FNCE2000 Assignment: Capital Budgeting, Portfolio Analysis and CAPM

VerifiedAdded on 2022/08/16

|8

|1640

|19

Report

AI Summary

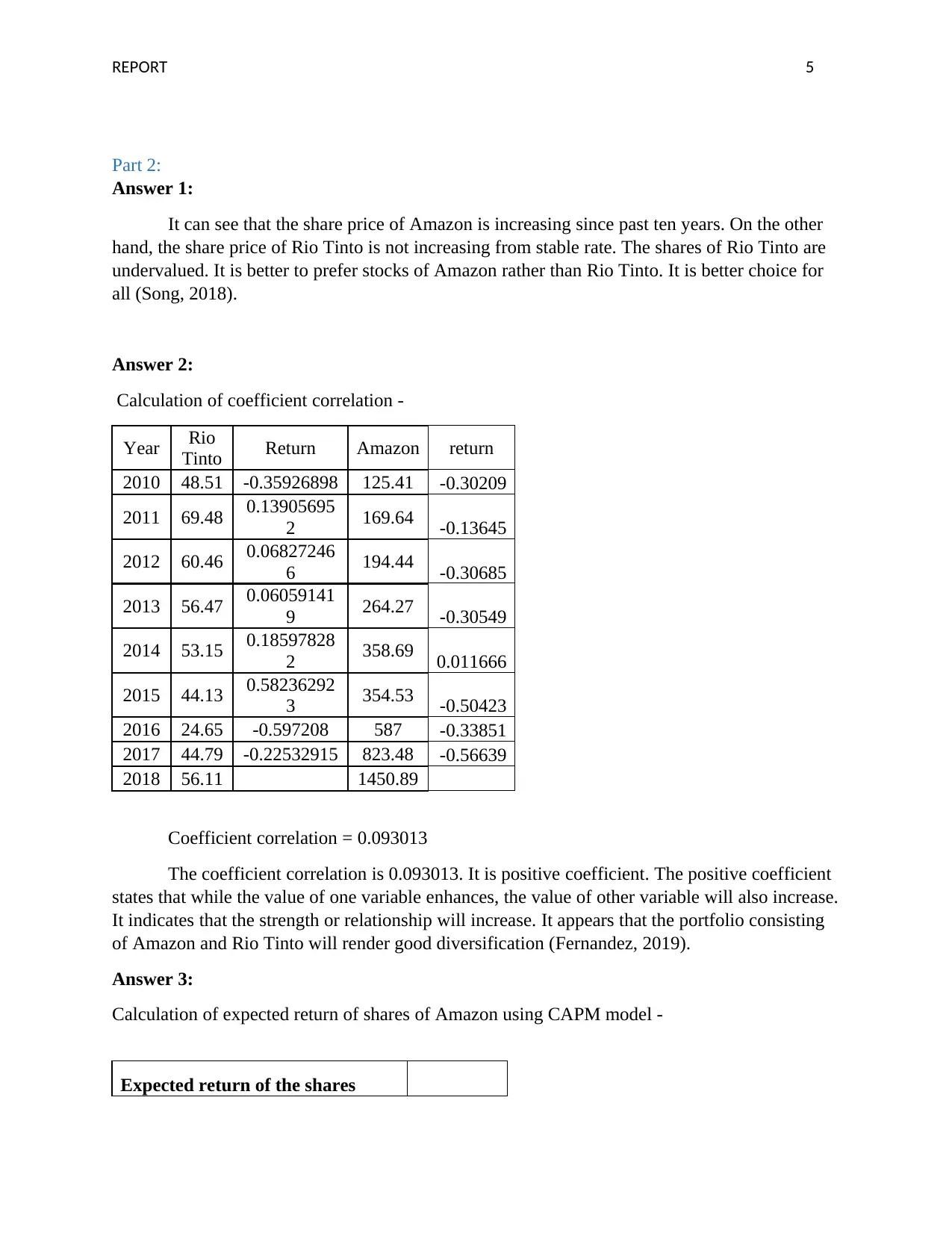

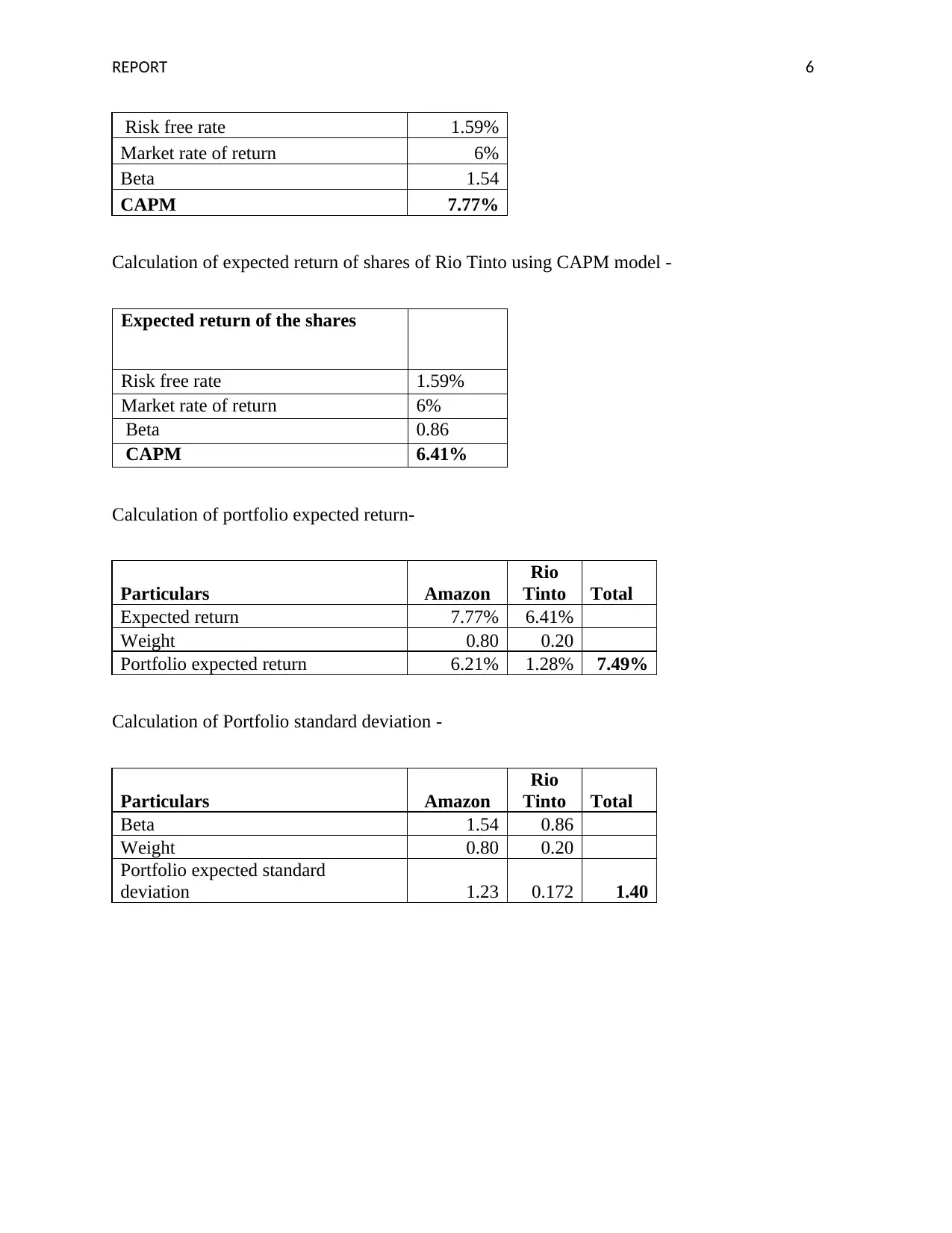

This finance report, prepared for FNCE2000, explores key financial concepts including capital budgeting, portfolio analysis, and the Capital Asset Pricing Model (CAPM). The report begins by examining relevant costs in capital budgeting decisions, calculating incremental free cash flow, and evaluating a new IT project using Net Present Value (NPV), Payback Period, and Internal Rate of Return (IRR). The second part of the report analyzes stock performance, calculating the correlation coefficient between Amazon and Rio Tinto, and applying the CAPM model to determine the expected return for these stocks. The report then calculates portfolio expected return and standard deviation, providing a comprehensive overview of financial analysis techniques. All calculations are presented with detailed working notes, making it a valuable resource for students studying finance principles.

1 out of 8

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.