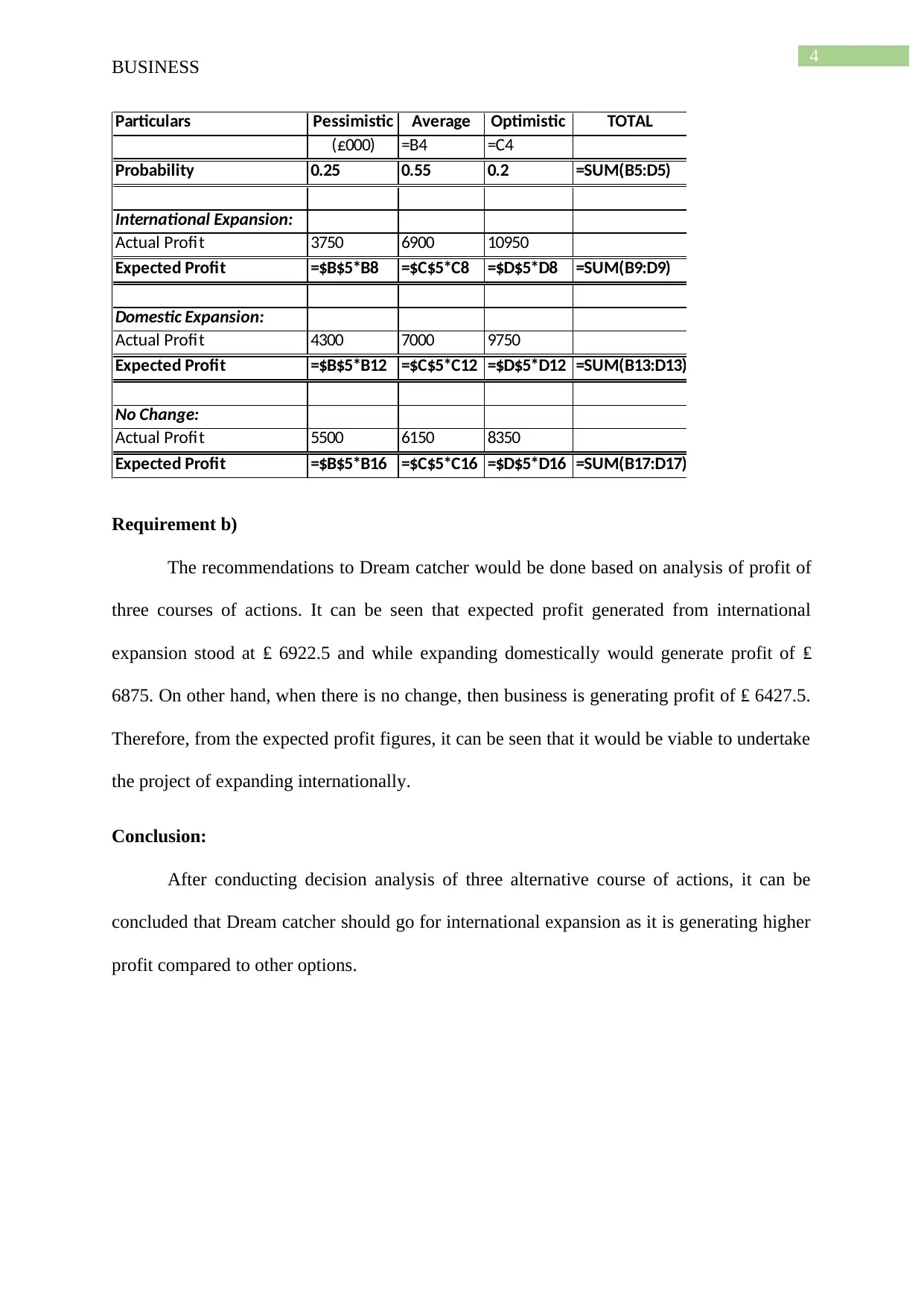

BUSINESS

Particulars Pessimistic Average Optimistic TOTAL

(£000) =B4 =C4

Probability 0.25 0.55 0.2 =SUM(B5:D5)

International Expansion:

Actual Profit 3750 6900 10950

Expected Profit =$B$5*B8 =$C$5*C8 =$D$5*D8 =SUM(B9:D9)

Domestic Expansion:

Actual Profit 4300 7000 9750

Expected Profit =$B$5*B12 =$C$5*C12 =$D$5*D12 =SUM(B13:D13)

No Change:

Actual Profit 5500 6150 8350

Expected Profit =$B$5*B16 =$C$5*C16 =$D$5*D16 =SUM(B17:D17)

Requirement b)

The recommendations to Dream catcher would be done based on analysis of profit of

three courses of actions. It can be seen that expected profit generated from international

expansion stood at ₤ 6922.5 and while expanding domestically would generate profit of ₤

6875. On other hand, when there is no change, then business is generating profit of ₤ 6427.5.

Therefore, from the expected profit figures, it can be seen that it would be viable to undertake

the project of expanding internationally.

Conclusion:

After conducting decision analysis of three alternative course of actions, it can be

concluded that Dream catcher should go for international expansion as it is generating higher

profit compared to other options.

BUSINESS

Particulars Pessimistic Average Optimistic TOTAL

(£000) =B4 =C4

Probability 0.25 0.55 0.2 =SUM(B5:D5)

International Expansion:

Actual Profit 3750 6900 10950

Expected Profit =$B$5*B8 =$C$5*C8 =$D$5*D8 =SUM(B9:D9)

Domestic Expansion:

Actual Profit 4300 7000 9750

Expected Profit =$B$5*B12 =$C$5*C12 =$D$5*D12 =SUM(B13:D13)

No Change:

Actual Profit 5500 6150 8350

Expected Profit =$B$5*B16 =$C$5*C16 =$D$5*D16 =SUM(B17:D17)

Requirement b)

The recommendations to Dream catcher would be done based on analysis of profit of

three courses of actions. It can be seen that expected profit generated from international

expansion stood at ₤ 6922.5 and while expanding domestically would generate profit of ₤

6875. On other hand, when there is no change, then business is generating profit of ₤ 6427.5.

Therefore, from the expected profit figures, it can be seen that it would be viable to undertake

the project of expanding internationally.

Conclusion:

After conducting decision analysis of three alternative course of actions, it can be

concluded that Dream catcher should go for international expansion as it is generating higher

profit compared to other options.

5

BUSINESS

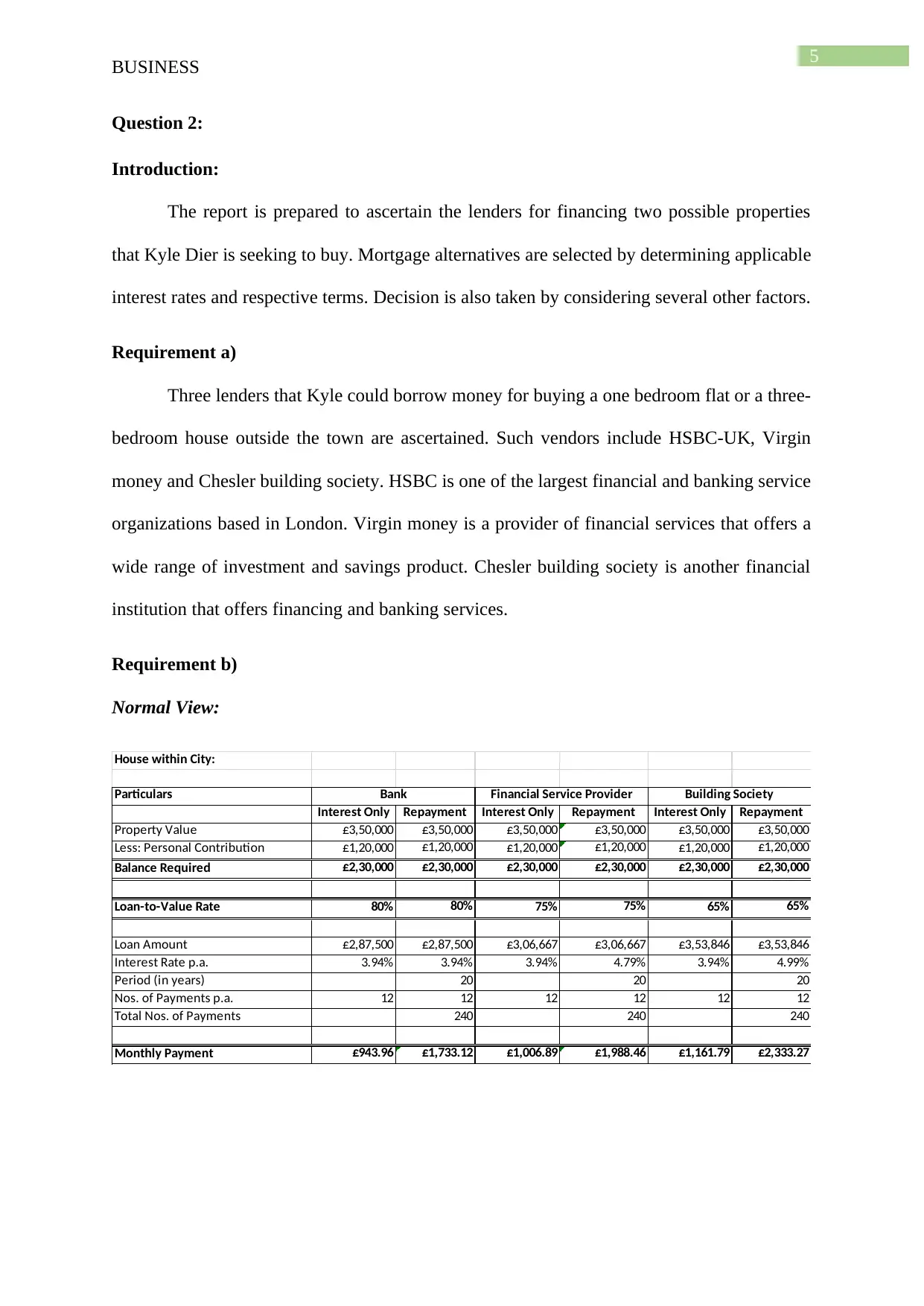

Question 2:

Introduction:

The report is prepared to ascertain the lenders for financing two possible properties

that Kyle Dier is seeking to buy. Mortgage alternatives are selected by determining applicable

interest rates and respective terms. Decision is also taken by considering several other factors.

Requirement a)

Three lenders that Kyle could borrow money for buying a one bedroom flat or a three-

bedroom house outside the town are ascertained. Such vendors include HSBC-UK, Virgin

money and Chesler building society. HSBC is one of the largest financial and banking service

organizations based in London. Virgin money is a provider of financial services that offers a

wide range of investment and savings product. Chesler building society is another financial

institution that offers financing and banking services.

Requirement b)

Normal View:

House within City:

Particulars

Interest Only Repayment Interest Only Repayment Interest Only Repayment

Property Value £3,50,000 £3,50,000 £3,50,000 £3,50,000 £3,50,000 £3,50,000

Less: Personal Contribution £1,20,000 £1,20,000 £1,20,000 £1,20,000 £1,20,000 £1,20,000

Balance Required £2,30,000 £2,30,000 £2,30,000 £2,30,000 £2,30,000 £2,30,000

Loan-to-Value Rate 80% 80% 75% 75% 65% 65%

Loan Amount £2,87,500 £2,87,500 £3,06,667 £3,06,667 £3,53,846 £3,53,846

Interest Rate p.a. 3.94% 3.94% 3.94% 4.79% 3.94% 4.99%

Period (in years) 20 20 20

Nos. of Payments p.a. 12 12 12 12 12 12

Total Nos. of Payments 240 240 240

Monthly Payment £943.96 £1,733.12 £1,006.89 £1,988.46 £1,161.79 £2,333.27

Bank Financial Service Provider Building Society

BUSINESS

Question 2:

Introduction:

The report is prepared to ascertain the lenders for financing two possible properties

that Kyle Dier is seeking to buy. Mortgage alternatives are selected by determining applicable

interest rates and respective terms. Decision is also taken by considering several other factors.

Requirement a)

Three lenders that Kyle could borrow money for buying a one bedroom flat or a three-

bedroom house outside the town are ascertained. Such vendors include HSBC-UK, Virgin

money and Chesler building society. HSBC is one of the largest financial and banking service

organizations based in London. Virgin money is a provider of financial services that offers a

wide range of investment and savings product. Chesler building society is another financial

institution that offers financing and banking services.

Requirement b)

Normal View:

House within City:

Particulars

Interest Only Repayment Interest Only Repayment Interest Only Repayment

Property Value £3,50,000 £3,50,000 £3,50,000 £3,50,000 £3,50,000 £3,50,000

Less: Personal Contribution £1,20,000 £1,20,000 £1,20,000 £1,20,000 £1,20,000 £1,20,000

Balance Required £2,30,000 £2,30,000 £2,30,000 £2,30,000 £2,30,000 £2,30,000

Loan-to-Value Rate 80% 80% 75% 75% 65% 65%

Loan Amount £2,87,500 £2,87,500 £3,06,667 £3,06,667 £3,53,846 £3,53,846

Interest Rate p.a. 3.94% 3.94% 3.94% 4.79% 3.94% 4.99%

Period (in years) 20 20 20

Nos. of Payments p.a. 12 12 12 12 12 12

Total Nos. of Payments 240 240 240

Monthly Payment £943.96 £1,733.12 £1,006.89 £1,988.46 £1,161.79 £2,333.27

Bank Financial Service Provider Building Society

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

BUSINESS

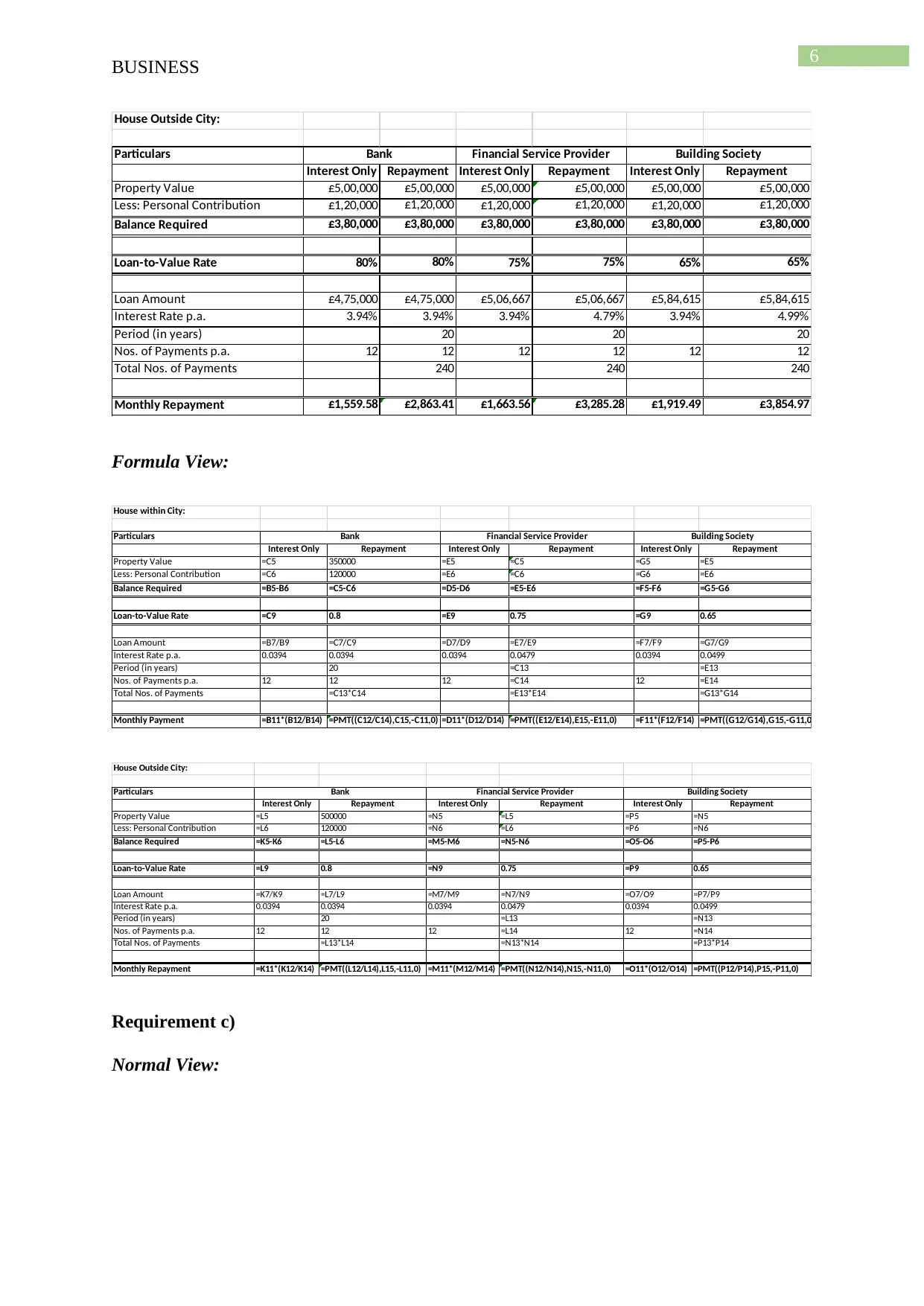

House Outside City:

Particulars

Interest Only Repayment Interest Only Repayment Interest Only Repayment

Property Value £5,00,000 £5,00,000 £5,00,000 £5,00,000 £5,00,000 £5,00,000

Less: Personal Contribution £1,20,000 £1,20,000 £1,20,000 £1,20,000 £1,20,000 £1,20,000

Balance Required £3,80,000 £3,80,000 £3,80,000 £3,80,000 £3,80,000 £3,80,000

Loan-to-Value Rate 80% 80% 75% 75% 65% 65%

Loan Amount £4,75,000 £4,75,000 £5,06,667 £5,06,667 £5,84,615 £5,84,615

Interest Rate p.a. 3.94% 3.94% 3.94% 4.79% 3.94% 4.99%

Period (in years) 20 20 20

Nos. of Payments p.a. 12 12 12 12 12 12

Total Nos. of Payments 240 240 240

Monthly Repayment £1,559.58 £2,863.41 £1,663.56 £3,285.28 £1,919.49 £3,854.97

Bank Financial Service Provider Building Society

Formula View:

House within City:

Particulars

Interest Only Repayment Interest Only Repayment Interest Only Repayment

Property Value =C5 350000 =E5 =C5 =G5 =E5

Less: Personal Contribution =C6 120000 =E6 =C6 =G6 =E6

Balance Required =B5-B6 =C5-C6 =D5-D6 =E5-E6 =F5-F6 =G5-G6

Loan-to-Value Rate =C9 0.8 =E9 0.75 =G9 0.65

Loan Amount =B7/B9 =C7/C9 =D7/D9 =E7/E9 =F7/F9 =G7/G9

Interest Rate p.a. 0.0394 0.0394 0.0394 0.0479 0.0394 0.0499

Period (in years) 20 =C13 =E13

Nos. of Payments p.a. 12 12 12 =C14 12 =E14

Total Nos. of Payments =C13*C14 =E13*E14 =G13*G14

Monthly Payment =B11*(B12/B14) =PMT((C12/C14),C15,-C11,0) =D11*(D12/D14) =PMT((E12/E14),E15,-E11,0) =F11*(F12/F14) =PMT((G12/G14),G15,-G11,0)

Bank Financial Service Provider Building Society

House Outside City:

Particulars

Interest Only Repayment Interest Only Repayment Interest Only Repayment

Property Value =L5 500000 =N5 =L5 =P5 =N5

Less: Personal Contribution =L6 120000 =N6 =L6 =P6 =N6

Balance Required =K5-K6 =L5-L6 =M5-M6 =N5-N6 =O5-O6 =P5-P6

Loan-to-Value Rate =L9 0.8 =N9 0.75 =P9 0.65

Loan Amount =K7/K9 =L7/L9 =M7/M9 =N7/N9 =O7/O9 =P7/P9

Interest Rate p.a. 0.0394 0.0394 0.0394 0.0479 0.0394 0.0499

Period (in years) 20 =L13 =N13

Nos. of Payments p.a. 12 12 12 =L14 12 =N14

Total Nos. of Payments =L13*L14 =N13*N14 =P13*P14

Monthly Repayment =K11*(K12/K14) =PMT((L12/L14),L15,-L11,0) =M11*(M12/M14) =PMT((N12/N14),N15,-N11,0) =O11*(O12/O14) =PMT((P12/P14),P15,-P11,0)

Bank Financial Service Provider Building Society

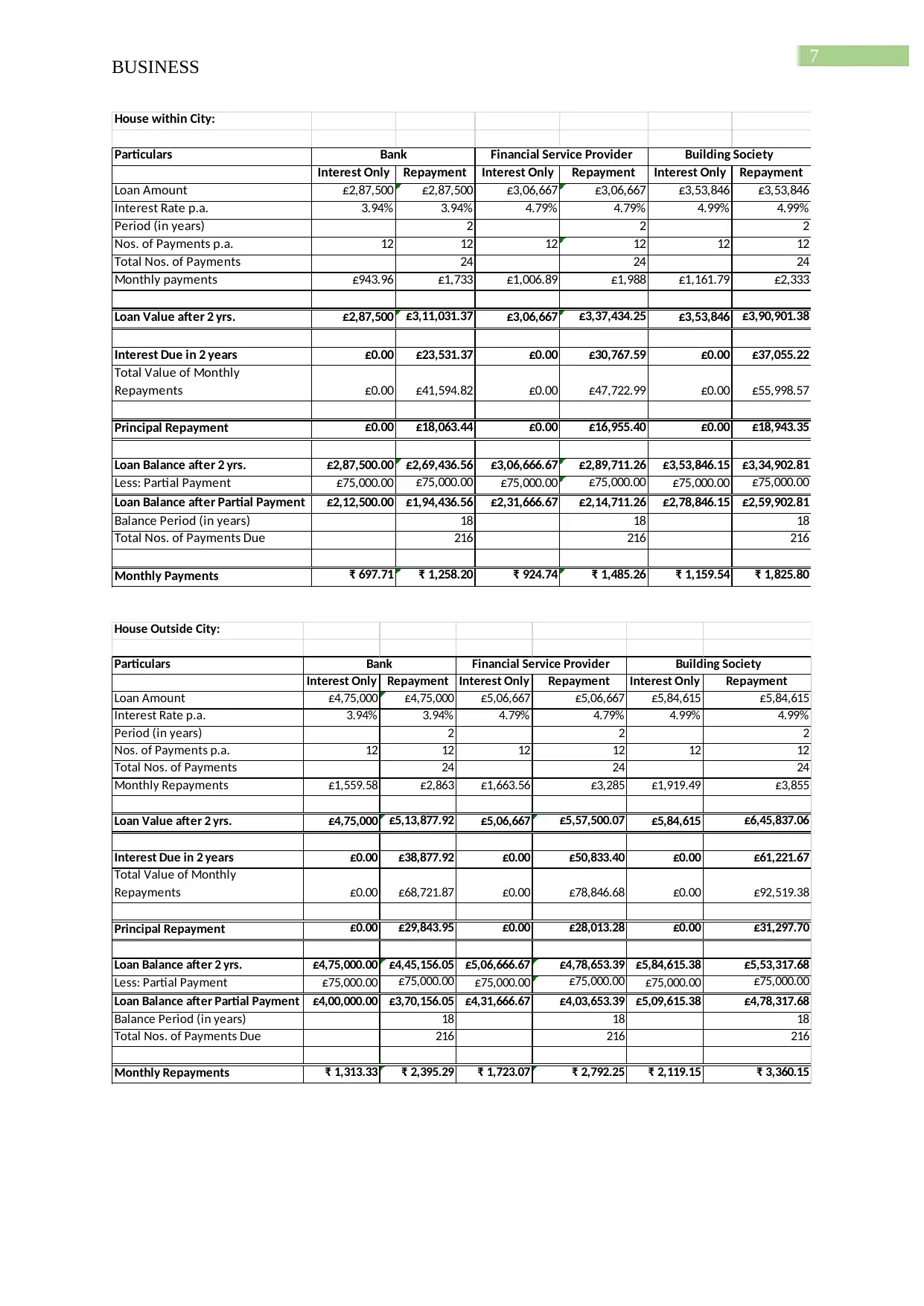

Requirement c)

Normal View:

BUSINESS

House Outside City:

Particulars

Interest Only Repayment Interest Only Repayment Interest Only Repayment

Property Value £5,00,000 £5,00,000 £5,00,000 £5,00,000 £5,00,000 £5,00,000

Less: Personal Contribution £1,20,000 £1,20,000 £1,20,000 £1,20,000 £1,20,000 £1,20,000

Balance Required £3,80,000 £3,80,000 £3,80,000 £3,80,000 £3,80,000 £3,80,000

Loan-to-Value Rate 80% 80% 75% 75% 65% 65%

Loan Amount £4,75,000 £4,75,000 £5,06,667 £5,06,667 £5,84,615 £5,84,615

Interest Rate p.a. 3.94% 3.94% 3.94% 4.79% 3.94% 4.99%

Period (in years) 20 20 20

Nos. of Payments p.a. 12 12 12 12 12 12

Total Nos. of Payments 240 240 240

Monthly Repayment £1,559.58 £2,863.41 £1,663.56 £3,285.28 £1,919.49 £3,854.97

Bank Financial Service Provider Building Society

Formula View:

House within City:

Particulars

Interest Only Repayment Interest Only Repayment Interest Only Repayment

Property Value =C5 350000 =E5 =C5 =G5 =E5

Less: Personal Contribution =C6 120000 =E6 =C6 =G6 =E6

Balance Required =B5-B6 =C5-C6 =D5-D6 =E5-E6 =F5-F6 =G5-G6

Loan-to-Value Rate =C9 0.8 =E9 0.75 =G9 0.65

Loan Amount =B7/B9 =C7/C9 =D7/D9 =E7/E9 =F7/F9 =G7/G9

Interest Rate p.a. 0.0394 0.0394 0.0394 0.0479 0.0394 0.0499

Period (in years) 20 =C13 =E13

Nos. of Payments p.a. 12 12 12 =C14 12 =E14

Total Nos. of Payments =C13*C14 =E13*E14 =G13*G14

Monthly Payment =B11*(B12/B14) =PMT((C12/C14),C15,-C11,0) =D11*(D12/D14) =PMT((E12/E14),E15,-E11,0) =F11*(F12/F14) =PMT((G12/G14),G15,-G11,0)

Bank Financial Service Provider Building Society

House Outside City:

Particulars

Interest Only Repayment Interest Only Repayment Interest Only Repayment

Property Value =L5 500000 =N5 =L5 =P5 =N5

Less: Personal Contribution =L6 120000 =N6 =L6 =P6 =N6

Balance Required =K5-K6 =L5-L6 =M5-M6 =N5-N6 =O5-O6 =P5-P6

Loan-to-Value Rate =L9 0.8 =N9 0.75 =P9 0.65

Loan Amount =K7/K9 =L7/L9 =M7/M9 =N7/N9 =O7/O9 =P7/P9

Interest Rate p.a. 0.0394 0.0394 0.0394 0.0479 0.0394 0.0499

Period (in years) 20 =L13 =N13

Nos. of Payments p.a. 12 12 12 =L14 12 =N14

Total Nos. of Payments =L13*L14 =N13*N14 =P13*P14

Monthly Repayment =K11*(K12/K14) =PMT((L12/L14),L15,-L11,0) =M11*(M12/M14) =PMT((N12/N14),N15,-N11,0) =O11*(O12/O14) =PMT((P12/P14),P15,-P11,0)

Bank Financial Service Provider Building Society

Requirement c)

Normal View:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

BUSINESS

House within City:

Particulars

Interest Only Repayment Interest Only Repayment Interest Only Repayment

Loan Amount £2,87,500 £2,87,500 £3,06,667 £3,06,667 £3,53,846 £3,53,846

Interest Rate p.a. 3.94% 3.94% 4.79% 4.79% 4.99% 4.99%

Period (in years) 2 2 2

Nos. of Payments p.a. 12 12 12 12 12 12

Total Nos. of Payments 24 24 24

Monthly payments £943.96 £1,733 £1,006.89 £1,988 £1,161.79 £2,333

Loan Value after 2 yrs. £2,87,500 £3,11,031.37 £3,06,667 £3,37,434.25 £3,53,846 £3,90,901.38

Interest Due in 2 years £0.00 £23,531.37 £0.00 £30,767.59 £0.00 £37,055.22

Total Value of Monthly

Repayments £0.00 £41,594.82 £0.00 £47,722.99 £0.00 £55,998.57

Principal Repayment £0.00 £18,063.44 £0.00 £16,955.40 £0.00 £18,943.35

Loan Balance after 2 yrs. £2,87,500.00 £2,69,436.56 £3,06,666.67 £2,89,711.26 £3,53,846.15 £3,34,902.81

Less: Partial Payment £75,000.00 £75,000.00 £75,000.00 £75,000.00 £75,000.00 £75,000.00

Loan Balance after Partial Payment £2,12,500.00 £1,94,436.56 £2,31,666.67 £2,14,711.26 £2,78,846.15 £2,59,902.81

Balance Period (in years) 18 18 18

Total Nos. of Payments Due 216 216 216

Monthly Payments ₹ 697.71 ₹ 1,258.20 ₹ 924.74 ₹ 1,485.26 ₹ 1,159.54 ₹ 1,825.80

Bank Financial Service Provider Building Society

House Outside City:

Particulars

Interest Only Repayment Interest Only Repayment Interest Only Repayment

Loan Amount £4,75,000 £4,75,000 £5,06,667 £5,06,667 £5,84,615 £5,84,615

Interest Rate p.a. 3.94% 3.94% 4.79% 4.79% 4.99% 4.99%

Period (in years) 2 2 2

Nos. of Payments p.a. 12 12 12 12 12 12

Total Nos. of Payments 24 24 24

Monthly Repayments £1,559.58 £2,863 £1,663.56 £3,285 £1,919.49 £3,855

Loan Value after 2 yrs. £4,75,000 £5,13,877.92 £5,06,667 £5,57,500.07 £5,84,615 £6,45,837.06

Interest Due in 2 years £0.00 £38,877.92 £0.00 £50,833.40 £0.00 £61,221.67

Total Value of Monthly

Repayments £0.00 £68,721.87 £0.00 £78,846.68 £0.00 £92,519.38

Principal Repayment £0.00 £29,843.95 £0.00 £28,013.28 £0.00 £31,297.70

Loan Balance after 2 yrs. £4,75,000.00 £4,45,156.05 £5,06,666.67 £4,78,653.39 £5,84,615.38 £5,53,317.68

Less: Partial Payment £75,000.00 £75,000.00 £75,000.00 £75,000.00 £75,000.00 £75,000.00

Loan Balance after Partial Payment £4,00,000.00 £3,70,156.05 £4,31,666.67 £4,03,653.39 £5,09,615.38 £4,78,317.68

Balance Period (in years) 18 18 18

Total Nos. of Payments Due 216 216 216

Monthly Repayments ₹ 1,313.33 ₹ 2,395.29 ₹ 1,723.07 ₹ 2,792.25 ₹ 2,119.15 ₹ 3,360.15

Bank Financial Service Provider Building Society

BUSINESS

House within City:

Particulars

Interest Only Repayment Interest Only Repayment Interest Only Repayment

Loan Amount £2,87,500 £2,87,500 £3,06,667 £3,06,667 £3,53,846 £3,53,846

Interest Rate p.a. 3.94% 3.94% 4.79% 4.79% 4.99% 4.99%

Period (in years) 2 2 2

Nos. of Payments p.a. 12 12 12 12 12 12

Total Nos. of Payments 24 24 24

Monthly payments £943.96 £1,733 £1,006.89 £1,988 £1,161.79 £2,333

Loan Value after 2 yrs. £2,87,500 £3,11,031.37 £3,06,667 £3,37,434.25 £3,53,846 £3,90,901.38

Interest Due in 2 years £0.00 £23,531.37 £0.00 £30,767.59 £0.00 £37,055.22

Total Value of Monthly

Repayments £0.00 £41,594.82 £0.00 £47,722.99 £0.00 £55,998.57

Principal Repayment £0.00 £18,063.44 £0.00 £16,955.40 £0.00 £18,943.35

Loan Balance after 2 yrs. £2,87,500.00 £2,69,436.56 £3,06,666.67 £2,89,711.26 £3,53,846.15 £3,34,902.81

Less: Partial Payment £75,000.00 £75,000.00 £75,000.00 £75,000.00 £75,000.00 £75,000.00

Loan Balance after Partial Payment £2,12,500.00 £1,94,436.56 £2,31,666.67 £2,14,711.26 £2,78,846.15 £2,59,902.81

Balance Period (in years) 18 18 18

Total Nos. of Payments Due 216 216 216

Monthly Payments ₹ 697.71 ₹ 1,258.20 ₹ 924.74 ₹ 1,485.26 ₹ 1,159.54 ₹ 1,825.80

Bank Financial Service Provider Building Society

House Outside City:

Particulars

Interest Only Repayment Interest Only Repayment Interest Only Repayment

Loan Amount £4,75,000 £4,75,000 £5,06,667 £5,06,667 £5,84,615 £5,84,615

Interest Rate p.a. 3.94% 3.94% 4.79% 4.79% 4.99% 4.99%

Period (in years) 2 2 2

Nos. of Payments p.a. 12 12 12 12 12 12

Total Nos. of Payments 24 24 24

Monthly Repayments £1,559.58 £2,863 £1,663.56 £3,285 £1,919.49 £3,855

Loan Value after 2 yrs. £4,75,000 £5,13,877.92 £5,06,667 £5,57,500.07 £5,84,615 £6,45,837.06

Interest Due in 2 years £0.00 £38,877.92 £0.00 £50,833.40 £0.00 £61,221.67

Total Value of Monthly

Repayments £0.00 £68,721.87 £0.00 £78,846.68 £0.00 £92,519.38

Principal Repayment £0.00 £29,843.95 £0.00 £28,013.28 £0.00 £31,297.70

Loan Balance after 2 yrs. £4,75,000.00 £4,45,156.05 £5,06,666.67 £4,78,653.39 £5,84,615.38 £5,53,317.68

Less: Partial Payment £75,000.00 £75,000.00 £75,000.00 £75,000.00 £75,000.00 £75,000.00

Loan Balance after Partial Payment £4,00,000.00 £3,70,156.05 £4,31,666.67 £4,03,653.39 £5,09,615.38 £4,78,317.68

Balance Period (in years) 18 18 18

Total Nos. of Payments Due 216 216 216

Monthly Repayments ₹ 1,313.33 ₹ 2,395.29 ₹ 1,723.07 ₹ 2,792.25 ₹ 2,119.15 ₹ 3,360.15

Bank Financial Service Provider Building Society

8

BUSINESS

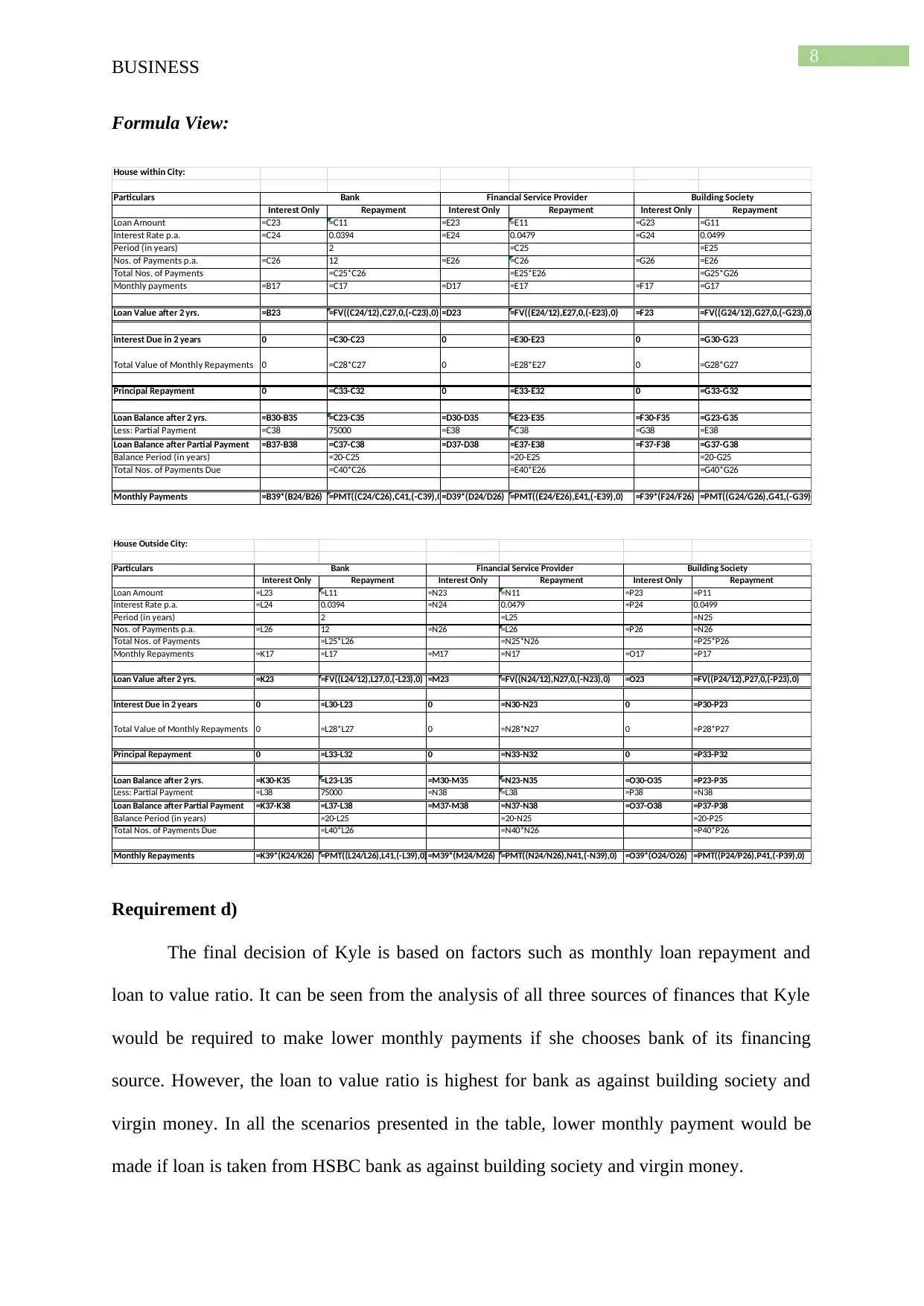

Formula View:

House within City:

Particulars

Interest Only Repayment Interest Only Repayment Interest Only Repayment

Loan Amount =C23 =C11 =E23 =E11 =G23 =G11

Interest Rate p.a. =C24 0.0394 =E24 0.0479 =G24 0.0499

Period (in years) 2 =C25 =E25

Nos. of Payments p.a. =C26 12 =E26 =C26 =G26 =E26

Total Nos. of Payments =C25*C26 =E25*E26 =G25*G26

Monthly payments =B17 =C17 =D17 =E17 =F17 =G17

Loan Value after 2 yrs. =B23 =FV((C24/12),C27,0,(-C23),0) =D23 =FV((E24/12),E27,0,(-E23),0) =F23 =FV((G24/12),G27,0,(-G23),0)

Interest Due in 2 years 0 =C30-C23 0 =E30-E23 0 =G30-G23

Total Value of Monthly Repayments 0 =C28*C27 0 =E28*E27 0 =G28*G27

Principal Repayment 0 =C33-C32 0 =E33-E32 0 =G33-G32

Loan Balance after 2 yrs. =B30-B35 =C23-C35 =D30-D35 =E23-E35 =F30-F35 =G23-G35

Less: Partial Payment =C38 75000 =E38 =C38 =G38 =E38

Loan Balance after Partial Payment =B37-B38 =C37-C38 =D37-D38 =E37-E38 =F37-F38 =G37-G38

Balance Period (in years) =20-C25 =20-E25 =20-G25

Total Nos. of Payments Due =C40*C26 =E40*E26 =G40*G26

Monthly Payments =B39*(B24/B26) =PMT((C24/C26),C41,(-C39),0)=D39*(D24/D26) =PMT((E24/E26),E41,(-E39),0) =F39*(F24/F26) =PMT((G24/G26),G41,(-G39),0)

Bank Financial Service Provider Building Society

House Outside City:

Particulars

Interest Only Repayment Interest Only Repayment Interest Only Repayment

Loan Amount =L23 =L11 =N23 =N11 =P23 =P11

Interest Rate p.a. =L24 0.0394 =N24 0.0479 =P24 0.0499

Period (in years) 2 =L25 =N25

Nos. of Payments p.a. =L26 12 =N26 =L26 =P26 =N26

Total Nos. of Payments =L25*L26 =N25*N26 =P25*P26

Monthly Repayments =K17 =L17 =M17 =N17 =O17 =P17

Loan Value after 2 yrs. =K23 =FV((L24/12),L27,0,(-L23),0) =M23 =FV((N24/12),N27,0,(-N23),0) =O23 =FV((P24/12),P27,0,(-P23),0)

Interest Due in 2 years 0 =L30-L23 0 =N30-N23 0 =P30-P23

Total Value of Monthly Repayments 0 =L28*L27 0 =N28*N27 0 =P28*P27

Principal Repayment 0 =L33-L32 0 =N33-N32 0 =P33-P32

Loan Balance after 2 yrs. =K30-K35 =L23-L35 =M30-M35 =N23-N35 =O30-O35 =P23-P35

Less: Partial Payment =L38 75000 =N38 =L38 =P38 =N38

Loan Balance after Partial Payment =K37-K38 =L37-L38 =M37-M38 =N37-N38 =O37-O38 =P37-P38

Balance Period (in years) =20-L25 =20-N25 =20-P25

Total Nos. of Payments Due =L40*L26 =N40*N26 =P40*P26

Monthly Repayments =K39*(K24/K26) =PMT((L24/L26),L41,(-L39),0)=M39*(M24/M26) =PMT((N24/N26),N41,(-N39),0) =O39*(O24/O26) =PMT((P24/P26),P41,(-P39),0)

Bank Financial Service Provider Building Society

Requirement d)

The final decision of Kyle is based on factors such as monthly loan repayment and

loan to value ratio. It can be seen from the analysis of all three sources of finances that Kyle

would be required to make lower monthly payments if she chooses bank of its financing

source. However, the loan to value ratio is highest for bank as against building society and

virgin money. In all the scenarios presented in the table, lower monthly payment would be

made if loan is taken from HSBC bank as against building society and virgin money.

BUSINESS

Formula View:

House within City:

Particulars

Interest Only Repayment Interest Only Repayment Interest Only Repayment

Loan Amount =C23 =C11 =E23 =E11 =G23 =G11

Interest Rate p.a. =C24 0.0394 =E24 0.0479 =G24 0.0499

Period (in years) 2 =C25 =E25

Nos. of Payments p.a. =C26 12 =E26 =C26 =G26 =E26

Total Nos. of Payments =C25*C26 =E25*E26 =G25*G26

Monthly payments =B17 =C17 =D17 =E17 =F17 =G17

Loan Value after 2 yrs. =B23 =FV((C24/12),C27,0,(-C23),0) =D23 =FV((E24/12),E27,0,(-E23),0) =F23 =FV((G24/12),G27,0,(-G23),0)

Interest Due in 2 years 0 =C30-C23 0 =E30-E23 0 =G30-G23

Total Value of Monthly Repayments 0 =C28*C27 0 =E28*E27 0 =G28*G27

Principal Repayment 0 =C33-C32 0 =E33-E32 0 =G33-G32

Loan Balance after 2 yrs. =B30-B35 =C23-C35 =D30-D35 =E23-E35 =F30-F35 =G23-G35

Less: Partial Payment =C38 75000 =E38 =C38 =G38 =E38

Loan Balance after Partial Payment =B37-B38 =C37-C38 =D37-D38 =E37-E38 =F37-F38 =G37-G38

Balance Period (in years) =20-C25 =20-E25 =20-G25

Total Nos. of Payments Due =C40*C26 =E40*E26 =G40*G26

Monthly Payments =B39*(B24/B26) =PMT((C24/C26),C41,(-C39),0)=D39*(D24/D26) =PMT((E24/E26),E41,(-E39),0) =F39*(F24/F26) =PMT((G24/G26),G41,(-G39),0)

Bank Financial Service Provider Building Society

House Outside City:

Particulars

Interest Only Repayment Interest Only Repayment Interest Only Repayment

Loan Amount =L23 =L11 =N23 =N11 =P23 =P11

Interest Rate p.a. =L24 0.0394 =N24 0.0479 =P24 0.0499

Period (in years) 2 =L25 =N25

Nos. of Payments p.a. =L26 12 =N26 =L26 =P26 =N26

Total Nos. of Payments =L25*L26 =N25*N26 =P25*P26

Monthly Repayments =K17 =L17 =M17 =N17 =O17 =P17

Loan Value after 2 yrs. =K23 =FV((L24/12),L27,0,(-L23),0) =M23 =FV((N24/12),N27,0,(-N23),0) =O23 =FV((P24/12),P27,0,(-P23),0)

Interest Due in 2 years 0 =L30-L23 0 =N30-N23 0 =P30-P23

Total Value of Monthly Repayments 0 =L28*L27 0 =N28*N27 0 =P28*P27

Principal Repayment 0 =L33-L32 0 =N33-N32 0 =P33-P32

Loan Balance after 2 yrs. =K30-K35 =L23-L35 =M30-M35 =N23-N35 =O30-O35 =P23-P35

Less: Partial Payment =L38 75000 =N38 =L38 =P38 =N38

Loan Balance after Partial Payment =K37-K38 =L37-L38 =M37-M38 =N37-N38 =O37-O38 =P37-P38

Balance Period (in years) =20-L25 =20-N25 =20-P25

Total Nos. of Payments Due =L40*L26 =N40*N26 =P40*P26

Monthly Repayments =K39*(K24/K26) =PMT((L24/L26),L41,(-L39),0)=M39*(M24/M26) =PMT((N24/N26),N41,(-N39),0) =O39*(O24/O26) =PMT((P24/P26),P41,(-P39),0)

Bank Financial Service Provider Building Society

Requirement d)

The final decision of Kyle is based on factors such as monthly loan repayment and

loan to value ratio. It can be seen from the analysis of all three sources of finances that Kyle

would be required to make lower monthly payments if she chooses bank of its financing

source. However, the loan to value ratio is highest for bank as against building society and

virgin money. In all the scenarios presented in the table, lower monthly payment would be

made if loan is taken from HSBC bank as against building society and virgin money.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

BUSINESS

Conclusion:

From the available mortgage alternatives, it can be seen that HSBC bank provides the

most feasible source of financing as the borrower would be required to make lower monthly

payments as against other two options available. Moreover, the amount of monthly interest

only payments for all the options are lower than the monthly interest, plus, principal

repayments. Hence, the borrower can opt for monthly interest only payments. However, in

such scenario, the borrower must have to accumulate the total principal amount separately

within 20 years.

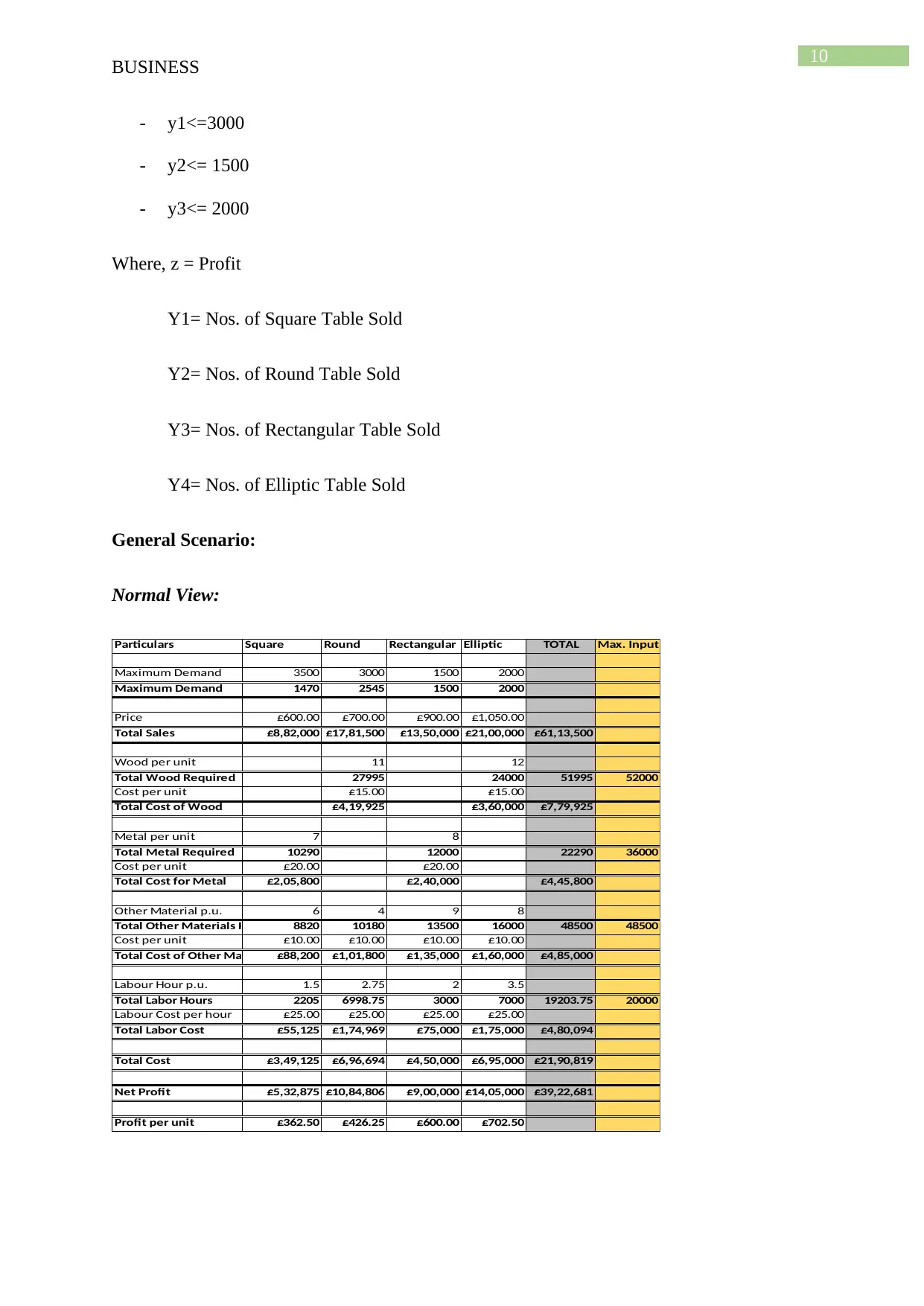

Question 3:

Introduction:

The report is prepared to conduct the review of most profitable models so that it

would help in addressing the problem of lower profit in table product line. Analysis of daily

production mix is done by considering three different scenarios.

Discussion:

The linear regression for maximizing the profit in the given situation is stated below:

- Maximize z = (600y + 700y1 + 900y2 + 1050y3) – [15 x (11y1 + 12y3)] – [20 x (7y +

8y2)] – [10 x (6y+4y1+9y2+8y3)] – [25 x (1.5y+2.75y1 + 2y2+3.5y3)]

Subject to Constraints:

- 11y1 + 12y3 <=52000

- 7y + 8y2 <= 36000

- 6y + 4y1 + 9y2 + 8y3 <= 48500

- 1.5y + 2.75y1 + 2y2 + 3.5y3 <=20000

- y<= 3500

BUSINESS

Conclusion:

From the available mortgage alternatives, it can be seen that HSBC bank provides the

most feasible source of financing as the borrower would be required to make lower monthly

payments as against other two options available. Moreover, the amount of monthly interest

only payments for all the options are lower than the monthly interest, plus, principal

repayments. Hence, the borrower can opt for monthly interest only payments. However, in

such scenario, the borrower must have to accumulate the total principal amount separately

within 20 years.

Question 3:

Introduction:

The report is prepared to conduct the review of most profitable models so that it

would help in addressing the problem of lower profit in table product line. Analysis of daily

production mix is done by considering three different scenarios.

Discussion:

The linear regression for maximizing the profit in the given situation is stated below:

- Maximize z = (600y + 700y1 + 900y2 + 1050y3) – [15 x (11y1 + 12y3)] – [20 x (7y +

8y2)] – [10 x (6y+4y1+9y2+8y3)] – [25 x (1.5y+2.75y1 + 2y2+3.5y3)]

Subject to Constraints:

- 11y1 + 12y3 <=52000

- 7y + 8y2 <= 36000

- 6y + 4y1 + 9y2 + 8y3 <= 48500

- 1.5y + 2.75y1 + 2y2 + 3.5y3 <=20000

- y<= 3500

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

BUSINESS

- y1<=3000

- y2<= 1500

- y3<= 2000

Where, z = Profit

Y1= Nos. of Square Table Sold

Y2= Nos. of Round Table Sold

Y3= Nos. of Rectangular Table Sold

Y4= Nos. of Elliptic Table Sold

General Scenario:

Normal View:

Particulars Square Round Rectangular Elliptic TOTAL Max. Input

Maximum Demand 3500 3000 1500 2000

Maximum Demand 1470 2545 1500 2000

Price £600.00 £700.00 £900.00 £1,050.00

Total Sales £8,82,000 £17,81,500 £13,50,000 £21,00,000 £61,13,500

Wood per unit 11 12

Total Wood Required 27995 24000 51995 52000

Cost per unit £15.00 £15.00

Total Cost of Wood £4,19,925 £3,60,000 £7,79,925

Metal per unit 7 8

Total Metal Required 10290 12000 22290 36000

Cost per unit £20.00 £20.00

Total Cost for Metal £2,05,800 £2,40,000 £4,45,800

Other Material p.u. 6 4 9 8

Total Other Materials Required 8820 10180 13500 16000 48500 48500

Cost per unit £10.00 £10.00 £10.00 £10.00

Total Cost of Other Material £88,200 £1,01,800 £1,35,000 £1,60,000 £4,85,000

Labour Hour p.u. 1.5 2.75 2 3.5

Total Labor Hours 2205 6998.75 3000 7000 19203.75 20000

Labour Cost per hour £25.00 £25.00 £25.00 £25.00

Total Labor Cost £55,125 £1,74,969 £75,000 £1,75,000 £4,80,094

Total Cost £3,49,125 £6,96,694 £4,50,000 £6,95,000 £21,90,819

Net Profit £5,32,875 £10,84,806 £9,00,000 £14,05,000 £39,22,681

Profit per unit £362.50 £426.25 £600.00 £702.50

BUSINESS

- y1<=3000

- y2<= 1500

- y3<= 2000

Where, z = Profit

Y1= Nos. of Square Table Sold

Y2= Nos. of Round Table Sold

Y3= Nos. of Rectangular Table Sold

Y4= Nos. of Elliptic Table Sold

General Scenario:

Normal View:

Particulars Square Round Rectangular Elliptic TOTAL Max. Input

Maximum Demand 3500 3000 1500 2000

Maximum Demand 1470 2545 1500 2000

Price £600.00 £700.00 £900.00 £1,050.00

Total Sales £8,82,000 £17,81,500 £13,50,000 £21,00,000 £61,13,500

Wood per unit 11 12

Total Wood Required 27995 24000 51995 52000

Cost per unit £15.00 £15.00

Total Cost of Wood £4,19,925 £3,60,000 £7,79,925

Metal per unit 7 8

Total Metal Required 10290 12000 22290 36000

Cost per unit £20.00 £20.00

Total Cost for Metal £2,05,800 £2,40,000 £4,45,800

Other Material p.u. 6 4 9 8

Total Other Materials Required 8820 10180 13500 16000 48500 48500

Cost per unit £10.00 £10.00 £10.00 £10.00

Total Cost of Other Material £88,200 £1,01,800 £1,35,000 £1,60,000 £4,85,000

Labour Hour p.u. 1.5 2.75 2 3.5

Total Labor Hours 2205 6998.75 3000 7000 19203.75 20000

Labour Cost per hour £25.00 £25.00 £25.00 £25.00

Total Labor Cost £55,125 £1,74,969 £75,000 £1,75,000 £4,80,094

Total Cost £3,49,125 £6,96,694 £4,50,000 £6,95,000 £21,90,819

Net Profit £5,32,875 £10,84,806 £9,00,000 £14,05,000 £39,22,681

Profit per unit £362.50 £426.25 £600.00 £702.50

11

BUSINESS

Formula View:

Particulars Square Round Rectangular Elliptic TOTAL Max. Input

Maximum Demand 3500 3000 1500 2000

Maximum Demand 1470 2545 1500 2000

Price 600 700 900 1050

Total Sales =B6*B8 =C6*C8 =D6*D8 =E6*E8 =SUM(B9:E9)

Wood per unit 11 12

Total Wood Required =C11*C6 =E11*E6 =SUM(B12:E12) 52000

Cost per unit 15 =C13

Total Cost of Wood =C12*C13 =E12*E13 =SUM(B14:E14)

Metal per unit 7 8

Total Metal Required =B16*B6 =D16*D6 =SUM(B17:E17) 36000

Cost per unit 20 =B18

Total Cost for Metal =B17*B18 =D17*D18 =SUM(B19:E19)

Other Material p.u. 6 4 9 8

Total Other Materials Required =B21*B6 =C21*C6 =D21*D6 =E21*E6 =SUM(B22:E22) 48500

Cost per unit 10 =B23 =C23 =D23

Total Cost of Other Material =B22*B23 =C22*C23 =D22*D23 =E22*E23 =SUM(B24:E24)

Labour Hour p.u. 1.5 =2+(3/4) 2 3.5

Total Labor Hours =B26*B6 =C26*C6 =D26*D6 =E26*E6 =SUM(B27:E27) 20000

Labour Cost per hour 25 =B28 =C28 =D28

Total Labor Cost =B28*B27 =C28*C27 =D28*D27 =E28*E27 =SUM(B29:E29)

Total Cost =B14+B19+B24+B29 =C14+C19+C24+C29 =D14+D19+D24+D29 =E14+E19+E24+E29 =SUM(B31:E31)

Net Profit =B9-B31 =C9-C31 =D9-D31 =E9-E31 =SUM(B33:E33)

Profit per unit =B33/B6 =C33/C6 =D33/D6 =E33/E6

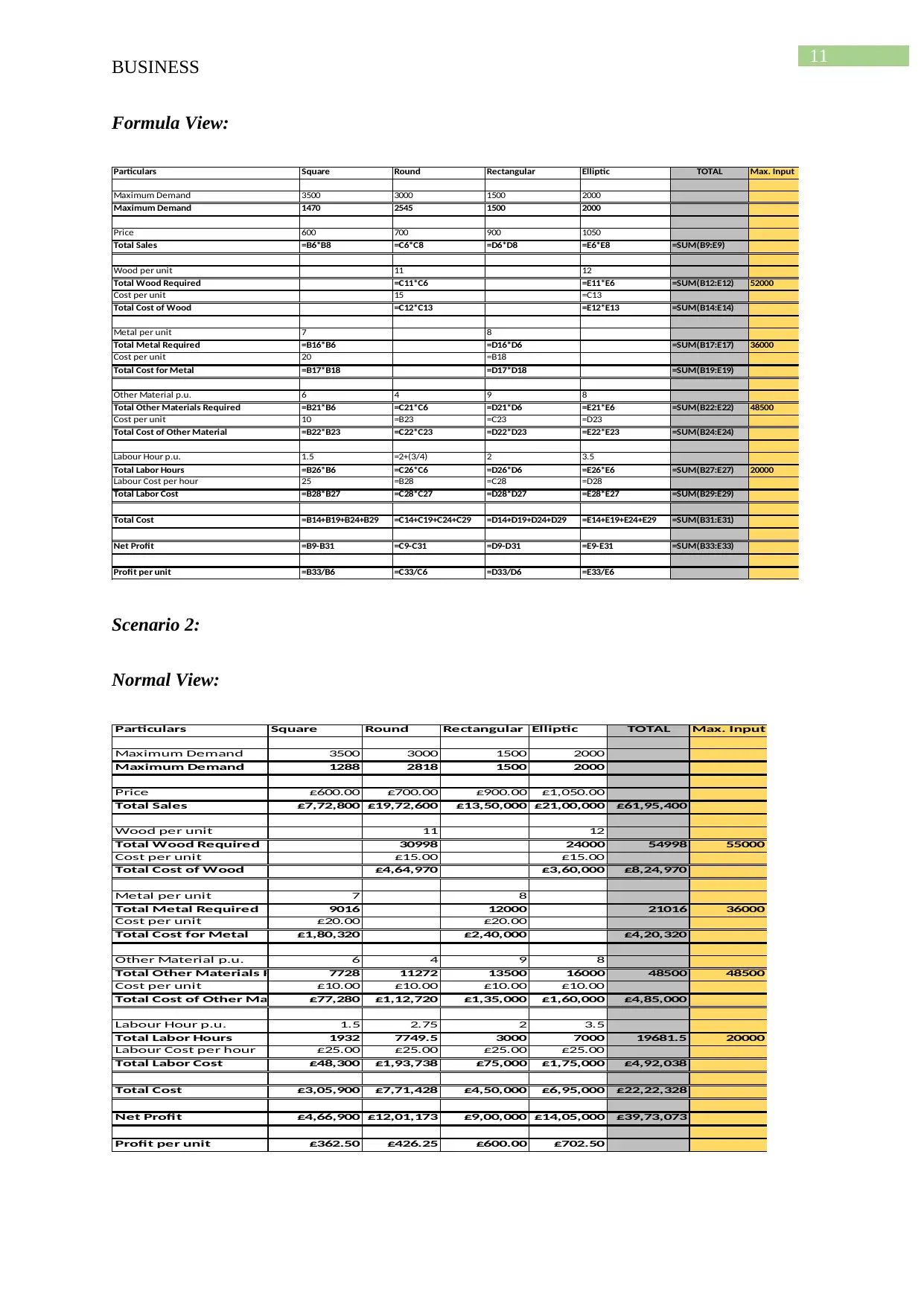

Scenario 2:

Normal View:

Particulars Square Round Rectangular Elliptic TOTAL Max. Input

Maximum Demand 3500 3000 1500 2000

Maximum Demand 1288 2818 1500 2000

Price £600.00 £700.00 £900.00 £1,050.00

Total Sales £7,72,800 £19,72,600 £13,50,000 £21,00,000 £61,95,400

Wood per unit 11 12

Total Wood Required 30998 24000 54998 55000

Cost per unit £15.00 £15.00

Total Cost of Wood £4,64,970 £3,60,000 £8,24,970

Metal per unit 7 8

Total Metal Required 9016 12000 21016 36000

Cost per unit £20.00 £20.00

Total Cost for Metal £1,80,320 £2,40,000 £4,20,320

Other Material p.u. 6 4 9 8

Total Other Materials Required 7728 11272 13500 16000 48500 48500

Cost per unit £10.00 £10.00 £10.00 £10.00

Total Cost of Other Material £77,280 £1,12,720 £1,35,000 £1,60,000 £4,85,000

Labour Hour p.u. 1.5 2.75 2 3.5

Total Labor Hours 1932 7749.5 3000 7000 19681.5 20000

Labour Cost per hour £25.00 £25.00 £25.00 £25.00

Total Labor Cost £48,300 £1,93,738 £75,000 £1,75,000 £4,92,038

Total Cost £3,05,900 £7,71,428 £4,50,000 £6,95,000 £22,22,328

Net Profit £4,66,900 £12,01,173 £9,00,000 £14,05,000 £39,73,073

Profit per unit £362.50 £426.25 £600.00 £702.50

BUSINESS

Formula View:

Particulars Square Round Rectangular Elliptic TOTAL Max. Input

Maximum Demand 3500 3000 1500 2000

Maximum Demand 1470 2545 1500 2000

Price 600 700 900 1050

Total Sales =B6*B8 =C6*C8 =D6*D8 =E6*E8 =SUM(B9:E9)

Wood per unit 11 12

Total Wood Required =C11*C6 =E11*E6 =SUM(B12:E12) 52000

Cost per unit 15 =C13

Total Cost of Wood =C12*C13 =E12*E13 =SUM(B14:E14)

Metal per unit 7 8

Total Metal Required =B16*B6 =D16*D6 =SUM(B17:E17) 36000

Cost per unit 20 =B18

Total Cost for Metal =B17*B18 =D17*D18 =SUM(B19:E19)

Other Material p.u. 6 4 9 8

Total Other Materials Required =B21*B6 =C21*C6 =D21*D6 =E21*E6 =SUM(B22:E22) 48500

Cost per unit 10 =B23 =C23 =D23

Total Cost of Other Material =B22*B23 =C22*C23 =D22*D23 =E22*E23 =SUM(B24:E24)

Labour Hour p.u. 1.5 =2+(3/4) 2 3.5

Total Labor Hours =B26*B6 =C26*C6 =D26*D6 =E26*E6 =SUM(B27:E27) 20000

Labour Cost per hour 25 =B28 =C28 =D28

Total Labor Cost =B28*B27 =C28*C27 =D28*D27 =E28*E27 =SUM(B29:E29)

Total Cost =B14+B19+B24+B29 =C14+C19+C24+C29 =D14+D19+D24+D29 =E14+E19+E24+E29 =SUM(B31:E31)

Net Profit =B9-B31 =C9-C31 =D9-D31 =E9-E31 =SUM(B33:E33)

Profit per unit =B33/B6 =C33/C6 =D33/D6 =E33/E6

Scenario 2:

Normal View:

Particulars Square Round Rectangular Elliptic TOTAL Max. Input

Maximum Demand 3500 3000 1500 2000

Maximum Demand 1288 2818 1500 2000

Price £600.00 £700.00 £900.00 £1,050.00

Total Sales £7,72,800 £19,72,600 £13,50,000 £21,00,000 £61,95,400

Wood per unit 11 12

Total Wood Required 30998 24000 54998 55000

Cost per unit £15.00 £15.00

Total Cost of Wood £4,64,970 £3,60,000 £8,24,970

Metal per unit 7 8

Total Metal Required 9016 12000 21016 36000

Cost per unit £20.00 £20.00

Total Cost for Metal £1,80,320 £2,40,000 £4,20,320

Other Material p.u. 6 4 9 8

Total Other Materials Required 7728 11272 13500 16000 48500 48500

Cost per unit £10.00 £10.00 £10.00 £10.00

Total Cost of Other Material £77,280 £1,12,720 £1,35,000 £1,60,000 £4,85,000

Labour Hour p.u. 1.5 2.75 2 3.5

Total Labor Hours 1932 7749.5 3000 7000 19681.5 20000

Labour Cost per hour £25.00 £25.00 £25.00 £25.00

Total Labor Cost £48,300 £1,93,738 £75,000 £1,75,000 £4,92,038

Total Cost £3,05,900 £7,71,428 £4,50,000 £6,95,000 £22,22,328

Net Profit £4,66,900 £12,01,173 £9,00,000 £14,05,000 £39,73,073

Profit per unit £362.50 £426.25 £600.00 £702.50

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 23

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.