Advanced Financial Accounting Report: Impairment, Leases, and IFRS 16

VerifiedAdded on 2020/05/28

|12

|2815

|329

Report

AI Summary

This advanced financial accounting report analyzes the financial practices of Bradken Limited, focusing on impairment testing of intangible assets and goodwill, as well as the adoption of AASB 136. The report details the company's methodologies for calculating value in use, the assumptions made in impairment testing, and the impact of impairment expenses on financial results. Furthermore, the report examines the implications of the new lease standard, IFRS 16, contrasting it with the former IAS 17, and discussing the incentives for companies to classify leases as operating or financing. It highlights the challenges and controversies associated with IFRS 16, including its potential impact on companies' balance sheets, financial ratios, and leasing behavior, while also emphasizing the increased transparency and faithfulness it brings to financial reporting, enabling investors to make more informed decisions. The report underscores the importance of understanding the complexities of financial accounting standards for accurate financial analysis.

Running head: ADVANCED FINANCIAL ACCOUNTING

Advanced financial accounting

Name of the university

Name of the student

Authors note

Advanced financial accounting

Name of the university

Name of the student

Authors note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

ADVANCED FINANCIAL ACCOUNTING

Table of Contents

Part A:..............................................................................................................................................2

Requirement i).................................................................................................................................2

Requirement ii)................................................................................................................................2

Requirement iii)...............................................................................................................................3

Requirement iv)...............................................................................................................................3

Requirement vii)..............................................................................................................................5

Requirement viii).............................................................................................................................5

Part B:..............................................................................................................................................6

Requirement i).................................................................................................................................6

Requirement ii)................................................................................................................................6

Requirement iii)...............................................................................................................................7

Requirement iv)...............................................................................................................................7

References list:...............................................................................................................................10

ADVANCED FINANCIAL ACCOUNTING

Table of Contents

Part A:..............................................................................................................................................2

Requirement i).................................................................................................................................2

Requirement ii)................................................................................................................................2

Requirement iii)...............................................................................................................................3

Requirement iv)...............................................................................................................................3

Requirement vii)..............................................................................................................................5

Requirement viii).............................................................................................................................5

Part B:..............................................................................................................................................6

Requirement i).................................................................................................................................6

Requirement ii)................................................................................................................................6

Requirement iii)...............................................................................................................................7

Requirement iv)...............................................................................................................................7

References list:...............................................................................................................................10

2

ADVANCED FINANCIAL ACCOUNTING

Part A:

Requirement i)

Intangible assets and goodwill of Bradken limited having indefinite useful life are tested

for impairment on annual basis as indicated by any event or by change in circumstances. S0ome

other assets are assessed for the impairment when it is indicted that recoverable amount will be

exceeding its carrying amount. Impairment of other financial assets are done when there is

objective evidence of occurrence of one more events. For the purpose of impairment testing,

allocation of goodwill is done to cash generating unit. Impairment value of goodwill and other

intangible assets for the financial year 2016 and 2015 stood at $ 64103 million and $ 167182

million. Total amount of impairment that was recorded on intangibles and goodwill is recorded

at $ 64.1 million. Moreover, impairment of investment has also been done during financial year

2016 for Austin engineering limited. Total amount of investment impairment for the year 2016

stood at $ 128182. Amount recorded in impairment of available for sale financial assets for 2016

is recorded at $ 6593 (Bradken.com 2018).

Requirement ii)

Impairment testing is conducted by Bradken limited for intangibles along with goodwill

by the identification of same that are acquired in business combination based on the estimates of

management about net present value of estimated future cash flows of assets. It also takes into

consideration the combinations of independent valuations in some cases. Computation of value

in use forms the basis of determination of recoverable amount of cash generating units.

Impairment testing of organization is done by the estimates and all the calculations relating to

impairment require the use of assumptions. Management of the group prepare financial forecast

ADVANCED FINANCIAL ACCOUNTING

Part A:

Requirement i)

Intangible assets and goodwill of Bradken limited having indefinite useful life are tested

for impairment on annual basis as indicated by any event or by change in circumstances. S0ome

other assets are assessed for the impairment when it is indicted that recoverable amount will be

exceeding its carrying amount. Impairment of other financial assets are done when there is

objective evidence of occurrence of one more events. For the purpose of impairment testing,

allocation of goodwill is done to cash generating unit. Impairment value of goodwill and other

intangible assets for the financial year 2016 and 2015 stood at $ 64103 million and $ 167182

million. Total amount of impairment that was recorded on intangibles and goodwill is recorded

at $ 64.1 million. Moreover, impairment of investment has also been done during financial year

2016 for Austin engineering limited. Total amount of investment impairment for the year 2016

stood at $ 128182. Amount recorded in impairment of available for sale financial assets for 2016

is recorded at $ 6593 (Bradken.com 2018).

Requirement ii)

Impairment testing is conducted by Bradken limited for intangibles along with goodwill

by the identification of same that are acquired in business combination based on the estimates of

management about net present value of estimated future cash flows of assets. It also takes into

consideration the combinations of independent valuations in some cases. Computation of value

in use forms the basis of determination of recoverable amount of cash generating units.

Impairment testing of organization is done by the estimates and all the calculations relating to

impairment require the use of assumptions. Management of the group prepare financial forecast

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

ADVANCED FINANCIAL ACCOUNTING

for projecting financial cash flows for a period of five years. Extrapolation of cash flows beyond

the five-year period using perpetual growth rate (Bradken.com 2018).

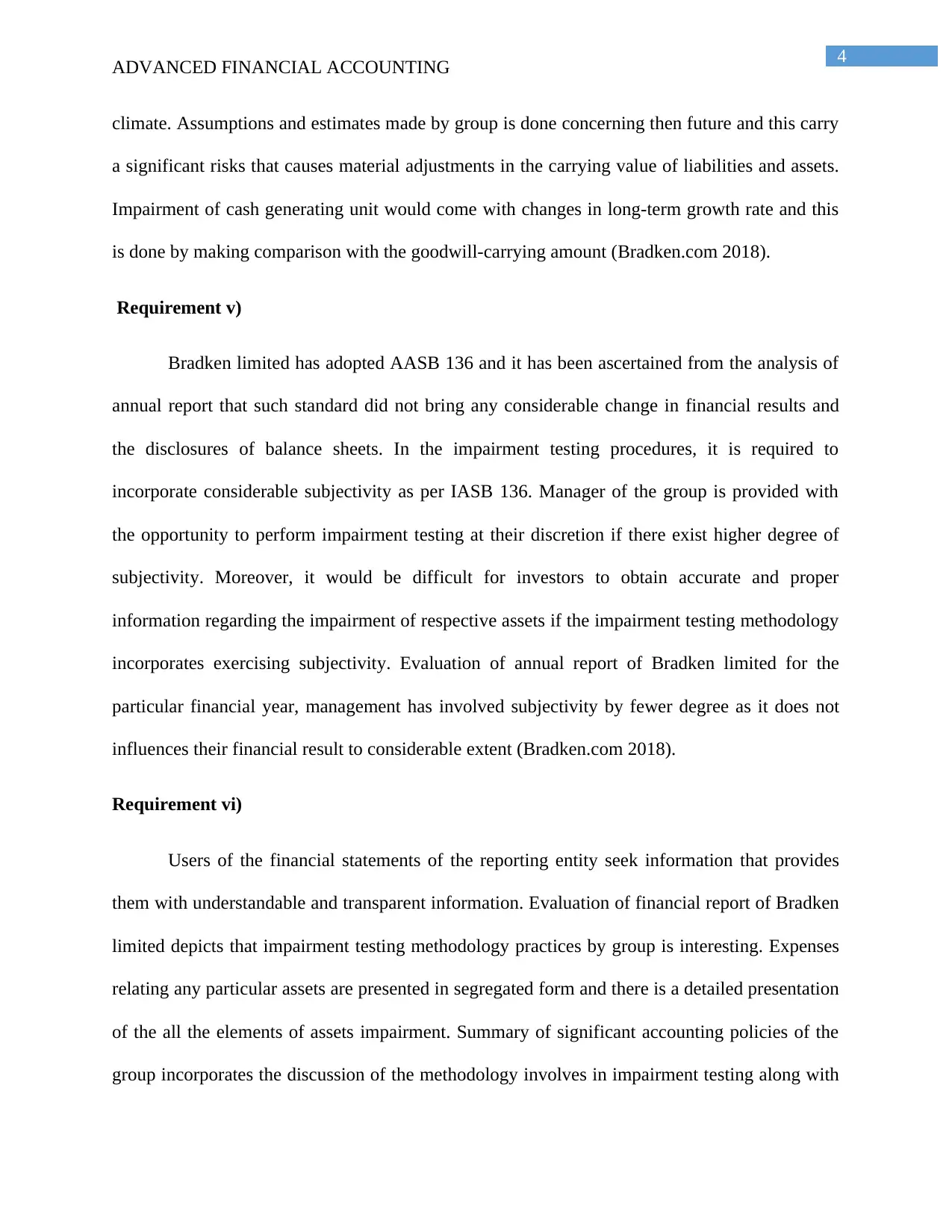

Requirement iii)

Yes, Bradken limited has recorded impairment expenses during the year 2016.

Impairment expense s relating to goodwill is recorded at $ 29039 million and 45503 for the

financial year 2016 and 2015 respectively. During the period 2016, impairment expense

attributable to mining and transport is recorded at $ 108 million, for the engineering product

segments, value stood at $ 50.8 million and for the mineral processing segment, impairment

expenses is recorded at $ 4.4 million. Moreover, impairment expense against license and

customer list was recorded at $ 2.3 million and $ 12.8 million respectively ((Bradken.com 2018).

Requirement iv)

Bradken limited calculates the value in use by making assumptions regarding discount

rates, sales margin and growth rates and all such assumptions have been determined by

management based on expectation of future and past performance. For discounting the forecasted

cash flows, a post tax discount rate has been applied by management. Assumptions about growth

rates are made by recognizing the competitive pressures and volatility of current economic

ADVANCED FINANCIAL ACCOUNTING

for projecting financial cash flows for a period of five years. Extrapolation of cash flows beyond

the five-year period using perpetual growth rate (Bradken.com 2018).

Requirement iii)

Yes, Bradken limited has recorded impairment expenses during the year 2016.

Impairment expense s relating to goodwill is recorded at $ 29039 million and 45503 for the

financial year 2016 and 2015 respectively. During the period 2016, impairment expense

attributable to mining and transport is recorded at $ 108 million, for the engineering product

segments, value stood at $ 50.8 million and for the mineral processing segment, impairment

expenses is recorded at $ 4.4 million. Moreover, impairment expense against license and

customer list was recorded at $ 2.3 million and $ 12.8 million respectively ((Bradken.com 2018).

Requirement iv)

Bradken limited calculates the value in use by making assumptions regarding discount

rates, sales margin and growth rates and all such assumptions have been determined by

management based on expectation of future and past performance. For discounting the forecasted

cash flows, a post tax discount rate has been applied by management. Assumptions about growth

rates are made by recognizing the competitive pressures and volatility of current economic

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

ADVANCED FINANCIAL ACCOUNTING

climate. Assumptions and estimates made by group is done concerning then future and this carry

a significant risks that causes material adjustments in the carrying value of liabilities and assets.

Impairment of cash generating unit would come with changes in long-term growth rate and this

is done by making comparison with the goodwill-carrying amount (Bradken.com 2018).

Requirement v)

Bradken limited has adopted AASB 136 and it has been ascertained from the analysis of

annual report that such standard did not bring any considerable change in financial results and

the disclosures of balance sheets. In the impairment testing procedures, it is required to

incorporate considerable subjectivity as per IASB 136. Manager of the group is provided with

the opportunity to perform impairment testing at their discretion if there exist higher degree of

subjectivity. Moreover, it would be difficult for investors to obtain accurate and proper

information regarding the impairment of respective assets if the impairment testing methodology

incorporates exercising subjectivity. Evaluation of annual report of Bradken limited for the

particular financial year, management has involved subjectivity by fewer degree as it does not

influences their financial result to considerable extent (Bradken.com 2018).

Requirement vi)

Users of the financial statements of the reporting entity seek information that provides

them with understandable and transparent information. Evaluation of financial report of Bradken

limited depicts that impairment testing methodology practices by group is interesting. Expenses

relating any particular assets are presented in segregated form and there is a detailed presentation

of the all the elements of assets impairment. Summary of significant accounting policies of the

group incorporates the discussion of the methodology involves in impairment testing along with

ADVANCED FINANCIAL ACCOUNTING

climate. Assumptions and estimates made by group is done concerning then future and this carry

a significant risks that causes material adjustments in the carrying value of liabilities and assets.

Impairment of cash generating unit would come with changes in long-term growth rate and this

is done by making comparison with the goodwill-carrying amount (Bradken.com 2018).

Requirement v)

Bradken limited has adopted AASB 136 and it has been ascertained from the analysis of

annual report that such standard did not bring any considerable change in financial results and

the disclosures of balance sheets. In the impairment testing procedures, it is required to

incorporate considerable subjectivity as per IASB 136. Manager of the group is provided with

the opportunity to perform impairment testing at their discretion if there exist higher degree of

subjectivity. Moreover, it would be difficult for investors to obtain accurate and proper

information regarding the impairment of respective assets if the impairment testing methodology

incorporates exercising subjectivity. Evaluation of annual report of Bradken limited for the

particular financial year, management has involved subjectivity by fewer degree as it does not

influences their financial result to considerable extent (Bradken.com 2018).

Requirement vi)

Users of the financial statements of the reporting entity seek information that provides

them with understandable and transparent information. Evaluation of financial report of Bradken

limited depicts that impairment testing methodology practices by group is interesting. Expenses

relating any particular assets are presented in segregated form and there is a detailed presentation

of the all the elements of assets impairment. Summary of significant accounting policies of the

group incorporates the discussion of the methodology involves in impairment testing along with

5

ADVANCED FINANCIAL ACCOUNTING

the assumptions and estimates. The group does not adopt amendment in the standard AASB 9,

relating to impairment that incorporated the requirement of new hedging accounting

(Bradken.com 2018). One interesting fact that is found after going through the annual report is

that each individual business segments of company has their own separate presentation of figures

related to impairment. Moreover, there is a segregation and proper presentation of impairment

charge and impairment expenses attributable to any particular asset.

Requirement vii)

Evaluation of the Badken limited annual report enables users with gaining relevant sights

about the impairment methodology adopted by the group. One crucial insight that have been

gained from the annual report of the group is that it had removed confusion regarding the

understandability of the concept of impairment expense and impairment charge that most users

find difficulty in segregating. Users of the report will be able to understand that impairment

charge is attributable to worthless goodwill and the impairment expenses are attributable to all

the assets (Bradken.com 2018).

Requirement viii)

Organization has adopted hierarchy of fair value measurement as per AASB 7 financial

instruments. For the measurement and disclosure of financial liabilities and assets, it is essential

to estimate the fair value of financial liabilities and assets. Classification of financial assets by

Bradken limited is done at fair value through loss and profits. Assets and liabilities of the group

that are recognized at fair value are derivative, patents, trademarks and payables (Bradken.com

2018).

ADVANCED FINANCIAL ACCOUNTING

the assumptions and estimates. The group does not adopt amendment in the standard AASB 9,

relating to impairment that incorporated the requirement of new hedging accounting

(Bradken.com 2018). One interesting fact that is found after going through the annual report is

that each individual business segments of company has their own separate presentation of figures

related to impairment. Moreover, there is a segregation and proper presentation of impairment

charge and impairment expenses attributable to any particular asset.

Requirement vii)

Evaluation of the Badken limited annual report enables users with gaining relevant sights

about the impairment methodology adopted by the group. One crucial insight that have been

gained from the annual report of the group is that it had removed confusion regarding the

understandability of the concept of impairment expense and impairment charge that most users

find difficulty in segregating. Users of the report will be able to understand that impairment

charge is attributable to worthless goodwill and the impairment expenses are attributable to all

the assets (Bradken.com 2018).

Requirement viii)

Organization has adopted hierarchy of fair value measurement as per AASB 7 financial

instruments. For the measurement and disclosure of financial liabilities and assets, it is essential

to estimate the fair value of financial liabilities and assets. Classification of financial assets by

Bradken limited is done at fair value through loss and profits. Assets and liabilities of the group

that are recognized at fair value are derivative, patents, trademarks and payables (Bradken.com

2018).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

ADVANCED FINANCIAL ACCOUNTING

Measurement of financial assets of the group is done at fair value by recognition of profit

and loss and carrying at fair value subsequently. Establishment of fair value is done by using the

techniques of valuation. Indication of assets impairment or that assets have been impaired are

done by observing a prolonged decline in fair value (Bradken.com 2018).

Part B:

Requirement i)

Companies are provided with the incentives of classifying their lease as either operating

or financing lease under the former lease accounting standard. This has led to evolvement of

tendencies among reporting entity having high level of debt to treat lease as operating lease and

the reason is that the principle underlying the existing standard do not mandate them to disclose

their operating lease commitments on their balance sheets and instead disclosing them as an

expenses in the notes to financial statements (Christensen et al. 2015). Therefore, the amount of

total liabilities that is presented in the balance sheet of entities would not reflect true worth of

lease commitments. Recording of the operation outside the balance sheet will leave the degree of

indebtedness unchanged and does not make any alterations in the capacity of organization to

contract debt (DeFond et al. 2014). In this regard, it can be said that leasing transactions under

the former standard do not reflect economic reality.

Requirement ii)

Former lease accounting standard makes it difficult for users to obtain accurate

information about leasing. This is attributable to the underlying principle of the standard that

provides company with the privilege of treating lease as operating and financing. Financing leas

is regarded as debt finance purchase and they are disclosed on the statement of financial position.

ADVANCED FINANCIAL ACCOUNTING

Measurement of financial assets of the group is done at fair value by recognition of profit

and loss and carrying at fair value subsequently. Establishment of fair value is done by using the

techniques of valuation. Indication of assets impairment or that assets have been impaired are

done by observing a prolonged decline in fair value (Bradken.com 2018).

Part B:

Requirement i)

Companies are provided with the incentives of classifying their lease as either operating

or financing lease under the former lease accounting standard. This has led to evolvement of

tendencies among reporting entity having high level of debt to treat lease as operating lease and

the reason is that the principle underlying the existing standard do not mandate them to disclose

their operating lease commitments on their balance sheets and instead disclosing them as an

expenses in the notes to financial statements (Christensen et al. 2015). Therefore, the amount of

total liabilities that is presented in the balance sheet of entities would not reflect true worth of

lease commitments. Recording of the operation outside the balance sheet will leave the degree of

indebtedness unchanged and does not make any alterations in the capacity of organization to

contract debt (DeFond et al. 2014). In this regard, it can be said that leasing transactions under

the former standard do not reflect economic reality.

Requirement ii)

Former lease accounting standard makes it difficult for users to obtain accurate

information about leasing. This is attributable to the underlying principle of the standard that

provides company with the privilege of treating lease as operating and financing. Financing leas

is regarded as debt finance purchase and they are disclosed on the statement of financial position.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

ADVANCED FINANCIAL ACCOUNTING

It would reflect the actual amount of indebtedness that is attributable towards company.

However, operating lease accounting treatment does not have any impact on overall debt

structure of company (El-Firjani et al. 2016). Although, in reality the total debt owed towards

company might be significantly higher than what is reported on balance sheets. It tempts most of

the company to classifying their lease as operating rather than financing. This explains why the

debt that is reported on balance sheet is 66 times less than on balance sheet liabilities.

Requirement iii)

Either airline companies lease their aircraft fleets or they buy them and the former

accounting standard that is IAS 17 gives them option of treating lease either as operating or as

financing lease. Users evaluating the financial position of Airline Company buying their aircraft

fleets might find different from the airline company that is leasing their fleets. It can be

explained with the help of an example, most of the fleets of German airline Lufthansa compared

to its competitor that is Emirates airlines that leases its fleets (Ramanna and Sletten 2014). It

would lead to appearance of differences between their financial positions. However, in reality,

their financial position might be similar and due to this reason, it is said that under the former

standard, there was no level playing field.

Requirement iv)

New lease standard IFRS 16 that have been introduced to overcome the drawback of the

former standard IAS 17 is facing oppositions due to several controversies associated with it.

Leasing behavior of some companies would change and they would be requiring purchasing

some of assets instead of leasing under new standard due to change in accounting treatment.

Companies would be experiencing increasing balance sheet and their overall structure of debt

resulting from increased focus on operating lease capitalization (Cascino and Gassen 2015).

ADVANCED FINANCIAL ACCOUNTING

It would reflect the actual amount of indebtedness that is attributable towards company.

However, operating lease accounting treatment does not have any impact on overall debt

structure of company (El-Firjani et al. 2016). Although, in reality the total debt owed towards

company might be significantly higher than what is reported on balance sheets. It tempts most of

the company to classifying their lease as operating rather than financing. This explains why the

debt that is reported on balance sheet is 66 times less than on balance sheet liabilities.

Requirement iii)

Either airline companies lease their aircraft fleets or they buy them and the former

accounting standard that is IAS 17 gives them option of treating lease either as operating or as

financing lease. Users evaluating the financial position of Airline Company buying their aircraft

fleets might find different from the airline company that is leasing their fleets. It can be

explained with the help of an example, most of the fleets of German airline Lufthansa compared

to its competitor that is Emirates airlines that leases its fleets (Ramanna and Sletten 2014). It

would lead to appearance of differences between their financial positions. However, in reality,

their financial position might be similar and due to this reason, it is said that under the former

standard, there was no level playing field.

Requirement iv)

New lease standard IFRS 16 that have been introduced to overcome the drawback of the

former standard IAS 17 is facing oppositions due to several controversies associated with it.

Leasing behavior of some companies would change and they would be requiring purchasing

some of assets instead of leasing under new standard due to change in accounting treatment.

Companies would be experiencing increasing balance sheet and their overall structure of debt

resulting from increased focus on operating lease capitalization (Cascino and Gassen 2015).

8

ADVANCED FINANCIAL ACCOUNTING

There will be increased tendencies among companies to shorten their lease term in lieu of taking

advantages of the amended standard. Reason for its unpopularity is also related to increased

complexities and costing of reporting along with enhanced administrative burden. It will be

required by companies to make investment for updating their accounting system, new

information technology system, educate their staff and update their knowledge and hence, there

will be increased cost will might have an impact on their net profit reported for the short-term

(Kraal et al. 2015). Furthermore, some companies will have considerable impact on their

financial ratios, which might not be favorable for their individual perspective and business

conditions. They will also be facing difficulties in receiving credits from banks and financial

institutions due to their worsening debt to equity ratio.

Requirement v)

Introduction of new lease standard will help in brining much needed transparency and

faithfulness required by investors when assessing the overall lease commitments. All the

subjective elements involved in the current lease standard will be eliminated and there will not

be any need for making rough computations and guesswork in the estimation of leases amount.

However, purchasing will become more attractive options for companies rather than leasing

them. New standard will facilitate investors in making comparison between the financial

positions of different reporting entities (Biddle et al. 2016). This will enable them to make

decisions that are more accurate and informed and accordingly making appropriate investment

decisions and will not be duped by the unfaithful presentation of financial position of entities.

New standard is more likely to be embraced by investors as they provide multiple benefits to

them when they seek investment decisions. Organizations relying on high level of debt initially

would face problems but eventually it has been perceived that IFRS 16 will help in improving

ADVANCED FINANCIAL ACCOUNTING

There will be increased tendencies among companies to shorten their lease term in lieu of taking

advantages of the amended standard. Reason for its unpopularity is also related to increased

complexities and costing of reporting along with enhanced administrative burden. It will be

required by companies to make investment for updating their accounting system, new

information technology system, educate their staff and update their knowledge and hence, there

will be increased cost will might have an impact on their net profit reported for the short-term

(Kraal et al. 2015). Furthermore, some companies will have considerable impact on their

financial ratios, which might not be favorable for their individual perspective and business

conditions. They will also be facing difficulties in receiving credits from banks and financial

institutions due to their worsening debt to equity ratio.

Requirement v)

Introduction of new lease standard will help in brining much needed transparency and

faithfulness required by investors when assessing the overall lease commitments. All the

subjective elements involved in the current lease standard will be eliminated and there will not

be any need for making rough computations and guesswork in the estimation of leases amount.

However, purchasing will become more attractive options for companies rather than leasing

them. New standard will facilitate investors in making comparison between the financial

positions of different reporting entities (Biddle et al. 2016). This will enable them to make

decisions that are more accurate and informed and accordingly making appropriate investment

decisions and will not be duped by the unfaithful presentation of financial position of entities.

New standard is more likely to be embraced by investors as they provide multiple benefits to

them when they seek investment decisions. Organizations relying on high level of debt initially

would face problems but eventually it has been perceived that IFRS 16 will help in improving

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

ADVANCED FINANCIAL ACCOUNTING

their overall debt structure (Walton 2016). Management of the organization will be able to

allocate their capital in a better way and designing the strategies so that it is compatible with

their business conditions. Actual picture of the financial position of entity will be presented to

investors (Ball et al. 2015). A proper evaluation of the need of leasing and purchasing will be

carried out and this will facilitate a balanced lease versus buy decision by management.

ADVANCED FINANCIAL ACCOUNTING

their overall debt structure (Walton 2016). Management of the organization will be able to

allocate their capital in a better way and designing the strategies so that it is compatible with

their business conditions. Actual picture of the financial position of entity will be presented to

investors (Ball et al. 2015). A proper evaluation of the need of leasing and purchasing will be

carried out and this will facilitate a balanced lease versus buy decision by management.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

ADVANCED FINANCIAL ACCOUNTING

References list:

Ball, R., Li, X. and Shivakumar, L., 2015. Contractibility and transparency of financial statement

information prepared under IFRS: Evidence from debt contracts around IFRS adoption. Journal

of Accounting Research, 53(5), pp.915-963

Biddle, G.C., Callahan, C.M., Hong, H.A. and Knowles, R.L., 2016. Do Adoptions of

International Financial Reporting Standards Enhance Capital Investment Efficiency?.

Bradken.com. (2018). [online] Available at: http://bradken.com/documents/default-source/ic-

annual-reports/pdf.pdf?sfvrsn=0 [Accessed 25 Jan. 2018].

Cascino, S. and Gassen, J., 2015. What drives the comparability effect of mandatory IFRS

adoption?. Review of Accounting Studies, 20(1), pp.242-282.

Christensen, H.B., Lee, E., Walker, M. and Zeng, C., 2015. Incentives or standards: What

determines accounting quality changes around IFRS adoption?. European Accounting Review,

24(1), pp.31-61.

DeFond, M.L., Hung, M., Li, S. and Li, Y., 2014. Does mandatory IFRS adoption affect crash

risk?. The Accounting Review, 90(1), pp.265-299.

El-Firjani, E.R. and Faraj, S.M., 2016. International Accounting Standards: Adoption,

Implementation and Challenges. In Economics and Political Implications of International

Financial Reporting Standards (pp. 231-250). IGI Global.

Florou, A., Kosi, U. and Pope, P.F., 2017. Are international accounting standards more credit

relevant than domestic standards?. Accounting and Business Research, 47(1), pp.1-29.

ADVANCED FINANCIAL ACCOUNTING

References list:

Ball, R., Li, X. and Shivakumar, L., 2015. Contractibility and transparency of financial statement

information prepared under IFRS: Evidence from debt contracts around IFRS adoption. Journal

of Accounting Research, 53(5), pp.915-963

Biddle, G.C., Callahan, C.M., Hong, H.A. and Knowles, R.L., 2016. Do Adoptions of

International Financial Reporting Standards Enhance Capital Investment Efficiency?.

Bradken.com. (2018). [online] Available at: http://bradken.com/documents/default-source/ic-

annual-reports/pdf.pdf?sfvrsn=0 [Accessed 25 Jan. 2018].

Cascino, S. and Gassen, J., 2015. What drives the comparability effect of mandatory IFRS

adoption?. Review of Accounting Studies, 20(1), pp.242-282.

Christensen, H.B., Lee, E., Walker, M. and Zeng, C., 2015. Incentives or standards: What

determines accounting quality changes around IFRS adoption?. European Accounting Review,

24(1), pp.31-61.

DeFond, M.L., Hung, M., Li, S. and Li, Y., 2014. Does mandatory IFRS adoption affect crash

risk?. The Accounting Review, 90(1), pp.265-299.

El-Firjani, E.R. and Faraj, S.M., 2016. International Accounting Standards: Adoption,

Implementation and Challenges. In Economics and Political Implications of International

Financial Reporting Standards (pp. 231-250). IGI Global.

Florou, A., Kosi, U. and Pope, P.F., 2017. Are international accounting standards more credit

relevant than domestic standards?. Accounting and Business Research, 47(1), pp.1-29.

11

ADVANCED FINANCIAL ACCOUNTING

Kraal, D., Yapa, P.W.S. and Joshi, M., 2015. The Adoption of International Accounting Standard

(IAS) 12 Income Taxes: Convergence or Divergence with Local Accounting Standards in

Selected ASEAN Countries?.

Li, S., Sougiannis, T. and Wang, I., 2017. Mandatory IFRS Adoption and the Usefulness of

Accounting Information in Predicting Future Earnings and Cash Flows.

Li, S., Sougiannis, T. and Wang, I., 2017. Mandatory IFRS Adoption and the Usefulness of

Accounting Information in Predicting Future Earnings and Cash Flows.

Mhedhbi, K., Mhedhbi, K., Zeghal, D. and Zeghal, D., 2016. Adoption of international

accounting standards and performance of emerging capital markets. Review of Accounting and

Finance, 15(2), pp.252-272.

Mügge, D. and Stellinga, B., 2015. The unstable core of global finance: Contingent valuation and

governance of international accounting standards. Regulation & Governance, 9(1), pp.47-62.

Mullinova, S., 2016. Use of the principles of IFRS (IAS) 39" Financial instruments: recognition

and assessment" for bank financial accounting. Modern European Researches, (1), pp.60-64.

Picker, R., Clark, K., Dunn, J., Kolitz, D., Livne, G., Loftus, J. and Van der Tas, L., 2016.

Applying international financial reporting standards. John Wiley & Sons

Ramanna, K. and Sletten, E., 2014. Network effects in countries' adoption of IFRS. The

Accounting Review, 89(4), pp.1517-1543.

Walton, P., 2016. Aiming for Global Accounting Standards–The International Accounting

Standards Board 2001–2011.

ADVANCED FINANCIAL ACCOUNTING

Kraal, D., Yapa, P.W.S. and Joshi, M., 2015. The Adoption of International Accounting Standard

(IAS) 12 Income Taxes: Convergence or Divergence with Local Accounting Standards in

Selected ASEAN Countries?.

Li, S., Sougiannis, T. and Wang, I., 2017. Mandatory IFRS Adoption and the Usefulness of

Accounting Information in Predicting Future Earnings and Cash Flows.

Li, S., Sougiannis, T. and Wang, I., 2017. Mandatory IFRS Adoption and the Usefulness of

Accounting Information in Predicting Future Earnings and Cash Flows.

Mhedhbi, K., Mhedhbi, K., Zeghal, D. and Zeghal, D., 2016. Adoption of international

accounting standards and performance of emerging capital markets. Review of Accounting and

Finance, 15(2), pp.252-272.

Mügge, D. and Stellinga, B., 2015. The unstable core of global finance: Contingent valuation and

governance of international accounting standards. Regulation & Governance, 9(1), pp.47-62.

Mullinova, S., 2016. Use of the principles of IFRS (IAS) 39" Financial instruments: recognition

and assessment" for bank financial accounting. Modern European Researches, (1), pp.60-64.

Picker, R., Clark, K., Dunn, J., Kolitz, D., Livne, G., Loftus, J. and Van der Tas, L., 2016.

Applying international financial reporting standards. John Wiley & Sons

Ramanna, K. and Sletten, E., 2014. Network effects in countries' adoption of IFRS. The

Accounting Review, 89(4), pp.1517-1543.

Walton, P., 2016. Aiming for Global Accounting Standards–The International Accounting

Standards Board 2001–2011.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.