AFA100 Winter 2020: Financial Accounting Case Assignment Solution

VerifiedAdded on 2022/09/06

|9

|557

|24

Homework Assignment

AI Summary

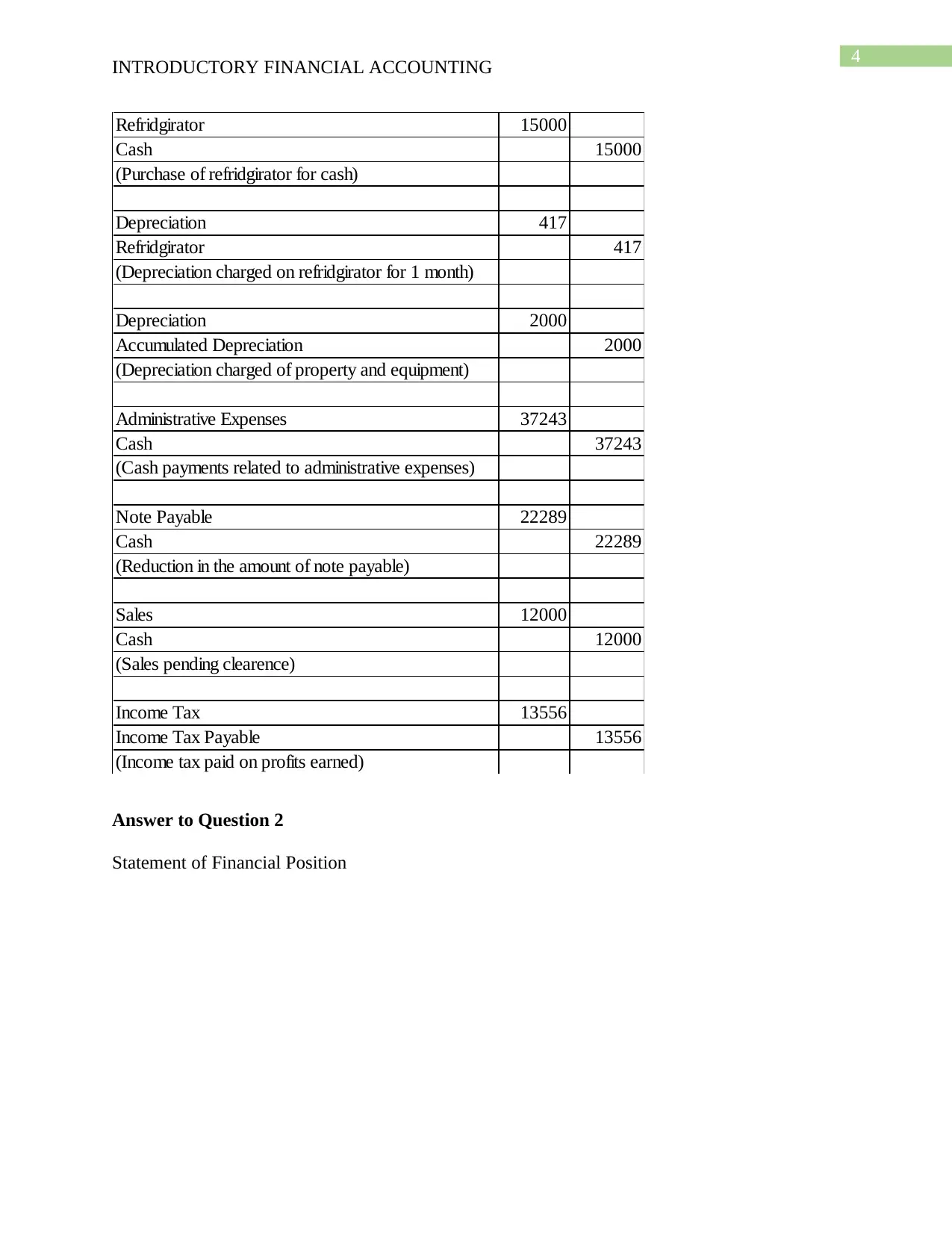

This document presents a complete solution to a financial accounting case assignment for Happy ReLeaf Ltd, a cannabis retail outlet. The solution includes journal entries for January 31, 2019, along with a statement of financial position, a statement of retained earnings, and a statement of earnings for the quarter. Furthermore, the assignment addresses the issue of revenue recognition, comparing the current method with an alternative approach based on product delivery completion. A memo to Penelope Wildflower discusses the impact of the alternative approach on the company's current ratio, arguing for its positive influence. The document concludes that the change in the revenue recognition method will have a positive impact on the current ratio of the business. The assignment is for AFA100 Introductory Financial Accounting. Bibliography is also included.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.