Financial Accounting Assignment: Trial Balance & Financial Statements

VerifiedAdded on 2023/01/12

|24

|5045

|38

Homework Assignment

AI Summary

This assignment focuses on financial accounting principles, including the preparation of a trial balance, journal entries, and financial statements. The solution begins with a trial balance as of March 31, 2020, followed by journal entries for April 2020. Ledger balances are presented, and a second trial balance is prepared as of April 30, 2020. The assignment analyzes transactions, demonstrating how they impact the trial balance. Finally, the trial balance figures are applied to illustrate the components of financial statements, including the income statement, balance sheet, and cash flow statement. The report also explains the importance of each financial statement, and their use to make decisions, in addition to the role they play in providing critical financial information to business stakeholders.

FINANCIAL ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

Task 1.1........................................................................................................................................1

Task 1.2........................................................................................................................................1

Task 1.3........................................................................................................................................8

TASK 2............................................................................................................................................9

Task 2.1........................................................................................................................................9

Task 2.2......................................................................................................................................12

Task 2.3......................................................................................................................................13

Task 2.4......................................................................................................................................14

TASK 3..........................................................................................................................................14

Task 3.1 .....................................................................................................................................14

Task 3.2......................................................................................................................................15

Task 3.3 .....................................................................................................................................16

Task 3.4.....................................................................................................................................16

TASK 4..........................................................................................................................................18

Task 4.1 .....................................................................................................................................18

Task 4.2 .....................................................................................................................................18

Task 4.3......................................................................................................................................19

Task 4.4......................................................................................................................................19

CONCLUSION..............................................................................................................................20

REFERENCES..............................................................................................................................22

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

Task 1.1........................................................................................................................................1

Task 1.2........................................................................................................................................1

Task 1.3........................................................................................................................................8

TASK 2............................................................................................................................................9

Task 2.1........................................................................................................................................9

Task 2.2......................................................................................................................................12

Task 2.3......................................................................................................................................13

Task 2.4......................................................................................................................................14

TASK 3..........................................................................................................................................14

Task 3.1 .....................................................................................................................................14

Task 3.2......................................................................................................................................15

Task 3.3 .....................................................................................................................................16

Task 3.4.....................................................................................................................................16

TASK 4..........................................................................................................................................18

Task 4.1 .....................................................................................................................................18

Task 4.2 .....................................................................................................................................18

Task 4.3......................................................................................................................................19

Task 4.4......................................................................................................................................19

CONCLUSION..............................................................................................................................20

REFERENCES..............................................................................................................................22

INTRODUCTION

Financial accounting is the one of the branch of accounting with the purpose of having

record of the financial transactions of organization. This is based on the guidelines set and

includes collecting, summarizing and interpreting the financial information of the business. It

presents the complete report to the stakeholders in a specific format. It is primarily prepared for

external users like stakeholders, owners, lenders, government etc. It is prepared following the

common accounting standards as well as GAAP. In this report, the complete financial accounting

is carried out with respect to scenario given. It includes recording the financial transaction,

preparing trial balance and final accounts as per with principles, conventions & standards given

by accounting board. Also, a bank reconciliation statement is prepared in order to ensure that

entity record & bank records are same and correct.

TASK 1

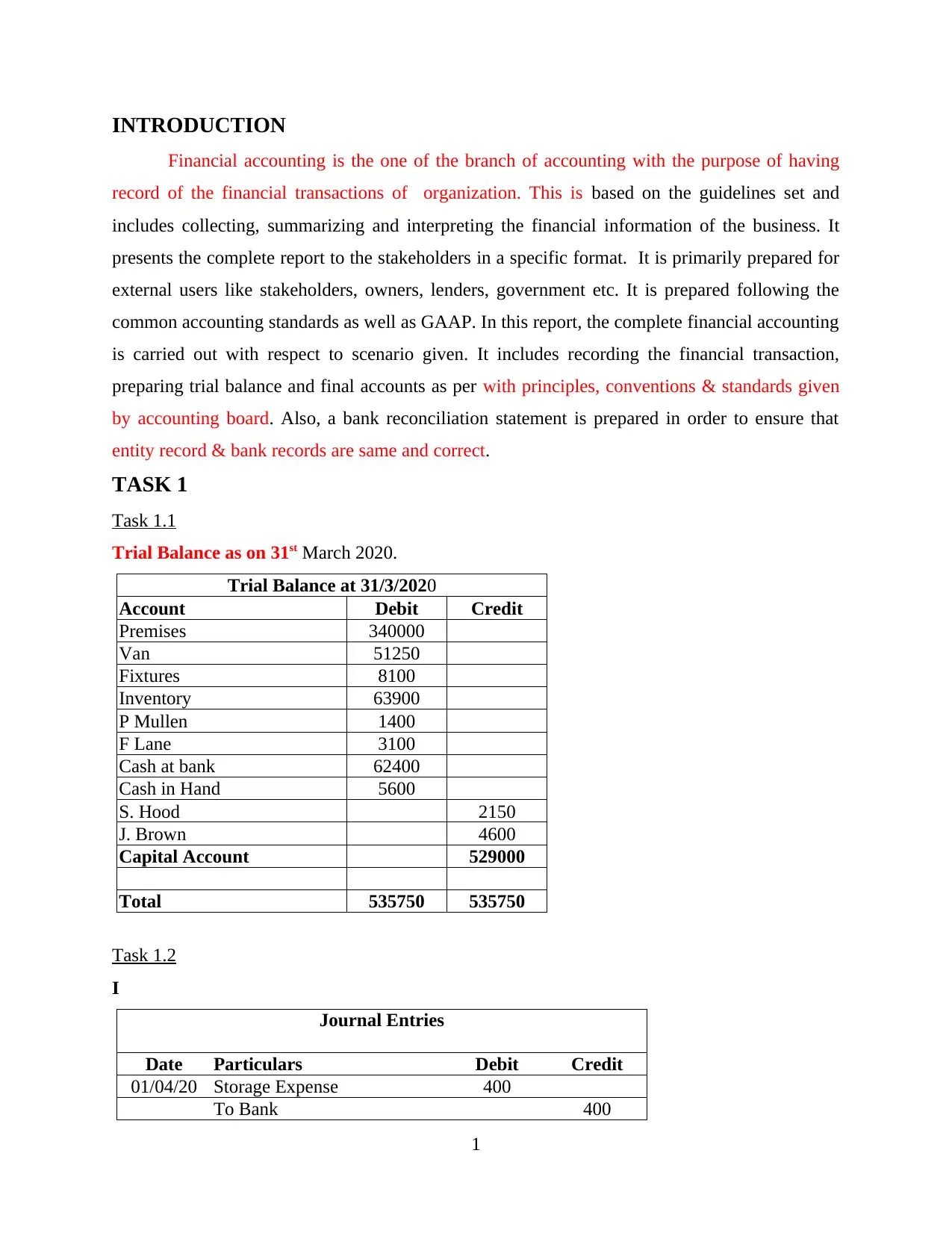

Task 1.1

Trial Balance as on 31st March 2020.

Trial Balance at 31/3/2020

Account Debit Credit

Premises 340000

Van 51250

Fixtures 8100

Inventory 63900

P Mullen 1400

F Lane 3100

Cash at bank 62400

Cash in Hand 5600

S. Hood 2150

J. Brown 4600

Capital Account 529000

Total 535750 535750

Task 1.2

I

Journal Entries

Date Particulars Debit Credit

01/04/20 Storage Expense 400

To Bank 400

1

Financial accounting is the one of the branch of accounting with the purpose of having

record of the financial transactions of organization. This is based on the guidelines set and

includes collecting, summarizing and interpreting the financial information of the business. It

presents the complete report to the stakeholders in a specific format. It is primarily prepared for

external users like stakeholders, owners, lenders, government etc. It is prepared following the

common accounting standards as well as GAAP. In this report, the complete financial accounting

is carried out with respect to scenario given. It includes recording the financial transaction,

preparing trial balance and final accounts as per with principles, conventions & standards given

by accounting board. Also, a bank reconciliation statement is prepared in order to ensure that

entity record & bank records are same and correct.

TASK 1

Task 1.1

Trial Balance as on 31st March 2020.

Trial Balance at 31/3/2020

Account Debit Credit

Premises 340000

Van 51250

Fixtures 8100

Inventory 63900

P Mullen 1400

F Lane 3100

Cash at bank 62400

Cash in Hand 5600

S. Hood 2150

J. Brown 4600

Capital Account 529000

Total 535750 535750

Task 1.2

I

Journal Entries

Date Particulars Debit Credit

01/04/20 Storage Expense 400

To Bank 400

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

02/04/20 Purchases 5000

To S. Hood a/c 1400

To D. Main a/c 2000

To R. Foot a/c 1600

03/04/20 T. Cole a/c 1650

F. Syme a/c 2000

J. Allen a/c 900

F. Lane a/c 750

To Sales a/c 5300

04/04/20 Motor Expenses 470

To Cash 470

07/04/20 Drawings 1500

To Cash 1500

09/04/20 T. Cole 650

J. Allen 1300

To Sales 1950

14/04/20 Van 28500

To Abel Motors 28500

16/04/20 Bank Ac 6500

To P. Mullen a/c 1400

To F. Lane a/c 3100

To F. Syme a/c 2000

22/04/20 Purchases 1800

To D. Main 1800

24/04/20 S. Hood 2150

J. Brown a/c 4600

R. Foot a/c 1400

To Bank 8150

27/04/20 Salaries 4800

To Bank 4800

30/04/20 Business Rates 1320

To Bank 1320

2

To S. Hood a/c 1400

To D. Main a/c 2000

To R. Foot a/c 1600

03/04/20 T. Cole a/c 1650

F. Syme a/c 2000

J. Allen a/c 900

F. Lane a/c 750

To Sales a/c 5300

04/04/20 Motor Expenses 470

To Cash 470

07/04/20 Drawings 1500

To Cash 1500

09/04/20 T. Cole 650

J. Allen 1300

To Sales 1950

14/04/20 Van 28500

To Abel Motors 28500

16/04/20 Bank Ac 6500

To P. Mullen a/c 1400

To F. Lane a/c 3100

To F. Syme a/c 2000

22/04/20 Purchases 1800

To D. Main 1800

24/04/20 S. Hood 2150

J. Brown a/c 4600

R. Foot a/c 1400

To Bank 8150

27/04/20 Salaries 4800

To Bank 4800

30/04/20 Business Rates 1320

To Bank 1320

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

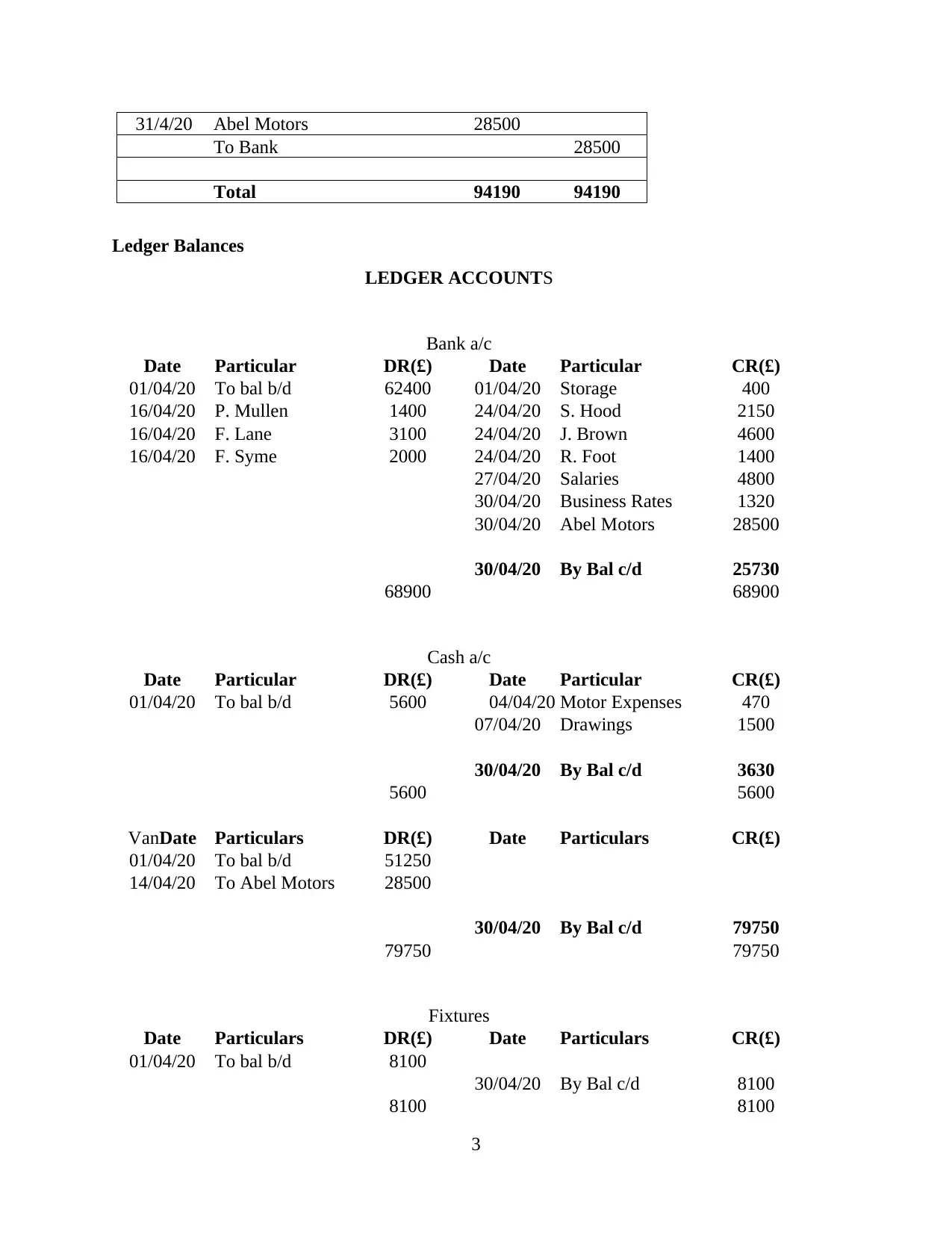

31/4/20 Abel Motors 28500

To Bank 28500

Total 94190 94190

Ledger Balances

LEDGER ACCOUNTS

Bank a/c

Date Particular DR(£) Date Particular CR(£)

01/04/20 To bal b/d 62400 01/04/20 Storage 400

16/04/20 P. Mullen 1400 24/04/20 S. Hood 2150

16/04/20 F. Lane 3100 24/04/20 J. Brown 4600

16/04/20 F. Syme 2000 24/04/20 R. Foot 1400

27/04/20 Salaries 4800

30/04/20 Business Rates 1320

30/04/20 Abel Motors 28500

30/04/20 By Bal c/d 25730

68900 68900

Cash a/c

Date Particular DR(£) Date Particular CR(£)

01/04/20 To bal b/d 5600 04/04/20 Motor Expenses 470

07/04/20 Drawings 1500

30/04/20 By Bal c/d 3630

5600 5600

VanDate Particulars DR(£) Date Particulars CR(£)

01/04/20 To bal b/d 51250

14/04/20 To Abel Motors 28500

30/04/20 By Bal c/d 79750

79750 79750

Fixtures

Date Particulars DR(£) Date Particulars CR(£)

01/04/20 To bal b/d 8100

30/04/20 By Bal c/d 8100

8100 8100

3

To Bank 28500

Total 94190 94190

Ledger Balances

LEDGER ACCOUNTS

Bank a/c

Date Particular DR(£) Date Particular CR(£)

01/04/20 To bal b/d 62400 01/04/20 Storage 400

16/04/20 P. Mullen 1400 24/04/20 S. Hood 2150

16/04/20 F. Lane 3100 24/04/20 J. Brown 4600

16/04/20 F. Syme 2000 24/04/20 R. Foot 1400

27/04/20 Salaries 4800

30/04/20 Business Rates 1320

30/04/20 Abel Motors 28500

30/04/20 By Bal c/d 25730

68900 68900

Cash a/c

Date Particular DR(£) Date Particular CR(£)

01/04/20 To bal b/d 5600 04/04/20 Motor Expenses 470

07/04/20 Drawings 1500

30/04/20 By Bal c/d 3630

5600 5600

VanDate Particulars DR(£) Date Particulars CR(£)

01/04/20 To bal b/d 51250

14/04/20 To Abel Motors 28500

30/04/20 By Bal c/d 79750

79750 79750

Fixtures

Date Particulars DR(£) Date Particulars CR(£)

01/04/20 To bal b/d 8100

30/04/20 By Bal c/d 8100

8100 8100

3

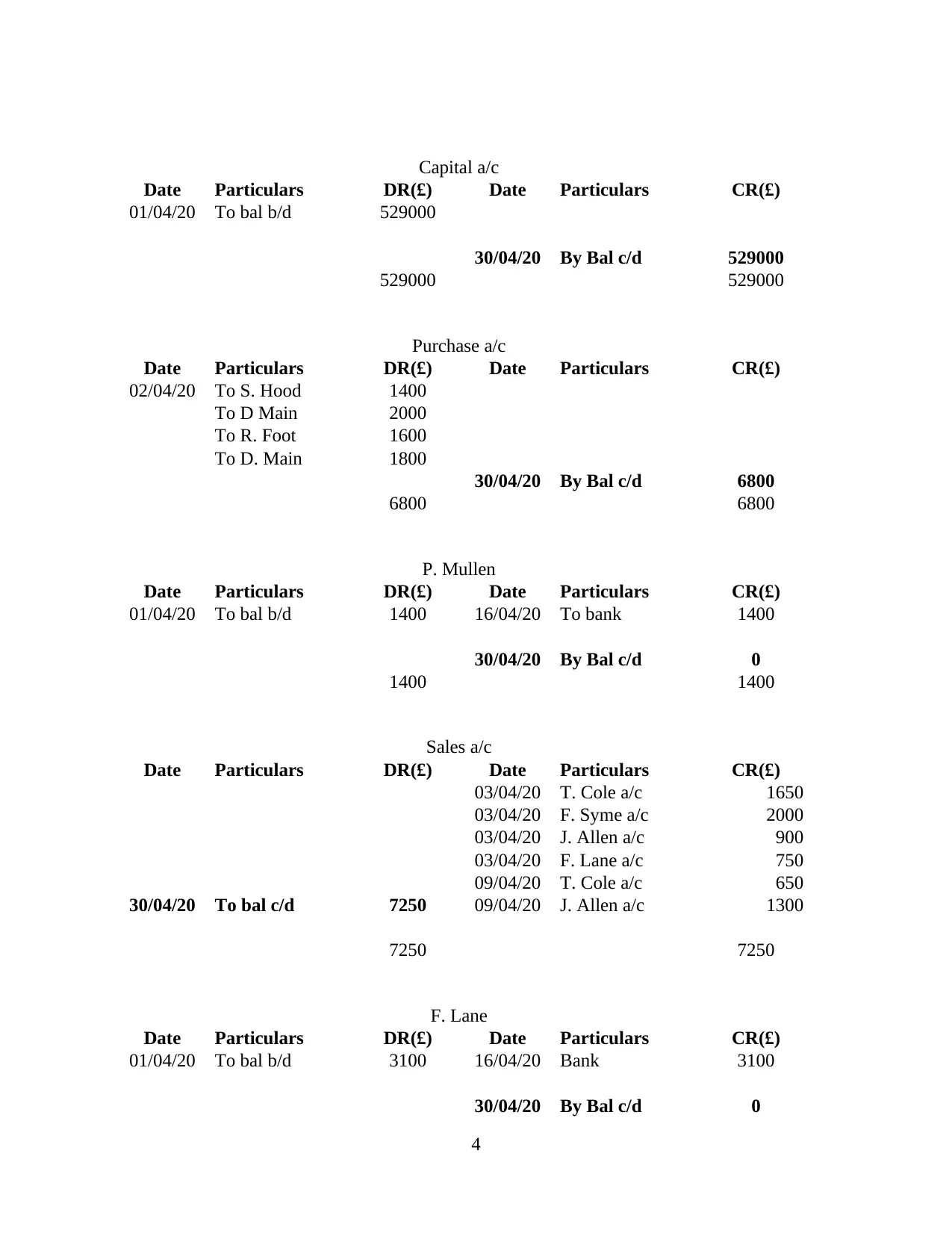

Capital a/c

Date Particulars DR(£) Date Particulars CR(£)

01/04/20 To bal b/d 529000

30/04/20 By Bal c/d 529000

529000 529000

Purchase a/c

Date Particulars DR(£) Date Particulars CR(£)

02/04/20 To S. Hood 1400

To D Main 2000

To R. Foot 1600

To D. Main 1800

30/04/20 By Bal c/d 6800

6800 6800

P. Mullen

Date Particulars DR(£) Date Particulars CR(£)

01/04/20 To bal b/d 1400 16/04/20 To bank 1400

30/04/20 By Bal c/d 0

1400 1400

Sales a/c

Date Particulars DR(£) Date Particulars CR(£)

03/04/20 T. Cole a/c 1650

03/04/20 F. Syme a/c 2000

03/04/20 J. Allen a/c 900

03/04/20 F. Lane a/c 750

09/04/20 T. Cole a/c 650

30/04/20 To bal c/d 7250 09/04/20 J. Allen a/c 1300

7250 7250

F. Lane

Date Particulars DR(£) Date Particulars CR(£)

01/04/20 To bal b/d 3100 16/04/20 Bank 3100

30/04/20 By Bal c/d 0

4

Date Particulars DR(£) Date Particulars CR(£)

01/04/20 To bal b/d 529000

30/04/20 By Bal c/d 529000

529000 529000

Purchase a/c

Date Particulars DR(£) Date Particulars CR(£)

02/04/20 To S. Hood 1400

To D Main 2000

To R. Foot 1600

To D. Main 1800

30/04/20 By Bal c/d 6800

6800 6800

P. Mullen

Date Particulars DR(£) Date Particulars CR(£)

01/04/20 To bal b/d 1400 16/04/20 To bank 1400

30/04/20 By Bal c/d 0

1400 1400

Sales a/c

Date Particulars DR(£) Date Particulars CR(£)

03/04/20 T. Cole a/c 1650

03/04/20 F. Syme a/c 2000

03/04/20 J. Allen a/c 900

03/04/20 F. Lane a/c 750

09/04/20 T. Cole a/c 650

30/04/20 To bal c/d 7250 09/04/20 J. Allen a/c 1300

7250 7250

F. Lane

Date Particulars DR(£) Date Particulars CR(£)

01/04/20 To bal b/d 3100 16/04/20 Bank 3100

30/04/20 By Bal c/d 0

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3100 3100

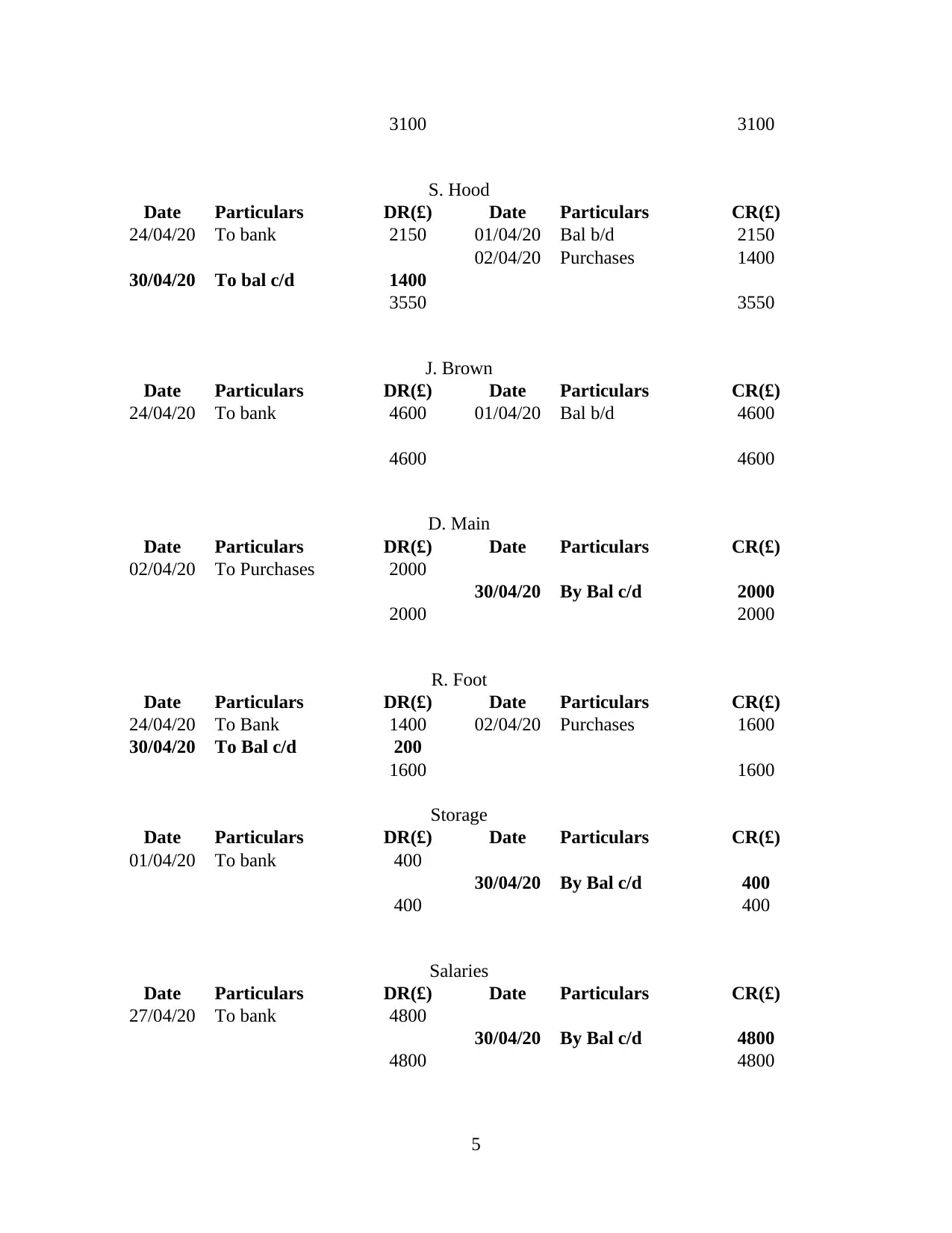

S. Hood

Date Particulars DR(£) Date Particulars CR(£)

24/04/20 To bank 2150 01/04/20 Bal b/d 2150

02/04/20 Purchases 1400

30/04/20 To bal c/d 1400

3550 3550

J. Brown

Date Particulars DR(£) Date Particulars CR(£)

24/04/20 To bank 4600 01/04/20 Bal b/d 4600

4600 4600

D. Main

Date Particulars DR(£) Date Particulars CR(£)

02/04/20 To Purchases 2000

30/04/20 By Bal c/d 2000

2000 2000

R. Foot

Date Particulars DR(£) Date Particulars CR(£)

24/04/20 To Bank 1400 02/04/20 Purchases 1600

30/04/20 To Bal c/d 200

1600 1600

Storage

Date Particulars DR(£) Date Particulars CR(£)

01/04/20 To bank 400

30/04/20 By Bal c/d 400

400 400

Salaries

Date Particulars DR(£) Date Particulars CR(£)

27/04/20 To bank 4800

30/04/20 By Bal c/d 4800

4800 4800

5

S. Hood

Date Particulars DR(£) Date Particulars CR(£)

24/04/20 To bank 2150 01/04/20 Bal b/d 2150

02/04/20 Purchases 1400

30/04/20 To bal c/d 1400

3550 3550

J. Brown

Date Particulars DR(£) Date Particulars CR(£)

24/04/20 To bank 4600 01/04/20 Bal b/d 4600

4600 4600

D. Main

Date Particulars DR(£) Date Particulars CR(£)

02/04/20 To Purchases 2000

30/04/20 By Bal c/d 2000

2000 2000

R. Foot

Date Particulars DR(£) Date Particulars CR(£)

24/04/20 To Bank 1400 02/04/20 Purchases 1600

30/04/20 To Bal c/d 200

1600 1600

Storage

Date Particulars DR(£) Date Particulars CR(£)

01/04/20 To bank 400

30/04/20 By Bal c/d 400

400 400

Salaries

Date Particulars DR(£) Date Particulars CR(£)

27/04/20 To bank 4800

30/04/20 By Bal c/d 4800

4800 4800

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Motor Expenses

Date Particulars DR(£) Date Particulars CR(£)

04/04/20 To Cash 470

30/04/20 By Bal c/d 470

470 470

Business Rates

Date Particulars DR(£) Date Particulars CR(£)

30/04/20 To Bank 1320

30/04/20 By Bal c/d 1320

1320 1320

T, Cole

Date Particulars DR(£) Date Particulars CR(£)

03/04/20 To Sales 1650

09/04/20 To Sales 650

30/04/20 By Bal c/d 2300

2300 2300

J. Allen

Date Particulars DR(£) Date Particulars CR(£)

03/04/20 To Sales 900

09/04/20 To Sales 1300

30/04/20 By Bal c/d 2200

2200 2200

F. Syme

Date Particulars DR(£) Date Particulars CR(£)

03/04/20 To Sales 2000 16/04/20 To bank 2000

2000 2000

Drawings

Date Particulars DR(£) Date Particulars CR(£)

07/04/20 To Cash 1500

30/04/20 By Bal c/d 1500

1500 1500

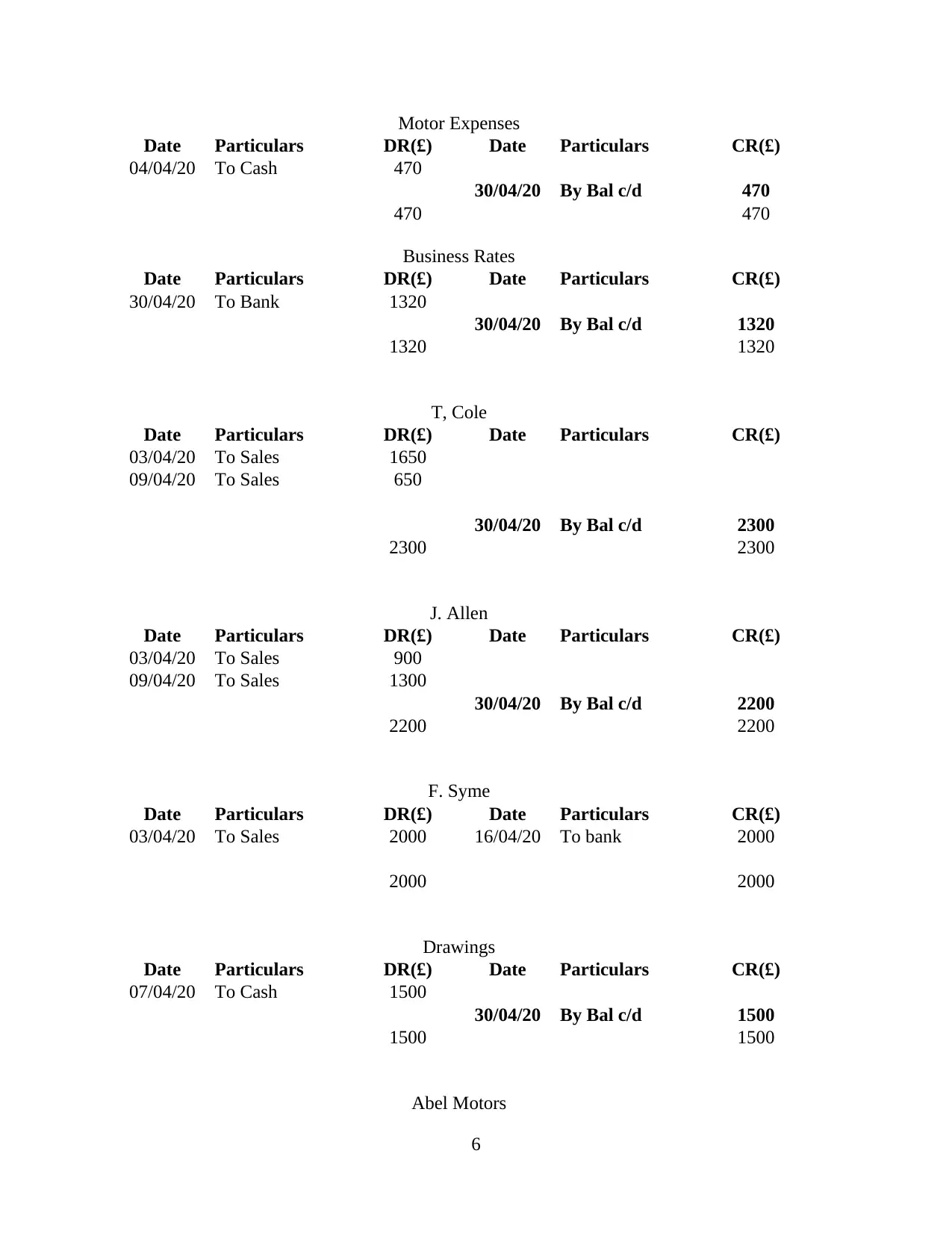

Abel Motors

6

Date Particulars DR(£) Date Particulars CR(£)

04/04/20 To Cash 470

30/04/20 By Bal c/d 470

470 470

Business Rates

Date Particulars DR(£) Date Particulars CR(£)

30/04/20 To Bank 1320

30/04/20 By Bal c/d 1320

1320 1320

T, Cole

Date Particulars DR(£) Date Particulars CR(£)

03/04/20 To Sales 1650

09/04/20 To Sales 650

30/04/20 By Bal c/d 2300

2300 2300

J. Allen

Date Particulars DR(£) Date Particulars CR(£)

03/04/20 To Sales 900

09/04/20 To Sales 1300

30/04/20 By Bal c/d 2200

2200 2200

F. Syme

Date Particulars DR(£) Date Particulars CR(£)

03/04/20 To Sales 2000 16/04/20 To bank 2000

2000 2000

Drawings

Date Particulars DR(£) Date Particulars CR(£)

07/04/20 To Cash 1500

30/04/20 By Bal c/d 1500

1500 1500

Abel Motors

6

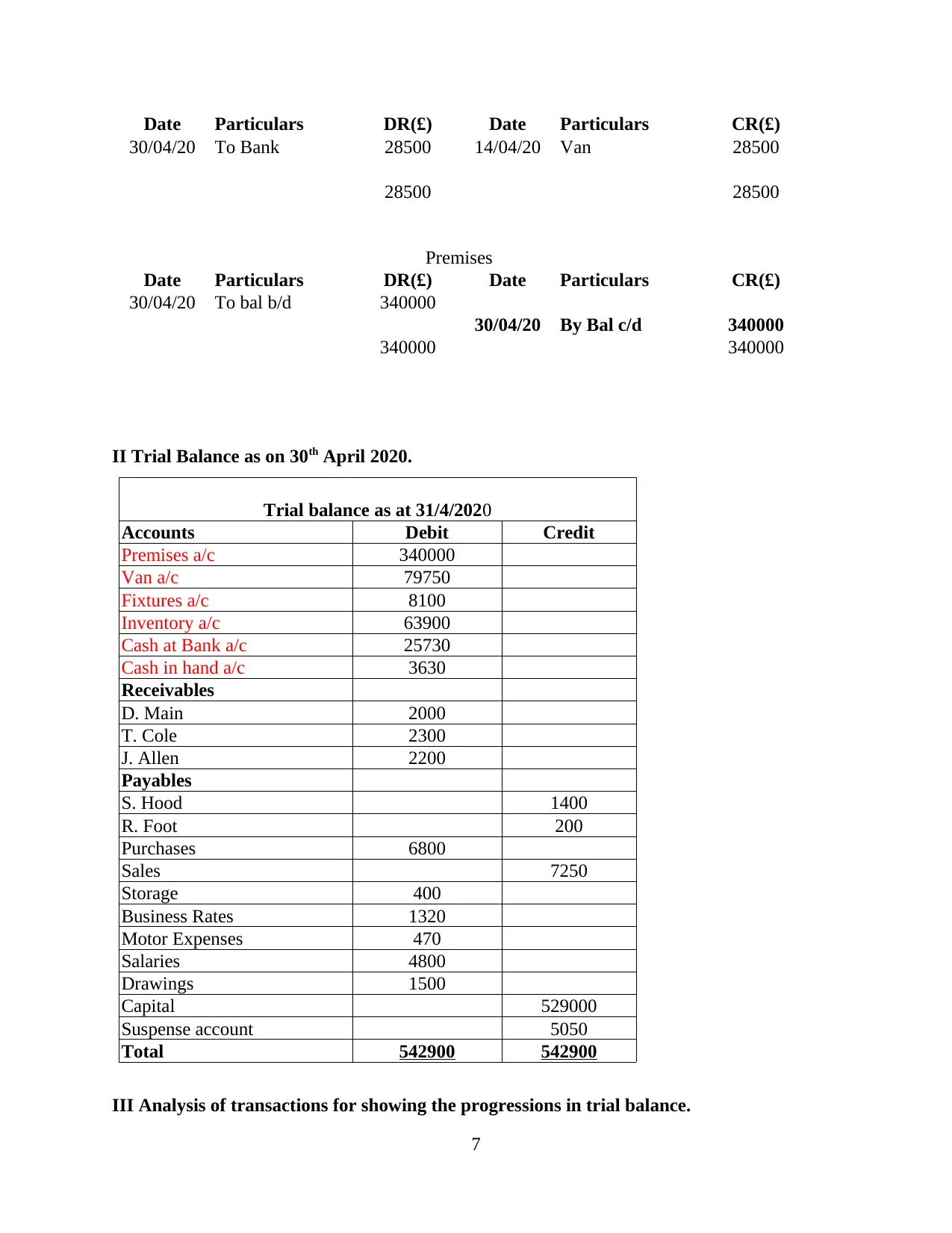

Date Particulars DR(£) Date Particulars CR(£)

30/04/20 To Bank 28500 14/04/20 Van 28500

28500 28500

Premises

Date Particulars DR(£) Date Particulars CR(£)

30/04/20 To bal b/d 340000

30/04/20 By Bal c/d 340000

340000 340000

II Trial Balance as on 30th April 2020.

Trial balance as at 31/4/2020

Accounts Debit Credit

Premises a/c 340000

Van a/c 79750

Fixtures a/c 8100

Inventory a/c 63900

Cash at Bank a/c 25730

Cash in hand a/c 3630

Receivables

D. Main 2000

T. Cole 2300

J. Allen 2200

Payables

S. Hood 1400

R. Foot 200

Purchases 6800

Sales 7250

Storage 400

Business Rates 1320

Motor Expenses 470

Salaries 4800

Drawings 1500

Capital 529000

Suspense account 5050

Total 542900 542900

III Analysis of transactions for showing the progressions in trial balance.

7

30/04/20 To Bank 28500 14/04/20 Van 28500

28500 28500

Premises

Date Particulars DR(£) Date Particulars CR(£)

30/04/20 To bal b/d 340000

30/04/20 By Bal c/d 340000

340000 340000

II Trial Balance as on 30th April 2020.

Trial balance as at 31/4/2020

Accounts Debit Credit

Premises a/c 340000

Van a/c 79750

Fixtures a/c 8100

Inventory a/c 63900

Cash at Bank a/c 25730

Cash in hand a/c 3630

Receivables

D. Main 2000

T. Cole 2300

J. Allen 2200

Payables

S. Hood 1400

R. Foot 200

Purchases 6800

Sales 7250

Storage 400

Business Rates 1320

Motor Expenses 470

Salaries 4800

Drawings 1500

Capital 529000

Suspense account 5050

Total 542900 542900

III Analysis of transactions for showing the progressions in trial balance.

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

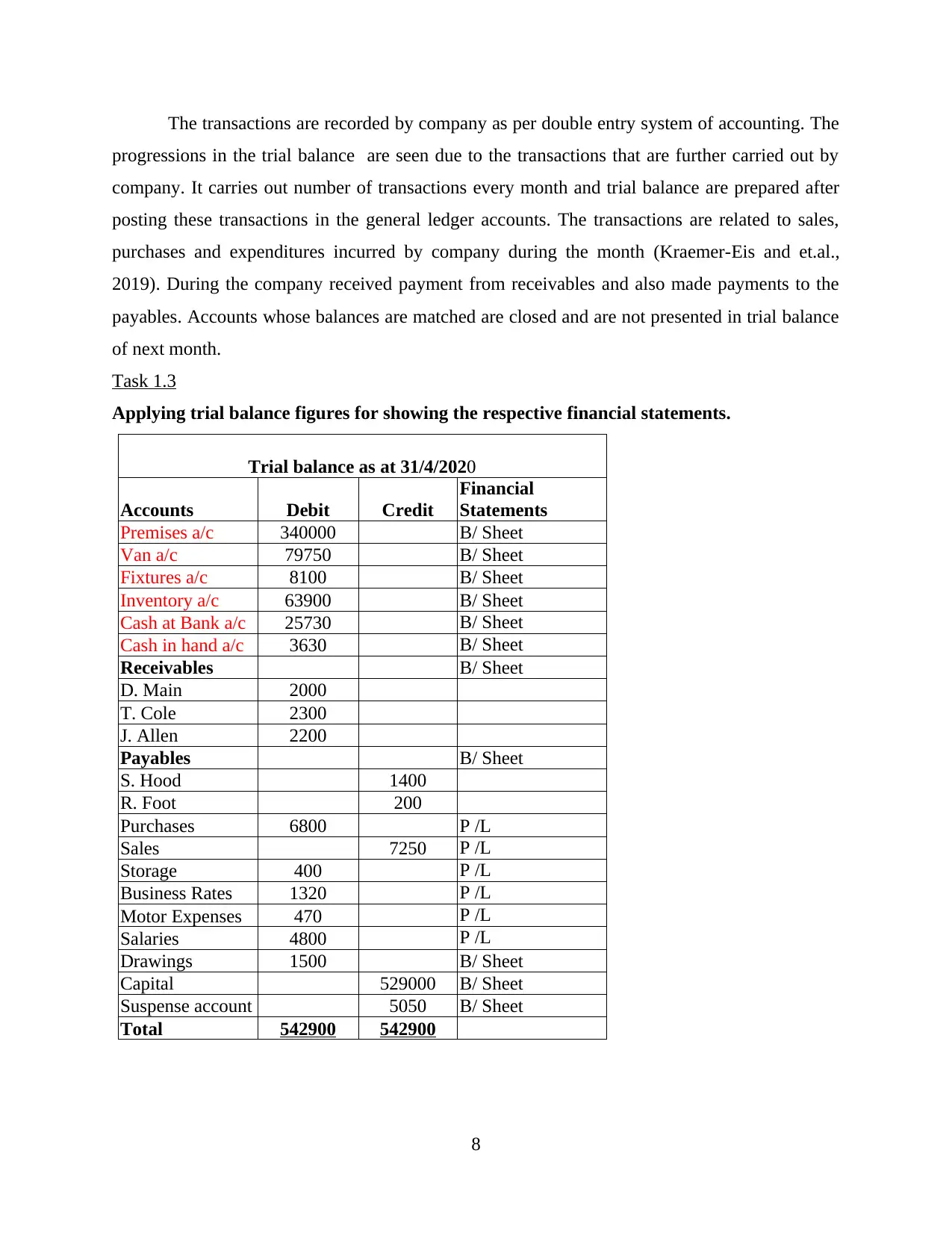

The transactions are recorded by company as per double entry system of accounting. The

progressions in the trial balance are seen due to the transactions that are further carried out by

company. It carries out number of transactions every month and trial balance are prepared after

posting these transactions in the general ledger accounts. The transactions are related to sales,

purchases and expenditures incurred by company during the month (Kraemer-Eis and et.al.,

2019). During the company received payment from receivables and also made payments to the

payables. Accounts whose balances are matched are closed and are not presented in trial balance

of next month.

Task 1.3

Applying trial balance figures for showing the respective financial statements.

Trial balance as at 31/4/2020

Accounts Debit Credit

Financial

Statements

Premises a/c 340000 B/ Sheet

Van a/c 79750 B/ Sheet

Fixtures a/c 8100 B/ Sheet

Inventory a/c 63900 B/ Sheet

Cash at Bank a/c 25730 B/ Sheet

Cash in hand a/c 3630 B/ Sheet

Receivables B/ Sheet

D. Main 2000

T. Cole 2300

J. Allen 2200

Payables B/ Sheet

S. Hood 1400

R. Foot 200

Purchases 6800 P /L

Sales 7250 P /L

Storage 400 P /L

Business Rates 1320 P /L

Motor Expenses 470 P /L

Salaries 4800 P /L

Drawings 1500 B/ Sheet

Capital 529000 B/ Sheet

Suspense account 5050 B/ Sheet

Total 542900 542900

8

progressions in the trial balance are seen due to the transactions that are further carried out by

company. It carries out number of transactions every month and trial balance are prepared after

posting these transactions in the general ledger accounts. The transactions are related to sales,

purchases and expenditures incurred by company during the month (Kraemer-Eis and et.al.,

2019). During the company received payment from receivables and also made payments to the

payables. Accounts whose balances are matched are closed and are not presented in trial balance

of next month.

Task 1.3

Applying trial balance figures for showing the respective financial statements.

Trial balance as at 31/4/2020

Accounts Debit Credit

Financial

Statements

Premises a/c 340000 B/ Sheet

Van a/c 79750 B/ Sheet

Fixtures a/c 8100 B/ Sheet

Inventory a/c 63900 B/ Sheet

Cash at Bank a/c 25730 B/ Sheet

Cash in hand a/c 3630 B/ Sheet

Receivables B/ Sheet

D. Main 2000

T. Cole 2300

J. Allen 2200

Payables B/ Sheet

S. Hood 1400

R. Foot 200

Purchases 6800 P /L

Sales 7250 P /L

Storage 400 P /L

Business Rates 1320 P /L

Motor Expenses 470 P /L

Salaries 4800 P /L

Drawings 1500 B/ Sheet

Capital 529000 B/ Sheet

Suspense account 5050 B/ Sheet

Total 542900 542900

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TASK 2

Task 2.1

Financial Accounting Statements prepared by business entities.

Financial accounting refers to the process of recording transactions carried out by the

business during the given financial year. Every business is required to keep a track record of the

business transactions undertaken by the company during the financial year. The transactions are

recorded by passing a journal entry. From these journals balances are posted in the ledger

accounts by the businesses. After the years end closing balance are posted in the trial balance

from which the balances are transferred in their respective trial balances. The financial statement

represents the summary of overall transactions carried out by the business during the year.

Financial transactions contain the details of company of its performance and position

during the relevant accounting year. Financial statements are prepared by the organisation for

analysing the performance of the business and making strategies for increasing the efficiency for

having effective sustainability in the business. Statements are prepared by the business in

accordance with accounting standards and accounting principles. These financial statements

provide the information regarding internal functioning of company.

Financial statements are prepared by the organisation for giving the stakeholders of the

business information regarding the performance and position of the company. These statements

are prepared to ensure that the financial position of the company is strong and effective.

Financial statements provide important information regarding the business to make effective

controls for the decisions making. This enables the analysts to assess the business for having

effective investments for the investors.

Companies are preparing financial statements prepared by the organisations are mainly

of three types that are profit or loss, balance sheet and the cash flow statement. All these

financial statements are having great importance for organisation (Adhikary and Kutsuna, 2016).

They provide important financial information to the business management and also to the

external users. These information are important for decision making related to the users of

financial statements.

Income Statement

Other name of Income statement is profit or loss statement. They provide information

related to expenditures & income of firm carried out during the year. Income statement represent

9

Task 2.1

Financial Accounting Statements prepared by business entities.

Financial accounting refers to the process of recording transactions carried out by the

business during the given financial year. Every business is required to keep a track record of the

business transactions undertaken by the company during the financial year. The transactions are

recorded by passing a journal entry. From these journals balances are posted in the ledger

accounts by the businesses. After the years end closing balance are posted in the trial balance

from which the balances are transferred in their respective trial balances. The financial statement

represents the summary of overall transactions carried out by the business during the year.

Financial transactions contain the details of company of its performance and position

during the relevant accounting year. Financial statements are prepared by the organisation for

analysing the performance of the business and making strategies for increasing the efficiency for

having effective sustainability in the business. Statements are prepared by the business in

accordance with accounting standards and accounting principles. These financial statements

provide the information regarding internal functioning of company.

Financial statements are prepared by the organisation for giving the stakeholders of the

business information regarding the performance and position of the company. These statements

are prepared to ensure that the financial position of the company is strong and effective.

Financial statements provide important information regarding the business to make effective

controls for the decisions making. This enables the analysts to assess the business for having

effective investments for the investors.

Companies are preparing financial statements prepared by the organisations are mainly

of three types that are profit or loss, balance sheet and the cash flow statement. All these

financial statements are having great importance for organisation (Adhikary and Kutsuna, 2016).

They provide important financial information to the business management and also to the

external users. These information are important for decision making related to the users of

financial statements.

Income Statement

Other name of Income statement is profit or loss statement. They provide information

related to expenditures & income of firm carried out during the year. Income statement represent

9

the actual outcomes of carrying out the business during the given specific period. It shows

whether the business was profitable or not for company. This shows ability of the company in

managing the operation from available resources. This is essential for users of the financial

statements to identify the profitability of the business. This gives important platform to the users

for making business decisions (Kapinos, Gurley-Calvez and Kapinos, 2016). Income statements

records each & every transaction that are carried out by business enterprise. Users can identify

clearly the revenues generated from the sales, the cost of goods sold, gross profits, operating

expense, finance cost and many other items. Every user takes up the information as per the needs

from the financial statements. There are number of information related to the business operations

which represents the capabilities of company in competing in market with the challenges of

business environment.

Statement of the financial Position

Statement is prepared by organisations for giving the interested parties idea about the

position of entity and its condition. The balance sheet provides essential informations that is used

by the experts and management for analysing the financial stability as well as business

performance. Balance sheet is an accounting equation where the assets of balance sheet should

always be equal to the liabilities and shareholder's equity. The statement is used by organisations

and other users for identifying how responsibly company is managing its resources and also how

efficiently it is financing them (Robyn and et.al., 2019). Investors analyse the capital structure of

company as it gives important insights for identifying whether sufficient funds are available are

not running the business. The balance sheet represent the assets and liabilities that contains

information regarding the different balances that are presented in the financial statements. The

balance enable the users to make comparisons between the companies for assessing the financial

health of organisations.

Cash Flow statements

Cash flow statement is one of the three financial statements that is prepared by

organisations. It presents the inflow and outflow of cash from the businesses. Cash flows

statements represents the areas where the cash is flowing of company. It contains information

related to the different activities where the cash is flowing among the three activities. Cash flow

statement consists of operating activities that represents the cash flow in business operations and

working capital changes. Investing activities of company represents the flow of cash towards the

10

whether the business was profitable or not for company. This shows ability of the company in

managing the operation from available resources. This is essential for users of the financial

statements to identify the profitability of the business. This gives important platform to the users

for making business decisions (Kapinos, Gurley-Calvez and Kapinos, 2016). Income statements

records each & every transaction that are carried out by business enterprise. Users can identify

clearly the revenues generated from the sales, the cost of goods sold, gross profits, operating

expense, finance cost and many other items. Every user takes up the information as per the needs

from the financial statements. There are number of information related to the business operations

which represents the capabilities of company in competing in market with the challenges of

business environment.

Statement of the financial Position

Statement is prepared by organisations for giving the interested parties idea about the

position of entity and its condition. The balance sheet provides essential informations that is used

by the experts and management for analysing the financial stability as well as business

performance. Balance sheet is an accounting equation where the assets of balance sheet should

always be equal to the liabilities and shareholder's equity. The statement is used by organisations

and other users for identifying how responsibly company is managing its resources and also how

efficiently it is financing them (Robyn and et.al., 2019). Investors analyse the capital structure of

company as it gives important insights for identifying whether sufficient funds are available are

not running the business. The balance sheet represent the assets and liabilities that contains

information regarding the different balances that are presented in the financial statements. The

balance enable the users to make comparisons between the companies for assessing the financial

health of organisations.

Cash Flow statements

Cash flow statement is one of the three financial statements that is prepared by

organisations. It presents the inflow and outflow of cash from the businesses. Cash flows

statements represents the areas where the cash is flowing of company. It contains information

related to the different activities where the cash is flowing among the three activities. Cash flow

statement consists of operating activities that represents the cash flow in business operations and

working capital changes. Investing activities of company represents the flow of cash towards the

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 24

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.