Financial Analysis: Management Accounting Report for Pele

VerifiedAdded on 2020/02/14

|9

|1616

|49

Report

AI Summary

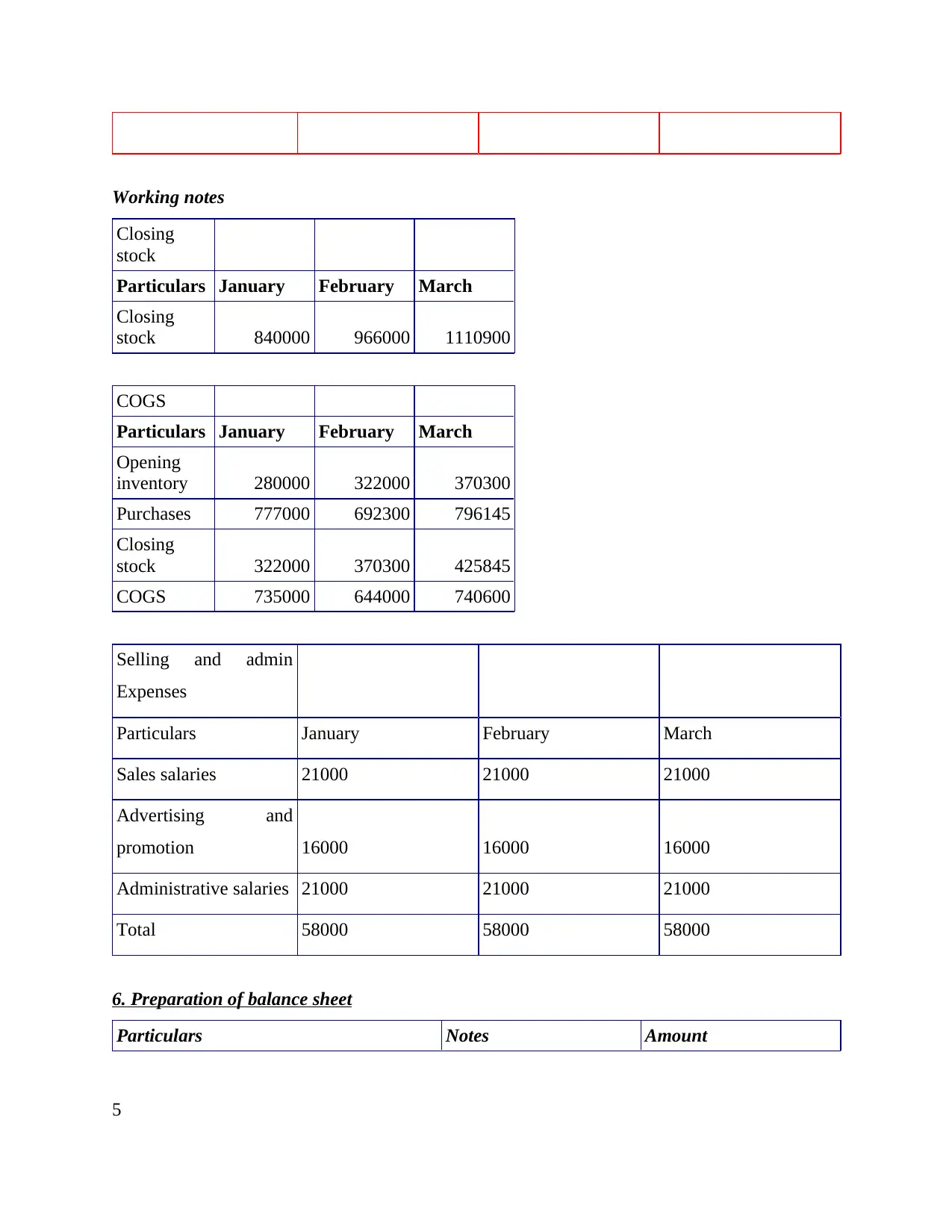

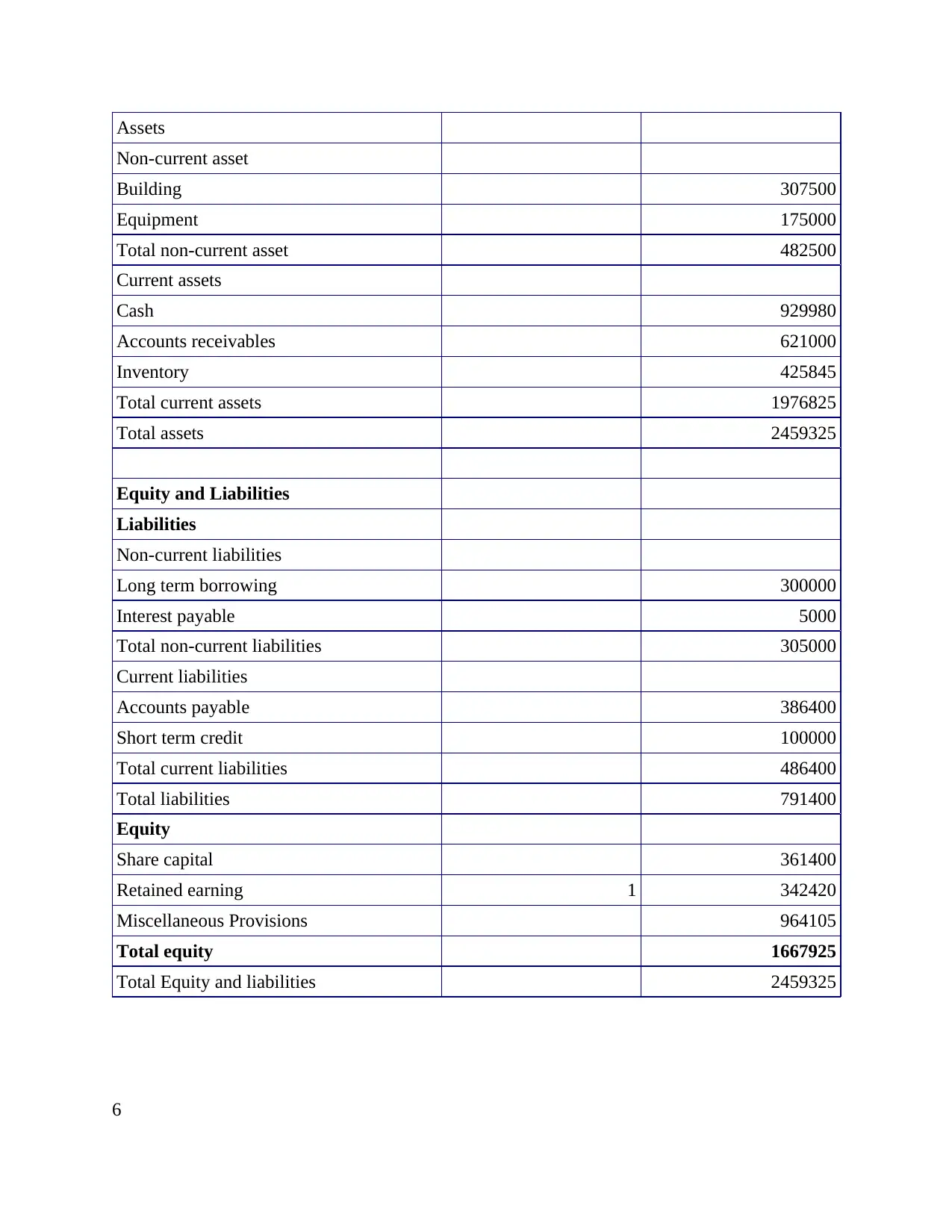

This report presents a comprehensive analysis of management accounting principles, focusing on the financial performance of Pele company. The report begins with the preparation of sales and cash budgets, detailing revenue projections and cash flow management. It then proceeds to construct key financial statements, including income statements and balance sheets, to assess the company's profitability and financial position. The report also explores the purpose of budgeting, emphasizing its role in forecasting, decision-making, and evaluating business performance. Furthermore, it highlights the importance of cash budgets in maintaining liquidity and improving the cash position, while also examining the interaction of human behavior with the budgeting process. The analysis incorporates working notes to explain calculations and assumptions, providing a clear understanding of the financial data and its implications for Pele company's management and strategic decisions. Finally, the report concludes with a synthesis of the findings and a list of relevant references.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.