Financial Accounting Report: Client Transactions and Analysis

VerifiedAdded on 2021/02/19

|21

|5902

|57

Report

AI Summary

This report delves into the core principles of financial accounting, providing a comprehensive analysis of its purpose, stakeholders, and practical applications. It examines financial reporting procedures, emphasizing the importance of accurate record-keeping for internal and external stakeholders. The report includes detailed examples of journal entries, cash books, and nominal ledgers, illustrating how financial transactions are recorded and managed. Client case studies are presented to demonstrate the application of these concepts in real-world scenarios. Furthermore, the report explains the purpose of bank reconciliation statements, the reasons for discrepancies between cash book and bank statements, and the use of imprest systems. It also covers the reconciliation process for control accounts and explores the features of suspense accounts. Overall, the report provides a thorough understanding of financial accounting practices, including the preparation and interpretation of financial statements. The report includes solved assignments to aid understanding.

UNIT 10 AND FINANCIAL

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

BUSINESS REPORT......................................................................................................................1

Financial Accounting: Purpose...................................................................................................1

Stakeholders................................................................................................................................2

CLIENT 1........................................................................................................................................3

Journal Entries.............................................................................................................................3

Cash Book...................................................................................................................................5

Nominal Ledger..........................................................................................................................5

Purchase Ledger........................................................................................................................11

Trial Balance using Balance-Off Rule......................................................................................11

CLIENT 2......................................................................................................................................12

CLIENT 3......................................................................................................................................14

1. Purpose of preparing Bank Reconciliation Statement..........................................................14

2. Reason for difference between balance of bank column of cash book and bank statements14

3. Imprest...................................................................................................................................15

Application of Bank Reconciliation Process.............................................................................15

CLIENT 4......................................................................................................................................15

Process to reconcile Control Accounts.....................................................................................15

3. Control Account....................................................................................................................16

CLIENT 5......................................................................................................................................16

1. Suspense Account and its main features:..............................................................................16

CONCLUSION..............................................................................................................................17

REFERENCES..............................................................................................................................18

INTRODUCTION...........................................................................................................................1

BUSINESS REPORT......................................................................................................................1

Financial Accounting: Purpose...................................................................................................1

Stakeholders................................................................................................................................2

CLIENT 1........................................................................................................................................3

Journal Entries.............................................................................................................................3

Cash Book...................................................................................................................................5

Nominal Ledger..........................................................................................................................5

Purchase Ledger........................................................................................................................11

Trial Balance using Balance-Off Rule......................................................................................11

CLIENT 2......................................................................................................................................12

CLIENT 3......................................................................................................................................14

1. Purpose of preparing Bank Reconciliation Statement..........................................................14

2. Reason for difference between balance of bank column of cash book and bank statements14

3. Imprest...................................................................................................................................15

Application of Bank Reconciliation Process.............................................................................15

CLIENT 4......................................................................................................................................15

Process to reconcile Control Accounts.....................................................................................15

3. Control Account....................................................................................................................16

CLIENT 5......................................................................................................................................16

1. Suspense Account and its main features:..............................................................................16

CONCLUSION..............................................................................................................................17

REFERENCES..............................................................................................................................18

INTRODUCTION

In present business scenario, the process of preparing annual accounts that are used by

internal and external parties of business in order to make meaningful decision is knows as

financial reporting. Financial accounting procedure includes reporting of each financial dealing

so that final accounts are prepared to define the predefined objective (Barth, 2015). It is

described that reporting is primary characteristic of financial accounting that aid to define the

actual financial position and overall performance of company to stakeholders.

In this project report a complete explanation and aim of financial accounting, internal or

external stakeholders, main intent of bank reconciliation statement and control accounts. Apart

this detail description of suspense and Imprest account and its primary characteristic are

discussed in this report.

BUSINESS REPORT

Financial Accounting: Purpose

The concept of Financial Accounting is mainly concerned with keeping track of the

financial transactions undertaken by a particular business entity. This is ensured by employing

standardized guidelines on the basis of which transactions of varying nature are identified,

recorded, classified, summarised and then reported in a financial report (Bebbington, Unerman

and O’DWYER, 2014). These financial reports are usually known as Annual Reports that

contain the final accounts or statements of a business enterprise for a given time period.

The main purpose of Financial Accounting is to provision sufficient information for

various internal as well as external parties for whom such subject matter is of great importance.

This helps such parties to assess the value of company in a discrete manner and enables them to

reach important conclusions for present as well as future investment purposes. Due to this fact,

the discipline of financial accounting consists of guidelines that are generalised all around the

world in the form of Accounting Standards (AS) as well as Generally Accepted Accounting

Principles (GAAP). Apart from this, the company is also able:

To plan and forecast its future strategic moves by analysing such information gained for a

particular accounting year.

To ensure conformity to various standardized guidelines by maintaining proper book-

keeping systems.

1

In present business scenario, the process of preparing annual accounts that are used by

internal and external parties of business in order to make meaningful decision is knows as

financial reporting. Financial accounting procedure includes reporting of each financial dealing

so that final accounts are prepared to define the predefined objective (Barth, 2015). It is

described that reporting is primary characteristic of financial accounting that aid to define the

actual financial position and overall performance of company to stakeholders.

In this project report a complete explanation and aim of financial accounting, internal or

external stakeholders, main intent of bank reconciliation statement and control accounts. Apart

this detail description of suspense and Imprest account and its primary characteristic are

discussed in this report.

BUSINESS REPORT

Financial Accounting: Purpose

The concept of Financial Accounting is mainly concerned with keeping track of the

financial transactions undertaken by a particular business entity. This is ensured by employing

standardized guidelines on the basis of which transactions of varying nature are identified,

recorded, classified, summarised and then reported in a financial report (Bebbington, Unerman

and O’DWYER, 2014). These financial reports are usually known as Annual Reports that

contain the final accounts or statements of a business enterprise for a given time period.

The main purpose of Financial Accounting is to provision sufficient information for

various internal as well as external parties for whom such subject matter is of great importance.

This helps such parties to assess the value of company in a discrete manner and enables them to

reach important conclusions for present as well as future investment purposes. Due to this fact,

the discipline of financial accounting consists of guidelines that are generalised all around the

world in the form of Accounting Standards (AS) as well as Generally Accepted Accounting

Principles (GAAP). Apart from this, the company is also able:

To plan and forecast its future strategic moves by analysing such information gained for a

particular accounting year.

To ensure conformity to various standardized guidelines by maintaining proper book-

keeping systems.

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

To measure financial performance and profitability in monetary terms.

To facilitate important decisions in regards to taxation, liabilities and other such matters.

To compare the performance on industrial as well as competitive lines that help the top-

management in knowing their key strengths and weaknesses.

To identify various points of competitive advantages that are posessed by the business.

Stakeholders

Stakeholders may be defined as those parties who are largely impacted by the actions of

an organisation for various reasons. These actions mostly include policies, current as well as

future objectives among others (Bryer, 2012). Stakeholders may be internal and external. It is

important to note that not all stakeholders are equal. These have been discussed as under:

Internal Stakeholders:

These are those parties or entities that are directly engaged within a business. For instance,

employees and board of directors are two of the main types of internal stakeholders. Employees

are those which are mainly involved in the execution of strategic goals and objectives in a

definite manner. On the other hand, Board of Directors are those who are directly involved in

the formulation and overlooking the operations so as to ensure that the predefined action plans

are carried out in a manner that result in achievement of goals. Hence, by coordinating and

cooperating together, internal stakeholders are able to carry out the operations of the business

profitably.

External Stakeholders:

These are those parties or entities that are not directly engaged within a business. For instance,

government, customers, regulatory bodies and investors are fourof the main types of external

stakeholders. Government is one that is resposible for creation of policies that govern the

internal as well as the external business environment in which a company operates. Hence,

information derived from financial accounting can help in the ascertainment of tax sheilds and

tax liabilities in an effective manner. Customers are those stakeholders which directly impact

the profitability of the business. Hence, they are interested in knowing how transparent the

company is in its operations and whether or not it is socially aware regarding its activities

(Chiang, Nouri and Samanta, 2014). Regulatory Bodies are interested in knowing how well the

company is able to conform with the various rules and guidelines that relevant to a particular

2

To facilitate important decisions in regards to taxation, liabilities and other such matters.

To compare the performance on industrial as well as competitive lines that help the top-

management in knowing their key strengths and weaknesses.

To identify various points of competitive advantages that are posessed by the business.

Stakeholders

Stakeholders may be defined as those parties who are largely impacted by the actions of

an organisation for various reasons. These actions mostly include policies, current as well as

future objectives among others (Bryer, 2012). Stakeholders may be internal and external. It is

important to note that not all stakeholders are equal. These have been discussed as under:

Internal Stakeholders:

These are those parties or entities that are directly engaged within a business. For instance,

employees and board of directors are two of the main types of internal stakeholders. Employees

are those which are mainly involved in the execution of strategic goals and objectives in a

definite manner. On the other hand, Board of Directors are those who are directly involved in

the formulation and overlooking the operations so as to ensure that the predefined action plans

are carried out in a manner that result in achievement of goals. Hence, by coordinating and

cooperating together, internal stakeholders are able to carry out the operations of the business

profitably.

External Stakeholders:

These are those parties or entities that are not directly engaged within a business. For instance,

government, customers, regulatory bodies and investors are fourof the main types of external

stakeholders. Government is one that is resposible for creation of policies that govern the

internal as well as the external business environment in which a company operates. Hence,

information derived from financial accounting can help in the ascertainment of tax sheilds and

tax liabilities in an effective manner. Customers are those stakeholders which directly impact

the profitability of the business. Hence, they are interested in knowing how transparent the

company is in its operations and whether or not it is socially aware regarding its activities

(Chiang, Nouri and Samanta, 2014). Regulatory Bodies are interested in knowing how well the

company is able to conform with the various rules and guidelines that relevant to a particular

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

organisation. Investors are interested in knowing how profitable it is for them to earn rewards in

the form of dividends from current as well as future perspective.

CLIENT 1

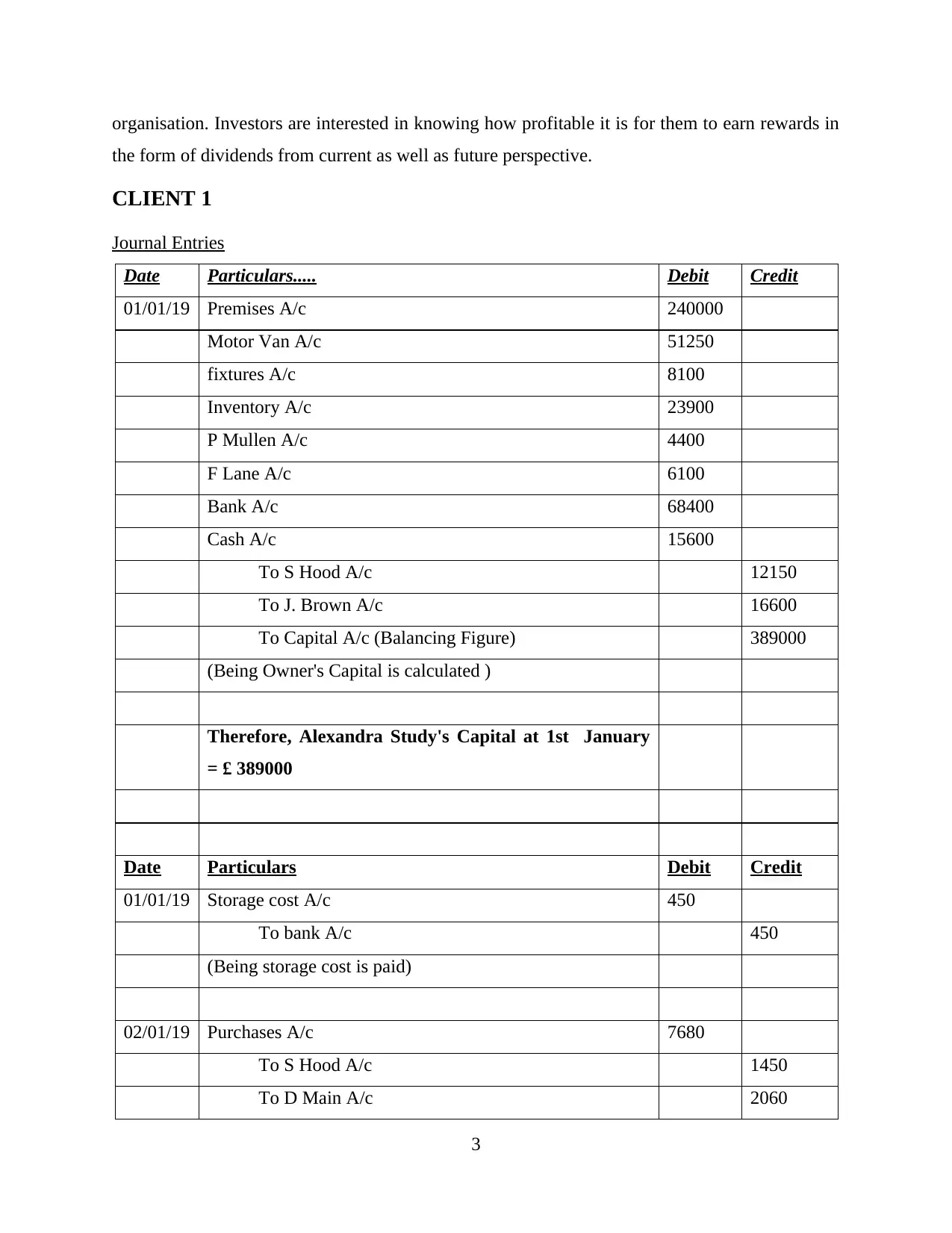

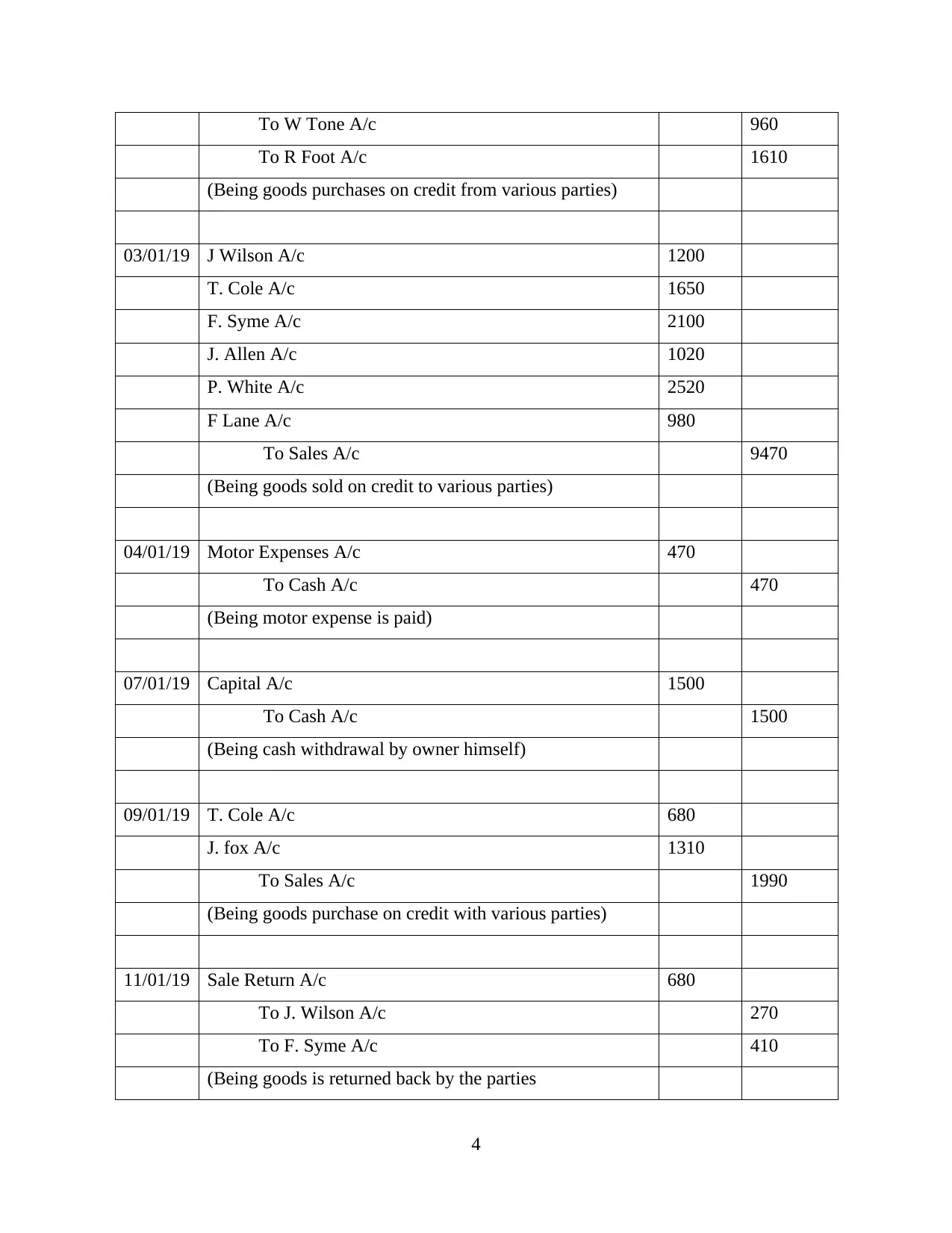

Journal Entries

Date Particulars..... Debit Credit

01/01/19 Premises A/c 240000

Motor Van A/c 51250

fixtures A/c 8100

Inventory A/c 23900

P Mullen A/c 4400

F Lane A/c 6100

Bank A/c 68400

Cash A/c 15600

To S Hood A/c 12150

To J. Brown A/c 16600

To Capital A/c (Balancing Figure) 389000

(Being Owner's Capital is calculated )

Therefore, Alexandra Study's Capital at 1st January

= £ 389000

Date Particulars Debit Credit

01/01/19 Storage cost A/c 450

To bank A/c 450

(Being storage cost is paid)

02/01/19 Purchases A/c 7680

To S Hood A/c 1450

To D Main A/c 2060

3

the form of dividends from current as well as future perspective.

CLIENT 1

Journal Entries

Date Particulars..... Debit Credit

01/01/19 Premises A/c 240000

Motor Van A/c 51250

fixtures A/c 8100

Inventory A/c 23900

P Mullen A/c 4400

F Lane A/c 6100

Bank A/c 68400

Cash A/c 15600

To S Hood A/c 12150

To J. Brown A/c 16600

To Capital A/c (Balancing Figure) 389000

(Being Owner's Capital is calculated )

Therefore, Alexandra Study's Capital at 1st January

= £ 389000

Date Particulars Debit Credit

01/01/19 Storage cost A/c 450

To bank A/c 450

(Being storage cost is paid)

02/01/19 Purchases A/c 7680

To S Hood A/c 1450

To D Main A/c 2060

3

To W Tone A/c 960

To R Foot A/c 1610

(Being goods purchases on credit from various parties)

03/01/19 J Wilson A/c 1200

T. Cole A/c 1650

F. Syme A/c 2100

J. Allen A/c 1020

P. White A/c 2520

F Lane A/c 980

To Sales A/c 9470

(Being goods sold on credit to various parties)

04/01/19 Motor Expenses A/c 470

To Cash A/c 470

(Being motor expense is paid)

07/01/19 Capital A/c 1500

To Cash A/c 1500

(Being cash withdrawal by owner himself)

09/01/19 T. Cole A/c 680

J. fox A/c 1310

To Sales A/c 1990

(Being goods purchase on credit with various parties)

11/01/19 Sale Return A/c 680

To J. Wilson A/c 270

To F. Syme A/c 410

(Being goods is returned back by the parties

4

To R Foot A/c 1610

(Being goods purchases on credit from various parties)

03/01/19 J Wilson A/c 1200

T. Cole A/c 1650

F. Syme A/c 2100

J. Allen A/c 1020

P. White A/c 2520

F Lane A/c 980

To Sales A/c 9470

(Being goods sold on credit to various parties)

04/01/19 Motor Expenses A/c 470

To Cash A/c 470

(Being motor expense is paid)

07/01/19 Capital A/c 1500

To Cash A/c 1500

(Being cash withdrawal by owner himself)

09/01/19 T. Cole A/c 680

J. fox A/c 1310

To Sales A/c 1990

(Being goods purchase on credit with various parties)

11/01/19 Sale Return A/c 680

To J. Wilson A/c 270

To F. Syme A/c 410

(Being goods is returned back by the parties

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

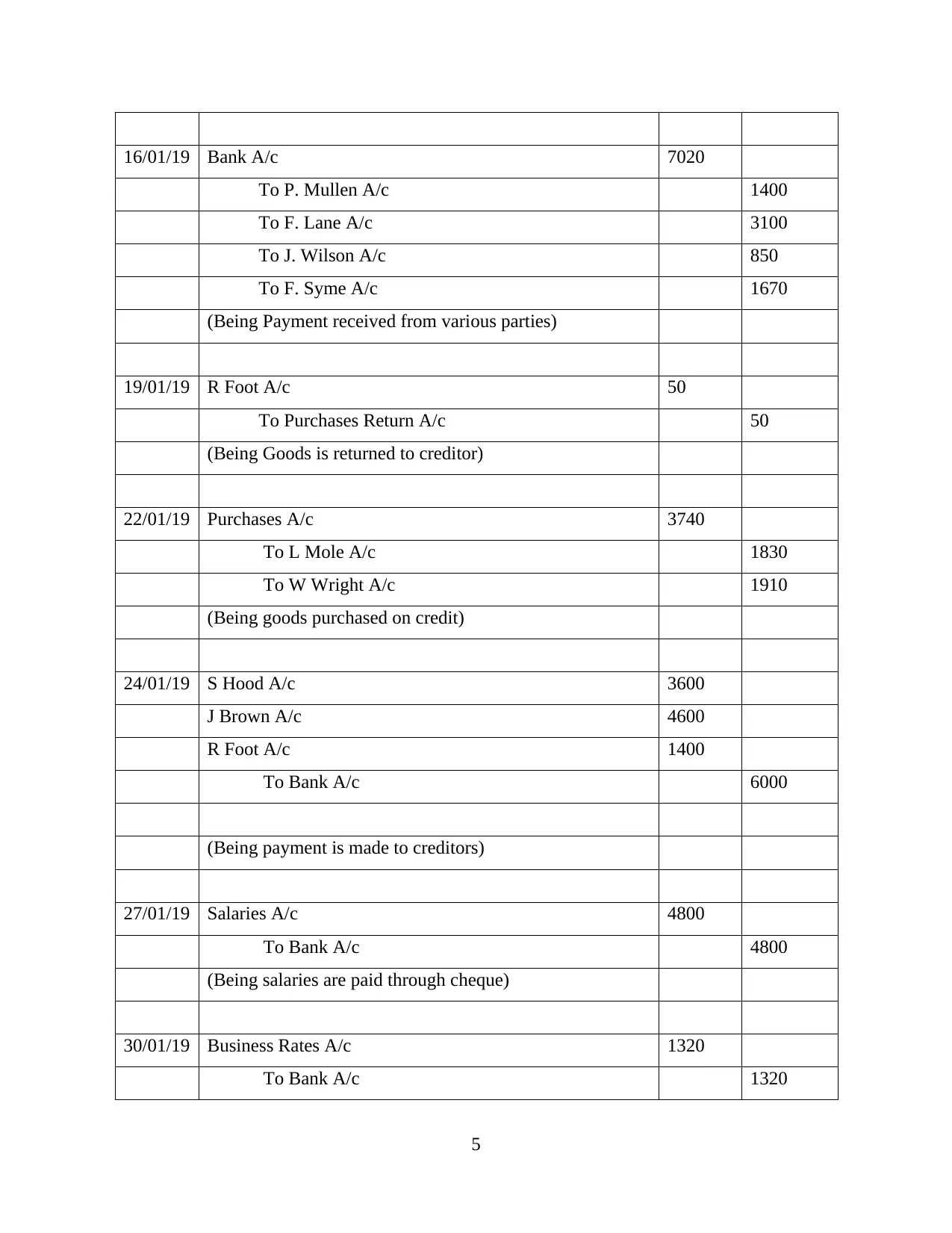

16/01/19 Bank A/c 7020

To P. Mullen A/c 1400

To F. Lane A/c 3100

To J. Wilson A/c 850

To F. Syme A/c 1670

(Being Payment received from various parties)

19/01/19 R Foot A/c 50

To Purchases Return A/c 50

(Being Goods is returned to creditor)

22/01/19 Purchases A/c 3740

To L Mole A/c 1830

To W Wright A/c 1910

(Being goods purchased on credit)

24/01/19 S Hood A/c 3600

J Brown A/c 4600

R Foot A/c 1400

To Bank A/c 6000

(Being payment is made to creditors)

27/01/19 Salaries A/c 4800

To Bank A/c 4800

(Being salaries are paid through cheque)

30/01/19 Business Rates A/c 1320

To Bank A/c 1320

5

To P. Mullen A/c 1400

To F. Lane A/c 3100

To J. Wilson A/c 850

To F. Syme A/c 1670

(Being Payment received from various parties)

19/01/19 R Foot A/c 50

To Purchases Return A/c 50

(Being Goods is returned to creditor)

22/01/19 Purchases A/c 3740

To L Mole A/c 1830

To W Wright A/c 1910

(Being goods purchased on credit)

24/01/19 S Hood A/c 3600

J Brown A/c 4600

R Foot A/c 1400

To Bank A/c 6000

(Being payment is made to creditors)

27/01/19 Salaries A/c 4800

To Bank A/c 4800

(Being salaries are paid through cheque)

30/01/19 Business Rates A/c 1320

To Bank A/c 1320

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

(Being business rates are paid through cheque)

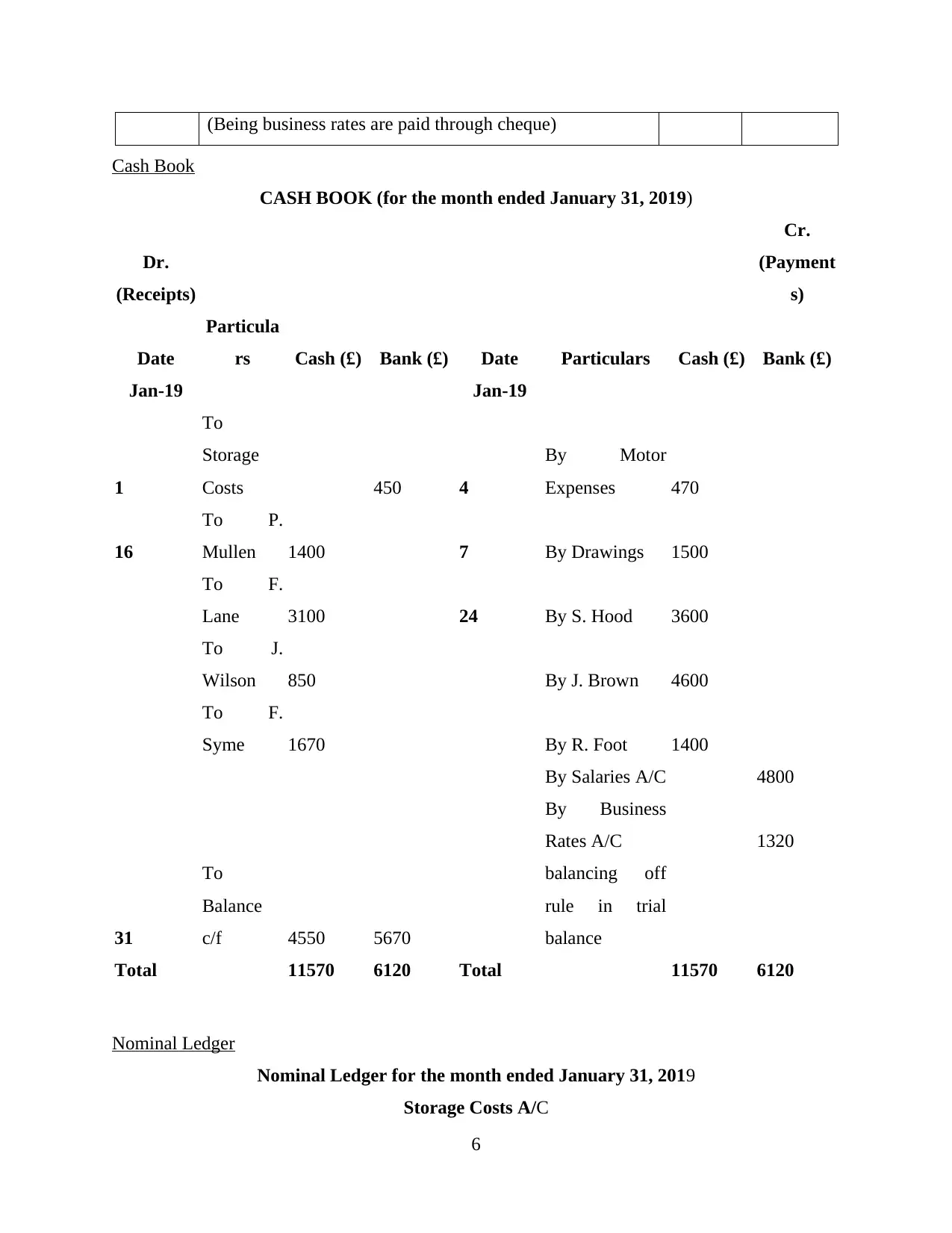

Cash Book

CASH BOOK (for the month ended January 31, 2019)

Dr.

(Receipts)

Cr.

(Payment

s)

Date

Particula

rs Cash (£) Bank (£) Date Particulars Cash (£) Bank (£)

Jan-19 Jan-19

1

To

Storage

Costs 450 4

By Motor

Expenses 470

16

To P.

Mullen 1400 7 By Drawings 1500

To F.

Lane 3100 24 By S. Hood 3600

To J.

Wilson 850 By J. Brown 4600

To F.

Syme 1670 By R. Foot 1400

By Salaries A/C 4800

By Business

Rates A/C 1320

31

To

Balance

c/f 4550 5670

balancing off

rule in trial

balance

Total 11570 6120 Total 11570 6120

Nominal Ledger

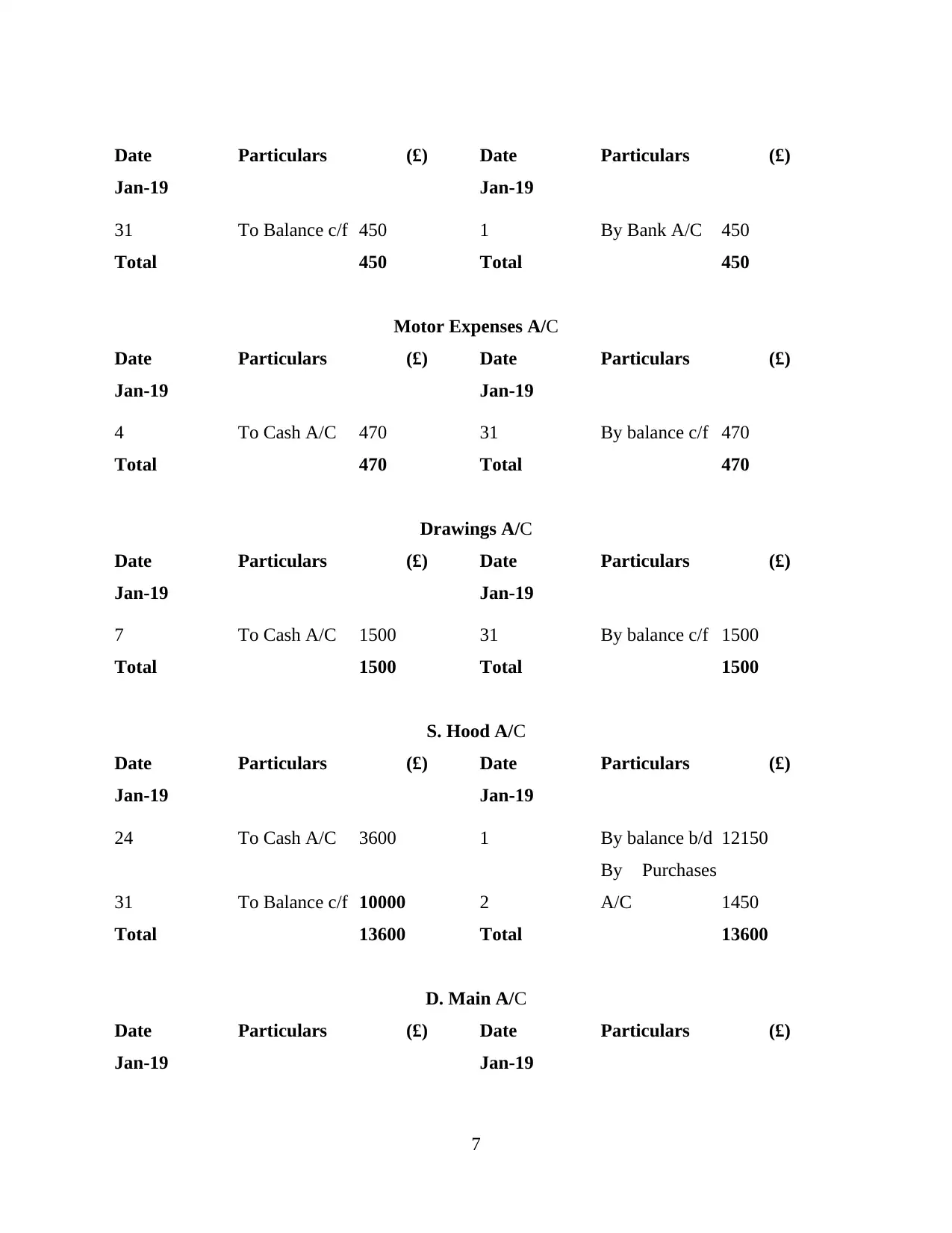

Nominal Ledger for the month ended January 31, 2019

Storage Costs A/C

6

Cash Book

CASH BOOK (for the month ended January 31, 2019)

Dr.

(Receipts)

Cr.

(Payment

s)

Date

Particula

rs Cash (£) Bank (£) Date Particulars Cash (£) Bank (£)

Jan-19 Jan-19

1

To

Storage

Costs 450 4

By Motor

Expenses 470

16

To P.

Mullen 1400 7 By Drawings 1500

To F.

Lane 3100 24 By S. Hood 3600

To J.

Wilson 850 By J. Brown 4600

To F.

Syme 1670 By R. Foot 1400

By Salaries A/C 4800

By Business

Rates A/C 1320

31

To

Balance

c/f 4550 5670

balancing off

rule in trial

balance

Total 11570 6120 Total 11570 6120

Nominal Ledger

Nominal Ledger for the month ended January 31, 2019

Storage Costs A/C

6

Date Particulars (£) Date Particulars (£)

Jan-19 Jan-19

31 To Balance c/f 450 1 By Bank A/C 450

Total 450 Total 450

Motor Expenses A/C

Date Particulars (£) Date Particulars (£)

Jan-19 Jan-19

4 To Cash A/C 470 31 By balance c/f 470

Total 470 Total 470

Drawings A/C

Date Particulars (£) Date Particulars (£)

Jan-19 Jan-19

7 To Cash A/C 1500 31 By balance c/f 1500

Total 1500 Total 1500

S. Hood A/C

Date Particulars (£) Date Particulars (£)

Jan-19 Jan-19

24 To Cash A/C 3600 1 By balance b/d 12150

31 To Balance c/f 10000 2

By Purchases

A/C 1450

Total 13600 Total 13600

D. Main A/C

Date Particulars (£) Date Particulars (£)

Jan-19 Jan-19

7

Jan-19 Jan-19

31 To Balance c/f 450 1 By Bank A/C 450

Total 450 Total 450

Motor Expenses A/C

Date Particulars (£) Date Particulars (£)

Jan-19 Jan-19

4 To Cash A/C 470 31 By balance c/f 470

Total 470 Total 470

Drawings A/C

Date Particulars (£) Date Particulars (£)

Jan-19 Jan-19

7 To Cash A/C 1500 31 By balance c/f 1500

Total 1500 Total 1500

S. Hood A/C

Date Particulars (£) Date Particulars (£)

Jan-19 Jan-19

24 To Cash A/C 3600 1 By balance b/d 12150

31 To Balance c/f 10000 2

By Purchases

A/C 1450

Total 13600 Total 13600

D. Main A/C

Date Particulars (£) Date Particulars (£)

Jan-19 Jan-19

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

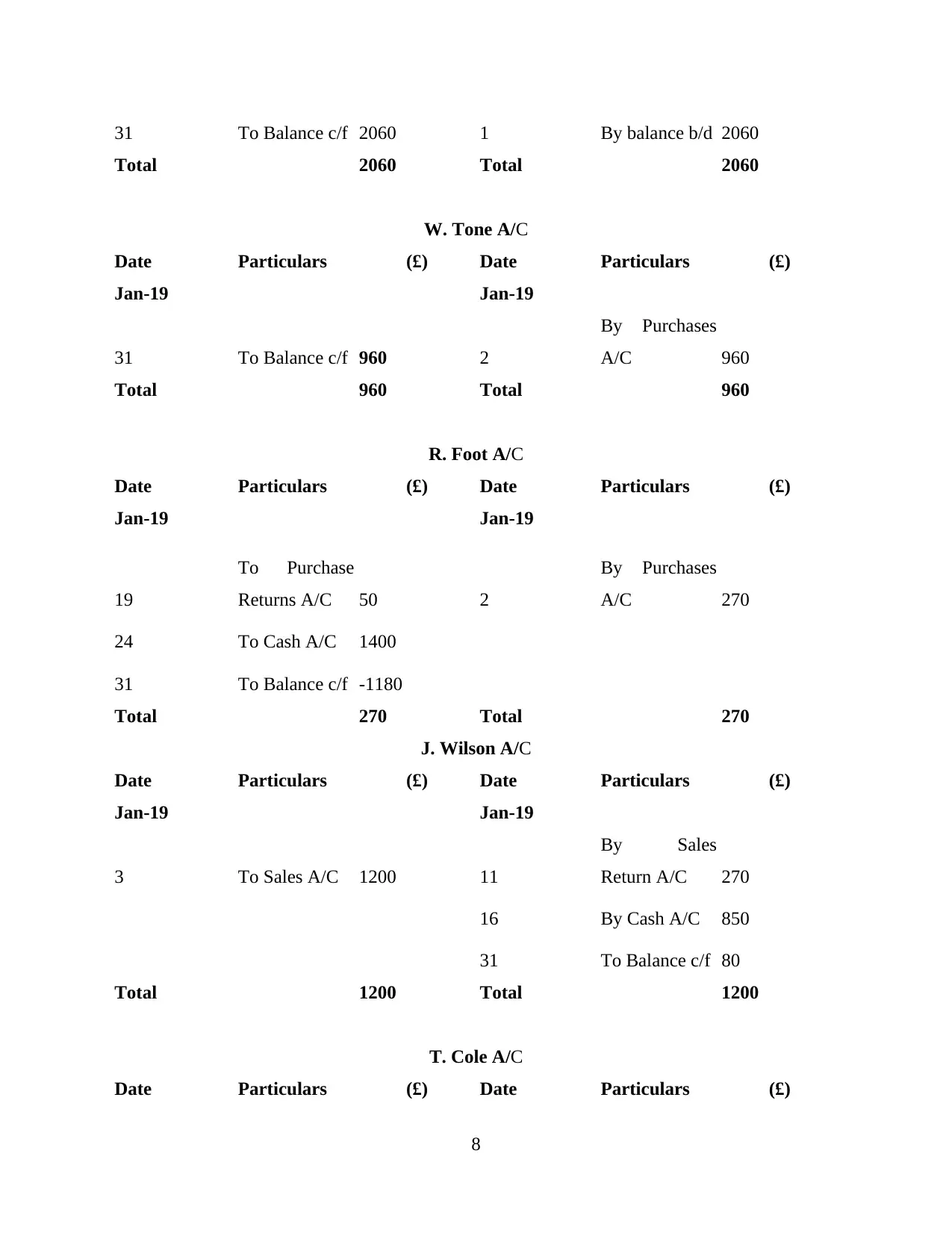

31 To Balance c/f 2060 1 By balance b/d 2060

Total 2060 Total 2060

W. Tone A/C

Date Particulars (£) Date Particulars (£)

Jan-19 Jan-19

31 To Balance c/f 960 2

By Purchases

A/C 960

Total 960 Total 960

R. Foot A/C

Date Particulars (£) Date Particulars (£)

Jan-19 Jan-19

19

To Purchase

Returns A/C 50 2

By Purchases

A/C 270

24 To Cash A/C 1400

31 To Balance c/f -1180

Total 270 Total 270

J. Wilson A/C

Date Particulars (£) Date Particulars (£)

Jan-19 Jan-19

3 To Sales A/C 1200 11

By Sales

Return A/C 270

16 By Cash A/C 850

31 To Balance c/f 80

Total 1200 Total 1200

T. Cole A/C

Date Particulars (£) Date Particulars (£)

8

Total 2060 Total 2060

W. Tone A/C

Date Particulars (£) Date Particulars (£)

Jan-19 Jan-19

31 To Balance c/f 960 2

By Purchases

A/C 960

Total 960 Total 960

R. Foot A/C

Date Particulars (£) Date Particulars (£)

Jan-19 Jan-19

19

To Purchase

Returns A/C 50 2

By Purchases

A/C 270

24 To Cash A/C 1400

31 To Balance c/f -1180

Total 270 Total 270

J. Wilson A/C

Date Particulars (£) Date Particulars (£)

Jan-19 Jan-19

3 To Sales A/C 1200 11

By Sales

Return A/C 270

16 By Cash A/C 850

31 To Balance c/f 80

Total 1200 Total 1200

T. Cole A/C

Date Particulars (£) Date Particulars (£)

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

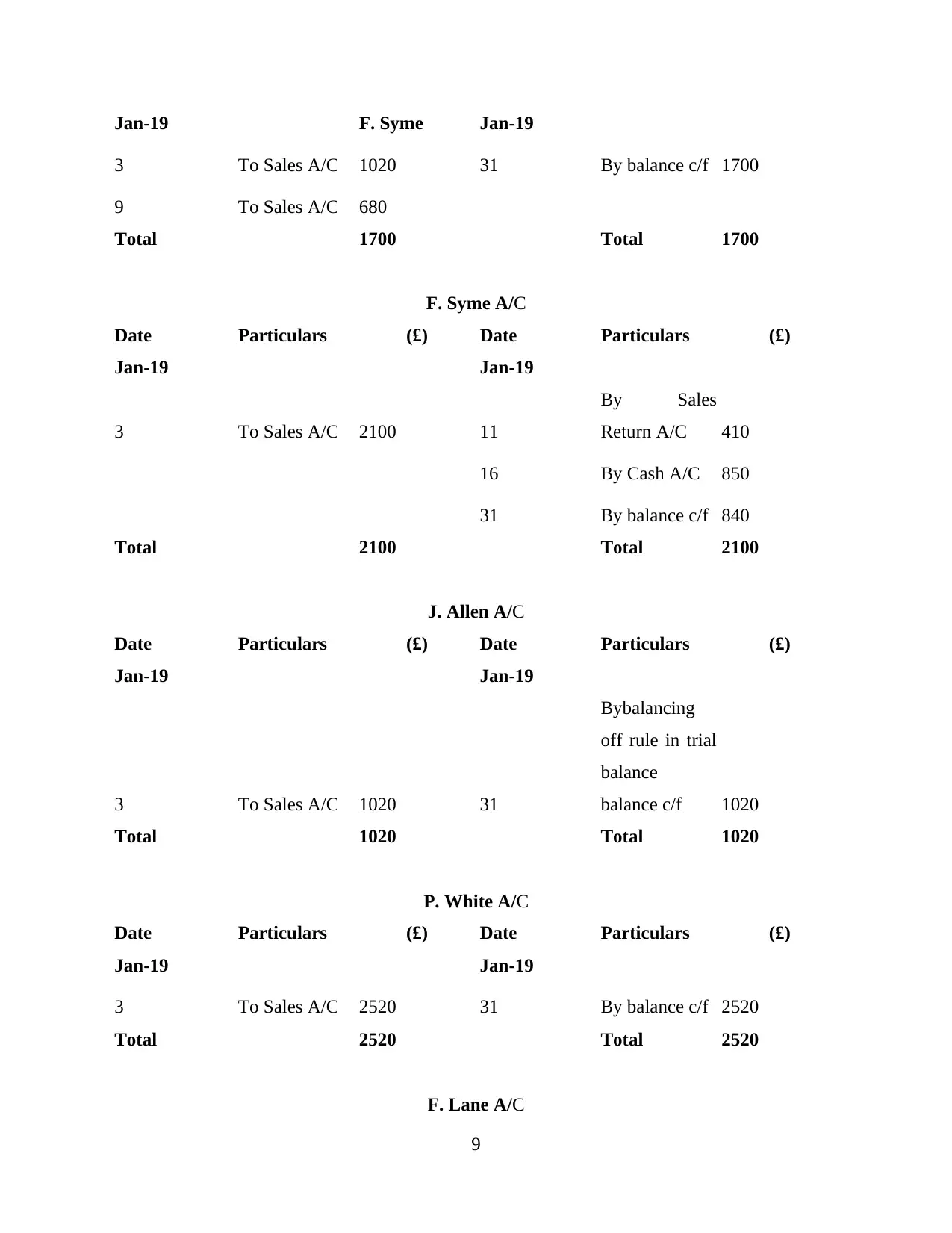

Jan-19 F. Syme Jan-19

3 To Sales A/C 1020 31 By balance c/f 1700

9 To Sales A/C 680

Total 1700 Total 1700

F. Syme A/C

Date Particulars (£) Date Particulars (£)

Jan-19 Jan-19

3 To Sales A/C 2100 11

By Sales

Return A/C 410

16 By Cash A/C 850

31 By balance c/f 840

Total 2100 Total 2100

J. Allen A/C

Date Particulars (£) Date Particulars (£)

Jan-19 Jan-19

3 To Sales A/C 1020 31

Bybalancing

off rule in trial

balance

balance c/f 1020

Total 1020 Total 1020

P. White A/C

Date Particulars (£) Date Particulars (£)

Jan-19 Jan-19

3 To Sales A/C 2520 31 By balance c/f 2520

Total 2520 Total 2520

F. Lane A/C

9

3 To Sales A/C 1020 31 By balance c/f 1700

9 To Sales A/C 680

Total 1700 Total 1700

F. Syme A/C

Date Particulars (£) Date Particulars (£)

Jan-19 Jan-19

3 To Sales A/C 2100 11

By Sales

Return A/C 410

16 By Cash A/C 850

31 By balance c/f 840

Total 2100 Total 2100

J. Allen A/C

Date Particulars (£) Date Particulars (£)

Jan-19 Jan-19

3 To Sales A/C 1020 31

Bybalancing

off rule in trial

balance

balance c/f 1020

Total 1020 Total 1020

P. White A/C

Date Particulars (£) Date Particulars (£)

Jan-19 Jan-19

3 To Sales A/C 2520 31 By balance c/f 2520

Total 2520 Total 2520

F. Lane A/C

9

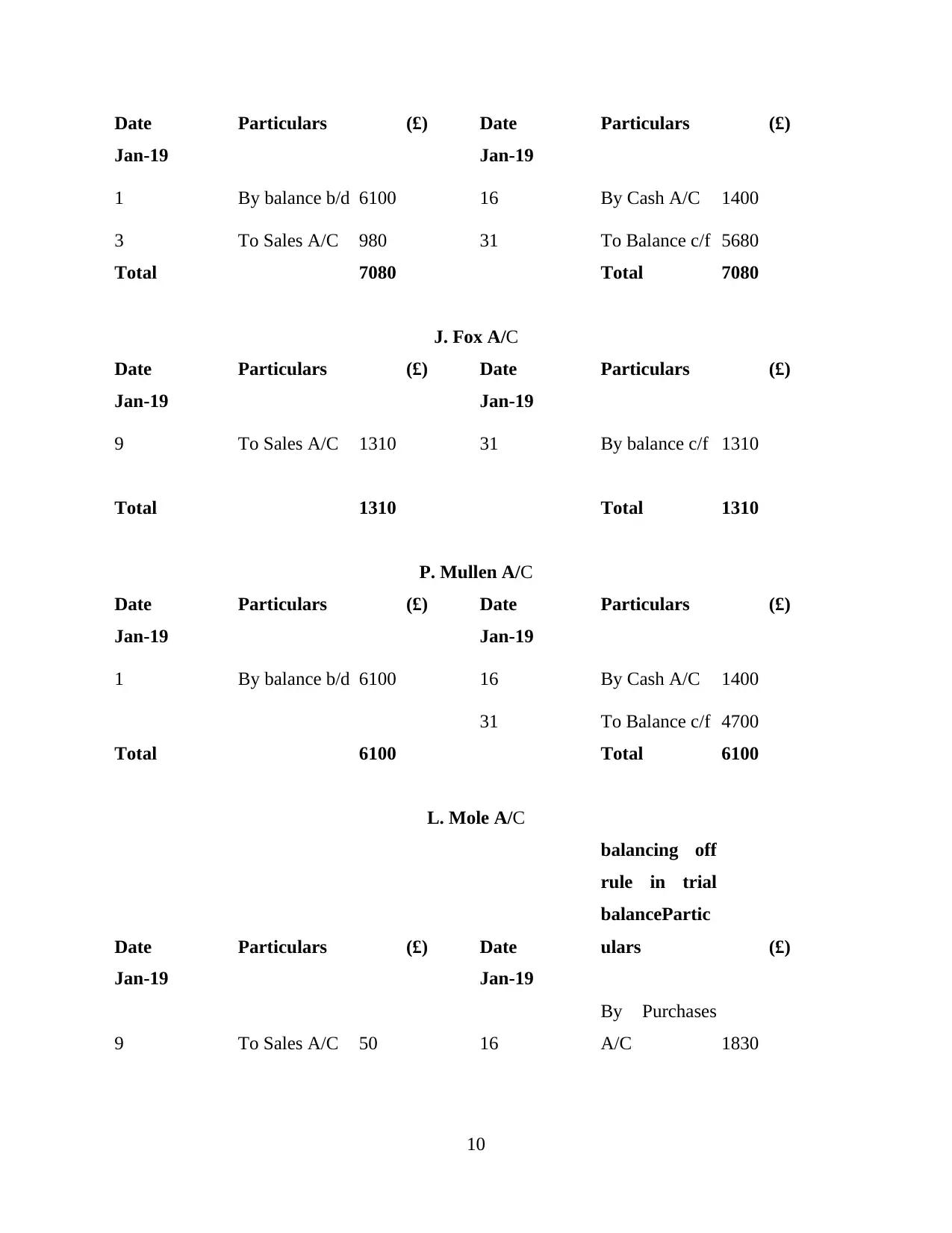

Date Particulars (£) Date Particulars (£)

Jan-19 Jan-19

1 By balance b/d 6100 16 By Cash A/C 1400

3 To Sales A/C 980 31 To Balance c/f 5680

Total 7080 Total 7080

J. Fox A/C

Date Particulars (£) Date Particulars (£)

Jan-19 Jan-19

9 To Sales A/C 1310 31 By balance c/f 1310

Total 1310 Total 1310

P. Mullen A/C

Date Particulars (£) Date Particulars (£)

Jan-19 Jan-19

1 By balance b/d 6100 16 By Cash A/C 1400

31 To Balance c/f 4700

Total 6100 Total 6100

L. Mole A/C

Date Particulars (£) Date

balancing off

rule in trial

balancePartic

ulars (£)

Jan-19 Jan-19

9 To Sales A/C 50 16

By Purchases

A/C 1830

10

Jan-19 Jan-19

1 By balance b/d 6100 16 By Cash A/C 1400

3 To Sales A/C 980 31 To Balance c/f 5680

Total 7080 Total 7080

J. Fox A/C

Date Particulars (£) Date Particulars (£)

Jan-19 Jan-19

9 To Sales A/C 1310 31 By balance c/f 1310

Total 1310 Total 1310

P. Mullen A/C

Date Particulars (£) Date Particulars (£)

Jan-19 Jan-19

1 By balance b/d 6100 16 By Cash A/C 1400

31 To Balance c/f 4700

Total 6100 Total 6100

L. Mole A/C

Date Particulars (£) Date

balancing off

rule in trial

balancePartic

ulars (£)

Jan-19 Jan-19

9 To Sales A/C 50 16

By Purchases

A/C 1830

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 21

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.