Detailed Report: Finance Resource Management for Taste Business

VerifiedAdded on 2020/01/15

|24

|8520

|162

Report

AI Summary

This report provides a comprehensive analysis of financial resource management for Taste, a medium-sized catering business seeking expansion. It explores various sources of finance, including short-term options like bank overdrafts and leases, and long-term options like share capital, bank loans, and debentures, comparing the advantages and disadvantages of each. The report also examines financial statements (profit and loss, financial position, cash flow) and their impact, including ratio analysis, and discusses investment appraisal techniques like payback period and net present value. It provides recommendations for financing buildings and working capital, emphasizing the importance of financial planning, cash flow management, and the needs of financial statement users. The analysis culminates in advice to the Taste business on interpreting financial statements and making informed financial decisions for sustainable growth.

MANAGING FINANCE

RESOURCE DECISION

RESOURCE DECISION

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

1. INTRODUCTION..................................................................................................................1

2. Sources of finance..................................................................................................................1

AC 2.1 Type of businesses................................................................................................1

AC 2.2 sources available to business................................................................................1

AC 2.3 Comparison between rights issue and loan stocks...............................................3

AC 2.3.1 Rights Issue.......................................................................................................3

AC 2.3.2 Loan Stock.........................................................................................................3

AC 2.3.3 Comparison.......................................................................................................3

AC 2.4 Beneficial source of finance for the Buildings and noncurrent assets.................3

AC 2.5 Advice to the Board of Directors on finance source for working capital.............4

AC 2.5.1 Definition of working capital ...........................................................................4

AC 2.5.2 Importance of working capital..........................................................................4

AC 2.5.3 Sources available for working capital...............................................................4

3. Financial statements...............................................................................................................5

AC 3.1 Statement of profits or loss...................................................................................5

AC 3.2 Statement of financial position.............................................................................5

AC 3.3 statement of cash flow..........................................................................................5

AC 3.4 Impact on financial statements.............................................................................5

AC 3.4.2 Gearing ratio......................................................................................................7

AC 3.4.3 Impact of the financial plans on the financial statements.................................7

AC 3.5 Calculation of EPS...............................................................................................7

AC 3.5.1 Information........................................................................................................7

AC 3.5.2 Calculation of EPS............................................................................................7

AC 3.5.3 Explanation........................................................................................................8

TasK 4 INVEstment Appraisal...................................................................................................8

AC 4.1 Investment appraisal importance..........................................................................8

AC 4.2 Risk to future cash flows and future values vs. present value..............................8

AC 4.3 Types of techniques..............................................................................................9

AC 4.3.1 Pay back period.................................................................................................9

AC 4.3.2 Calculation and explanation of pay back period...............................................9

AC 4.3.3 Net present value...............................................................................................9

AC 4.3.4 Calculation and explanation of net present value...........................................10

1. INTRODUCTION..................................................................................................................1

2. Sources of finance..................................................................................................................1

AC 2.1 Type of businesses................................................................................................1

AC 2.2 sources available to business................................................................................1

AC 2.3 Comparison between rights issue and loan stocks...............................................3

AC 2.3.1 Rights Issue.......................................................................................................3

AC 2.3.2 Loan Stock.........................................................................................................3

AC 2.3.3 Comparison.......................................................................................................3

AC 2.4 Beneficial source of finance for the Buildings and noncurrent assets.................3

AC 2.5 Advice to the Board of Directors on finance source for working capital.............4

AC 2.5.1 Definition of working capital ...........................................................................4

AC 2.5.2 Importance of working capital..........................................................................4

AC 2.5.3 Sources available for working capital...............................................................4

3. Financial statements...............................................................................................................5

AC 3.1 Statement of profits or loss...................................................................................5

AC 3.2 Statement of financial position.............................................................................5

AC 3.3 statement of cash flow..........................................................................................5

AC 3.4 Impact on financial statements.............................................................................5

AC 3.4.2 Gearing ratio......................................................................................................7

AC 3.4.3 Impact of the financial plans on the financial statements.................................7

AC 3.5 Calculation of EPS...............................................................................................7

AC 3.5.1 Information........................................................................................................7

AC 3.5.2 Calculation of EPS............................................................................................7

AC 3.5.3 Explanation........................................................................................................8

TasK 4 INVEstment Appraisal...................................................................................................8

AC 4.1 Investment appraisal importance..........................................................................8

AC 4.2 Risk to future cash flows and future values vs. present value..............................8

AC 4.3 Types of techniques..............................................................................................9

AC 4.3.1 Pay back period.................................................................................................9

AC 4.3.2 Calculation and explanation of pay back period...............................................9

AC 4.3.3 Net present value...............................................................................................9

AC 4.3.4 Calculation and explanation of net present value...........................................10

AC 4.4 Recommendation for the investment opportunity..............................................10

AC 4.5 Unit cost.............................................................................................................11

AC 4.5.1 Importance of cost per unit and its calculation................................................11

AC 4.6 Factors to be considered while deciding the selling prices................................11

TASK 5 CASH FLOW VS. Profits..........................................................................................12

AC 5.1 Need of cash budget and trends of the Taste business budget...........................12

AC 5.2 Importance of financial planning.......................................................................13

AC 5.3 Liquidity problems with having proper availability of profits...........................13

AC 5.4 Users of the accounts..........................................................................................14

AC 5.4.1 Users................................................................................................................14

AC 5.4.2 Information need and importance....................................................................14

TASK 6 Interpretation of financial statements.........................................................................14

AC 6.1 Ratio Analysis....................................................................................................14

AC 6.1.1 Profitability ratio.............................................................................................15

AC 6.1.2 Liquidity ratio..................................................................................................15

AC 6.2 Advice to the Taste Business..............................................................................16

TASK 7 Financial statements of sole trader, partnership and limited companies...................16

Conclusion................................................................................................................................17

REFERENCES.........................................................................................................................18

AC 4.5 Unit cost.............................................................................................................11

AC 4.5.1 Importance of cost per unit and its calculation................................................11

AC 4.6 Factors to be considered while deciding the selling prices................................11

TASK 5 CASH FLOW VS. Profits..........................................................................................12

AC 5.1 Need of cash budget and trends of the Taste business budget...........................12

AC 5.2 Importance of financial planning.......................................................................13

AC 5.3 Liquidity problems with having proper availability of profits...........................13

AC 5.4 Users of the accounts..........................................................................................14

AC 5.4.1 Users................................................................................................................14

AC 5.4.2 Information need and importance....................................................................14

TASK 6 Interpretation of financial statements.........................................................................14

AC 6.1 Ratio Analysis....................................................................................................14

AC 6.1.1 Profitability ratio.............................................................................................15

AC 6.1.2 Liquidity ratio..................................................................................................15

AC 6.2 Advice to the Taste Business..............................................................................16

TASK 7 Financial statements of sole trader, partnership and limited companies...................16

Conclusion................................................................................................................................17

REFERENCES.........................................................................................................................18

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INDEX OF TABLES

Table 1: Calculation of enterprise value for computing WACC of 5, 00,000 shares................4

Table 2: Computation of WACC...............................................................................................4

Table 3: Calculation of enterprise value for computing WACC for loan stocks.......................5

Table 4: Calculation of WACC..................................................................................................5

Table 5: Calculation of enterprise value for computing WACC for stocks and loan................5

Table 6: Calculation of WACC.................................................................................................6

Table 7: Calculation of EPS.......................................................................................................6

Table 8: Calculation of cash flows.............................................................................................8

Table 9: Calculation of payback period.....................................................................................8

Table 10: Calculation of net present value.................................................................................8

Table 1: Calculation of enterprise value for computing WACC of 5, 00,000 shares................4

Table 2: Computation of WACC...............................................................................................4

Table 3: Calculation of enterprise value for computing WACC for loan stocks.......................5

Table 4: Calculation of WACC..................................................................................................5

Table 5: Calculation of enterprise value for computing WACC for stocks and loan................5

Table 6: Calculation of WACC.................................................................................................6

Table 7: Calculation of EPS.......................................................................................................6

Table 8: Calculation of cash flows.............................................................................................8

Table 9: Calculation of payback period.....................................................................................8

Table 10: Calculation of net present value.................................................................................8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1. INTRODUCTION

Managing financial resources is very important activity for the organization success.

Adequate availability and efficient management of finance resources helps business to

operate successfully. There are different sources available to the organizations for fulfilling

its finance requirement. Taste is a medium size company that want to expand its catering

business therefore business need finance requirement. Present report will helps us in

identifying the available short term as well as long term fund sources for the businesses. In

addition to it, organization needs to take decisions for pricing, investment and budgeting.

Therefore, the report describes the decision making process so as to take efficient and

strategic decisions. Investment appraisal techniques help the businesses to take effective

investment decisions that yield higher the profits. On contrary, the importance of financial

planning will have been discussed for achieving the organization objectives. Furthermore, the

preparation of financial statements helps companies to determine their operating and financial

performance. Business corporations can take better decisions by analysing and interpreting

their financial statements.

2. SOURCES OF FINANCE

AC 2.1 Type of businesses

Sole proprietorship: It is the most common form of business. Under this business

organization, only a single entrepreneur establishes the business hence, all the business

profits as well as losses are available for themselves.

Partnership: Under this form of business organization, two or more individual can

start the business operations. Therefore, all the business profits and losses are share in their

decided profit loss sharing ratio.

Company: It is a legal body that came into existence by following the companies act.

Shareholders are the owners of the company who make investment in the business and get the

return.

AC 2.2 sources available to business

In order to operate successfully business need to have adequate availability of

working capital. There are distinct sources available for fulfilling short term as well as long

term finance requirement that are explained below:

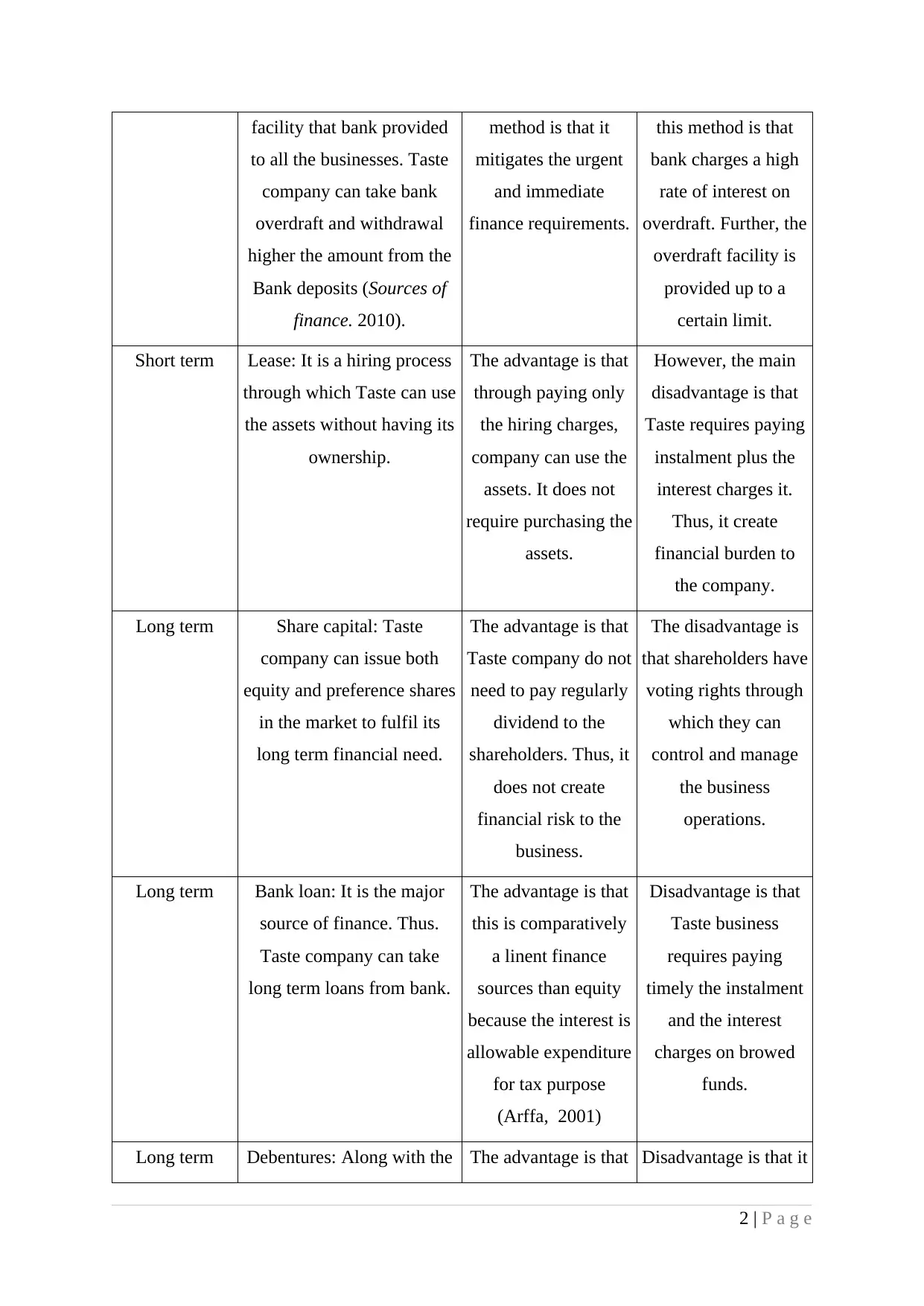

Sources Feature Advantage Disadvantage

Short term Bank Overdraft: It is a The advantage of this The disadvantage of

1 | P a g e

Managing financial resources is very important activity for the organization success.

Adequate availability and efficient management of finance resources helps business to

operate successfully. There are different sources available to the organizations for fulfilling

its finance requirement. Taste is a medium size company that want to expand its catering

business therefore business need finance requirement. Present report will helps us in

identifying the available short term as well as long term fund sources for the businesses. In

addition to it, organization needs to take decisions for pricing, investment and budgeting.

Therefore, the report describes the decision making process so as to take efficient and

strategic decisions. Investment appraisal techniques help the businesses to take effective

investment decisions that yield higher the profits. On contrary, the importance of financial

planning will have been discussed for achieving the organization objectives. Furthermore, the

preparation of financial statements helps companies to determine their operating and financial

performance. Business corporations can take better decisions by analysing and interpreting

their financial statements.

2. SOURCES OF FINANCE

AC 2.1 Type of businesses

Sole proprietorship: It is the most common form of business. Under this business

organization, only a single entrepreneur establishes the business hence, all the business

profits as well as losses are available for themselves.

Partnership: Under this form of business organization, two or more individual can

start the business operations. Therefore, all the business profits and losses are share in their

decided profit loss sharing ratio.

Company: It is a legal body that came into existence by following the companies act.

Shareholders are the owners of the company who make investment in the business and get the

return.

AC 2.2 sources available to business

In order to operate successfully business need to have adequate availability of

working capital. There are distinct sources available for fulfilling short term as well as long

term finance requirement that are explained below:

Sources Feature Advantage Disadvantage

Short term Bank Overdraft: It is a The advantage of this The disadvantage of

1 | P a g e

facility that bank provided

to all the businesses. Taste

company can take bank

overdraft and withdrawal

higher the amount from the

Bank deposits (Sources of

finance. 2010).

method is that it

mitigates the urgent

and immediate

finance requirements.

this method is that

bank charges a high

rate of interest on

overdraft. Further, the

overdraft facility is

provided up to a

certain limit.

Short term Lease: It is a hiring process

through which Taste can use

the assets without having its

ownership.

The advantage is that

through paying only

the hiring charges,

company can use the

assets. It does not

require purchasing the

assets.

However, the main

disadvantage is that

Taste requires paying

instalment plus the

interest charges it.

Thus, it create

financial burden to

the company.

Long term Share capital: Taste

company can issue both

equity and preference shares

in the market to fulfil its

long term financial need.

The advantage is that

Taste company do not

need to pay regularly

dividend to the

shareholders. Thus, it

does not create

financial risk to the

business.

The disadvantage is

that shareholders have

voting rights through

which they can

control and manage

the business

operations.

Long term Bank loan: It is the major

source of finance. Thus.

Taste company can take

long term loans from bank.

The advantage is that

this is comparatively

a linent finance

sources than equity

because the interest is

allowable expenditure

for tax purpose

(Arffa, 2001)

Disadvantage is that

Taste business

requires paying

timely the instalment

and the interest

charges on browed

funds.

Long term Debentures: Along with the The advantage is that Disadvantage is that it

2 | P a g e

to all the businesses. Taste

company can take bank

overdraft and withdrawal

higher the amount from the

Bank deposits (Sources of

finance. 2010).

method is that it

mitigates the urgent

and immediate

finance requirements.

this method is that

bank charges a high

rate of interest on

overdraft. Further, the

overdraft facility is

provided up to a

certain limit.

Short term Lease: It is a hiring process

through which Taste can use

the assets without having its

ownership.

The advantage is that

through paying only

the hiring charges,

company can use the

assets. It does not

require purchasing the

assets.

However, the main

disadvantage is that

Taste requires paying

instalment plus the

interest charges it.

Thus, it create

financial burden to

the company.

Long term Share capital: Taste

company can issue both

equity and preference shares

in the market to fulfil its

long term financial need.

The advantage is that

Taste company do not

need to pay regularly

dividend to the

shareholders. Thus, it

does not create

financial risk to the

business.

The disadvantage is

that shareholders have

voting rights through

which they can

control and manage

the business

operations.

Long term Bank loan: It is the major

source of finance. Thus.

Taste company can take

long term loans from bank.

The advantage is that

this is comparatively

a linent finance

sources than equity

because the interest is

allowable expenditure

for tax purpose

(Arffa, 2001)

Disadvantage is that

Taste business

requires paying

timely the instalment

and the interest

charges on browed

funds.

Long term Debentures: Along with the The advantage is that Disadvantage is that it

2 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

share capital, Taste

company can also issue

debentures for getting funds.

it fulfils the financial

requirement to a great

extent. Therefore,

Taste can use this

source to acquire

larger the funds.

create fixed financial

burden to the

company. The reason

behind that is Taste

business requires to

pay timely interest to

the debenture holders.

AC 2.3 Comparison between rights issue and loan stocks

AC 2.3.1 Rights Issue

Right issue: It is a way of raising the equity capital of the business. It is an offer and

invitation to the existing shareholders to purchase new shares proportionate to their holdings.

Equity is an instrument for issuing rights to the shareholders.

AC 2.3.2 Loan Stock

Loan stock: Debenture is the instrument for acquiring loan stock which is an

acknowledgement of company's debt capital. It is a long term debt capital on which

businesses requires paying interest.

AC 2.3.3 Comparison

There are many advantages and disadvantages of issuing rights to the shareholders. In

context to Taste business, one of the main advantages for the company is that it does not

require making any payments as it is not the borrowings. Further, it can increase the business

credit rating therefore; company can take borrowings easier in future period. However, the

disadvantage is that it provides ownership to the shareholders (Baum and Crosby, 2014).

Thus, they have rights to take part in business decisions. Further, they invest their funds with

the purpose of getting higher the return. Therefore Taste company need to pay dividend

payments. Further, in case of any default it can hurt the business reputation and share prices

in an adverse manner. However, The advantage of the loan stock is that bondholders have not

any controlling rights hence; they cannot take part in the business management. Moreover,

the interest payment is deducted for computing tax (Burton, 2007). On contrary, the

disadvantage is that Taste company need to pay fixed interest payment periodically.

Therefore, it brings fixed financial burden to the company. Thus, it may create cash flow

problems and reduce profitability.

3 | P a g e

company can also issue

debentures for getting funds.

it fulfils the financial

requirement to a great

extent. Therefore,

Taste can use this

source to acquire

larger the funds.

create fixed financial

burden to the

company. The reason

behind that is Taste

business requires to

pay timely interest to

the debenture holders.

AC 2.3 Comparison between rights issue and loan stocks

AC 2.3.1 Rights Issue

Right issue: It is a way of raising the equity capital of the business. It is an offer and

invitation to the existing shareholders to purchase new shares proportionate to their holdings.

Equity is an instrument for issuing rights to the shareholders.

AC 2.3.2 Loan Stock

Loan stock: Debenture is the instrument for acquiring loan stock which is an

acknowledgement of company's debt capital. It is a long term debt capital on which

businesses requires paying interest.

AC 2.3.3 Comparison

There are many advantages and disadvantages of issuing rights to the shareholders. In

context to Taste business, one of the main advantages for the company is that it does not

require making any payments as it is not the borrowings. Further, it can increase the business

credit rating therefore; company can take borrowings easier in future period. However, the

disadvantage is that it provides ownership to the shareholders (Baum and Crosby, 2014).

Thus, they have rights to take part in business decisions. Further, they invest their funds with

the purpose of getting higher the return. Therefore Taste company need to pay dividend

payments. Further, in case of any default it can hurt the business reputation and share prices

in an adverse manner. However, The advantage of the loan stock is that bondholders have not

any controlling rights hence; they cannot take part in the business management. Moreover,

the interest payment is deducted for computing tax (Burton, 2007). On contrary, the

disadvantage is that Taste company need to pay fixed interest payment periodically.

Therefore, it brings fixed financial burden to the company. Thus, it may create cash flow

problems and reduce profitability.

3 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

AC 2.4 Beneficial source of finance for the Buildings and noncurrent assets

As per the scenario, Taste wants to expand its business in market therefore the

company require to invest £1000000 in building and other noncurrent assets. On the basis of

above mentioned benefits and disadvantages, it can be advised to Taste business that issuing

loan stocks will be more beneficial finance source. Company can issue debt capital and invest

acquired funds in the building and its noncurrent assets (Cowton, 2004). The reason for such

decision is that scenario indicate that Taste business have good track record and growing

continuously over the past six years. Thus, it is clear that company is financially strong and

having adequate availability of profits. Therefore, Taste business can bear fixed financial

burden for making timely interest payments. Further, by doing that, business do not require

diversifying its controlling rights and managing its operations on its own basis. Moreover,

Taste can acquire funds at easier the rate helps to minimize the finance cost and increase the

business profits (Fridson and Alvarez, 2011). Another benefit will be that the interest

payments made by Taste will be deducted so as to calculate business tax liability and reduce

the tax payments.

AC 2.5 Advice to the Board of Directors on finance source for working capital

AC 2.5.1 Definition of working capital

The type of capital that is needed to run business operating functions is known as

working capital. The need for working capital arises for operational purpose.

AC 2.5.2 Importance of working capital

The need for working capital arises for operational purpose. Every business

organization needs adequate availability of working capital to run business operations in an

effective manner.

AC 2.5.3 Sources available for working capital

As disused earlier, it is clear that both short term and long term finance sources are

available for fulfil Taste business working capital need. Under the short term finance sources,

bank overdraft and lease sources are available to the company. However, loan capital,

debentures and share capital are available as long term sources (Gonenc, 2005). On the basis

of above information it can be concluded that share capital will be the best finance source for

Taste Company. Company can issue shares in the market and get the required funds. The

reason for such decision is that company do not require paying regular payment of dividend

to the shareholders. Further, company is growing continuously in the market therefore it can

easily attract the investors due to higher the profitability (Gotze, Northcott and Schuster,

4 | P a g e

As per the scenario, Taste wants to expand its business in market therefore the

company require to invest £1000000 in building and other noncurrent assets. On the basis of

above mentioned benefits and disadvantages, it can be advised to Taste business that issuing

loan stocks will be more beneficial finance source. Company can issue debt capital and invest

acquired funds in the building and its noncurrent assets (Cowton, 2004). The reason for such

decision is that scenario indicate that Taste business have good track record and growing

continuously over the past six years. Thus, it is clear that company is financially strong and

having adequate availability of profits. Therefore, Taste business can bear fixed financial

burden for making timely interest payments. Further, by doing that, business do not require

diversifying its controlling rights and managing its operations on its own basis. Moreover,

Taste can acquire funds at easier the rate helps to minimize the finance cost and increase the

business profits (Fridson and Alvarez, 2011). Another benefit will be that the interest

payments made by Taste will be deducted so as to calculate business tax liability and reduce

the tax payments.

AC 2.5 Advice to the Board of Directors on finance source for working capital

AC 2.5.1 Definition of working capital

The type of capital that is needed to run business operating functions is known as

working capital. The need for working capital arises for operational purpose.

AC 2.5.2 Importance of working capital

The need for working capital arises for operational purpose. Every business

organization needs adequate availability of working capital to run business operations in an

effective manner.

AC 2.5.3 Sources available for working capital

As disused earlier, it is clear that both short term and long term finance sources are

available for fulfil Taste business working capital need. Under the short term finance sources,

bank overdraft and lease sources are available to the company. However, loan capital,

debentures and share capital are available as long term sources (Gonenc, 2005). On the basis

of above information it can be concluded that share capital will be the best finance source for

Taste Company. Company can issue shares in the market and get the required funds. The

reason for such decision is that company do not require paying regular payment of dividend

to the shareholders. Further, company is growing continuously in the market therefore it can

easily attract the investors due to higher the profitability (Gotze, Northcott and Schuster,

4 | P a g e

2007). Moreover, through providing regular return, Taste business can enhance its share

prices and credit rating. This in turn, business can enjoy long term success and sustainability.

3. FINANCIAL STATEMENTS

AC 3.1 Statement of profits or loss

Profit or loss is a profitability statement that helps to determine the operational result

of the business. All the business expenditures and incomes are shown in profit or loss

account. It determines the business operational performance through determining profits or

loss.

AC 3.2 Statement of financial position

Balance sheet is known as statement of financial position. It combines all the business

assets and liabilities so as to determine the financial position. Assets include all the fixed,

current and noncurrent assets. However, balance sheet involves the current liabilities, long

term debt and equity capital. Financial performance can be determined through the balance

sheet.

AC 3.3 statement of cash flow

Cash flow statement: It combines all the cash incomes and cash expenditures. Cash

incomes are the cash sources whereas cash expenditures indicate the application of cash

funds. The purpose of the statement is to determine the cash changes between two balance

sheet dates. Cash flow from operating activities determined so as to identify the cash earning

capacity. Cash flow from investing activities indicate the acquisition and selling of business

assets. In addition to it, cash flow from financing activities identifies the sources through

which funds are generated and payment made to them.

AC 3.4 Impact on financial statements

AC 3.4.1 Weighted average cost of capital

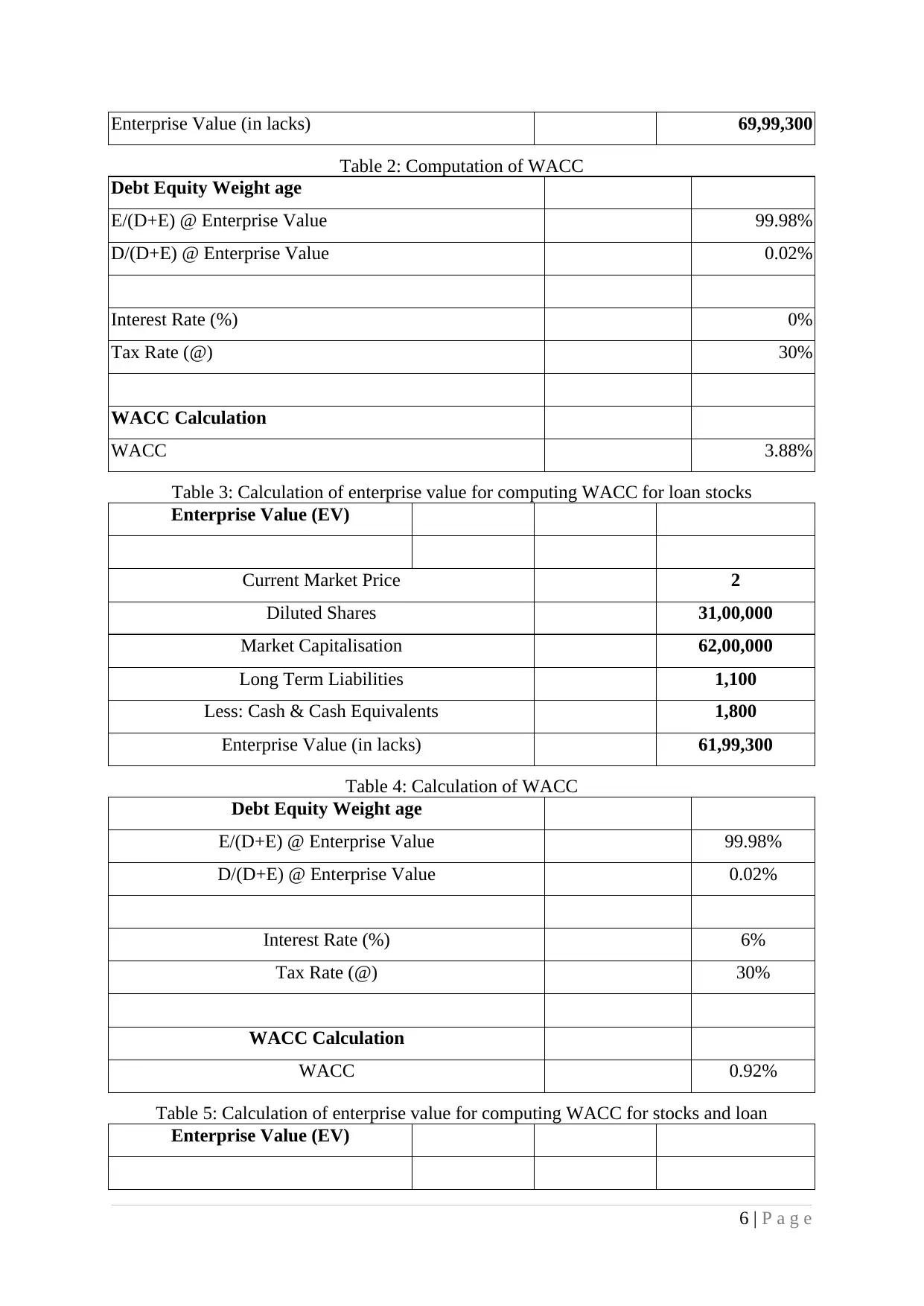

Table 1: Calculation of enterprise value for computing WACC of 5, 00,000 shares

Enterprise Value (EV)

Current Market Price 2

Diluted Shares 35,00,000

Market Capitalisation 70,00,000

Long Term Liabilities 1,100

Less: Cash & Cash Equivalents 1,800

5 | P a g e

prices and credit rating. This in turn, business can enjoy long term success and sustainability.

3. FINANCIAL STATEMENTS

AC 3.1 Statement of profits or loss

Profit or loss is a profitability statement that helps to determine the operational result

of the business. All the business expenditures and incomes are shown in profit or loss

account. It determines the business operational performance through determining profits or

loss.

AC 3.2 Statement of financial position

Balance sheet is known as statement of financial position. It combines all the business

assets and liabilities so as to determine the financial position. Assets include all the fixed,

current and noncurrent assets. However, balance sheet involves the current liabilities, long

term debt and equity capital. Financial performance can be determined through the balance

sheet.

AC 3.3 statement of cash flow

Cash flow statement: It combines all the cash incomes and cash expenditures. Cash

incomes are the cash sources whereas cash expenditures indicate the application of cash

funds. The purpose of the statement is to determine the cash changes between two balance

sheet dates. Cash flow from operating activities determined so as to identify the cash earning

capacity. Cash flow from investing activities indicate the acquisition and selling of business

assets. In addition to it, cash flow from financing activities identifies the sources through

which funds are generated and payment made to them.

AC 3.4 Impact on financial statements

AC 3.4.1 Weighted average cost of capital

Table 1: Calculation of enterprise value for computing WACC of 5, 00,000 shares

Enterprise Value (EV)

Current Market Price 2

Diluted Shares 35,00,000

Market Capitalisation 70,00,000

Long Term Liabilities 1,100

Less: Cash & Cash Equivalents 1,800

5 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Enterprise Value (in lacks) 69,99,300

Table 2: Computation of WACC

Debt Equity Weight age

E/(D+E) @ Enterprise Value 99.98%

D/(D+E) @ Enterprise Value 0.02%

Interest Rate (%) 0%

Tax Rate (@) 30%

WACC Calculation

WACC 3.88%

Table 3: Calculation of enterprise value for computing WACC for loan stocks

Enterprise Value (EV)

Current Market Price 2

Diluted Shares 31,00,000

Market Capitalisation 62,00,000

Long Term Liabilities 1,100

Less: Cash & Cash Equivalents 1,800

Enterprise Value (in lacks) 61,99,300

Table 4: Calculation of WACC

Debt Equity Weight age

E/(D+E) @ Enterprise Value 99.98%

D/(D+E) @ Enterprise Value 0.02%

Interest Rate (%) 6%

Tax Rate (@) 30%

WACC Calculation

WACC 0.92%

Table 5: Calculation of enterprise value for computing WACC for stocks and loan

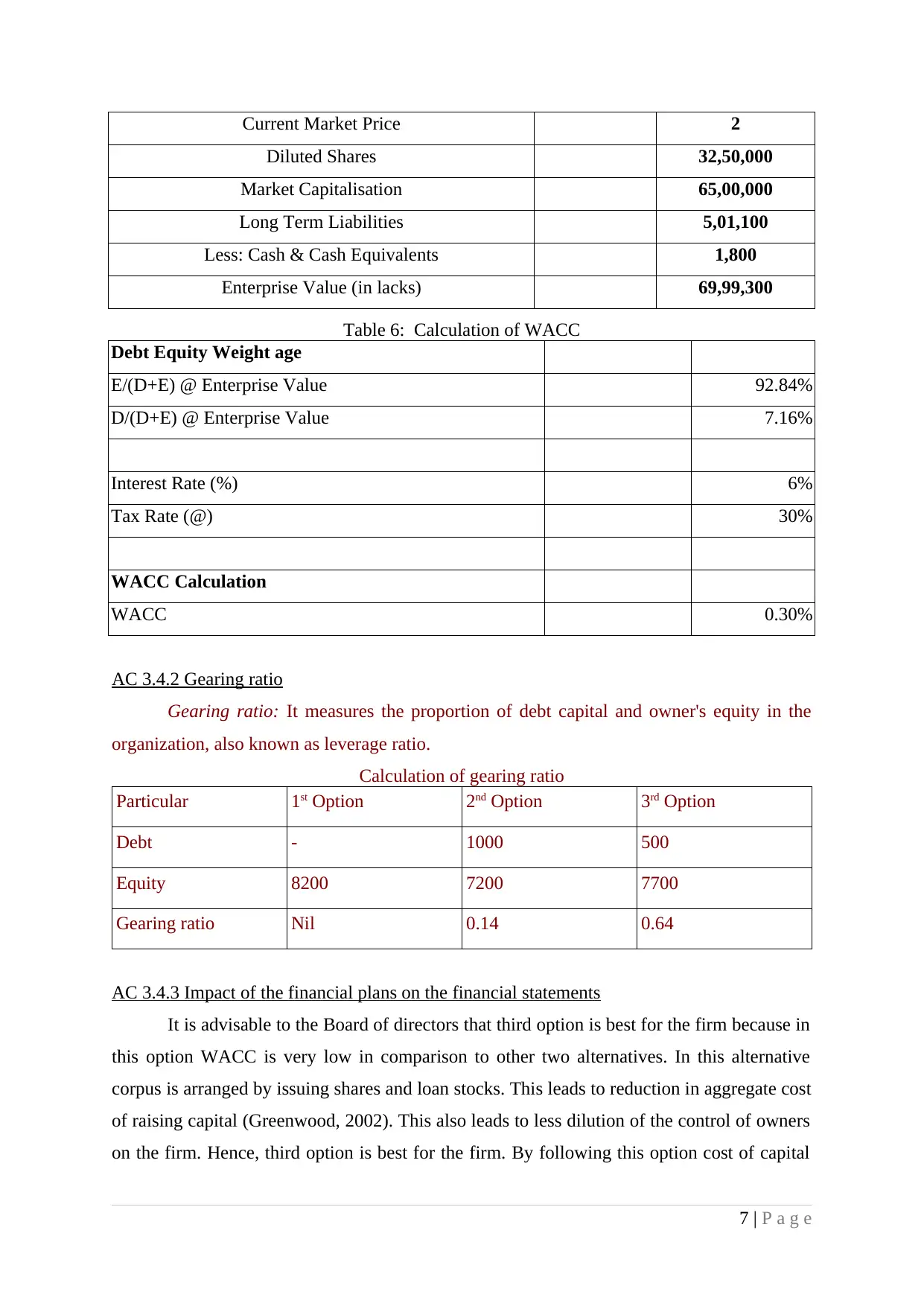

Enterprise Value (EV)

6 | P a g e

Table 2: Computation of WACC

Debt Equity Weight age

E/(D+E) @ Enterprise Value 99.98%

D/(D+E) @ Enterprise Value 0.02%

Interest Rate (%) 0%

Tax Rate (@) 30%

WACC Calculation

WACC 3.88%

Table 3: Calculation of enterprise value for computing WACC for loan stocks

Enterprise Value (EV)

Current Market Price 2

Diluted Shares 31,00,000

Market Capitalisation 62,00,000

Long Term Liabilities 1,100

Less: Cash & Cash Equivalents 1,800

Enterprise Value (in lacks) 61,99,300

Table 4: Calculation of WACC

Debt Equity Weight age

E/(D+E) @ Enterprise Value 99.98%

D/(D+E) @ Enterprise Value 0.02%

Interest Rate (%) 6%

Tax Rate (@) 30%

WACC Calculation

WACC 0.92%

Table 5: Calculation of enterprise value for computing WACC for stocks and loan

Enterprise Value (EV)

6 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Current Market Price 2

Diluted Shares 32,50,000

Market Capitalisation 65,00,000

Long Term Liabilities 5,01,100

Less: Cash & Cash Equivalents 1,800

Enterprise Value (in lacks) 69,99,300

Table 6: Calculation of WACC

Debt Equity Weight age

E/(D+E) @ Enterprise Value 92.84%

D/(D+E) @ Enterprise Value 7.16%

Interest Rate (%) 6%

Tax Rate (@) 30%

WACC Calculation

WACC 0.30%

AC 3.4.2 Gearing ratio

Gearing ratio: It measures the proportion of debt capital and owner's equity in the

organization, also known as leverage ratio.

Calculation of gearing ratio

Particular 1st Option 2nd Option 3rd Option

Debt - 1000 500

Equity 8200 7200 7700

Gearing ratio Nil 0.14 0.64

AC 3.4.3 Impact of the financial plans on the financial statements

It is advisable to the Board of directors that third option is best for the firm because in

this option WACC is very low in comparison to other two alternatives. In this alternative

corpus is arranged by issuing shares and loan stocks. This leads to reduction in aggregate cost

of raising capital (Greenwood, 2002). This also leads to less dilution of the control of owners

on the firm. Hence, third option is best for the firm. By following this option cost of capital

7 | P a g e

Diluted Shares 32,50,000

Market Capitalisation 65,00,000

Long Term Liabilities 5,01,100

Less: Cash & Cash Equivalents 1,800

Enterprise Value (in lacks) 69,99,300

Table 6: Calculation of WACC

Debt Equity Weight age

E/(D+E) @ Enterprise Value 92.84%

D/(D+E) @ Enterprise Value 7.16%

Interest Rate (%) 6%

Tax Rate (@) 30%

WACC Calculation

WACC 0.30%

AC 3.4.2 Gearing ratio

Gearing ratio: It measures the proportion of debt capital and owner's equity in the

organization, also known as leverage ratio.

Calculation of gearing ratio

Particular 1st Option 2nd Option 3rd Option

Debt - 1000 500

Equity 8200 7200 7700

Gearing ratio Nil 0.14 0.64

AC 3.4.3 Impact of the financial plans on the financial statements

It is advisable to the Board of directors that third option is best for the firm because in

this option WACC is very low in comparison to other two alternatives. In this alternative

corpus is arranged by issuing shares and loan stocks. This leads to reduction in aggregate cost

of raising capital (Greenwood, 2002). This also leads to less dilution of the control of owners

on the firm. Hence, third option is best for the firm. By following this option cost of capital

7 | P a g e

will reduced which will lead to less reduction in profitability. Hence, this will benefit to the

shareholders in terms of dividend receipt from the company.

These financial plans to large extent will affect firm financial statements. If shares are

issued alone then shareholder equity will increase. In other words, it can be said that liability

side will increase in the balance sheet. If loan stocks and ordinary shares are issued then long

term loan amount will increase in balance sheet and shareholder equity will also increase in

same (Ho, Liu and Tsay, 2008). If loan shares are issued then ordinary shares and loan

amount will increase in the liability side of balance sheet.

AC 3.5 Calculation of EPS

AC 3.5.1 Information

Earning per share indicate the shareholders return on each share. All the business

shareholders have the objective of getting larger the return on their invested funds. Thus, it is

important for the companies to provide increased return to the shareholders.

AC 3.5.2 Calculation of EPS

Table 7: Calculation of EPS

PBIT 720000

Outstanding shares 3000000

EPS 0.24

AC 3.5.3 Explanation

EPS refers to the part of earning that is coming on each and every unit of share

(Langdon, 2002). Dividend is paid to the shareholders from the EPS on per unit basis. EPS of

the shares is 0.24 and it indicates that there is a very low earning on per unit of share. This

happens because there is large number of outstanding shares. Hence, it can be said that firm is

giving poor performance to its shareholders.

4. INVESTMENT APPRAISAL

AC 4.1 Investment appraisal importance

As per the scenario, Taste has a branch in Cattibbean that providing food, leisure and

accommodation facility to large number of tourists from all over the world. Company's Board

of Directors wants to acquire other similar organization that operates in other parts of the

world. The Chief Executive Officer (CEO) of the company considers a possible takeover of

hotel chain in Europe and Asia.

8 | P a g e

shareholders in terms of dividend receipt from the company.

These financial plans to large extent will affect firm financial statements. If shares are

issued alone then shareholder equity will increase. In other words, it can be said that liability

side will increase in the balance sheet. If loan stocks and ordinary shares are issued then long

term loan amount will increase in balance sheet and shareholder equity will also increase in

same (Ho, Liu and Tsay, 2008). If loan shares are issued then ordinary shares and loan

amount will increase in the liability side of balance sheet.

AC 3.5 Calculation of EPS

AC 3.5.1 Information

Earning per share indicate the shareholders return on each share. All the business

shareholders have the objective of getting larger the return on their invested funds. Thus, it is

important for the companies to provide increased return to the shareholders.

AC 3.5.2 Calculation of EPS

Table 7: Calculation of EPS

PBIT 720000

Outstanding shares 3000000

EPS 0.24

AC 3.5.3 Explanation

EPS refers to the part of earning that is coming on each and every unit of share

(Langdon, 2002). Dividend is paid to the shareholders from the EPS on per unit basis. EPS of

the shares is 0.24 and it indicates that there is a very low earning on per unit of share. This

happens because there is large number of outstanding shares. Hence, it can be said that firm is

giving poor performance to its shareholders.

4. INVESTMENT APPRAISAL

AC 4.1 Investment appraisal importance

As per the scenario, Taste has a branch in Cattibbean that providing food, leisure and

accommodation facility to large number of tourists from all over the world. Company's Board

of Directors wants to acquire other similar organization that operates in other parts of the

world. The Chief Executive Officer (CEO) of the company considers a possible takeover of

hotel chain in Europe and Asia.

8 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 24

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.