Management Accounting Report: Decision Making at Imda Tech

VerifiedAdded on 2023/04/04

|12

|3691

|167

Report

AI Summary

This report, prepared for Imda Tech (UK) Limited, explores the functions and importance of management accounting. It differentiates between management and financial accounting, emphasizing the role of management accounting in decision-making. The report details various management accounting systems, including cost accounting, inventory management, and job costing. It provides income statements under both marginal and absorption costing methods. Furthermore, it covers different types of budgets, their advantages, disadvantages, and the budgeting process. The report also explains pricing strategies and the application of the balanced scorecard for identifying financial problems and improving financial governance. The content covers tools and techniques of financial statements and the importance of Marginal and absorption cost techniques. It also covers the various types of budgets like operational, cash, master, and sales budgets. It also explains pricing strategies and how the balanced scorecard is used to identify financial problems.

Management

Accounting

Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENT

INTRODUCTION..............................................................................................................................................3

TASK 1..............................................................................................................................................................3

P1 (i) What is management accounting. Differentiate between management accounting and financial accounting....3

(ii) Importance of management accounting information as a decision making tool....................................................4

P2 Describe the systems of management accounting..................................................................................................4

TASK 2..............................................................................................................................................................5

P2 (i) Income statement under marginal costing........................................................................................................5

(ii) Income statement of absorption costing.................................................................................................................5

TASK 3..............................................................................................................................................................6

P4 (a) What are the types of budgets and their advantages and disadvantages............................................................6

(b) The process of preparing budgets..........................................................................................................................6

(c) Explains what are pricing strategies.......................................................................................................................7

TASK 4..............................................................................................................................................................7

P5 (i) What is balanced scorecard and how can be used to identify the financial problems.......................................7

(ii) How it can be used to improve financial governance and development of effective strategies..............................8

CONCLUSION..................................................................................................................................................8

REFERENCES...................................................................................................................................................9

INTRODUCTION..............................................................................................................................................3

TASK 1..............................................................................................................................................................3

P1 (i) What is management accounting. Differentiate between management accounting and financial accounting....3

(ii) Importance of management accounting information as a decision making tool....................................................4

P2 Describe the systems of management accounting..................................................................................................4

TASK 2..............................................................................................................................................................5

P2 (i) Income statement under marginal costing........................................................................................................5

(ii) Income statement of absorption costing.................................................................................................................5

TASK 3..............................................................................................................................................................6

P4 (a) What are the types of budgets and their advantages and disadvantages............................................................6

(b) The process of preparing budgets..........................................................................................................................6

(c) Explains what are pricing strategies.......................................................................................................................7

TASK 4..............................................................................................................................................................7

P5 (i) What is balanced scorecard and how can be used to identify the financial problems.......................................7

(ii) How it can be used to improve financial governance and development of effective strategies..............................8

CONCLUSION..................................................................................................................................................8

REFERENCES...................................................................................................................................................9

INTRODUCTION

Management accounting is a combination of finance and management, that includes business tools

and techniques, it also added the real values of any business organisation. It helps managers in order to take

financial and non-financial decisions. The practice of management is extends in three areas, such are as: -

Strategic management, risk management and performance management. There is a huge difference in

management accounting and financial accounting; management accounting is being focused on overall

activities of the company. Although financial accounting is relates with providing details regarding products,

divisional, operations, plans and individual activities. Management accountants are able to work across the

organization, they are working not only just in finance but also in articulating business strategies & policies,

implications of big financial decisions or monitoring risk (Ward, 2012). The information is provided by

financial managers is helpful in developing dynamic solutions in order to improve business. Management

accounting is helpful in making budgets and collects information regarding cash inflow, outstanding debts

and revenues. On the other hand, financial management procedures, the useful data and information that is

related with other business functions ie. Department managers. The responsibilities of these accountants is

to providing comprehensive data of planning and forecasting, mentoring and reviewing cost inherent and

performing variance analysis.

TASK 1

P1 (i) What is management accounting. Differentiate between management accounting and financial

accounting.

Management is the process of creating management accounts and reports that is helpful in providing

exact and timely financial as well as statistical information to the managers in orders to take day to day or

short term decisions. It involves the tools and techniques of financial management that are helpful in

formulating strategies and policies. The reports of management accounting that are only useful for internal

environment, and they are confidential. In Imda Tech Limited, management accounting is helpful in analysis

the corporate as well as competitive environment, evaluate strategic options. It reviewing risk control and

evaluate auditing by which managers can easily make financial strategies. It is able to communicate

effective and gives suggestions on product developments and manufacturing (Kaplan and Atkinson, 2015).

Management accounting manages the price and cost for competitive advantage and is able to set up or

executes projects. It is helpful in reduces risk and uncertainties in organisation by applied forecasting

theories. It is assistive in evaluation of overall business environment, internal as well as external

environment by calculating capital expenditures.

Difference between Financial accounting and management accounting:-

Financial Accounting Management accounting

Financial accounting is concerned with prepare the

financial reports and statements of outsiders, such

as:- creditors, investors, suppliers, stakeholders,

customers and lenders.

Management accounting is also known as

managerial accounting, and it is the accounting that

helps managers in order to formulate strategies,

planning, forecasting and policies.

It is based on various principles, assumptions

and convention like consistency, realisation,

matching, materiality and going concern etc

(Burritt, Schaltegger. and Zvezdov, 2011.).

It is able to provide both quantitative and qualitative

information’s and data as well that is being assessed

and captured by accounting managers.

The statements of financial accounting are made for

one financial year that enables financials positions,

performance and profitability of the company.

It is answerable for day to day and short term

financial decisions that can be helpful for internal

uses only.

The format of financial accounting is specified and

provides only monetary information as well

It’s format is non-specified and its provide both

monetary as well as non-monetary information to the

Management accounting is a combination of finance and management, that includes business tools

and techniques, it also added the real values of any business organisation. It helps managers in order to take

financial and non-financial decisions. The practice of management is extends in three areas, such are as: -

Strategic management, risk management and performance management. There is a huge difference in

management accounting and financial accounting; management accounting is being focused on overall

activities of the company. Although financial accounting is relates with providing details regarding products,

divisional, operations, plans and individual activities. Management accountants are able to work across the

organization, they are working not only just in finance but also in articulating business strategies & policies,

implications of big financial decisions or monitoring risk (Ward, 2012). The information is provided by

financial managers is helpful in developing dynamic solutions in order to improve business. Management

accounting is helpful in making budgets and collects information regarding cash inflow, outstanding debts

and revenues. On the other hand, financial management procedures, the useful data and information that is

related with other business functions ie. Department managers. The responsibilities of these accountants is

to providing comprehensive data of planning and forecasting, mentoring and reviewing cost inherent and

performing variance analysis.

TASK 1

P1 (i) What is management accounting. Differentiate between management accounting and financial

accounting.

Management is the process of creating management accounts and reports that is helpful in providing

exact and timely financial as well as statistical information to the managers in orders to take day to day or

short term decisions. It involves the tools and techniques of financial management that are helpful in

formulating strategies and policies. The reports of management accounting that are only useful for internal

environment, and they are confidential. In Imda Tech Limited, management accounting is helpful in analysis

the corporate as well as competitive environment, evaluate strategic options. It reviewing risk control and

evaluate auditing by which managers can easily make financial strategies. It is able to communicate

effective and gives suggestions on product developments and manufacturing (Kaplan and Atkinson, 2015).

Management accounting manages the price and cost for competitive advantage and is able to set up or

executes projects. It is helpful in reduces risk and uncertainties in organisation by applied forecasting

theories. It is assistive in evaluation of overall business environment, internal as well as external

environment by calculating capital expenditures.

Difference between Financial accounting and management accounting:-

Financial Accounting Management accounting

Financial accounting is concerned with prepare the

financial reports and statements of outsiders, such

as:- creditors, investors, suppliers, stakeholders,

customers and lenders.

Management accounting is also known as

managerial accounting, and it is the accounting that

helps managers in order to formulate strategies,

planning, forecasting and policies.

It is based on various principles, assumptions

and convention like consistency, realisation,

matching, materiality and going concern etc

(Burritt, Schaltegger. and Zvezdov, 2011.).

It is able to provide both quantitative and qualitative

information’s and data as well that is being assessed

and captured by accounting managers.

The statements of financial accounting are made for

one financial year that enables financials positions,

performance and profitability of the company.

It is answerable for day to day and short term

financial decisions that can be helpful for internal

uses only.

The format of financial accounting is specified and

provides only monetary information as well

It’s format is non-specified and its provide both

monetary as well as non-monetary information to the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

managers.

(ii) Importance of management accounting information as a decision making tool.

The significance of management as decision making tool, it is helpful in providing needed data

whether the organisation is in profit or loss. Management accounting information is helpful for making

decisions that short term or as well as long term also (Parker, 2012). In Imda Tech Limited, it is working as

a powerful tool that makes business more successful. The information is used by managers to determines

that what product to be sold and how to sell it. Meanwhile it is helpful in relevant cost analysis, activity

based analysis and make or buy decisions of the company .

P2 Describe the systems of management accounting

There four main systems of management accounting, which are as follows:-

Cost accounting system: - This system is also known as costing system or product costing system. It

is used a framework in order to estimate the price of their products for cost control, profitability

analysis and inventory valuation. Cost accounting is procedure of summarising, allocating,

classifying, analysing, collecting and recording the alternative course of action that are helpful in

controlling costs (Otley and Emmanuel, 2013). In standard costing method, all production cost are

applied or charged to the charged for the inventory by using standard prices and cost. In normal

costing is uses historical methods of costing, in that overhead is charged or applied by the inventory,

and in actual costing method a new type of product process that can be used as inventory.

Inventory management system :- The system is helpful in manages stock and inventory of the

business organisations. It is able to deals with when order to and how order to. The main aim of

inventory cost accounting is to minimize the inventory cost in order to generate high returns. If Imda

Tech, hold more than the average level of stock, it is an substantial opportunity cost because the

investments are tied up in these inventories. There are some explicit costs that holding inventory,

such are as:- insurance cost and standard cost. Basically, it is an on-going process of moving

products and parts into and out from organisation’s location. Many companies manage their on daily

basis so they can easily place new orders and projects.

Job costing system :- Job costing system is the procedure of accruing information about the price is

associated with a specific production or job (Granlund, 2011). The information is helpful in

determining the correctness of a company's evaluation system, that is able to quote cost that allow for

a reasonable profit.

Price optimising system :- In that system, the price of the product is assessed, means it involves on

which price product will be sell out in market or what is its wholesale rate.

M1

Management accounting is helpful in providing the financial data and records to the managers, so

that they can easily use it at the time of needed. It is also helpful in reduces expenses by reviewing the cost

of economic resources and other business operations and activities. It also improves cash flow of the

company by making annual budgets.

D1

Management accounting and reporting is a system by organisations can easily evaluate their financial

as well as corporate performance. It is related with day to day accounting operation and assistive in making

short term decisions. It collects all the financial statements and reports by company can able to assess its

financial performance and position in market.

(ii) Importance of management accounting information as a decision making tool.

The significance of management as decision making tool, it is helpful in providing needed data

whether the organisation is in profit or loss. Management accounting information is helpful for making

decisions that short term or as well as long term also (Parker, 2012). In Imda Tech Limited, it is working as

a powerful tool that makes business more successful. The information is used by managers to determines

that what product to be sold and how to sell it. Meanwhile it is helpful in relevant cost analysis, activity

based analysis and make or buy decisions of the company .

P2 Describe the systems of management accounting

There four main systems of management accounting, which are as follows:-

Cost accounting system: - This system is also known as costing system or product costing system. It

is used a framework in order to estimate the price of their products for cost control, profitability

analysis and inventory valuation. Cost accounting is procedure of summarising, allocating,

classifying, analysing, collecting and recording the alternative course of action that are helpful in

controlling costs (Otley and Emmanuel, 2013). In standard costing method, all production cost are

applied or charged to the charged for the inventory by using standard prices and cost. In normal

costing is uses historical methods of costing, in that overhead is charged or applied by the inventory,

and in actual costing method a new type of product process that can be used as inventory.

Inventory management system :- The system is helpful in manages stock and inventory of the

business organisations. It is able to deals with when order to and how order to. The main aim of

inventory cost accounting is to minimize the inventory cost in order to generate high returns. If Imda

Tech, hold more than the average level of stock, it is an substantial opportunity cost because the

investments are tied up in these inventories. There are some explicit costs that holding inventory,

such are as:- insurance cost and standard cost. Basically, it is an on-going process of moving

products and parts into and out from organisation’s location. Many companies manage their on daily

basis so they can easily place new orders and projects.

Job costing system :- Job costing system is the procedure of accruing information about the price is

associated with a specific production or job (Granlund, 2011). The information is helpful in

determining the correctness of a company's evaluation system, that is able to quote cost that allow for

a reasonable profit.

Price optimising system :- In that system, the price of the product is assessed, means it involves on

which price product will be sell out in market or what is its wholesale rate.

M1

Management accounting is helpful in providing the financial data and records to the managers, so

that they can easily use it at the time of needed. It is also helpful in reduces expenses by reviewing the cost

of economic resources and other business operations and activities. It also improves cash flow of the

company by making annual budgets.

D1

Management accounting and reporting is a system by organisations can easily evaluate their financial

as well as corporate performance. It is related with day to day accounting operation and assistive in making

short term decisions. It collects all the financial statements and reports by company can able to assess its

financial performance and position in market.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TASK 2

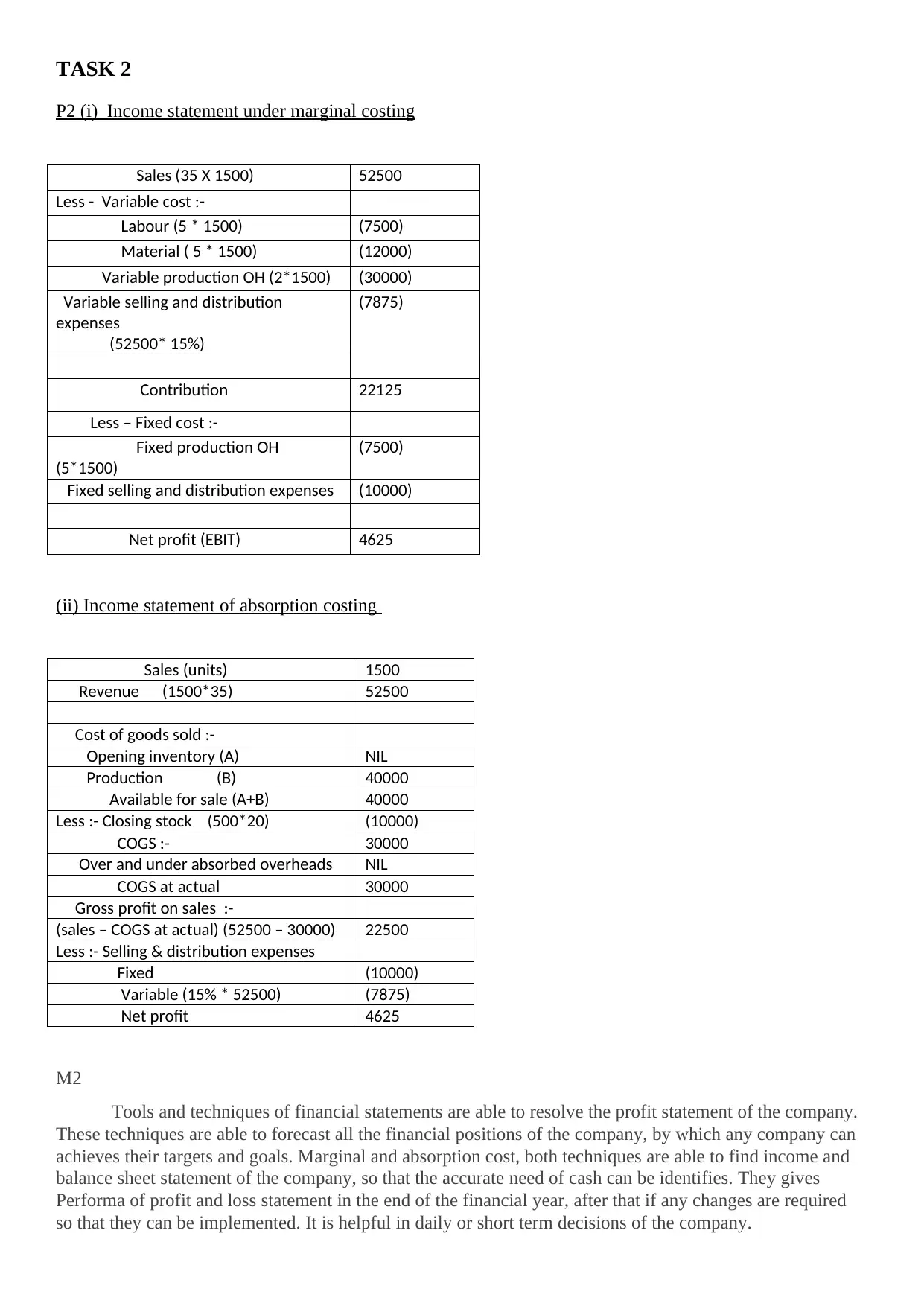

P2 (i) Income statement under marginal costing

Sales (35 X 1500) 52500

Less - Variable cost :-

Labour (5 * 1500) (7500)

Material ( 5 * 1500) (12000)

Variable production OH (2*1500) (30000)

Variable selling and distribution

expenses

(52500* 15%)

(7875)

Contribution 22125

Less – Fixed cost :-

Fixed production OH

(5*1500)

(7500)

Fixed selling and distribution expenses (10000)

Net profit (EBIT) 4625

(ii) Income statement of absorption costing

Sales (units) 1500

Revenue (1500*35) 52500

Cost of goods sold :-

Opening inventory (A) NIL

Production (B) 40000

Available for sale (A+B) 40000

Less :- Closing stock (500*20) (10000)

COGS :- 30000

Over and under absorbed overheads NIL

COGS at actual 30000

Gross profit on sales :-

(sales – COGS at actual) (52500 – 30000) 22500

Less :- Selling & distribution expenses

Fixed (10000)

Variable (15% * 52500) (7875)

Net profit 4625

M2

Tools and techniques of financial statements are able to resolve the profit statement of the company.

These techniques are able to forecast all the financial positions of the company, by which any company can

achieves their targets and goals. Marginal and absorption cost, both techniques are able to find income and

balance sheet statement of the company, so that the accurate need of cash can be identifies. They gives

Performa of profit and loss statement in the end of the financial year, after that if any changes are required

so that they can be implemented. It is helpful in daily or short term decisions of the company.

P2 (i) Income statement under marginal costing

Sales (35 X 1500) 52500

Less - Variable cost :-

Labour (5 * 1500) (7500)

Material ( 5 * 1500) (12000)

Variable production OH (2*1500) (30000)

Variable selling and distribution

expenses

(52500* 15%)

(7875)

Contribution 22125

Less – Fixed cost :-

Fixed production OH

(5*1500)

(7500)

Fixed selling and distribution expenses (10000)

Net profit (EBIT) 4625

(ii) Income statement of absorption costing

Sales (units) 1500

Revenue (1500*35) 52500

Cost of goods sold :-

Opening inventory (A) NIL

Production (B) 40000

Available for sale (A+B) 40000

Less :- Closing stock (500*20) (10000)

COGS :- 30000

Over and under absorbed overheads NIL

COGS at actual 30000

Gross profit on sales :-

(sales – COGS at actual) (52500 – 30000) 22500

Less :- Selling & distribution expenses

Fixed (10000)

Variable (15% * 52500) (7875)

Net profit 4625

M2

Tools and techniques of financial statements are able to resolve the profit statement of the company.

These techniques are able to forecast all the financial positions of the company, by which any company can

achieves their targets and goals. Marginal and absorption cost, both techniques are able to find income and

balance sheet statement of the company, so that the accurate need of cash can be identifies. They gives

Performa of profit and loss statement in the end of the financial year, after that if any changes are required

so that they can be implemented. It is helpful in daily or short term decisions of the company.

D2

Marginal cost is the modification in the opportunity cost that generates when the quantity produced is

improves by one unit and absorption costing refers that all of the production cost that are immersed by the

units created. Applying both methods in the organisation can gives better financial decisions. They provide

accurate and sustainable financial data, so that companies can easily analyse their financial performance of

the company. It involves sales revenues, capital expenditures, cash inflow cash outflow and gross & net

profit of the company. The information and data that is generates with all those elements is able to take long

term financial decision and provides instant change in company’s net cash.

TASK 3

P4 (a) What are the types of budgets and their advantages and disadvantages

Budgets are helpful in making financial decisions of company. There are 5 main types of budgets.

Such are as follows :-

Operational budgets: - These budgets are helpful in covers overall revenues and expenses that are

surrounding the day to day activities of the business. Operation budgets describe goods and services

of a firm, that expects to use in a budget period and it also involves the income and profit generating

activities of the business organisation (Fullerton, Kennedy and Widener, 2013). Revenues signifies

the sales of goods and services whereas the expenses defines the cost of products & administrative

and overhead costs, they are directly concerned with the process of products and services

Cash budgets:- Cash budgets are generally create for cash inflow and out flow in an business

organisation for the next year. A cash budgets is essential cause it allows managers to timely

identifies periods with cash shortage and overages, by which can they can easily take necessary

actions. It involves four different components, such as :- net changes in cash, new financing, cash

disbursement and cash recipients. It expects to Imda Tech, ability in order to take more cash than is

able to pays out.

Master Budgets: - A master budget is a inclusive projection of the management expects in order to

conduct all phases of business above the budget period, usually a financial year. The budget also

summarizes probable activities with budgeted income statement, cash budget and budgeted balance

sheet. Mostly master budgets involve interconnected budgets from the several departments.

Sales budgets:- Sales budgets describes the sales in an business organisation to produces goods and

services in units and dollars for a financial year(Qian, Burritt and Monroe, 2011). It describes the

quantities of products of a firm, that expect to sell and revenue acquired from those sales and all

expenses accrued during selling.

(b) The process of preparing budgets

There are these steps that are helpful in making effective budgets, such are as follows:-

Update budget information – When the managers are trying to prepare budget, they have to collect

the proper and accurate information by using financial statements and reports, so that they can easily

create the outline or format of the budget as well.

Create budget packages :- After that managers have to create budget package, so that is makes easier

the budget process. They have to determine whether any step cost will be acquired during the budget

process. The likely range of business procedure in the forthcoming budget period, and also describes

the amount of these costs and at which activity levels they will be sustained.

Update the budget model :- It refers to ease up all the issues and challenges, that are coming in

budget making process. These issues can be reduces by using of latest and updated technologies

Marginal cost is the modification in the opportunity cost that generates when the quantity produced is

improves by one unit and absorption costing refers that all of the production cost that are immersed by the

units created. Applying both methods in the organisation can gives better financial decisions. They provide

accurate and sustainable financial data, so that companies can easily analyse their financial performance of

the company. It involves sales revenues, capital expenditures, cash inflow cash outflow and gross & net

profit of the company. The information and data that is generates with all those elements is able to take long

term financial decision and provides instant change in company’s net cash.

TASK 3

P4 (a) What are the types of budgets and their advantages and disadvantages

Budgets are helpful in making financial decisions of company. There are 5 main types of budgets.

Such are as follows :-

Operational budgets: - These budgets are helpful in covers overall revenues and expenses that are

surrounding the day to day activities of the business. Operation budgets describe goods and services

of a firm, that expects to use in a budget period and it also involves the income and profit generating

activities of the business organisation (Fullerton, Kennedy and Widener, 2013). Revenues signifies

the sales of goods and services whereas the expenses defines the cost of products & administrative

and overhead costs, they are directly concerned with the process of products and services

Cash budgets:- Cash budgets are generally create for cash inflow and out flow in an business

organisation for the next year. A cash budgets is essential cause it allows managers to timely

identifies periods with cash shortage and overages, by which can they can easily take necessary

actions. It involves four different components, such as :- net changes in cash, new financing, cash

disbursement and cash recipients. It expects to Imda Tech, ability in order to take more cash than is

able to pays out.

Master Budgets: - A master budget is a inclusive projection of the management expects in order to

conduct all phases of business above the budget period, usually a financial year. The budget also

summarizes probable activities with budgeted income statement, cash budget and budgeted balance

sheet. Mostly master budgets involve interconnected budgets from the several departments.

Sales budgets:- Sales budgets describes the sales in an business organisation to produces goods and

services in units and dollars for a financial year(Qian, Burritt and Monroe, 2011). It describes the

quantities of products of a firm, that expect to sell and revenue acquired from those sales and all

expenses accrued during selling.

(b) The process of preparing budgets

There are these steps that are helpful in making effective budgets, such are as follows:-

Update budget information – When the managers are trying to prepare budget, they have to collect

the proper and accurate information by using financial statements and reports, so that they can easily

create the outline or format of the budget as well.

Create budget packages :- After that managers have to create budget package, so that is makes easier

the budget process. They have to determine whether any step cost will be acquired during the budget

process. The likely range of business procedure in the forthcoming budget period, and also describes

the amount of these costs and at which activity levels they will be sustained.

Update the budget model :- It refers to ease up all the issues and challenges, that are coming in

budget making process. These issues can be reduces by using of latest and updated technologies

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

(Soin and Collier, 2013). A budget should be make accordingly the needs of organisation as well

their employees also fulfils. It is also obtain with department budgets and revenue forecasts.

Budget implementation:- After budget formulation, budget is ready to be implement. Amending the

budget as the financial year progress.

(c) Explains what are pricing strategies

Pricing strategies is the forecasting of price determination of a product. A business is able to use

various varieties of pricing strategies in order to selling a product or services. The price of the product can

be can be set to develop profitability for each and individual unit of product can be sold in overall market. It

can be used to protect prevailing market from new competitors; it is helpful in increasing the market share

within a market. Pricing is one the important and highly demanded element in the marketing mix theory (van

der Steen, 2011). It helps customers to carry an image of the morals that the firm has offer through their

products.

M3

Different planning methods of budgets are helpful in forecasting the financial situation of the company.

Planned budgets are always successful, because they have proper idea of how to spend cash of different

commercial activities, of the business. They gives support to the managers, in order to make another

specific policies for the next financial year, it is also supplying flexible cash flow in the company. It is also

accommodating in pinpoint of shortfalls and increases the instant changes in net cash. It gives an proper

format of sales revenue and expenditure to the business organisation. Budget forecasting is helpful in

making long term decision s for the organisation as well as day to day operations also, by using this

company can easily grow its market share in the overall capital market place.

D3

Planning tools and techniques are able to reduce risk and uncertainties in the capital market. They are

responsible for organisational success and its growth & development. It is able to provide the long term

business polices and strategies, so that any business can compete with new entrants in the corporate market.

Planning tools a makes easier the decision making process of the company, in that mangers can easily

communicate with their employees and take effective and efficient decisions. It identifies all the issues and

challenges in in business organisation and reduce them with the help of internal and external environmental

analysis.

TASK 4

P5 (i) What is balanced scorecard and how can be used to identify the financial problems

The balanced scorecard refers to the strategic management and planning tool that is used

comprehensively in the business, industries and as well as government and non-government organisations. It

is aligned with worldwide business activities in order to make the visions and strategy of the organisation,

developing external and internal communications and monitoring the overall business unit. In Imda Tech

limited, it predicts with day to day activities that are involved in strategic management, and give properties

products, services and projects (Li and et. al., 2012). A balanced scorecard effort to interpret the vague and

pious hopes of a company’s mission that is able to manage the business enhanced at every level. It is an

approach, that is to be take a universal view of an organization and co-ordinate MDIs so that effectiveness

are experienced by all over departments.

Benefits of balanced scorecard in order to identifying the financial problems: -

their employees also fulfils. It is also obtain with department budgets and revenue forecasts.

Budget implementation:- After budget formulation, budget is ready to be implement. Amending the

budget as the financial year progress.

(c) Explains what are pricing strategies

Pricing strategies is the forecasting of price determination of a product. A business is able to use

various varieties of pricing strategies in order to selling a product or services. The price of the product can

be can be set to develop profitability for each and individual unit of product can be sold in overall market. It

can be used to protect prevailing market from new competitors; it is helpful in increasing the market share

within a market. Pricing is one the important and highly demanded element in the marketing mix theory (van

der Steen, 2011). It helps customers to carry an image of the morals that the firm has offer through their

products.

M3

Different planning methods of budgets are helpful in forecasting the financial situation of the company.

Planned budgets are always successful, because they have proper idea of how to spend cash of different

commercial activities, of the business. They gives support to the managers, in order to make another

specific policies for the next financial year, it is also supplying flexible cash flow in the company. It is also

accommodating in pinpoint of shortfalls and increases the instant changes in net cash. It gives an proper

format of sales revenue and expenditure to the business organisation. Budget forecasting is helpful in

making long term decision s for the organisation as well as day to day operations also, by using this

company can easily grow its market share in the overall capital market place.

D3

Planning tools and techniques are able to reduce risk and uncertainties in the capital market. They are

responsible for organisational success and its growth & development. It is able to provide the long term

business polices and strategies, so that any business can compete with new entrants in the corporate market.

Planning tools a makes easier the decision making process of the company, in that mangers can easily

communicate with their employees and take effective and efficient decisions. It identifies all the issues and

challenges in in business organisation and reduce them with the help of internal and external environmental

analysis.

TASK 4

P5 (i) What is balanced scorecard and how can be used to identify the financial problems

The balanced scorecard refers to the strategic management and planning tool that is used

comprehensively in the business, industries and as well as government and non-government organisations. It

is aligned with worldwide business activities in order to make the visions and strategy of the organisation,

developing external and internal communications and monitoring the overall business unit. In Imda Tech

limited, it predicts with day to day activities that are involved in strategic management, and give properties

products, services and projects (Li and et. al., 2012). A balanced scorecard effort to interpret the vague and

pious hopes of a company’s mission that is able to manage the business enhanced at every level. It is an

approach, that is to be take a universal view of an organization and co-ordinate MDIs so that effectiveness

are experienced by all over departments.

Benefits of balanced scorecard in order to identifying the financial problems: -

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

A proper balanced scorecard is helpful in all dynamic challenges in order to measuring performance.

Senior executive managers can realise that their organization’s measurement system effectively impact on

the behaviour and attitude of employees. It provides some realistic facts and data by which managers can

easily identifies the problems of financial management. BSCs reviewing the overall business performance,

internal as well as external and giving suggestion according to with that (Pitkänen and Lukka, 2011). It is an

analysis of overall organisation strategies and position, by which all financial challenges and issues of Imda

Tech limited, can be easily solved in order to make effective measurement. It provides managers a

comprehensive framework, so that they can easily take decisions makes policies with their long term

mission and vision.

(ii) How it can be used to improve financial governance and development of effective strategies.

Balanced scorecard is helpful in making effective performance strategies, and it makes easier the

process of making strategies and decisions in an business organisation. It is an planning of an business’s

financial success and growth because it assistive in defining and communicate what that organisation wants

to achieve and what are the necessary steps to do it (Cuganesan, Dunford and Palmer, 2012). Unfortunately,

less than 10% policies are effectively implemented in Imda Tech limited, whether success is often defined

mostly in terms of dollar raised that is a narrow or short term outlook in order to measuring a strategic

planning. To make an effective and comprehensive strategic plan, companies should develop a balanced

scorecard. It is a tool that improves financial perspectives of the company, internal process, learning and

growth of the organisation.

It also reduces the chances of risk and uncertainties of financial department, suggest them better and

effective performance measurement techniques. It also makes easier the process of decision making and

managers capable to create innovative techniques by using them the chances of risk and uncertainties can be

reduces. The process of financial development is generates from the financial conditions and financial

positions of the company in capital market, it gives support to the managers by applying strategic

management techniques (Cadez and Guilding, 2012). It provides an objective way to see that plans are

working or not, it also focuses on employees attention in order to take review about what matters most to the

success. In that, the most crucial element is success and profit, so that managers have to worked on it, to

develop their market share and financial statements by using budgetary tools and techniques.

M4

Management accounting is helpful in resolving the financial problems of the company; it gives

proper suggestions and guidance in order to making decisions and strategies. It is the combination of finance

and management, so that if management accounting works effectively, the problems regarding finance are

automatically solves. It provides the better suggestions to the managers; by using them they can solve their

day to day operations as well as their long term activities. It is the process of reducing risk and generating

high profit in capital market. Management accounting makes business capable to compete with their external

competitors and also reduces the chances of internal conflict.

CONCLUSION

From the above mentioned, it has been concluded that management accounting is a essential tool for an

business organisation. It is helpful in assessment of overall financial conditions ad position of the company in capital

market, whereas financial accounting is related with financial report and statements that are prepared for outsider such

as creditors and investors. Absorption and marginal cost, both are able to provide accurate and exact information of

income and balance sheet statements, so that managers can evaluates the cash inflow and outflow. Budgets are also

necessary to take long terms as well as day to day financial decisions. There are such types of budgets:- cash,

operational, sales, financial and master budgets. Financial tools and techniques are helpful reducing all financial risk

and uncertainties by assessing the overall analysis of internal and external business environment.

Senior executive managers can realise that their organization’s measurement system effectively impact on

the behaviour and attitude of employees. It provides some realistic facts and data by which managers can

easily identifies the problems of financial management. BSCs reviewing the overall business performance,

internal as well as external and giving suggestion according to with that (Pitkänen and Lukka, 2011). It is an

analysis of overall organisation strategies and position, by which all financial challenges and issues of Imda

Tech limited, can be easily solved in order to make effective measurement. It provides managers a

comprehensive framework, so that they can easily take decisions makes policies with their long term

mission and vision.

(ii) How it can be used to improve financial governance and development of effective strategies.

Balanced scorecard is helpful in making effective performance strategies, and it makes easier the

process of making strategies and decisions in an business organisation. It is an planning of an business’s

financial success and growth because it assistive in defining and communicate what that organisation wants

to achieve and what are the necessary steps to do it (Cuganesan, Dunford and Palmer, 2012). Unfortunately,

less than 10% policies are effectively implemented in Imda Tech limited, whether success is often defined

mostly in terms of dollar raised that is a narrow or short term outlook in order to measuring a strategic

planning. To make an effective and comprehensive strategic plan, companies should develop a balanced

scorecard. It is a tool that improves financial perspectives of the company, internal process, learning and

growth of the organisation.

It also reduces the chances of risk and uncertainties of financial department, suggest them better and

effective performance measurement techniques. It also makes easier the process of decision making and

managers capable to create innovative techniques by using them the chances of risk and uncertainties can be

reduces. The process of financial development is generates from the financial conditions and financial

positions of the company in capital market, it gives support to the managers by applying strategic

management techniques (Cadez and Guilding, 2012). It provides an objective way to see that plans are

working or not, it also focuses on employees attention in order to take review about what matters most to the

success. In that, the most crucial element is success and profit, so that managers have to worked on it, to

develop their market share and financial statements by using budgetary tools and techniques.

M4

Management accounting is helpful in resolving the financial problems of the company; it gives

proper suggestions and guidance in order to making decisions and strategies. It is the combination of finance

and management, so that if management accounting works effectively, the problems regarding finance are

automatically solves. It provides the better suggestions to the managers; by using them they can solve their

day to day operations as well as their long term activities. It is the process of reducing risk and generating

high profit in capital market. Management accounting makes business capable to compete with their external

competitors and also reduces the chances of internal conflict.

CONCLUSION

From the above mentioned, it has been concluded that management accounting is a essential tool for an

business organisation. It is helpful in assessment of overall financial conditions ad position of the company in capital

market, whereas financial accounting is related with financial report and statements that are prepared for outsider such

as creditors and investors. Absorption and marginal cost, both are able to provide accurate and exact information of

income and balance sheet statements, so that managers can evaluates the cash inflow and outflow. Budgets are also

necessary to take long terms as well as day to day financial decisions. There are such types of budgets:- cash,

operational, sales, financial and master budgets. Financial tools and techniques are helpful reducing all financial risk

and uncertainties by assessing the overall analysis of internal and external business environment.

REFERENCES

Books and Journal

Kaplan, R.S. and Atkinson, A.A., 2015. Advanced management accounting. PHI Learning.

Ward, K., 2012. Strategic management accounting. Routledge.

Burritt, R.L., Schaltegger, S. and Zvezdov, D., 2011. Carbon management accounting: explaining practice in

leading German companies. Australian Accounting Review. 21(1). pp.80-98.

Parker, L.D., 2012. Qualitative management accounting research: Assessing deliverables and

relevance. Critical perspectives on accounting. 23(1). pp.54-70.

Otley, D. and Emmanuel, K.M.C., 2013. Readings in accounting for management control. Springer.

Granlund, M., 2011. Extending AIS research to management accounting and control issues: A research

note. International Journal of Accounting Information Systems, 12(1). pp.3-19.

Fullerton, R.R., Kennedy, F.A. and Widener, S.K., 2013. Management accounting and control practices in a

lean manufacturing environment. Accounting, Organizations and Society. 38(1). pp.50-71.

Qian, W., Burritt, R. and Monroe, G., 2011. Environmental management accounting in local

government: A case of waste management. Accounting, Auditing & Accountability Journal.

24(1). pp.93-128.

Soin, K. and Collier, P., 2013. Risk and risk management in management accounting and control.

Contrafatto, M. and Burns, J., 2013. Social and environmental accounting, organisational change and

management accounting: A processual view. Management Accounting Research. 24(4). pp.349-

365.

Van der Steen, M., 2011. The emergence and change of management accounting routines. Accounting,

Auditing & Accountability Journal. 24(4). pp.502-547.

Li, X., and et. al., 2012. A comparative analysis of management accounting systems’ impact on lean

implementation. International Journal of Technology Management. 57(1/2/3). pp.33-48

Pitkänen, H. and Lukka, K., 2011. Three dimensions of formal and informal feedback in management

accounting. Management Accounting Research. 22(2). pp.125-137.

Cuganesan, S., Dunford, R. and Palmer, I., 2012. Strategic management accounting and strategy practices

within a public sector agency. Management Accounting Research. 23(4). pp.245-260.

Cadez, S. and Guilding, C., 2012. Strategy, strategic management accounting and performance: a

configurational analysis. Industrial Management & Data Systems. 112(3). pp.484-501.

Online

The Differences Between Financial Accounting & Management Accounting. 2017. [Online]. Available

through: < http://smallbusiness.chron.com/differences-between-financial-accounting-management-

accounting-3985.html>. [Accessed on 23rd April 2017].

Budget : Meaning, Features and Its Types | Accounting. 2016. [Online]. Available through: <

http://www.yourarticlelibrary.com/accounting/budget-accounting/budget-meaning-features-and-its-

types-accounting/65284/>. [Accessed on 23rd April 2017].

Books and Journal

Kaplan, R.S. and Atkinson, A.A., 2015. Advanced management accounting. PHI Learning.

Ward, K., 2012. Strategic management accounting. Routledge.

Burritt, R.L., Schaltegger, S. and Zvezdov, D., 2011. Carbon management accounting: explaining practice in

leading German companies. Australian Accounting Review. 21(1). pp.80-98.

Parker, L.D., 2012. Qualitative management accounting research: Assessing deliverables and

relevance. Critical perspectives on accounting. 23(1). pp.54-70.

Otley, D. and Emmanuel, K.M.C., 2013. Readings in accounting for management control. Springer.

Granlund, M., 2011. Extending AIS research to management accounting and control issues: A research

note. International Journal of Accounting Information Systems, 12(1). pp.3-19.

Fullerton, R.R., Kennedy, F.A. and Widener, S.K., 2013. Management accounting and control practices in a

lean manufacturing environment. Accounting, Organizations and Society. 38(1). pp.50-71.

Qian, W., Burritt, R. and Monroe, G., 2011. Environmental management accounting in local

government: A case of waste management. Accounting, Auditing & Accountability Journal.

24(1). pp.93-128.

Soin, K. and Collier, P., 2013. Risk and risk management in management accounting and control.

Contrafatto, M. and Burns, J., 2013. Social and environmental accounting, organisational change and

management accounting: A processual view. Management Accounting Research. 24(4). pp.349-

365.

Van der Steen, M., 2011. The emergence and change of management accounting routines. Accounting,

Auditing & Accountability Journal. 24(4). pp.502-547.

Li, X., and et. al., 2012. A comparative analysis of management accounting systems’ impact on lean

implementation. International Journal of Technology Management. 57(1/2/3). pp.33-48

Pitkänen, H. and Lukka, K., 2011. Three dimensions of formal and informal feedback in management

accounting. Management Accounting Research. 22(2). pp.125-137.

Cuganesan, S., Dunford, R. and Palmer, I., 2012. Strategic management accounting and strategy practices

within a public sector agency. Management Accounting Research. 23(4). pp.245-260.

Cadez, S. and Guilding, C., 2012. Strategy, strategic management accounting and performance: a

configurational analysis. Industrial Management & Data Systems. 112(3). pp.484-501.

Online

The Differences Between Financial Accounting & Management Accounting. 2017. [Online]. Available

through: < http://smallbusiness.chron.com/differences-between-financial-accounting-management-

accounting-3985.html>. [Accessed on 23rd April 2017].

Budget : Meaning, Features and Its Types | Accounting. 2016. [Online]. Available through: <

http://www.yourarticlelibrary.com/accounting/budget-accounting/budget-meaning-features-and-its-

types-accounting/65284/>. [Accessed on 23rd April 2017].

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.