Management Accounting Report: Budgetary Control and Costing

VerifiedAdded on 2020/10/22

|10

|3301

|79

Report

AI Summary

This report delves into the core concepts of management accounting, exploring topics such as marginal and absorption costing, and their implications on profit calculations. It examines the advantages and disadvantages of various planning tools used in budgetary control, including fixed, flexible, incremental, and zero-based budgets. The report also highlights the application of variance analysis in assessing financial performance. Furthermore, it analyzes how organizations adapt their management accounting systems to address financial challenges and evaluates the effectiveness of management accounting in achieving sustainable success. The report provides a comprehensive overview of these key areas, offering valuable insights into financial management practices.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

P4 Advantages and disadvantages of diverse kind of planning tools used in budgetary control2

P5 Analyse how organisations are adapting management accounting system to respond

financial problems..................................................................................................................6

M4 Evaluation of effectiveness of management accounting in terms of leading organisation to

sustainable success.................................................................................................................7

CONCLUSION................................................................................................................................7

REFERENCES................................................................................................................................8

INTRODUCTION...........................................................................................................................1

P4 Advantages and disadvantages of diverse kind of planning tools used in budgetary control2

P5 Analyse how organisations are adapting management accounting system to respond

financial problems..................................................................................................................6

M4 Evaluation of effectiveness of management accounting in terms of leading organisation to

sustainable success.................................................................................................................7

CONCLUSION................................................................................................................................7

REFERENCES................................................................................................................................8

INTRODUCTION

Management of information related to financial and non-financial transactions, events

and assumptions are considered as management accounting. It is a part of strategic planning and

decision making process (Abdelmoneim Mohamed and Jones, 2014). This report focuses upon

marginal costing, absorption costing, closing stock and profit figures. It mainly focuses upon

essentialness of various type of planning tools used in budgetary control process. Use of

management accounting in resolving the monetary conflicts and emphasising the sustainability

of business is evaluated in this report.

Marginal cost

Evaluation of change in total cost by producing extra unit is considered as marginal cost.

A cost that helps to determine the cost of incremental production change due to increase by

producing each extra unit. Marginal costing considered very effective while calculating break

even analysis and variability of cost in various sections. Marginal costing helps in dividing the

changes in cost or incremental cost among the increased units. Material cost, labour cost and

direct expenses cost are the main elements in marginal costing.

Absorption cost

It is one of the essential method of compiling the cost that remain associated with the

process of production units. This costing method mainly help in valuation of inventories with in

organisational context (Absorption costing, 2018). The additional cost is analysed subject to

analyse the marginal cost proportionate to production. Ingestion costing implies that the

majority of the assembling costs are consumed by the units delivered. As it were, the expense of

a completed unit in stock will incorporate direct materials, coordinate work, and both variable

and fixed assembling overhead. Fixed overheads cost is considered as absorbed rate while

calculating cost.

Why are the closing stock and profit figures different?

There are two elective procedures for the valuation of stock as marginal costing and

absorption costing. Simply factor costs are charged to movement, however the fixed cost is

restricted from it and are charged to profit and mishap speak to the period. In marginal costing,

minor cost is controlled by bifurcating fixed cost and variable cost. It it reckoned that profit

form marginal and absorption costing are counted different. There are some assumptions made in

terms of calculating profitability form absorption and marginal costing. Main reason of getting

1

Management of information related to financial and non-financial transactions, events

and assumptions are considered as management accounting. It is a part of strategic planning and

decision making process (Abdelmoneim Mohamed and Jones, 2014). This report focuses upon

marginal costing, absorption costing, closing stock and profit figures. It mainly focuses upon

essentialness of various type of planning tools used in budgetary control process. Use of

management accounting in resolving the monetary conflicts and emphasising the sustainability

of business is evaluated in this report.

Marginal cost

Evaluation of change in total cost by producing extra unit is considered as marginal cost.

A cost that helps to determine the cost of incremental production change due to increase by

producing each extra unit. Marginal costing considered very effective while calculating break

even analysis and variability of cost in various sections. Marginal costing helps in dividing the

changes in cost or incremental cost among the increased units. Material cost, labour cost and

direct expenses cost are the main elements in marginal costing.

Absorption cost

It is one of the essential method of compiling the cost that remain associated with the

process of production units. This costing method mainly help in valuation of inventories with in

organisational context (Absorption costing, 2018). The additional cost is analysed subject to

analyse the marginal cost proportionate to production. Ingestion costing implies that the

majority of the assembling costs are consumed by the units delivered. As it were, the expense of

a completed unit in stock will incorporate direct materials, coordinate work, and both variable

and fixed assembling overhead. Fixed overheads cost is considered as absorbed rate while

calculating cost.

Why are the closing stock and profit figures different?

There are two elective procedures for the valuation of stock as marginal costing and

absorption costing. Simply factor costs are charged to movement, however the fixed cost is

restricted from it and are charged to profit and mishap speak to the period. In marginal costing,

minor cost is controlled by bifurcating fixed cost and variable cost. It it reckoned that profit

form marginal and absorption costing are counted different. There are some assumptions made in

terms of calculating profitability form absorption and marginal costing. Main reason of getting

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

different results in terms of profitability form absorption and marginal costing changing value of

opening and closing stock. This also help in consolidating the changes with appropriate

management and approach and magnitude of opening stock. The management process of

managing the sections are analysed with absorbed rate and appropriate products.

Conversely, Absorption costing or similarly called full costing, is a costing methodology

in which all costs, paying little respect to whether fixed or variable are devoured by the total

units conveyed (Bovens,Goodin and Schillemans, 2014). It is mainly used for declaring

purposes, i.e. for cash related and evaluate uncovering. There are various who say irrelevant

costing is better, while others lean toward digestion costing. Thusly, one should know the

refinement between minor costing and maintenance costing to reach at goals, about which one to

be supported over the other. There are various differences considered essential for mentioning

the points for better change and development.

Methods

Uniform costing: this is one of the form of costing system that helps in analysing the

principles and standard accounting practise. This helps in analysing the accounting procedures

for better aspects.

Process costing: This costing method is based upon different manufacturing and

production sections. There is a individual manufacturing cost is evaluated of individual

processes. It helps in managing the process costing for better change and development.

Purpose of marginal cost

Main purpose of marginal costing is to evaluate the per unit’s production cost incurred

during the year. Marginal costing helps in correlating the cost information and helps in better

strategic planning and strategic planning process.

P4 Advantages and disadvantages of diverse kind of planning tools used in budgetary control

Budgetary control

Budgetary control alludes to how well directors use spending plans to screen and control

expenses and tasks in a given accounting period. It is considered as a spending plan of dispersing

assets by qualitative (Nielsen, Mitchell and Nørreklit, 2015). It seems to be one of the effective

system of management control under which actual profit and spending are taken into account

with proper planned income and expenses. Thus, company can looks in case specific planning

are being followed and those plans are required to be modified in respect to attain maximum

2

opening and closing stock. This also help in consolidating the changes with appropriate

management and approach and magnitude of opening stock. The management process of

managing the sections are analysed with absorbed rate and appropriate products.

Conversely, Absorption costing or similarly called full costing, is a costing methodology

in which all costs, paying little respect to whether fixed or variable are devoured by the total

units conveyed (Bovens,Goodin and Schillemans, 2014). It is mainly used for declaring

purposes, i.e. for cash related and evaluate uncovering. There are various who say irrelevant

costing is better, while others lean toward digestion costing. Thusly, one should know the

refinement between minor costing and maintenance costing to reach at goals, about which one to

be supported over the other. There are various differences considered essential for mentioning

the points for better change and development.

Methods

Uniform costing: this is one of the form of costing system that helps in analysing the

principles and standard accounting practise. This helps in analysing the accounting procedures

for better aspects.

Process costing: This costing method is based upon different manufacturing and

production sections. There is a individual manufacturing cost is evaluated of individual

processes. It helps in managing the process costing for better change and development.

Purpose of marginal cost

Main purpose of marginal costing is to evaluate the per unit’s production cost incurred

during the year. Marginal costing helps in correlating the cost information and helps in better

strategic planning and strategic planning process.

P4 Advantages and disadvantages of diverse kind of planning tools used in budgetary control

Budgetary control

Budgetary control alludes to how well directors use spending plans to screen and control

expenses and tasks in a given accounting period. It is considered as a spending plan of dispersing

assets by qualitative (Nielsen, Mitchell and Nørreklit, 2015). It seems to be one of the effective

system of management control under which actual profit and spending are taken into account

with proper planned income and expenses. Thus, company can looks in case specific planning

are being followed and those plans are required to be modified in respect to attain maximum

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

profit. Budgetary control would be balancing of techniques that can provide overall stability for

an organisation in respect to real profit and utility stick intently to their money related planning.

Subsequently budgets are prepared for the purpose of estimating the future cost and risk

those are going to be incurred within an organisation. It has been seen that budgets are not only a

means of control but would also assist the manager in performing other operations within an

organization. This would help in overall planning or pointing deviation from the estimated

results. Various type of budgets is used in organisational context such as;

Fixed budget

Fixed budget is a type of budget that does not change due to change in sales volume and

variable expenses. A fixed budget plan is a spending that does not change or flex when

arrangements or some other activity additions or decreases. It is in like manner suggested as a

static spending plan. most associations experience extensive assortments from their ordinary

activity levels over the period fused by a money related arrangement, the totals in the financial

recompense are presumably going to isolate from genuine results (Lavia López and Hiebl, 2014).

Associations that are static, execute a comparable sort of trades can exceptionally benefit by a

settled spending plan.

Advantages of fixed budget: A fixed budget plan enables a business to gauge both here

and now and long haul spending plans. The fixed budgeting plan dispenses a set measure of cash

towards fundamentals, for example, overhead expenses. Any cash left over toward the month's

end or some other period you survey settled spending plan is viewebudgetary control definitiond

as benefit. It

Disadvantage of fixed budget: There are type of adjustments are analysed in term of

managing the breached equipment’s. Fixed spending makes benefit estimation less demanding,

since you apportion a similar measure of cash towards necessities all the time. The fluctuation

rate remains same in both the perspectives in terms of managing the sections with different cost

aspects that reduce the credibility of business. Benefit estimation turns out to be more

troublesome if the financial backing always varies (Messner, 2016).

Flexible budget

A flexible budget is one of the valuable budget for an organisation that keep on changing

with volume or activities performed during the period of time. It is more sophisticated and

crucial other than static budget. It is considered as flex because variable rate per unit of units

3

an organisation in respect to real profit and utility stick intently to their money related planning.

Subsequently budgets are prepared for the purpose of estimating the future cost and risk

those are going to be incurred within an organisation. It has been seen that budgets are not only a

means of control but would also assist the manager in performing other operations within an

organization. This would help in overall planning or pointing deviation from the estimated

results. Various type of budgets is used in organisational context such as;

Fixed budget

Fixed budget is a type of budget that does not change due to change in sales volume and

variable expenses. A fixed budget plan is a spending that does not change or flex when

arrangements or some other activity additions or decreases. It is in like manner suggested as a

static spending plan. most associations experience extensive assortments from their ordinary

activity levels over the period fused by a money related arrangement, the totals in the financial

recompense are presumably going to isolate from genuine results (Lavia López and Hiebl, 2014).

Associations that are static, execute a comparable sort of trades can exceptionally benefit by a

settled spending plan.

Advantages of fixed budget: A fixed budget plan enables a business to gauge both here

and now and long haul spending plans. The fixed budgeting plan dispenses a set measure of cash

towards fundamentals, for example, overhead expenses. Any cash left over toward the month's

end or some other period you survey settled spending plan is viewebudgetary control definitiond

as benefit. It

Disadvantage of fixed budget: There are type of adjustments are analysed in term of

managing the breached equipment’s. Fixed spending makes benefit estimation less demanding,

since you apportion a similar measure of cash towards necessities all the time. The fluctuation

rate remains same in both the perspectives in terms of managing the sections with different cost

aspects that reduce the credibility of business. Benefit estimation turns out to be more

troublesome if the financial backing always varies (Messner, 2016).

Flexible budget

A flexible budget is one of the valuable budget for an organisation that keep on changing

with volume or activities performed during the period of time. It is more sophisticated and

crucial other than static budget. It is considered as flex because variable rate per unit of units

3

instead of one fixed value. Thus, it is more useful for increasing the efficiency of the business for

longer period of time (Siverbo, 2014). At the end of the day, an adaptable spending utilizes

overall value for the production that tend to increase overall profitability for an organisation and

make plan in such a way that always assist in generating maximum return in near future. It is

designed to change in relation to the level of activity actually attained. A flexible budget is one

that takes account of a range of possible volumes. It is sometimes referred to as a multi-volume

budget.

Advantages of flexible budget: Flexible spending plan empower an association to

anticipate its execution and pay levels at a given scope of offers levels and movement levels.

Flexible budgeting plans empower more exact evaluation of administrative and authoritative

performance. It very well may be seen the effect of changes in deals and generation levels on

income, costs and at last salary.

Disadvantage of flexible budget: Accurate is the important element to address the

requirements of forming flexible budget that may lead organisation towards serious concerns.

Flexible spending demonstrates differences between spending plans yet it doesn't intricate the

detail or the principle reasons of the fluctuations which could be secured.

Incremental budgets

An incremental budget plan is a financial plan arranged utilizing a past period's financial

plan or genuine execution as a premise with incremental sums included for the new spending

time frame. This kind of spending stays straightforward in typical course of business (Strauss,

Kristandl and Quinn, 2015). However, it isn't by and large prescribed by most experts because of

its irregularity. One of the most serious issues with this kind of planning is that it regularly drives

offices to spend more cash.

Advantages of incremental budget: Managers can work their specialities on a reliable

premise. The financial backing is steady and change is slow. The framework is moderately easy

to work and straightforward. It easy to see the growth more vastly as the production gets increase

during the time. Co-appointment between spending plans is simpler to accomplish.

Disadvantage of incremental budget: Assumes exercises and strategies for working

will proceed similarly. No motivating force for growing new thoughts. The financial backing

may wind up outdated and never again identify with the dimension of action or sort of work

being completed. No motivating forces to lessen costs. Urges spending up to the financial plan so

4

longer period of time (Siverbo, 2014). At the end of the day, an adaptable spending utilizes

overall value for the production that tend to increase overall profitability for an organisation and

make plan in such a way that always assist in generating maximum return in near future. It is

designed to change in relation to the level of activity actually attained. A flexible budget is one

that takes account of a range of possible volumes. It is sometimes referred to as a multi-volume

budget.

Advantages of flexible budget: Flexible spending plan empower an association to

anticipate its execution and pay levels at a given scope of offers levels and movement levels.

Flexible budgeting plans empower more exact evaluation of administrative and authoritative

performance. It very well may be seen the effect of changes in deals and generation levels on

income, costs and at last salary.

Disadvantage of flexible budget: Accurate is the important element to address the

requirements of forming flexible budget that may lead organisation towards serious concerns.

Flexible spending demonstrates differences between spending plans yet it doesn't intricate the

detail or the principle reasons of the fluctuations which could be secured.

Incremental budgets

An incremental budget plan is a financial plan arranged utilizing a past period's financial

plan or genuine execution as a premise with incremental sums included for the new spending

time frame. This kind of spending stays straightforward in typical course of business (Strauss,

Kristandl and Quinn, 2015). However, it isn't by and large prescribed by most experts because of

its irregularity. One of the most serious issues with this kind of planning is that it regularly drives

offices to spend more cash.

Advantages of incremental budget: Managers can work their specialities on a reliable

premise. The financial backing is steady and change is slow. The framework is moderately easy

to work and straightforward. It easy to see the growth more vastly as the production gets increase

during the time. Co-appointment between spending plans is simpler to accomplish.

Disadvantage of incremental budget: Assumes exercises and strategies for working

will proceed similarly. No motivating force for growing new thoughts. The financial backing

may wind up outdated and never again identify with the dimension of action or sort of work

being completed. No motivating forces to lessen costs. Urges spending up to the financial plan so

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

the monetary allowance is kept up one year from now. The need for assets may have changed

since the financial plans were set initially.

Zero based budget

This is one of the type of budget that mainly starts with zero base. Budget basically not

remain related with previous budgets and analytical aspects (Tappura and et. al., 2015). This

budget helps in consolidating the cost aspects with zero based budgeting and plans for combining

the business expenses at starting level. This strategy mainly helps in dividing the changes in

various form such as business goals, prioritization of funds and analysing the business process.

Advantages of zero based budget: It involves re-evaluating every line item of cash

flow statement and justifying all the expenditure that is to be incurred by the department. ZBB

permits top-level vital objectives to be actualized into the planning procedure by binds them to

particular practical regions of the organisation. where expenses can be first gathered and

afterwards estimated against past outcomes and current desires.

Disadvantage of zero based budget: Explaining every line item and every cost is a

difficult task and requires training the managers. The budgeting process may sometime become

rigid and thus an organisation cannot be able to react to those unforeseen opportunities or threats.

Zero-based budgeting is a very time-intensive exercise for a company or a government-funded

entity to do every year as against incremental budgeting which is a far easier method.

Variance analysis

Variance analysis is the investigation of deviations of real conduct versus estimated or

arranged conduct in planning or administration accounting (Zaleha Abdul Rasid, Ruhana Isa

and Khairuzzaman Wan Ismail, 2014). Difference investigation is generally connected with a

producer's item costs. It investigation projects and elements to distinguish the reasons for the

contrasts between a manufacturer's. It is a method that helps to analyse the differences between

the actual cost and standard cost and try to correlate the difference in respect of saving

unconditional cost.

Advantages of variance analysis

It is one of the essential tool that helps in analysing the differences between the projected

and expected figures. It is a type of annual budget exercise that helps in assessing the

responsibilities and liabilities for better change and development.

Disadvantage of variance analysis

5

since the financial plans were set initially.

Zero based budget

This is one of the type of budget that mainly starts with zero base. Budget basically not

remain related with previous budgets and analytical aspects (Tappura and et. al., 2015). This

budget helps in consolidating the cost aspects with zero based budgeting and plans for combining

the business expenses at starting level. This strategy mainly helps in dividing the changes in

various form such as business goals, prioritization of funds and analysing the business process.

Advantages of zero based budget: It involves re-evaluating every line item of cash

flow statement and justifying all the expenditure that is to be incurred by the department. ZBB

permits top-level vital objectives to be actualized into the planning procedure by binds them to

particular practical regions of the organisation. where expenses can be first gathered and

afterwards estimated against past outcomes and current desires.

Disadvantage of zero based budget: Explaining every line item and every cost is a

difficult task and requires training the managers. The budgeting process may sometime become

rigid and thus an organisation cannot be able to react to those unforeseen opportunities or threats.

Zero-based budgeting is a very time-intensive exercise for a company or a government-funded

entity to do every year as against incremental budgeting which is a far easier method.

Variance analysis

Variance analysis is the investigation of deviations of real conduct versus estimated or

arranged conduct in planning or administration accounting (Zaleha Abdul Rasid, Ruhana Isa

and Khairuzzaman Wan Ismail, 2014). Difference investigation is generally connected with a

producer's item costs. It investigation projects and elements to distinguish the reasons for the

contrasts between a manufacturer's. It is a method that helps to analyse the differences between

the actual cost and standard cost and try to correlate the difference in respect of saving

unconditional cost.

Advantages of variance analysis

It is one of the essential tool that helps in analysing the differences between the projected

and expected figures. It is a type of annual budget exercise that helps in assessing the

responsibilities and liabilities for better change and development.

Disadvantage of variance analysis

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

There is lack of certainty found while calculating the variances between the actual and

standard results. It only presents the variations and difference but do not presents the main reason

of differences between standard and actual figures.

P5 Analyse how organisations are adapting management accounting system to respond financial

problems

There are type of financial issues remain associated with management and operation in

organisations. These issues may be related with management of cash, incorporating the changes

with in different organisational aspects, determining the adequate financial sources or

management of investment planning. Legal challenges, policy change, changes in economic rate,

expansion plans and cash flow management are the main financial challenges faced by

organisations. These challenges can be identified by following ways such as;

Financial governance

Financial governance incorporates how organizations track money related exchanges,

oversee execution and consistence, activities, control information and revelations. Financial

administration suggests the manner in which an organization gathers, oversees, screens and

controls budgetary data. Financial Governance assists CFOs in their tasks to assemble controls

along the nearby cycle, accomplish chance balanced knowledge with brought together money

related detailing and consistence examination, and upgrade the convenience and nature of

monetary announcing.

Benchmarking

Benchmarking is the standard method for contrasting one item with another. With

innovation specifically, it remains against contending items is frequently the best way to get a

target proportion of value. In order to analyses the financial position of the company it is crucial

to determine to other firms in respects to deal with an organization competitiveness. This seems

to be a well organise procedures for making comparison of a firms overall performance certain

criteria and business processes to get competitive advantages over other.

KPI: It stand for Key performance indicators that are mainly used to success and failure

of the processes that are used by the organizations. It also helps to evaluate that company is

going to attain profits or face losses. It is mainly used by Tesco and Apple to resolve the problem

of sudden expenses that may occur due to improper planning. It guides business entities to

6

standard results. It only presents the variations and difference but do not presents the main reason

of differences between standard and actual figures.

P5 Analyse how organisations are adapting management accounting system to respond financial

problems

There are type of financial issues remain associated with management and operation in

organisations. These issues may be related with management of cash, incorporating the changes

with in different organisational aspects, determining the adequate financial sources or

management of investment planning. Legal challenges, policy change, changes in economic rate,

expansion plans and cash flow management are the main financial challenges faced by

organisations. These challenges can be identified by following ways such as;

Financial governance

Financial governance incorporates how organizations track money related exchanges,

oversee execution and consistence, activities, control information and revelations. Financial

administration suggests the manner in which an organization gathers, oversees, screens and

controls budgetary data. Financial Governance assists CFOs in their tasks to assemble controls

along the nearby cycle, accomplish chance balanced knowledge with brought together money

related detailing and consistence examination, and upgrade the convenience and nature of

monetary announcing.

Benchmarking

Benchmarking is the standard method for contrasting one item with another. With

innovation specifically, it remains against contending items is frequently the best way to get a

target proportion of value. In order to analyses the financial position of the company it is crucial

to determine to other firms in respects to deal with an organization competitiveness. This seems

to be a well organise procedures for making comparison of a firms overall performance certain

criteria and business processes to get competitive advantages over other.

KPI: It stand for Key performance indicators that are mainly used to success and failure

of the processes that are used by the organizations. It also helps to evaluate that company is

going to attain profits or face losses. It is mainly used by Tesco and Apple to resolve the problem

of sudden expenses that may occur due to improper planning. It guides business entities to

6

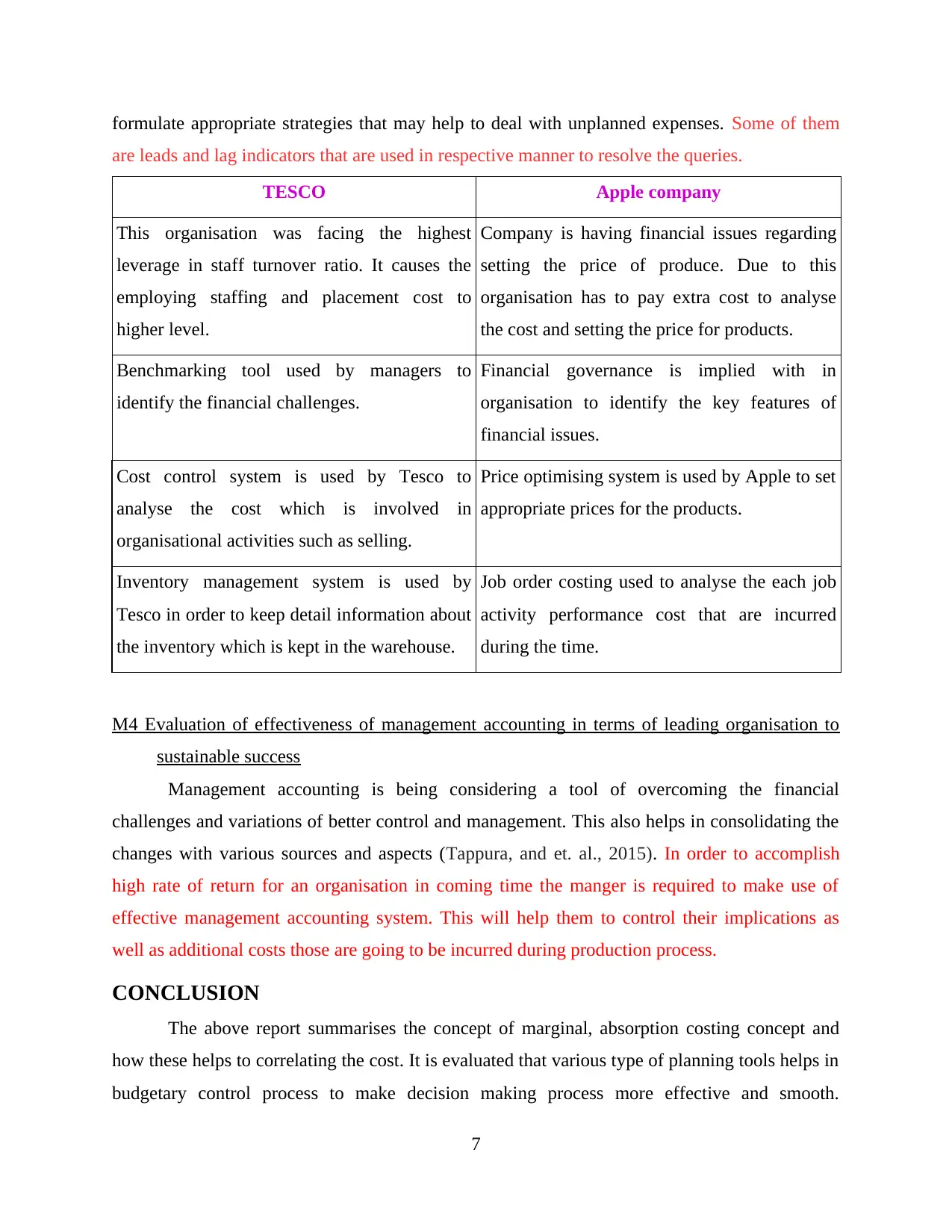

formulate appropriate strategies that may help to deal with unplanned expenses. Some of them

are leads and lag indicators that are used in respective manner to resolve the queries.

TESCO Apple company

This organisation was facing the highest

leverage in staff turnover ratio. It causes the

employing staffing and placement cost to

higher level.

Company is having financial issues regarding

setting the price of produce. Due to this

organisation has to pay extra cost to analyse

the cost and setting the price for products.

Benchmarking tool used by managers to

identify the financial challenges.

Financial governance is implied with in

organisation to identify the key features of

financial issues.

Cost control system is used by Tesco to

analyse the cost which is involved in

organisational activities such as selling.

Price optimising system is used by Apple to set

appropriate prices for the products.

Inventory management system is used by

Tesco in order to keep detail information about

the inventory which is kept in the warehouse.

Job order costing used to analyse the each job

activity performance cost that are incurred

during the time.

M4 Evaluation of effectiveness of management accounting in terms of leading organisation to

sustainable success

Management accounting is being considering a tool of overcoming the financial

challenges and variations of better control and management. This also helps in consolidating the

changes with various sources and aspects (Tappura, and et. al., 2015). In order to accomplish

high rate of return for an organisation in coming time the manger is required to make use of

effective management accounting system. This will help them to control their implications as

well as additional costs those are going to be incurred during production process.

CONCLUSION

The above report summarises the concept of marginal, absorption costing concept and

how these helps to correlating the cost. It is evaluated that various type of planning tools helps in

budgetary control process to make decision making process more effective and smooth.

7

are leads and lag indicators that are used in respective manner to resolve the queries.

TESCO Apple company

This organisation was facing the highest

leverage in staff turnover ratio. It causes the

employing staffing and placement cost to

higher level.

Company is having financial issues regarding

setting the price of produce. Due to this

organisation has to pay extra cost to analyse

the cost and setting the price for products.

Benchmarking tool used by managers to

identify the financial challenges.

Financial governance is implied with in

organisation to identify the key features of

financial issues.

Cost control system is used by Tesco to

analyse the cost which is involved in

organisational activities such as selling.

Price optimising system is used by Apple to set

appropriate prices for the products.

Inventory management system is used by

Tesco in order to keep detail information about

the inventory which is kept in the warehouse.

Job order costing used to analyse the each job

activity performance cost that are incurred

during the time.

M4 Evaluation of effectiveness of management accounting in terms of leading organisation to

sustainable success

Management accounting is being considering a tool of overcoming the financial

challenges and variations of better control and management. This also helps in consolidating the

changes with various sources and aspects (Tappura, and et. al., 2015). In order to accomplish

high rate of return for an organisation in coming time the manger is required to make use of

effective management accounting system. This will help them to control their implications as

well as additional costs those are going to be incurred during production process.

CONCLUSION

The above report summarises the concept of marginal, absorption costing concept and

how these helps to correlating the cost. It is evaluated that various type of planning tools helps in

budgetary control process to make decision making process more effective and smooth.

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Effectiveness of management accounting system in terms of resolving financial issues are also

correlated with in organisational context.

8

correlated with in organisational context.

8

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.