Financial Resource Management and Decision Making Analysis

VerifiedAdded on 2020/02/05

|17

|5074

|100

Report

AI Summary

This report provides a comprehensive analysis of financial resource management, covering various aspects such as sources of finance, including equity, debt, and retained earnings, along with their advantages and disadvantages. It explores different types of business structures and their financial implications. The report delves into financial statements, including the statement of profit or loss, statement of financial position, and statement of cash flow, and their impact on key financial metrics. It also examines investment appraisal techniques like payback period and net present value (NPV), and recommends investment opportunities. The report further discusses working capital management, cash flow versus profit, and the importance of financial planning. Finally, it covers the interpretation of financial statements using ratio analysis, assessing the current performance of a company and highlighting the differences in financial statements. The report concludes with a discussion of the key findings and recommendations.

MANAGING FINANCIAL

RESOURCES AND

DECISIONS

RESOURCES AND

DECISIONS

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

2.0 Sources of finance for business.............................................................................................1

2.1 Types of business...................................................................................................................1

2.2 Source available to business..................................................................................................2

2.3 Comparison between right issue and loan stocks..................................................................3

2.3.1 Right issue..........................................................................................................................3

2.3.2 Loan stock...........................................................................................................................3

2.3.3 Comparison.........................................................................................................................3

2.4 Source of finance for building and non current assets...........................................................3

2.5 Working capital.....................................................................................................................4

2.5.1 Define.................................................................................................................................4

2.5.2 Why it is important.............................................................................................................4

2.5.3 What sources are available for working capital..................................................................4

3.0 Financial statements...............................................................................................................5

3.1 Statement of profit or loss......................................................................................................5

3.2 Statement of financial position..............................................................................................5

3.3 Statement of cash flow...........................................................................................................5

3.4 Impact on these financial statements.....................................................................................5

3.4.1 WACC for three options.....................................................................................................5

3.4.2 Gearing for three options present.......................................................................................7

3.4.3 How finance has impact on financial statements................................................................7

3.5 Earnings per share..................................................................................................................7

3.5.1 What information does this give you?................................................................................7

3.5.2 Calculation of EPS..............................................................................................................7

3.5.3 Explanation of answer........................................................................................................8

4 Investment appraisal.................................................................................................................8

4.1 Why it is important to appraise potential investments...........................................................8

4.2 What are the risks to future cash flows?................................................................................8

4.3 Different type of techniques..................................................................................................9

4.3.1 Payback period....................................................................................................................9

4.3.2 Calculation and explanation of answer...............................................................................9

4.3.3 Net present value................................................................................................................9

INTRODUCTION...........................................................................................................................1

2.0 Sources of finance for business.............................................................................................1

2.1 Types of business...................................................................................................................1

2.2 Source available to business..................................................................................................2

2.3 Comparison between right issue and loan stocks..................................................................3

2.3.1 Right issue..........................................................................................................................3

2.3.2 Loan stock...........................................................................................................................3

2.3.3 Comparison.........................................................................................................................3

2.4 Source of finance for building and non current assets...........................................................3

2.5 Working capital.....................................................................................................................4

2.5.1 Define.................................................................................................................................4

2.5.2 Why it is important.............................................................................................................4

2.5.3 What sources are available for working capital..................................................................4

3.0 Financial statements...............................................................................................................5

3.1 Statement of profit or loss......................................................................................................5

3.2 Statement of financial position..............................................................................................5

3.3 Statement of cash flow...........................................................................................................5

3.4 Impact on these financial statements.....................................................................................5

3.4.1 WACC for three options.....................................................................................................5

3.4.2 Gearing for three options present.......................................................................................7

3.4.3 How finance has impact on financial statements................................................................7

3.5 Earnings per share..................................................................................................................7

3.5.1 What information does this give you?................................................................................7

3.5.2 Calculation of EPS..............................................................................................................7

3.5.3 Explanation of answer........................................................................................................8

4 Investment appraisal.................................................................................................................8

4.1 Why it is important to appraise potential investments...........................................................8

4.2 What are the risks to future cash flows?................................................................................8

4.3 Different type of techniques..................................................................................................9

4.3.1 Payback period....................................................................................................................9

4.3.2 Calculation and explanation of answer...............................................................................9

4.3.3 Net present value................................................................................................................9

4.3.4 Calculation of net present value.......................................................................................10

4.4 Recommendation for the investment opportunity...............................................................10

4.5 Unit cost...............................................................................................................................10

4.5.1 Concept of unit cost..........................................................................................................10

4.6 Factors to be considered while setting price........................................................................11

5.0 Cash flow vs profit...............................................................................................................11

5.1 Need to have cash budget along with its trend and messages.............................................11

5.2 Importance of financial planning.........................................................................................12

5.3 Why company making profits can still face liquidity problem...........................................12

5.4 The users of accounts...........................................................................................................12

5.4.1 Who are they.....................................................................................................................12

5.4.2 What information do they need........................................................................................12

6.0 Interpretation of financial statement....................................................................................13

6.1 Ratio analysis.......................................................................................................................13

6.1.1 Profitability ratios.............................................................................................................13

6.1.2 Liquidity ratios..................................................................................................................13

6.2 Opinion regarding current performance of company..........................................................13

7.0 Difference in financial statements.......................................................................................14

CONCLUSION..............................................................................................................................14

REFERENCES..............................................................................................................................15

4.4 Recommendation for the investment opportunity...............................................................10

4.5 Unit cost...............................................................................................................................10

4.5.1 Concept of unit cost..........................................................................................................10

4.6 Factors to be considered while setting price........................................................................11

5.0 Cash flow vs profit...............................................................................................................11

5.1 Need to have cash budget along with its trend and messages.............................................11

5.2 Importance of financial planning.........................................................................................12

5.3 Why company making profits can still face liquidity problem...........................................12

5.4 The users of accounts...........................................................................................................12

5.4.1 Who are they.....................................................................................................................12

5.4.2 What information do they need........................................................................................12

6.0 Interpretation of financial statement....................................................................................13

6.1 Ratio analysis.......................................................................................................................13

6.1.1 Profitability ratios.............................................................................................................13

6.1.2 Liquidity ratios..................................................................................................................13

6.2 Opinion regarding current performance of company..........................................................13

7.0 Difference in financial statements.......................................................................................14

CONCLUSION..............................................................................................................................14

REFERENCES..............................................................................................................................15

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Business organizations are required to make various decisions regarding their operational

activities in order to attain their objectives in an effective manner. These decision has direct

impact on the success of business thus management is required to assess appropriate information

prior making final action. For this aspect, they are required to make financial tools in order to

analyse information in proper manner. On the basis of this evaluation, viable decisions are

required to be made (Herman, 2011). Present report is focused on the description of these

financial tools and its applicability on information of business. In this report, description will be

provided regarding various financial sources along with the cost and impact. Further, financial

techniques will be discussed such as budgeting, investment appraisal and WACC. In addition to

this, financial position of business will be assessed by computing financial ratios by considering

information from the financial statements.

2.0 Sources of finance for business

2.1 Types of business

Sole Proprietorship: Sole proprietorship is where an individual is carrying business and

is solely responsible for all the happenings in business. This Business does not have

separate assets and liabilities i.e all personal assets and liabilities of the individual will be

of business. Further, sole proprietor are personally liable for the obligations of business.

Partnership: Partnership business exists when two or more person comes together to run

a business jointly and share profits and are liable for all the acts done in the business in

the proportion as decided by them (Nickels, McHugh and McHugh, 2011). All the terms

decided by the parties are entered in a legal deed known as partnership deed, which

includes their profit sharing ratio, etc.

Company: Company is a legal entity owned by shareholders. Shareholders are the

persons by whom amount is invested in the company and in return are allotted shares. It

is different from partnership as it is separate from its owners i.e company can be sued or

can sue or can take any legal action on its own name rather than shareholders. In

companies, liability of owners is restricted to their share in the company.

1

Business organizations are required to make various decisions regarding their operational

activities in order to attain their objectives in an effective manner. These decision has direct

impact on the success of business thus management is required to assess appropriate information

prior making final action. For this aspect, they are required to make financial tools in order to

analyse information in proper manner. On the basis of this evaluation, viable decisions are

required to be made (Herman, 2011). Present report is focused on the description of these

financial tools and its applicability on information of business. In this report, description will be

provided regarding various financial sources along with the cost and impact. Further, financial

techniques will be discussed such as budgeting, investment appraisal and WACC. In addition to

this, financial position of business will be assessed by computing financial ratios by considering

information from the financial statements.

2.0 Sources of finance for business

2.1 Types of business

Sole Proprietorship: Sole proprietorship is where an individual is carrying business and

is solely responsible for all the happenings in business. This Business does not have

separate assets and liabilities i.e all personal assets and liabilities of the individual will be

of business. Further, sole proprietor are personally liable for the obligations of business.

Partnership: Partnership business exists when two or more person comes together to run

a business jointly and share profits and are liable for all the acts done in the business in

the proportion as decided by them (Nickels, McHugh and McHugh, 2011). All the terms

decided by the parties are entered in a legal deed known as partnership deed, which

includes their profit sharing ratio, etc.

Company: Company is a legal entity owned by shareholders. Shareholders are the

persons by whom amount is invested in the company and in return are allotted shares. It

is different from partnership as it is separate from its owners i.e company can be sued or

can sue or can take any legal action on its own name rather than shareholders. In

companies, liability of owners is restricted to their share in the company.

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

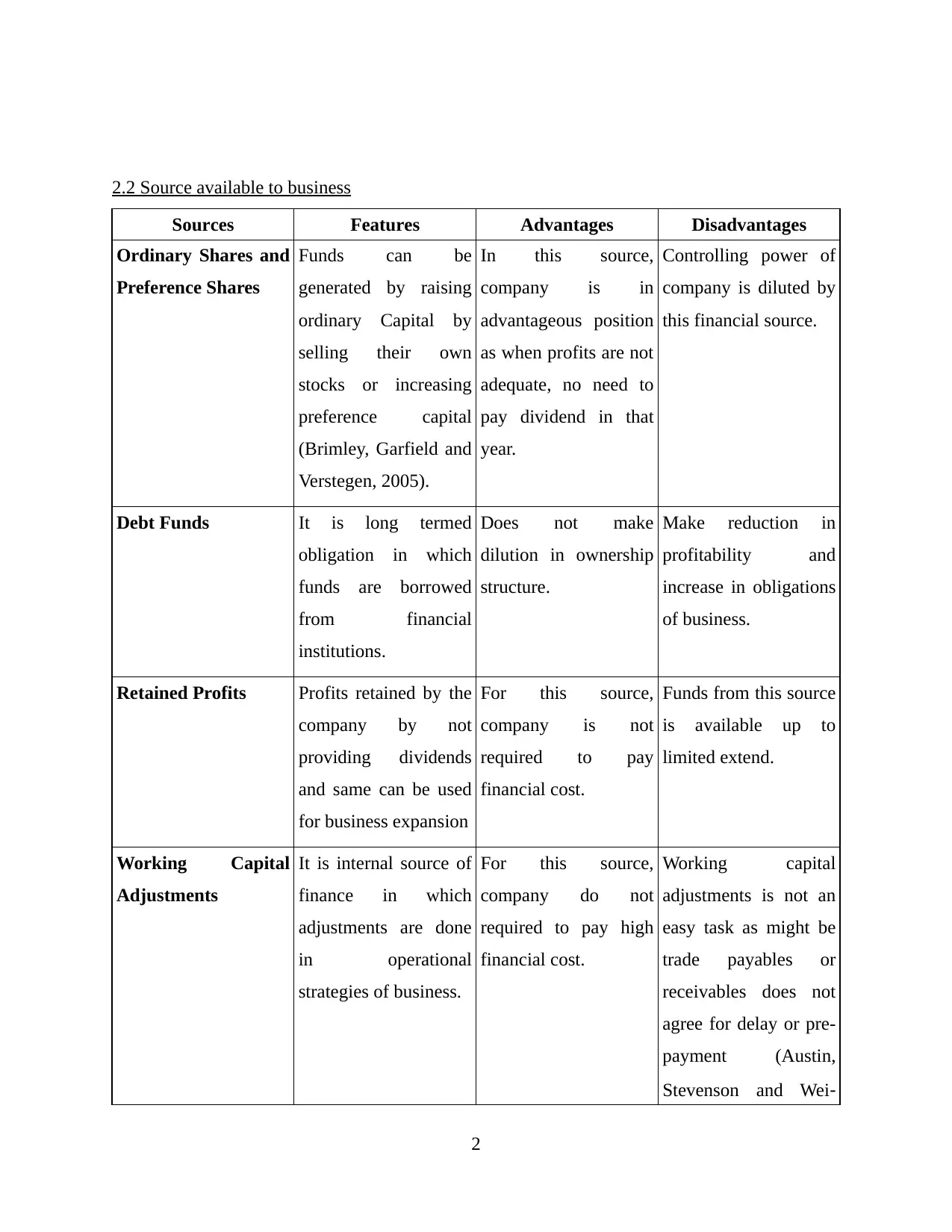

2.2 Source available to business

Sources Features Advantages Disadvantages

Ordinary Shares and

Preference Shares

Funds can be

generated by raising

ordinary Capital by

selling their own

stocks or increasing

preference capital

(Brimley, Garfield and

Verstegen, 2005).

In this source,

company is in

advantageous position

as when profits are not

adequate, no need to

pay dividend in that

year.

Controlling power of

company is diluted by

this financial source.

Debt Funds It is long termed

obligation in which

funds are borrowed

from financial

institutions.

Does not make

dilution in ownership

structure.

Make reduction in

profitability and

increase in obligations

of business.

Retained Profits Profits retained by the

company by not

providing dividends

and same can be used

for business expansion

For this source,

company is not

required to pay

financial cost.

Funds from this source

is available up to

limited extend.

Working Capital

Adjustments

It is internal source of

finance in which

adjustments are done

in operational

strategies of business.

For this source,

company do not

required to pay high

financial cost.

Working capital

adjustments is not an

easy task as might be

trade payables or

receivables does not

agree for delay or pre-

payment (Austin,

Stevenson and Wei‐

2

Sources Features Advantages Disadvantages

Ordinary Shares and

Preference Shares

Funds can be

generated by raising

ordinary Capital by

selling their own

stocks or increasing

preference capital

(Brimley, Garfield and

Verstegen, 2005).

In this source,

company is in

advantageous position

as when profits are not

adequate, no need to

pay dividend in that

year.

Controlling power of

company is diluted by

this financial source.

Debt Funds It is long termed

obligation in which

funds are borrowed

from financial

institutions.

Does not make

dilution in ownership

structure.

Make reduction in

profitability and

increase in obligations

of business.

Retained Profits Profits retained by the

company by not

providing dividends

and same can be used

for business expansion

For this source,

company is not

required to pay

financial cost.

Funds from this source

is available up to

limited extend.

Working Capital

Adjustments

It is internal source of

finance in which

adjustments are done

in operational

strategies of business.

For this source,

company do not

required to pay high

financial cost.

Working capital

adjustments is not an

easy task as might be

trade payables or

receivables does not

agree for delay or pre-

payment (Austin,

Stevenson and Wei‐

2

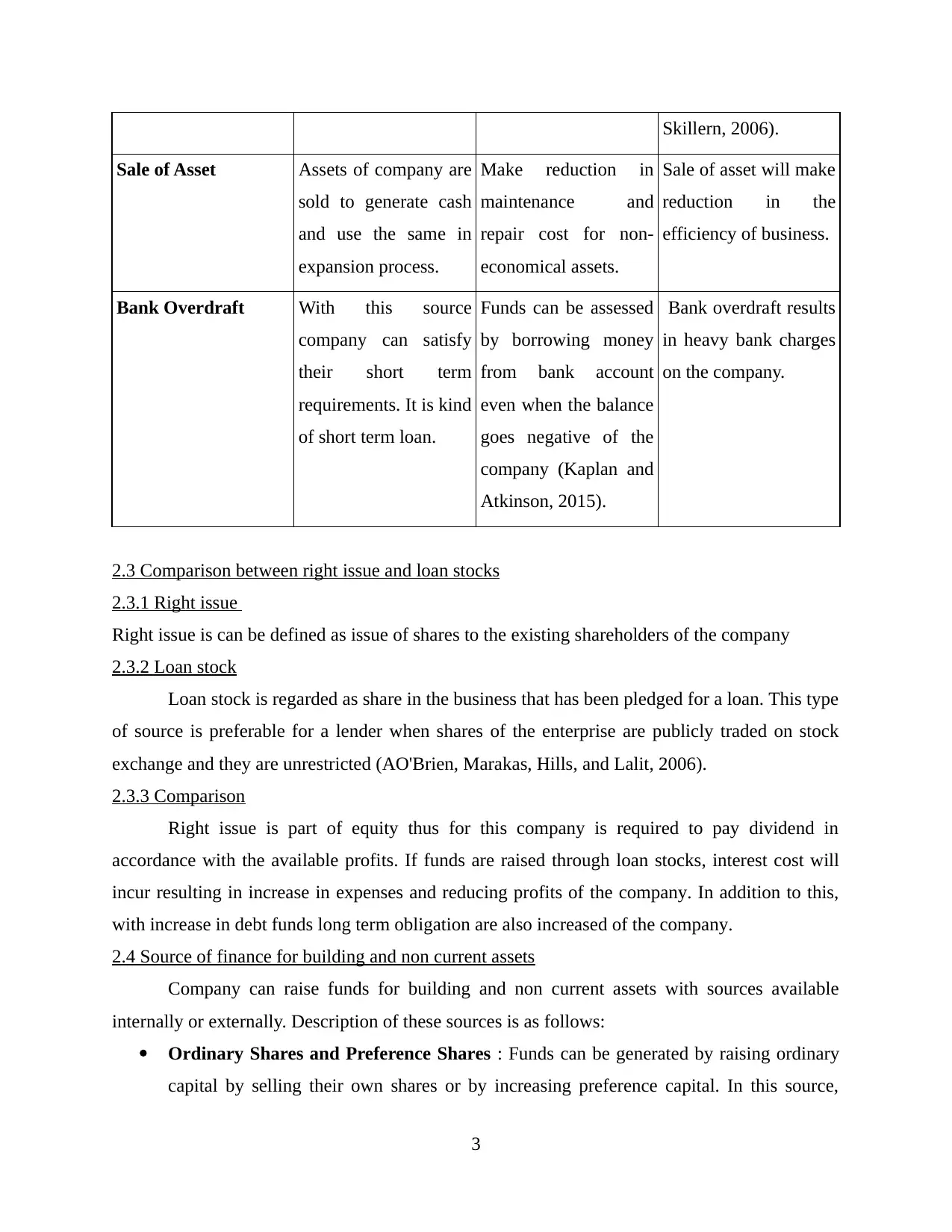

Skillern, 2006).

Sale of Asset Assets of company are

sold to generate cash

and use the same in

expansion process.

Make reduction in

maintenance and

repair cost for non-

economical assets.

Sale of asset will make

reduction in the

efficiency of business.

Bank Overdraft With this source

company can satisfy

their short term

requirements. It is kind

of short term loan.

Funds can be assessed

by borrowing money

from bank account

even when the balance

goes negative of the

company (Kaplan and

Atkinson, 2015).

Bank overdraft results

in heavy bank charges

on the company.

2.3 Comparison between right issue and loan stocks

2.3.1 Right issue

Right issue is can be defined as issue of shares to the existing shareholders of the company

2.3.2 Loan stock

Loan stock is regarded as share in the business that has been pledged for a loan. This type

of source is preferable for a lender when shares of the enterprise are publicly traded on stock

exchange and they are unrestricted (AO'Brien, Marakas, Hills, and Lalit, 2006).

2.3.3 Comparison

Right issue is part of equity thus for this company is required to pay dividend in

accordance with the available profits. If funds are raised through loan stocks, interest cost will

incur resulting in increase in expenses and reducing profits of the company. In addition to this,

with increase in debt funds long term obligation are also increased of the company.

2.4 Source of finance for building and non current assets

Company can raise funds for building and non current assets with sources available

internally or externally. Description of these sources is as follows:

Ordinary Shares and Preference Shares : Funds can be generated by raising ordinary

capital by selling their own shares or by increasing preference capital. In this source,

3

Sale of Asset Assets of company are

sold to generate cash

and use the same in

expansion process.

Make reduction in

maintenance and

repair cost for non-

economical assets.

Sale of asset will make

reduction in the

efficiency of business.

Bank Overdraft With this source

company can satisfy

their short term

requirements. It is kind

of short term loan.

Funds can be assessed

by borrowing money

from bank account

even when the balance

goes negative of the

company (Kaplan and

Atkinson, 2015).

Bank overdraft results

in heavy bank charges

on the company.

2.3 Comparison between right issue and loan stocks

2.3.1 Right issue

Right issue is can be defined as issue of shares to the existing shareholders of the company

2.3.2 Loan stock

Loan stock is regarded as share in the business that has been pledged for a loan. This type

of source is preferable for a lender when shares of the enterprise are publicly traded on stock

exchange and they are unrestricted (AO'Brien, Marakas, Hills, and Lalit, 2006).

2.3.3 Comparison

Right issue is part of equity thus for this company is required to pay dividend in

accordance with the available profits. If funds are raised through loan stocks, interest cost will

incur resulting in increase in expenses and reducing profits of the company. In addition to this,

with increase in debt funds long term obligation are also increased of the company.

2.4 Source of finance for building and non current assets

Company can raise funds for building and non current assets with sources available

internally or externally. Description of these sources is as follows:

Ordinary Shares and Preference Shares : Funds can be generated by raising ordinary

capital by selling their own shares or by increasing preference capital. In this source,

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

company is in advantageous position as when profits are not adequate, no need to pay

dividend in that year (Rose and Hudgins, 2014).

Debt Funds : Company can raise funds either by borrowing money from other financial

institutions on payment of interest in timely manner or by issuing debenture securities.

Further, they will also be obliged for the payment of principal amount.

Retained Profits : Profits retained by the company by not providing dividends and same

can be used for business expansion. Profits are reinvested in form of building and non

current assets.

2.5 Working capital

2.5.1 Define

Working capital can be termed as difference between current assets and current liabilities.

It shows how capital is used to meet needs of short term operational activities of the company

2.5.2 Why it is important

Company has many short term needs to be fulfilled and company cannot use its long term

sources for meeting the same. Working capital is important for business to manage its liquidity

and preventing barriers in smooth operations (Slack, Chambers and Johnston, 2010). This capital

includes current assets and current liabilities, thus it can be increased by either reducing short

term liabilities like delaying payment of trade payables or by increasing current assets like

receiving amount early from sundry debtors or by reducing inventories. Further, company can

make use of facility of bank overdraft in order to satisfy their working capital requirements.

Major components of working capital are receivable, inventory, cash and cash equivalence etc.

2.5.3 What sources are available for working capital

One of the most suitable sources for working capital finance is bank overdraft as through

this firm can withdraw more amount than those lying in the account. Further, company has to

pay interest for the amount obtained and through this it is possible to manage components of

working capital (Chrisman, Chua and Sharma, 2005). Further, it is possible to delay payment to

creditors with the aim to recover funds from debtors.

3.0 Financial statements

3.1 Statement of profit or loss

This Statement shows the net profitability over a period of time after incurring various

expenses and revenues earned from different sources. It is also known as income statement.

4

dividend in that year (Rose and Hudgins, 2014).

Debt Funds : Company can raise funds either by borrowing money from other financial

institutions on payment of interest in timely manner or by issuing debenture securities.

Further, they will also be obliged for the payment of principal amount.

Retained Profits : Profits retained by the company by not providing dividends and same

can be used for business expansion. Profits are reinvested in form of building and non

current assets.

2.5 Working capital

2.5.1 Define

Working capital can be termed as difference between current assets and current liabilities.

It shows how capital is used to meet needs of short term operational activities of the company

2.5.2 Why it is important

Company has many short term needs to be fulfilled and company cannot use its long term

sources for meeting the same. Working capital is important for business to manage its liquidity

and preventing barriers in smooth operations (Slack, Chambers and Johnston, 2010). This capital

includes current assets and current liabilities, thus it can be increased by either reducing short

term liabilities like delaying payment of trade payables or by increasing current assets like

receiving amount early from sundry debtors or by reducing inventories. Further, company can

make use of facility of bank overdraft in order to satisfy their working capital requirements.

Major components of working capital are receivable, inventory, cash and cash equivalence etc.

2.5.3 What sources are available for working capital

One of the most suitable sources for working capital finance is bank overdraft as through

this firm can withdraw more amount than those lying in the account. Further, company has to

pay interest for the amount obtained and through this it is possible to manage components of

working capital (Chrisman, Chua and Sharma, 2005). Further, it is possible to delay payment to

creditors with the aim to recover funds from debtors.

3.0 Financial statements

3.1 Statement of profit or loss

This Statement shows the net profitability over a period of time after incurring various

expenses and revenues earned from different sources. It is also known as income statement.

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

3.2 Statement of financial position

This statement provides review of company's financial position at a given date. Position

of assets and liabilities of a company is shown by Balance sheet thus it is also known as Position

statement.

3.3 Statement of cash flow

This statement shows cash transaction through various activities which results in cash and

cash equivalent movement over a period of time (Bojadziev and Bojadziev, 2007). These

activities are categorised in three parts namely operating activities which includes revenue

generating items, investing activities in which cash flow from sale and purchase of assets are

shown and financing activities in which cash flow from any activity from share capital and long

term debts are shown including interest.

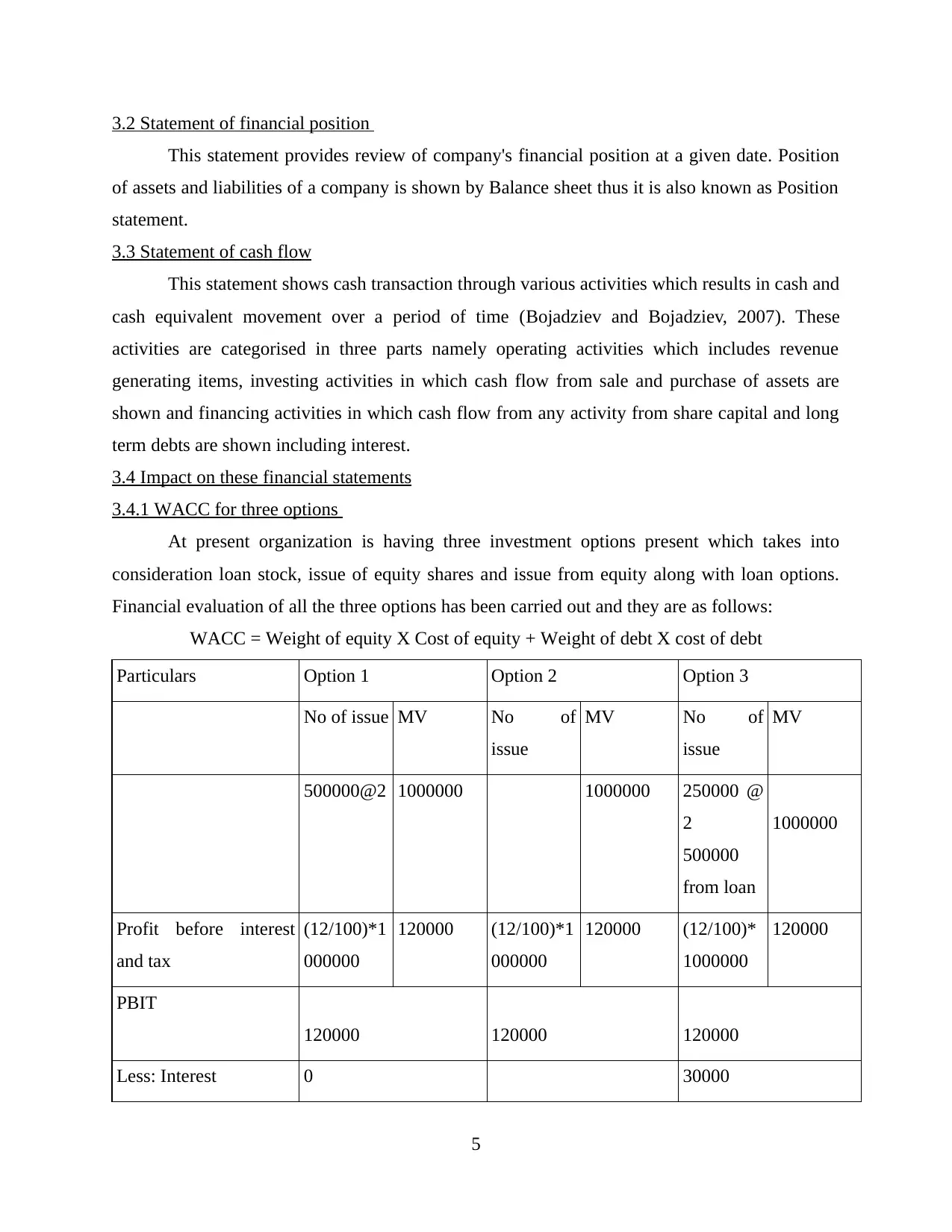

3.4 Impact on these financial statements

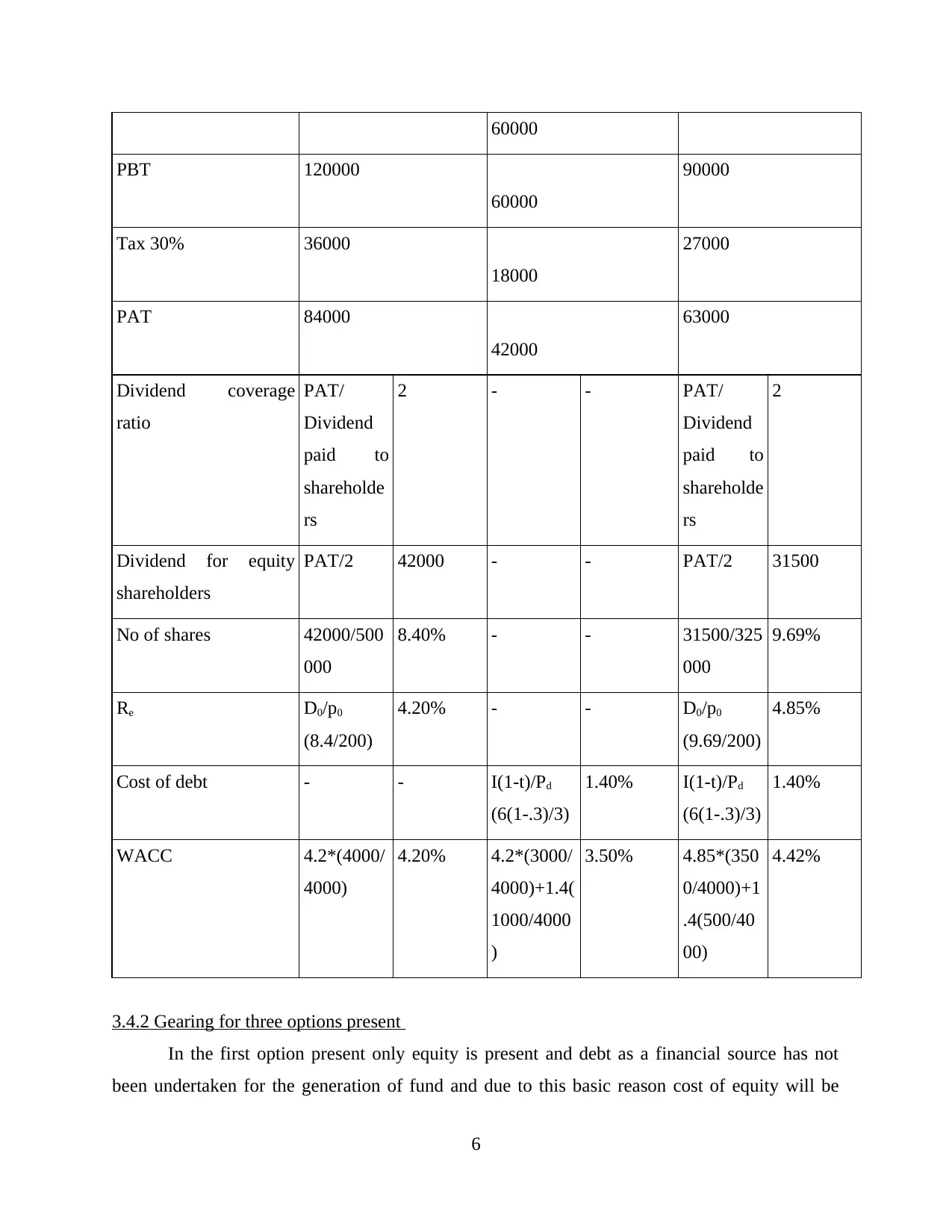

3.4.1 WACC for three options

At present organization is having three investment options present which takes into

consideration loan stock, issue of equity shares and issue from equity along with loan options.

Financial evaluation of all the three options has been carried out and they are as follows:

WACC = Weight of equity X Cost of equity + Weight of debt X cost of debt

Particulars Option 1 Option 2 Option 3

No of issue MV No of

issue

MV No of

issue

MV

500000@2 1000000 1000000 250000 @

2

500000

from loan

1000000

Profit before interest

and tax

(12/100)*1

000000

120000 (12/100)*1

000000

120000 (12/100)*

1000000

120000

PBIT

120000 120000 120000

Less: Interest 0 30000

5

This statement provides review of company's financial position at a given date. Position

of assets and liabilities of a company is shown by Balance sheet thus it is also known as Position

statement.

3.3 Statement of cash flow

This statement shows cash transaction through various activities which results in cash and

cash equivalent movement over a period of time (Bojadziev and Bojadziev, 2007). These

activities are categorised in three parts namely operating activities which includes revenue

generating items, investing activities in which cash flow from sale and purchase of assets are

shown and financing activities in which cash flow from any activity from share capital and long

term debts are shown including interest.

3.4 Impact on these financial statements

3.4.1 WACC for three options

At present organization is having three investment options present which takes into

consideration loan stock, issue of equity shares and issue from equity along with loan options.

Financial evaluation of all the three options has been carried out and they are as follows:

WACC = Weight of equity X Cost of equity + Weight of debt X cost of debt

Particulars Option 1 Option 2 Option 3

No of issue MV No of

issue

MV No of

issue

MV

500000@2 1000000 1000000 250000 @

2

500000

from loan

1000000

Profit before interest

and tax

(12/100)*1

000000

120000 (12/100)*1

000000

120000 (12/100)*

1000000

120000

PBIT

120000 120000 120000

Less: Interest 0 30000

5

60000

PBT 120000

60000

90000

Tax 30% 36000

18000

27000

PAT 84000

42000

63000

Dividend coverage

ratio

PAT/

Dividend

paid to

shareholde

rs

2 - - PAT/

Dividend

paid to

shareholde

rs

2

Dividend for equity

shareholders

PAT/2 42000 - - PAT/2 31500

No of shares 42000/500

000

8.40% - - 31500/325

000

9.69%

Re D0/p0

(8.4/200)

4.20% - - D0/p0

(9.69/200)

4.85%

Cost of debt - - I(1-t)/Pd

(6(1-.3)/3)

1.40% I(1-t)/Pd

(6(1-.3)/3)

1.40%

WACC 4.2*(4000/

4000)

4.20% 4.2*(3000/

4000)+1.4(

1000/4000

)

3.50% 4.85*(350

0/4000)+1

.4(500/40

00)

4.42%

3.4.2 Gearing for three options present

In the first option present only equity is present and debt as a financial source has not

been undertaken for the generation of fund and due to this basic reason cost of equity will be

6

PBT 120000

60000

90000

Tax 30% 36000

18000

27000

PAT 84000

42000

63000

Dividend coverage

ratio

PAT/

Dividend

paid to

shareholde

rs

2 - - PAT/

Dividend

paid to

shareholde

rs

2

Dividend for equity

shareholders

PAT/2 42000 - - PAT/2 31500

No of shares 42000/500

000

8.40% - - 31500/325

000

9.69%

Re D0/p0

(8.4/200)

4.20% - - D0/p0

(9.69/200)

4.85%

Cost of debt - - I(1-t)/Pd

(6(1-.3)/3)

1.40% I(1-t)/Pd

(6(1-.3)/3)

1.40%

WACC 4.2*(4000/

4000)

4.20% 4.2*(3000/

4000)+1.4(

1000/4000

)

3.50% 4.85*(350

0/4000)+1

.4(500/40

00)

4.42%

3.4.2 Gearing for three options present

In the first option present only equity is present and debt as a financial source has not

been undertaken for the generation of fund and due to this basic reason cost of equity will be

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

regarded as cost of debt. Further, it is not possible to calculate gearing as debt portion in capital

structure is not at all present. Moreover, in the second option debt to equity ratio is 3:1 and in the

last option debt to equity ratio is 7:1. Therefore, by comparing all the three options present it is

recommended to company to consider second option whose ratio is favorable for enterprise and

through this it is possible to mitigate risk and stability is also present.

It is recommended to the board of directors of enterprise to undertake the second option

which is appropriate for enterprise. By considering this option business can easily satisfy its

financial needs by taking loan of 1000000 @ 6%. Apart from this, the source considered can

deliver tax shield to the entity and posses less financial cost.

3.4.3 How finance has impact on financial statements

The source being adopted by enterprise has direct impact on financial statement. The

alternative chosen by business such as debt financing will affect balance sheet of the enterprise

as through this long term obligations of the business will rise and simultaneously cash along with

cash equivalence of the business enterprise will increase (Saunders, Cornett and McGraw, 2006).

Moreover, it will also affect income statement of the business as it is represented on the debit

side and thus profitability of the company decreases due to burden of financial cost. Therefore, in

this way the sources adopted for satisfying financial needs have direct impact on financial

statements.

3.5 Earnings per share

3.5.1 What information does this give you?

Earnings per share supports in knowing the profitability level of the organization and in

turn it can be known whether business is effective enough in carrying out overall operations in

the market or not (Jensen, 2005). Through this investors of the firm obtains idea regarding

whether to purchase shares of the firm or not.

3.5.2 Calculation of EPS

Profit before interest and tax 720,000

Profit after interest 720,000 – 60,000 = 6,60,000

Profit after interest 6,60,000*(1-.3) = 4,62,000

Earning per share PAIT/ no. of equity shareholders = 462/3000

EPS =15.4%

7

structure is not at all present. Moreover, in the second option debt to equity ratio is 3:1 and in the

last option debt to equity ratio is 7:1. Therefore, by comparing all the three options present it is

recommended to company to consider second option whose ratio is favorable for enterprise and

through this it is possible to mitigate risk and stability is also present.

It is recommended to the board of directors of enterprise to undertake the second option

which is appropriate for enterprise. By considering this option business can easily satisfy its

financial needs by taking loan of 1000000 @ 6%. Apart from this, the source considered can

deliver tax shield to the entity and posses less financial cost.

3.4.3 How finance has impact on financial statements

The source being adopted by enterprise has direct impact on financial statement. The

alternative chosen by business such as debt financing will affect balance sheet of the enterprise

as through this long term obligations of the business will rise and simultaneously cash along with

cash equivalence of the business enterprise will increase (Saunders, Cornett and McGraw, 2006).

Moreover, it will also affect income statement of the business as it is represented on the debit

side and thus profitability of the company decreases due to burden of financial cost. Therefore, in

this way the sources adopted for satisfying financial needs have direct impact on financial

statements.

3.5 Earnings per share

3.5.1 What information does this give you?

Earnings per share supports in knowing the profitability level of the organization and in

turn it can be known whether business is effective enough in carrying out overall operations in

the market or not (Jensen, 2005). Through this investors of the firm obtains idea regarding

whether to purchase shares of the firm or not.

3.5.2 Calculation of EPS

Profit before interest and tax 720,000

Profit after interest 720,000 – 60,000 = 6,60,000

Profit after interest 6,60,000*(1-.3) = 4,62,000

Earning per share PAIT/ no. of equity shareholders = 462/3000

EPS =15.4%

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

3.5.3 Explanation of answer

Earning per share highlights the income level which shareholders of the enterprise

receives by investing funds in the shares of the company. Moreover, it is well known fact that

investors of company are interested in knowing the income level of firm and for the same they

obtain information. Company like Taste plc is financially sound and is efficient enough in

satisfying financial needs of its investors.

EPS of company is 15.4% and it is representing worthwhile investment depending on the

market price of the stock. It is showing that Taste plc is satisfying financial needs of its investors

in effective manner and through this financial needs of the business are also satisfied. Income

earned by business is quite high and due to this reason company is having higher income which

can be distributed among investors. Further, every year income level of Taste plc is rising and

through this business is able to distribute more income in between its investors.

4 Investment appraisal

4.1 Why it is important to appraise potential investments

Investment appraisal technique supports organization in knowing the feasibility of the

proposal in which funds can be allocated easily (Bartram, Brown and Fehle, 2009). Further, it is

required to appraise investment as through this it can be known which investment yields higher

return and the amount invested can be recovered easily. By applying techniques such as net

present value, internal rate of return and payback period it is possible to know feasibility of

investment proposal.

4.2 What are the risks to future cash flows?

One of the major risks associated with future cash flow is future uncertainty where it is

not possible to know the level of return which can be obtained in near future (Brigham and

Ehrhardt, 2013). Further, by investing in the present proposal company sacrifices investment in

other project which can provide benefit which is regarded as opportunity cost. Apart from this

some other risks are also present which involves fluctuations in the number of customers along

with rise or decline in prices of raw materials.

8

Earning per share highlights the income level which shareholders of the enterprise

receives by investing funds in the shares of the company. Moreover, it is well known fact that

investors of company are interested in knowing the income level of firm and for the same they

obtain information. Company like Taste plc is financially sound and is efficient enough in

satisfying financial needs of its investors.

EPS of company is 15.4% and it is representing worthwhile investment depending on the

market price of the stock. It is showing that Taste plc is satisfying financial needs of its investors

in effective manner and through this financial needs of the business are also satisfied. Income

earned by business is quite high and due to this reason company is having higher income which

can be distributed among investors. Further, every year income level of Taste plc is rising and

through this business is able to distribute more income in between its investors.

4 Investment appraisal

4.1 Why it is important to appraise potential investments

Investment appraisal technique supports organization in knowing the feasibility of the

proposal in which funds can be allocated easily (Bartram, Brown and Fehle, 2009). Further, it is

required to appraise investment as through this it can be known which investment yields higher

return and the amount invested can be recovered easily. By applying techniques such as net

present value, internal rate of return and payback period it is possible to know feasibility of

investment proposal.

4.2 What are the risks to future cash flows?

One of the major risks associated with future cash flow is future uncertainty where it is

not possible to know the level of return which can be obtained in near future (Brigham and

Ehrhardt, 2013). Further, by investing in the present proposal company sacrifices investment in

other project which can provide benefit which is regarded as opportunity cost. Apart from this

some other risks are also present which involves fluctuations in the number of customers along

with rise or decline in prices of raw materials.

8

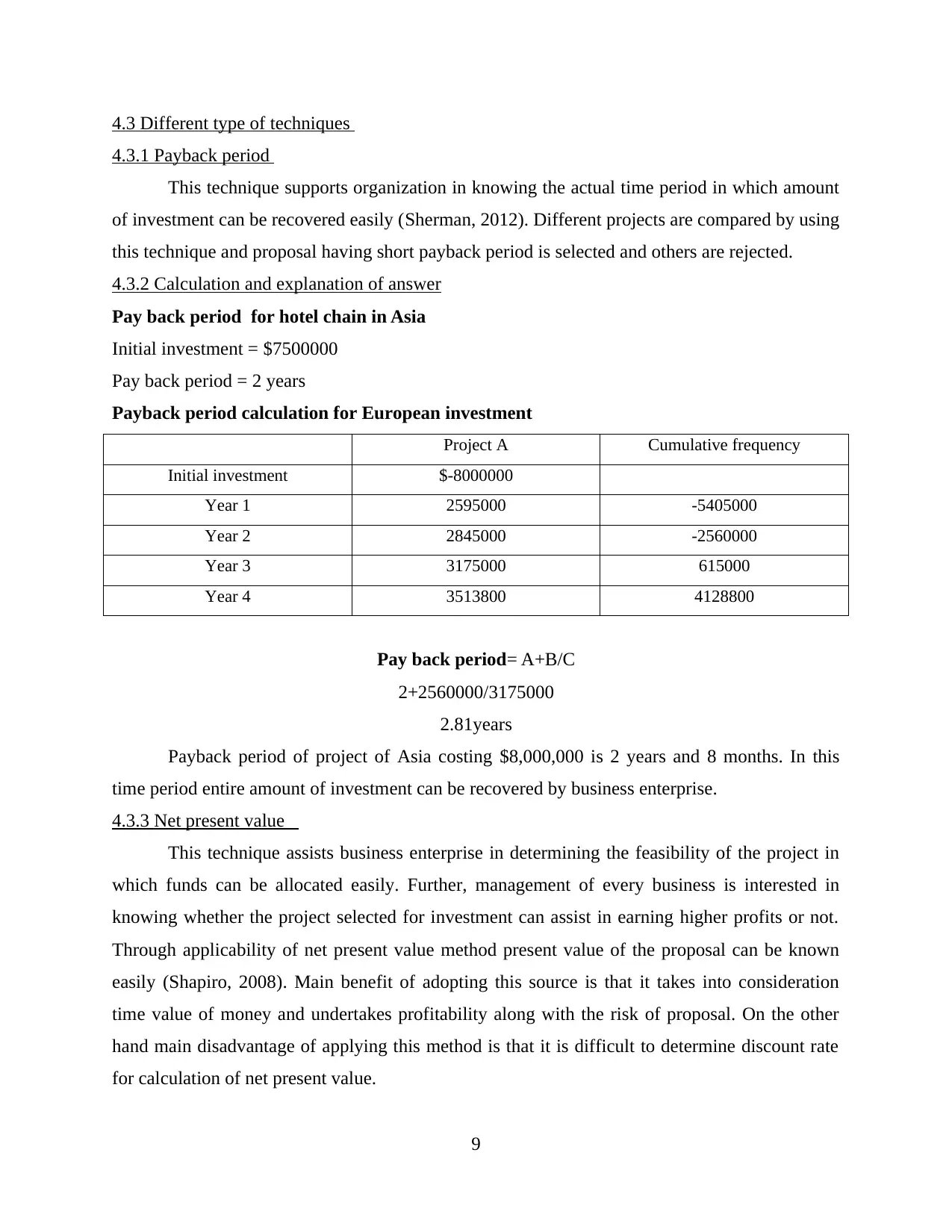

4.3 Different type of techniques

4.3.1 Payback period

This technique supports organization in knowing the actual time period in which amount

of investment can be recovered easily (Sherman, 2012). Different projects are compared by using

this technique and proposal having short payback period is selected and others are rejected.

4.3.2 Calculation and explanation of answer

Pay back period for hotel chain in Asia

Initial investment = $7500000

Pay back period = 2 years

Payback period calculation for European investment

Project A Cumulative frequency

Initial investment $-8000000

Year 1 2595000 -5405000

Year 2 2845000 -2560000

Year 3 3175000 615000

Year 4 3513800 4128800

Pay back period= A+B/C

2+2560000/3175000

2.81years

Payback period of project of Asia costing $8,000,000 is 2 years and 8 months. In this

time period entire amount of investment can be recovered by business enterprise.

4.3.3 Net present value

This technique assists business enterprise in determining the feasibility of the project in

which funds can be allocated easily. Further, management of every business is interested in

knowing whether the project selected for investment can assist in earning higher profits or not.

Through applicability of net present value method present value of the proposal can be known

easily (Shapiro, 2008). Main benefit of adopting this source is that it takes into consideration

time value of money and undertakes profitability along with the risk of proposal. On the other

hand main disadvantage of applying this method is that it is difficult to determine discount rate

for calculation of net present value.

9

4.3.1 Payback period

This technique supports organization in knowing the actual time period in which amount

of investment can be recovered easily (Sherman, 2012). Different projects are compared by using

this technique and proposal having short payback period is selected and others are rejected.

4.3.2 Calculation and explanation of answer

Pay back period for hotel chain in Asia

Initial investment = $7500000

Pay back period = 2 years

Payback period calculation for European investment

Project A Cumulative frequency

Initial investment $-8000000

Year 1 2595000 -5405000

Year 2 2845000 -2560000

Year 3 3175000 615000

Year 4 3513800 4128800

Pay back period= A+B/C

2+2560000/3175000

2.81years

Payback period of project of Asia costing $8,000,000 is 2 years and 8 months. In this

time period entire amount of investment can be recovered by business enterprise.

4.3.3 Net present value

This technique assists business enterprise in determining the feasibility of the project in

which funds can be allocated easily. Further, management of every business is interested in

knowing whether the project selected for investment can assist in earning higher profits or not.

Through applicability of net present value method present value of the proposal can be known

easily (Shapiro, 2008). Main benefit of adopting this source is that it takes into consideration

time value of money and undertakes profitability along with the risk of proposal. On the other

hand main disadvantage of applying this method is that it is difficult to determine discount rate

for calculation of net present value.

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.