Management Accounting Report: Costing and Budgetary Control for DELL

VerifiedAdded on 2020/09/17

|17

|3831

|96

Report

AI Summary

This report delves into the realm of management accounting, specifically focusing on its application within the DELL company. It begins by defining management accounting systems and explores various types, emphasizing their role in effective decision-making. The report then examines essential techniques for management accounting reporting, including cost reports, budgets, and performance reports. A key section involves calculating the cost per unit using both marginal and absorption costing methods, accompanied by income statements for each method. The report also provides a financial report and discusses the advantages and disadvantages of budgetary control. It further explores the integration of management accounting systems with reporting, highlighting the importance of planning tools and their application in solving financial problems. The report concludes with an examination of challenges in choosing a management accounting system and its role in addressing financial problems, offering a comprehensive overview of management accounting practices and their impact on organizational performance.

Management

Accounting

Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1 Concept of management accounting system and their different types use in it................1

P2 Techniques which are essential for Management Accounting reporting..........................2

M1 Benefits of Management Accounting Systems................................................................2

D1 Integration of Management Accounting System and Management Accounting Reporting. 3

TASK 2............................................................................................................................................3

P3 Calculation of cost per unit by using marginal and absorption costing methods..............3

Calculation of cost per unit:...................................................................................................3

M2 Income statement under Marginal costing.......................................................................5

D2 Financial report.................................................................................................................6

TASK 3............................................................................................................................................7

P4 Advantages and Disadvantages of budgetary control.......................................................7

M3 Usage of planning tool's applidcation..............................................................................9

D3 Use of planning tools for solving financial problems.....................................................10

TASK 4..........................................................................................................................................10

P5 Examination with the challenger for choosing management accounting system............10

M4 Management accounting in respond to financial problems...........................................11

REFERENCES..............................................................................................................................13

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1 Concept of management accounting system and their different types use in it................1

P2 Techniques which are essential for Management Accounting reporting..........................2

M1 Benefits of Management Accounting Systems................................................................2

D1 Integration of Management Accounting System and Management Accounting Reporting. 3

TASK 2............................................................................................................................................3

P3 Calculation of cost per unit by using marginal and absorption costing methods..............3

Calculation of cost per unit:...................................................................................................3

M2 Income statement under Marginal costing.......................................................................5

D2 Financial report.................................................................................................................6

TASK 3............................................................................................................................................7

P4 Advantages and Disadvantages of budgetary control.......................................................7

M3 Usage of planning tool's applidcation..............................................................................9

D3 Use of planning tools for solving financial problems.....................................................10

TASK 4..........................................................................................................................................10

P5 Examination with the challenger for choosing management accounting system............10

M4 Management accounting in respond to financial problems...........................................11

REFERENCES..............................................................................................................................13

INTRODUCTION

Management accounting is a managerial tool in which manager of an organisation

prepare accounting reports. In the report, all the information will be collected by the manager

and prepared in a managerial report. Organisation use this accounting system to improve the

performance level of an organisation (Ward, 2012). In this report, DELL company is use to make

effective management accounting techniques. This report gives the complete information of

management accounting and their importance in an organisation. It also describes the various

types management accounting system and Computation of cost per unit also explain in this

report. Furthermore, it also helps to prepare a financial reporting by use absorption and marginal

costing techniques. This report includes the advantages and disadvantages of different types of

budgetary tool and planning system. By making comparison of DELL with HP, effective

management accounting techniques are used so that organisation can work more better.

TASK 1

P1 Concept of management accounting system and their different types use in it

In management accounting, it consider all the know-how and idea which are useful to

make effectual preparation, choosing best alternatives among various alternatives which are best

fit for the organisation. To make effective decision in an organisation, all the information is

collected and classified as per such manner that such information can be used appropriately for

an organisation (Vosselman, 2014). Thus, to make effective decision in an organisation,

information is collected, classified and analysed by the manager.

Management accounting is essential for every organisation. Thus, DELL company use

various kinds of systems so that they can measure their performance, identify the risk and use

resources optimally. There are various kind of management accounting system, which are as

follows:

Batch costing: In this type of costing in which group of products and services are

produced which generated the cluster cost. Such cost is not easily identified and it is considered

as the best tool in which cost of batch is transferred to the individual while making the cost

accounting.

Process costing: This type of costing is suitable for those activity in which large number

of homogeneous products are produced by the organisation. In this method, cost of products is

identifying at each stage of production.

1

Management accounting is a managerial tool in which manager of an organisation

prepare accounting reports. In the report, all the information will be collected by the manager

and prepared in a managerial report. Organisation use this accounting system to improve the

performance level of an organisation (Ward, 2012). In this report, DELL company is use to make

effective management accounting techniques. This report gives the complete information of

management accounting and their importance in an organisation. It also describes the various

types management accounting system and Computation of cost per unit also explain in this

report. Furthermore, it also helps to prepare a financial reporting by use absorption and marginal

costing techniques. This report includes the advantages and disadvantages of different types of

budgetary tool and planning system. By making comparison of DELL with HP, effective

management accounting techniques are used so that organisation can work more better.

TASK 1

P1 Concept of management accounting system and their different types use in it

In management accounting, it consider all the know-how and idea which are useful to

make effectual preparation, choosing best alternatives among various alternatives which are best

fit for the organisation. To make effective decision in an organisation, all the information is

collected and classified as per such manner that such information can be used appropriately for

an organisation (Vosselman, 2014). Thus, to make effective decision in an organisation,

information is collected, classified and analysed by the manager.

Management accounting is essential for every organisation. Thus, DELL company use

various kinds of systems so that they can measure their performance, identify the risk and use

resources optimally. There are various kind of management accounting system, which are as

follows:

Batch costing: In this type of costing in which group of products and services are

produced which generated the cluster cost. Such cost is not easily identified and it is considered

as the best tool in which cost of batch is transferred to the individual while making the cost

accounting.

Process costing: This type of costing is suitable for those activity in which large number

of homogeneous products are produced by the organisation. In this method, cost of products is

identifying at each stage of production.

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Contract costing: This costing is used to identify the cost of product while making

contract with the customers. In this agreed party make a contract in which both parties are united

upon certain kind of compensate to the institution.

P2 Techniques which are essential for Management Accounting reporting

Cost Report: Cost report all the techniques which is used to calculate the cost of raw

material, labour and overheads. Hence, all this information are recorded in cost report which is a

summarized form, so that it will help the organisation for making effective planning and control

on profits.

Budgets: Budget is very essential of management accounting because by making the

budget organisation can forecast their future activities. It includes collection of all the income

and expenses, so that by analysis these information organisations can identify the future

condition in the market (van der Meer-Kooistra and Vosselman, 2012).

Performance report: In a performance report, it includes the variation between the actual

expenses and income in an organisation. It is a new form of budget, which help to analysis the

deviation in performance by the organisation.

Other reports: It includes all the additional information of organisational activity which

are used by the manager to make comparison of different activities which make positive as well

as negative impact on organisation.

M1 Benefits of Management Accounting Systems

Planning: Management accounting helps to prepare an effective plan for effective

operations which are used by the DELL company. To prepare and implement a plan, company

need to identify the objectives and as per decided objective effective planning helps to

accomplishes such goals and objectives.

Controlling: Management accounting system also help to make effective control on

various kinds of deviation which is generated from actual and standard performance. Through

this accounting methods it helps the DELL company to make effective control in each deviation.

Coordinating: DELL company also make effective coordination between various

departments by use of management accounting system. It makes effective coordination between

production, sales, finance etc. departments for effective functioning.

2

contract with the customers. In this agreed party make a contract in which both parties are united

upon certain kind of compensate to the institution.

P2 Techniques which are essential for Management Accounting reporting

Cost Report: Cost report all the techniques which is used to calculate the cost of raw

material, labour and overheads. Hence, all this information are recorded in cost report which is a

summarized form, so that it will help the organisation for making effective planning and control

on profits.

Budgets: Budget is very essential of management accounting because by making the

budget organisation can forecast their future activities. It includes collection of all the income

and expenses, so that by analysis these information organisations can identify the future

condition in the market (van der Meer-Kooistra and Vosselman, 2012).

Performance report: In a performance report, it includes the variation between the actual

expenses and income in an organisation. It is a new form of budget, which help to analysis the

deviation in performance by the organisation.

Other reports: It includes all the additional information of organisational activity which

are used by the manager to make comparison of different activities which make positive as well

as negative impact on organisation.

M1 Benefits of Management Accounting Systems

Planning: Management accounting helps to prepare an effective plan for effective

operations which are used by the DELL company. To prepare and implement a plan, company

need to identify the objectives and as per decided objective effective planning helps to

accomplishes such goals and objectives.

Controlling: Management accounting system also help to make effective control on

various kinds of deviation which is generated from actual and standard performance. Through

this accounting methods it helps the DELL company to make effective control in each deviation.

Coordinating: DELL company also make effective coordination between various

departments by use of management accounting system. It makes effective coordination between

production, sales, finance etc. departments for effective functioning.

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Improving the efficiency: Managerial accounting system also helps to improve the

efficiency of the workers as well the it also enhances the profitability and productivity of an

organisation.

Motivating: It is beneficial to motivate the workers as per determining the actual

performance and make a complete reports so that workers can be identified/ classified as per

their skills, capability. In this motivation in the form of monetary and non-monetary also make a

great impact on the employees’ performance level (Simons, 2013).

D1 Integration of Management Accounting System and Management Accounting Reporting

Organisation adopt the new system to perform better so that management accounting is

used by the company. If accounting techniques are used in an organisation so that reporting also

exist. Hence, both the term management accounting system and reporting are related to each

other. If DELL company use the management accounting system, managers of the company

prepare a report for making effective plan, decision and motivate to the employees. Hence, by

using management accounting system is used to make effective management accounting

reporting. By using these techniques, it gives the opportunities to the company to achieve the

competitive advantage by providing quality of services to the customers.

TASK 2

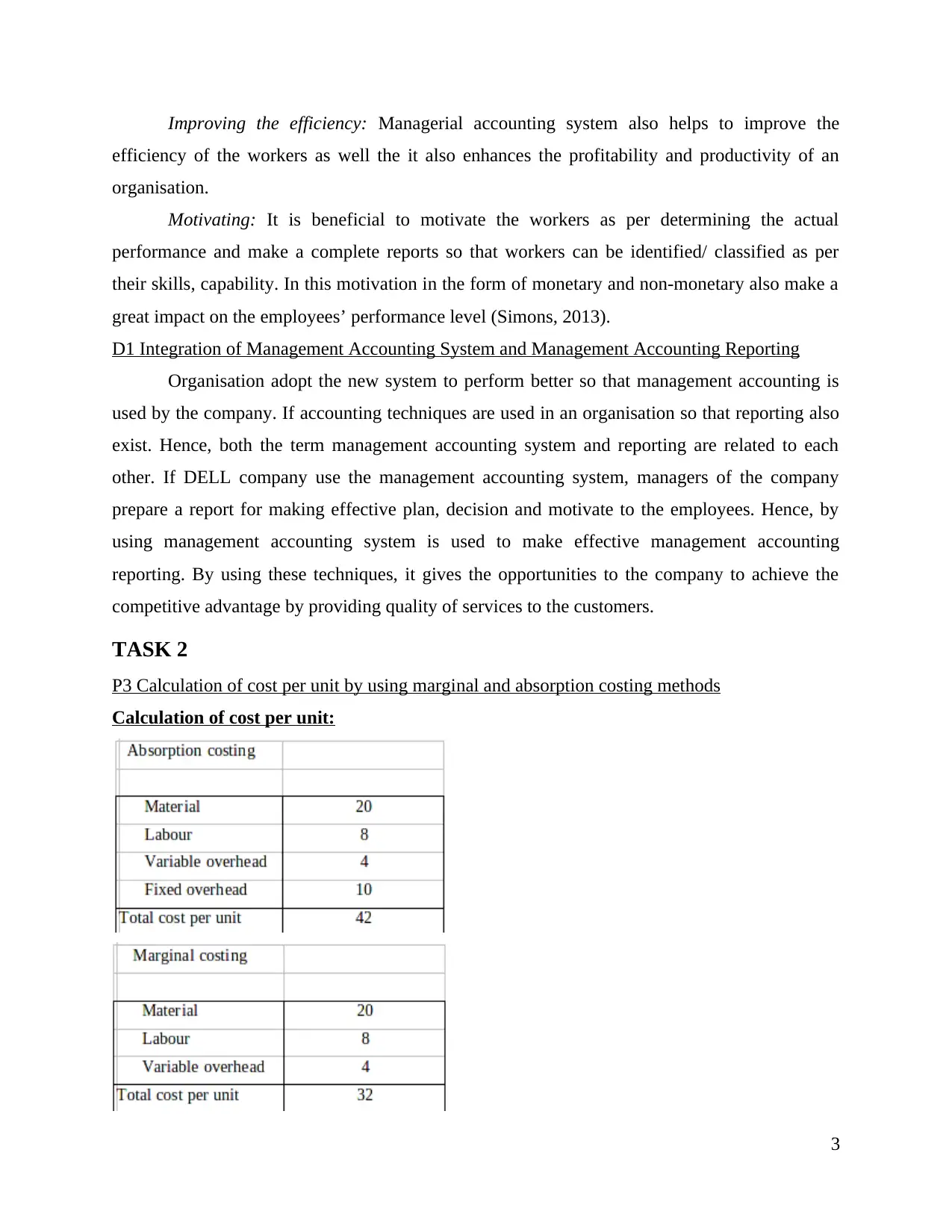

P3 Calculation of cost per unit by using marginal and absorption costing methods

Calculation of cost per unit:

3

efficiency of the workers as well the it also enhances the profitability and productivity of an

organisation.

Motivating: It is beneficial to motivate the workers as per determining the actual

performance and make a complete reports so that workers can be identified/ classified as per

their skills, capability. In this motivation in the form of monetary and non-monetary also make a

great impact on the employees’ performance level (Simons, 2013).

D1 Integration of Management Accounting System and Management Accounting Reporting

Organisation adopt the new system to perform better so that management accounting is

used by the company. If accounting techniques are used in an organisation so that reporting also

exist. Hence, both the term management accounting system and reporting are related to each

other. If DELL company use the management accounting system, managers of the company

prepare a report for making effective plan, decision and motivate to the employees. Hence, by

using management accounting system is used to make effective management accounting

reporting. By using these techniques, it gives the opportunities to the company to achieve the

competitive advantage by providing quality of services to the customers.

TASK 2

P3 Calculation of cost per unit by using marginal and absorption costing methods

Calculation of cost per unit:

3

To figure the cost of part, the results are different by using different method. The

different results are caused due to fixed overhead cost. Fixed overhead cost is a cost which

remain fixed, so that it is used in absorption costing while calculating cost of unit, but on the

other side, it is ignored in marginal costing techniques. While calculating the cost of unit by

absorption costing, it is considered as most suitable method because it includes all kinds of cost

which are generated in production activity. Hence, DELL company also calculate their cost of

unit by using absorption costing method. In this, the full value per unit is calculate by the overall

figure of unit which are produced while preparing an financial gain statements. By using both

methods cost of unit can be calculated:

Here, Total number of units produced = 5000 units

By using absorption costing method, it can be = 42 * 5000 = 2100000

By using marginal costing method, it can be = 32 * 50000= 1600000

By calculating the cost of unit by using absorption and marginal costing techniques, all

the amount is generated is to be deducted from the total sales amount, so that gross profit will be

calculated by this method. If in the question, opening and closing amount are not given then net

profit will be affected. As per the above computation, cost of product is 2100000 and 1600000

by using both the two methods. It is clear that by using the absorption costing the amount of cost

is higher than the amount which comes from marginal costing techniques. Hence, absorption

coasting techniques is considered as a suitable technique of calculating the cost for any kinds of

organisation.

4

different results are caused due to fixed overhead cost. Fixed overhead cost is a cost which

remain fixed, so that it is used in absorption costing while calculating cost of unit, but on the

other side, it is ignored in marginal costing techniques. While calculating the cost of unit by

absorption costing, it is considered as most suitable method because it includes all kinds of cost

which are generated in production activity. Hence, DELL company also calculate their cost of

unit by using absorption costing method. In this, the full value per unit is calculate by the overall

figure of unit which are produced while preparing an financial gain statements. By using both

methods cost of unit can be calculated:

Here, Total number of units produced = 5000 units

By using absorption costing method, it can be = 42 * 5000 = 2100000

By using marginal costing method, it can be = 32 * 50000= 1600000

By calculating the cost of unit by using absorption and marginal costing techniques, all

the amount is generated is to be deducted from the total sales amount, so that gross profit will be

calculated by this method. If in the question, opening and closing amount are not given then net

profit will be affected. As per the above computation, cost of product is 2100000 and 1600000

by using both the two methods. It is clear that by using the absorption costing the amount of cost

is higher than the amount which comes from marginal costing techniques. Hence, absorption

coasting techniques is considered as a suitable technique of calculating the cost for any kinds of

organisation.

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

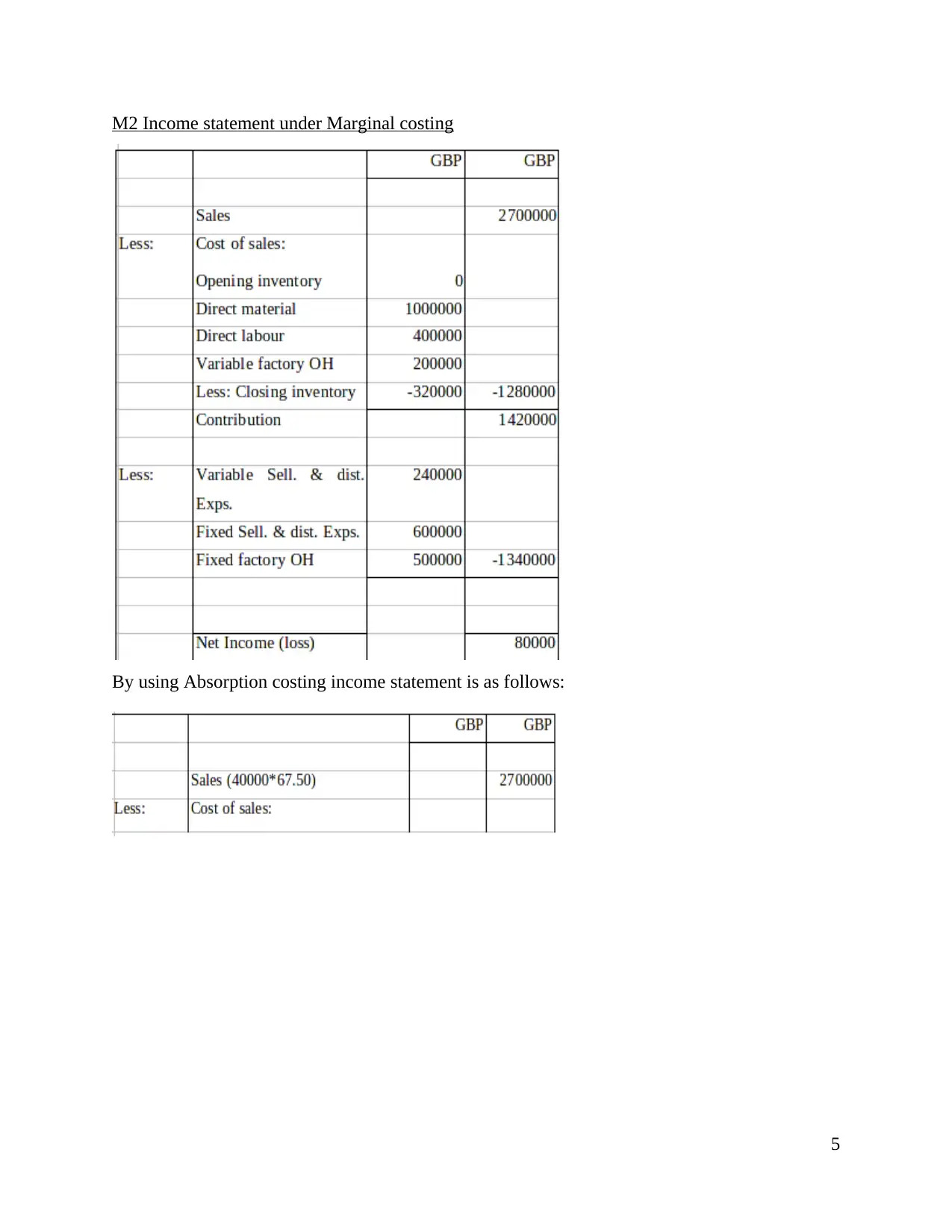

M2 Income statement under Marginal costing

By using Absorption costing income statement is as follows:

5

By using Absorption costing income statement is as follows:

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

D2 Financial report

To

Managing Director

DELL Company

Date: 15 June 2017

Subject: Data are accurately implemented by using the costing techniques.

By using both of two methods like absorption costing and marginal costing techniques cost per

unit can be calculated. By using such two methods, the results are occurring differently. As per

above, gross profit is higher by using the marginal costing techniques whereas, on the opposite

side net profit of a company is lower by using the absorption costing techniques. There is

variation of changes can be done because of the use of fixed manufacturing overhead. In

absorption costing techniques, fixed overhead is taken while making the computation, but in

marginal costing fixed overhead does not take while making the computation. In this way, by

using different techniques there will be fraction changes in the company's net profit and gross

profit. It can be said that, absorption costing method is suitable for the DELL company and

company should continue with this method for achieving the growth.

Truly,

6

To

Managing Director

DELL Company

Date: 15 June 2017

Subject: Data are accurately implemented by using the costing techniques.

By using both of two methods like absorption costing and marginal costing techniques cost per

unit can be calculated. By using such two methods, the results are occurring differently. As per

above, gross profit is higher by using the marginal costing techniques whereas, on the opposite

side net profit of a company is lower by using the absorption costing techniques. There is

variation of changes can be done because of the use of fixed manufacturing overhead. In

absorption costing techniques, fixed overhead is taken while making the computation, but in

marginal costing fixed overhead does not take while making the computation. In this way, by

using different techniques there will be fraction changes in the company's net profit and gross

profit. It can be said that, absorption costing method is suitable for the DELL company and

company should continue with this method for achieving the growth.

Truly,

6

Management Accountant

TASK 3

P4 Advantages and Disadvantages of budgetary control

Budgetary control is a technique, in which it is examined that how a manager can make

effective control in budget. It includes effective planning of budget, so that manager can utilize

the budget appropriately. It also includes the complete monitoring process which are performed

by the manager to check that budgets are allocate in different department appropriately or not.

Hence, by making effective budgetary control, manager can take effective decision and make

effective control in each operational activity.

Merits of Budgetary Control

Definite planning: Budget are based on the definite plan which help the manager to

estimate the actual earning and after that goals can be accomplished.

Enhanced efficiency: By making effective control on budget also helps to increase the

efficiency and also promote the economy (Siegel, 2010).

Proper communication: Budgets are prepared so that after making the budget funds are

allocate appropriately. In addition to this, budgets are constructed by making consultation in

different departments. In this way, it creates a proper communication facility between the staff

members and employers.

Control: By making comparison between actual and standard performance budgeting

make full control in firm's activities.

Co-ordination: By making effective control on budgets helps to make effective

coordination among various departments like production, sales etc.

Delegation of Authority: Budgeting also encourage the delegation of authority and set the

budgets limit by making effective judgement in an organisation.

Motivation: Budgets also provides incentives to the workers, so that by making effective

control in budget helps to motivate the employees.

Maximisation of profit: To make effective control on budget helps to maximize the

profits so that such profits can be used in future.

Forecasting credit needs: By making budgets it helps to determine the need of cash in

various department so that future goals of an organisation can be fulfilled.

7

TASK 3

P4 Advantages and Disadvantages of budgetary control

Budgetary control is a technique, in which it is examined that how a manager can make

effective control in budget. It includes effective planning of budget, so that manager can utilize

the budget appropriately. It also includes the complete monitoring process which are performed

by the manager to check that budgets are allocate in different department appropriately or not.

Hence, by making effective budgetary control, manager can take effective decision and make

effective control in each operational activity.

Merits of Budgetary Control

Definite planning: Budget are based on the definite plan which help the manager to

estimate the actual earning and after that goals can be accomplished.

Enhanced efficiency: By making effective control on budget also helps to increase the

efficiency and also promote the economy (Siegel, 2010).

Proper communication: Budgets are prepared so that after making the budget funds are

allocate appropriately. In addition to this, budgets are constructed by making consultation in

different departments. In this way, it creates a proper communication facility between the staff

members and employers.

Control: By making comparison between actual and standard performance budgeting

make full control in firm's activities.

Co-ordination: By making effective control on budgets helps to make effective

coordination among various departments like production, sales etc.

Delegation of Authority: Budgeting also encourage the delegation of authority and set the

budgets limit by making effective judgement in an organisation.

Motivation: Budgets also provides incentives to the workers, so that by making effective

control in budget helps to motivate the employees.

Maximisation of profit: To make effective control on budget helps to maximize the

profits so that such profits can be used in future.

Forecasting credit needs: By making budgets it helps to determine the need of cash in

various department so that future goals of an organisation can be fulfilled.

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Uniform policy: To make control ion budget is known as uniform policy because this

technique is used in various departments (Parker, 2012).

Demerits of Budgetary Control

It makes negative impact on relations with labours because budgets are mainly focus on

workforce so that it makes high pressure to the workers by the top-level management.

There is less chances to motivate the employees because pressure make wrong impact in

the recording of data.

By allocating the funds inappropriately it makes conflicts and create a competitive

position in a various department.

It only uses historical analysis while comparing the current costs with estimated cost.

While making a budgetary control, there will be a chance of uncertainty in various

departments like demand of the cash, weather, competition, inflation, techniques etc.

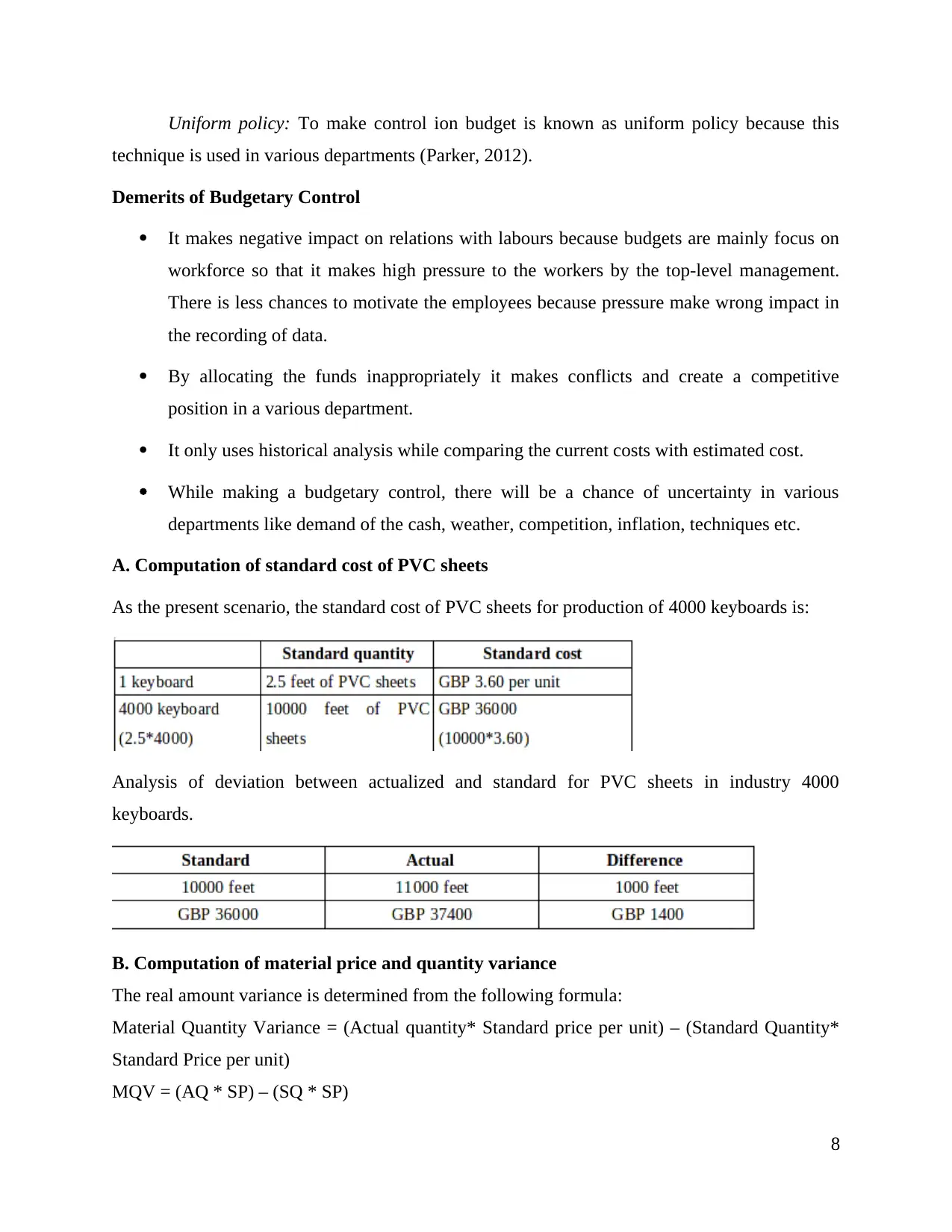

A. Computation of standard cost of PVC sheets

As the present scenario, the standard cost of PVC sheets for production of 4000 keyboards is:

Analysis of deviation between actualized and standard for PVC sheets in industry 4000

keyboards.

B. Computation of material price and quantity variance

The real amount variance is determined from the following formula:

Material Quantity Variance = (Actual quantity* Standard price per unit) – (Standard Quantity*

Standard Price per unit)

MQV = (AQ * SP) – (SQ * SP)

8

technique is used in various departments (Parker, 2012).

Demerits of Budgetary Control

It makes negative impact on relations with labours because budgets are mainly focus on

workforce so that it makes high pressure to the workers by the top-level management.

There is less chances to motivate the employees because pressure make wrong impact in

the recording of data.

By allocating the funds inappropriately it makes conflicts and create a competitive

position in a various department.

It only uses historical analysis while comparing the current costs with estimated cost.

While making a budgetary control, there will be a chance of uncertainty in various

departments like demand of the cash, weather, competition, inflation, techniques etc.

A. Computation of standard cost of PVC sheets

As the present scenario, the standard cost of PVC sheets for production of 4000 keyboards is:

Analysis of deviation between actualized and standard for PVC sheets in industry 4000

keyboards.

B. Computation of material price and quantity variance

The real amount variance is determined from the following formula:

Material Quantity Variance = (Actual quantity* Standard price per unit) – (Standard Quantity*

Standard Price per unit)

MQV = (AQ * SP) – (SQ * SP)

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

= (11000 * 3.60) – (10000 * 3.60)

= 3600

The physical cost deviation is ascertained from the following formula:

Material Price Variance = (Actual quantity* Actual price per unit) – (Actual quantity* Standard

price per unit)

= (11000* 3.40) – (11000* 3.60)

= 37400 – 39600

= -2200

M3 Usage of planning tool's applidcation

For fixing a budget of DELL company, there are various kinds of planning tools which

help to make effective forecasting of budgets, which are as follows:

Material price and usage variances: This concentration on value and use of real. The outcome

is adverse in the status of affirmative response and it is approving if the response is antagonistic

(Modell, 2010).

Physical value deviation – The deviation between standardized outgo and the existent

cost for the real amount of acquisition physical is to be statement as substantial price

deviation. The expression is:

Material price variance= (Actual quantity* Actual price per unit) – (Actual quantity* Standard

price per unit)

Material usage variance – It is to be ascertained by characteristic the divergence between

standardized amount of physical and actualized amount of physical utilized.

Material usage variance= (Actual quantity* Standard price per unit) – (Standard Quantity*

Standard Price per unit)

Labour rate and efficiency variances: It mainly concentration on revenue enhancement and

work time of labour (Macintosh and Quattrone, 2010.). The affirmative outcome is adverse and

counter effect is approximative

Working class rate variance – This is measured by calculating the deviation between

actualised work time increased by the existent charge per unit and actualized work time

multiplied by the standardized rate.

9

= 3600

The physical cost deviation is ascertained from the following formula:

Material Price Variance = (Actual quantity* Actual price per unit) – (Actual quantity* Standard

price per unit)

= (11000* 3.40) – (11000* 3.60)

= 37400 – 39600

= -2200

M3 Usage of planning tool's applidcation

For fixing a budget of DELL company, there are various kinds of planning tools which

help to make effective forecasting of budgets, which are as follows:

Material price and usage variances: This concentration on value and use of real. The outcome

is adverse in the status of affirmative response and it is approving if the response is antagonistic

(Modell, 2010).

Physical value deviation – The deviation between standardized outgo and the existent

cost for the real amount of acquisition physical is to be statement as substantial price

deviation. The expression is:

Material price variance= (Actual quantity* Actual price per unit) – (Actual quantity* Standard

price per unit)

Material usage variance – It is to be ascertained by characteristic the divergence between

standardized amount of physical and actualized amount of physical utilized.

Material usage variance= (Actual quantity* Standard price per unit) – (Standard Quantity*

Standard Price per unit)

Labour rate and efficiency variances: It mainly concentration on revenue enhancement and

work time of labour (Macintosh and Quattrone, 2010.). The affirmative outcome is adverse and

counter effect is approximative

Working class rate variance – This is measured by calculating the deviation between

actualised work time increased by the existent charge per unit and actualized work time

multiplied by the standardized rate.

9

Labour rate variance= (Actual hours*Actual rate per hour) – (Actual hour * Standard rate per

hour)

Labour ratio variance – This deviation calculates the deviation between actualized period

of time and modular unit of time calculate by the modular rates.

Labour efficiency variance= (Actual hours*Standard rate per hour) – (Standard hours*Standard

rate per hour)

By calculating discrepancy, DELL can determine the deviant and capable to take disciplinary act

if required for the administration.

D3 Use of planning tools for solving financial problems

Activity Based Budgeting: This technique helps to calculate the income which are created

from research activity. With help of ABC techniques, DELL company can divide the cost of

overhead so that it can reduce the wastage of cost which are unnecessary done by the company.

Balanced Score Cards: BSC is a framework which are used in identify and manage the

strategies of an organisation. In this, two indicators are used by the organisation like leading and

lagging. Such indicators help the company to determine their goals which are accomplished or

not and they also synthesis the right way to increase their profits.

Value chain Analysis: To identify the internal activities value chain analysis can be

applied by the organisation. By using this, company can determine that which activity is best for

the organisation. Hence, by analysing the value chain company can creates the value for the

customers and also maximise their profits (Kaplan and Atkinson, 2015).

TASK 4

P5 Examination with the challenger for choosing management accounting system

DELL HP

1. For taking the advantage of competitive

position and improving their core

competencies DELL company uses the

management accounting system.

2. There are various kind of planning tools

which are used to determine the opportunities

of success in the external environment.

1. The working style of HP is different from

DELL company but company also use the

management accounting techniques.

2. To calculate the profits company also use

marginal costing techniques.

3. Report of the company also examined the

effectual situation and interpret the plan as per

10

hour)

Labour ratio variance – This deviation calculates the deviation between actualized period

of time and modular unit of time calculate by the modular rates.

Labour efficiency variance= (Actual hours*Standard rate per hour) – (Standard hours*Standard

rate per hour)

By calculating discrepancy, DELL can determine the deviant and capable to take disciplinary act

if required for the administration.

D3 Use of planning tools for solving financial problems

Activity Based Budgeting: This technique helps to calculate the income which are created

from research activity. With help of ABC techniques, DELL company can divide the cost of

overhead so that it can reduce the wastage of cost which are unnecessary done by the company.

Balanced Score Cards: BSC is a framework which are used in identify and manage the

strategies of an organisation. In this, two indicators are used by the organisation like leading and

lagging. Such indicators help the company to determine their goals which are accomplished or

not and they also synthesis the right way to increase their profits.

Value chain Analysis: To identify the internal activities value chain analysis can be

applied by the organisation. By using this, company can determine that which activity is best for

the organisation. Hence, by analysing the value chain company can creates the value for the

customers and also maximise their profits (Kaplan and Atkinson, 2015).

TASK 4

P5 Examination with the challenger for choosing management accounting system

DELL HP

1. For taking the advantage of competitive

position and improving their core

competencies DELL company uses the

management accounting system.

2. There are various kind of planning tools

which are used to determine the opportunities

of success in the external environment.

1. The working style of HP is different from

DELL company but company also use the

management accounting techniques.

2. To calculate the profits company also use

marginal costing techniques.

3. Report of the company also examined the

effectual situation and interpret the plan as per

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.