CX554001 Assignment 3: Financial Analysis of Handles Plus (2016-2018)

VerifiedAdded on 2023/06/03

|14

|2561

|429

Homework Assignment

AI Summary

This assignment analyzes the financial performance of Handles Plus, a sole proprietorship selling door handles in Auckland, using financial statement analysis and ratio analysis techniques. The report examines profitability (gross profit margin, net profit margin, and return on equity), financial stability (current ratio, quick ratio, and equity ratio), and asset utilization efficiency (inventory turnover and debtor turnover). It calculates financial ratios for the years 2016, 2017, and 2018 and compares them with industry averages. The assignment also includes budgeting, variance analysis, and CVP (Cost-Volume-Profit) analysis to assess the company's financial health and make recommendations for improvement. Key areas of focus include working capital management, trade credit policies, inventory management, and debt reduction.

Running Head: Financial Statement Analysis

Financial Management

Financial Management

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Financial Statement Analysis 1

Introduction:

The basic objective of this report is to provide insights about the financial performance of

Handles Plus which is a sole proprietorship firm. The firm is engaged in the business of

selling door handles in East Tamaki, Auckland. Financial analysis of Handles Plus is carried

using the key technique of financial management, Ratio analysis. As a part of ratio analysis

various ratios in relation to entity’s financial statements for the years 2016, 2017 and 2018

are calculated and the results of firm’s financial ratios are compared with the industry ratios

so as to determine the financial position of Handle Plus’s business in the market. Financial

performance has been analysed using different aspects such as profitability position, financial

stability and asset utilisation efficiency. On the basis of the financial results derived from the

use of ratio analysis tool various recommendations have been made to improve the financial

health in the subsequent periods of the business so as to enable it to achieve the competitive

edge in the market.

Financial analysis:

Part a

A financial analysis can be undertaken on both inter-firm and intra-firm basis. Under inter-

firm basis the financial results of the firm are compared with its competitor’s results or with

the average results of all the firms operating within the same or similar industry. However, in

intra-firm’s financial analysis, the financial results achieved in one period by the firm are

compared with that of other year’s results so as to assess whether the financial performance

of the business has improved or degraded over the last few years.

Part b: Analysis of profitability of the business:

2016 2017 2018 Industr

Introduction:

The basic objective of this report is to provide insights about the financial performance of

Handles Plus which is a sole proprietorship firm. The firm is engaged in the business of

selling door handles in East Tamaki, Auckland. Financial analysis of Handles Plus is carried

using the key technique of financial management, Ratio analysis. As a part of ratio analysis

various ratios in relation to entity’s financial statements for the years 2016, 2017 and 2018

are calculated and the results of firm’s financial ratios are compared with the industry ratios

so as to determine the financial position of Handle Plus’s business in the market. Financial

performance has been analysed using different aspects such as profitability position, financial

stability and asset utilisation efficiency. On the basis of the financial results derived from the

use of ratio analysis tool various recommendations have been made to improve the financial

health in the subsequent periods of the business so as to enable it to achieve the competitive

edge in the market.

Financial analysis:

Part a

A financial analysis can be undertaken on both inter-firm and intra-firm basis. Under inter-

firm basis the financial results of the firm are compared with its competitor’s results or with

the average results of all the firms operating within the same or similar industry. However, in

intra-firm’s financial analysis, the financial results achieved in one period by the firm are

compared with that of other year’s results so as to assess whether the financial performance

of the business has improved or degraded over the last few years.

Part b: Analysis of profitability of the business:

2016 2017 2018 Industr

Financial Statement Analysis 2

y

Gross Profit Margin Gross Profit / Sales 60.50% 61.73% 68.00% 65%

Net profit Margin EBIT/ Sales 0.53% 14.34% 28.89% 20.68%

Return on equity Net profit after/Average

shareholder's equity -1.79% 10.93% 46.16% 38.98%

The profitability business of the firm is achieved when it has sufficient amount of earnings

left after meeting all the business expenses and costs. The profitability of the business can be

analysed using various ratios such as gross profit ratio, net profit ratio and the return on

equity (Penman & Penman, 2007). The gross profit ratio of the firm is showing an increasing

trend since 2016 till 2018. The reason for the increase in the gross margin of the business of

Handle Plus is its increasing sales. In 2018, the firm has also beaten the industry average and

hence its profitability position in terms of gross profit margin can be said as sound. Further,

with the increasing market share the net margin of the business of Handles Plus is also

improving. In 2016, the net losses were reported as result of normal business operations of

the firm. However, the net margin ratio has improved significantly in the subsequent periods

i.e. 2017 and 2018. The increasing trend in the net profit margin reflects the improving

profitability state of the business and as a result of this Handles Plus has even outperformed

the average industry performance. The return on equity ratio shows the quantum of profits

earned by the firm for its shareholders. It reflects the returns offered to the shareholders in

consideration of the investments made by them in the firm to provide it required financial

assistance (Zimmerman & Yahya-Zadeh, 2011). The ROE has continuously improved over

the last three financial years and also Handles Plus has crossed the average industry

benchmarks.

Part c: Analysis of financial stability position of business:

y

Gross Profit Margin Gross Profit / Sales 60.50% 61.73% 68.00% 65%

Net profit Margin EBIT/ Sales 0.53% 14.34% 28.89% 20.68%

Return on equity Net profit after/Average

shareholder's equity -1.79% 10.93% 46.16% 38.98%

The profitability business of the firm is achieved when it has sufficient amount of earnings

left after meeting all the business expenses and costs. The profitability of the business can be

analysed using various ratios such as gross profit ratio, net profit ratio and the return on

equity (Penman & Penman, 2007). The gross profit ratio of the firm is showing an increasing

trend since 2016 till 2018. The reason for the increase in the gross margin of the business of

Handle Plus is its increasing sales. In 2018, the firm has also beaten the industry average and

hence its profitability position in terms of gross profit margin can be said as sound. Further,

with the increasing market share the net margin of the business of Handles Plus is also

improving. In 2016, the net losses were reported as result of normal business operations of

the firm. However, the net margin ratio has improved significantly in the subsequent periods

i.e. 2017 and 2018. The increasing trend in the net profit margin reflects the improving

profitability state of the business and as a result of this Handles Plus has even outperformed

the average industry performance. The return on equity ratio shows the quantum of profits

earned by the firm for its shareholders. It reflects the returns offered to the shareholders in

consideration of the investments made by them in the firm to provide it required financial

assistance (Zimmerman & Yahya-Zadeh, 2011). The ROE has continuously improved over

the last three financial years and also Handles Plus has crossed the average industry

benchmarks.

Part c: Analysis of financial stability position of business:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

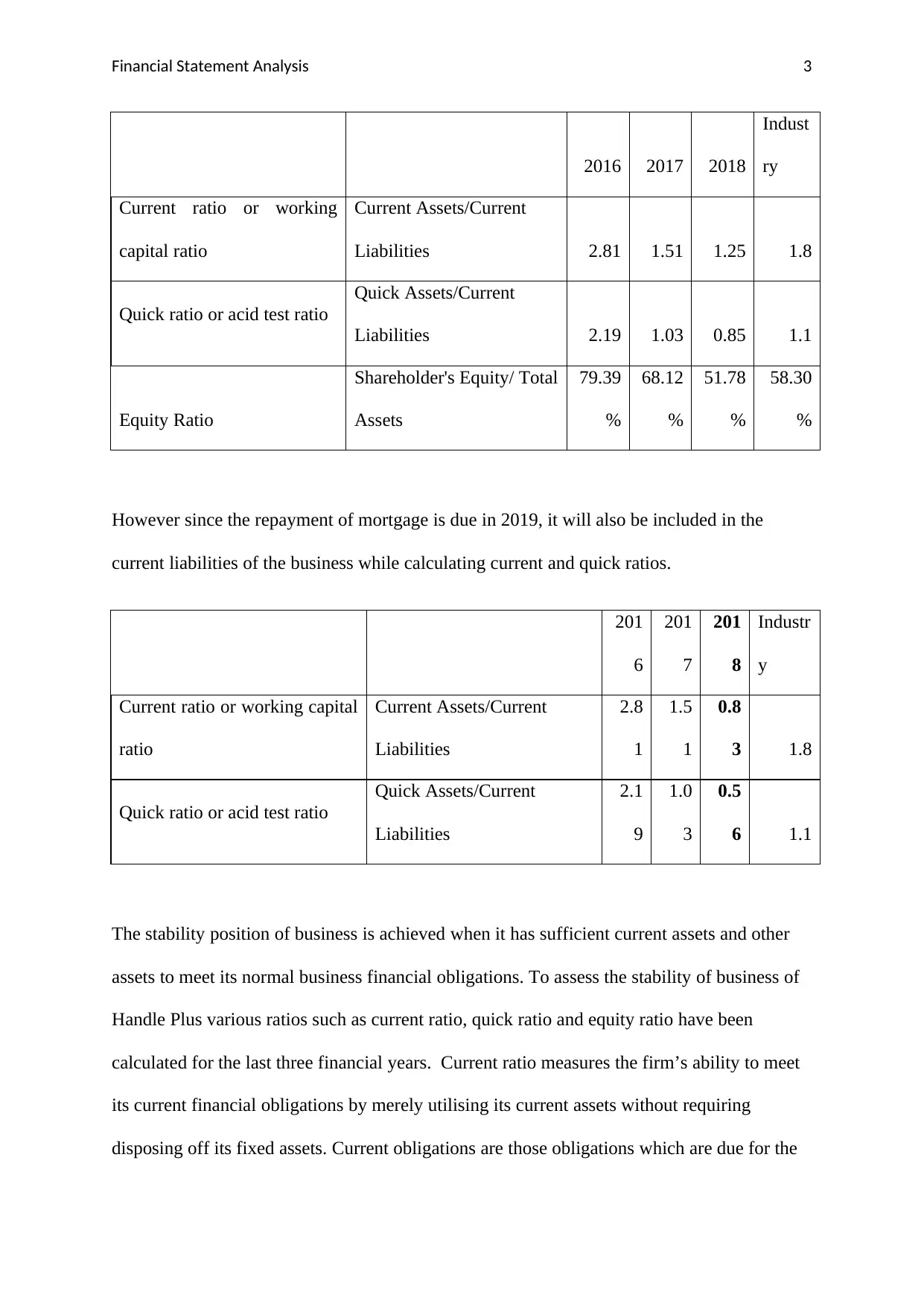

Financial Statement Analysis 3

2016 2017 2018

Indust

ry

Current ratio or working

capital ratio

Current Assets/Current

Liabilities 2.81 1.51 1.25 1.8

Quick ratio or acid test ratio

Quick Assets/Current

Liabilities 2.19 1.03 0.85 1.1

Equity Ratio

Shareholder's Equity/ Total

Assets

79.39

%

68.12

%

51.78

%

58.30

%

However since the repayment of mortgage is due in 2019, it will also be included in the

current liabilities of the business while calculating current and quick ratios.

201

6

201

7

201

8

Industr

y

Current ratio or working capital

ratio

Current Assets/Current

Liabilities

2.8

1

1.5

1

0.8

3 1.8

Quick ratio or acid test ratio

Quick Assets/Current

Liabilities

2.1

9

1.0

3

0.5

6 1.1

The stability position of business is achieved when it has sufficient current assets and other

assets to meet its normal business financial obligations. To assess the stability of business of

Handle Plus various ratios such as current ratio, quick ratio and equity ratio have been

calculated for the last three financial years. Current ratio measures the firm’s ability to meet

its current financial obligations by merely utilising its current assets without requiring

disposing off its fixed assets. Current obligations are those obligations which are due for the

2016 2017 2018

Indust

ry

Current ratio or working

capital ratio

Current Assets/Current

Liabilities 2.81 1.51 1.25 1.8

Quick ratio or acid test ratio

Quick Assets/Current

Liabilities 2.19 1.03 0.85 1.1

Equity Ratio

Shareholder's Equity/ Total

Assets

79.39

%

68.12

%

51.78

%

58.30

%

However since the repayment of mortgage is due in 2019, it will also be included in the

current liabilities of the business while calculating current and quick ratios.

201

6

201

7

201

8

Industr

y

Current ratio or working capital

ratio

Current Assets/Current

Liabilities

2.8

1

1.5

1

0.8

3 1.8

Quick ratio or acid test ratio

Quick Assets/Current

Liabilities

2.1

9

1.0

3

0.5

6 1.1

The stability position of business is achieved when it has sufficient current assets and other

assets to meet its normal business financial obligations. To assess the stability of business of

Handle Plus various ratios such as current ratio, quick ratio and equity ratio have been

calculated for the last three financial years. Current ratio measures the firm’s ability to meet

its current financial obligations by merely utilising its current assets without requiring

disposing off its fixed assets. Current obligations are those obligations which are due for the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Financial Statement Analysis 4

payment within the next one year. The ideal current ratio is generally considered at 2:1

(Higgins, 2012). In 2016, the business of Handle Plus enjoyed strong liquidity position but

after that the liquidity position of the business has declined and in 2018 the firm could not

even meet the average industry standards. Although the balance of current assets has

increased over the last 3 years but at the same time the balance of current liabilities has also

increased significantly which has tightened the liquidity position of the business of Handle

Plus. Further, the results of quick ratio show that there is lack of such currents assets in the

business which can easily be convertible into cash as and when required to meet the current

liabilities. The liquidity position of business was satisfactory till 2017 but after that the firm is

facing high instability in terms of its liquidity state. The equity ratio is the good indicator of

financial leverage faced by the business (Huang, et. al., 2004). It shows the quantum of total

assets that are financed using the equity sources as against the debt financing. The equity

ratio of Handle Plus had continuously declined over the last three financial years. This

indicates that the firm is facing more financial risk in the years that are ahead of 2016.

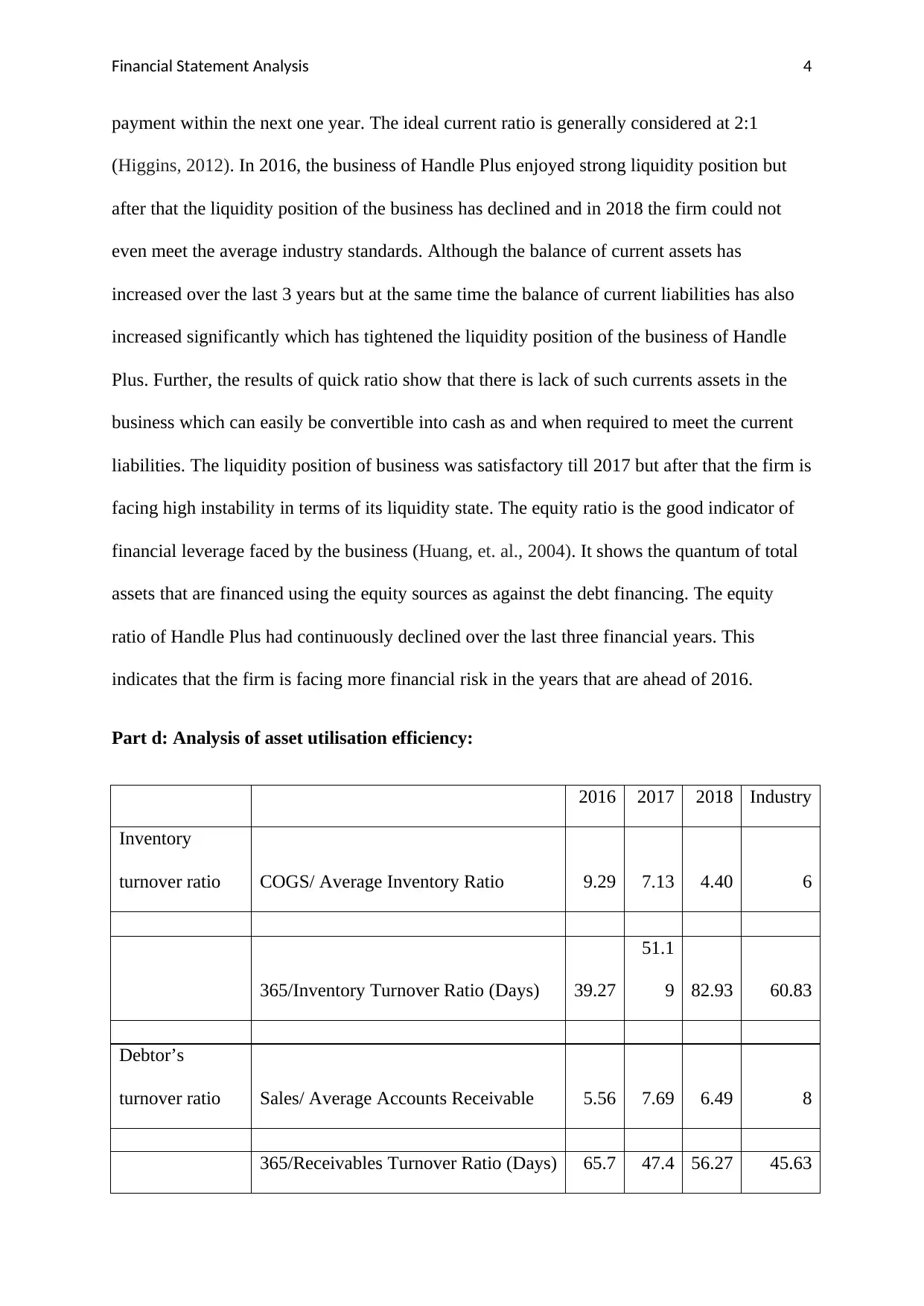

Part d: Analysis of asset utilisation efficiency:

2016 2017 2018 Industry

Inventory

turnover ratio COGS/ Average Inventory Ratio 9.29 7.13 4.40 6

365/Inventory Turnover Ratio (Days) 39.27

51.1

9 82.93 60.83

Debtor’s

turnover ratio Sales/ Average Accounts Receivable 5.56 7.69 6.49 8

365/Receivables Turnover Ratio (Days) 65.7 47.4 56.27 45.63

payment within the next one year. The ideal current ratio is generally considered at 2:1

(Higgins, 2012). In 2016, the business of Handle Plus enjoyed strong liquidity position but

after that the liquidity position of the business has declined and in 2018 the firm could not

even meet the average industry standards. Although the balance of current assets has

increased over the last 3 years but at the same time the balance of current liabilities has also

increased significantly which has tightened the liquidity position of the business of Handle

Plus. Further, the results of quick ratio show that there is lack of such currents assets in the

business which can easily be convertible into cash as and when required to meet the current

liabilities. The liquidity position of business was satisfactory till 2017 but after that the firm is

facing high instability in terms of its liquidity state. The equity ratio is the good indicator of

financial leverage faced by the business (Huang, et. al., 2004). It shows the quantum of total

assets that are financed using the equity sources as against the debt financing. The equity

ratio of Handle Plus had continuously declined over the last three financial years. This

indicates that the firm is facing more financial risk in the years that are ahead of 2016.

Part d: Analysis of asset utilisation efficiency:

2016 2017 2018 Industry

Inventory

turnover ratio COGS/ Average Inventory Ratio 9.29 7.13 4.40 6

365/Inventory Turnover Ratio (Days) 39.27

51.1

9 82.93 60.83

Debtor’s

turnover ratio Sales/ Average Accounts Receivable 5.56 7.69 6.49 8

365/Receivables Turnover Ratio (Days) 65.7 47.4 56.27 45.63

Financial Statement Analysis 5

5

The inventory turnover ratio shows the number of days taken by the business to convert its

inventory into sales (Higgins, 2012). There is an increasing trend in the inventory turnover

period over the last 3 reported years. The increasing number of days of inventory turnover

shows that Handle Plus is inefficiently managing their inventory holding which is resulting in

prolonged duration of conversion of inventory into sales. In 2016 and 2017, the firm could

meet the average industry benchmarks in respect of inventory turnover but in 2018, it could

not even meet the industry targets. Further, Debtor turnover ratio in days measures the time

taken by business to turn down its trade receivables to the cash. The receivable turnover is

fluctuating over the last 3 years but it was always higher than the average industry ratio in

this respect. It clearly reflects that firm is not maintaining its cash cycle properly (Foster,

2004).

Recommendations:

Handle plus must improve its working capital management practices by making

further investments in current assets to meet the short term financial obligations of the

business.

It must design such trade credit policies which could encourage the trade customers of

the business to pay-off for the purchases made from the firm.

Further, the inventory management practices must be improved by implementing Just

in Time technique so as to control the cost of inventory holdings.

The proportion of debt must be reduced from the capital structure of the company so

as to reduce the risk of financial insolvency of the business.

Conclusion:

5

The inventory turnover ratio shows the number of days taken by the business to convert its

inventory into sales (Higgins, 2012). There is an increasing trend in the inventory turnover

period over the last 3 reported years. The increasing number of days of inventory turnover

shows that Handle Plus is inefficiently managing their inventory holding which is resulting in

prolonged duration of conversion of inventory into sales. In 2016 and 2017, the firm could

meet the average industry benchmarks in respect of inventory turnover but in 2018, it could

not even meet the industry targets. Further, Debtor turnover ratio in days measures the time

taken by business to turn down its trade receivables to the cash. The receivable turnover is

fluctuating over the last 3 years but it was always higher than the average industry ratio in

this respect. It clearly reflects that firm is not maintaining its cash cycle properly (Foster,

2004).

Recommendations:

Handle plus must improve its working capital management practices by making

further investments in current assets to meet the short term financial obligations of the

business.

It must design such trade credit policies which could encourage the trade customers of

the business to pay-off for the purchases made from the firm.

Further, the inventory management practices must be improved by implementing Just

in Time technique so as to control the cost of inventory holdings.

The proportion of debt must be reduced from the capital structure of the company so

as to reduce the risk of financial insolvency of the business.

Conclusion:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Financial Statement Analysis 6

The above report can be concluded with the main points that Handle Plus has sound

profitability position but it does not have strong financial stability in the market because of

liquidity crunch and also it can be said that the firm is not managing its assets efficiently

which is resulting in disturbed cash cycle for its business.

Apart from ratio analysis, the other advanced techniques of management accounting have

such as variance analysis and customer profitability analysis also been used to assess the

financial performance of the business.

Requirement 2: Preparation of Budgets

Budgeted

Amount in

$

Sales 656250

Cost of Goods Sold 251125

Gross Profit 405125

Selling Expenses

Sales Bonus and

Delivery 24500

Advertisement 65625 90125

Administration

Expenses

Wages and others 183862.125

Insurance 14000

197862.12

5

Financial Expenses

Bad Debts 16800

Interest 19268 36068

Profit 81069.875

Requirement 3: Variance analysis:

Part a and b

Amount in $

The above report can be concluded with the main points that Handle Plus has sound

profitability position but it does not have strong financial stability in the market because of

liquidity crunch and also it can be said that the firm is not managing its assets efficiently

which is resulting in disturbed cash cycle for its business.

Apart from ratio analysis, the other advanced techniques of management accounting have

such as variance analysis and customer profitability analysis also been used to assess the

financial performance of the business.

Requirement 2: Preparation of Budgets

Budgeted

Amount in

$

Sales 656250

Cost of Goods Sold 251125

Gross Profit 405125

Selling Expenses

Sales Bonus and

Delivery 24500

Advertisement 65625 90125

Administration

Expenses

Wages and others 183862.125

Insurance 14000

197862.12

5

Financial Expenses

Bad Debts 16800

Interest 19268 36068

Profit 81069.875

Requirement 3: Variance analysis:

Part a and b

Amount in $

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Financial Statement Analysis 7

Budgete

d Actual

Varianc

es

Varianc

es as a

percent

age

Sales 656250

84000

0 183750 F

Cost of

Goods

Sold 251125

26880

0 17675 U 28%

Gross

Profit

40512

5 571200 166075 7.04% 41%

Selling

Expenses

Sales

Bonus and

Delivery 24500 29400 4900 U

Advertise

ment 65625 90125 70000 99400 4375 9275 U 20.00% 10%

6.67%

Administr

ation

Expenses

Wages and

others

183862.

125

16476

3

-

19099.

1 F

Insurance 14000

19786

2.125 14000 178763 0 -19099.1

-

10.39%

-

9.65%

0.00%

Financial

Expenses

Bad Debts 16800 50400 33600 U

Interest 19268 36068 28088 78488 8820 42420 U

200.00

%

117.6

1%

45.78%

Profit

81069.

875 214549 133479.1 F

164.6

5%

Workings:

Results Calculations

Cost of Goods Sold % 38.27% 200900/525000

Sales bonus and

delivery % 3.73% 19600/525000

Wages and others

Fixed 81716.5 163433*50%

Budgete

d Actual

Varianc

es

Varianc

es as a

percent

age

Sales 656250

84000

0 183750 F

Cost of

Goods

Sold 251125

26880

0 17675 U 28%

Gross

Profit

40512

5 571200 166075 7.04% 41%

Selling

Expenses

Sales

Bonus and

Delivery 24500 29400 4900 U

Advertise

ment 65625 90125 70000 99400 4375 9275 U 20.00% 10%

6.67%

Administr

ation

Expenses

Wages and

others

183862.

125

16476

3

-

19099.

1 F

Insurance 14000

19786

2.125 14000 178763 0 -19099.1

-

10.39%

-

9.65%

0.00%

Financial

Expenses

Bad Debts 16800 50400 33600 U

Interest 19268 36068 28088 78488 8820 42420 U

200.00

%

117.6

1%

45.78%

Profit

81069.

875 214549 133479.1 F

164.6

5%

Workings:

Results Calculations

Cost of Goods Sold % 38.27% 200900/525000

Sales bonus and

delivery % 3.73% 19600/525000

Wages and others

Fixed 81716.5 163433*50%

Financial Statement Analysis 8

Variable 15.57% 81716.5/525000

Variable portion 102145.625 656250*15.57%

Total Wages 183862.125

81716.5+102145.6

3

Part c

The variance analysis has shown that the actual performance of the business and its budgeted

performance did not match and there are some instances where positive (favorable) variations

are reported but in certain areas, negative variances (unfavorable) are reported. When the

actual cost of the business exceeds the budgeted cost, then negative variances are reported but

when the lesser cost is actually incurred than the budgeted cost then favorable variances are

reported. The situation is vice-versa in case of profits or incomes of business. The two major

areas where investigation is required are:

Bad debts: As there is no increase in the bad debts even with the increase in sales.

Interest: As the financing cost of the business did not increase with the widened

business operations and increased debt structure of business.

Requirement 4: CVP Analysis

Part a: Categorization of expenses

Variable Sales Bonus and Delivery

Advertisement

Fixed Interest

Insurance

Bad Debts

Semi Variable Wages and others

Variable 15.57% 81716.5/525000

Variable portion 102145.625 656250*15.57%

Total Wages 183862.125

81716.5+102145.6

3

Part c

The variance analysis has shown that the actual performance of the business and its budgeted

performance did not match and there are some instances where positive (favorable) variations

are reported but in certain areas, negative variances (unfavorable) are reported. When the

actual cost of the business exceeds the budgeted cost, then negative variances are reported but

when the lesser cost is actually incurred than the budgeted cost then favorable variances are

reported. The situation is vice-versa in case of profits or incomes of business. The two major

areas where investigation is required are:

Bad debts: As there is no increase in the bad debts even with the increase in sales.

Interest: As the financing cost of the business did not increase with the widened

business operations and increased debt structure of business.

Requirement 4: CVP Analysis

Part a: Categorization of expenses

Variable Sales Bonus and Delivery

Advertisement

Fixed Interest

Insurance

Bad Debts

Semi Variable Wages and others

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Financial Statement Analysis 9

Part b:

Total Variable Expenses Expenses Total

Cost of goods sold 251125

Sales Bonus and

Delivery 24500

Advertisement 65625

Wages and others 102145.6 443395.6

Total Fixed Expenses

Interest 19268

Insurance 14000

Bad Debts 16800

Wages and others 81716.5 131784.5

Part c: Breakeven Point Determination

Sales 656250

Less: Variable Cost 443395.6

Contribution Margin 212854.4

Less: Fixed Cost 131784.5

Profit 81069.9

Contribution per unit Total Contribution/Number of units 26.61

Contribution Margin Contribution /Sales 32.43%

BEP( UNITS)

Total Fixed Cost/Contribution per

unit 4953

BEP ($)

Total Fixed Cost/Contribution

Margin 406303.97

Part d:

Number of Units to be

sold Total Fixed Cost + Desired Profit 331784.5

Contribution per unit 26.61

Units to be sold 12470

Part b:

Total Variable Expenses Expenses Total

Cost of goods sold 251125

Sales Bonus and

Delivery 24500

Advertisement 65625

Wages and others 102145.6 443395.6

Total Fixed Expenses

Interest 19268

Insurance 14000

Bad Debts 16800

Wages and others 81716.5 131784.5

Part c: Breakeven Point Determination

Sales 656250

Less: Variable Cost 443395.6

Contribution Margin 212854.4

Less: Fixed Cost 131784.5

Profit 81069.9

Contribution per unit Total Contribution/Number of units 26.61

Contribution Margin Contribution /Sales 32.43%

BEP( UNITS)

Total Fixed Cost/Contribution per

unit 4953

BEP ($)

Total Fixed Cost/Contribution

Margin 406303.97

Part d:

Number of Units to be

sold Total Fixed Cost + Desired Profit 331784.5

Contribution per unit 26.61

Units to be sold 12470

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Financial Statement Analysis 10

Financial Statement Analysis 11

References

Foster, G. (2004). Financial Statement Analysis, 2/e. Pearson Education India.

Higgins, R. C. (2012). Analysis for financial management. McGraw-Hill/Irwin.

Horngren, C. T., Bhimani, A., Datar, S. M., Foster, G., & Horngren, C. T.

(2002). Management and cost accounting. Harlow: Financial Times/Prentice

Hall.

Huang, Z., Chen, H., Hsu, C. J., Chen, W. H., & Wu, S. (2004). Credit rating analysis with

support vector machines and neural networks: a market comparative

study. Decision support systems, 37(4), 543-558.

Penman, S. H., & Penman, S. H. (2007). Financial statement analysis and security

valuation (p. 476). New York: McGraw-Hill.

Schmidgall, R. S., & DeFranco, A. L. (2004). Ratio analysis: Financial benchmarks for the

club industry. The Journal of Hospitality Financial Management, 12(1), 1-14.

Zimmerman, J. L., & Yahya-Zadeh, M. (2011). Accounting for decision making and

control. Issues in Accounting Education, 26(1), 258-259.

References

Foster, G. (2004). Financial Statement Analysis, 2/e. Pearson Education India.

Higgins, R. C. (2012). Analysis for financial management. McGraw-Hill/Irwin.

Horngren, C. T., Bhimani, A., Datar, S. M., Foster, G., & Horngren, C. T.

(2002). Management and cost accounting. Harlow: Financial Times/Prentice

Hall.

Huang, Z., Chen, H., Hsu, C. J., Chen, W. H., & Wu, S. (2004). Credit rating analysis with

support vector machines and neural networks: a market comparative

study. Decision support systems, 37(4), 543-558.

Penman, S. H., & Penman, S. H. (2007). Financial statement analysis and security

valuation (p. 476). New York: McGraw-Hill.

Schmidgall, R. S., & DeFranco, A. L. (2004). Ratio analysis: Financial benchmarks for the

club industry. The Journal of Hospitality Financial Management, 12(1), 1-14.

Zimmerman, J. L., & Yahya-Zadeh, M. (2011). Accounting for decision making and

control. Issues in Accounting Education, 26(1), 258-259.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.