University Financial Accounting Assignment: Consolidation and Analysis

VerifiedAdded on 2023/01/18

|12

|1333

|1

Homework Assignment

AI Summary

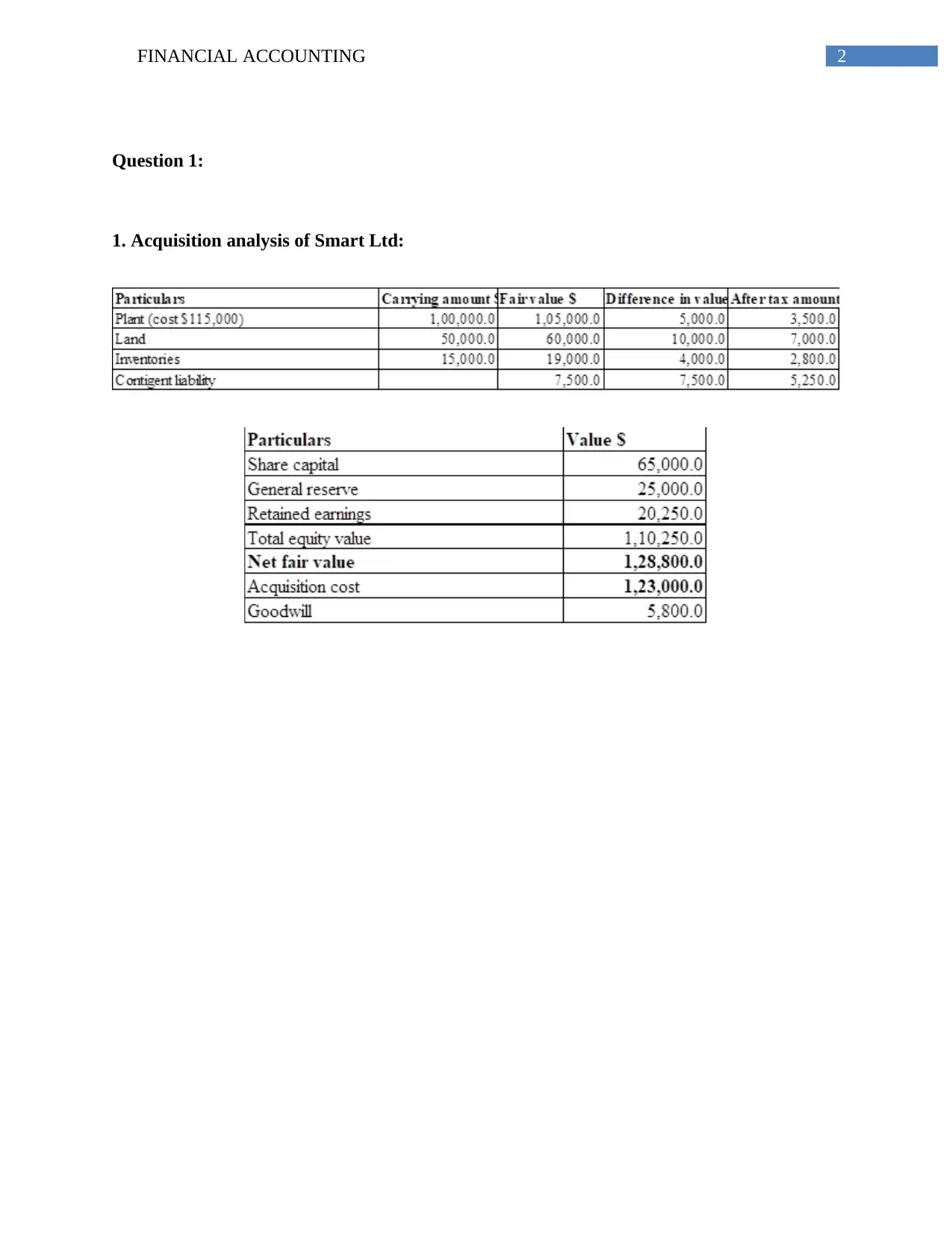

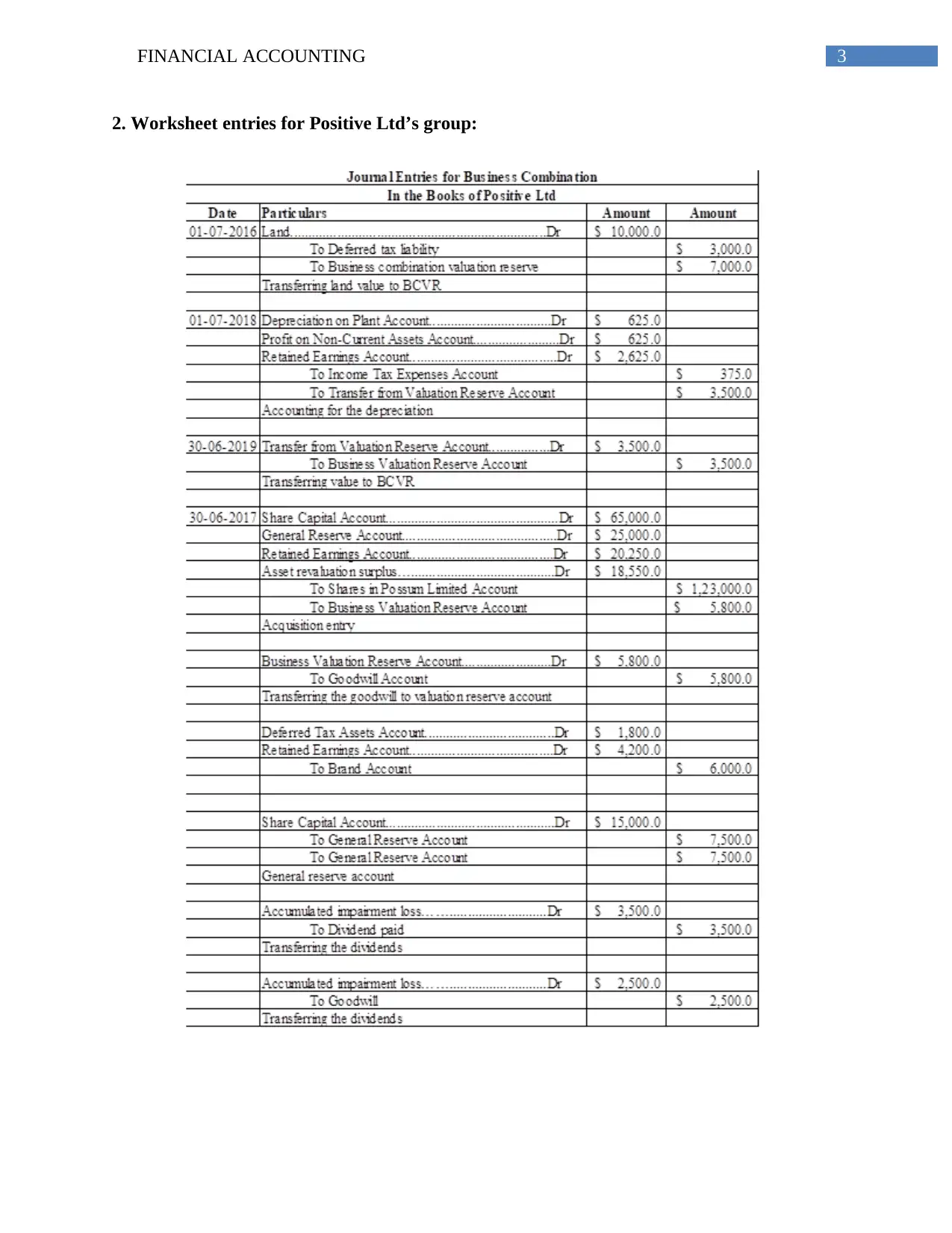

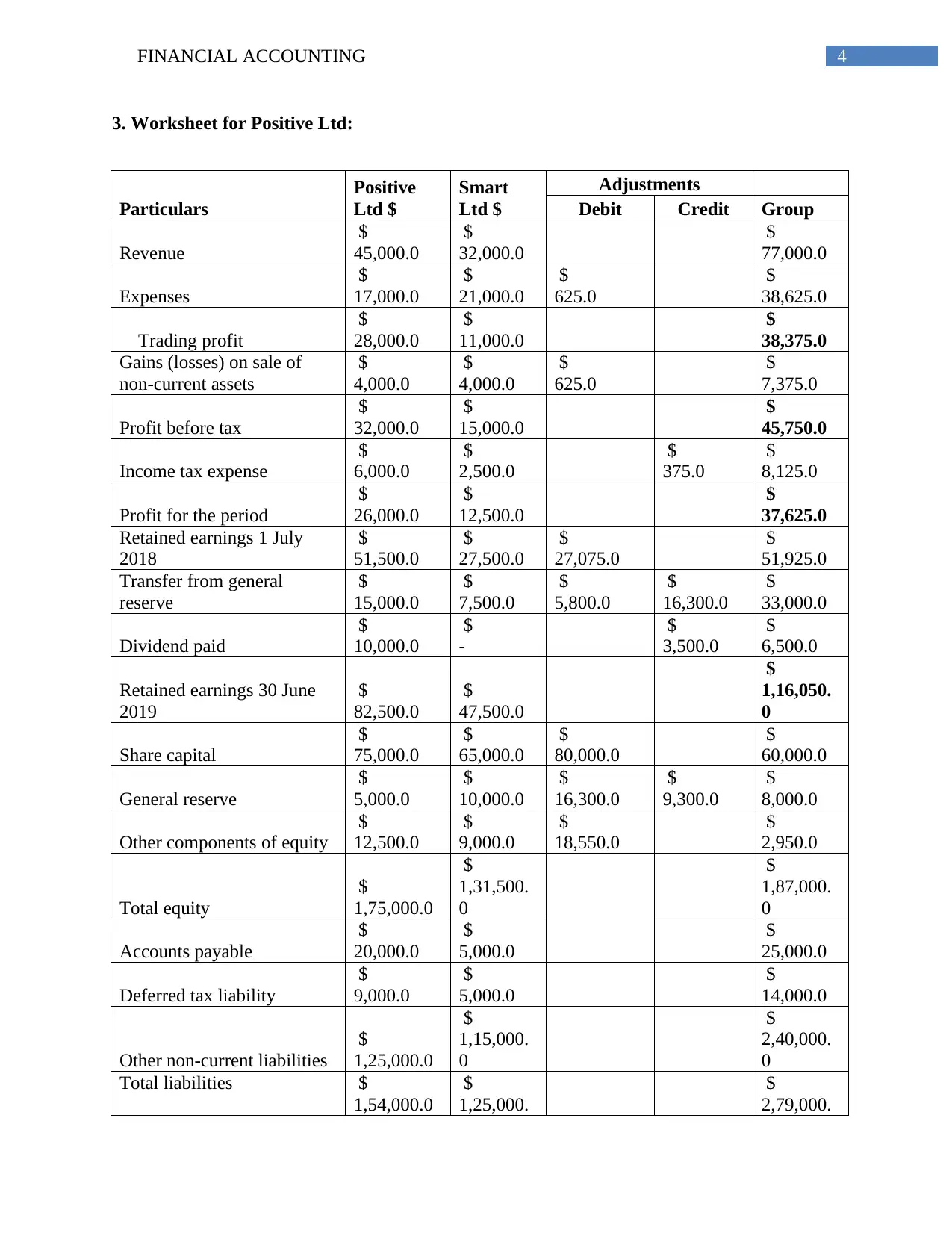

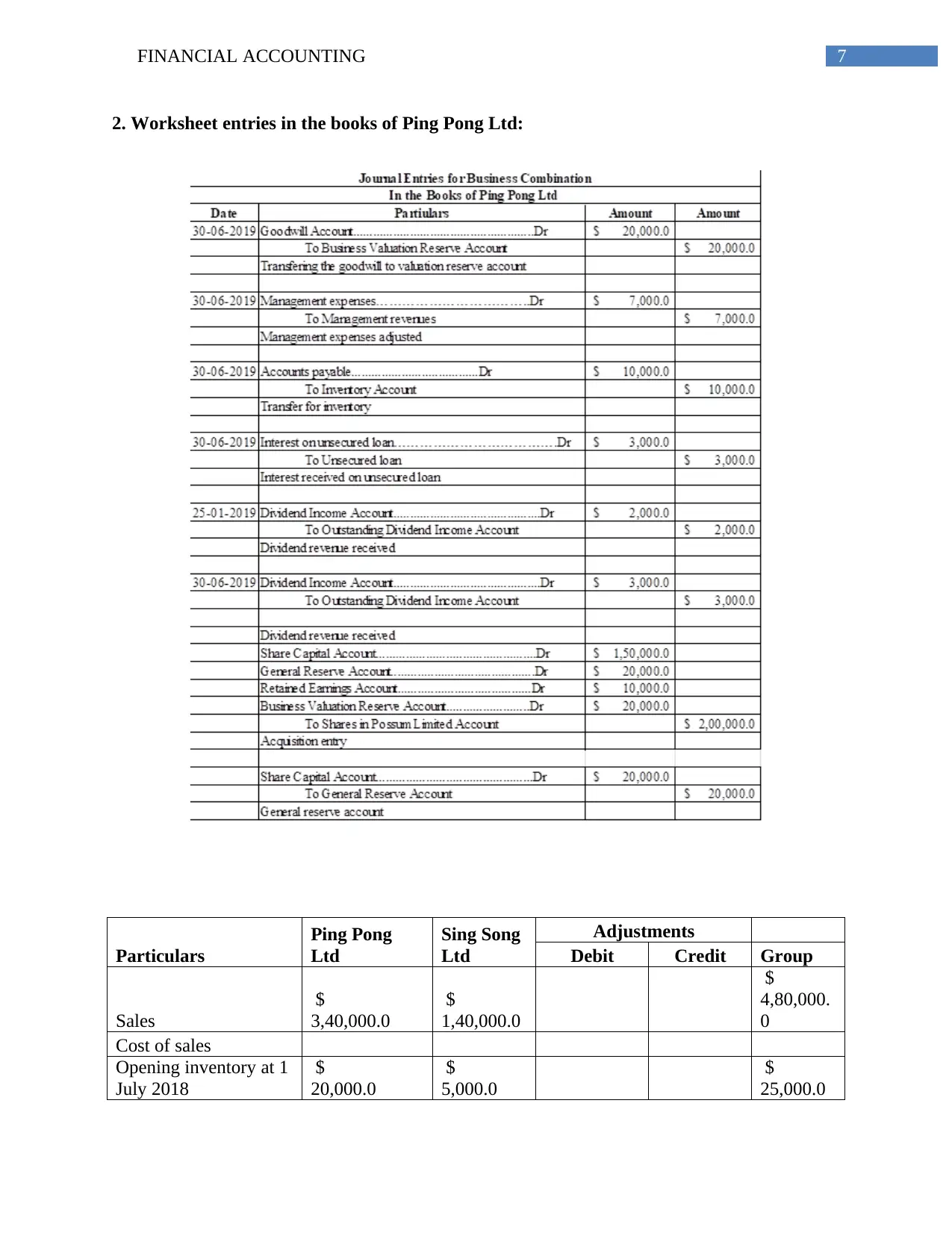

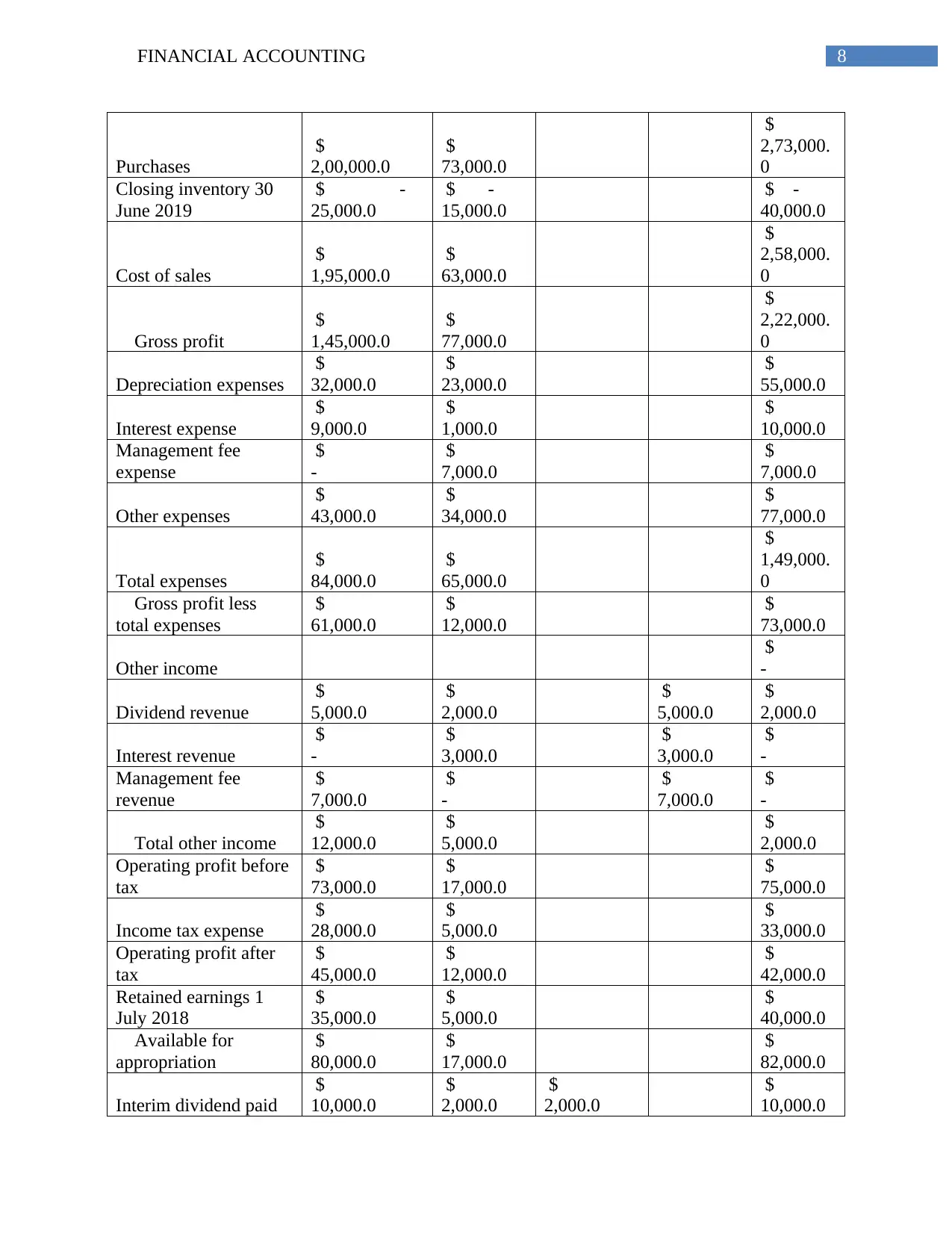

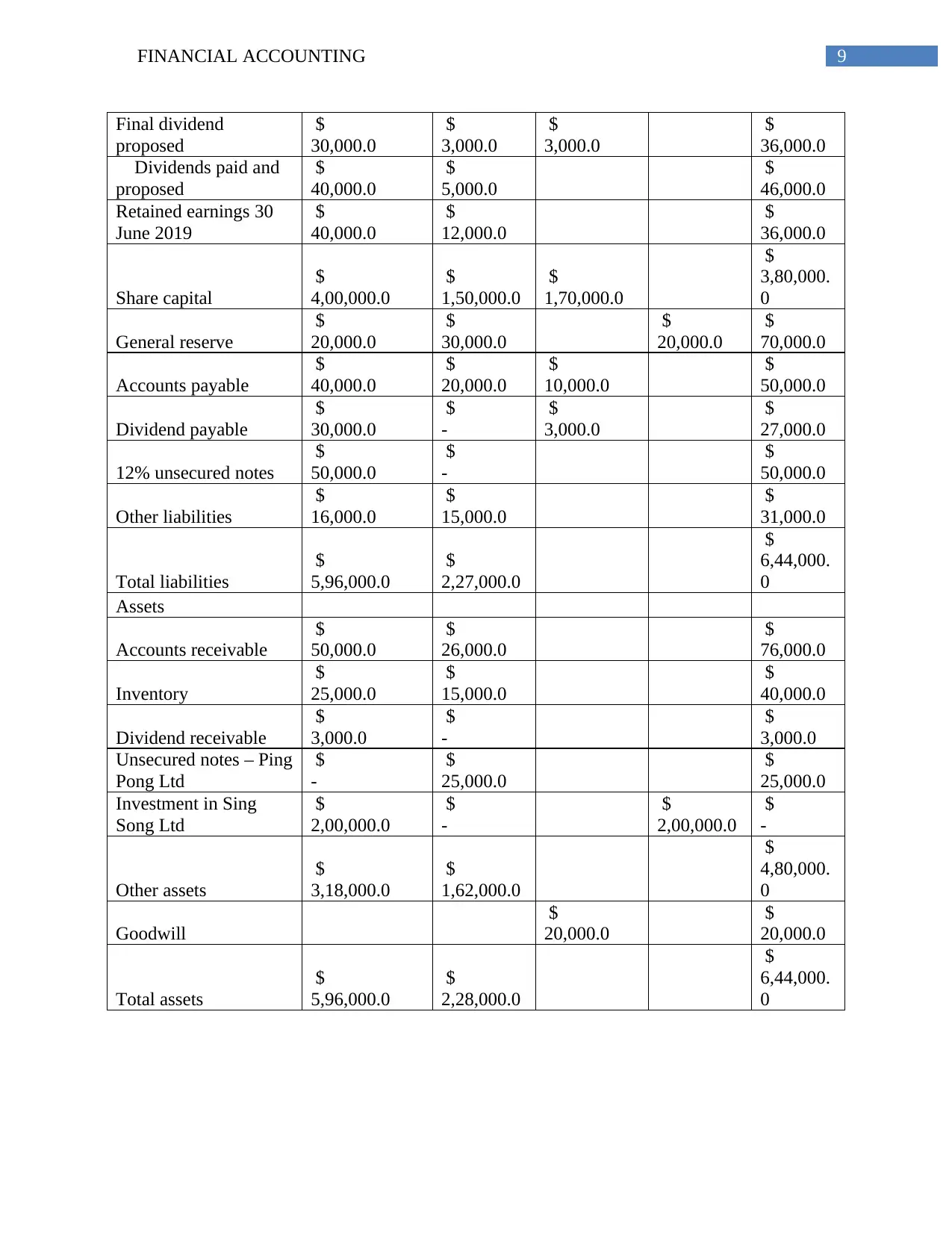

This document presents a comprehensive solution to a financial accounting assignment focusing on consolidation principles and accounting requirements. The assignment includes detailed analyses of acquisitions, specifically examining Smart Ltd and Positive Ltd. It involves preparing worksheet entries and consolidated financial statements, including balance sheets and income statements. The solution also addresses the complexities of intercompany transactions, such as the sale of inventory and plant assets, and their impact on consolidated figures. Furthermore, the assignment explores the consolidation of Ping Pong Ltd and Sing Song Ltd, covering similar aspects of worksheet entries, sales, cost of sales, and other expenses. The solution provides a step-by-step approach to ensure accurate financial reporting and compliance with accounting standards.

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.