Unit 2 Managing Financial Resources and Decision Making Report

VerifiedAdded on 2020/01/15

|23

|5627

|386

Report

AI Summary

This report provides a comprehensive analysis of financial resource management, focusing on a case study involving Sweet Menu Restaurant Ltd. The report begins by identifying and evaluating various sources of finance, including equity shares, retained earnings, loans, and third-party investments, along with their implications and costs. It then delves into the importance of financial planning, emphasizing the creation of cash budgets and the assessment of market trends to ensure financial stability. The report also examines the analysis of costs associated with different financing options, such as interest payments and lease rentals, and their tax implications. Furthermore, it covers the assessment of information needs for different decision-makers, the impact of finance on financial statements, budget analysis, unit cost calculations, pricing decisions, and the use of investment appraisal techniques to assess project viability. Finally, the report explains the content of financial statements, compares different formats for various business types, and interprets financial statements to provide a holistic understanding of financial management principles.

Unit 2 MANAGING FINANCIAL

RESORCES AND DECISION

1

RESORCES AND DECISION

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

1.1 Identification of sources of finance available to a business.............................................3

1.2 Implication of different sources of finance......................................................................4

1.3 Evaluation of appropriate sources of finance for a business project................................7

TASK 2............................................................................................................................................8

2.1 Analysis of costs of different sources of finance identified in task 1.3............................8

2.2 Importance of financial planning......................................................................................8

2.3 Assessing information needs of different decision makers..............................................9

2.4 Impact of finance on financial statements........................................................................9

TASK 3..........................................................................................................................................11

3.1 Analyzing budget and making appropriate decision......................................................11

3.2 Calculation of unit costs and making pricing decisions.................................................13

3.3 Assessing the viability of a project using investment appraisal techniques...................14

TASK 4..........................................................................................................................................15

4.1 Explain the content of Financial statement....................................................................15

4.2 Comparison between different formats of financial statements for different types of

business.................................................................................................................................16

4.3 Interpretation of financial statements.............................................................................19

CONCLUSION..............................................................................................................................21

REFERENCES..............................................................................................................................22

2

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

1.1 Identification of sources of finance available to a business.............................................3

1.2 Implication of different sources of finance......................................................................4

1.3 Evaluation of appropriate sources of finance for a business project................................7

TASK 2............................................................................................................................................8

2.1 Analysis of costs of different sources of finance identified in task 1.3............................8

2.2 Importance of financial planning......................................................................................8

2.3 Assessing information needs of different decision makers..............................................9

2.4 Impact of finance on financial statements........................................................................9

TASK 3..........................................................................................................................................11

3.1 Analyzing budget and making appropriate decision......................................................11

3.2 Calculation of unit costs and making pricing decisions.................................................13

3.3 Assessing the viability of a project using investment appraisal techniques...................14

TASK 4..........................................................................................................................................15

4.1 Explain the content of Financial statement....................................................................15

4.2 Comparison between different formats of financial statements for different types of

business.................................................................................................................................16

4.3 Interpretation of financial statements.............................................................................19

CONCLUSION..............................................................................................................................21

REFERENCES..............................................................................................................................22

2

INTRODUCTION

Management of financial resources means planning, organizing, controlling and directing

the financial activities of the organization. In simple words it means getting the most from the

resources available. It deals with procurement of financial resources from appropriate sources

and utilizing the same in an optimum manner. Effective and efficient management of financial

resources ensures long term growth and profitability of the organization and it will also ensure

adequate and regular supply of funds to the organization (Beck and Demirguc-Kunt, 2006).

Sweet menu restaurant ltd is a reputable restaurant and it was founded by three students

ten years ago. The owners of sweet menu want to open two new branches so as to take advantage

of this fast growing and dynamic food industry. According to its new business plan, it will

require £ 300000 to £ 500000 to open the proposed new branches. The present report

emphasizes on analyzing different sources of finance and their implications, costs of finance and

importance of financial planning for the sweet menu restaurant.

TASK 1

1.1 Identification of sources of finance available to a business.

Long Term Sources Of Finance Description

1. Issue of equity share capital

2. Retained earnings

3. Loans

A company can offer its shares to the general

public to raise huge amount of capital. Equity

shares are permanent in nature and equity

shareholders are considered as owners of the

company. Part of profits of the company is

distributed among equity shareholders (Baker and

Mukherjee, 2007).

These are earnings of the previous year’s which

were accumulated by the company instead of

distributing them as dividend.

Loans mean money borrowed by the company

from the financial institutions in exchange for

3

Management of financial resources means planning, organizing, controlling and directing

the financial activities of the organization. In simple words it means getting the most from the

resources available. It deals with procurement of financial resources from appropriate sources

and utilizing the same in an optimum manner. Effective and efficient management of financial

resources ensures long term growth and profitability of the organization and it will also ensure

adequate and regular supply of funds to the organization (Beck and Demirguc-Kunt, 2006).

Sweet menu restaurant ltd is a reputable restaurant and it was founded by three students

ten years ago. The owners of sweet menu want to open two new branches so as to take advantage

of this fast growing and dynamic food industry. According to its new business plan, it will

require £ 300000 to £ 500000 to open the proposed new branches. The present report

emphasizes on analyzing different sources of finance and their implications, costs of finance and

importance of financial planning for the sweet menu restaurant.

TASK 1

1.1 Identification of sources of finance available to a business.

Long Term Sources Of Finance Description

1. Issue of equity share capital

2. Retained earnings

3. Loans

A company can offer its shares to the general

public to raise huge amount of capital. Equity

shares are permanent in nature and equity

shareholders are considered as owners of the

company. Part of profits of the company is

distributed among equity shareholders (Baker and

Mukherjee, 2007).

These are earnings of the previous year’s which

were accumulated by the company instead of

distributing them as dividend.

Loans mean money borrowed by the company

from the financial institutions in exchange for

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

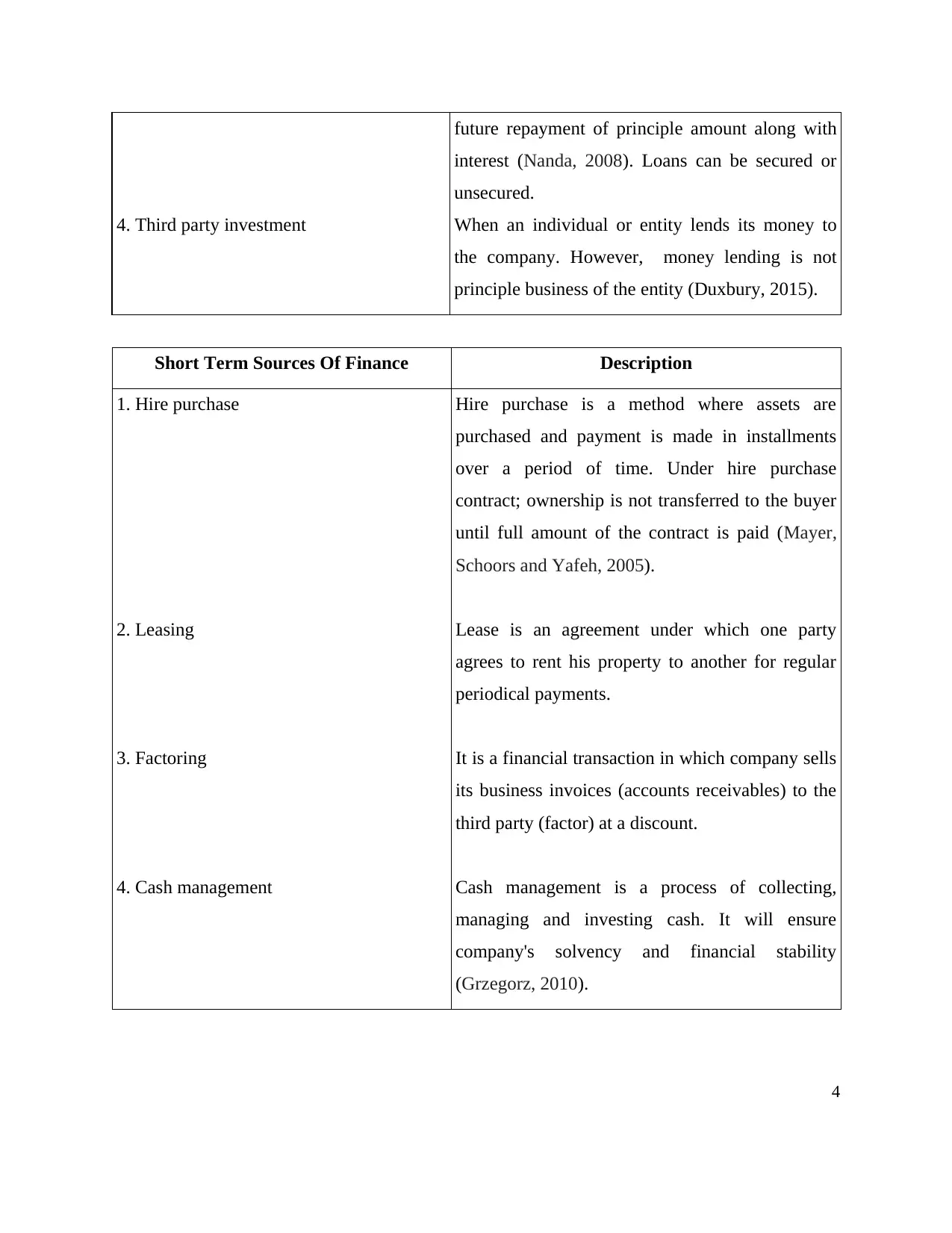

4. Third party investment

future repayment of principle amount along with

interest (Nanda, 2008). Loans can be secured or

unsecured.

When an individual or entity lends its money to

the company. However, money lending is not

principle business of the entity (Duxbury, 2015).

Short Term Sources Of Finance Description

1. Hire purchase

2. Leasing

3. Factoring

4. Cash management

Hire purchase is a method where assets are

purchased and payment is made in installments

over a period of time. Under hire purchase

contract; ownership is not transferred to the buyer

until full amount of the contract is paid (Mayer,

Schoors and Yafeh, 2005).

Lease is an agreement under which one party

agrees to rent his property to another for regular

periodical payments.

It is a financial transaction in which company sells

its business invoices (accounts receivables) to the

third party (factor) at a discount.

Cash management is a process of collecting,

managing and investing cash. It will ensure

company's solvency and financial stability

(Grzegorz, 2010).

4

future repayment of principle amount along with

interest (Nanda, 2008). Loans can be secured or

unsecured.

When an individual or entity lends its money to

the company. However, money lending is not

principle business of the entity (Duxbury, 2015).

Short Term Sources Of Finance Description

1. Hire purchase

2. Leasing

3. Factoring

4. Cash management

Hire purchase is a method where assets are

purchased and payment is made in installments

over a period of time. Under hire purchase

contract; ownership is not transferred to the buyer

until full amount of the contract is paid (Mayer,

Schoors and Yafeh, 2005).

Lease is an agreement under which one party

agrees to rent his property to another for regular

periodical payments.

It is a financial transaction in which company sells

its business invoices (accounts receivables) to the

third party (factor) at a discount.

Cash management is a process of collecting,

managing and investing cash. It will ensure

company's solvency and financial stability

(Grzegorz, 2010).

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1.2 Implication of different sources of finance

Sources of

finance

Legal implications Financial

implications

Dilution of

Control

Bankruptcy

implications

1.Equity Share

Capital

2.Retained

Earnings

3. Loans

Prior approval of

stock exchange is to

be obtained before

bringing initial public

offer in the market.

Moreover, the

company has to follow

all rules and

regulations formed by

governing body.

There are no legal

implications where a

company is utilizing

its free reserves.

Obtaining loans from

banks is very difficult

because banks lend to

only those companies

A company can

obtain huge funds

from the general

public by offering

them equity shares

and company has

to pay dividend to

its equity

shareholders

periodically.

If too much funds

are devoted from

the retained

earnings then it

will lower the

liquidity position.

Tax benefit can be

obtained on the

amount of interest

paid.

Ownership

control of the

company will

be diluted

among the

shareholders

(Lau and

Proimos, 2010).

No risk of

dilution of

control because

it is

reinvestment of

earnings of

past.

No risk of

dilution of

control because

lenders do not

There is no

risk of

bankruptcy in

case of

issuance of

equity shares

because it is

not liability of

the company

to repay the

funds to the

equity

shareholders.

This amount is

not added to

the debt

profile so there

is no risk of

bankruptcy.

There is high

risk of

bankruptcy

when company

5

Sources of

finance

Legal implications Financial

implications

Dilution of

Control

Bankruptcy

implications

1.Equity Share

Capital

2.Retained

Earnings

3. Loans

Prior approval of

stock exchange is to

be obtained before

bringing initial public

offer in the market.

Moreover, the

company has to follow

all rules and

regulations formed by

governing body.

There are no legal

implications where a

company is utilizing

its free reserves.

Obtaining loans from

banks is very difficult

because banks lend to

only those companies

A company can

obtain huge funds

from the general

public by offering

them equity shares

and company has

to pay dividend to

its equity

shareholders

periodically.

If too much funds

are devoted from

the retained

earnings then it

will lower the

liquidity position.

Tax benefit can be

obtained on the

amount of interest

paid.

Ownership

control of the

company will

be diluted

among the

shareholders

(Lau and

Proimos, 2010).

No risk of

dilution of

control because

it is

reinvestment of

earnings of

past.

No risk of

dilution of

control because

lenders do not

There is no

risk of

bankruptcy in

case of

issuance of

equity shares

because it is

not liability of

the company

to repay the

funds to the

equity

shareholders.

This amount is

not added to

the debt

profile so there

is no risk of

bankruptcy.

There is high

risk of

bankruptcy

when company

5

4.Third Party

Investment

5. Hire Purchase

6.Leasing

which are capable of

repaying their loans.

They also demand

valuable collateral as

security.

No legal implications.

Very easy to obtain

third party loan.

Contract between

vendor and purchaser

is to be properly

signed before

transaction.

Contract between both

the parties is to be

properly signed before

entering into lease

Usually they carry

low interest rates.

Purchaser has to

pay periodical

installments and

tax benefit can be

obtained on the

amount of interest

paid.

Lessee can use the

assets without

take ownership

position in the

company.

No risk of

dilution of

control.

No risk of

dilution of

control.

No risk of

dilution of

does not have

enough funds

for repayment

of loan

amount.

Usually fewer

amounts are

borrowed from

third parties so

no bankruptcy

implications

are involved.

Risk of

bankruptcy is

involved in

only those

cases where

large amount

of money is

involved in

hire purchase

transactions.

Repayment of

the principle

amount and

finance

6

Investment

5. Hire Purchase

6.Leasing

which are capable of

repaying their loans.

They also demand

valuable collateral as

security.

No legal implications.

Very easy to obtain

third party loan.

Contract between

vendor and purchaser

is to be properly

signed before

transaction.

Contract between both

the parties is to be

properly signed before

entering into lease

Usually they carry

low interest rates.

Purchaser has to

pay periodical

installments and

tax benefit can be

obtained on the

amount of interest

paid.

Lessee can use the

assets without

take ownership

position in the

company.

No risk of

dilution of

control.

No risk of

dilution of

control.

No risk of

dilution of

does not have

enough funds

for repayment

of loan

amount.

Usually fewer

amounts are

borrowed from

third parties so

no bankruptcy

implications

are involved.

Risk of

bankruptcy is

involved in

only those

cases where

large amount

of money is

involved in

hire purchase

transactions.

Repayment of

the principle

amount and

finance

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

7.Factoring

transaction.

An agreement is to be

signed between the

company and factor.

investing funds in

the assets. Tax

benefit can be

obtained on the

amount of interest

paid.

Factoring provides

quick boost to cash

flows. It is very

good source of

short term finance.

control.

No risk of

dilution of

control.

charges is

obligation for

the company

so there is high

risk of

bankruptcy.

No risk of

bankruptcy.

1.3 Evaluation of appropriate sources of finance for a business project.

Long term – Long term sources of finance available to Sweet Menu is issue of equity shares,

obtaining bank loan, third party investment etc. This option is viable only when company has

to invest large amount of funds for the expansion of its business. In this company has to

repay the principle amount along with interest usually in 10 – 20 years. High amount of

interest and dividends are involved in long term sources of finance. So company should go

for this option only when return from the project is higher than interest amount.

Short term – Short term sources of finance are hire purchase, leasing, factoring and cash

management etc. Usually these sources of finance last up to 5 years. Short term sources of

finance are obtained for meeting day to day expenses or purchasing new asset.

Sweet Menu wants to open new branches in different cities of UK. Therefore it can

obtain long term loans or it can also go for leasing option for financing land and buildings. Due

to good market reputation, no bank will hesitate in giving loan to Sweet Menu and it can also

easily repay the principle amount along with interest due to high sales. Sweet Menu can use its

retained earnings for meeting other expenses related to new branches.

7

transaction.

An agreement is to be

signed between the

company and factor.

investing funds in

the assets. Tax

benefit can be

obtained on the

amount of interest

paid.

Factoring provides

quick boost to cash

flows. It is very

good source of

short term finance.

control.

No risk of

dilution of

control.

charges is

obligation for

the company

so there is high

risk of

bankruptcy.

No risk of

bankruptcy.

1.3 Evaluation of appropriate sources of finance for a business project.

Long term – Long term sources of finance available to Sweet Menu is issue of equity shares,

obtaining bank loan, third party investment etc. This option is viable only when company has

to invest large amount of funds for the expansion of its business. In this company has to

repay the principle amount along with interest usually in 10 – 20 years. High amount of

interest and dividends are involved in long term sources of finance. So company should go

for this option only when return from the project is higher than interest amount.

Short term – Short term sources of finance are hire purchase, leasing, factoring and cash

management etc. Usually these sources of finance last up to 5 years. Short term sources of

finance are obtained for meeting day to day expenses or purchasing new asset.

Sweet Menu wants to open new branches in different cities of UK. Therefore it can

obtain long term loans or it can also go for leasing option for financing land and buildings. Due

to good market reputation, no bank will hesitate in giving loan to Sweet Menu and it can also

easily repay the principle amount along with interest due to high sales. Sweet Menu can use its

retained earnings for meeting other expenses related to new branches.

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TASK 2

2.1 Analysis of costs of different sources of finance identified in task 1.31. Retained earnings - When the company uses its retained earnings then the concept of

opportunity cost cannot be ignored. It means profits avoided by the company if it spend

those money in some other proposals There are no tax implications when company

utilizes its retained earnings (Brammer, Brooks and Pavelin, 2006).2. Loans and third party investments - Interest paid to the banks and third parties will be

cost of this source of finance. Interest cost is allowed as deduction from the profits of

company for the purpose of calculating tax.3. Hire purchase – Cost of hire purchase will be payment of interests charges to the vendor.

Interest charges will be allowed as deduction from the profits of company for the purpose

of calculating tax.4. Lease – Cost of the lease will be payment of periodical lease rentals to the lessor. Lease

rentals will be allowed as deduction from the profits of company for the purpose of

calculating tax.

2.2 Importance of financial planning

Sweet menu should try to adopt optimal capital structure because it will minimizes its cost of

finance and maximize the profitability of the company. It will also ensure adequacy of funds and

stability in the company. Following are the benefits of financial planning.

1. Financial planning ensures adequacy of funds in the organization.

2. Planning helps in maintaining reasonable balance between inflow and outflow of cash

and cash equivalents which ensures stability of the organization.

3. Planning helps in achieving optimal capital structure (Frank and Goyal, 2009).

One of the most important part of financial planning is preparation of cash budget. Cash

budget includes estimation of cash inflows and outflows which can highlight the company's

probable surplus or deficit position. So cash budget helps in planning the most efficient usage of

cash. Sweet menu wants to open new branches of its restaurant so company should prepare cash

budgets and carefully monitor the estimated cash inflows and outflows because it is very helpful

in projecting future profitability and stability of the company. Sweet menu should also consider

8

2.1 Analysis of costs of different sources of finance identified in task 1.31. Retained earnings - When the company uses its retained earnings then the concept of

opportunity cost cannot be ignored. It means profits avoided by the company if it spend

those money in some other proposals There are no tax implications when company

utilizes its retained earnings (Brammer, Brooks and Pavelin, 2006).2. Loans and third party investments - Interest paid to the banks and third parties will be

cost of this source of finance. Interest cost is allowed as deduction from the profits of

company for the purpose of calculating tax.3. Hire purchase – Cost of hire purchase will be payment of interests charges to the vendor.

Interest charges will be allowed as deduction from the profits of company for the purpose

of calculating tax.4. Lease – Cost of the lease will be payment of periodical lease rentals to the lessor. Lease

rentals will be allowed as deduction from the profits of company for the purpose of

calculating tax.

2.2 Importance of financial planning

Sweet menu should try to adopt optimal capital structure because it will minimizes its cost of

finance and maximize the profitability of the company. It will also ensure adequacy of funds and

stability in the company. Following are the benefits of financial planning.

1. Financial planning ensures adequacy of funds in the organization.

2. Planning helps in maintaining reasonable balance between inflow and outflow of cash

and cash equivalents which ensures stability of the organization.

3. Planning helps in achieving optimal capital structure (Frank and Goyal, 2009).

One of the most important part of financial planning is preparation of cash budget. Cash

budget includes estimation of cash inflows and outflows which can highlight the company's

probable surplus or deficit position. So cash budget helps in planning the most efficient usage of

cash. Sweet menu wants to open new branches of its restaurant so company should prepare cash

budgets and carefully monitor the estimated cash inflows and outflows because it is very helpful

in projecting future profitability and stability of the company. Sweet menu should also consider

8

the market trend. If the cash budget reflects negative cash flows then then it should not open that

particular branch.

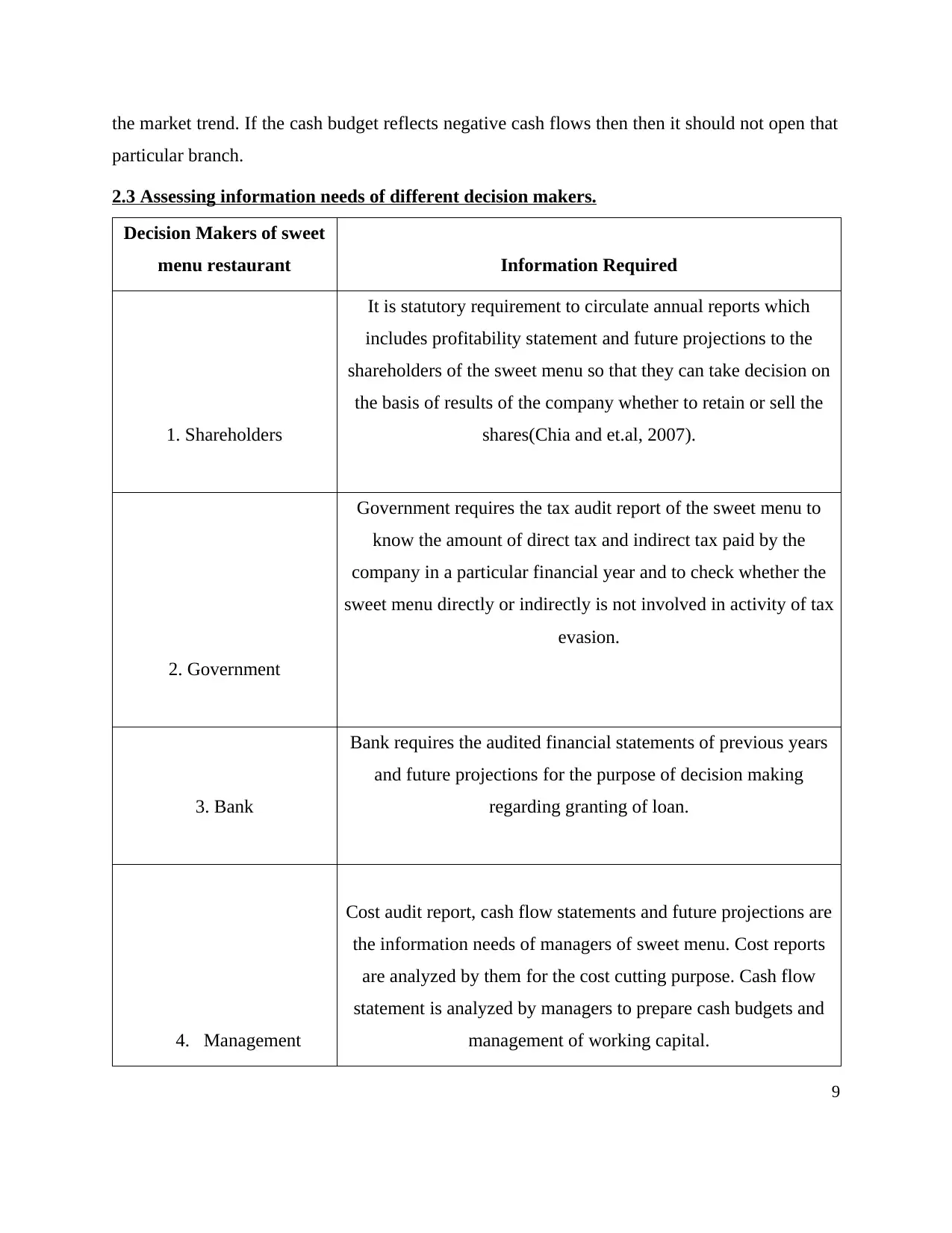

2.3 Assessing information needs of different decision makers.

Decision Makers of sweet

menu restaurant Information Required

1. Shareholders

It is statutory requirement to circulate annual reports which

includes profitability statement and future projections to the

shareholders of the sweet menu so that they can take decision on

the basis of results of the company whether to retain or sell the

shares(Chia and et.al, 2007).

2. Government

Government requires the tax audit report of the sweet menu to

know the amount of direct tax and indirect tax paid by the

company in a particular financial year and to check whether the

sweet menu directly or indirectly is not involved in activity of tax

evasion.

3. Bank

Bank requires the audited financial statements of previous years

and future projections for the purpose of decision making

regarding granting of loan.

4. Management

Cost audit report, cash flow statements and future projections are

the information needs of managers of sweet menu. Cost reports

are analyzed by them for the cost cutting purpose. Cash flow

statement is analyzed by managers to prepare cash budgets and

management of working capital.

9

particular branch.

2.3 Assessing information needs of different decision makers.

Decision Makers of sweet

menu restaurant Information Required

1. Shareholders

It is statutory requirement to circulate annual reports which

includes profitability statement and future projections to the

shareholders of the sweet menu so that they can take decision on

the basis of results of the company whether to retain or sell the

shares(Chia and et.al, 2007).

2. Government

Government requires the tax audit report of the sweet menu to

know the amount of direct tax and indirect tax paid by the

company in a particular financial year and to check whether the

sweet menu directly or indirectly is not involved in activity of tax

evasion.

3. Bank

Bank requires the audited financial statements of previous years

and future projections for the purpose of decision making

regarding granting of loan.

4. Management

Cost audit report, cash flow statements and future projections are

the information needs of managers of sweet menu. Cost reports

are analyzed by them for the cost cutting purpose. Cash flow

statement is analyzed by managers to prepare cash budgets and

management of working capital.

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

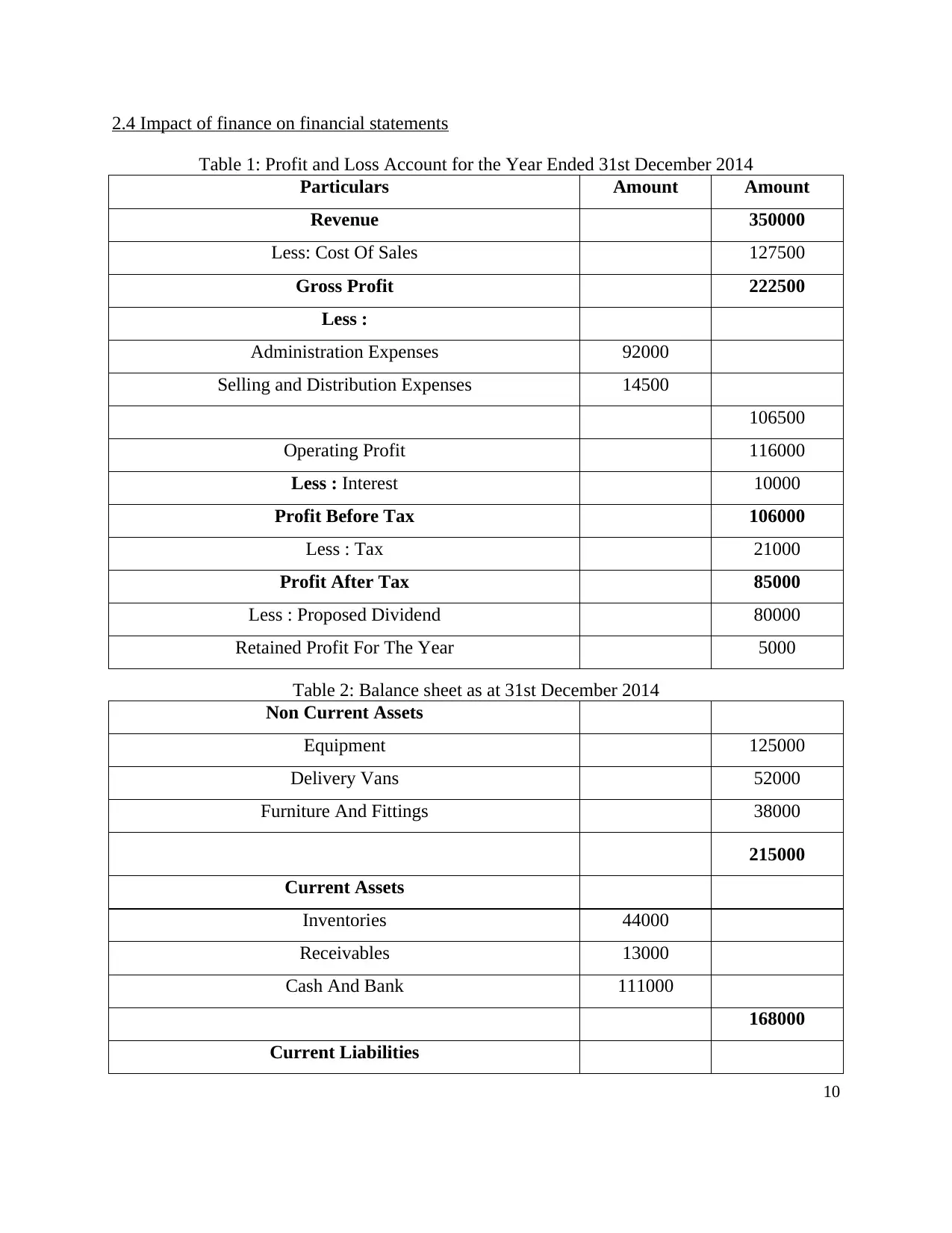

2.4 Impact of finance on financial statements

Table 1: Profit and Loss Account for the Year Ended 31st December 2014

Particulars Amount Amount

Revenue 350000

Less: Cost Of Sales 127500

Gross Profit 222500

Less :

Administration Expenses 92000

Selling and Distribution Expenses 14500

106500

Operating Profit 116000

Less : Interest 10000

Profit Before Tax 106000

Less : Tax 21000

Profit After Tax 85000

Less : Proposed Dividend 80000

Retained Profit For The Year 5000

Table 2: Balance sheet as at 31st December 2014

Non Current Assets

Equipment 125000

Delivery Vans 52000

Furniture And Fittings 38000

215000

Current Assets

Inventories 44000

Receivables 13000

Cash And Bank 111000

168000

Current Liabilities

10

Table 1: Profit and Loss Account for the Year Ended 31st December 2014

Particulars Amount Amount

Revenue 350000

Less: Cost Of Sales 127500

Gross Profit 222500

Less :

Administration Expenses 92000

Selling and Distribution Expenses 14500

106500

Operating Profit 116000

Less : Interest 10000

Profit Before Tax 106000

Less : Tax 21000

Profit After Tax 85000

Less : Proposed Dividend 80000

Retained Profit For The Year 5000

Table 2: Balance sheet as at 31st December 2014

Non Current Assets

Equipment 125000

Delivery Vans 52000

Furniture And Fittings 38000

215000

Current Assets

Inventories 44000

Receivables 13000

Cash And Bank 111000

168000

Current Liabilities

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Payables 38000

Net Current Assets 130000

Net Assets 345000

Equities

160000 Ordinary Share Capital @ GBP 1 per share 160000

Revenue Reserves 104000

Noncurrent liabilities

Long Term Loan 81000

Net Assets 345000

The company has issued equity share capital of GBP 100'000 so “equities” on the

liability side will be increased by GBP 100'000 and on the other hand cash/bank balance will be

increased by GBP 100'000.

Company has also obtained long term bank loan of GBP 50'000 so long term loans under

head noncurrent liabilities will be increased by GBP 50'000 and company utilizes those loans in

purchasing equipment so amount of equipment under head noncurrent assets will be increased by

GBP 50'000.

TASK 3

3.1 Analyzing budget and making appropriate decision

Cash Budget

Receipts

Septem

ber

£

Octobe

r

£

Novem

ber

£

Decem

ber

£

Total

£

Cash sales 15000 13000 15000 18000 58000

Total 15000 15500 18000 20000 58000

Payments

Van 12000 12000

Furniture & Fittings 18000 10000 28000

Salaries & wages 7500 7500 8500 9000 32500

11

Net Current Assets 130000

Net Assets 345000

Equities

160000 Ordinary Share Capital @ GBP 1 per share 160000

Revenue Reserves 104000

Noncurrent liabilities

Long Term Loan 81000

Net Assets 345000

The company has issued equity share capital of GBP 100'000 so “equities” on the

liability side will be increased by GBP 100'000 and on the other hand cash/bank balance will be

increased by GBP 100'000.

Company has also obtained long term bank loan of GBP 50'000 so long term loans under

head noncurrent liabilities will be increased by GBP 50'000 and company utilizes those loans in

purchasing equipment so amount of equipment under head noncurrent assets will be increased by

GBP 50'000.

TASK 3

3.1 Analyzing budget and making appropriate decision

Cash Budget

Receipts

Septem

ber

£

Octobe

r

£

Novem

ber

£

Decem

ber

£

Total

£

Cash sales 15000 13000 15000 18000 58000

Total 15000 15500 18000 20000 58000

Payments

Van 12000 12000

Furniture & Fittings 18000 10000 28000

Salaries & wages 7500 7500 8500 9000 32500

11

Petrol 280 280 280 840

Lighting &Energy 500 600 650 1750

Insurance 350 350 350 350 1400

Purchases - inventory 3000 3000 3500 4000 13500

Total 40850 11630 13230 24280 89990

Net balance (25850) 3870 4770 (4280) (21490)

Balance b/fwd 18500 (7350) (3480) 1290 8690

Balance c/fwd (7350) (3480) 1290 (2990)

(12530

)

Trade payables budget (Inventory)

Septem

ber

£

Octobe

r

£

Novem

ber

£

Decem

ber

£

August purchases 40% 1200

September purchases

60% 1800

September purchases

40% 1200

October purchases

60% 1800

October purchases

40% 1200

November purchases

60% 2300

November purchases

40% 1380

December purchases

40% 2620

12

Lighting &Energy 500 600 650 1750

Insurance 350 350 350 350 1400

Purchases - inventory 3000 3000 3500 4000 13500

Total 40850 11630 13230 24280 89990

Net balance (25850) 3870 4770 (4280) (21490)

Balance b/fwd 18500 (7350) (3480) 1290 8690

Balance c/fwd (7350) (3480) 1290 (2990)

(12530

)

Trade payables budget (Inventory)

Septem

ber

£

Octobe

r

£

Novem

ber

£

Decem

ber

£

August purchases 40% 1200

September purchases

60% 1800

September purchases

40% 1200

October purchases

60% 1800

October purchases

40% 1200

November purchases

60% 2300

November purchases

40% 1380

December purchases

40% 2620

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 23

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.