B10597 Financial Accounting Assignment: Statements and Ratios

VerifiedAdded on 2023/01/12

|18

|3444

|86

Homework Assignment

AI Summary

This financial accounting assignment provides a comprehensive overview of key accounting concepts and practices. It begins with an introduction to business transactions and double-entry bookkeeping, followed by a detailed analysis of a trial balance, including the calculation of owner's capital. The assignment then delves into ledger accounts, providing examples for various transactions such as purchases, sales, and expenses. It also presents an income statement and balance sheet, illustrating how to prepare financial statements for a company, including the calculation of net profit and financial position. Furthermore, the assignment covers bank reconciliation statements and the calculation and interpretation of financial ratios, such as return on capital employed, gross profit margin, and gearing ratio, providing a holistic understanding of financial accounting principles and their application.

B10597

FINANCIAL

ACCOUNTING

FINANCIAL

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

Task 1.1............................................................................................................................................3

Task 1.2............................................................................................................................................4

Task 2.1............................................................................................................................................8

Task 2.2............................................................................................................................................9

Task 2.3..........................................................................................................................................10

Task 2.4..........................................................................................................................................11

Task 3.1..........................................................................................................................................12

Task 3.2..........................................................................................................................................13

Task 3.3..........................................................................................................................................13

Task 3.4..........................................................................................................................................14

Task 4.1..........................................................................................................................................14

Task 4.2..........................................................................................................................................15

Task 4.3..........................................................................................................................................15

Task 4.4..........................................................................................................................................16

CONCLUSION..............................................................................................................................17

REFERENCES:.............................................................................................................................18

INTRODUCTION...........................................................................................................................3

Task 1.1............................................................................................................................................3

Task 1.2............................................................................................................................................4

Task 2.1............................................................................................................................................8

Task 2.2............................................................................................................................................9

Task 2.3..........................................................................................................................................10

Task 2.4..........................................................................................................................................11

Task 3.1..........................................................................................................................................12

Task 3.2..........................................................................................................................................13

Task 3.3..........................................................................................................................................13

Task 3.4..........................................................................................................................................14

Task 4.1..........................................................................................................................................14

Task 4.2..........................................................................................................................................15

Task 4.3..........................................................................................................................................15

Task 4.4..........................................................................................................................................16

CONCLUSION..............................................................................................................................17

REFERENCES:.............................................................................................................................18

INTRODUCTION

The main purpose of this report is to understand basic concepts about types of business

transactions such as sales, purchases, receipts and payments. Double entry book-keeping is the

basic principal which works on balancing the figure concept; which means if something debit

from the company than it should credit with equal amount to match final figures. Trial balance is

the technique where closing ledger balance directly transfers to match the figures; it is the strong

method to know about any errors in recording transactions either in journal or trial balance.

Financial statements show internal strength of company; this statement covers profit and loss

account, balance sheet and cash flow statement. Bank reconciliation statement is essential to find

any mismatch between cash book and bank passbook. Project contains different scenarios; each

scenario analyses give separate accounting concept with practical examples.

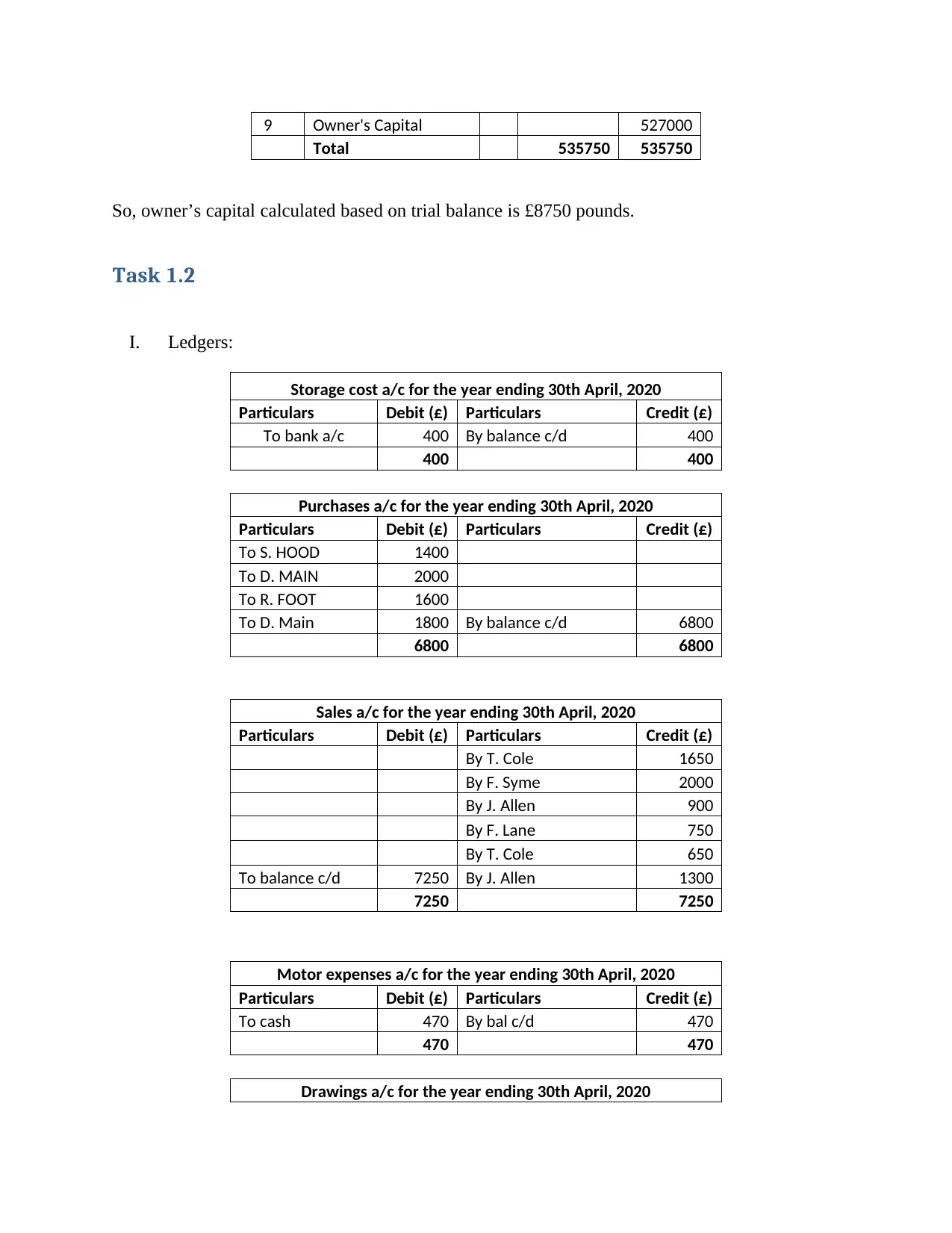

Task 1.1

Trial balance: It is the method of bookkeeping where all ledgers balances arranged into debit

and credit side column; and balance of both side should match. If not matched; indicates there

some errors like omission, wrong entry and double entry errors. Such mismatch balanced with

the help of suspense account which settles later (Smith, 2019).

Ledger: It is a book of accounts which records journal entries and all ledger accounts showing

opening and closing balances which later adjusted in trial balance (Apostolides, 2016).

Trial balance as on 31st March, 2020:

Trial balance as on 31st March, 2020

S.No

. Particulars

L/

F Debit (£)

Credit

(£)

1 Premises 340000

2 Van 51250

3 Fixtures 8100

4 Inventory 63900

5 Receivables 4500

6 Cash at bank 62400

7 Cash in hand 5600

8 Payables 8750

The main purpose of this report is to understand basic concepts about types of business

transactions such as sales, purchases, receipts and payments. Double entry book-keeping is the

basic principal which works on balancing the figure concept; which means if something debit

from the company than it should credit with equal amount to match final figures. Trial balance is

the technique where closing ledger balance directly transfers to match the figures; it is the strong

method to know about any errors in recording transactions either in journal or trial balance.

Financial statements show internal strength of company; this statement covers profit and loss

account, balance sheet and cash flow statement. Bank reconciliation statement is essential to find

any mismatch between cash book and bank passbook. Project contains different scenarios; each

scenario analyses give separate accounting concept with practical examples.

Task 1.1

Trial balance: It is the method of bookkeeping where all ledgers balances arranged into debit

and credit side column; and balance of both side should match. If not matched; indicates there

some errors like omission, wrong entry and double entry errors. Such mismatch balanced with

the help of suspense account which settles later (Smith, 2019).

Ledger: It is a book of accounts which records journal entries and all ledger accounts showing

opening and closing balances which later adjusted in trial balance (Apostolides, 2016).

Trial balance as on 31st March, 2020:

Trial balance as on 31st March, 2020

S.No

. Particulars

L/

F Debit (£)

Credit

(£)

1 Premises 340000

2 Van 51250

3 Fixtures 8100

4 Inventory 63900

5 Receivables 4500

6 Cash at bank 62400

7 Cash in hand 5600

8 Payables 8750

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9 Owner's Capital 527000

Total 535750 535750

So, owner’s capital calculated based on trial balance is £8750 pounds.

Task 1.2

I. Ledgers:

Storage cost a/c for the year ending 30th April, 2020

Particulars Debit (£) Particulars Credit (£)

To bank a/c 400 By balance c/d 400

400 400

Purchases a/c for the year ending 30th April, 2020

Particulars Debit (£) Particulars Credit (£)

To S. HOOD 1400

To D. MAIN 2000

To R. FOOT 1600

To D. Main 1800 By balance c/d 6800

6800 6800

Sales a/c for the year ending 30th April, 2020

Particulars Debit (£) Particulars Credit (£)

By T. Cole 1650

By F. Syme 2000

By J. Allen 900

By F. Lane 750

By T. Cole 650

To balance c/d 7250 By J. Allen 1300

7250 7250

Motor expenses a/c for the year ending 30th April, 2020

Particulars Debit (£) Particulars Credit (£)

To cash 470 By bal c/d 470

470 470

Drawings a/c for the year ending 30th April, 2020

Total 535750 535750

So, owner’s capital calculated based on trial balance is £8750 pounds.

Task 1.2

I. Ledgers:

Storage cost a/c for the year ending 30th April, 2020

Particulars Debit (£) Particulars Credit (£)

To bank a/c 400 By balance c/d 400

400 400

Purchases a/c for the year ending 30th April, 2020

Particulars Debit (£) Particulars Credit (£)

To S. HOOD 1400

To D. MAIN 2000

To R. FOOT 1600

To D. Main 1800 By balance c/d 6800

6800 6800

Sales a/c for the year ending 30th April, 2020

Particulars Debit (£) Particulars Credit (£)

By T. Cole 1650

By F. Syme 2000

By J. Allen 900

By F. Lane 750

By T. Cole 650

To balance c/d 7250 By J. Allen 1300

7250 7250

Motor expenses a/c for the year ending 30th April, 2020

Particulars Debit (£) Particulars Credit (£)

To cash 470 By bal c/d 470

470 470

Drawings a/c for the year ending 30th April, 2020

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Particulars Debit (£) Particulars Credit (£)

To Capital a/c 1500 By bal c/d 1500

1500 1500

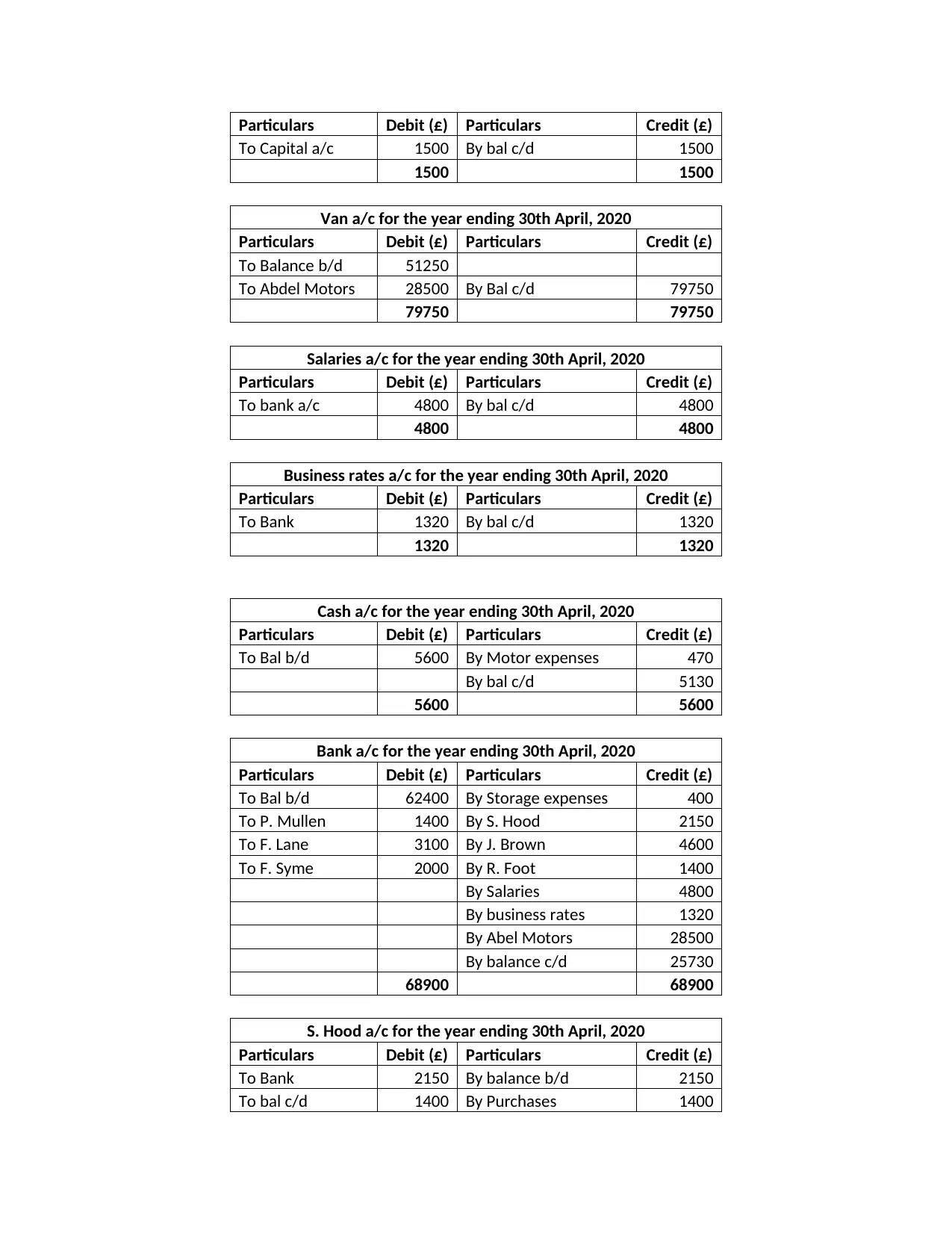

Van a/c for the year ending 30th April, 2020

Particulars Debit (£) Particulars Credit (£)

To Balance b/d 51250

To Abdel Motors 28500 By Bal c/d 79750

79750 79750

Salaries a/c for the year ending 30th April, 2020

Particulars Debit (£) Particulars Credit (£)

To bank a/c 4800 By bal c/d 4800

4800 4800

Business rates a/c for the year ending 30th April, 2020

Particulars Debit (£) Particulars Credit (£)

To Bank 1320 By bal c/d 1320

1320 1320

Cash a/c for the year ending 30th April, 2020

Particulars Debit (£) Particulars Credit (£)

To Bal b/d 5600 By Motor expenses 470

By bal c/d 5130

5600 5600

Bank a/c for the year ending 30th April, 2020

Particulars Debit (£) Particulars Credit (£)

To Bal b/d 62400 By Storage expenses 400

To P. Mullen 1400 By S. Hood 2150

To F. Lane 3100 By J. Brown 4600

To F. Syme 2000 By R. Foot 1400

By Salaries 4800

By business rates 1320

By Abel Motors 28500

By balance c/d 25730

68900 68900

S. Hood a/c for the year ending 30th April, 2020

Particulars Debit (£) Particulars Credit (£)

To Bank 2150 By balance b/d 2150

To bal c/d 1400 By Purchases 1400

To Capital a/c 1500 By bal c/d 1500

1500 1500

Van a/c for the year ending 30th April, 2020

Particulars Debit (£) Particulars Credit (£)

To Balance b/d 51250

To Abdel Motors 28500 By Bal c/d 79750

79750 79750

Salaries a/c for the year ending 30th April, 2020

Particulars Debit (£) Particulars Credit (£)

To bank a/c 4800 By bal c/d 4800

4800 4800

Business rates a/c for the year ending 30th April, 2020

Particulars Debit (£) Particulars Credit (£)

To Bank 1320 By bal c/d 1320

1320 1320

Cash a/c for the year ending 30th April, 2020

Particulars Debit (£) Particulars Credit (£)

To Bal b/d 5600 By Motor expenses 470

By bal c/d 5130

5600 5600

Bank a/c for the year ending 30th April, 2020

Particulars Debit (£) Particulars Credit (£)

To Bal b/d 62400 By Storage expenses 400

To P. Mullen 1400 By S. Hood 2150

To F. Lane 3100 By J. Brown 4600

To F. Syme 2000 By R. Foot 1400

By Salaries 4800

By business rates 1320

By Abel Motors 28500

By balance c/d 25730

68900 68900

S. Hood a/c for the year ending 30th April, 2020

Particulars Debit (£) Particulars Credit (£)

To Bank 2150 By balance b/d 2150

To bal c/d 1400 By Purchases 1400

3550 3550

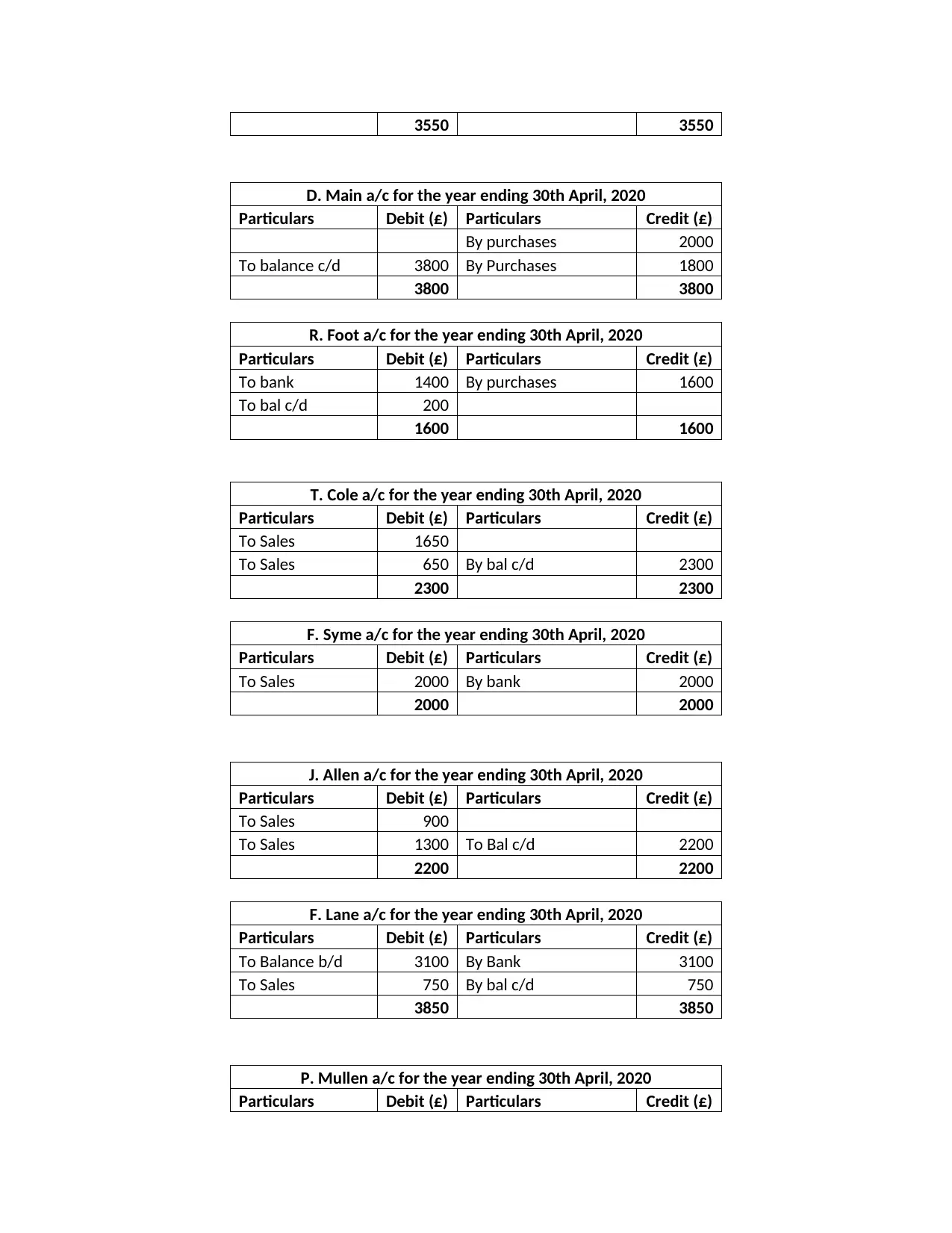

D. Main a/c for the year ending 30th April, 2020

Particulars Debit (£) Particulars Credit (£)

By purchases 2000

To balance c/d 3800 By Purchases 1800

3800 3800

R. Foot a/c for the year ending 30th April, 2020

Particulars Debit (£) Particulars Credit (£)

To bank 1400 By purchases 1600

To bal c/d 200

1600 1600

T. Cole a/c for the year ending 30th April, 2020

Particulars Debit (£) Particulars Credit (£)

To Sales 1650

To Sales 650 By bal c/d 2300

2300 2300

F. Syme a/c for the year ending 30th April, 2020

Particulars Debit (£) Particulars Credit (£)

To Sales 2000 By bank 2000

2000 2000

J. Allen a/c for the year ending 30th April, 2020

Particulars Debit (£) Particulars Credit (£)

To Sales 900

To Sales 1300 To Bal c/d 2200

2200 2200

F. Lane a/c for the year ending 30th April, 2020

Particulars Debit (£) Particulars Credit (£)

To Balance b/d 3100 By Bank 3100

To Sales 750 By bal c/d 750

3850 3850

P. Mullen a/c for the year ending 30th April, 2020

Particulars Debit (£) Particulars Credit (£)

D. Main a/c for the year ending 30th April, 2020

Particulars Debit (£) Particulars Credit (£)

By purchases 2000

To balance c/d 3800 By Purchases 1800

3800 3800

R. Foot a/c for the year ending 30th April, 2020

Particulars Debit (£) Particulars Credit (£)

To bank 1400 By purchases 1600

To bal c/d 200

1600 1600

T. Cole a/c for the year ending 30th April, 2020

Particulars Debit (£) Particulars Credit (£)

To Sales 1650

To Sales 650 By bal c/d 2300

2300 2300

F. Syme a/c for the year ending 30th April, 2020

Particulars Debit (£) Particulars Credit (£)

To Sales 2000 By bank 2000

2000 2000

J. Allen a/c for the year ending 30th April, 2020

Particulars Debit (£) Particulars Credit (£)

To Sales 900

To Sales 1300 To Bal c/d 2200

2200 2200

F. Lane a/c for the year ending 30th April, 2020

Particulars Debit (£) Particulars Credit (£)

To Balance b/d 3100 By Bank 3100

To Sales 750 By bal c/d 750

3850 3850

P. Mullen a/c for the year ending 30th April, 2020

Particulars Debit (£) Particulars Credit (£)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

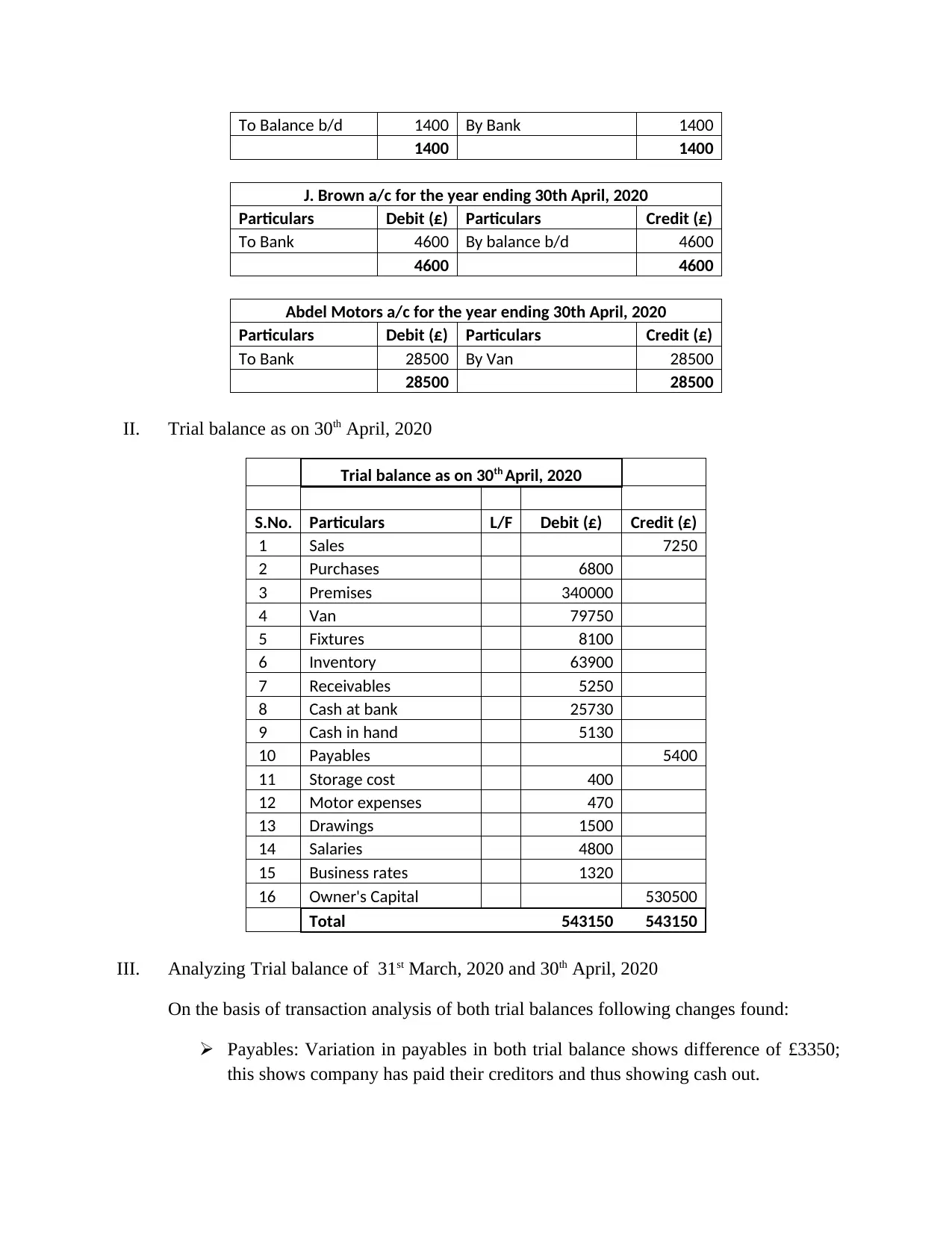

To Balance b/d 1400 By Bank 1400

1400 1400

J. Brown a/c for the year ending 30th April, 2020

Particulars Debit (£) Particulars Credit (£)

To Bank 4600 By balance b/d 4600

4600 4600

Abdel Motors a/c for the year ending 30th April, 2020

Particulars Debit (£) Particulars Credit (£)

To Bank 28500 By Van 28500

28500 28500

II. Trial balance as on 30th April, 2020

Trial balance as on 30th April, 2020

S.No. Particulars L/F Debit (£) Credit (£)

1 Sales 7250

2 Purchases 6800

3 Premises 340000

4 Van 79750

5 Fixtures 8100

6 Inventory 63900

7 Receivables 5250

8 Cash at bank 25730

9 Cash in hand 5130

10 Payables 5400

11 Storage cost 400

12 Motor expenses 470

13 Drawings 1500

14 Salaries 4800

15 Business rates 1320

16 Owner's Capital 530500

Total 543150 543150

III. Analyzing Trial balance of 31st March, 2020 and 30th April, 2020

On the basis of transaction analysis of both trial balances following changes found:

Payables: Variation in payables in both trial balance shows difference of £3350;

this shows company has paid their creditors and thus showing cash out.

1400 1400

J. Brown a/c for the year ending 30th April, 2020

Particulars Debit (£) Particulars Credit (£)

To Bank 4600 By balance b/d 4600

4600 4600

Abdel Motors a/c for the year ending 30th April, 2020

Particulars Debit (£) Particulars Credit (£)

To Bank 28500 By Van 28500

28500 28500

II. Trial balance as on 30th April, 2020

Trial balance as on 30th April, 2020

S.No. Particulars L/F Debit (£) Credit (£)

1 Sales 7250

2 Purchases 6800

3 Premises 340000

4 Van 79750

5 Fixtures 8100

6 Inventory 63900

7 Receivables 5250

8 Cash at bank 25730

9 Cash in hand 5130

10 Payables 5400

11 Storage cost 400

12 Motor expenses 470

13 Drawings 1500

14 Salaries 4800

15 Business rates 1320

16 Owner's Capital 530500

Total 543150 543150

III. Analyzing Trial balance of 31st March, 2020 and 30th April, 2020

On the basis of transaction analysis of both trial balances following changes found:

Payables: Variation in payables in both trial balance shows difference of £3350;

this shows company has paid their creditors and thus showing cash out.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Receivables: The debtors closing account shows the variation of £750 decreases

from previous month; here cash is coming to business (Carey, Knowles &

Towers-Clark, 2017).

Cash at bank: Companies bank balance has decreased to £36670; due to

purchasing of Van and payment to creditors during month.

Cash in hand: Company has paid salaries and storage cost which has decreased

cash balance by £470

Total balance: As on 31st March, 2020 trial balance shows balancing figure of

£535750 and on 30th April, 2020 it has increased to £543150; also owner’s capital

increased with approx. £10000 pounds due because of raise in sales revenue,

Purchases and Van amount.

Task 2.1

Financial Accounting Statement: These are the progression statement of every company

which shows how efficiently its assets and strategies work for earning profit. The main

purpose behind preparing financial accounting statement is to show financial performance and

positions of the company. Some of financial statements include balance sheet, income

statement, cash flows and owner’s equity (Breton, 2018).

Comparison of different financial statements:

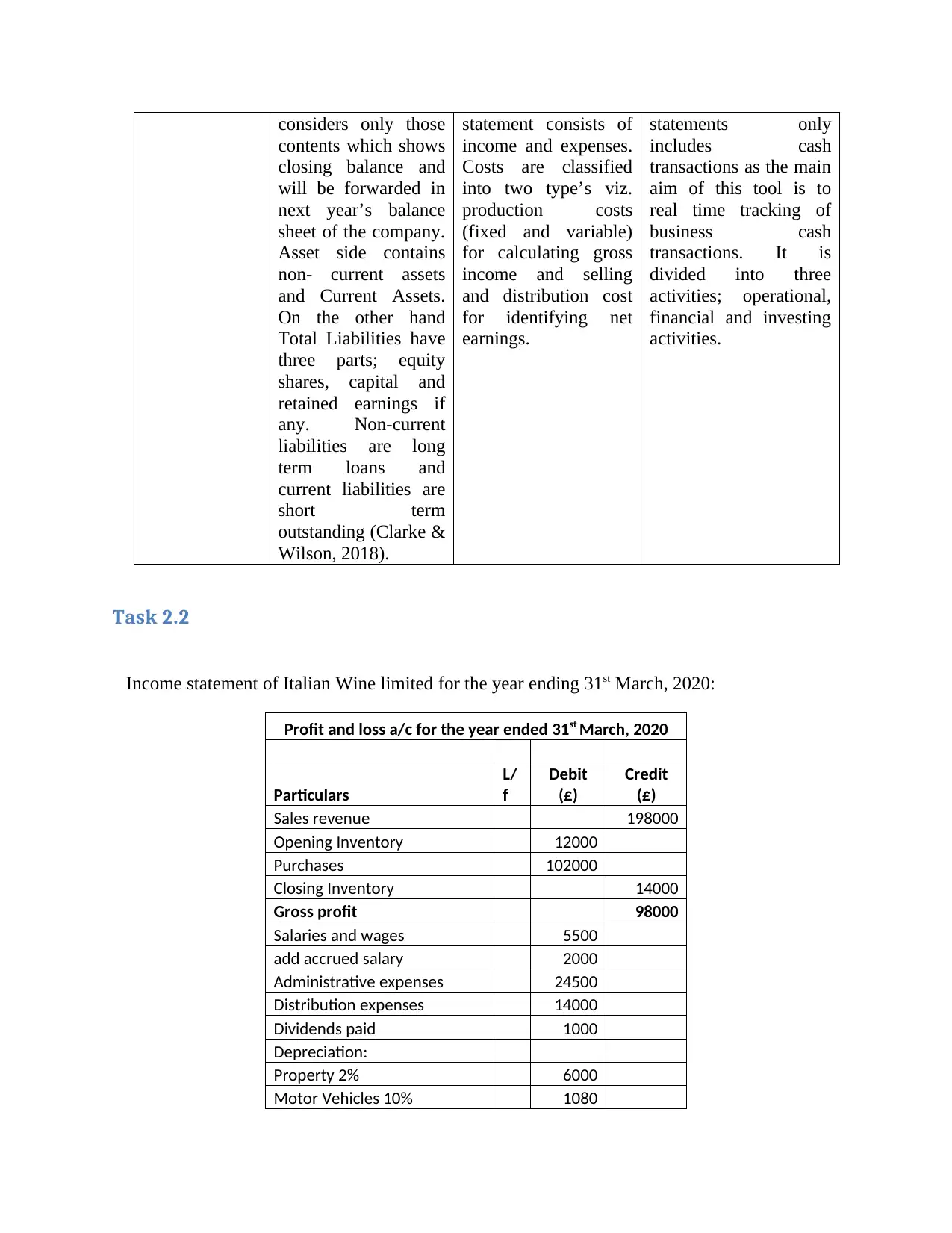

Bases Balance sheet Income statement Cash flow statements

Purpose It is prepared mainly

for showing financial

position of the

company. To know

how much debt and

equity own by

company (Tracy,

2016).

It is mainly prepared

to know total earnings

receive by

organization during a

year.

It has internal use by

companies management

staff to know financial

strength of company to

carry new operations.

Structure Balance sheet is

matching concept

where Total assets

should match with

Equity and liabilities;

where equity is drive

from remaining after

deducting total

liabilities from total

assets.

This statement

contains classification

of expenses and

income separately;

where expenses shows

credit balance and

incomes shows debit

balance.

This statement consists

of three different types

of activities which cash

from operating,

financing and investing

activities (Clarke &

Wilson, 2018).

Content Balance Sheet Content of income Content of cash flow

from previous month; here cash is coming to business (Carey, Knowles &

Towers-Clark, 2017).

Cash at bank: Companies bank balance has decreased to £36670; due to

purchasing of Van and payment to creditors during month.

Cash in hand: Company has paid salaries and storage cost which has decreased

cash balance by £470

Total balance: As on 31st March, 2020 trial balance shows balancing figure of

£535750 and on 30th April, 2020 it has increased to £543150; also owner’s capital

increased with approx. £10000 pounds due because of raise in sales revenue,

Purchases and Van amount.

Task 2.1

Financial Accounting Statement: These are the progression statement of every company

which shows how efficiently its assets and strategies work for earning profit. The main

purpose behind preparing financial accounting statement is to show financial performance and

positions of the company. Some of financial statements include balance sheet, income

statement, cash flows and owner’s equity (Breton, 2018).

Comparison of different financial statements:

Bases Balance sheet Income statement Cash flow statements

Purpose It is prepared mainly

for showing financial

position of the

company. To know

how much debt and

equity own by

company (Tracy,

2016).

It is mainly prepared

to know total earnings

receive by

organization during a

year.

It has internal use by

companies management

staff to know financial

strength of company to

carry new operations.

Structure Balance sheet is

matching concept

where Total assets

should match with

Equity and liabilities;

where equity is drive

from remaining after

deducting total

liabilities from total

assets.

This statement

contains classification

of expenses and

income separately;

where expenses shows

credit balance and

incomes shows debit

balance.

This statement consists

of three different types

of activities which cash

from operating,

financing and investing

activities (Clarke &

Wilson, 2018).

Content Balance Sheet Content of income Content of cash flow

considers only those

contents which shows

closing balance and

will be forwarded in

next year’s balance

sheet of the company.

Asset side contains

non- current assets

and Current Assets.

On the other hand

Total Liabilities have

three parts; equity

shares, capital and

retained earnings if

any. Non-current

liabilities are long

term loans and

current liabilities are

short term

outstanding (Clarke &

Wilson, 2018).

statement consists of

income and expenses.

Costs are classified

into two type’s viz.

production costs

(fixed and variable)

for calculating gross

income and selling

and distribution cost

for identifying net

earnings.

statements only

includes cash

transactions as the main

aim of this tool is to

real time tracking of

business cash

transactions. It is

divided into three

activities; operational,

financial and investing

activities.

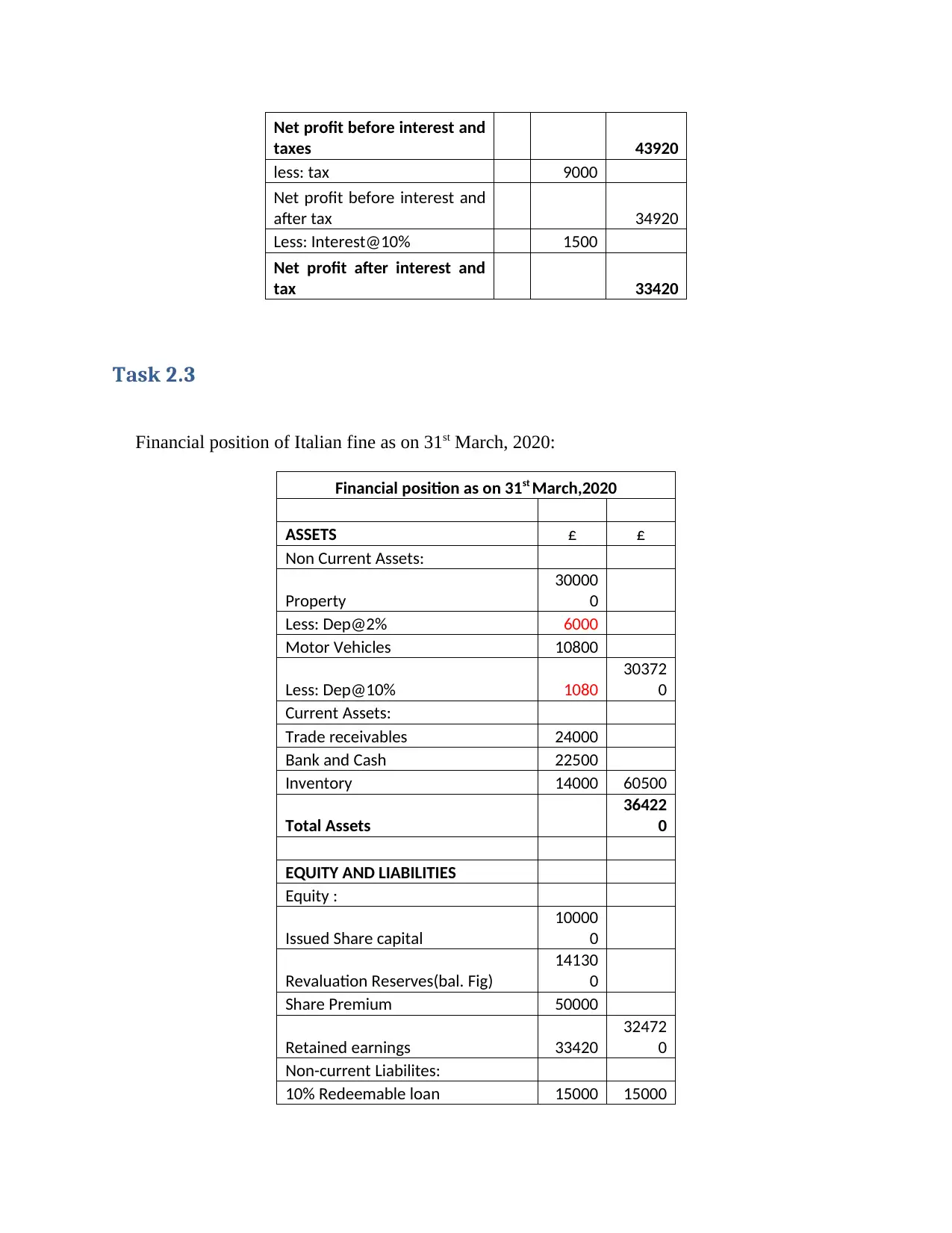

Task 2.2

Income statement of Italian Wine limited for the year ending 31st March, 2020:

Profit and loss a/c for the year ended 31st March, 2020

Particulars

L/

f

Debit

(£)

Credit

(£)

Sales revenue 198000

Opening Inventory 12000

Purchases 102000

Closing Inventory 14000

Gross profit 98000

Salaries and wages 5500

add accrued salary 2000

Administrative expenses 24500

Distribution expenses 14000

Dividends paid 1000

Depreciation:

Property 2% 6000

Motor Vehicles 10% 1080

contents which shows

closing balance and

will be forwarded in

next year’s balance

sheet of the company.

Asset side contains

non- current assets

and Current Assets.

On the other hand

Total Liabilities have

three parts; equity

shares, capital and

retained earnings if

any. Non-current

liabilities are long

term loans and

current liabilities are

short term

outstanding (Clarke &

Wilson, 2018).

statement consists of

income and expenses.

Costs are classified

into two type’s viz.

production costs

(fixed and variable)

for calculating gross

income and selling

and distribution cost

for identifying net

earnings.

statements only

includes cash

transactions as the main

aim of this tool is to

real time tracking of

business cash

transactions. It is

divided into three

activities; operational,

financial and investing

activities.

Task 2.2

Income statement of Italian Wine limited for the year ending 31st March, 2020:

Profit and loss a/c for the year ended 31st March, 2020

Particulars

L/

f

Debit

(£)

Credit

(£)

Sales revenue 198000

Opening Inventory 12000

Purchases 102000

Closing Inventory 14000

Gross profit 98000

Salaries and wages 5500

add accrued salary 2000

Administrative expenses 24500

Distribution expenses 14000

Dividends paid 1000

Depreciation:

Property 2% 6000

Motor Vehicles 10% 1080

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Net profit before interest and

taxes 43920

less: tax 9000

Net profit before interest and

after tax 34920

Less: Interest@10% 1500

Net profit after interest and

tax 33420

Task 2.3

Financial position of Italian fine as on 31st March, 2020:

Financial position as on 31st March,2020

ASSETS £ £

Non Current Assets:

Property

30000

0

Less: Dep@2% 6000

Motor Vehicles 10800

Less: Dep@10% 1080

30372

0

Current Assets:

Trade receivables 24000

Bank and Cash 22500

Inventory 14000 60500

Total Assets

36422

0

EQUITY AND LIABILITIES

Equity :

Issued Share capital

10000

0

Revaluation Reserves(bal. Fig)

14130

0

Share Premium 50000

Retained earnings 33420

32472

0

Non-current Liabilites:

10% Redeemable loan 15000 15000

taxes 43920

less: tax 9000

Net profit before interest and

after tax 34920

Less: Interest@10% 1500

Net profit after interest and

tax 33420

Task 2.3

Financial position of Italian fine as on 31st March, 2020:

Financial position as on 31st March,2020

ASSETS £ £

Non Current Assets:

Property

30000

0

Less: Dep@2% 6000

Motor Vehicles 10800

Less: Dep@10% 1080

30372

0

Current Assets:

Trade receivables 24000

Bank and Cash 22500

Inventory 14000 60500

Total Assets

36422

0

EQUITY AND LIABILITIES

Equity :

Issued Share capital

10000

0

Revaluation Reserves(bal. Fig)

14130

0

Share Premium 50000

Retained earnings 33420

32472

0

Non-current Liabilites:

10% Redeemable loan 15000 15000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Current Liabilities:

Accrued salary 2000

Trade payables 21000

Accrued Interest@10% 1500 24500

Total Equity and liabilities

36422

0

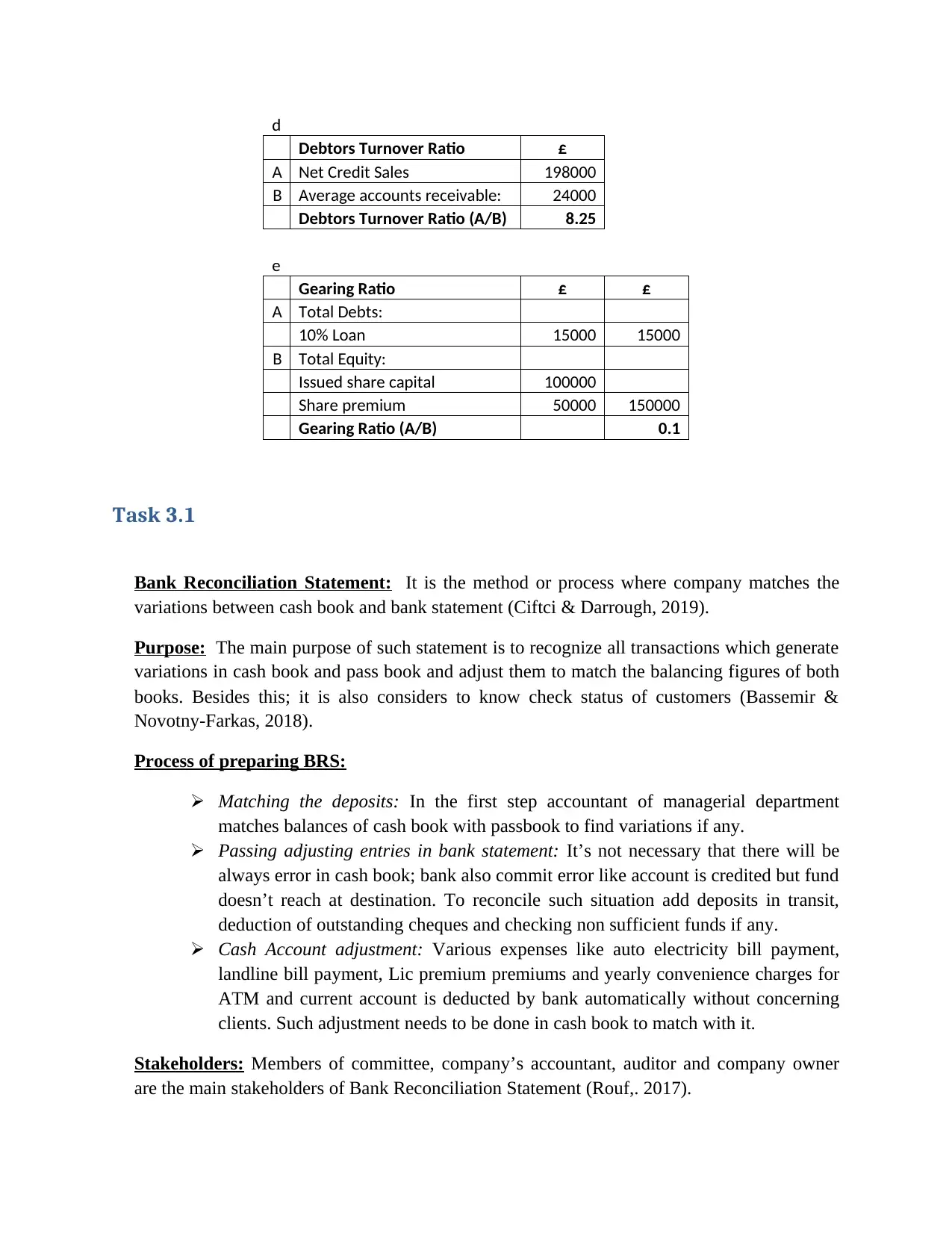

Task 2.4

Calculations of various ratios:

a) Return on Capital employed:

b) Gross profit margin:

c) Net profit Margin:

d) Debtors turnover:

e) Gearing ratio:

Return on capital employed £ £

A

Earnings before Interest and

Tax (EBIT) 43920

Total Assets 364220

Less: Current Liabilities 24500

B Capital Employed 339720

ROCE (A/B) × 100 13%

b

Gross Profit Margin £

A Gross Profit 98000

B Net Sales 198000

Gross Profit Margin (A/B) ×

100 49%

c

Net Profit Margin £

A

Net profit after interest and

tax 33420

B Net sales 198000

Net Profit margin(A/B) × 100 17%

Accrued salary 2000

Trade payables 21000

Accrued Interest@10% 1500 24500

Total Equity and liabilities

36422

0

Task 2.4

Calculations of various ratios:

a) Return on Capital employed:

b) Gross profit margin:

c) Net profit Margin:

d) Debtors turnover:

e) Gearing ratio:

Return on capital employed £ £

A

Earnings before Interest and

Tax (EBIT) 43920

Total Assets 364220

Less: Current Liabilities 24500

B Capital Employed 339720

ROCE (A/B) × 100 13%

b

Gross Profit Margin £

A Gross Profit 98000

B Net Sales 198000

Gross Profit Margin (A/B) ×

100 49%

c

Net Profit Margin £

A

Net profit after interest and

tax 33420

B Net sales 198000

Net Profit margin(A/B) × 100 17%

d

Debtors Turnover Ratio £

A Net Credit Sales 198000

B Average accounts receivable: 24000

Debtors Turnover Ratio (A/B) 8.25

e

Gearing Ratio £ £

A Total Debts:

10% Loan 15000 15000

B Total Equity:

Issued share capital 100000

Share premium 50000 150000

Gearing Ratio (A/B) 0.1

Task 3.1

Bank Reconciliation Statement: It is the method or process where company matches the

variations between cash book and bank statement (Ciftci & Darrough, 2019).

Purpose: The main purpose of such statement is to recognize all transactions which generate

variations in cash book and pass book and adjust them to match the balancing figures of both

books. Besides this; it is also considers to know check status of customers (Bassemir &

Novotny‐Farkas, 2018).

Process of preparing BRS:

Matching the deposits: In the first step accountant of managerial department

matches balances of cash book with passbook to find variations if any.

Passing adjusting entries in bank statement: It’s not necessary that there will be

always error in cash book; bank also commit error like account is credited but fund

doesn’t reach at destination. To reconcile such situation add deposits in transit,

deduction of outstanding cheques and checking non sufficient funds if any.

Cash Account adjustment: Various expenses like auto electricity bill payment,

landline bill payment, Lic premium premiums and yearly convenience charges for

ATM and current account is deducted by bank automatically without concerning

clients. Such adjustment needs to be done in cash book to match with it.

Stakeholders: Members of committee, company’s accountant, auditor and company owner

are the main stakeholders of Bank Reconciliation Statement (Rouf,. 2017).

Debtors Turnover Ratio £

A Net Credit Sales 198000

B Average accounts receivable: 24000

Debtors Turnover Ratio (A/B) 8.25

e

Gearing Ratio £ £

A Total Debts:

10% Loan 15000 15000

B Total Equity:

Issued share capital 100000

Share premium 50000 150000

Gearing Ratio (A/B) 0.1

Task 3.1

Bank Reconciliation Statement: It is the method or process where company matches the

variations between cash book and bank statement (Ciftci & Darrough, 2019).

Purpose: The main purpose of such statement is to recognize all transactions which generate

variations in cash book and pass book and adjust them to match the balancing figures of both

books. Besides this; it is also considers to know check status of customers (Bassemir &

Novotny‐Farkas, 2018).

Process of preparing BRS:

Matching the deposits: In the first step accountant of managerial department

matches balances of cash book with passbook to find variations if any.

Passing adjusting entries in bank statement: It’s not necessary that there will be

always error in cash book; bank also commit error like account is credited but fund

doesn’t reach at destination. To reconcile such situation add deposits in transit,

deduction of outstanding cheques and checking non sufficient funds if any.

Cash Account adjustment: Various expenses like auto electricity bill payment,

landline bill payment, Lic premium premiums and yearly convenience charges for

ATM and current account is deducted by bank automatically without concerning

clients. Such adjustment needs to be done in cash book to match with it.

Stakeholders: Members of committee, company’s accountant, auditor and company owner

are the main stakeholders of Bank Reconciliation Statement (Rouf,. 2017).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.