Financial Accounting Report: Depreciation, Ethics, and Governance

VerifiedAdded on 2020/06/05

|10

|2578

|53

Report

AI Summary

This report examines financial accounting principles, focusing on Sunshine Ltd. and its financial practices. It delves into accounting theories, emphasizing descriptive, normative, evaluative, deductive, and inductive approaches. The report explores ethics and governance in accounting, highlighting the accountant's role in decision-making and adherence to standards like AASB 116. A key section analyzes the accountant's role in changing depreciation methods, comparing straight-line and sum-of-year digits methods and their impact on financial statements. The report also assesses the stakeholders affected by AASB 116 and provides recommendations for financial management. The analysis covers depreciation calculations, ethical considerations, and the overall impact of accounting practices on the company's financial health and stakeholder relations. The report emphasizes the importance of ethical conduct and the application of accounting standards for accurate financial reporting.

Financial Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

EXECUTIVE SUMMARY.............................................................................................................1

Concept and usefulness of accounting theories......................................................................2

Ethics and governance ...........................................................................................................3

Accountant role in changing depreciation method:................................................................4

Stakeholders and impacts of AASB 116 ...............................................................................6

Recommendation:...................................................................................................................7

REFERENCES................................................................................................................................8

EXECUTIVE SUMMARY.............................................................................................................1

Concept and usefulness of accounting theories......................................................................2

Ethics and governance ...........................................................................................................3

Accountant role in changing depreciation method:................................................................4

Stakeholders and impacts of AASB 116 ...............................................................................6

Recommendation:...................................................................................................................7

REFERENCES................................................................................................................................8

EXECUTIVE SUMMARY

Financial accounting is an essential aspect of an organisation by which they can help to

maintain their everyday accounting transactions. The primary objective of an organisation is to

follow standardised rules and regulations that can be helpful in recording, summarising and

presenting valuable results for company. It is necessary to prepare financial statements more

accurately so that chances of getting maximum profitability can be enhanced in the coming

future. This project report presents the perfect highlight of ethics and governances those are

related with managing accounts of Sunshine Ltd. Role of accountant in using depreciation

methods and shareholder impacts according to AASB116 are explain under this report.

1

Financial accounting is an essential aspect of an organisation by which they can help to

maintain their everyday accounting transactions. The primary objective of an organisation is to

follow standardised rules and regulations that can be helpful in recording, summarising and

presenting valuable results for company. It is necessary to prepare financial statements more

accurately so that chances of getting maximum profitability can be enhanced in the coming

future. This project report presents the perfect highlight of ethics and governances those are

related with managing accounts of Sunshine Ltd. Role of accountant in using depreciation

methods and shareholder impacts according to AASB116 are explain under this report.

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Concept and usefulness of accounting theories

As, accounting is a systematic techniques through which information can be determine ,

measure, classify and summarise as financial data of an organisation those are incur during the

year. Depreciation is an accounting technique related with the cost of a tangible asset over its

reusable life. It is an effective aspect that are related with the long term assets in order to

compute both tax and for the objective of accounting data. For the purpose of calculating

depreciation, it requires current series of entries that are charge as fixed assets with the total

expenditure (Weil, Schipper and Francis, 2013). There is mainly a prime reason behind every

action of a human being. A management does not do anything without using an effective sound

accounting system. As accounting system deal with the financial transaction. Hence, every

accounting work is based on certain reasoning. Accounting theories always try to provide useful

reason in other logic underlying practices.

It will provide scientific ways of rational for the solution of any actual accounting issues.

It have develop by complete observation, analysis, scrutiny and scanning of the everyday

accounting practices. There are various theories in other branches of analysis. However, some of

them are discuss underneath:

Descriptive theory: According to this particular theory which is based on descriptive

approaches. The cause and effects of every day activities of operations are determine

through using this theory. It will be help full to estimate occurrence of an activities.

Normative theory: It is basically, concern with the coming acts in the light of current

performance of an organization. Normative accounting theory involves best possible

theories that are independent with the current practices. It can be easy to overcome

certain issues those are arises in coming time to the Sunshine Ltd. For the purpose of

making proper balance in the profitability in coming years they need to go with this

theory as they can manage their resources in more effectively.

Evaluative accounting theory: The theory which helps to provide necessary information

about the quality and quantity of any specific objectives or events (Beatty and Liao,

2014). It will be to measure the qualitative aspects of an event those are expected to be

occur.

Deductive theory: As per this, particular theory is followed by using various deduction

concepts. They are commonly, formulated to attain some specific aims and objectives.

2

As, accounting is a systematic techniques through which information can be determine ,

measure, classify and summarise as financial data of an organisation those are incur during the

year. Depreciation is an accounting technique related with the cost of a tangible asset over its

reusable life. It is an effective aspect that are related with the long term assets in order to

compute both tax and for the objective of accounting data. For the purpose of calculating

depreciation, it requires current series of entries that are charge as fixed assets with the total

expenditure (Weil, Schipper and Francis, 2013). There is mainly a prime reason behind every

action of a human being. A management does not do anything without using an effective sound

accounting system. As accounting system deal with the financial transaction. Hence, every

accounting work is based on certain reasoning. Accounting theories always try to provide useful

reason in other logic underlying practices.

It will provide scientific ways of rational for the solution of any actual accounting issues.

It have develop by complete observation, analysis, scrutiny and scanning of the everyday

accounting practices. There are various theories in other branches of analysis. However, some of

them are discuss underneath:

Descriptive theory: According to this particular theory which is based on descriptive

approaches. The cause and effects of every day activities of operations are determine

through using this theory. It will be help full to estimate occurrence of an activities.

Normative theory: It is basically, concern with the coming acts in the light of current

performance of an organization. Normative accounting theory involves best possible

theories that are independent with the current practices. It can be easy to overcome

certain issues those are arises in coming time to the Sunshine Ltd. For the purpose of

making proper balance in the profitability in coming years they need to go with this

theory as they can manage their resources in more effectively.

Evaluative accounting theory: The theory which helps to provide necessary information

about the quality and quantity of any specific objectives or events (Beatty and Liao,

2014). It will be to measure the qualitative aspects of an event those are expected to be

occur.

Deductive theory: As per this, particular theory is followed by using various deduction

concepts. They are commonly, formulated to attain some specific aims and objectives.

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Inductive theory: Such kind of theories are useful to examine and identify the

happenings of past activities. It is based on repeated experiments and informs that are

more similar events which are occur in future.

Ethics and governance

Accounting ethics are primarily related with the field of practical ethics and is a crucial

aspect of every business concern. This particular study helps to examine the moral values and

judgement which are applied to accounting techniques. It is considered as one of the best

examples of professional ethics. It is a core element of the knowledge and skills that are followed

by professional accountants (May, 2013). In order to take key business decision making,

accountants must be proficient in the formulation of regulation regimes, compliance requirement,

etc. A better understanding of ethics and corporate governance with various roles and

responsibilities would be more effective for company as well as accountant to make accurate and

reliable reporting. From an individual potential, this particular aspects is related with the ethics

those are needed to be analyse by using appropriate strategies so that better results can be

generated in future times.

The skills and ability require in the preparation of accounting records. Such as advance

taxation, financial reporting and auditing. It is necessary for the accountant to follow all those

rules and policies that are made in AASB116 (Narayanaswamy, 2017). The overall plan and set

of standards are used so that they can generate more positive outcomes rather than carrying

unethical considerations to company. The AASB for application is to record all those standard

rules and regulations that are applicable in recording of financial transactions in books of

Sunshine Ltd. Exception for a particular standards those are specific to the net profit motive and

are completed based on domestic nature. The AASB is using IASB standards that are applicable

according to Australian environment.

Objectives:

This particular concept will be helpful in providing positive knowledge and skills that are

required to the professional accountant in order to operate effectively in analysing accounting

system of Sunshine Ltd. This particular system is designed to make sure that the implementation

of rules and policies in the development of wide range of professional ethics, value and norms

must be consider by an accountant.

3

happenings of past activities. It is based on repeated experiments and informs that are

more similar events which are occur in future.

Ethics and governance

Accounting ethics are primarily related with the field of practical ethics and is a crucial

aspect of every business concern. This particular study helps to examine the moral values and

judgement which are applied to accounting techniques. It is considered as one of the best

examples of professional ethics. It is a core element of the knowledge and skills that are followed

by professional accountants (May, 2013). In order to take key business decision making,

accountants must be proficient in the formulation of regulation regimes, compliance requirement,

etc. A better understanding of ethics and corporate governance with various roles and

responsibilities would be more effective for company as well as accountant to make accurate and

reliable reporting. From an individual potential, this particular aspects is related with the ethics

those are needed to be analyse by using appropriate strategies so that better results can be

generated in future times.

The skills and ability require in the preparation of accounting records. Such as advance

taxation, financial reporting and auditing. It is necessary for the accountant to follow all those

rules and policies that are made in AASB116 (Narayanaswamy, 2017). The overall plan and set

of standards are used so that they can generate more positive outcomes rather than carrying

unethical considerations to company. The AASB for application is to record all those standard

rules and regulations that are applicable in recording of financial transactions in books of

Sunshine Ltd. Exception for a particular standards those are specific to the net profit motive and

are completed based on domestic nature. The AASB is using IASB standards that are applicable

according to Australian environment.

Objectives:

This particular concept will be helpful in providing positive knowledge and skills that are

required to the professional accountant in order to operate effectively in analysing accounting

system of Sunshine Ltd. This particular system is designed to make sure that the implementation

of rules and policies in the development of wide range of professional ethics, value and norms

must be consider by an accountant.

3

Role of Accountant:

An accountant is a useful person that can help the company to analyse performance as

well as current position during the time. An accountant performs financial operations such as

collection of data, accuracy, recording and presentation of business and function operations of

Sunshine Ltd.

Accountant role in changing depreciation method:

Accountant is an individual body which helps the firm to measure performance by

making financial statements and other money related transactions. However, this can be said that

the accountant must be needed in any firm for development and prospering it. An accountant

records transactions and make financial reports as per the set guidelines (Balakrishnan and

Cohen, 2013). There are certain regulatory bodies which operate at domestic and international

level. Australian Accounting Standard Board is the one which is accountable for emerging,

issuing and controlling AASB and concerned pronouncements. The main aim of board is to

record transactions in organisations as per the set standards so that they could comply with

accounts related issues effectively. To comply with all financial related transactions as per the

set standards of AASB, is known as adhering the norms and rules or laws applicable in these

situation.

In the cited case, profits in 2016-17 is high which reflects that Sunshine Ltd is earning

more profits in their industry benchmark. But financial analyst predicts that due to economic

slowdown, company’s profits have become lower. The general manager wants to make a policy

by which profits of the firm in 2016-17 would compensate expenses of 2018-19. This is only

possible by changing the depreciation. Currently, firm is using straight line method and now to

stabilise profits of 2018-19, the accountant is thinking to implement “sum of year digit method”

so that they could stable the profits in an effective manner (Krueger and et. al., 2011).

Straight line method is the depreciation which applies on the year. Straight line method

charges cost evenly via useful life of a fixed asset. This kind of depreciation method is adequate

where economic advantages from an asset are forecasted to be realised over its total life of a

fixed assets. SLM is the most convenient and easy to use method where no valid estimate could

be formed relating to pattern of economic benefits forecasted to be derived over an asset’s useful

life. There are certain methods by which depreciation can be used:

4

An accountant is a useful person that can help the company to analyse performance as

well as current position during the time. An accountant performs financial operations such as

collection of data, accuracy, recording and presentation of business and function operations of

Sunshine Ltd.

Accountant role in changing depreciation method:

Accountant is an individual body which helps the firm to measure performance by

making financial statements and other money related transactions. However, this can be said that

the accountant must be needed in any firm for development and prospering it. An accountant

records transactions and make financial reports as per the set guidelines (Balakrishnan and

Cohen, 2013). There are certain regulatory bodies which operate at domestic and international

level. Australian Accounting Standard Board is the one which is accountable for emerging,

issuing and controlling AASB and concerned pronouncements. The main aim of board is to

record transactions in organisations as per the set standards so that they could comply with

accounts related issues effectively. To comply with all financial related transactions as per the

set standards of AASB, is known as adhering the norms and rules or laws applicable in these

situation.

In the cited case, profits in 2016-17 is high which reflects that Sunshine Ltd is earning

more profits in their industry benchmark. But financial analyst predicts that due to economic

slowdown, company’s profits have become lower. The general manager wants to make a policy

by which profits of the firm in 2016-17 would compensate expenses of 2018-19. This is only

possible by changing the depreciation. Currently, firm is using straight line method and now to

stabilise profits of 2018-19, the accountant is thinking to implement “sum of year digit method”

so that they could stable the profits in an effective manner (Krueger and et. al., 2011).

Straight line method is the depreciation which applies on the year. Straight line method

charges cost evenly via useful life of a fixed asset. This kind of depreciation method is adequate

where economic advantages from an asset are forecasted to be realised over its total life of a

fixed assets. SLM is the most convenient and easy to use method where no valid estimate could

be formed relating to pattern of economic benefits forecasted to be derived over an asset’s useful

life. There are certain methods by which depreciation can be used:

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

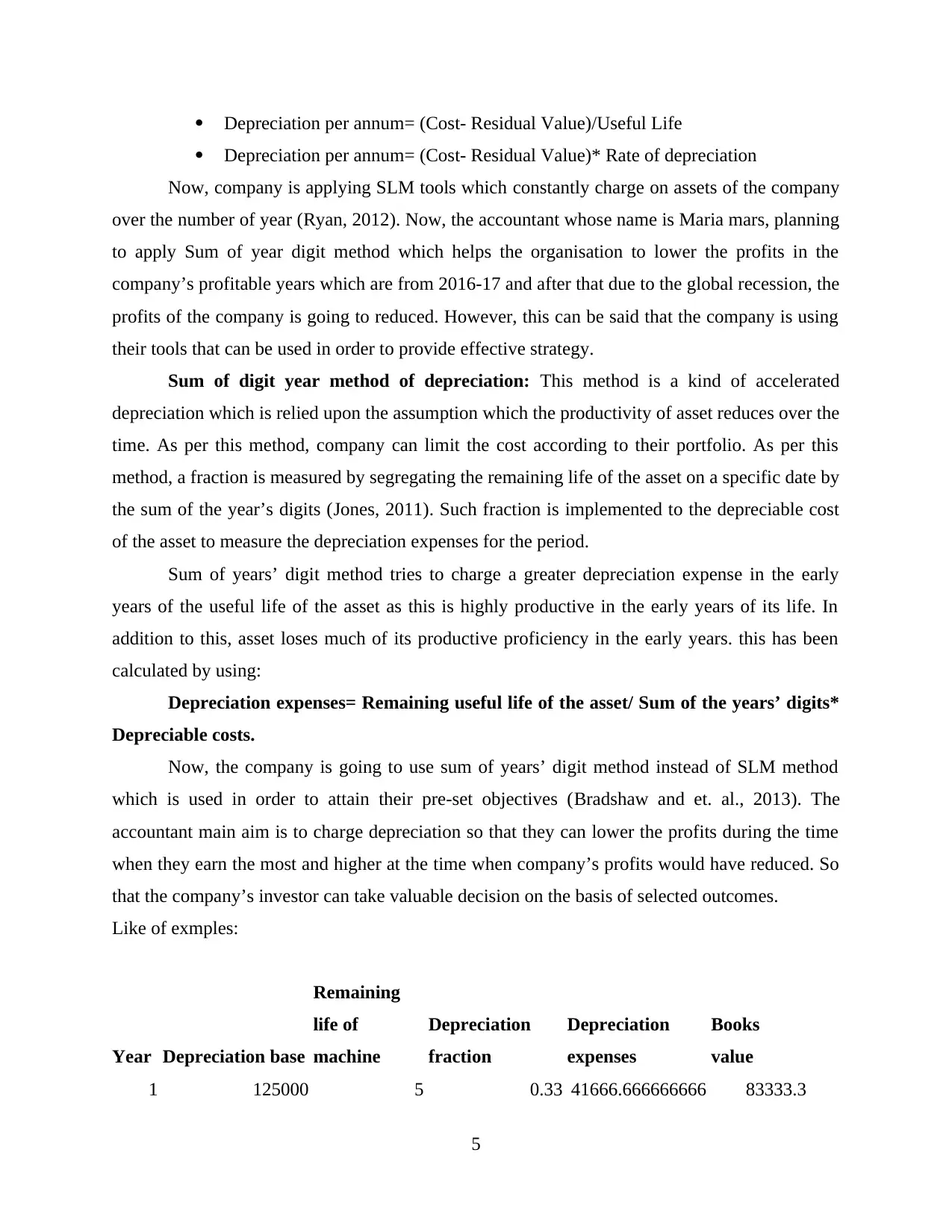

Depreciation per annum= (Cost- Residual Value)/Useful Life

Depreciation per annum= (Cost- Residual Value)* Rate of depreciation

Now, company is applying SLM tools which constantly charge on assets of the company

over the number of year (Ryan, 2012). Now, the accountant whose name is Maria mars, planning

to apply Sum of year digit method which helps the organisation to lower the profits in the

company’s profitable years which are from 2016-17 and after that due to the global recession, the

profits of the company is going to reduced. However, this can be said that the company is using

their tools that can be used in order to provide effective strategy.

Sum of digit year method of depreciation: This method is a kind of accelerated

depreciation which is relied upon the assumption which the productivity of asset reduces over the

time. As per this method, company can limit the cost according to their portfolio. As per this

method, a fraction is measured by segregating the remaining life of the asset on a specific date by

the sum of the year’s digits (Jones, 2011). Such fraction is implemented to the depreciable cost

of the asset to measure the depreciation expenses for the period.

Sum of years’ digit method tries to charge a greater depreciation expense in the early

years of the useful life of the asset as this is highly productive in the early years of its life. In

addition to this, asset loses much of its productive proficiency in the early years. this has been

calculated by using:

Depreciation expenses= Remaining useful life of the asset/ Sum of the years’ digits*

Depreciable costs.

Now, the company is going to use sum of years’ digit method instead of SLM method

which is used in order to attain their pre-set objectives (Bradshaw and et. al., 2013). The

accountant main aim is to charge depreciation so that they can lower the profits during the time

when they earn the most and higher at the time when company’s profits would have reduced. So

that the company’s investor can take valuable decision on the basis of selected outcomes.

Like of exmples:

Year Depreciation base

Remaining

life of

machine

Depreciation

fraction

Depreciation

expenses

Books

value

1 125000 5 0.33 41666.666666666 83333.3

5

Depreciation per annum= (Cost- Residual Value)* Rate of depreciation

Now, company is applying SLM tools which constantly charge on assets of the company

over the number of year (Ryan, 2012). Now, the accountant whose name is Maria mars, planning

to apply Sum of year digit method which helps the organisation to lower the profits in the

company’s profitable years which are from 2016-17 and after that due to the global recession, the

profits of the company is going to reduced. However, this can be said that the company is using

their tools that can be used in order to provide effective strategy.

Sum of digit year method of depreciation: This method is a kind of accelerated

depreciation which is relied upon the assumption which the productivity of asset reduces over the

time. As per this method, company can limit the cost according to their portfolio. As per this

method, a fraction is measured by segregating the remaining life of the asset on a specific date by

the sum of the year’s digits (Jones, 2011). Such fraction is implemented to the depreciable cost

of the asset to measure the depreciation expenses for the period.

Sum of years’ digit method tries to charge a greater depreciation expense in the early

years of the useful life of the asset as this is highly productive in the early years of its life. In

addition to this, asset loses much of its productive proficiency in the early years. this has been

calculated by using:

Depreciation expenses= Remaining useful life of the asset/ Sum of the years’ digits*

Depreciable costs.

Now, the company is going to use sum of years’ digit method instead of SLM method

which is used in order to attain their pre-set objectives (Bradshaw and et. al., 2013). The

accountant main aim is to charge depreciation so that they can lower the profits during the time

when they earn the most and higher at the time when company’s profits would have reduced. So

that the company’s investor can take valuable decision on the basis of selected outcomes.

Like of exmples:

Year Depreciation base

Remaining

life of

machine

Depreciation

fraction

Depreciation

expenses

Books

value

1 125000 5 0.33 41666.666666666 83333.3

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

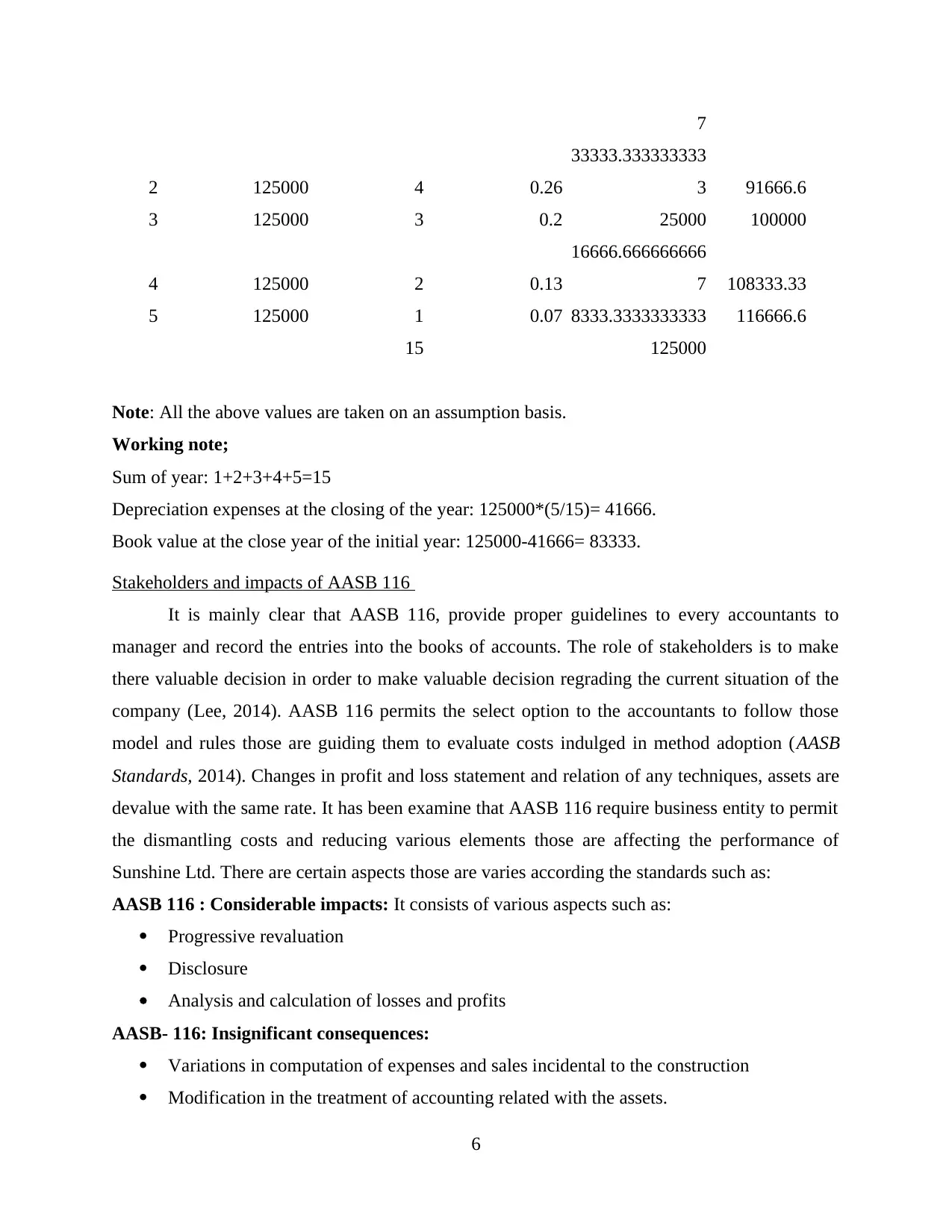

7

2 125000 4 0.26

33333.333333333

3 91666.6

3 125000 3 0.2 25000 100000

4 125000 2 0.13

16666.666666666

7 108333.33

5 125000 1 0.07 8333.3333333333 116666.6

15 125000

Note: All the above values are taken on an assumption basis.

Working note;

Sum of year: 1+2+3+4+5=15

Depreciation expenses at the closing of the year: 125000*(5/15)= 41666.

Book value at the close year of the initial year: 125000-41666= 83333.

Stakeholders and impacts of AASB 116

It is mainly clear that AASB 116, provide proper guidelines to every accountants to

manager and record the entries into the books of accounts. The role of stakeholders is to make

there valuable decision in order to make valuable decision regrading the current situation of the

company (Lee, 2014). AASB 116 permits the select option to the accountants to follow those

model and rules those are guiding them to evaluate costs indulged in method adoption (AASB

Standards, 2014). Changes in profit and loss statement and relation of any techniques, assets are

devalue with the same rate. It has been examine that AASB 116 require business entity to permit

the dismantling costs and reducing various elements those are affecting the performance of

Sunshine Ltd. There are certain aspects those are varies according the standards such as:

AASB 116 : Considerable impacts: It consists of various aspects such as:

Progressive revaluation

Disclosure

Analysis and calculation of losses and profits

AASB- 116: Insignificant consequences:

Variations in computation of expenses and sales incidental to the construction

Modification in the treatment of accounting related with the assets.

6

2 125000 4 0.26

33333.333333333

3 91666.6

3 125000 3 0.2 25000 100000

4 125000 2 0.13

16666.666666666

7 108333.33

5 125000 1 0.07 8333.3333333333 116666.6

15 125000

Note: All the above values are taken on an assumption basis.

Working note;

Sum of year: 1+2+3+4+5=15

Depreciation expenses at the closing of the year: 125000*(5/15)= 41666.

Book value at the close year of the initial year: 125000-41666= 83333.

Stakeholders and impacts of AASB 116

It is mainly clear that AASB 116, provide proper guidelines to every accountants to

manager and record the entries into the books of accounts. The role of stakeholders is to make

there valuable decision in order to make valuable decision regrading the current situation of the

company (Lee, 2014). AASB 116 permits the select option to the accountants to follow those

model and rules those are guiding them to evaluate costs indulged in method adoption (AASB

Standards, 2014). Changes in profit and loss statement and relation of any techniques, assets are

devalue with the same rate. It has been examine that AASB 116 require business entity to permit

the dismantling costs and reducing various elements those are affecting the performance of

Sunshine Ltd. There are certain aspects those are varies according the standards such as:

AASB 116 : Considerable impacts: It consists of various aspects such as:

Progressive revaluation

Disclosure

Analysis and calculation of losses and profits

AASB- 116: Insignificant consequences:

Variations in computation of expenses and sales incidental to the construction

Modification in the treatment of accounting related with the assets.

6

Identifying attributable costs.

Recommendation:

In the given case, accountant will use sum of year digit method as this will reduce the

profit at the time of optimising profit by the firm. I.e 2016-17 and increase the profit in the later

year which will satiate the general manager need. Investors will think that the company's

performance is consistent as irrespective of economic slow down company is able to earn profit

with the previous rate. The decision related with the implementation of such kind of method they

need to be slight focus various impacts that are healthy for the company.

7

Recommendation:

In the given case, accountant will use sum of year digit method as this will reduce the

profit at the time of optimising profit by the firm. I.e 2016-17 and increase the profit in the later

year which will satiate the general manager need. Investors will think that the company's

performance is consistent as irrespective of economic slow down company is able to earn profit

with the previous rate. The decision related with the implementation of such kind of method they

need to be slight focus various impacts that are healthy for the company.

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

REFERENCES

Books and Journals:

Balakrishnan, K. and Cohen, D. A., 2013. Competition and financial accounting misreporting.

Beatty, A. and Liao, S., 2014. Financial accounting in the banking industry: A review of the

empirical literature. Journal of Accounting and Economics. 58(2). pp.339-383.

Bradshaw, M and et. al., 2013. Financial reporting policy committee of the American accounting

association's financial accounting and reporting section: Accounting standard setting for

private companies. Accounting Horizons. 28(1). pp.175-192.

Jones, M. ed., 2011. Creative accounting, fraud and international accounting scandals. John

Wiley & Sons.

Krueger, J and et. al., 2011. Fast updates on read-optimized databases using multi-core CPUs.

Proceedings of the VLDB Endowment. 5(1). pp.61-72.

Lee, T. A. ed., 2014. Cash Flow Reporting (RLE Accounting): A Recent History of an

Accounting Practice. Routledge.

May, G.O., 2013. Financial accounting. Read Books Ltd.

Narayanaswamy, R., 2017. Financial accounting: a managerial perspective. PHI Learning Pvt.

Ltd..

Ryan, S.G., 2012. Financial reporting for financial instruments. Foundations and Trends® in

Accounting. 6(3–4). pp.187-354.

Weil, R.L., Schipper, K. and Francis, J., 2013. Financial accounting: an introduction to

concepts, methods and uses. Cengage Learning.

Online

AASB Standards. 2014.[Online].Available through:

<http://www.aasb.gov.au/Pronouncements/Current-standards.aspx>.

8

Books and Journals:

Balakrishnan, K. and Cohen, D. A., 2013. Competition and financial accounting misreporting.

Beatty, A. and Liao, S., 2014. Financial accounting in the banking industry: A review of the

empirical literature. Journal of Accounting and Economics. 58(2). pp.339-383.

Bradshaw, M and et. al., 2013. Financial reporting policy committee of the American accounting

association's financial accounting and reporting section: Accounting standard setting for

private companies. Accounting Horizons. 28(1). pp.175-192.

Jones, M. ed., 2011. Creative accounting, fraud and international accounting scandals. John

Wiley & Sons.

Krueger, J and et. al., 2011. Fast updates on read-optimized databases using multi-core CPUs.

Proceedings of the VLDB Endowment. 5(1). pp.61-72.

Lee, T. A. ed., 2014. Cash Flow Reporting (RLE Accounting): A Recent History of an

Accounting Practice. Routledge.

May, G.O., 2013. Financial accounting. Read Books Ltd.

Narayanaswamy, R., 2017. Financial accounting: a managerial perspective. PHI Learning Pvt.

Ltd..

Ryan, S.G., 2012. Financial reporting for financial instruments. Foundations and Trends® in

Accounting. 6(3–4). pp.187-354.

Weil, R.L., Schipper, K. and Francis, J., 2013. Financial accounting: an introduction to

concepts, methods and uses. Cengage Learning.

Online

AASB Standards. 2014.[Online].Available through:

<http://www.aasb.gov.au/Pronouncements/Current-standards.aspx>.

8

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.