Management Accounting Report: Dell's Costing and Budgeting Analysis

VerifiedAdded on 2020/02/12

|15

|4027

|128

Report

AI Summary

This report provides a comprehensive analysis of management accounting principles and their application within Dell, a leading information technology and cloud computing service provider. The report begins by defining management accounting and its essential role in providing crucial information to managers for strategic decision-making, contrasting it with financial accounting. It delves into various management accounting systems such as cost accounting systems, including job order costing, process costing, and batch costing, as well as price optimization. The report then evaluates different managerial accounting reporting methods, including job cost reports, accounts receivable reports, budgeted reports, and inventory management reports. A significant portion of the report focuses on the computation of costs per unit under marginal and absorption costing, highlighting their differences through detailed calculations and interpretations. Furthermore, the report explores the advantages and disadvantages of different budgetary planning tools, such as incremental budgeting, zero-based budgeting, and activity-based budgeting. The report also includes practical applications, such as computing standard costs and variance analysis. The report concludes with a comparative analysis of Dell and HP, adapting management accounting to address financial problems and improve business strategies.

MANAGEMENT

ACCOUNTING

1.

ACCOUNTING

1.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION 4

TASK 1 4

P1 Explaining the concept of management accounting & the essential requirement of different

MAS 4

P2 Evaluating different methods for the managerial accounting reporting 5

TASK 2 6

P3 Computation of costs per unit under marginal and absorption costing and explaining their

difference 6

TASK 3 8

P4 Explaining the advantages and disadvantages of different types of budgetary planning tools

8

A. Computing the standard costs of PVC sheets required to manufacture 4,000 keyboards

9

B. Computing the material price and quantity variance 10

TASK 4 10

P5 Comparing dell with HP in order to adapt MAS to respond financial problems 10

CONCLUSION 12

REFERENCES 13

1.

INTRODUCTION 4

TASK 1 4

P1 Explaining the concept of management accounting & the essential requirement of different

MAS 4

P2 Evaluating different methods for the managerial accounting reporting 5

TASK 2 6

P3 Computation of costs per unit under marginal and absorption costing and explaining their

difference 6

TASK 3 8

P4 Explaining the advantages and disadvantages of different types of budgetary planning tools

8

A. Computing the standard costs of PVC sheets required to manufacture 4,000 keyboards

9

B. Computing the material price and quantity variance 10

TASK 4 10

P5 Comparing dell with HP in order to adapt MAS to respond financial problems 10

CONCLUSION 12

REFERENCES 13

1.

2. Table of figures

Table 1 Calculation of unit cost under absorption & marginal costing 6

Table 2 Calculation of cost of production & sale under absorption costing 6

Table 3 Calculation of gross profit and net profit under absorption costing 7

Table 4 Calculation of cost of production & sale under marginal costing 7

Table 5 Calculation of contribution and net margin under marginal/variable costing 7

Table 1 Calculation of unit cost under absorption & marginal costing 6

Table 2 Calculation of cost of production & sale under absorption costing 6

Table 3 Calculation of gross profit and net profit under absorption costing 7

Table 4 Calculation of cost of production & sale under marginal costing 7

Table 5 Calculation of contribution and net margin under marginal/variable costing 7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Managerial accounting is a process of reporting and communication business performance to

the mangers and top executives which aids in right strategy formulation and smarter business

decisions. It is totally different from the financial accounting because in this, firm’s top directors

not only look after the preparation of annual accounts but their main target is to gather essential or

important information for bringing out efficiency into the operations and ensure sustainable success.

The present assignment here emphasizes on the managerial accounting operations and reporting for

a leading information technology & cloud computing service provider firm, named Dell. In the

report, various techniques like cost calculation, standard costing and different kinds of managerial

accounting system will be analysed.

1. TASK 1

1. P1 Explaining the concept of management accounting & the essential requirement of

different MAS

Management accounting is a process of furnishing accounting information by the managers

in order to make viable and feasible business decisions. It serves vital information to the managers

for making right planning through modifying, analysing and interpreting the financial information.

It plays a significant role in Dell to streamline their daily operations, effective and efficient

functionality and appropriate business planning. At the same time, it also helps firm to put better

control by comparison of the actual performance with the targets and co-ordinate various functions.

Management accounting system can be deployed by the Dell to deliver required information to the

managers on time for making better decisions. It helps to generate reports that allow managers to

make plans, policies and strategies for the smooth functionality. With reference to Dell, its

managers can take assistance of the following system, described here as under:

Cost accounting system: Dell is a profit-oriented business which aims at maximizing their

net profitability by effective control over their cost. Thus, CAS furnishes cost related data and

provides it to the managers i.e. cost of material purchase, labour’s wages and others which helps in

valuation of closing stock (Banerjee and Das, 2017). By analysing the cost reports, top managers

and personnel can create innovative planning and decisions to minimize expenditures and thereby

drive better return. Here, two types of cost accounting system can be used by the Dell that are

presented here as under:

Managerial accounting is a process of reporting and communication business performance to

the mangers and top executives which aids in right strategy formulation and smarter business

decisions. It is totally different from the financial accounting because in this, firm’s top directors

not only look after the preparation of annual accounts but their main target is to gather essential or

important information for bringing out efficiency into the operations and ensure sustainable success.

The present assignment here emphasizes on the managerial accounting operations and reporting for

a leading information technology & cloud computing service provider firm, named Dell. In the

report, various techniques like cost calculation, standard costing and different kinds of managerial

accounting system will be analysed.

1. TASK 1

1. P1 Explaining the concept of management accounting & the essential requirement of

different MAS

Management accounting is a process of furnishing accounting information by the managers

in order to make viable and feasible business decisions. It serves vital information to the managers

for making right planning through modifying, analysing and interpreting the financial information.

It plays a significant role in Dell to streamline their daily operations, effective and efficient

functionality and appropriate business planning. At the same time, it also helps firm to put better

control by comparison of the actual performance with the targets and co-ordinate various functions.

Management accounting system can be deployed by the Dell to deliver required information to the

managers on time for making better decisions. It helps to generate reports that allow managers to

make plans, policies and strategies for the smooth functionality. With reference to Dell, its

managers can take assistance of the following system, described here as under:

Cost accounting system: Dell is a profit-oriented business which aims at maximizing their

net profitability by effective control over their cost. Thus, CAS furnishes cost related data and

provides it to the managers i.e. cost of material purchase, labour’s wages and others which helps in

valuation of closing stock (Banerjee and Das, 2017). By analysing the cost reports, top managers

and personnel can create innovative planning and decisions to minimize expenditures and thereby

drive better return. Here, two types of cost accounting system can be used by the Dell that are

presented here as under:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Job order costing: This system accumulates all the costs incurred i.e. material, labour etc.

for each job work and enables Dell’s managerial team to find out the total cost of the order placed

by the customer. By identifying the cost, manager can make good pricing decisions at where they

will be ready to offer their goods to the consumer and meet their return requirement (Romano,

2015).

Process costing: Unlike the above, this system accumulates or incorporates cost of

manufacturing for each of the process. It is helpful for those companies where goods are

manufactured in different divisions and accumulation of costs of all the departments helps to find

out the total cost.

Batch costing: This system is useful for determining the cost for a group of items and

services produced by the Dell. It helps to identify and determine total batch costs comprising fixed

and variable costs (Bhimani and et.al., 2013). Here, per unit batch cost can be founded out by

dividing the total costs with the number of units produced in batch.

Price optimization: This system is very useful in distributing the market into various sub-

sets and thereby defines the target market to receive maximum yield. Dell’s managerial team can

use it to find out the extent to which consumers are price-sensitive (Price optimization, 2015). With

the help of this, top managers can track that how change in their offering prices will bring

fluctuations in the market demand, which helps to set a right price for the target market to earn

maximum return.

1. P2 Evaluating different methods for the managerial accounting reporting

In the business, managers acquire various set of operational data from different reports and

analyse the information for making viable & informed decisions to ensure sustainable progress. The

main reports which Dell’s higher authority can use for designing the best strategies and decisions

are enumerated here as under:

Job cost reports: As discussed earlier, that job costing system accumulates the expenditures

made by the firm for manufacturing a given number of units (Yigitbasioglu, 2017). Thus, this

system generates costing reports for every job work, which assist decision-makers in cost evaluation

and right selling pricing decisions.

Accounts receivable/debtors reports: This reports indicates the amount of outstanding

debtors, their bills, amount and maturity dates as well. It facilitates credit collection division of Dell

to make better plans for taking out money promptly from the debtors to maintain adequate cash

for each job work and enables Dell’s managerial team to find out the total cost of the order placed

by the customer. By identifying the cost, manager can make good pricing decisions at where they

will be ready to offer their goods to the consumer and meet their return requirement (Romano,

2015).

Process costing: Unlike the above, this system accumulates or incorporates cost of

manufacturing for each of the process. It is helpful for those companies where goods are

manufactured in different divisions and accumulation of costs of all the departments helps to find

out the total cost.

Batch costing: This system is useful for determining the cost for a group of items and

services produced by the Dell. It helps to identify and determine total batch costs comprising fixed

and variable costs (Bhimani and et.al., 2013). Here, per unit batch cost can be founded out by

dividing the total costs with the number of units produced in batch.

Price optimization: This system is very useful in distributing the market into various sub-

sets and thereby defines the target market to receive maximum yield. Dell’s managerial team can

use it to find out the extent to which consumers are price-sensitive (Price optimization, 2015). With

the help of this, top managers can track that how change in their offering prices will bring

fluctuations in the market demand, which helps to set a right price for the target market to earn

maximum return.

1. P2 Evaluating different methods for the managerial accounting reporting

In the business, managers acquire various set of operational data from different reports and

analyse the information for making viable & informed decisions to ensure sustainable progress. The

main reports which Dell’s higher authority can use for designing the best strategies and decisions

are enumerated here as under:

Job cost reports: As discussed earlier, that job costing system accumulates the expenditures

made by the firm for manufacturing a given number of units (Yigitbasioglu, 2017). Thus, this

system generates costing reports for every job work, which assist decision-makers in cost evaluation

and right selling pricing decisions.

Accounts receivable/debtors reports: This reports indicates the amount of outstanding

debtors, their bills, amount and maturity dates as well. It facilitates credit collection division of Dell

to make better plans for taking out money promptly from the debtors to maintain adequate cash

resources in the business (Choi, Kulick and Mayer, 2009).

Budgeted reports: Every departmental manager set standard target for their divisional

revenues and payments made for the continual of operations. Thus, this reports delivers information

to the policy makers about targets which is compared with the actual results to detect deviations

whether favourable or unfavourable and thereby make remedial actions to combat negative

variances.

Inventory management reports: Stock management is an essential part of the operational

management so as to maintain stock at sufficient level for safeguarding against sudden increase in

the consumer demand (Fullerton, Kennedy and Widener, 2013). Such reports delivers information

regarding hourly wages rate, closing stock & others which managers analyse for the right inventory

planning & its management.

1. TASK 2

2. P3 Computation of costs per unit under marginal and absorption costing and explaining their

difference

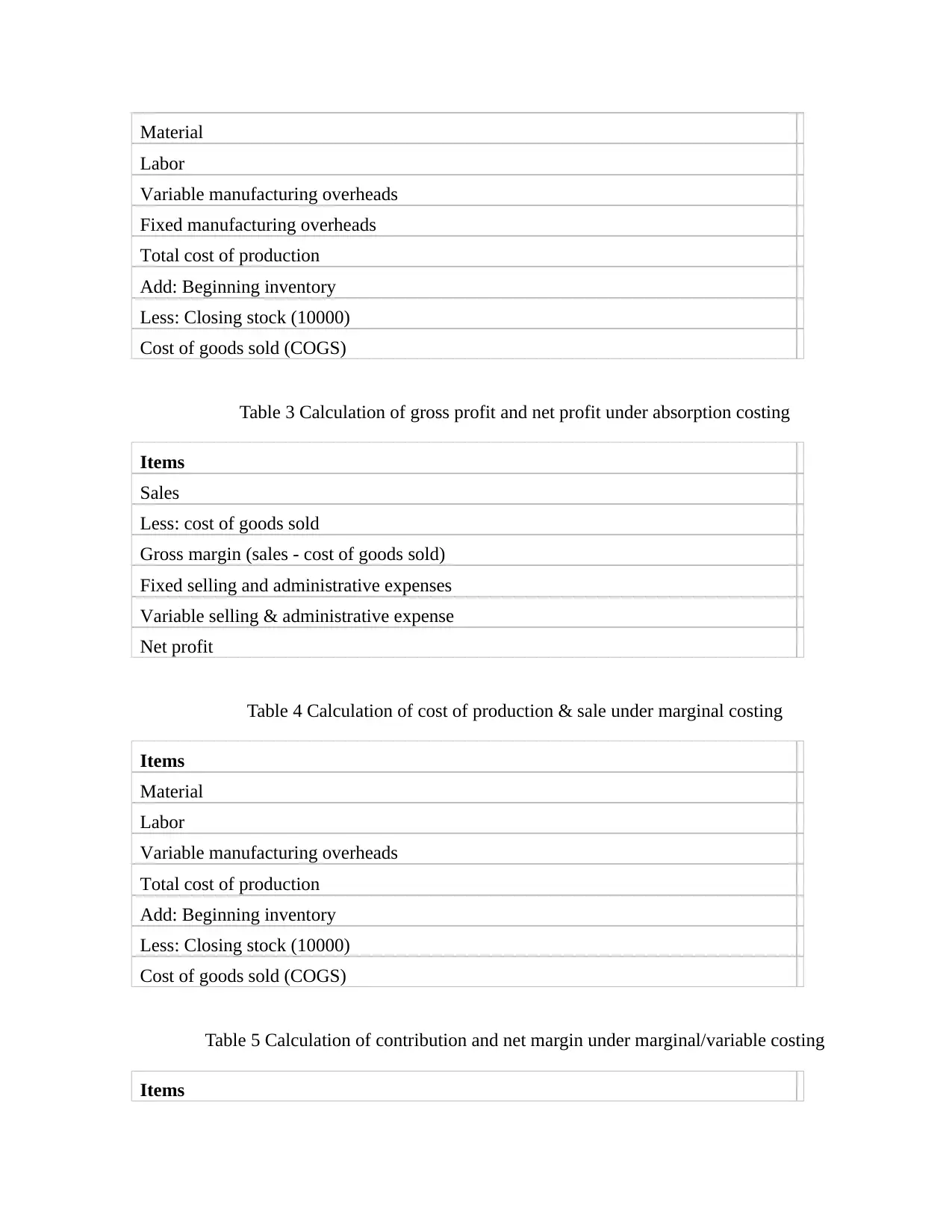

The main difference marginal & absorption costing methods, is that, former uses only the

variable cost for measuring cost of production whereas later gives consideration to both the fixed &

variable costs for valuation of closing inventory (Banerjee and Das, 2017).

Table 1 Calculation of unit cost under absorption & marginal costing

Particulars Full/Absorption costingVariable/Marginal costing

Direct Material purchase 20 20

Direct labour 8 8

Variable manufacturing overheads 4 4

Fixed manufacturing overheads 10 -

Costs/unit 42 32

Table 2 Calculation of cost of production & sale under absorption costing

Items

Budgeted reports: Every departmental manager set standard target for their divisional

revenues and payments made for the continual of operations. Thus, this reports delivers information

to the policy makers about targets which is compared with the actual results to detect deviations

whether favourable or unfavourable and thereby make remedial actions to combat negative

variances.

Inventory management reports: Stock management is an essential part of the operational

management so as to maintain stock at sufficient level for safeguarding against sudden increase in

the consumer demand (Fullerton, Kennedy and Widener, 2013). Such reports delivers information

regarding hourly wages rate, closing stock & others which managers analyse for the right inventory

planning & its management.

1. TASK 2

2. P3 Computation of costs per unit under marginal and absorption costing and explaining their

difference

The main difference marginal & absorption costing methods, is that, former uses only the

variable cost for measuring cost of production whereas later gives consideration to both the fixed &

variable costs for valuation of closing inventory (Banerjee and Das, 2017).

Table 1 Calculation of unit cost under absorption & marginal costing

Particulars Full/Absorption costingVariable/Marginal costing

Direct Material purchase 20 20

Direct labour 8 8

Variable manufacturing overheads 4 4

Fixed manufacturing overheads 10 -

Costs/unit 42 32

Table 2 Calculation of cost of production & sale under absorption costing

Items

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Material

Labor

Variable manufacturing overheads

Fixed manufacturing overheads

Total cost of production

Add: Beginning inventory

Less: Closing stock (10000)

Cost of goods sold (COGS)

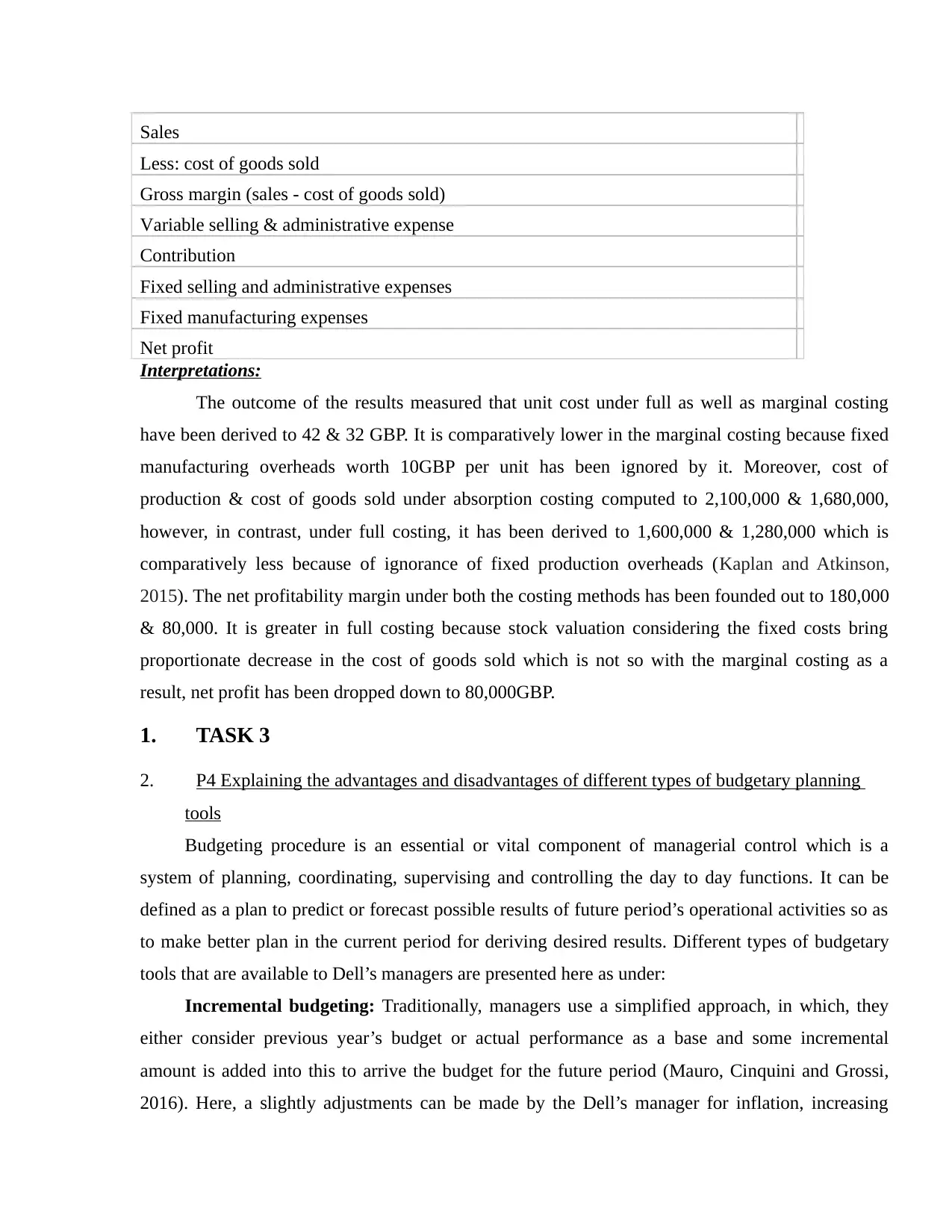

Table 3 Calculation of gross profit and net profit under absorption costing

Items

Sales

Less: cost of goods sold

Gross margin (sales - cost of goods sold)

Fixed selling and administrative expenses

Variable selling & administrative expense

Net profit

Table 4 Calculation of cost of production & sale under marginal costing

Items

Material

Labor

Variable manufacturing overheads

Total cost of production

Add: Beginning inventory

Less: Closing stock (10000)

Cost of goods sold (COGS)

Table 5 Calculation of contribution and net margin under marginal/variable costing

Items

Labor

Variable manufacturing overheads

Fixed manufacturing overheads

Total cost of production

Add: Beginning inventory

Less: Closing stock (10000)

Cost of goods sold (COGS)

Table 3 Calculation of gross profit and net profit under absorption costing

Items

Sales

Less: cost of goods sold

Gross margin (sales - cost of goods sold)

Fixed selling and administrative expenses

Variable selling & administrative expense

Net profit

Table 4 Calculation of cost of production & sale under marginal costing

Items

Material

Labor

Variable manufacturing overheads

Total cost of production

Add: Beginning inventory

Less: Closing stock (10000)

Cost of goods sold (COGS)

Table 5 Calculation of contribution and net margin under marginal/variable costing

Items

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Sales

Less: cost of goods sold

Gross margin (sales - cost of goods sold)

Variable selling & administrative expense

Contribution

Fixed selling and administrative expenses

Fixed manufacturing expenses

Net profit

Interpretations:

The outcome of the results measured that unit cost under full as well as marginal costing

have been derived to 42 & 32 GBP. It is comparatively lower in the marginal costing because fixed

manufacturing overheads worth 10GBP per unit has been ignored by it. Moreover, cost of

production & cost of goods sold under absorption costing computed to 2,100,000 & 1,680,000,

however, in contrast, under full costing, it has been derived to 1,600,000 & 1,280,000 which is

comparatively less because of ignorance of fixed production overheads (Kaplan and Atkinson,

2015). The net profitability margin under both the costing methods has been founded out to 180,000

& 80,000. It is greater in full costing because stock valuation considering the fixed costs bring

proportionate decrease in the cost of goods sold which is not so with the marginal costing as a

result, net profit has been dropped down to 80,000GBP.

1. TASK 3

2. P4 Explaining the advantages and disadvantages of different types of budgetary planning

tools

Budgeting procedure is an essential or vital component of managerial control which is a

system of planning, coordinating, supervising and controlling the day to day functions. It can be

defined as a plan to predict or forecast possible results of future period’s operational activities so as

to make better plan in the current period for deriving desired results. Different types of budgetary

tools that are available to Dell’s managers are presented here as under:

Incremental budgeting: Traditionally, managers use a simplified approach, in which, they

either consider previous year’s budget or actual performance as a base and some incremental

amount is added into this to arrive the budget for the future period (Mauro, Cinquini and Grossi,

2016). Here, a slightly adjustments can be made by the Dell’s manager for inflation, increasing

Less: cost of goods sold

Gross margin (sales - cost of goods sold)

Variable selling & administrative expense

Contribution

Fixed selling and administrative expenses

Fixed manufacturing expenses

Net profit

Interpretations:

The outcome of the results measured that unit cost under full as well as marginal costing

have been derived to 42 & 32 GBP. It is comparatively lower in the marginal costing because fixed

manufacturing overheads worth 10GBP per unit has been ignored by it. Moreover, cost of

production & cost of goods sold under absorption costing computed to 2,100,000 & 1,680,000,

however, in contrast, under full costing, it has been derived to 1,600,000 & 1,280,000 which is

comparatively less because of ignorance of fixed production overheads (Kaplan and Atkinson,

2015). The net profitability margin under both the costing methods has been founded out to 180,000

& 80,000. It is greater in full costing because stock valuation considering the fixed costs bring

proportionate decrease in the cost of goods sold which is not so with the marginal costing as a

result, net profit has been dropped down to 80,000GBP.

1. TASK 3

2. P4 Explaining the advantages and disadvantages of different types of budgetary planning

tools

Budgeting procedure is an essential or vital component of managerial control which is a

system of planning, coordinating, supervising and controlling the day to day functions. It can be

defined as a plan to predict or forecast possible results of future period’s operational activities so as

to make better plan in the current period for deriving desired results. Different types of budgetary

tools that are available to Dell’s managers are presented here as under:

Incremental budgeting: Traditionally, managers use a simplified approach, in which, they

either consider previous year’s budget or actual performance as a base and some incremental

amount is added into this to arrive the budget for the future period (Mauro, Cinquini and Grossi,

2016). Here, a slightly adjustments can be made by the Dell’s manager for inflation, increasing

selling price, high cost and others.

Advantages:

a. 1. It is very easy to prepare and can be prepared promptly because it requires a little bit

changes in the previous period’s budget or actual results.

b. 2. Less time in the budget preparation leads to less costs of preparation.

c. 3. It prevents possible conflicts among all the departmental managers of the Dell

because it follows consistent approach for the resource allocation.

Limitations:

• • It favour the execution of all the activities which believe that current running costs

will be incur in future period’s also thus it give rises to the unnecessarily spending in the

unproductive functions.

• • Managers and workers are not motivated or incentivised to reduce their costs

because they are not rewarded with any incentive for the same (Renz, 2016).

• • It decides unchallenging performance targets which do not encourage employees or

managers to accept tough challenges for maximizing operational efficiency, minimizing cost

and others.

Zero-based budgeting: This method overcome the drawback of incremental budgeting

which tries to make optimal resource allocation by forcing every managers of all the Dell’s division

to fully justify every activity and cost properly which leads to optimum resource utilization.

Benefits:

• • It helps to motivate staff by setting challenging performance targets and also

encourage them to take initiatives to control cost (Sehgal, 2017).

• • It helps to respond changing conditions by considering the underlying trends in the

industry and market.

• • Another advantage of ZBB methods is that it helps in an efficient and optimum

resource allocation.

Drawbacks:

• • It may be possible that Dell’s departmental manager may not have required skills to

create the budget, which in turn, training may be required which takes time and cost as well.

• • Many-times, decisions are made at the time of budget creation which is not accepted

by some managers which may leads to have a detrimental effect on the firm.

Advantages:

a. 1. It is very easy to prepare and can be prepared promptly because it requires a little bit

changes in the previous period’s budget or actual results.

b. 2. Less time in the budget preparation leads to less costs of preparation.

c. 3. It prevents possible conflicts among all the departmental managers of the Dell

because it follows consistent approach for the resource allocation.

Limitations:

• • It favour the execution of all the activities which believe that current running costs

will be incur in future period’s also thus it give rises to the unnecessarily spending in the

unproductive functions.

• • Managers and workers are not motivated or incentivised to reduce their costs

because they are not rewarded with any incentive for the same (Renz, 2016).

• • It decides unchallenging performance targets which do not encourage employees or

managers to accept tough challenges for maximizing operational efficiency, minimizing cost

and others.

Zero-based budgeting: This method overcome the drawback of incremental budgeting

which tries to make optimal resource allocation by forcing every managers of all the Dell’s division

to fully justify every activity and cost properly which leads to optimum resource utilization.

Benefits:

• • It helps to motivate staff by setting challenging performance targets and also

encourage them to take initiatives to control cost (Sehgal, 2017).

• • It helps to respond changing conditions by considering the underlying trends in the

industry and market.

• • Another advantage of ZBB methods is that it helps in an efficient and optimum

resource allocation.

Drawbacks:

• • It may be possible that Dell’s departmental manager may not have required skills to

create the budget, which in turn, training may be required which takes time and cost as well.

• • Many-times, decisions are made at the time of budget creation which is not accepted

by some managers which may leads to have a detrimental effect on the firm.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Activity based budgeting:

Under this method, budget is prepared by the managers, in which, spending proposition is

totally based upon past period’s production activities (Saladrigues and Tena, 2017). They examine

the cost of various activities and every activity is allocated with the fund derived from the related

activity.

Benefit:

• • It draws managerial attention towards overheads which may be incur in the large

proportion of total costs of the Dell.

• • It helps firm to control the cause of the cost for the better cost management.

• • ABB method helps to provide an important insight to the management for total

quality management by presenting a link between costs with the service delivery system.

Drawback:

• • High level of understanding is the first and foremost requirement of ABB, thus, in

case of lack of expertise knowledge and speciality, the technique cannot be applied.

• • Training requirement also leads to drive excessive costs to the Dell and results in

lesser yield.

1. A. Computing the standard costs of PVC sheets required to manufacture 4,000 keyboards

Standard costs refers to the costs that Dell’s production manager has expected to incur for

producing 4000 keyboards. In other words, it refers to the target cost that has been decided to be

incur in the production of target number of units (Schaltegger, Gibassier and Zvezdov, 2013). With

the stated scenario, Dell has been decided to produce 4000 keyboards which standard costs has been

computed here as under:

PVC sheets/per unit – 2.5 feet

Price per sheet – 3.60 GBP

Total sheets required to produce 4,000 keyboards = 4,000*2.5 = 10,000 feet

Costs of 100,000 PVC sheets = 10,000*3.60 = 36,000 GBP

Thus, standard costs of 4,000 key boards = 36,000 GBP

Actual costs = 37,400GBP

Difference: standard cost – actual cost

= 36,000 GBP – 37,400 GBP

= 1,400 GBP (Adverse/Unfavorable)

Under this method, budget is prepared by the managers, in which, spending proposition is

totally based upon past period’s production activities (Saladrigues and Tena, 2017). They examine

the cost of various activities and every activity is allocated with the fund derived from the related

activity.

Benefit:

• • It draws managerial attention towards overheads which may be incur in the large

proportion of total costs of the Dell.

• • It helps firm to control the cause of the cost for the better cost management.

• • ABB method helps to provide an important insight to the management for total

quality management by presenting a link between costs with the service delivery system.

Drawback:

• • High level of understanding is the first and foremost requirement of ABB, thus, in

case of lack of expertise knowledge and speciality, the technique cannot be applied.

• • Training requirement also leads to drive excessive costs to the Dell and results in

lesser yield.

1. A. Computing the standard costs of PVC sheets required to manufacture 4,000 keyboards

Standard costs refers to the costs that Dell’s production manager has expected to incur for

producing 4000 keyboards. In other words, it refers to the target cost that has been decided to be

incur in the production of target number of units (Schaltegger, Gibassier and Zvezdov, 2013). With

the stated scenario, Dell has been decided to produce 4000 keyboards which standard costs has been

computed here as under:

PVC sheets/per unit – 2.5 feet

Price per sheet – 3.60 GBP

Total sheets required to produce 4,000 keyboards = 4,000*2.5 = 10,000 feet

Costs of 100,000 PVC sheets = 10,000*3.60 = 36,000 GBP

Thus, standard costs of 4,000 key boards = 36,000 GBP

Actual costs = 37,400GBP

Difference: standard cost – actual cost

= 36,000 GBP – 37,400 GBP

= 1,400 GBP (Adverse/Unfavorable)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

As per the founded results, Dell has incurred a negative variance of 1,400 GBP on the

production of 4,000 keyboards because targeted cost has been decided to 36,000 GBP whilst the

actual costs has been set to 37,400 GBP.

1. B. Computing the material price and quantity variance

Material price variance (MPV): Actual quantity (standard price – actual price)

= 10,000 feet (3.60 GBP – 3.40 GBP)

= 10,000 feet (0.20 GBP)

= 2,000 (favourable)

Material quantity variance (MQV): Actual price (standard quantity – actual quantity)

= 3.4GBP (10,000 feet – 11,000 feet)

= 3.4GBP (-1,000 feet)

= 3,400 GBP (adverse)

From the results, it can be seen that MPV is founded positive to 2,000GBP because Dell has

decided that per sheet, it would have to pay 3.60GBP whilst, in the actual market, there is a cheaper

availability of sheets at a price of 3.40GBP reduced the targeted cost by 2,000 which is good. On

the contrary side, MQV reported negative results to 3,400 GBP. It is because, firm has decided to

use 10,000 feet of PVC sheet for producing 4,000 keyboards while the actual consumption of PVC

sheets reported to 11,000 feet higher by 1,000. Inefficient and unoptimal use of PVC sheets, theft

activities and wastage of the sheets may be the reason behind high use of material, as a result, it

leads to cause a negative variance of 3,400 GBP.

1. TASK 4

2. P5 Comparing dell with HP in order to adapt MAS to respond financial problems

In the stated case, it has been given that Dell is suffering profitability issues in comparison

to the competitors which impact its operational results and competitive position in an adverse

manner. In order to overcome such financial difficulties, Dell’s management can be suggested with

the following ways that are presented underneath:

Ratio analysis: It is the best technique, under this, Dell’s managerial team can compare their

own profitability ratios like gross margin, operational margin and net margin with the HP’s

profitability performance. With the comparative evaluation, company can find out their sales as well

as cost performance and come up with the right strategy for minimizing costs and maximizing total

production of 4,000 keyboards because targeted cost has been decided to 36,000 GBP whilst the

actual costs has been set to 37,400 GBP.

1. B. Computing the material price and quantity variance

Material price variance (MPV): Actual quantity (standard price – actual price)

= 10,000 feet (3.60 GBP – 3.40 GBP)

= 10,000 feet (0.20 GBP)

= 2,000 (favourable)

Material quantity variance (MQV): Actual price (standard quantity – actual quantity)

= 3.4GBP (10,000 feet – 11,000 feet)

= 3.4GBP (-1,000 feet)

= 3,400 GBP (adverse)

From the results, it can be seen that MPV is founded positive to 2,000GBP because Dell has

decided that per sheet, it would have to pay 3.60GBP whilst, in the actual market, there is a cheaper

availability of sheets at a price of 3.40GBP reduced the targeted cost by 2,000 which is good. On

the contrary side, MQV reported negative results to 3,400 GBP. It is because, firm has decided to

use 10,000 feet of PVC sheet for producing 4,000 keyboards while the actual consumption of PVC

sheets reported to 11,000 feet higher by 1,000. Inefficient and unoptimal use of PVC sheets, theft

activities and wastage of the sheets may be the reason behind high use of material, as a result, it

leads to cause a negative variance of 3,400 GBP.

1. TASK 4

2. P5 Comparing dell with HP in order to adapt MAS to respond financial problems

In the stated case, it has been given that Dell is suffering profitability issues in comparison

to the competitors which impact its operational results and competitive position in an adverse

manner. In order to overcome such financial difficulties, Dell’s management can be suggested with

the following ways that are presented underneath:

Ratio analysis: It is the best technique, under this, Dell’s managerial team can compare their

own profitability ratios like gross margin, operational margin and net margin with the HP’s

profitability performance. With the comparative evaluation, company can find out their sales as well

as cost performance and come up with the right strategy for minimizing costs and maximizing total

sales in order to drive greater return (Schipper, Francis and Weil, 2017). Besides this, Dell can also

compare its own financial position with the Dell’s financial health through the evaluation of their

liquidity position and solvency performance. With the evaluation of it, company can devise right

strategies and create right plans for the effective working capital decisions, designing a right capital

structure, cash management strategies, negotiating plan with the suppliers and prompt receipts from

the debtors as well, as a result, firm can achieve success and overcome financial consequences.

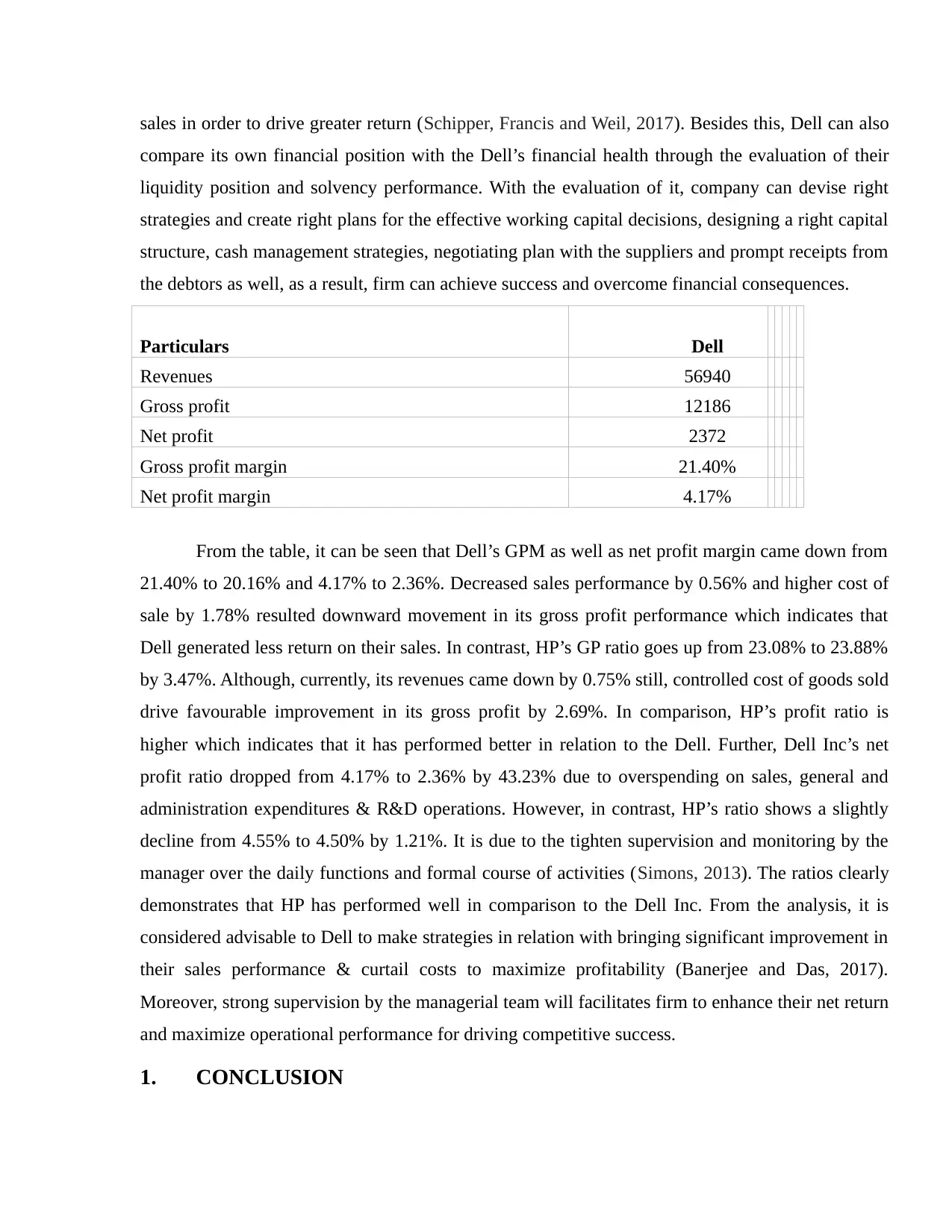

Particulars Dell

Revenues 56940

Gross profit 12186

Net profit 2372

Gross profit margin 21.40%

Net profit margin 4.17%

From the table, it can be seen that Dell’s GPM as well as net profit margin came down from

21.40% to 20.16% and 4.17% to 2.36%. Decreased sales performance by 0.56% and higher cost of

sale by 1.78% resulted downward movement in its gross profit performance which indicates that

Dell generated less return on their sales. In contrast, HP’s GP ratio goes up from 23.08% to 23.88%

by 3.47%. Although, currently, its revenues came down by 0.75% still, controlled cost of goods sold

drive favourable improvement in its gross profit by 2.69%. In comparison, HP’s profit ratio is

higher which indicates that it has performed better in relation to the Dell. Further, Dell Inc’s net

profit ratio dropped from 4.17% to 2.36% by 43.23% due to overspending on sales, general and

administration expenditures & R&D operations. However, in contrast, HP’s ratio shows a slightly

decline from 4.55% to 4.50% by 1.21%. It is due to the tighten supervision and monitoring by the

manager over the daily functions and formal course of activities (Simons, 2013). The ratios clearly

demonstrates that HP has performed well in comparison to the Dell Inc. From the analysis, it is

considered advisable to Dell to make strategies in relation with bringing significant improvement in

their sales performance & curtail costs to maximize profitability (Banerjee and Das, 2017).

Moreover, strong supervision by the managerial team will facilitates firm to enhance their net return

and maximize operational performance for driving competitive success.

1. CONCLUSION

compare its own financial position with the Dell’s financial health through the evaluation of their

liquidity position and solvency performance. With the evaluation of it, company can devise right

strategies and create right plans for the effective working capital decisions, designing a right capital

structure, cash management strategies, negotiating plan with the suppliers and prompt receipts from

the debtors as well, as a result, firm can achieve success and overcome financial consequences.

Particulars Dell

Revenues 56940

Gross profit 12186

Net profit 2372

Gross profit margin 21.40%

Net profit margin 4.17%

From the table, it can be seen that Dell’s GPM as well as net profit margin came down from

21.40% to 20.16% and 4.17% to 2.36%. Decreased sales performance by 0.56% and higher cost of

sale by 1.78% resulted downward movement in its gross profit performance which indicates that

Dell generated less return on their sales. In contrast, HP’s GP ratio goes up from 23.08% to 23.88%

by 3.47%. Although, currently, its revenues came down by 0.75% still, controlled cost of goods sold

drive favourable improvement in its gross profit by 2.69%. In comparison, HP’s profit ratio is

higher which indicates that it has performed better in relation to the Dell. Further, Dell Inc’s net

profit ratio dropped from 4.17% to 2.36% by 43.23% due to overspending on sales, general and

administration expenditures & R&D operations. However, in contrast, HP’s ratio shows a slightly

decline from 4.55% to 4.50% by 1.21%. It is due to the tighten supervision and monitoring by the

manager over the daily functions and formal course of activities (Simons, 2013). The ratios clearly

demonstrates that HP has performed well in comparison to the Dell Inc. From the analysis, it is

considered advisable to Dell to make strategies in relation with bringing significant improvement in

their sales performance & curtail costs to maximize profitability (Banerjee and Das, 2017).

Moreover, strong supervision by the managerial team will facilitates firm to enhance their net return

and maximize operational performance for driving competitive success.

1. CONCLUSION

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.