Financial Analysis and Decision Making: A Comprehensive Report

VerifiedAdded on 2023/06/10

|12

|2571

|90

Report

AI Summary

This report presents a comprehensive financial analysis and decision-making process. It begins with a break-even analysis, calculating break-even points in units and revenue, and the margin of safety for two alternative scenarios (A and B), evaluating profitability under different production levels. The report then delves into investment appraisal techniques, including payback period and net present value (NPV), comparing two project options and assessing their financial viability. The internal rate of return (IRR) is also discussed, along with recommendations for investment choices, emphasizing the importance of financial and non-financial factors in decision-making. Finally, the report examines the limitations of break-even analysis and the strengths and weaknesses of Return on Capital Employed (ROCE), and the importance of cost of capital, and non-financial measures for business efficiency.

Financial Analysis and

Decision Making

Decision Making

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

Question 1........................................................................................................................................3

a) Calculate..................................................................................................................................3

b) Profit made under following....................................................................................................4

c)..................................................................................................................................................5

d) Recommendation.....................................................................................................................6

e) Limitations of Break – even analysis......................................................................................6

Question 2........................................................................................................................................7

a)..................................................................................................................................................7

b)..................................................................................................................................................7

c)..................................................................................................................................................9

d)..................................................................................................................................................9

e)................................................................................................................................................10

Question 3......................................................................................................................................10

a)................................................................................................................................................10

b)................................................................................................................................................10

c)................................................................................................................................................11

d)................................................................................................................................................11

REFERENCES..............................................................................................................................12

Question 1........................................................................................................................................3

a) Calculate..................................................................................................................................3

b) Profit made under following....................................................................................................4

c)..................................................................................................................................................5

d) Recommendation.....................................................................................................................6

e) Limitations of Break – even analysis......................................................................................6

Question 2........................................................................................................................................7

a)..................................................................................................................................................7

b)..................................................................................................................................................7

c)..................................................................................................................................................9

d)..................................................................................................................................................9

e)................................................................................................................................................10

Question 3......................................................................................................................................10

a)................................................................................................................................................10

b)................................................................................................................................................10

c)................................................................................................................................................11

d)................................................................................................................................................11

REFERENCES..............................................................................................................................12

Question 1.

a) Calculate

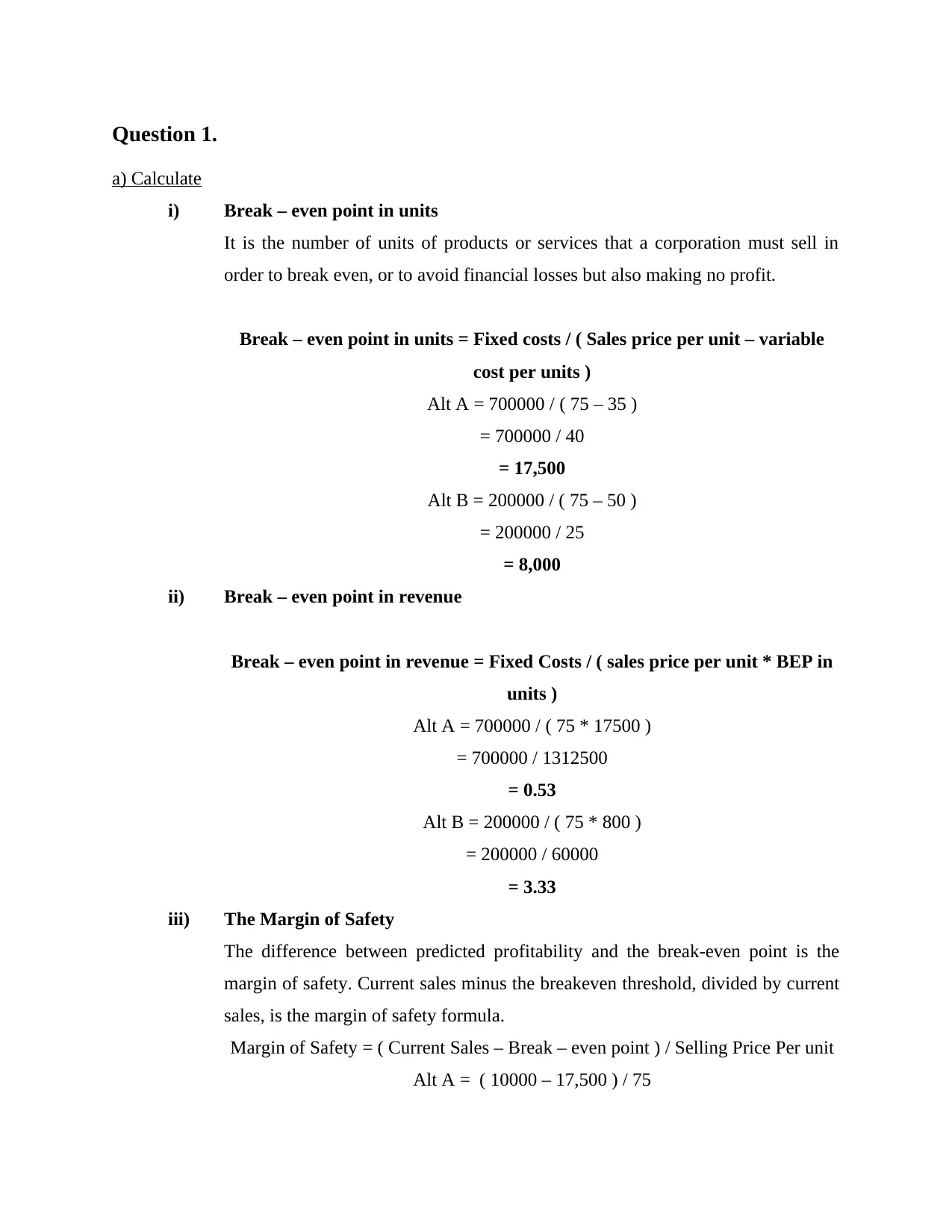

i) Break – even point in units

It is the number of units of products or services that a corporation must sell in

order to break even, or to avoid financial losses but also making no profit.

Break – even point in units = Fixed costs / ( Sales price per unit – variable

cost per units )

Alt A = 700000 / ( 75 – 35 )

= 700000 / 40

= 17,500

Alt B = 200000 / ( 75 – 50 )

= 200000 / 25

= 8,000

ii) Break – even point in revenue

Break – even point in revenue = Fixed Costs / ( sales price per unit * BEP in

units )

Alt A = 700000 / ( 75 * 17500 )

= 700000 / 1312500

= 0.53

Alt B = 200000 / ( 75 * 800 )

= 200000 / 60000

= 3.33

iii) The Margin of Safety

The difference between predicted profitability and the break-even point is the

margin of safety. Current sales minus the breakeven threshold, divided by current

sales, is the margin of safety formula.

Margin of Safety = ( Current Sales – Break – even point ) / Selling Price Per unit

Alt A = ( 10000 – 17,500 ) / 75

a) Calculate

i) Break – even point in units

It is the number of units of products or services that a corporation must sell in

order to break even, or to avoid financial losses but also making no profit.

Break – even point in units = Fixed costs / ( Sales price per unit – variable

cost per units )

Alt A = 700000 / ( 75 – 35 )

= 700000 / 40

= 17,500

Alt B = 200000 / ( 75 – 50 )

= 200000 / 25

= 8,000

ii) Break – even point in revenue

Break – even point in revenue = Fixed Costs / ( sales price per unit * BEP in

units )

Alt A = 700000 / ( 75 * 17500 )

= 700000 / 1312500

= 0.53

Alt B = 200000 / ( 75 * 800 )

= 200000 / 60000

= 3.33

iii) The Margin of Safety

The difference between predicted profitability and the break-even point is the

margin of safety. Current sales minus the breakeven threshold, divided by current

sales, is the margin of safety formula.

Margin of Safety = ( Current Sales – Break – even point ) / Selling Price Per unit

Alt A = ( 10000 – 17,500 ) / 75

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

= - 7,500 / 75

= - 100

Alt B = ( 10000 – 8000 ) / 75

= 2000 / 75

= 26.66

b) Profit made under following

i) 10000 units are produced

Alt A

Sales – 10000 * 75 = 750000

Direct Material – 10000 * 15 = 150000

Direct Labour – 10000 * 15 = 150000

Variable costs – 10000 * 5 = 50000

Fixed Costs = 700000

Total Costs = 1050000

Profit = 750000 – 1050000 = - 300000 or Loss of 300000

Alt B

Sales – 10000 * 75 = 750000

Direct Material – 10000 * 10 = 100000

Direct Labour – 10000 * 20 = 200000

Variable costs – 10000 * 20 = 200000

Fixed Costs = 200000

Total Costs = 700000

Profit = 750000 – 700000 = 50000

ii) 8000 units are produced

Alt A

Sales – 8000 * 75 = 600000

Direct Material – 8000 * 15 = 120000

Direct Labour – 8000 * 15 = 120000

Variable costs – 8000 * 5 = 40000

= - 100

Alt B = ( 10000 – 8000 ) / 75

= 2000 / 75

= 26.66

b) Profit made under following

i) 10000 units are produced

Alt A

Sales – 10000 * 75 = 750000

Direct Material – 10000 * 15 = 150000

Direct Labour – 10000 * 15 = 150000

Variable costs – 10000 * 5 = 50000

Fixed Costs = 700000

Total Costs = 1050000

Profit = 750000 – 1050000 = - 300000 or Loss of 300000

Alt B

Sales – 10000 * 75 = 750000

Direct Material – 10000 * 10 = 100000

Direct Labour – 10000 * 20 = 200000

Variable costs – 10000 * 20 = 200000

Fixed Costs = 200000

Total Costs = 700000

Profit = 750000 – 700000 = 50000

ii) 8000 units are produced

Alt A

Sales – 8000 * 75 = 600000

Direct Material – 8000 * 15 = 120000

Direct Labour – 8000 * 15 = 120000

Variable costs – 8000 * 5 = 40000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

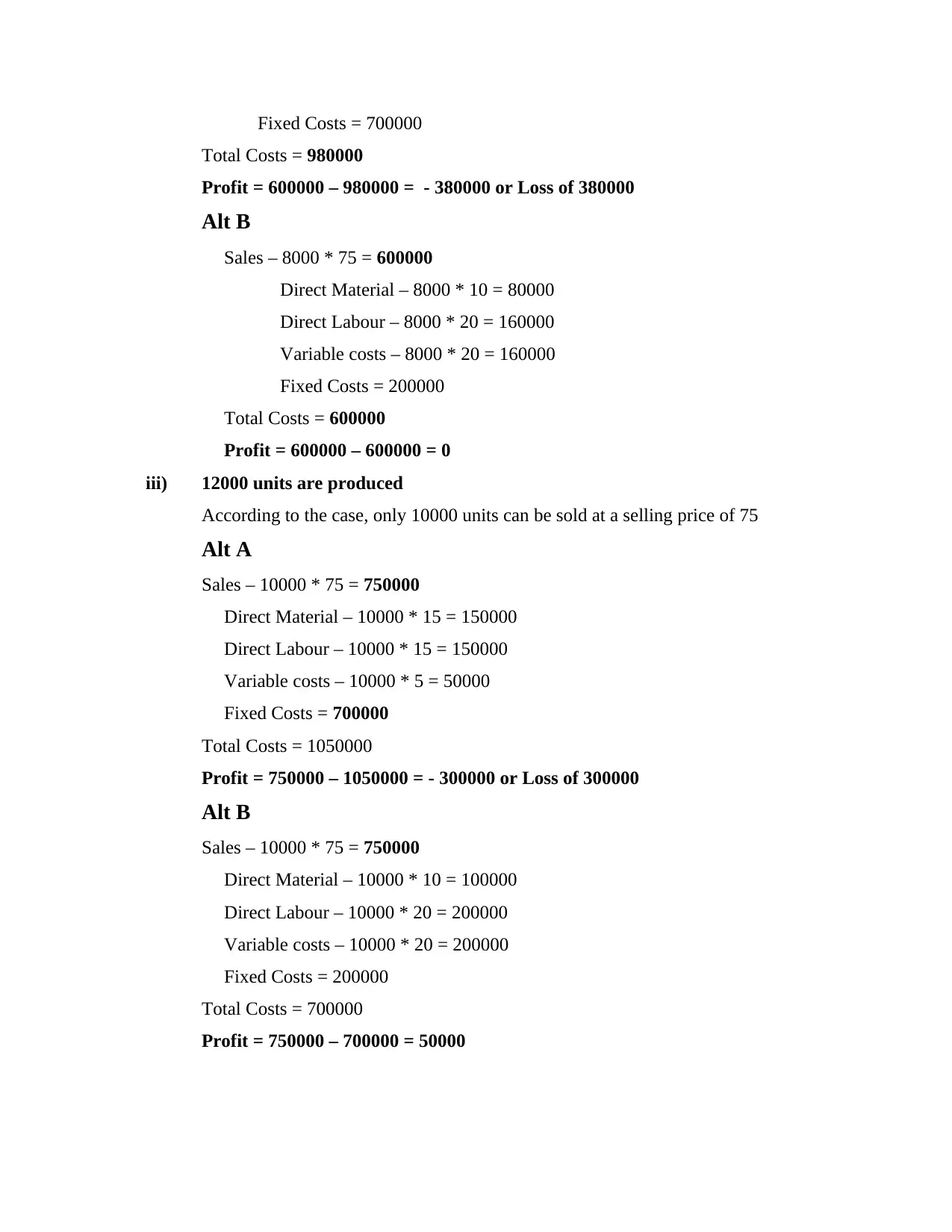

Fixed Costs = 700000

Total Costs = 980000

Profit = 600000 – 980000 = - 380000 or Loss of 380000

Alt B

Sales – 8000 * 75 = 600000

Direct Material – 8000 * 10 = 80000

Direct Labour – 8000 * 20 = 160000

Variable costs – 8000 * 20 = 160000

Fixed Costs = 200000

Total Costs = 600000

Profit = 600000 – 600000 = 0

iii) 12000 units are produced

According to the case, only 10000 units can be sold at a selling price of 75

Alt A

Sales – 10000 * 75 = 750000

Direct Material – 10000 * 15 = 150000

Direct Labour – 10000 * 15 = 150000

Variable costs – 10000 * 5 = 50000

Fixed Costs = 700000

Total Costs = 1050000

Profit = 750000 – 1050000 = - 300000 or Loss of 300000

Alt B

Sales – 10000 * 75 = 750000

Direct Material – 10000 * 10 = 100000

Direct Labour – 10000 * 20 = 200000

Variable costs – 10000 * 20 = 200000

Fixed Costs = 200000

Total Costs = 700000

Profit = 750000 – 700000 = 50000

Total Costs = 980000

Profit = 600000 – 980000 = - 380000 or Loss of 380000

Alt B

Sales – 8000 * 75 = 600000

Direct Material – 8000 * 10 = 80000

Direct Labour – 8000 * 20 = 160000

Variable costs – 8000 * 20 = 160000

Fixed Costs = 200000

Total Costs = 600000

Profit = 600000 – 600000 = 0

iii) 12000 units are produced

According to the case, only 10000 units can be sold at a selling price of 75

Alt A

Sales – 10000 * 75 = 750000

Direct Material – 10000 * 15 = 150000

Direct Labour – 10000 * 15 = 150000

Variable costs – 10000 * 5 = 50000

Fixed Costs = 700000

Total Costs = 1050000

Profit = 750000 – 1050000 = - 300000 or Loss of 300000

Alt B

Sales – 10000 * 75 = 750000

Direct Material – 10000 * 10 = 100000

Direct Labour – 10000 * 20 = 200000

Variable costs – 10000 * 20 = 200000

Fixed Costs = 200000

Total Costs = 700000

Profit = 750000 – 700000 = 50000

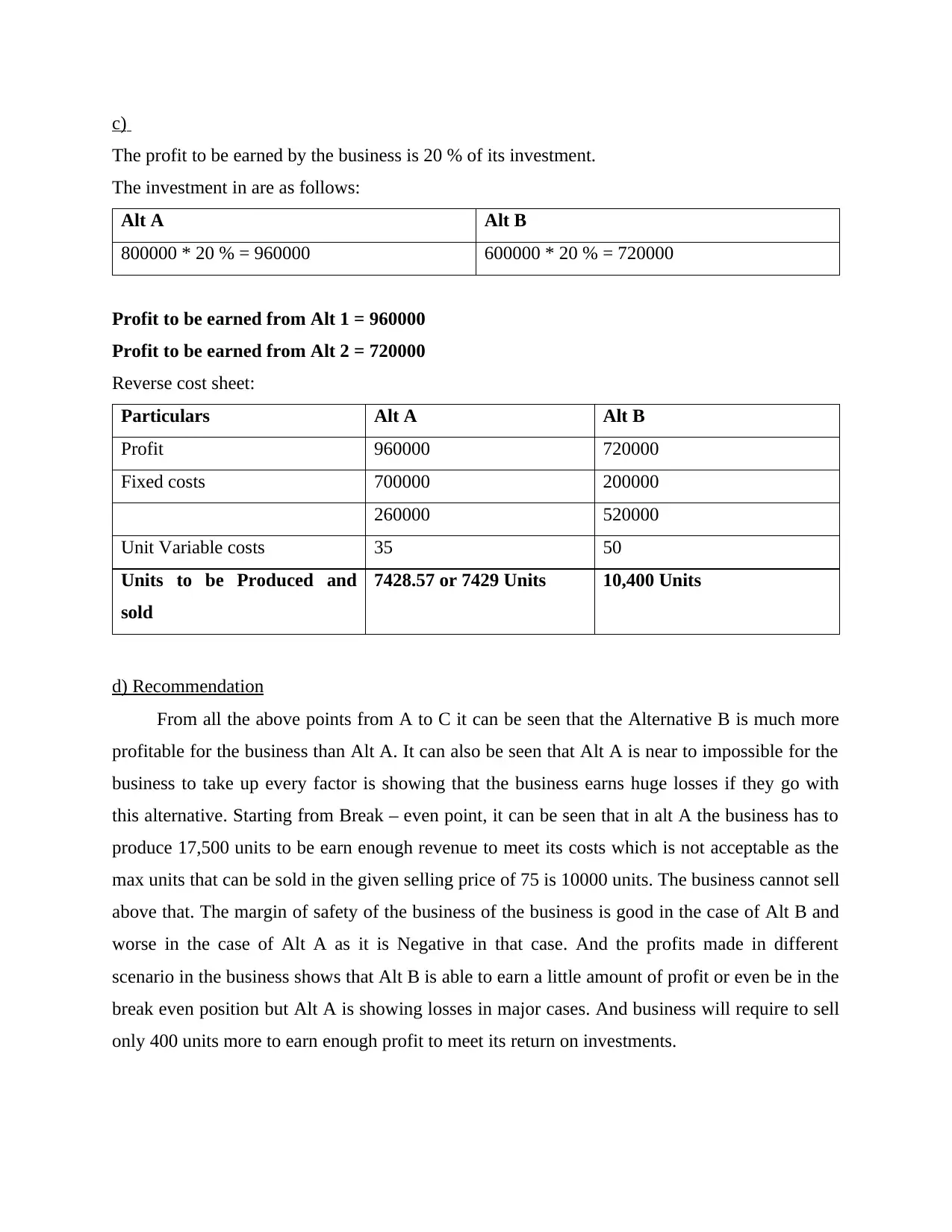

c)

The profit to be earned by the business is 20 % of its investment.

The investment in are as follows:

Alt A Alt B

800000 * 20 % = 960000 600000 * 20 % = 720000

Profit to be earned from Alt 1 = 960000

Profit to be earned from Alt 2 = 720000

Reverse cost sheet:

Particulars Alt A Alt B

Profit 960000 720000

Fixed costs 700000 200000

260000 520000

Unit Variable costs 35 50

Units to be Produced and

sold

7428.57 or 7429 Units 10,400 Units

d) Recommendation

From all the above points from A to C it can be seen that the Alternative B is much more

profitable for the business than Alt A. It can also be seen that Alt A is near to impossible for the

business to take up every factor is showing that the business earns huge losses if they go with

this alternative. Starting from Break – even point, it can be seen that in alt A the business has to

produce 17,500 units to be earn enough revenue to meet its costs which is not acceptable as the

max units that can be sold in the given selling price of 75 is 10000 units. The business cannot sell

above that. The margin of safety of the business of the business is good in the case of Alt B and

worse in the case of Alt A as it is Negative in that case. And the profits made in different

scenario in the business shows that Alt B is able to earn a little amount of profit or even be in the

break even position but Alt A is showing losses in major cases. And business will require to sell

only 400 units more to earn enough profit to meet its return on investments.

The profit to be earned by the business is 20 % of its investment.

The investment in are as follows:

Alt A Alt B

800000 * 20 % = 960000 600000 * 20 % = 720000

Profit to be earned from Alt 1 = 960000

Profit to be earned from Alt 2 = 720000

Reverse cost sheet:

Particulars Alt A Alt B

Profit 960000 720000

Fixed costs 700000 200000

260000 520000

Unit Variable costs 35 50

Units to be Produced and

sold

7428.57 or 7429 Units 10,400 Units

d) Recommendation

From all the above points from A to C it can be seen that the Alternative B is much more

profitable for the business than Alt A. It can also be seen that Alt A is near to impossible for the

business to take up every factor is showing that the business earns huge losses if they go with

this alternative. Starting from Break – even point, it can be seen that in alt A the business has to

produce 17,500 units to be earn enough revenue to meet its costs which is not acceptable as the

max units that can be sold in the given selling price of 75 is 10000 units. The business cannot sell

above that. The margin of safety of the business of the business is good in the case of Alt B and

worse in the case of Alt A as it is Negative in that case. And the profits made in different

scenario in the business shows that Alt B is able to earn a little amount of profit or even be in the

break even position but Alt A is showing losses in major cases. And business will require to sell

only 400 units more to earn enough profit to meet its return on investments.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

e) Limitations of Break – even analysis

The production in a given time may not be the only driver of costs in that period.

Maintenance costs, for example, might be the outcome of previous output or a preparation for

future output. As a result, it may be difficult to connect them to a certain time period.

In a break-even analysis, it's extremely challenging to account for selling expenses. Because

variations in selling costs are a cause, not an effect, of changes in output and sales, this is the

case. The cost-revenue-volume connection is assumed to be linear in break-even analysis. This is

only feasible across a limited range of output.

Question 2.

a)

The amount of £ 6000 which has been incurred by Tom in its investment for conducting

the feasibility study is not a relevant cost. It will be termed as the sunk cost in the business.

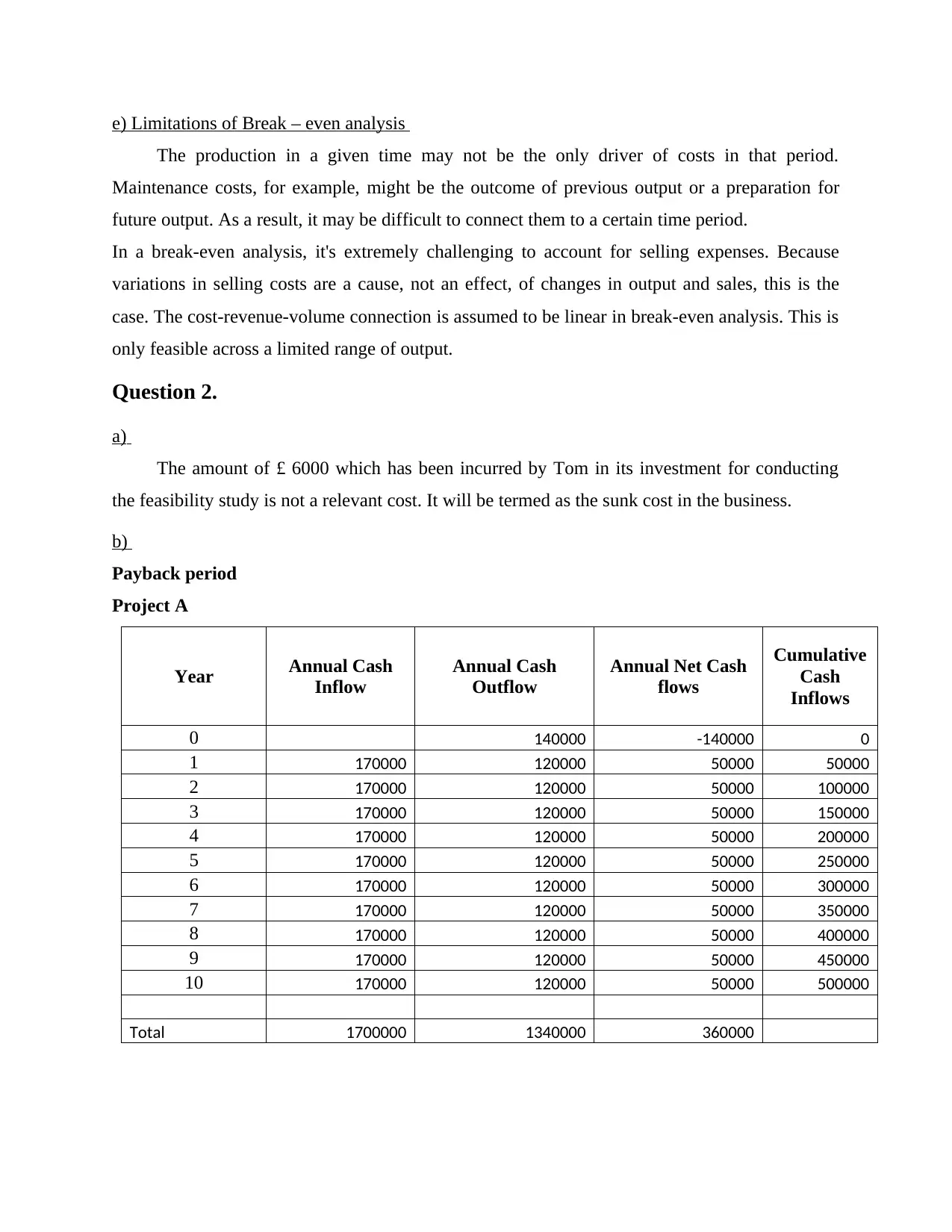

b)

Payback period

Project A

Year Annual Cash

Inflow

Annual Cash

Outflow

Annual Net Cash

flows

Cumulative

Cash

Inflows

0 140000 -140000 0

1 170000 120000 50000 50000

2 170000 120000 50000 100000

3 170000 120000 50000 150000

4 170000 120000 50000 200000

5 170000 120000 50000 250000

6 170000 120000 50000 300000

7 170000 120000 50000 350000

8 170000 120000 50000 400000

9 170000 120000 50000 450000

10 170000 120000 50000 500000

Total 1700000 1340000 360000

The production in a given time may not be the only driver of costs in that period.

Maintenance costs, for example, might be the outcome of previous output or a preparation for

future output. As a result, it may be difficult to connect them to a certain time period.

In a break-even analysis, it's extremely challenging to account for selling expenses. Because

variations in selling costs are a cause, not an effect, of changes in output and sales, this is the

case. The cost-revenue-volume connection is assumed to be linear in break-even analysis. This is

only feasible across a limited range of output.

Question 2.

a)

The amount of £ 6000 which has been incurred by Tom in its investment for conducting

the feasibility study is not a relevant cost. It will be termed as the sunk cost in the business.

b)

Payback period

Project A

Year Annual Cash

Inflow

Annual Cash

Outflow

Annual Net Cash

flows

Cumulative

Cash

Inflows

0 140000 -140000 0

1 170000 120000 50000 50000

2 170000 120000 50000 100000

3 170000 120000 50000 150000

4 170000 120000 50000 200000

5 170000 120000 50000 250000

6 170000 120000 50000 300000

7 170000 120000 50000 350000

8 170000 120000 50000 400000

9 170000 120000 50000 450000

10 170000 120000 50000 500000

Total 1700000 1340000 360000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

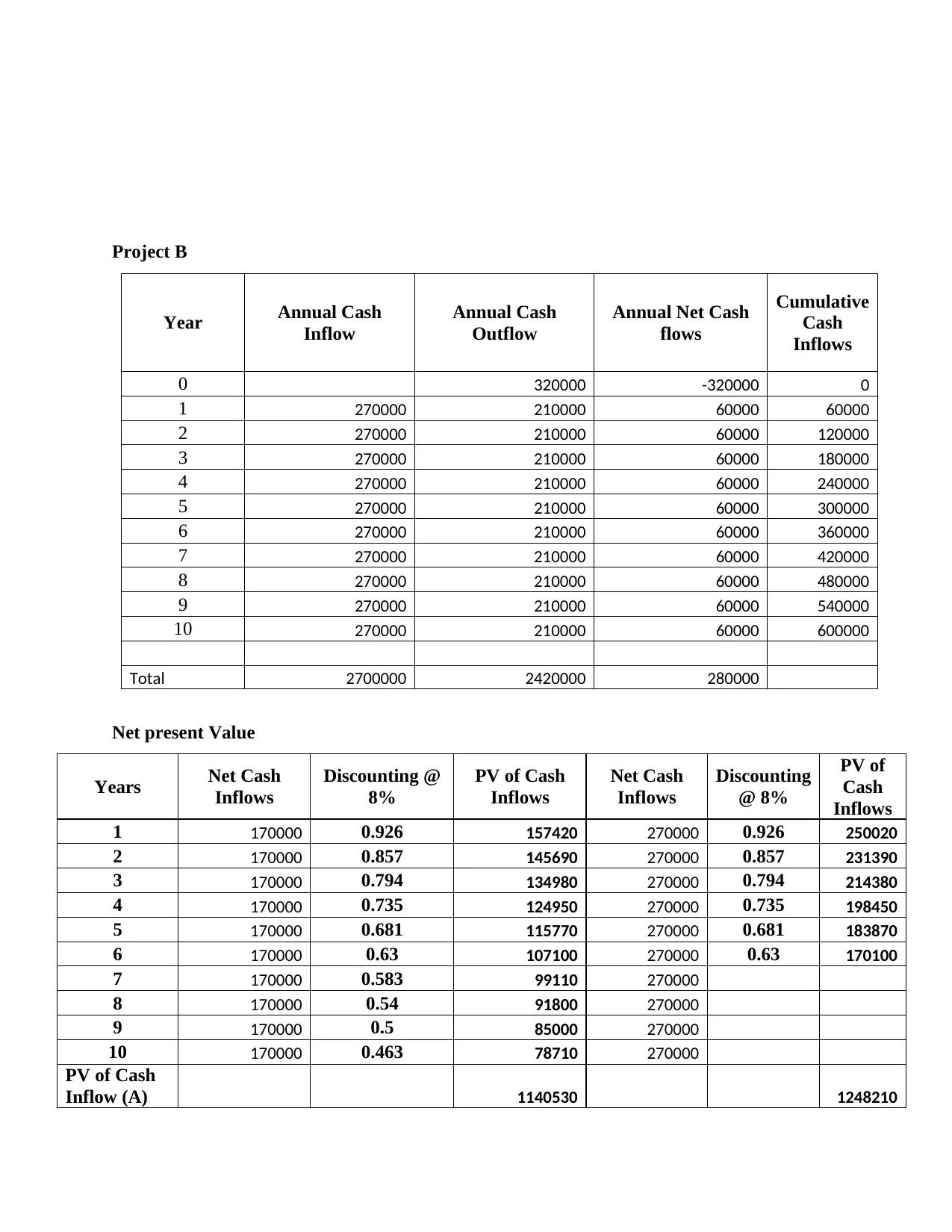

Project B

Year Annual Cash

Inflow

Annual Cash

Outflow

Annual Net Cash

flows

Cumulative

Cash

Inflows

0 320000 -320000 0

1 270000 210000 60000 60000

2 270000 210000 60000 120000

3 270000 210000 60000 180000

4 270000 210000 60000 240000

5 270000 210000 60000 300000

6 270000 210000 60000 360000

7 270000 210000 60000 420000

8 270000 210000 60000 480000

9 270000 210000 60000 540000

10 270000 210000 60000 600000

Total 2700000 2420000 280000

Net present Value

Years Net Cash

Inflows

Discounting @

8%

PV of Cash

Inflows

Net Cash

Inflows

Discounting

@ 8%

PV of

Cash

Inflows

1 170000 0.926 157420 270000 0.926 250020

2 170000 0.857 145690 270000 0.857 231390

3 170000 0.794 134980 270000 0.794 214380

4 170000 0.735 124950 270000 0.735 198450

5 170000 0.681 115770 270000 0.681 183870

6 170000 0.63 107100 270000 0.63 170100

7 170000 0.583 99110 270000

8 170000 0.54 91800 270000

9 170000 0.5 85000 270000

10 170000 0.463 78710 270000

PV of Cash

Inflow (A) 1140530 1248210

Year Annual Cash

Inflow

Annual Cash

Outflow

Annual Net Cash

flows

Cumulative

Cash

Inflows

0 320000 -320000 0

1 270000 210000 60000 60000

2 270000 210000 60000 120000

3 270000 210000 60000 180000

4 270000 210000 60000 240000

5 270000 210000 60000 300000

6 270000 210000 60000 360000

7 270000 210000 60000 420000

8 270000 210000 60000 480000

9 270000 210000 60000 540000

10 270000 210000 60000 600000

Total 2700000 2420000 280000

Net present Value

Years Net Cash

Inflows

Discounting @

8%

PV of Cash

Inflows

Net Cash

Inflows

Discounting

@ 8%

PV of

Cash

Inflows

1 170000 0.926 157420 270000 0.926 250020

2 170000 0.857 145690 270000 0.857 231390

3 170000 0.794 134980 270000 0.794 214380

4 170000 0.735 124950 270000 0.735 198450

5 170000 0.681 115770 270000 0.681 183870

6 170000 0.63 107100 270000 0.63 170100

7 170000 0.583 99110 270000

8 170000 0.54 91800 270000

9 170000 0.5 85000 270000

10 170000 0.463 78710 270000

PV of Cash

Inflow (A) 1140530 1248210

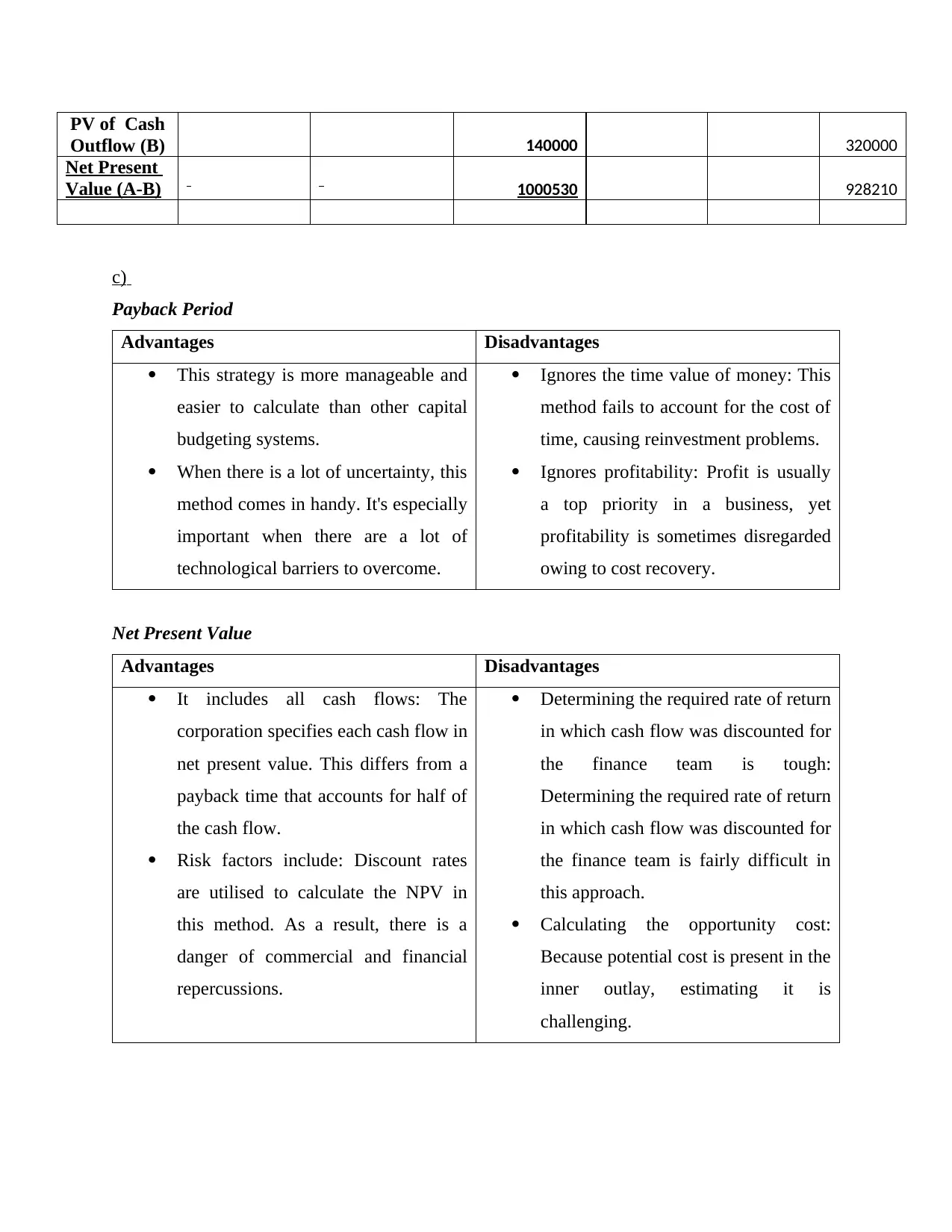

PV of Cash

Outflow (B) 140000 320000

Net Present

Value (A-B) 1000530 928210

c)

Payback Period

Advantages Disadvantages

This strategy is more manageable and

easier to calculate than other capital

budgeting systems.

When there is a lot of uncertainty, this

method comes in handy. It's especially

important when there are a lot of

technological barriers to overcome.

Ignores the time value of money: This

method fails to account for the cost of

time, causing reinvestment problems.

Ignores profitability: Profit is usually

a top priority in a business, yet

profitability is sometimes disregarded

owing to cost recovery.

Net Present Value

Advantages Disadvantages

It includes all cash flows: The

corporation specifies each cash flow in

net present value. This differs from a

payback time that accounts for half of

the cash flow.

Risk factors include: Discount rates

are utilised to calculate the NPV in

this method. As a result, there is a

danger of commercial and financial

repercussions.

Determining the required rate of return

in which cash flow was discounted for

the finance team is tough:

Determining the required rate of return

in which cash flow was discounted for

the finance team is fairly difficult in

this approach.

Calculating the opportunity cost:

Because potential cost is present in the

inner outlay, estimating it is

challenging.

Outflow (B) 140000 320000

Net Present

Value (A-B) 1000530 928210

c)

Payback Period

Advantages Disadvantages

This strategy is more manageable and

easier to calculate than other capital

budgeting systems.

When there is a lot of uncertainty, this

method comes in handy. It's especially

important when there are a lot of

technological barriers to overcome.

Ignores the time value of money: This

method fails to account for the cost of

time, causing reinvestment problems.

Ignores profitability: Profit is usually

a top priority in a business, yet

profitability is sometimes disregarded

owing to cost recovery.

Net Present Value

Advantages Disadvantages

It includes all cash flows: The

corporation specifies each cash flow in

net present value. This differs from a

payback time that accounts for half of

the cash flow.

Risk factors include: Discount rates

are utilised to calculate the NPV in

this method. As a result, there is a

danger of commercial and financial

repercussions.

Determining the required rate of return

in which cash flow was discounted for

the finance team is tough:

Determining the required rate of return

in which cash flow was discounted for

the finance team is fairly difficult in

this approach.

Calculating the opportunity cost:

Because potential cost is present in the

inner outlay, estimating it is

challenging.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

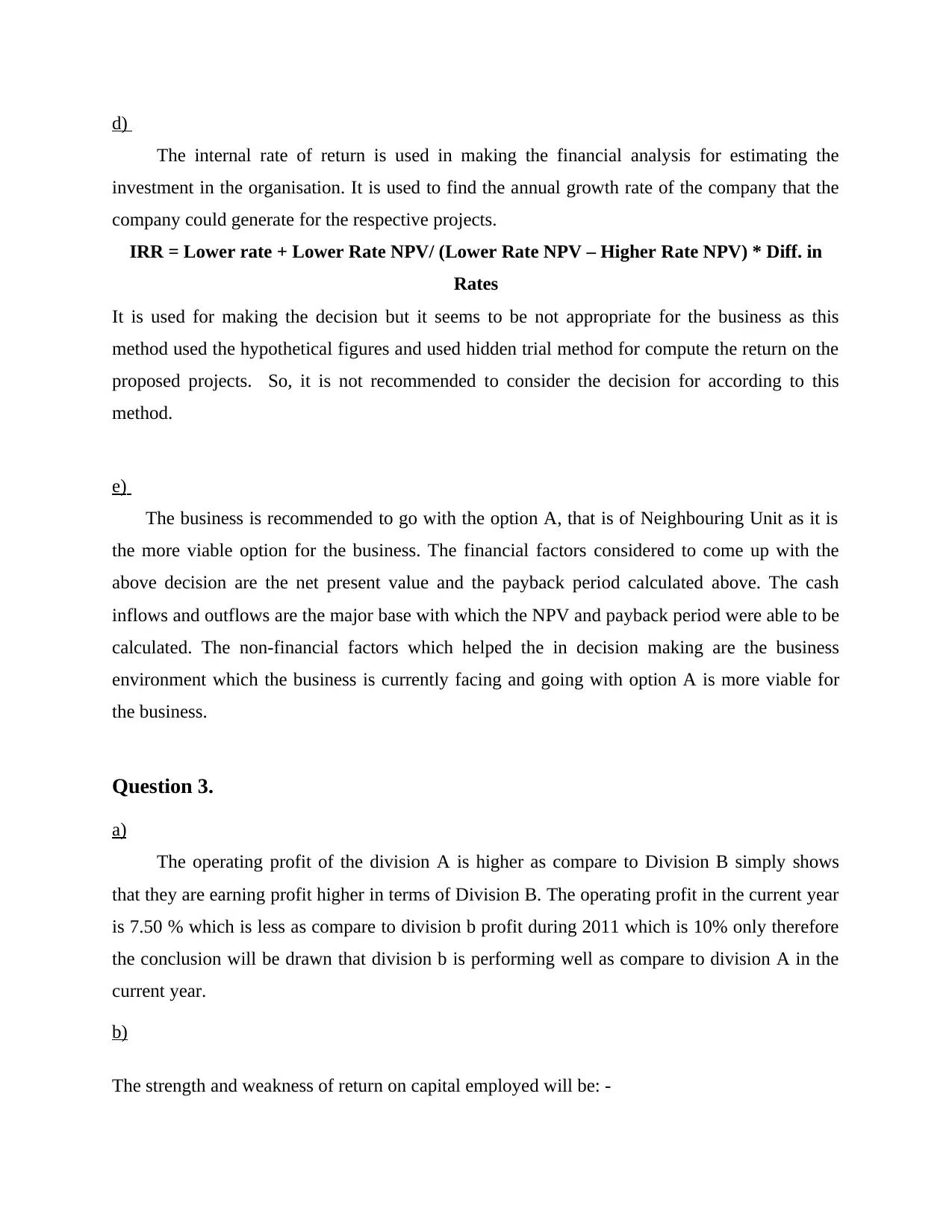

d)

The internal rate of return is used in making the financial analysis for estimating the

investment in the organisation. It is used to find the annual growth rate of the company that the

company could generate for the respective projects.

IRR = Lower rate + Lower Rate NPV/ (Lower Rate NPV – Higher Rate NPV) * Diff. in

Rates

It is used for making the decision but it seems to be not appropriate for the business as this

method used the hypothetical figures and used hidden trial method for compute the return on the

proposed projects. So, it is not recommended to consider the decision for according to this

method.

e)

The business is recommended to go with the option A, that is of Neighbouring Unit as it is

the more viable option for the business. The financial factors considered to come up with the

above decision are the net present value and the payback period calculated above. The cash

inflows and outflows are the major base with which the NPV and payback period were able to be

calculated. The non-financial factors which helped the in decision making are the business

environment which the business is currently facing and going with option A is more viable for

the business.

Question 3.

a)

The operating profit of the division A is higher as compare to Division B simply shows

that they are earning profit higher in terms of Division B. The operating profit in the current year

is 7.50 % which is less as compare to division b profit during 2011 which is 10% only therefore

the conclusion will be drawn that division b is performing well as compare to division A in the

current year.

b)

The strength and weakness of return on capital employed will be: -

The internal rate of return is used in making the financial analysis for estimating the

investment in the organisation. It is used to find the annual growth rate of the company that the

company could generate for the respective projects.

IRR = Lower rate + Lower Rate NPV/ (Lower Rate NPV – Higher Rate NPV) * Diff. in

Rates

It is used for making the decision but it seems to be not appropriate for the business as this

method used the hypothetical figures and used hidden trial method for compute the return on the

proposed projects. So, it is not recommended to consider the decision for according to this

method.

e)

The business is recommended to go with the option A, that is of Neighbouring Unit as it is

the more viable option for the business. The financial factors considered to come up with the

above decision are the net present value and the payback period calculated above. The cash

inflows and outflows are the major base with which the NPV and payback period were able to be

calculated. The non-financial factors which helped the in decision making are the business

environment which the business is currently facing and going with option A is more viable for

the business.

Question 3.

a)

The operating profit of the division A is higher as compare to Division B simply shows

that they are earning profit higher in terms of Division B. The operating profit in the current year

is 7.50 % which is less as compare to division b profit during 2011 which is 10% only therefore

the conclusion will be drawn that division b is performing well as compare to division A in the

current year.

b)

The strength and weakness of return on capital employed will be: -

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

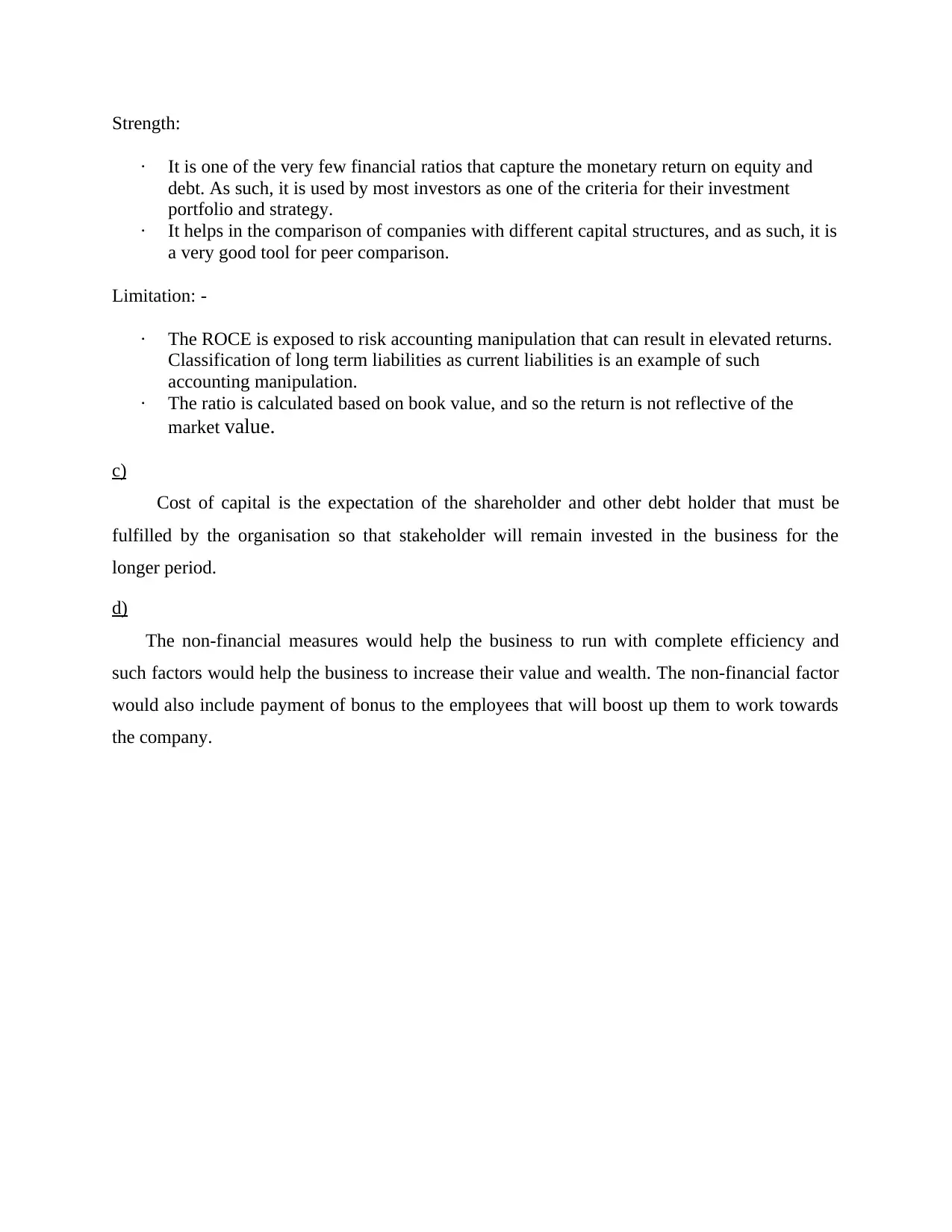

Strength:

· It is one of the very few financial ratios that capture the monetary return on equity and

debt. As such, it is used by most investors as one of the criteria for their investment

portfolio and strategy.

· It helps in the comparison of companies with different capital structures, and as such, it is

a very good tool for peer comparison.

Limitation: -

· The ROCE is exposed to risk accounting manipulation that can result in elevated returns.

Classification of long term liabilities as current liabilities is an example of such

accounting manipulation.

· The ratio is calculated based on book value, and so the return is not reflective of the

market value.

c)

Cost of capital is the expectation of the shareholder and other debt holder that must be

fulfilled by the organisation so that stakeholder will remain invested in the business for the

longer period.

d)

The non-financial measures would help the business to run with complete efficiency and

such factors would help the business to increase their value and wealth. The non-financial factor

would also include payment of bonus to the employees that will boost up them to work towards

the company.

· It is one of the very few financial ratios that capture the monetary return on equity and

debt. As such, it is used by most investors as one of the criteria for their investment

portfolio and strategy.

· It helps in the comparison of companies with different capital structures, and as such, it is

a very good tool for peer comparison.

Limitation: -

· The ROCE is exposed to risk accounting manipulation that can result in elevated returns.

Classification of long term liabilities as current liabilities is an example of such

accounting manipulation.

· The ratio is calculated based on book value, and so the return is not reflective of the

market value.

c)

Cost of capital is the expectation of the shareholder and other debt holder that must be

fulfilled by the organisation so that stakeholder will remain invested in the business for the

longer period.

d)

The non-financial measures would help the business to run with complete efficiency and

such factors would help the business to increase their value and wealth. The non-financial factor

would also include payment of bonus to the employees that will boost up them to work towards

the company.

REFERENCES

Books and Journals

Martin, J.D., Keown, A.J. and Titman, S., 2020. Financial management: principles and

applications. Prentice Hall.

Okanazu, O.O., 2018. Financial management decision practices for ensuring business solvency

by small and medium scale enterprises. Acta Oeconomica Universitatis Selye, 7(2),

pp.109-121.

Andreeva, O.V., Vovchenko, N.G., Ivanova, O.B. and Kostoglodova, E.D., 2018. Green finance:

trends and financial regulation prospects. In Contemporary Issues in Business and

Financial Management in Eastern Europe. Emerald Publishing Limited.

Haw, I.M., Hu, B., Wu, D. and Zhang, X., 2018. Having a finger in the pie: labor power and

corporate payout policy. Financial Management, 47(4), pp.993-1027.

Egginton, J.F. and McCumber, W.R., 2019. Executive network centrality and stock liquidity.

Financial Management, 48(3), pp.849-871.

Rachidi, H. and El Mohajir, M., 2021. Improving SMEs’ performance using innovative

knowledge and financial system designed from the Moroccan business environment.

African Journal of Science, Technology, Innovation and Development, 13(1), pp.15-30.

Drake, P.P., Fabozzi, F.J. and Fabozzi, F.A., 2022. Financial risk management. World Scientific

Book Chapters, pp.295-311.

Byun, H.S., Kim, W., Lee, E.J. and Park, K.S., 2019. When and why do takeovers lead to fraud?.

Financial Management, 48(1), pp.45-76.

Grossi, G., Ho, A.T. and Joyce, P.G., 2020. Budgetary responses to a global pandemic:

international experiences and lessons for a sustainable future. Journal of Public

Budgeting, Accounting & Financial Management.

Islam, M.A., Liu, H., Khan, M.A., Islam, M.T. and Sultanuzzaman, M.R., 2021. Does foreign

direct investment deepen the financial system in Southeast Asian economies?. Journal

of Multinational Financial Management, 61, p.100682.

Books and Journals

Martin, J.D., Keown, A.J. and Titman, S., 2020. Financial management: principles and

applications. Prentice Hall.

Okanazu, O.O., 2018. Financial management decision practices for ensuring business solvency

by small and medium scale enterprises. Acta Oeconomica Universitatis Selye, 7(2),

pp.109-121.

Andreeva, O.V., Vovchenko, N.G., Ivanova, O.B. and Kostoglodova, E.D., 2018. Green finance:

trends and financial regulation prospects. In Contemporary Issues in Business and

Financial Management in Eastern Europe. Emerald Publishing Limited.

Haw, I.M., Hu, B., Wu, D. and Zhang, X., 2018. Having a finger in the pie: labor power and

corporate payout policy. Financial Management, 47(4), pp.993-1027.

Egginton, J.F. and McCumber, W.R., 2019. Executive network centrality and stock liquidity.

Financial Management, 48(3), pp.849-871.

Rachidi, H. and El Mohajir, M., 2021. Improving SMEs’ performance using innovative

knowledge and financial system designed from the Moroccan business environment.

African Journal of Science, Technology, Innovation and Development, 13(1), pp.15-30.

Drake, P.P., Fabozzi, F.J. and Fabozzi, F.A., 2022. Financial risk management. World Scientific

Book Chapters, pp.295-311.

Byun, H.S., Kim, W., Lee, E.J. and Park, K.S., 2019. When and why do takeovers lead to fraud?.

Financial Management, 48(1), pp.45-76.

Grossi, G., Ho, A.T. and Joyce, P.G., 2020. Budgetary responses to a global pandemic:

international experiences and lessons for a sustainable future. Journal of Public

Budgeting, Accounting & Financial Management.

Islam, M.A., Liu, H., Khan, M.A., Islam, M.T. and Sultanuzzaman, M.R., 2021. Does foreign

direct investment deepen the financial system in Southeast Asian economies?. Journal

of Multinational Financial Management, 61, p.100682.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.